JAPAN NRG WEEKLY

SEPT 4, 2023

JAPAN NRG WEEKLY

Sept 4, 2023

NEWS

TOP

- Govt to extend multi-trillion-yen subsidies to mitigate hikes in electricity, gas and fuel bills

- Activist investor Market Forces calls on major banks to reconsider making loans to JERA citing climate concerns

- Over 70% of solar facilities plan to continue operations even after their FIT contract expires

ENERGY TRANSITION & POLICY

- Sendai City to tighten solar installation rules from Oct 1

- Govt solicits feedback on new wind power promotion zones

- Osaka Gas, ENEOS mull large e-methane project in Osaka Bay

- Mitsubishi, Tokyo Gas, etc to partner with Sempra on e-methane

- Mitsui, IHI, etc to work on hydrogen and ammonia supply chains

- METI seeks to double target for 2030 EV charger installations

- Panasonic starts glass-mounted PSC test at Fujisawa City

- Scientists develop method for all-solid-state battery production

ELECTRICITY MARKETS

- Round 17 solar auctions: lowest bid under ¥9.00/ kWh, a first

- Top power distribution firms set up new entity to aggregate data

- Hokkaido Electric to increase capacity of connection with Honshu

- Environmental concerns over GPI’s new wind power station

- Toshiba, CO2OS and DEI plan to expand solar power business

- Japan Nuclear Fuel resumes uranium enrichment facility operation

- NRA to confirm TEPCO ability to operate Kashiwazaki-Kariwa NPP

- Terras Energy plans mid-sized wind power station in Fukui area

OIL, GAS & MINING

- Toyofuji Shipping to introduce LNG-powered car transport ships

- Australian LNG accounts for close to half of Japan’s July imports

- Saudi Arabian crude has 44.2% share in July

- LNG stockpiles held by utilities jump 10% in a week

ANALYSIS

BALANCING MARKET REFORM:

EPRX TO COMPLETE MAKEOVER IN 2024

One major change in the next 10 months will occur in the “balancing market”, which is used by power firms to buy additional volumes in case electricity demand surges above what’s expected, or the opposite. This ensures that power supply matches demand, preventing blackouts or wasted energy. METI recently provided more details about how exactly the new balancing market will look.

FINANCING JAPAN’S CCS ACTIVITIES

As Japan promotes CCS as a clean energy solution to the decarbonization of heavy industry, cost performance will need to improve. Also, companies need to create viable business models for a storage system that inherently stops generating income once it’s full. Announcing plans for future CCS projects is one thing, finding the financing and developing cost-efficient technologies is another.

GLOBAL VIEW

A wrap of top energy news from around the world.

EVENTS SCHEDULE

A selection of events to keep an eye on in 2023.

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group

Events

Editorial Team

Yuriy Humber (Editor-in-Chief)

John Varoli (Senior Editor, Americas)

Mayumi Watanabe (Japan)

Wilfried Goossens (Events, global)

Kyoko Fukuda (Japan)

Filippo Pedretti (Japan)

Regular Contributors

Chisaki Watanabe (Japan)

Takehiro Masutomo (Japan)

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

OFTEN USED ACRONYMS

|

METI |

The Ministry of Economy, |

mmbtu |

Million British Thermal Units | |

|

MoE |

Ministry of Environment |

mb/d |

Million barrels per day | |

|

ANRE |

Agency for Natural Resources and Energy |

mtoe |

Million Tons of Oil Equivalent | |

|

NEDO |

New Energy and Industrial Technology Development Organization |

kWh |

Kilowatt hours (electricity generation volume) | |

|

TEPCO |

Tokyo Electric Power Company |

FIT |

Feed-in Tariff | |

|

KEPCO |

Kansai Electric Power Company |

FIP |

Feed-in Premium | |

|

EPCO |

Electric Power Company |

SAF |

Sustainable Aviation Fuel | |

|

JCC |

Japan Crude Cocktail |

NPP |

Nuclear power plant | |

|

JKM |

Japan Korea Market, the Platt’s LNG benchmark |

JOGMEC |

Japan Organization for Metals and Energy Security | |

|

CCUS |

Carbon Capture, Utilization and Storage | |||

|

OCCTO |

Organization for Cross-regional Coordination of Transmission Operators | |||

|

NRA |

Nuclear Regulation Authority | |||

|

GX |

Green Transformation |

NEWS: ENERGY TRANSITION & POLICY

Govt to extend multi-trillion-yen subsidies to mitigate hikes in electricity and gas bills

(Denki Shimbun, Sept 1)

- The govt said it will continue to provide subsidies to mitigate higher electricity and gas bills. There is ¥3.1 trillion left for the measures from funding secured in the supplementary budget for FY2022.

- The subsidies were introduced in January this year to cover rising electricity and gas bills. Up until September, ¥2.5 trillion has been spent.

- In the last three months of this calendar year through December, the govt will likely spend about ¥500 billion on subsidies, according to its estimates.

- CONTEXT: From January, for low-voltage electricity contracts such as those used by households, the subsidy was ¥7/ kWh; for high-voltage contracts (for businesses) the subsidy was ¥3.5/ kWh. For September, the subsidy level will drop to ¥3.5/ kWh for low-voltage contracts and ¥1.8 k/Wh for high-voltage contracts.

- September levels of power and gas subsidies will continue in October and after.

- SIDE DEVELOPMENT:

Kishida to ramp up gasoline subsidies from Sept 7

(Government statement, Aug 30)- PM Kishida decided to ramp up gasoline subsidies so that in October, retail prices will ease to ¥175/ liter, from the present ¥185/ liter.

- Without subsidies gasoline prices would be ¥195/ liter.

- The subsidy was to end in September but Kishida decided to continue it until Dec 31.

Investor activist Market Forces calls on major banks to reconsider loans to JERA

(Bloomberg, Aug 30)

- Market Forces, an investor activist group, called on eight major banks, including Deutsche Bank and Standard Chartered, to reconsider loans to JERA. The group is concerned that the loans could help expand JERA’s fossil fuel business.

- The group wants the banks to engage with JERA and push for a clear plan to achieve net-zero emissions by 2050. Climate activists are increasingly pressuring financial institutions to influence major polluters to accelerate decarbonization efforts.

- JERA said it aims for carbon neutrality by 2050 and seeks new tech to reduce emissions. The company said it didn’t receive a letter from Market Forces.

TAKEAWAY: Activist investors in the climate space have had limited success in Japan so far with all the climate resolutions proposed at this year’s company shareholders meetings rejected. However, targeting non-Japanese banks may lead to some degree of cooling in financing for JERA, which has said in the past that it wants to aim for a listing on a stock exchange.

Sendai City to tighten solar installation rules from Oct 1

(Government statement, Sept 1)

- Sendai City (Miyagi Pref) will introduce a set of regulations for solar operators; this will be more rigorous than those of the prefecture.

- Miyagi Pref restricts solar panel installations in certain areas to improve resilience to landslides. Sendai will tighten solar installation rules to further increase landslide resilience and to protect livelihoods and natural landscapes.

- All plans for solar units of over 20 kW will require filing to the city; for the rest of Miyagi Pref, the threshold is 50 kW. Rooftop panels will be exempted.

- Also, the city defined eight types of zones where solar installations will require the mayor’s own approval. Sendai will set restricted zones for natural and landscape protection.

- The new rules take effect on Oct 1, and will expand to other renewable energy sources in the future.

- CONTEXT: It’s becoming more challenging for renewables to operate in Miyagi Pref. The prefecture authority plans to introduce the country’s first renewable tax on operators tearing down forest areas starting FY2024.

TAKEAWAY: Join a Japan NRG webinar on Sept 14, at 5pm Tokyo time, for an in-depth report and discussion of these developments in Miyagi. A sign-up link is available here.

Wakaya governor asks METI to amend or cancel Tokyu Fudosan wind project

(Government statement, Aug 25)

- The Wakayama governor said that a planned 94.6 MW wind turbine site (to be operated by Tokyu Fudosan) raises safety and ecological concerns and called for either amending or entirely cancelling the project if it’s not improved.

- There are multiple wind stations operating in the area. The governor said that an assessment on “aggregate environmental impacts” is needed, pointing out that Tokyu Fudosan expanded the project size from the initial impact assessment phase.

