Negotiations on Japan’s FY2024 budget are underway, with the Ministry of Finance squaring off against METI, the MoE, and others. The need to invest big in clean energy is substantial. The amount of funds, and for which pathways, will determine where Japan sits mid-way through a decade during which it vowed to slash emissions by half. This budget will be the biggest yet and will struggle to satisfy all parties. Who are the likely winners?

For the energy transition to succeed in Japan, the national grid will have to undergo significant modernization. Now, a new entity will act as a central repository for electricity transmission and distribution data. For Japan to support increased reliance on variable renewable energy, distributed systems, batteries and EVs, etc., it needs to create a next-generation grid that speaks the same language. Hopefully, the central data entity will enable just that.

GLOBAL VIEW

A wrap of top energy news from around the world.

EVENTS SCHEDULE

A selection of events to keep an eye on in 2023.

JAPAN NRG WEEKLY

PUBLISHER K. K. Yuri Group

Editorial Team Yuriy Humber (Editor-in-Chief) John Varoli (Senior Editor, Americas) Mayumi Watanabe (Japan) Wilfried Goossens (Events, global) Kyoko Fukuda (Japan) Filippo Pedretti (Japan) Tim Young (Design, Japan)

New Energy and Industrial Technology Development Organization

kWh

Kilowatt hours (electricity generation volume)

TEPCO

Tokyo Electric Power Company

FIT

Feed-in Tariff

KEPCO

Kansai Electric Power Company

FIP

Feed-in Premium

EPCO

Electric Power Company

SAF

Sustainable Aviation Fuel

JCC

Japan Crude Cocktail

NPP

Nuclear power plant

JKM

Japan Korea Market, the Platt’s LNG benchmark

JOGMEC

Japan Organization for Metals and Energy Security

CCUS

Carbon Capture, Utilization and Storage

OCCTO

Organization for Cross-regional Coordination of Transmission Operators

NRA

Nuclear Regulation Authority

GX

Green Transformation

NEWS: ENERGY TRANSITION & POLICY

Banks set core criteria to finance hydrogen projects, long-term offtake agreement vital

(Japan NRG, Oct 17)

To get financing for a hydrogen project, Japan’s top banks stated these conditions:

The technology is approved as a valid decarbonization tool by the govt;

The reduction in CO2 emissions can be monitored and measured/ confirmed;

There’s a long-term offtake agreement with a buyer.

Other factors will be the project’s ability to qualify for state subsidies that make the clean fuel affordable, said Japan’s top three banks (known as “megabanks”) during Connecting Green Hydrogen Japan 2023.

Japanese banks are willing to finance hydrogen and related projects at home and globally, as long as one entity is Japanese, said Fujiki Masayuki, head of Structured Finance at MUFG Bank.

Sumitomo Mitsui Banking Corp is creating specialist funds to finance hydrogen projects, said Kaneko Tadahiro, senior assistant to the head of global banking.

Japan’s 2030 hydrogen price target is no longer “feasible”: Mitsubishi

(Japan NRG, Oct 18)

Amid rising costs, the govt’s 2030 target to reduce the price of imported hydrogen to $2-3/ kg “isn’t feasible anymore,” said Fujimoto Kiichiro, the GM of hydrogen infrastructure development at Mitsubishi Corporation.

Japan will try to find ways to reduce the cost of producing and importing hydrogen and related fuels, but the current market can’t be ignored, said Fujimoto, speaking at Connecting Green Hydrogen Japan 2023.

Mitsubishi is developing hydrogen projects globally and remains open to dealing with all hydrogen carrier technologies, Fujimoto said. “We don’t think there’s a clear winner at this stage.”

CONTEXT: Japan’s latest iteration of the national hydrogen strategy, released in summer, has kept the govt’s original target of lowering the cost of imported hydrogen to $2/ kg, and domestically manufactured to $4/ kg. These levels are several times lower than what’s estimated by clean hydrogen project developers outside Japan.

TAKEAWAY: At the same conference, an advisor on GX matters to Mitsubishi Group, Endo Hidetaka, said that the cost of domestic hydrogen projects is now as high as $6-$9/ kg, making them uncompetitive with imports. Most of Japan’s hydrogen production would rely on electrolysis powered by renewables (or in the future nuclear stations). The cost of electricity generated by renewables in Japan is higher than in most other countries, which consequently pushes up the cost of hydrogen production.

GFG Alliance, which seeks to transform its steelworks from coal-based to clean hydrogen, is willing to export “green” steel products at prices similar to those now made using fossil fuels.

The company won’t initially seek a premium from buyers, and will structure pricing to reflect today’s market in order to capture demand, said Theuns Victor, head of GFG’s Liberty Primary Metals, speaking at Connecting Green Hydrogen Japan 2023.

The company is expanding steelworks and mining at its Whyalla site in Australia, and is in talks with Japanese steelmakers and traders interested in these assets, said Victor. Japanese interest is both in terms of offtake for products and as investments.

Tokyo Stock Exchange wants to create futures market for carbon credits

(Japan NRG, Oct 18)

Tokyo Stock Exchange (TSE) would like to facilitate trading in futures contracts for the carbon market, said Ishizaki Takashi, CEO of TOCOM, a part of TSE, during a power market seminar.

TSE will study market models in Europe and North America.

CONTEXT: TSE began trading carbon credits on Oct 11. Registered members can trade the existing carbon credit, known as J-Credit.

So far, close to 200 companies have registered in the carbon market, Ishizaki said.

Climate-change information disclosures will likely further affect Japanese company stock evaluations, amid a growing focus on Scope 3 emissions — those emissions from entire supply chains.

For Japanese companies, GHGs emitted by companies in which they have invested as part of their business will likely affect their own stock prices.

For example, when taking into account the emissions of companies in which real estate developer Sumitomo Realty holds cross-holdings, its emissions are 2.6 times higher. Toyota Industries is another whose Scope 1-3 emissions would double if the emissions related to its shareholdings are taken into account.

Japan aims for carbon neutrality by 2050, through legal mandates and establishing the Japan In-house Counsel Network (JICN).

GHG emissions increased 2% since 2020, but dropped 20.3% over 2013.

In August, over ¥1.2 trillion was allocated in 2024’s budget for decarbonization and private sector involvement.

However, a survey indicates only 6.8% of companies feel a positive impact, with over 70% seeing no impact or unsure of the benefits.

TAKEAWAY: PM Kishida, and his predecessors, have been keen to stress that the move to net zero / carbon neutrality / GX will be a plus for the economy. That messaging was important because many industrials in Japan saw the transformation as a cost item. The mood had appeared to shift from 2020, but it’s fair to say that few companies have as yet developed sizable businesses for the carbon-neutral era. In Japan, most clean energy projects are still at a pilot stage or in early commercialization. So, they have yet to show their financial benefit.

METI Minister Nishimura said gasoline and power subsidies will be extended for a second time, as gasoline prices hit record highs, amid increased winter demand.

Next week the govt will make an economic package with new subsidies.

Such subsidies, which began in January 2022, were supposed to end in September 2023 but were extended through December.

Nishimura said an exit strategy from the subsidies is needed, but he didn’t elaborate.

TAKEAWAY: As noted several times in our Data Book reports, the exit from energy subsidies is very hard to create because in addition to high fossil fuel prices, Japan is suffering from a weak yen. In effect, the energy subsidies are covering the currency depreciation, which is a macroeconomic factor, more than energy price fundamentals.

METI officially updated plans for EV charging stations, including a new goal of 300,000 charging stations by 2030, double the previous goal.

METI will promote chargers with higher output, averaging 80 kW. Existing stations have 40 kW output on average. METI may introduce auctions for subsidies to prioritize cost-effective projects.

JERA, JGC Holdings, and the Indonesian State Electricity Company (PLN) signed an MoU for a study on CCS projects at PLN’s thermal power plants.

They’ll explore the feasibility, technical, and legal aspects of introducing CCS at coal and gas-fired power plants, with JGC focusing on storage technologies and cost estimation; PLN will work on data provision and local coordination.

The study will receive funding from METI under a new initiative promoting overseas infrastructure development by Japanese firms.

TAKEAWAY: Indonesia is the only ASEAN country with a legislative framework on CCS at the national level. Together with funding from METI and technical support from Japanese trading houses, this is a strong foundation for CCS development in that country.

Mitsubishi Heavy Industries (MHI), along with two subsidiaries, began a demo to test a system liquefying captured CO2 from gas engine generator sets. Held at the Sagamihara Plant, it utilizes a compact CO2 capture and liquefaction system.

The liquefied CO2 is easily transportable and helps in adopting CCUS technologies.

Support services will be verified using MHI’s remote monitoring, continuing a CO2 capture demo launched in 2022. The goal is to learn about handling liquefied CO2 and develop a fully integrated customer support system from capture to liquefaction.

KEPCO and JFE Steel signed an MoU to study the capture, liquefaction, storage, and transportation of CO2 emissions from their power plants and steel mills to underground storage sites.

This study will address technical and cost-related challenges.

TAKEAWAY: While some energy transition experts see CCS as unacceptable since it seeks to prolong the operations of carbon-intensive industries, others see it as the optimal solution for hard to decarbonize processes like steelmaking, which accounts for about 40% of CO2 emissions in the industrial sector.

Enecoat Technologies, Mitsui Fudosan Residential and Kyoto University began research on perovskite solar cells (PSC) for the residential market. They’ll install PSC on Mitsui Fudosan condos to test performance and safety.

CONTEXT: PSC made of perovskite crystals are lighter, thinner and could be more flexibly shaped compared to silicon panels. However, silicon panels have also become lighter and thinner as panel manufacturers focus on the residential market on the back of tighter solar farm regulations.

TAKEAWAY: The PSC manufacturers are likely to seek alliances with construction companies to develop technical and safety standards essential for PSC product launches and effectively compete with silicon panels.

Mitsubishi Chemical Group developed a solar panel recycling process that cuts costs by 20-30%. Shinryo, a group company in Kitakyushu City, will recycle the panels.

The process involves heating and gasifying the sealing materials, to break apart the panel components without crushing.

Shinryo plans to triple its recycling capacity to 4,300 tons /year by 2030. It will double its Kitakyushu plant capacity and build new plants on the premises of Mitsubishi Chemical.

CONTEXT: NEDO forecasts that 170,000-280,000 tons of panels will be recycled in 2030, surging from 3,000 tons in 2020.

TAKEAWAY: Treatment of the sealing materials has been the most labor-intensive process of panel recycling. According to NEDO, the best available technologies had achieved a ¥5/ watt recycling cost before Mitsubishi Chemical’s development.