- CONTEXT: Over 100 opinions and questions from the public were filed to Tokyu Fudosan; many concerned protection of mountain hawk-eagles. METI’s wind project panel met on Aug 25 to discuss the project, but the conclusion was not announced.

TAKEAWAY: Strong concern from local authorities can lead to the cancellation of a project, as happened to Sojitz Corp. in June of this year. The trading company walked away from plans to develop a 109 MW wind farm in Hokkaido after locals objected to the impact it may have on the local flora and fauna. Should the project in Wakayama also fall through, that will delete over 200 MW of capacity from Japan’s wind pipeline in a matter of a few months. The bigger risk is that project developers will simply decide that pursuing lengthy wind power developments onshore is not worth the trouble, hampering national renewables targets.

- SIDE DEVELOPMENT:

Govt solicits public feedback on new wind power promotion zones

(Government statement, Sept 1)- METI and MLIT are soliciting public feedback on designating the coast along Yuza Town in Yamagata Pref and the Sea of Japan Coast of Aomori Pref as Offshore Wind Project Promotion Zones. The feedback period closes Sept 15.

- In 2020-2021, the two areas gained the “promising zone” status, a phase preceding the final “promotion” status. Local community stakeholders concluded that the fishery and shipping industries won’t be impacted by the wind turbines.

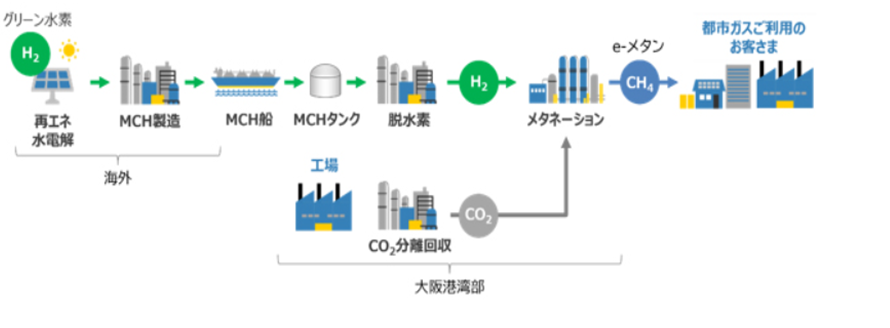

Osaka Gas, ENEOS to study project to produce 60 million m3/ year e-methane

(Company statement, Aug 29)

- Osaka Gas and ENEOS began to study a plan to set up 60 million cubic meters/ year of synthetic methane (e-methane) production in Osaka Bay using “carbon neutral” hydrogen.

- E-methane is made by combining hydrogen and carbon in a process called methanation, which Osaka Gas is developing. Green hydrogen will be imported by converting the gas into Methylcyclohexane (MCH), a technology developed by ENEOS. Carbon will be captured locally.

- The goal is to start e-methane production in Osaka Bay by 2030, which would make it the country’s first such facility.

- CONTEXT: Osaka Gas and ENEOS are building a large-scale international supply chain despite calls to limit hydrogen to local consumption because its transportation requires much energy. On the other hand, renewable suppliers overseas are keen to export hydrogen to Japan.

TAKEAWAY: Osaka Gas and ENEOS plan to convert hydrogen into MCH by reacting it with toluene and separating it back into hydrogen in a process called dehydrogenation. Legacy tankers and refinery dehydrogenation units can be used, but there are emissions released during dehydrogenation. Alternative transport options include converting hydrogen into ammonia or liquid hydrogen. Further options for hydrogen storage under research are the use of formic acid and magnetic refrigeration.

E-methane supply chain

- SIDE DEVELOPMENT:

Mitsubishi, Tokyo Gas, Osaka Gas partner with Sempra on e-methane in the U.S.

(Company statement, Aug 30)- A consortium of Tokyo Gas, Osaka Gas, Toho Gas, and trading house Mitsubishi Corp will partner with Sempra Infrastructure to produce e-methane near the U.S. Gulf Coast.

- The project aims to establish the world’s first large-scale production supply chain of e-methane. Up to 130,000 tons of e-methane will be made each year and then liquefied at the Cameron LNG terminal in Louisiana for export to Japan.

- The project will involve the production or procurement of clean hydrogen and the construction of facilities for e-methane manufacture.

- CONTEXT: These companies have been working on the project since 2022 and are now involving Sempra so as to build a global market for liquefied e-methane.

TAKEAWAY: This initiative aligns with the MoC signed by the U.S. Department of Energy and METI that focuses on carbon capture, utilization, storage, conversion, recycling, and CO2 removal. However, it remains to be seen if e-methane will be recognized as a carbon-neutral fuel.

Mitsui, IHI and KEPCO to work on hydrogen and ammonia supply chains in Osaka

(Company statement, Aug 30)

- Mitsui, Mitsui Chemicals, IHI, and KEPCO plan to explore creating hydrogen and ammonia supply chains in the Osaka coastal industrial zone.

- The companies will study the development of infrastructure for ammonia storage and supply, focusing on the Osaka region, and are in discussions with Kobe Steel, which could benefit from the availability of ammonia supply.

- CONTEXT: Mitsui holds Japan’s largest share of ammonia imports.

METI seeks to double 2030 target for installed EV chargers nationwide

(Nikkei, Aug 28)

- METI issued a proposal to increase the installation target for EV chargers, including charging stations, to 300,000 units by 2030.

- This target is twice the current goal of 150,000 units, and it represents a tenfold increase compared to the present number of installations. The guideline encourages installations in places like commercial facilities.

- CONTEXT: Charging infrastructure currently stands at around 30,000 units. The trend of having multiple charging outlets per charger is growing. The proposal sees 270,000 units as regular chargers in commercial facilities and 30,000 units as fast chargers at locations such as highways.

Panasonic starts glass-mounted PSC test at Fujisawa City

(Company statement, Aug 31)

- Panasonic developed a prototype perovskite solar cell (PSC) module mounted on glass and installed it on a balcony in a demo house in Fujisawa City’s sustainable smart town. The transparent PSC module is 387.6 cm by 95 cm.

- Panasonic claims that this is a world-first. The prototype will be in the demo house until November 29, 2024, during which time data will be gathered on its power efficiency and endurance.

- Panasonic has a module with an area of 800 cm2 and 17.9% efficiency, a world record. Other modules that post efficiency numbers in excess of 20% are much smaller.

- CONTEXT: Panasonic is now the third Japanese company after Toshiba Energy Systems and Sekisui Chemical to test PSC outside of the lab. The other two companies are testing PSC on thin-films installed on building walls, which are more difficult to maintain since films absorb moisture and dust particles easily. The drawbacks of glass-mounted PSC are a lack of flexibility and their heavy weight, which is comparable to that of current silicon PVs. As such, some researchers do not consider them to be “authentic PSC”.

TAKEAWAY: This issue will come down to whether the cost of generating electricity from PSC tech is lower than the ¥10-¥25/ kWh power utilities charge today. PSCs are expensive to make because gold or silver are used as electrodes, and other materials made via nano-level process controls are costly. There have also been questions about durability. Developers have reacted to some of these challenges by, for example, putting a protective layer on top of PSC layers to lengthen the product-life of film-based PSC. However, this has in turn further inflated costs and complicated the module production process, one university researcher told Japan NRG. So, Panasonic may be being more realistic by putting its focus on glass-mounted PSCs.

Thin-film PSC challenges and possible solutions

|

Challenges |

Possible solutions |

Drawbacks of the solutions |

|

Endurance |

A protective layer to block moisture |

Cost rises |

|

Aqueous lead solution as a raw material |

Power efficiency falls | |

|

Costs |

Substitute gold/silver electrodes with by graphite |

Application on film-based PSC is difficult |

|

Recycling of lead compounds used in PSC |

Substitute with copper or tin |

Power efficiency falls |

Power-generating glass

Source: Panasonic

Source: Panasonic

- SIDE DEVELOPMENT:

Sekisui Chemical promotes PSC modules at ASEAN clean energy event

(Company statement, Aug 31)- Sekisui Chemical delivered a presentation of its perovskite solar cell (PSC) module at the Clean Energy Future Initiative for the ASEAN (CEFIA) meeting in Indonesia.

- CONTEXT: Last year, China’s DaZheng Macro-Nano Technology began the world’s first mass production of PSCs. The ASEAN audience was most likely comparing Sekisui product with that of DaZheng.