The Bases Conversion and Development Authority (BCDA) in the Philippines joined forces with United District Energy International (UDEI) and Marubeni to research low-carbon district cooling technologies for New Clark City.

The collaboration seeks to address high energy consumption during the hot season in Central Luzon. District cooling systems, which are alternatives to traditional air conditioners, will be studied.

An MoU was signed for a feasibility study to gauge the technology’s potential. If implemented, these systems could reduce electricity consumption by up to 50%.

Cosmo Energy and Sekisui Chemical agreed to study applications of Sekisui’s “chemical looping reaction” technology for producing SAF and other clean fuels.

It converts CO2 into carbon monoxide at a 90% conversion rate, which is then used as feedstock for methanol and ethanol that’s processed into synthetic fuels and SAF.

The companies will explore using CO2 emissions from Cosmo oil refineries in Japan to produce clean fuels.

Tokyo Gas, Tokyo Gas Engineering Solutions and Calbee began testing biogas production from potato chip waste, which, after fermentation, will generate biogas to be used as fuel to generate power.

TAKEAWAY: This development shows the spread of waste recycling in the food sector. The ideas are diverse: apple waste mixed with chemicals to make “vegan leather”, peanut skins for car seat covers, etc. However, they’re not all sustainable and some are costly. Biogas production requires heat to store the feedstock at 35-40°C, which is problematic in winter.

The Japan Fair Trade Commission has asked the Japan Containers and Recycling Association to improve competition in the used plastic bottles and packaging market by opening the association’s auctions to wider participation.

The JFTC request reflected the results of its fact-finding survey on the plastic bottle recycling practices and material flow.

TAKEAWAY: About 19% of waste is recycled and the govt aims to raise that figure. The JFTC move will help build proper market mechanisms in the recycling sector.

Nissan Motor has unveiled a prototype of a mini-van that runs on all solid-state batteries at the Japan Mobility Show 2023. The batteries have capacities large enough for V2Home and emergency power supply outlets. Detailed data on performance was not provided.

METI and ANRE unveiled a new strategy to reduce curtailment of renewable energy, which has become more frequent nationwide.

The proposal calls for taking budgetary measures and improving system design in residential and industrial sectors; it involves promoting power demand during the day with discounted electricity rates and expanding the range of pricing options.

Also, it calls for utilizing pumped-storage during times of surplus renewables energy production and for generating electricity during the evening and night.

As far as grid reinforcement, the plan calls for revising operation of interconnector gates / lines to expand the volume of electricity that can be transmitted outside the home region. The final version of this new strategy will be completed by year’s end.

TEPCO Power Grid outlined its plans for solar power curtailment in FY2024. It forecasts 1.51 MW of curtailment on the 154,000 V Joetsu trunk line and 66,000 V Tamamoro line for non-firm power sources.

A uniform control method will be used to maintain a consistent proportion of output reduction to the power generation plan. This approach allocates curtailment in 30 minute intervals based on a pro rata calculation of required volumes versus planned generation volumes.

In the future, TEPCO PG will also require facilities that have a high possibility of being curtailed to submit individual power generation plans.

The uniform control method is undergoing test runs this fiscal year. The power control system will be updated and modified next year and is expected to transition fully to the new curtailment methodology from as soon as January 2025.

Engineering giant JGC Holdings will rent space on the roofs and walls of other companies’ logistics warehouses and factories, install perovskite solar cell (PSC) equipment, and start supplying electricity. JGC will use cells made by Enecoat.

The company is keen to enter the power business and sees PSC as the basis for a business model for “power generation anywhere” technology.

JGC will also consider delivering electricity through power lines to factories and logistics warehouses other than those where solar cells are installed. In this case, it will need to get a METI license as an electricity retailer.

In 2024, JGC will run a demonstration test for this business by installing PSC at a distribution warehouse in Tomakomai City, Hokkaido. Large-scale use is slated for 2026.

According to power demand data for May compiled by METI and ANRE, the number of new electricity providers decreased by six compared to the previous month to total 673 providers. Of these, only 512 providers had actually recorded sales.

The total electricity sales volume of new electricity providers (the so-called shin denryoku) decreased by 10.4% to 8,525 GWh. Low-voltage sales decreased by 13.3%, high-voltage by 8.0%, and extra-high voltage by 2.2%.

In the low-voltage category, many new electricity providers fell short of their sales performance from the previous month. The period from April to May saw a lull in electricity demand. In April, the weather was warm nationwide.

In the high-voltage category, the leading companies showed a noticeable decline in sales, with ENNet (1st place) and Eneres Power Marketing (8th place) especially experiencing a significant drop in sales volume.

According to the Electricity and Gas Trading Monitoring Committee, sales of electricity in July were 6,882 GWh, down 3.2% compared to a year earlier (but up 16% month-on-month).

New electricity providers, on the other hand, saw a 21.4% decrease in the same period, amounting to 1,138 GWh (but up 24.8% MoM). This marks the tenth consecutive month of double-digit decreases on a YoY basis.

As far as electricity sales volume in July, the share of new electricity providers was 16.5%, which is a decrease of 3.9 points compared to the previous month (an increase of 1.1 points from the previous month).

Kyushu Electric Power Transmission & Distribution plans to invest ¥650 billion in facilities by FY2027, a 10% increase over the previous five years.

This investment is driven by expected growth in electricity demand due to the entry of semiconductor-related companies and the expansion of renewable energy.

The company will upgrade substations and transmission lines to meet this growing demand and work to reduce power loss through initiatives to avoid curtailment.

They’ll also invest in additional transformers at various locations, and plan to increase transformer capacity at substations and expand transmission lines.

Mitsubishi Corporation Offshore Wind and Mitsubishi Corporation Clean Energy quit the Japan Wind Power Association on Oct 10, claiming it had gaps in “perception” with the association that remain unresolved.

The JWDA, along with lawmaker Akimoto Masatoshi, pushed for changes in offshore auction rules after a Mitsubishi consortium won all three main offshore wind project auctions in 2021. Akimoto was indicted for alleged bribery.

TAKEAWAY: Due to the outcry and controversy that followed Japan’s first offshore wind auction in December 2021, the auction rules were changed in December 2022. One of the biggest changes was to make the electricity price offered by the project developer less important in the evaluation of their plan. Another change was to limit how much capacity one company could bid for at the same time. With these new rules in place, the standout winner of that Round 1 auctions, Mitsubishi, chose not to participate in Round 2.

Japan Wind Development and its officials who served as board members have left the Japan Wind Power Association, effective Oct 18.

ANRE has advised third-party reviews of JWPA activities, and the association will conduct reforms.

CONTEXT: METI has suspended the company Japan Wind Development, which had allegedly financed Akimoto, from auction participation during the period Sept 29 to June 29, 2024.

Valhall, the Japanese subsidiary of Yggdrasil Commodities in Denmark, launched offtake for large renewable energy projects in the country, and said it seeks more clients in Japan.

Earlier this year, the company registered as an Energy Resource Aggregation Business Operator. It now manages over 300 MW across eight out of the nine Transmission system operator (TSO) areas in Japan.

Valhall aims to collaborate on wind, hydro, and solar projects in all TSO areas.

Tohoku Electric conducted a demo test at the Niigata Thermal Power Plant, mixing 1% hydrogen by volume with LNG. The test aims to analyze data and advance the practical use of hydrogen-based thermal power generation.

This co-firing test will run until March 2025, with plans to increase the number of demo tests.

The mixture of hydrogen and LNG results in a 0.3% reduction in CO2 emissions compared to using only LNG as a fuel.

TAKEAWAY: The CO2 reduction is small, but the goal is to increase the ratio of hydrogen over time. If the CO2 footprint of the hydrogen is low, then it could enable the reduction of emissions from thermal power generation. However, these are very early days and in addition to the environmental benefits there are questions over the cost of this approach.

Speaking in Tokyo, Hokkaido Governor Suzuki Naomichi reiterated his opposition to hosting in his prefecture a preliminary survey for selecting the final disposal site for high-level radioactive waste from reactors.

CONTEXT: The selection of a final nuclear waste disposal site requires three stages, the first of which is currently ending in the locality of Suttsu (Hokkaido), where a council election was held on Oct 3. Five candidates in favor of continuing the review process were elected, securing a majority. But proceeding to the next stage of the preliminary survey also requires the prefectural governor’s consent.

TAKEAWAY: The governor’s position cites a prefectural ordinance that discourages the import of nuclear waste into the region. Central and local govt representatives in favor of the surveys claim that at this stage the surveys do not violate this ordinance. However, this only seems to be a way of buying time.

The Hokkaido environmental panel, which reviews wind projects and writes recommendations to the governor, is divided on the review results of the 650 MW Rumoi Wide Area Wind Project planned by Eurus Energy.

On Oct 2, the nine panel members discussed Eurus’ proposed environmental assessment methodology before writing a recommendation to the Hokkaido governor.

The draft of the recommendation said the proposed Eurus methodology lacked clarity. The project is divided into four areas, but no details on the facility installations were given. It also urged Eurus to rewrite the survey methodology. The final recommendation will reflect the Oct 2 discussions.

Nyuzen Marine Wind, which is owned by Venti Japan, JFE Engineering and Hokuriku Electric, brought online its 4.8 MW offshore wind power station off the coast of Nyuzen township (Toyama Pref) on Sept 22.

This is claimed as the first offshore wind power station to be fully owned by the private sector.

Tsuruoka City (Yamagata Pref) said Japan Renewable Energy canceled its 40 MW Kamo wind project. The city previously raised concerns that the project might impact areas protected by the Ramsar Convention.

TAKEAWAY: Uncertainty clouds JRE’s wind projects. In August, Kami Township (Miyagi Pref), where JRE plans a 42 MW wind project, elected an anti-wind mayor. The project site is protected under the Globally Important Agricultural Heritage Systems framework.

Due to damage in the heat transfer tubes in the steam generator, KEPCO will delay the restart of Unit 3 at Takahama NPP that’s now under regular inspection.

Although no radioactive material leak was reported, the restart, initially planned for early December, will be postponed.

The steam generator will be replaced during the regular inspection in June 2026.

CONTEXT: Similar damage was discovered in Takahama’s Units 3 and 4.

A task force with the International Atomic Energy Agency tested fish near the Fukushima Daiichi NPP to assess the impact on marine life as treated water from the damaged facility is released into the Pacific Ocean.

In the coming weeks, the IAEA will announce the test results along with other data.