Scientists develop new method for all-solid-state battery production

(Nikkei Asia, Aug 30)

- Scientists from the Tokyo Institute of Technology developed an innovative method for producing all-solid-state batteries, potentially making their mass production more cost-effective compared to traditional lithium-ion batteries.

- This innovative method allows battery materials to be exposed to air during the manufacturing process, reducing the need for expensive equipment.

- The battery has high ionic conductivity and can withstand 300 charging cycles.

- However, its temperature resistance and suitability for higher voltages are still not clear. Researchers hope to commercialize the technology within the next decade.

- CONTEXT: These batteries are seen as a safer alternative due to their lack of flammable solvents and higher energy density. Several automakers plan to integrate all-solid-state batteries into vehicles by 2030.

Mitsui acquires stake in RNG company in the U.S.

(Company statement, Aug 31)

- Mitsui acquired a 33.3% stake in Terreva Renewables, a U.S. company that processes methane from landfills to produce and sell renewable natural gas (RNG).

- Mitsui intends to help Terreva grow its customer base; it sees opportunities for RNG value chains to expand globally, including supplying RNG-based low-carbon products like methanol and LNG.

- CONTEXT: RNG is gaining interest as a green alternative to fossil fuels, with increasing demand in the U.S. for low-carbon transportation fuels like clean hydrogen and compressed natural gas (CNG).

MOL to join feasibility study for CCS projects in western Japan

(Company statement, Aug 29)

- Mitsui O.S.K. Lines (MOL) has been tapped to research the maritime transportation of liquefied CO2 for a feasibility study of CCS projects in western Japan.

- Apart from navigational plans for ships carrying liquefied CO2, MOL will also estimate transportation costs and identify challenges related to sea transport of CO2.

- ENEOS Holdings, J-POWER and JX Nippon Oil & Gas are also involved.

- The plan calls for capturing CO2 emitted from J-POWER’s thermal power plants and ENEOS’ refineries in western Japan, then annually burying about 3 million tons of CO2 under the seabed off of Kyushu. The goal is to be operational by FY2030.

NEWS: POWER MARKETS

Over 70% of graduated FIT solar power systems intend to continue generation

(Denki Shimbun, Aug 30)

- Research by the Renewable Energy Advancement Association for Long-Term Stable Power Generation (REASPA), which surveyed 100 renewable energy companies, revealed that over 70% of solar power generation operators plan to continue running their facilities even after the 20-year purchase period under the Feed-in Tariff (FIT) expires. This is known as “graduating” from FIT.

- The peak period for the disposal of solar panels, which were widely introduced in the mid-2010s, is anticipated to occur in the late 2030s, after the graduated FIT period. However, considering the survey results, it’s now believed that a second peak may occur in the 2040s as operators extend project lifetime.

- CONTEXT: Since the launch of the FIT program in 2012, solar power has rapidly expanded. Installed commercial solar capacity exceeded 8 GW annually in both FY2014 and FY2015. The govt had previously anticipated that the peak for disposal of panels introduced during this period would occur around 2035-2037.

Round 17 solar auctions: lowest bid under ¥9.00/ kWh for the first time

(Japan NRG, Aug 25)

- OCCTO held Round 17 of solar auctions. The number of bids (offered capacity) was 110.89 MW; the auction price cap was ¥9.43/ kWh. There was a total of 55 bids, all successful. Of the total capacity, 69.07 MW was awarded.

- The lowest bid was ¥8.95/ kWh, under the ¥9 level for the first time. The highest was ¥9.43. The weighted average bid was ¥9.30. The biggest was 15 MW.

- The next bidding period will be from Nov 6 to Nov 11. It will offer 105 MW of capacity at a maximum price of ¥9.35/ kWh.

- CONTEXT: In June, OCCTO held Round 16 of solar auctions. For the first time, the auction was a unified system. Previously, bids were split between FIT and FIP.

TAKEAWAY: Compared to the previous auction, where there were 20 awarded projects for the full offered capacity of 105 MW, this auction saw a significant decrease in capacity but a doubling of the number of projects. This difference can be attributed to the fact that one single bid by Pacifico Energy was for 89.6 MW, which accounted for 85% of the total solicited capacity.

Country’s top power distribution firms set up new company to aggregate data

(Nikkan Kogyo, Sept 1)

- Japan’s 10 largest power distribution companies, including TEPCO Power Grid, Chubu Electric Power Grid, and Kansai Transmission and Distribution, established a new entity to act as a hub for aggregating electricity data for local governments and businesses. It will help to unify the specifications of the central power dispatching system, and develop a cost-effective national system for electricity transfer.

- The new entity will collect data from smart-meters for disaster response and provide it to local governments. It will provide data for various services like elderly care and environmental initiatives.

- The data will be input starting from September in the TEPCO Power Grid area and then extent to other parts of the country. Additionally, a new central power dispatching system is in development to balance electricity consumption and generation, targeting operation in the late 2020s.

- The new company’s name is “Electricity Transmission and Distribution Systems”. While the exact amount of investment from each party has not been disclosed, nine of the grid firms will each account for 11% of the equity, and Okinawa Electric Power (which will not participate in the integration of the next-generation central supply system) will have 1%.

Hokkaido Electric PN to increase capacity of main connection with Honshu

(Nikkei, Aug 31)

- Hokkaido Electric Power Network will begin construction to increase the capacity of the “Shin-Hokkaido Main Connection Line” that connects Hokkaido and Honshu.

- When operational in March 2028, the transmission capacity between Hokkaido and Honshu will expand from 900 MW to 1.2 GW.

- Total construction cost, including the work by the Tohoku Electric Power Network in Aomori Pref, will be about ¥48 billion.

Japan Nuclear Fuel resumes uranium enrichment operation after 6-year hiatus

(Denki Shimbun, Aug 28)

- Japan Nuclear Fuel Ltd announced the resumption of operations at its uranium enrichment facility in Rokkasho, Aomori Pref. This is the first since Sept 2017.

- Given the strong position of Russian companies in the international market for enriched uranium, many nations are taking steps to reduce dependence on Russia.

- CONTEXT: JNF’s uranium enrichment facility began operations in March 1992 with an annual production capacity of 150 metric tons of separative work units (SWU). It eventually expanded its annual capacity to 1,050 metric tons of SWU. By FY2027, the plan is to reach an annual production capacity of 450 metric tons of SWU. The facility aims to expand capacity to 1,500 metric tons of SWU per year.

Environmental concerns over GPI’s new wind power station in Shimane Pref

(New Energy Business, Sep 1)

- Green Power Investment (GPI) plans a 56 MW onshore Shin Hamada Wind Farm over 344 hectares near Hamada city and Masuda city in Shimane Pref; it will have fourteen 4.2 MW wind turbines.

- The MoE asked GPI to reconsider its environmental protection measures because rare species such as mountain hawk-eagles and Iwami salamanders live in the area.

- CONTEXT: In Feb 2023, the Nature Conservation Society of Japan (NACS-J) said that four of the 14 wind turbines should be removed or relocated to protect a nearby forest preserve. It also said that the Iwami salamander is an endangered species.

Terras Energy plans a 38.7 MW wind power station in Fukui Pref

(Company statement, Aug 25)

- Terras Energy, a subsidiary of Toyota Tsusho, published an environmental assessment report for its planned wind power station in Kunimi, Fukui Pref. The company plans to build 9 units of 4.3 MW wind turbines.

- Fukui Pref will develop 1.3 GW of renewable energy, of which 280 MW will be wind power by 2030. This project contributes 14% towards that goal.

- Construction is planned to start in April 2025; commercial operation in Nov 2027.

Toshiba ESS, CO2OS and DEI to expand solar power business

(Company statement, Aug 24)

- Toshiba Energy Systems (Toshiba ESS), CO2OS, and Daiwa Energy & Infrastructure (DEI) signed an agreement to develop solar power stations, including via EPC (engineering, procurement, and construction), and operation & maintenance (O&M), as a one-stop-shop.

- Toshiba ESS will be responsible for technical and engineering matters, such as VPPs (virtual power plants). CO2OS has over 5.5 GW of experience in O&M of solar power stations and helps customers find project locations and obtain state approvals. As an investment firm, DEI will provide financial instruments for customers.

- CONTEXT: In May 2022, the three companies announced a project in which Toshiba ESS was the consumer and a high-voltage solar power station in Satsuma, Kagoshima Pref ― developed and operated by COS2OS and financed by DEI – was the provider. It began selling electricity in April 2023 using the FIP.