CONTEXT: Citing the treated water release that began in late August, China and Russia have suspended purchases of Japanese seafood.

SIDE DEVELOPMENT: TEPCO opens reactor hatch for robotic arm at Fukushima Daiichi Unit 2 (Japan NRG, Oct 17)

TEPCO fully opened the hatch to the reactor containment vessel for Unit 2 at the Fukushima Daiichi NPP, for a trial removal of fuel debris by inserting a robotic arm.

TAKEAWAY: Units 1, 2 and 3 contain more than 800 tons of nuclear waste. TEPCO plans to undertake trials of waste removal by late FY2024, starting with small quantities. While public attention has focused on Fukushima treated water release this summer, this process is critical for the plant’s decommissioning.

The world will need $7 trillion to ensure sufficient gas supply through 2050 as nations shift to cleaner energy sources, according to the Institute of Energy Economics, Japan.

As countries look to cut emissions and shift to gas from dirtier coal, investments will go to develop new gas fields, construction of new LNG export facilities, and expansion of existing plants, according to the IEEJ report.

The scenario assumes the world will move to reduce emissions by 56% by 2050, and that emerging nations won’t be able to hit carbon neutrality by mid-century, the IEEJ said.

CONTEXT: After a boom period from 2000 to 2021, the world’s gas markets have entered a more uncertain period marked by slower growth and greater volatility. This is due to both global efforts to end the use of fossil fuels and transition to clean energy, as well as geopolitical tensions between G7 nations and Russia.

TAKEAWAY: Competing agendas have complicated forecasts for the use of fossil fuels and their planned phase-out. These contrasting outlooks on natural gas demand in the coming years make companies hesitant to invest in new supply. The IEA sees gas demand peaking this decade and says no new projects are required. But leading natural gas producers, such as Chevron and Shell, say that gas will play a long-term role in the energy transition, especially as countries shift away from coal.

ADNOC Gas inked an approximate $500 to $700 million LNG deal with JERA Global Markets, pushing its total LNG deals to the $9.4 to $12 billion range since its March listing.

This deal is part of plans to boost UAE-Japan energy relations. Following a similar deal with JAPEX and other international agreements, ADNOC is growing its global presence, notably in East and South Asian markets. In August, ADNOC invested $3.6 billion to enhance gas processing, with expanded production at home in the UAE.

CONTEXT: In July, PM Kishida visited the UAE and other nearby countries to improve existing partnerships on energy supplies.

Mitsui is considering taking a stake in the expansion of Qatar’s North Field LNG, but no details were provided.

Mitsui’s interest in North Field might be part of a consortium potentially including JERA, which also seeks long-term LNG agreements.

CONTEXT: In 2022, Japan was the top global LNG importer, primarily sourcing from the Middle East. During a visit to Qatar in July, PM Kishida emphasized enhancing energy and economic collaboration.

TAKEAWAY: The potential Mitsui contract with Qatar has now been reported in two different media outlets. In a recent interview with Bloomberg, a Mitsui energy executive avoided confirming the talks with Qatar, but it looks like an agreement could be struck in the near future.

The expansion of the Tangguh LNG facility in Indonesia, which has several Japanese stakeholders, has shipped its first cargo.

The new unit’s launch was postponed from 2020, partly due to COVID-19.

Tangguh’s annual production has now increased by 3.8 million tons to 11.4 million tons. Of this, 2.8 million tons will be sold to Indonesian power utility PLN, and up to 1 million tons to KEPCO. BP operates the Tangguh facility, owning around 40%; six Japanese investors, including Mitsubishi and Inpex, collectively hold about 46%.

CONTEXT: In 2022, Japan sourced around 10% of its LNG from Russia, but seeks to reduce this dependency by supporting LNG projects with friendly nations.

BHP Mitsubishi Alliance (BMA) agreed to sell the Blackwater and Daunia mines to Whitehaven Coal for about $4.1 billion, with a primary transaction of $3.2 billion and contingencies of up to $900 million over three years.

BMA is jointly owned by Mitsubishi Corporation and global mining behemoth BHP, and focuses on metallurgical coal ventures in Australia.

Whitehaven, an Australian coal producer, will take over the operations. This sale will be finalized in FY2024.

CONTEXT: The Blackwater mine produces about 12 million tons a year, while Daunia produces about 2.5 million tons a year. BMA will still keep its premium hard coking coal mines in Australia such as Peak Downs and Saraji.

TAKEAWAY: Among the reasons for the sale was the BMA’s desire to focus on other projects involving heavy coking coal and iron ore, copper and nickel. Whitehaven’s decision is out of sync with a global market that is increasingly moving away from coal. But events of the past 18 months have shown that when energy supplies are tight, the market will gladly expand coal purchases to keep the lights on.

Japan’s LNG imports in September were 5.5 million tons, up 3.8% YoY, the first such rise in eight months; the total import value was ¥484 billion, down 44.8% YoY.

September crude oil imports were 11.2 million kiloliters (70.7 million barrels), down 16.7% YoY; the total import value fell 3.2% to ¥895 billion.

Thermal coal imports were 8.4 million tons, down 11% YoY; the total import value was ¥219 billion, down 56.2%.

Cosmo Energy set up Cosmo Energy Exploration & Production in the U.S.

The company holds proprietary technologies for sub-surface extraction of lithium from underground brine, taking less time with less environmental impact.

LNG stocks of 10 power utilities stood at 2.16 million tons as of Oct 15, up 15.5% from 1.87 million tons a week earlier. METI initially reported the Oct 8 stocks as 1.89 million tons but revised the figure.

The end-October stocks last year were 2.53 million tons. The five-year average for this time of year was 2.01 million tons.

ANALYSIS

BY PROF. ANDREW DeWIT

Energy Policy Studies

Rikkyo University

Japan’s GX and Public Finance

Negotiations on Japan’s FY2024 budget are well underway, pitting the Ministry of Finance bean counters against METI, the MoE and other ministries that seek to maintain or increase their funding in the wake of the COVID splurge. Some of the key budget items – and arguments – will revolve around decarbonization.

Japan needs to invest substantially in clean energy, but it also faces massive fiscal challenges. How much of the proposed energy-related spending will eventually be approved, and for which pathways, will determine where the country sits mid-way through a decade during which it has vowed to slash emissions by as much as half.

A number of emergent industries, such as clean hydrogen and carbon capture, see this state funding as the catalyst they need to move from pilot projects to commercial scale. For the established players in thermal and nuclear power, funds are vital for revamping aging infrastructure and introducing new technologies. For those involved in renewables, state support could help revive flagging momentum.

Japan’s FY2024 budget is almost certain to be the biggest yet. Even so, it will still struggle to satisfy all parties. So, who are the likely winners?

The new gold rush

Virtually all Japan’s central agencies seek a role in the new gold rush of the Green Transformation (GX). On May 12, Japan’s Diet (parliament) formally adopted the GX industrial policy as the key mechanism for promoting carbon neutrality. Much like the roughly $400 billion American Inflation Reduction Act (IRA), which accelerated Japanese action, the GX initiative is technologically neutral on clean energy supply. GX includes nuclear power in addition to the gamut of renewable energy sources, efficiency, digitalization, and the emergent areas of hydrogen, ammonia, carbon recycling and other avenues of decarbonization.

But unlike the IRA, two-thirds of whose climate and energy provisions are financed by tax credits, Japan’s GX proposes a big dollop of direct public finance – cumulatively as much as ¥20 trillion over the next decade. This spending is to prime the pump of private-sector investment and achieve a combined public-private total of ¥150 trillion of GX investment by the mid-2030s.

Policymakers plan to have most of Japan’s GX public-sector spending backed by GX transition bonds, paid down with revenues from pricing carbon. While adopting these carbon pricing and related mechanisms is not slated to start until 2026, the first issuance of Japan’s GX transition bonds is imminent.

To be sure, some environmental analysts fret that GX transition bonds may not be ready for ESG prime time. But these presumed issues are perhaps overstated given, for example, the $200 billion (2022 data) scale and diversity of the Asian green, social, sustainable, and sustainability-linked bond market.

Budget process and details

In any event, late August saw the various ministries publish their fiscal requests for the 2024 budget, submissions that are now being debated with the MoF. The normal budget cycle sees the MoF then compile a draft budget for the Cabinet in December, followed by the Cabinet’s submission of the budget for debate in the Diet. Its approval is generally secured in March, and the budget implemented with the April 1 start of the fiscal year.

The August spending requests for GX are part of a massive ¥114 trillion in the total 2024 initial budget request. The overall GX component is generally assessed at about ¥2 trillion, a sum that seems likely to survive MoF scrutiny given the imperative of GX for the government’s foreign and economic policy.

Among the major components proposed for the 2024 budget:

¥52.3 billion for research on next-generation nuclear power (and ¥152.1 billion over 2024-2026)

¥40.7 billion for fostering GX start-up initiatives (and ¥203.4 billion over 2024-2028)

¥720.7 billion for advanced solar, hydrogen catalyzers, batteries, wind, power microprocessors (and ¥1.2 trillion over 2024-2028)

¥91 billion for helping SMEs transition from fossil fuels and adopt cutting-edge efficiency (and ¥192.5 billion over 2024-2028)

¥148.4 billion for heat pumps, insulation and other building efficiency

¥141.7 billion for diffusing EVs, hybrids, and fuel-cell vehicles in addition to charging stations

As we can see, ¥1.2 trillion is slated for FY2024, with the balance spread over periods of three to five years. The ¥720.7 billion ear-marked for solar, wind, and other renewables may look significant, but caution seems in order: the eye-watering costs of subsidizing power microprocessor projects could readily consume most of that money.

GX funding yet to be determined includes measures to help hard-to-decarbonize sectors reduce emissions, recycling initiatives, hydrogen, ammonia, sustainable aviation fuels, and other project areas. Hydrogen in particular appears to be an area to watch, as investors are eagerly anticipating the signaling effect of public sector GX investment.

At present, the government, which seeks the best return on investment, is preparing to convene an expert committee to deliberate on how to fine-tune the dispersal of the 10-year, ¥20 trillion in GX public finance. It will be instructive to examine how many of these experts share METI’s broad-portfolio decarbonization view of the world.

Levels of scrutiny

The current ministerial proposals for GX spending not only have to make it through the scrutiny of MoF assessments. A host of academics and environmental activist organizations are already deriding most of the non-renewable energy items as wasteful and likely to prolong Japan’s reliance on fossil fuels.