- SIDE DEVELOPMENT:

Toyo Tire launched 14 MW solar power systems at its factory in Malaysia

(Company statement, Aug 28)- Toyo Tire installed 14 MW solar power systems at its factory, Toyo Tyre Malaysia (TTM) in partnership with Solarvest, a Malaysian clean energy supplier.

- The solar power system will be fully operational in December.

NRA to confirm TEPCO ability to operate Kashiwazaki-Kariwa NPP, but restart delayed

(Nikkei, Aug 31)

- The NRA convened to reconfirm TEPCO’s suitability as a nuclear plant operator for the Kashiwazaki-Kariwa NPP restart. TEPCO hopes to restart Unit 7 in October but it faces obstacles, including local consent.

- TEPCO wanted to restart the plant in October, but that’s impossible given that the NRA decided to conduct inspections from mid-September.

- Issues with terrorism countermeasures and nuclear protection at the plant are ongoing. The restart process involves rigorous inspections by NRA and local consent.

- CONTEXT: The combined electricity generation capacity of the NPP’s Units 6 and 7 is 2.7 GW, equal to about 4-5% of Tokyo’s demand. In July and Aug, the govt called for energy conservation within TEPCO’s service area. Restarting the plant could improve the situation and lower electricity costs.

TAKEAWAY: This is part of a very long process that may or may not lead to TEPCO operating a nuclear power generation facility again. Since all previous deadlines for the restart of Kashiwazaki-Kariwa NPP have been blown apart, it’s anyone’s guess if this power plant will eventually be allowed to come back online and if TEPCO will be the nameplate operator at the time. What possibly doesn’t help TEPCO’s cause is the fact that the Tokyo area energy system has so far coped mostly well without the NPP’s contributions. Should that situation changes, the govt may be more invested in seeing a faster resolution to the saga around the Kashiwazaki-Kariwa restart.

KEPCO’s Takahama NPP Unit 1 resumes full operation; Unit 2 ready to start

(Company statement, media reports, Sept 3)

- KEPCO’s Takahama NPP Unit 1 (PWR, 826 MW) completed its final comprehensive load performance inspection and resumed full operation.

- Takahama Unit 2 (826 MW) has also passed its preliminary inspections and is on course to restart on Sept 15. If that occurs, all seven nuclear power plants operated by KEPCO will have restarted after the introduction of new regulatory standards and installation of new specialized safety facilities.

- CONTEXT: KEPCO, however, has taken Ohi NPP Unit 4 offline on Aug 31 for regular checks and maintenance, so it won’t have all seven units operating at the same time.

Baseload market: agreements in all areas for two-year products

(Various media, Sept 1)

- The Japan Electric Power Exchange (JEPX) announced results of an agreement for the Base Load (BL) market. It will see the first introduction of long-term products with a delivery period of two years and change market area categories into three: Tokyo, Kansai, and Kyushu.

- Two-year contracts (delivery from 2024 to 2025) were concluded for all three areas.

- Kansai’s contracted volume was 96.4 MW, at a price of ¥14.21/ kWh; Tokyo was 99.1 MW, at ¥19.22/ kWh; Kyushu was 1.1 MW, at ¥14.35.

- CONTEXT: METI and ANRE decided to change the rules of the BL market to allow for a better fuel adjustment mechanism via longer contracts.

Non-fossil, non-FIT certificates trade at minimum price

(Denki Shimbun, Sept 1)

- The results of the first trading session for non-FIT, non-fossil certificates for FY2023 were announced on Aug 31.

- CONTEXT: The Non-Fossil Value Trading Market was set up to auction certificates provided by clean power sources that operate outside for the FIT scheme. The certificates represent the “environmental value” of the generated electricity. In other words, the volume of CO2 that was avoided because electricity was generated by non-CO2-emitting sources. This market covers electricity generated both with FIT and without FIT.

- Contracted prices for non-FIT non-fossil certificates remained at a minimum level of ¥0.6/ kWh for both generation marked as renewable and for other clean energy sources that are not classified as renewable.

- The non-renewable category of certificates, primarily related to nuclear power but also large-scale hydro, recorded an all-time high in terms of contracted volume, exceeding 11 TWh.

- CONTEXT: Non-FIT certificates are used by retail electricity companies to fulfill obligations under the Advanced Energy Supply Structure Enhancement Act.

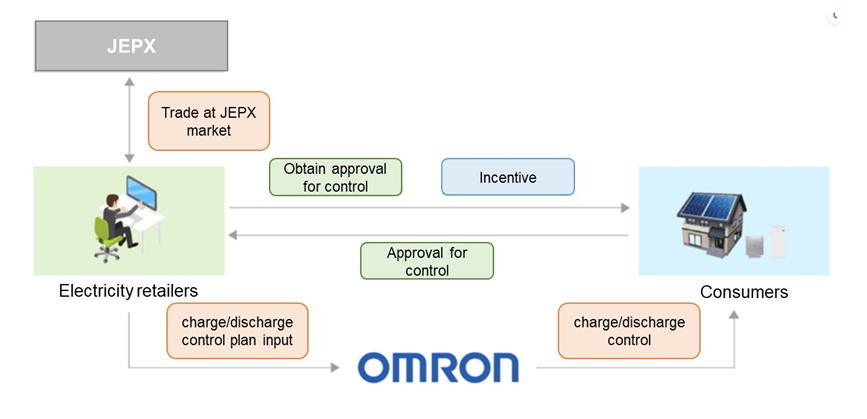

Omron starts Power Juggling service to reduce electricity cost

(Company statement, Aug 23)

- Omron Social Solutions (OSS) began a new service, Power Juggling, to reduce procurement costs and help electricity retailers balance the cost of electricity with storage batteries, and to cope with the fluctuation of fuel prices.

- Power Juggling controls OSS’s storage battery systems for residential use. The system stores electricity when the spot (JEPX) electricity price is low, and releases electricity when it is high. OSS plans to provide 10,000 systems in 3 years.

- SIDE DEVELOPMENT:

Omron and Toho Gas test the Power Juggling service

(Company statement, Aug 24)- Omron Social Solutions (OSS) and Toho Gas began testing Power Juggling. When electricity supply is tight, Toho Gas asks customers to release electricity from their storage batteries. Toho Gas will buy the reverse power flow from this action.

- The test takes place from Sept 2023 to Sept 2024 for 50 customers who have solar PV and OSS’s storage batteries at home and contracts with Toho Gas.

- The companies will verify the reliability of the service and try to commercialize this virtual power plant (VPP) system as quickly as possible.

NEWS: OIL, GAS & MINING

Toyofuji Shipping to introduce its first LNG-powered car transport ships by 2025

(Nikkei, Aug 31)

- Toyota subsidiary Toyofuji Shipping plans LNG-powered car transport ships by 2025; an order of two ships from Mitsubishi Shipbuilding will cost several billion yen each.

- These ships will reduce CO2 emissions by about 25% compared to current heavy oil-fueled vessels. To address the long lifespan of ships (20-30 years), the company’s interim approach involves transitioning foreign trade vessels to LNG ships while increasing the use of biofuels for coastal vessels.

- CONTEXT: Toyofuji Shipping manages Toyota’s port facilities and plays a central role in transporting vehicles. The company operates six coastal vessels and over 20 international trade vessels, with an annual volume of about 1.5 million vehicles on coastal routes and around 800,000 vehicles on international routes.