They argue that the bulk of spending should be devoted to energy from solar and wind, to maximize GHG reductions and help Japanese firms compete in an evolving world of green premiums and carbon border adjustments.

But these critics of spending on next-generation nuclear, hydrogen, ammonia, carbon-capture and other innovation overlook several discomfiting realities. For one thing, Japan increasingly confronts political and other constraints on its capacity to further expand its sizable solar domestic deployment, let alone ramp up wind, hydro, geothermal and other conventional renewables.

Moreover, Japan is hobbled by the high cost of conventional renewable energy in the context of serious fiscal constraints. These include the incredible scale of Japan’s public debt plus the burgeoning burdens from social security, national defense, and the risk of higher interest payments.

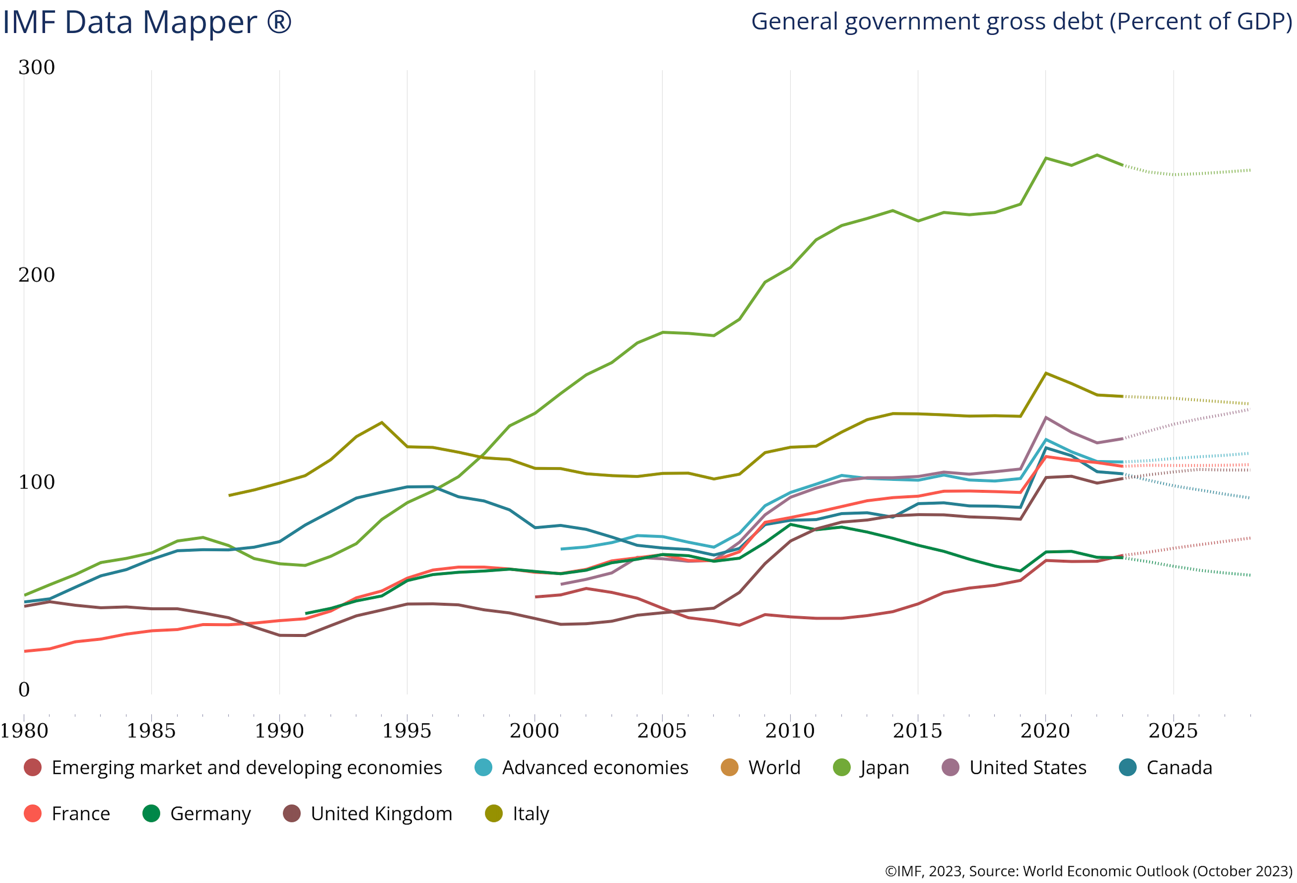

As we see in figure 1, Japan’s government debt of about ¥1270 trillion represents a debt/ GDP ratio of about 250%, well more than double even Italy. Three decades ago, Japan was a paragon of fiscal probity. But after Japan’s 1980s bubble economy collapsed, the state stepped in to goose private-sector investment via public works and tax cuts.

Source: IMF

That profligate approach was recognized as a failure in the early 2000s. Even so, the continuing expansion of the debt suggests that the tax increases and spending cuts required to regain fiscal discipline are politically difficult.

COVID and other crises intervened to blow away carefully constructed pathways to fiscal rectitude. Hence, 2023 saw the government’s debt finance exceed ¥35.6 trillion, accounting for 31.1% of revenues.