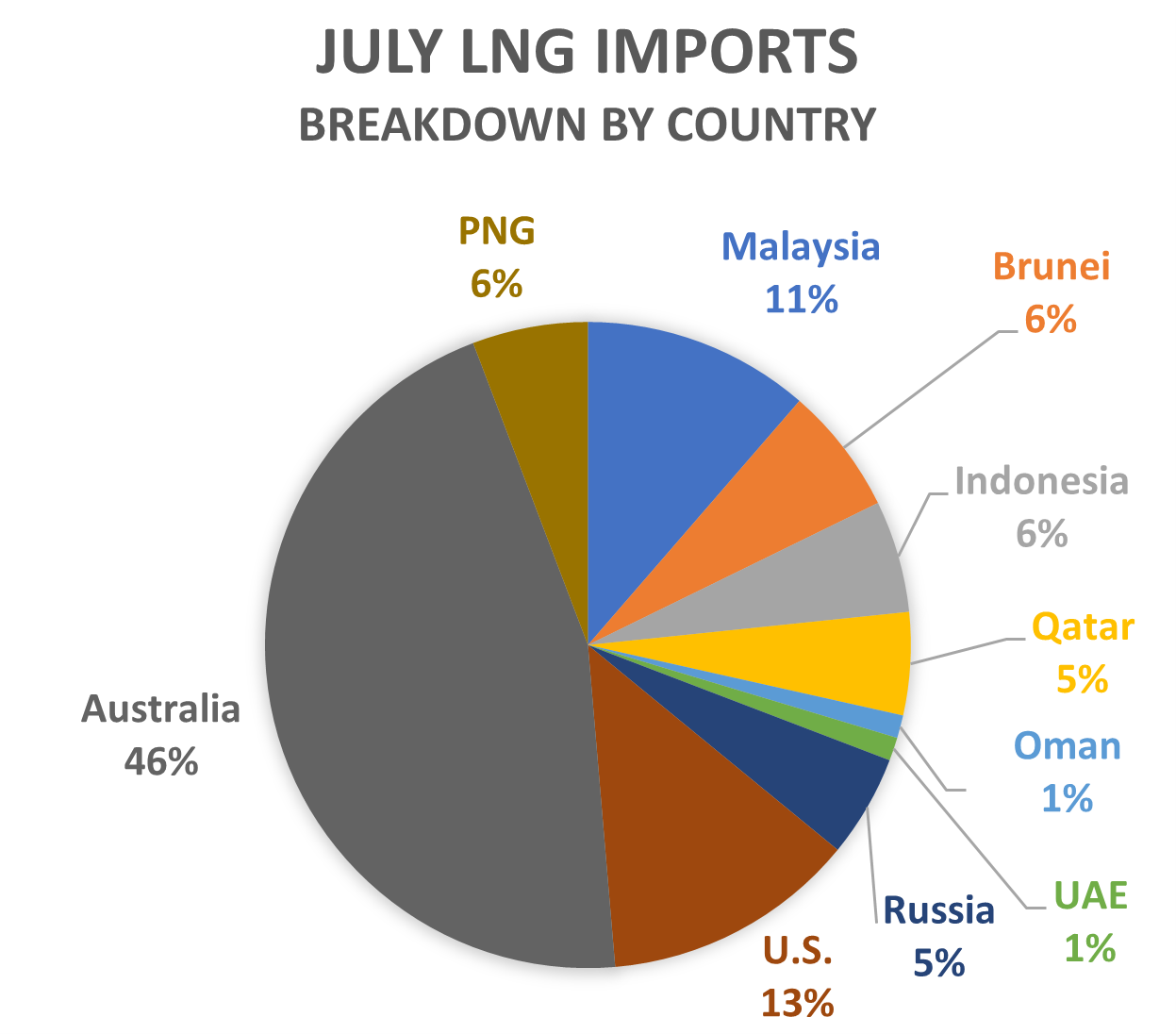

Australian LNG accounted for 45.6% of total in July

(Government data, Aug 30)

- LNG imports from Australia were 2.3 million tons in July, or 45.6% of Japan’s total. Imports included those from Chevron whose workers plan to strike this week.

- Imports from Russia halved, as Sakhalin-2 closed in July for maintenance, dropping to 0.26 million tons from the usual monthly volume of 0.4 to 0.5 million tons.

- Japan’s total LNG imports were 5.09 million tons in July, down 17.4% YoY.

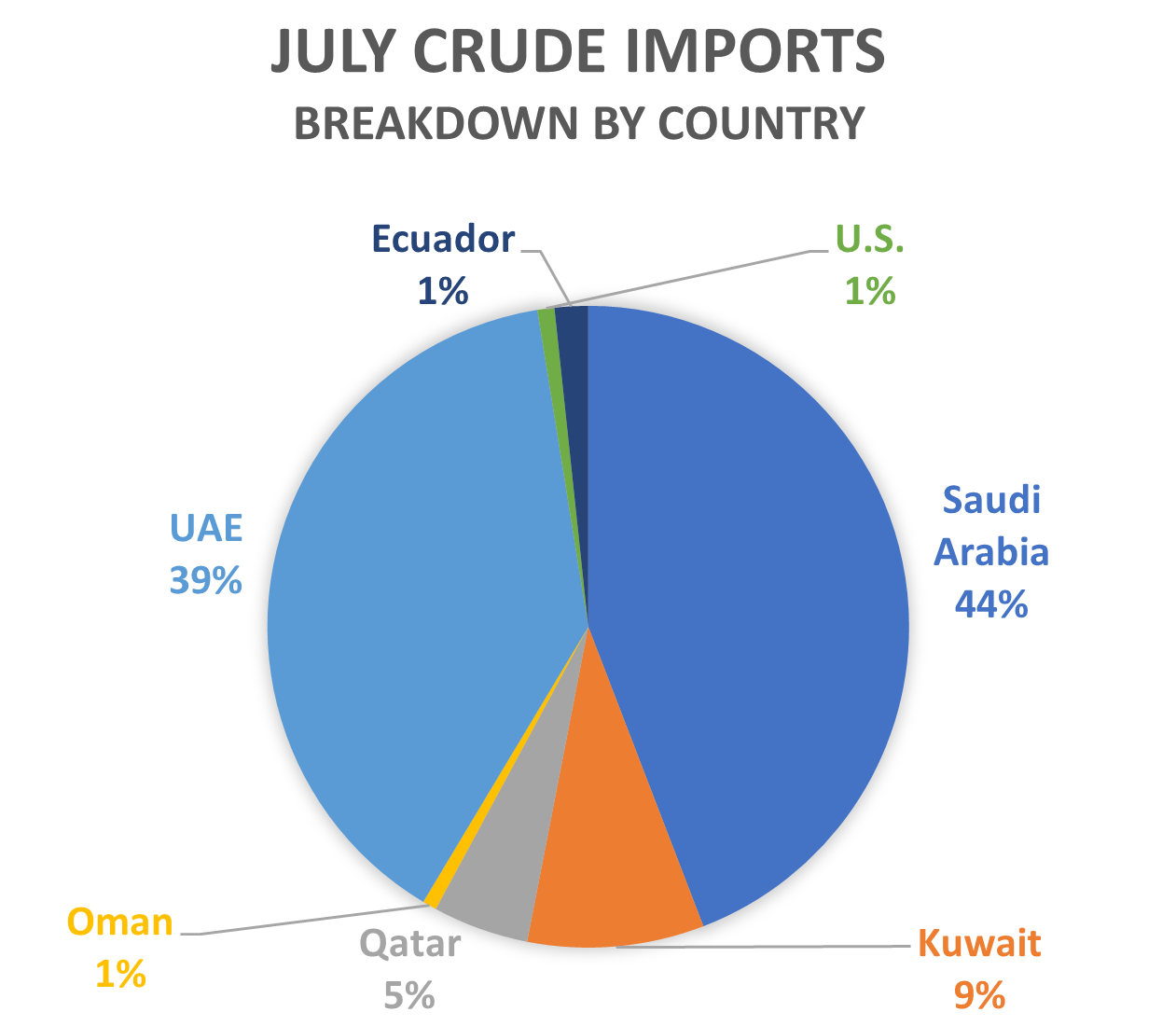

Saudi Arabian crude has 44.2% share in July

(Government data, Aug 30)

- Japan imported 4.6 million kiloliters (32 million barrels) of crude oil from Saudi Arabia in July, or 44.2% of Japan’s total. Saudi imports were the highest since March.

- Next was the UAE, with 4.3 million kl, or 38.9% of the total.

- Total crude oil imports were 11.15 million kiloliters, down 2.9% YoY.

LNG stocks rise to 2.01 million tons

(Government data, Aug 30)

- LNG stocks of 10 power utilities stood at 2.01 million tons as of Aug 27, up 10% from 1.82 million tons a week earlier. The Aug 20 stocks were first reported at 1.81 million tons but METI corrected the figure.

- The end-August stocks last year were 2.75 million tons. The five-year average for this time of year was 2 million tons.

ANALYSIS

BY JAPAN NRG TEAM

Electricity Balancing Power Market Reform:

EPRX to Complete Makeover in 2024

As more renewables are brought online, the nation’s power trading is adjusting to reflect the new market dynamics. And one of the biggest changes in the next 10 months or so will occur in the supply-demand adjustment trading segment, also known as the “balancing market”.

Japan’s full liberalization of the power market in 2016 allowed a variety of new players to trade and sell electricity. This drew interest to the electricity wholesale market, or spot trading, and several years later two exchanges launched for futures contracts, as well as a new platform for power capacity auctions.

Amid all the changes, the “balancing system” is one electricity marketplace that has received little attention. This system is used by power firms to buy additional volumes in case electricity demand surges above what’s expected, or the opposite. This ensures that power supply always matches demand, keeping the grid stable and preventing blackouts or wasted energy.

As the role of variable energy sources like solar and wind generation has increased, so has the demand for flexibility and speed of response to balance the market. This is what drives the changes to Japan’s power supply-demand adjustment market that should be fully in place by fiscal year 2024.

METI recently provided more details about how the new balancing market will look.

Background

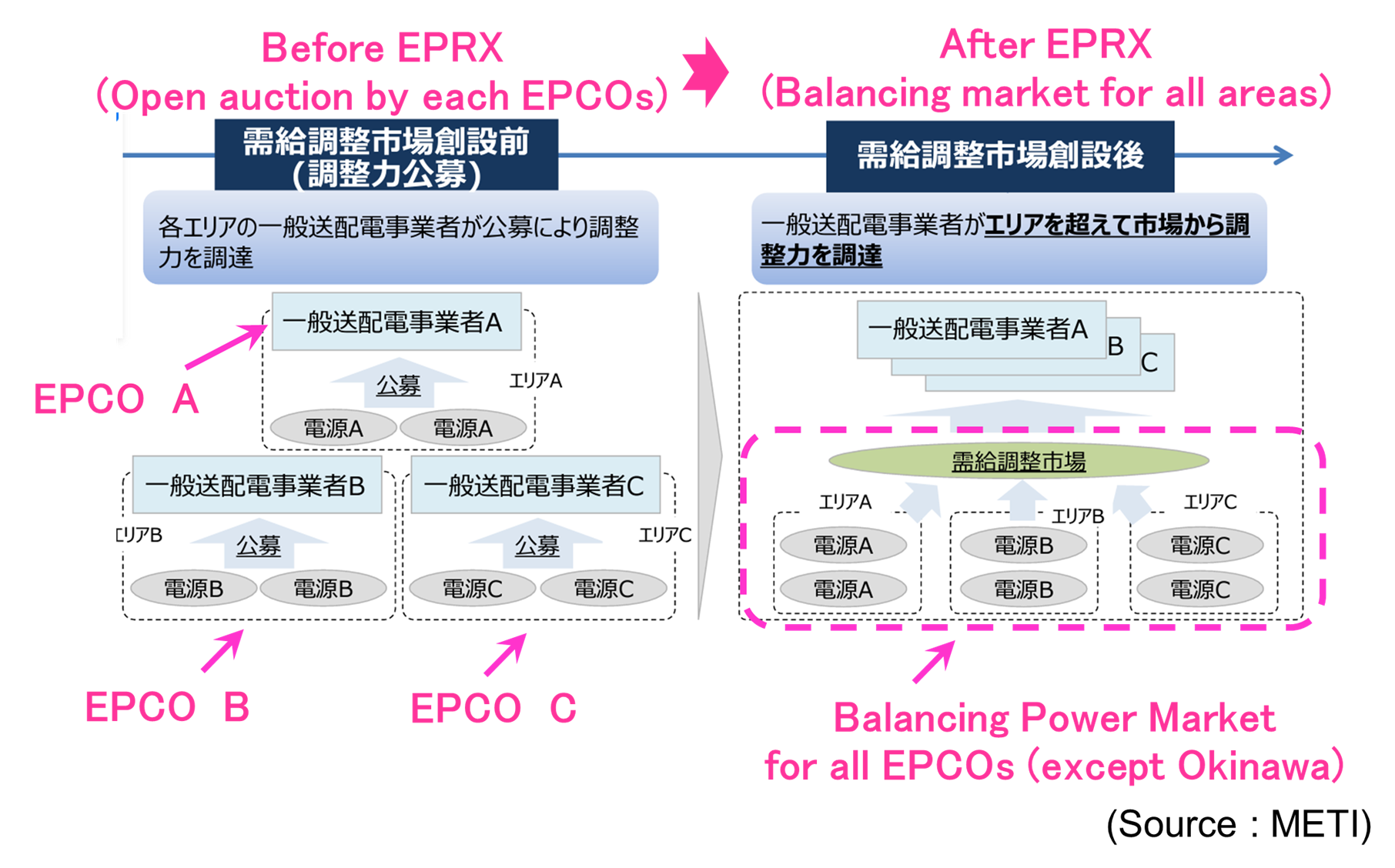

Before the electricity market liberalization, regional power utilities, or EPCOs (Electric power companies), maintained the balance of electricity demand and supply using their own power generation capacity, filling the gaps with energy sources such as pumped storage hydro. In worse cases, they requested large electricity consumers, such as factories, to curtail usage. This system was straightforward and efficient, helping Japan boast one of the world’s lowest blackout rates.

Once the power industry expanded to accommodate an influx of hundreds of new electricity retailers, balancing the market became more complex and more important. With the EPCOs told to unbundle their generation from transmission assets, it fell on the newly independent transmission and distribution (T&D) companies to secure balancing power volumes through open auctions.

The smaller volumes in the balancing market made it less attractive for new market entrants, however. Thus, relatively few companies participated in supply-demand adjustment trades. In all regions, the most active and even dominant traders of balance capacity are the long-established EPCO groups.

With prompting from METI, the biggest power industry players decided to shift away from an auction to a market system. This was to allow for the creation of a comprehensive system that covered the entire country (apart from Okinawa), making the process of balancing more efficient and more able to respond to short-term adjustment needs stemming from a greater reliance on solar and wind power.

In 2021, the nine T&D companies related to regional EPCOs, such as TEPCO Power Grid, Kansai Transmission and Distribution, and Kyushu Electric Power Transmission and Distribution, formed a new market system operator – the Electric Power Reserve Exchange (EPRX).

Since then, the EPRX has continuously worked to optimize the procurement of balancing power, leveraging the “merit order” to ensure power system stability at minimal costs. This transition dovetails with the planned integration of all EPCO power control centers in the late 2020s.

According to a recent METI briefing with market participants, changes at the EPRX should be completed in 2024.

“Merit order” refers to the sequence in which different power sources are dispatched based on their short-run marginal costs of production. It’s a system used by grid operators to prioritize the dispatch of power plants to ensure that the least expensive electricity is used first. The merit order is particularly relevant in the context of power markets and electricity supply-demand adjustments.

Renewable sources like wind and solar often appear first in the merit order “stack” because, once installed, their marginal costs are minor. Next might come nuclear and hydropower, followed by natural gas. So-called “peaking” power plants, which are usually gas-fired, are expensive to run but can be started quickly. Traditional thermal power plants that run on coal or oil take longer to start and have higher fuel costs.

The merit order effect becomes especially noticeable with a high penetration of renewable energy in the grid. On sunny and windy days, the influx of cheap renewable energy can push out more expensive sources, leading to lower wholesale electricity prices. However, this dynamic can also present challenges in terms of grid reliability and the financial viability of non-renewable plants, which may still be needed for periods when renewables volumes are low.

Balancing market system pre- and post-2021

New order

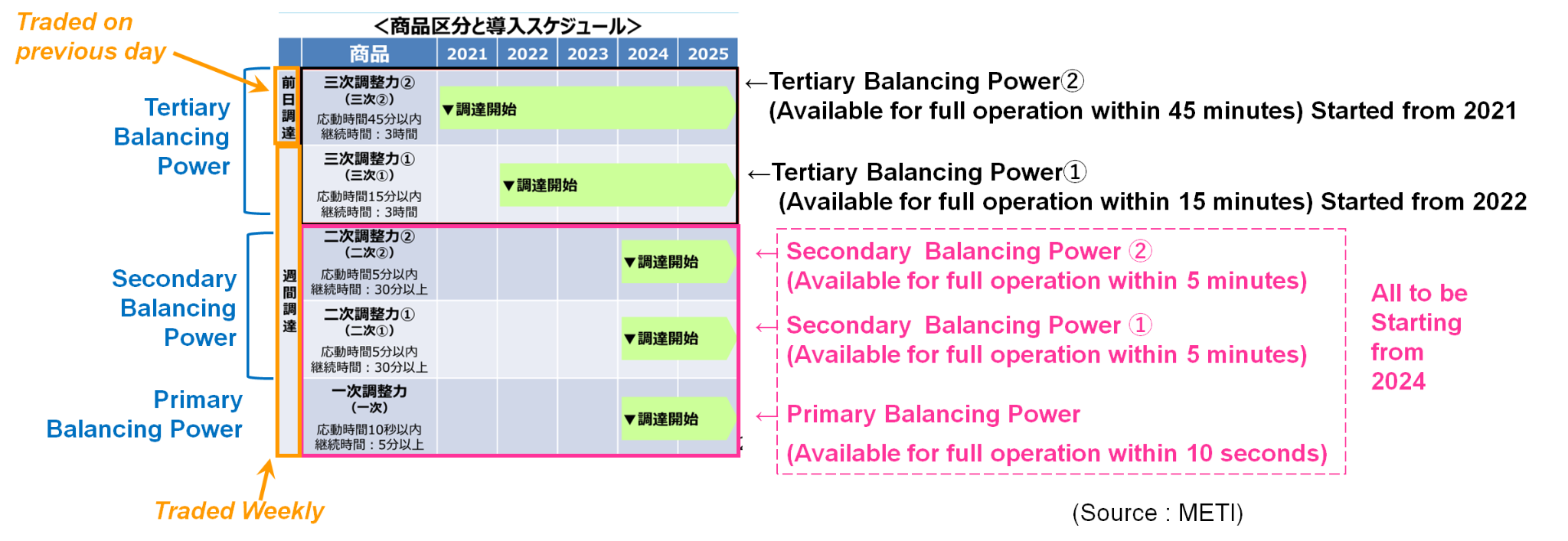

One of the biggest changes is the gradual introduction of new segments on the balancing market that correspond with the different conditions of various power sources.

The main balancing segments, or market products, are classified as “primary,” “secondary,” and “tertiary”. The former tends to refer to resources that can offer a near immediate response to power frequency deviations in real-time.

Secondary sources, such as natural gas peaker plants, can be called upon within a short period, often minutes, to adjust for more prolonged imbalances. Tertiary power corresponds to older thermal plants that run on coal or oil that require considerable time to restart, but which can be dispatched to manage long periods of imbalance in electricity supply and demand.

EPRX began its operations with two offerings:

- Tertiary Balancing Power ② (launched in 2021): To adjust imbalances, especially under specific programs, with operations commencing within 45 minutes of a request.

- Tertiary Balancing Power ① (launched in 2022): To address discrepancies between forecasted and real-time demand, starting within 15 minutes.

Three more offerings are set to be introduced in 2024:

- Secondary Balancing Power ②: Operational within 5 minutes.

- Secondary Balancing Power ①: Also operational within 5 minutes but using a distinct control mechanism.

- Primary Balancing Power: Operational within a rapid 10 seconds.

Each of the above categories has different requirements concerning the duration for which they should be supplied continuously and their control signals, LFC or EDC.

As per the current system, only Tertiary Balancing Power ② is traded on a daily basis, with the rest is traded weekly.

Split by frequencies

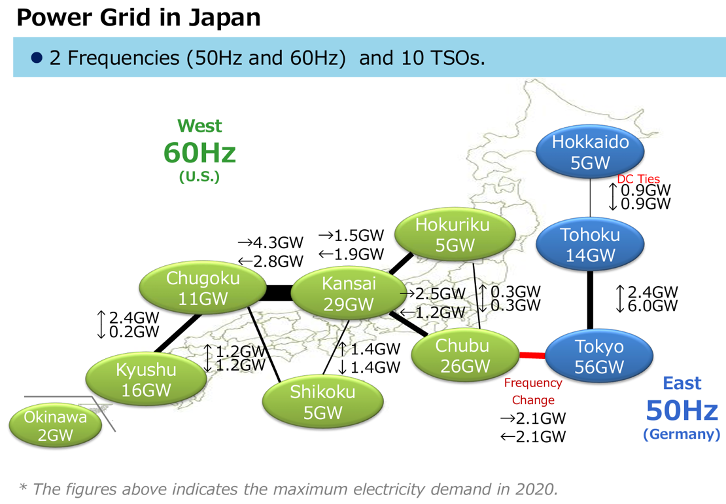

Japan’s unique power landscape, shaped over years with regional systems that are operated independently by EPCOs, presents challenges for the market’s evolution. Also, making a nationwide marketplace allows to integrate the trading of electricity, but it cannot overcome the physical challenges inherent in the power system.

The national power grid is bifurcated into 60 Hz and 50 Hz, and the capacity that can pass from one region to the next is limited.

Despite the liberalization and the establishment of EPRX, the primary suppliers for the upcoming 2024 offerings on the balancing market are projected to be the EPCO’s own generation companies. As noted earlier, most bidders for balancing auctions today are the EPCOs themselves.

While the reforms offer an innovative solution, METI will need to closely monitor, and when necessary, refine the balancing system to ensure the changes deliver a fair and competitive market, while also promoting the nation’s decarbonization policies.

But above all, the government and EPRX will need to ensure stability and efficiency in the power grid.

Source: METI

ANALYSIS

BY KYOKO FUKUDA

Paying for the Void:

Japan Looks for Business Model to Support CCS Projects

Japan spent around ¥100,000 ($686) per ton of CO2 to capture and store carbon emissions in this technology’s first trial a few years ago – five times more than the price of CO2 traded on any global carbon credits exchange. Luckily, the Carbon Capture and Storage (CCS) tech demonstration off the coast of Tomakomai port, Hokkaido, was almost entirely state-funded.

As the nation looks this year to promote CCS as a realistic clean energy solution and a technology that’s vital to the decarbonization of heavy industry, such cost performance will need to improve. At the same time, companies will also need to create viable business models for a storage system that inherently stops generating income once it’s full.

For now, the burgeoning sector is creating a buzz in Japan and attracting a wide array of businesses, from utilities like J-Power to cement-makers and pulp & paper companies. This is in part driven by growing state commitments in terms of funding and other support measures.

Announcing plans for future CCS projects is one thing, finding the financing and developing cost-efficient technologies is another. With many details in this industry as yet unclear, Japan NRG has reviewed some of the calculations that will be involved in CCS development.

What is CCS?

Carbon capture and storage (CCS) has been tapped as an integral part of Japan’s plan to achieve net zero emissions by 2050. It involves the capture of CO2 from power generation and industrial facilities that use fossil fuels or biomass as fuel; prominent among these are heavy industries like cement, steel or chemicals.

If not used on-site, the captured CO2 is compressed and transported by pipeline, ship, or rail for use in a range of applications, or injected deep into the ground. The two approaches are what separates CCS (i.e. storage only) from CCUS (in which the U stands for utilization).

Unless the carbon is re-used to make plastic, concrete or biofuels, in which it carries value as a raw material for a sellable product, carbon is essentially a cost. The expense of capturing, moving and then storing it has to be covered by the emitter or a third-party that’s invested in removing the CO2 from the atmosphere. In which case, the cost of CO2 could be covered by a carbon credit, which typically represents just that – one ton of CO2 removed from the air.

Credits are usually purchased by companies to offset CO2 emissions from their operations. In this sense, a buyer of carbon credits “sponsors” the removal of CO2 from the atmosphere.

The world’s biggest carbon credits system, the EU’s ETS mechanism, is also among the most expensive. Yet even on the ETS, the highest price to date is around 100 euros (¥15,864) per ton of CO2.

Japan’s carbon credits marketplace, being developed by the Japan Stock Exchange, is currently in test mode with full-scale trading not expected before 2026. In trials earlier this year, carbon credits derived from emission reductions in agriculture received the highest price of ¥50,000 (per 1 ton of CO2) but in very limited trading.

So, for the economics of CCS and CCUS to work, the price of CO2 as a feedstock or the cost of a carbon credit has to be higher than the cost of removing and processing the carbon.

Preparing the soil for CCS

In FY2021, Japan’s total CO2 emissions amounted to about 1.07 billion tons, or roughly 3% of the global total. CCS technology is believed to be capable of capturing an estimated 90% of CO2 emissions from power plants and industry. In fact, CCS is considered the only way to decarbonize Japan’s industrial sector without causing significant financial losses that would leave many industries unable to compete.

Between 2008 and 2020, Japan ran a trial to demonstrate the technical capabilities of CCS at the Tomakomai port on the island of Hokkaido. The experiment received ¥30 billion of state funds to capture and store 300,000 tons of CO2. The emissions were injected as far as 2.6 km below sea level between 2016 and 2019, after which the site was monitored. No leaks were found and the trial was deemed a success.

To follow up, the government has gradually sought to install a CCS regulatory framework:

- In 2020, it announced the “Green Growth Strategy Through Achieving Carbon Neutrality in 2050,” which for the first time positioned carbon recycling as an important decarbonization technology

- In the 6th Basic Energy Plan from October 2021, the government positioned CCS as a long-term project that needed to establish technologies, reduce costs, and develop appropriate sites

- In FY2022, the government allocated about ¥54 billion for CCS R&D and set up an experimental site for carbon recycling

- In the first three months of 2023, ANRE and METI unveiled long-term strategy documents for a new CCS-based sector and flagged how it should be financed

- In June 2023, state energy enterprise JOGMEC selected five domestic and two overseas sites for the first round of CCS projects that could be active by 2030

- The government plans to submit new CCS-specific legislation to parliament in the coming weeks, which will aim to clarify how the industry supply chain should work and certain technical and technological standards (“CCS Business Act”)

Further details on the above can be found in last week’s Japan NRG Weekly report.

What are the costs involved?

Interestingly, the government spent as much R&D funds in FY2022 on developing business model configurations for CCUS as on development of its technologies, according to METI’s annual report on energy (published in June 2023).

Below are some of the cost estimates for the industry that METI has come up with through several working group meetings.

In October 2022, the working group worked out a cost estimation based on the assumptions made by Research Institute of Innovative technology for the Earth (RITE) as follows.

|

Yen / ton of CO2 |

Current |

2030 |

2050 |

|

4,000 |

< 3,000 |

< 1,000 |

|

2,600 (500 KtCO2/year) |

2,600 (500 KtCO2/year) |

1,600 (3 MtCO2/year) |

|

9,300 (500 KtCO2/year) |

9,300 (500 KtCO2/year) |

6,000 (3 MtCO2/year) |

|

6,200 (200 KtCO2/year) |

6,200 (200 KtCO2/year) |

5,400 (500 KtCO2/year) |

|

6,900 (200 KtCO2/year) |

6,900 (200 KtCO2/year) |

5,400 (500 KtCO2/year) |

|

TOTAL | |||

|

12,800 |

10,800 |

8,000 |

|

13,500 |

11,500 |

8,000 |

|

19,500 |

17,500 |

12,400 |

|

20,200 |

18,200 |

12,400 |

Reference: METI

The Ministry of Environment will finance development of separation and capturing CO2, which is expected to be the most costly part of CCS tech, along with sea transportation.

Further development of technologies to compress and liquefy CO2, and transport it safely, is required to lower costs, according to METI, which suggests that the government will also take on the bulk of the financing of these R&D efforts.

The total R&D expenses for technologies to transport CO2 by vessel alone are expected to be around ¥18.5 billion, according to METI. Companies involved in this R&D area began preparatory work in 2021 so that actual sea transport of liquid CO2 from the Maizuru thermal power plant (KEPCO) near Kyoto to Tomakomai in Hokkaido (about 1,000 km) can begin in 2024. The trial should lead to the establishment of a set methodology for the process by 2026.

Once this R&D succeeds, the construction cost for a CO2 tank onboard a transport vessel and at onshore facilities will drop to ¥4.1 billion, partly thanks to the scaling up of tank sizes.

Finally, there are the monitoring costs of CO2 once it’s stored underground. METI estimates these at about ¥600 to ¥800 million per year for each CCS site. Twice in five years, a 3D seismic assessment will be required, which increases the total annual cost of monitoring to ¥1 billion to ¥1.2 billion.

Should the industry succeed in its initial phases, and achieve technology breakthroughs, Japan expects that the overall cost of CCS will drop by up to 40% by 2050.

Funding the development

The financing and development of cost-efficient technologies is another major challenge. After all, CCS requires significant capital expenditures in order to develop its infrastructure.

Initially, the government has said that JOGMEC and other state actors will cover the cost of searching for new CCS sites and the geological inspections of candidate areas. Once it moves to a feasibility study stage, the costs will be shared between companies and the government.

JOGMEC has announced an initial five sites in Japan and two abroad to provide up to 13 million tons of CO2 per annum by 2030 in storage capacity, but it then aims to secure up to 20 to 25 sites by 2050 that could receive annually 120 million to 240 million tons.

The government also decided to provide 100% of the capital expenditures needed for the development and construction of CCS sites in Japan. If a project is financed by private sources, JOGMEC will be available to assist by providing funds as needed.

Once a CCS project is operational, state support will come via tax breaks or other voluntary credits. One likely form for the latter will be credits under the Joint Crediting Mechanism (JCM) that Japan has used to coin carbon credits abroad. METI said it also wants to support the launch of an international crediting system for CCS-derived emissions.

The biggest challenge that CCS businesses might face, however, could come at the end once the reservoir’s capacity is full. When there will be no new tonnage of CO2 coming in, the operating company will be deprived of income from its core business. Meanwhile, expenses associated with monitoring the site would remain.

How the business will work for the long-term and be financially sustainable – without state support – is yet to be resolved.

GLOBAL VIEW

BY JOHN VAROLI

Below are some of last week’s most important international energy developments monitored by the Japan NRG team because of their potential to impact energy supply and demand, as well as prices. We see the following as relevant to Japanese and international energy investors.

Offshore wind

Europe slipped as the world’s largest offshore wind market. As a result of rising costs and supply chain disruptions, the Asia-Pacific region, led by China, is now the leader. In 2022, Europe accounted for about 47% of the 64 GW of total global offshore wind capacity, while Asia-Pacific surpassed it with almost 53%. China alone made up 49%.

EU/ Fossil fuels

Fossil fuels produced just 33% of the EU’s power in the first half of 2023, which is 17% lower YoY, and the lowest share on record since 1990. The main reason was lower electricity demand. Mild weather, consumption-cutting policies and high gas and power prices have encouraged industries and consumers to curb energy use.

EU/ Solar power

The EU has 40 GW of solar panels stored in warehouses due to various bottlenecks and barriers in the supply chain, including labor shortages, critical material delays and long interconnection queues. This is equal to the amount of solar capacity that the EU deployed in 2022. This figure might increase to 100 GW by year’s end.

India/ Net-zero

More than a dozen companies led by industrial conglomerate JSW Group wrote to G20 leaders to push for an end to fossil fuels use without emissions captured, as well as support for green vehicles and clean power. G20 leaders will gather in New Delhi on Sept 9-10.

LNG

In the past year, Germany, the Philippines, and Vietnam began importing LNG. The EIA also expects Australia, Cyprus, and Nicaragua to start importing LNG, and many other countries are in the final stages of developing LNG import capacity. Global LNG import capacity is set to expand by 16%, or 23 bcfd, by late 2024.

Namibia/ Oil

Shell and TotalEnergies will develop a giant oilfield in the Atlantic Ocean off the African country’s coast. This year, Total will spend $300 million — half of its global exploration budget — in Namibia.

Russia/ LNG

In the first seven months of this year, Belgium and Spain were the second and third-biggest buyers of Russian LNG, behind China. Overall, EU imports of LNG were up 40% between January and July compared with the same period in 2021. Before the war in Ukraine, the EU did not import significant amounts of LNG due to its reliance on piped gas from Russia.

Saudi Arabia/ Nuclear power

Riyadh is speaking with China to build a nuclear power plant, a move that might be meant to pressure the U.S. to compromise on its conditions. U.S. nuclear aid is contingent on the Saudis agreeing to not enrich or mine their own uranium, which China doesn’t demand.

U.S./ Offshore wind

The first auction of offshore wind rights in the Gulf of Mexico ended with a single $5.6 million bid, reflecting meager demand in a region known for oil and gas. Germany’s RWE won rights to the site off Louisiana, while the other two areas in Texas received no bids.

U.S./ Power output

Total power generation from January to August 20 declined 2.1%, YoY. But the share of power generated from natural gas averaged 40.4% through mid-August, up from under 36% in the same period in 2022. This was due to low wind power output.

2023 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Hulic Ochanomizu Bldg. 3F, 2-3-11, Surugadai, Kanda, Chiyoda-ku, Tokyo, Japan, 101-0062.