Moreover, Japan has to confront the double whammy of more costly social and national security. Social security spending for FY2023 is just under ¥37 trillion (32.3% of the national budget), rising at increments of about ¥500 billion per year. And national defense spending is to be doubled from the traditional 1% of GDP (roughly ¥5 trillion), through a cumulative ¥43 trillion hike over the five years from FY2023 to FY2027. Defense spending in FY2023 has already increased 26.3% from FY2022, to ¥6.83 trillion.

Spreading bets wisely?

In light of the above realities, Japan’s emphasis on a great diversity of GX projects perhaps makes sense. Japanese policymakers evidently seek to spread their GX bets across several decarbonization pathways. This approach may be more prudent than gambling that Japan can not only cut the high cost of domestic renewable energy, but also use renewables to supply both a major portion of electricity demand in addition to fueling industrial and other processes.

It is also clear that Japanese authorities want to foster GX approaches that dovetail with the needs of their Asian counterparts, seeing CCUS as one common focus area.

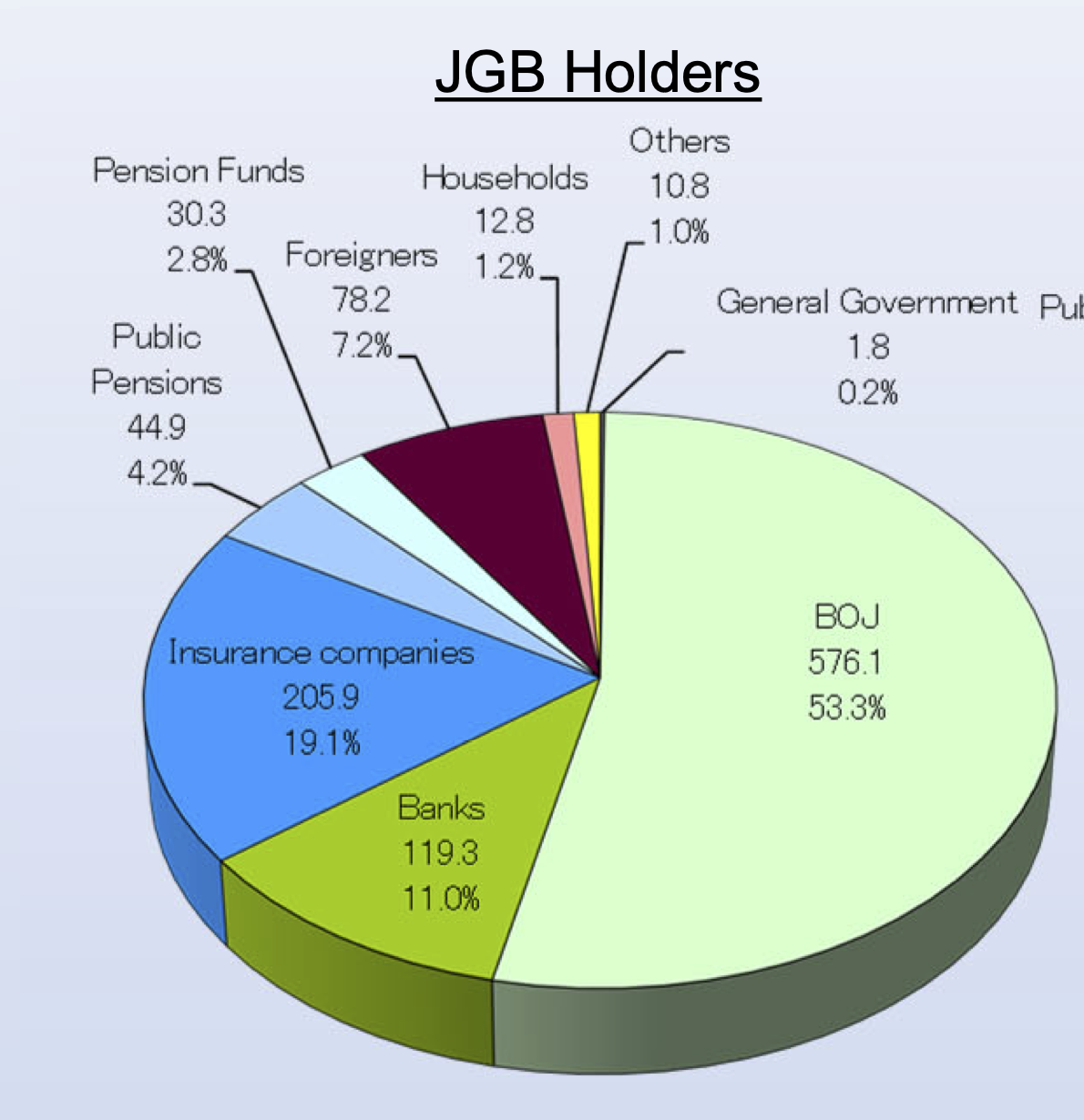

Japan’s desire to maximize returns from what it can invest seems understandable. The main reason Japan’s fiscal regime hasn’t collapsed is – as we see in figure 2 – that the BoJ holds an astounding 53.3% of Japanese government bonds versus the mere 7.2% held by foreigners. Among G7 countries, only Italy’s credit rating is worse than Japan’s, whose capacity to stick to ultra-low interest rates relies on a small foreign presence in the inner sanctum of the bond markets.

In any other country, pressure from bond investors would have driven up rates and caused debt repayment (service on the national debt) to rise well beyond the fiscal 2023 budget’s ¥25.3 trillion (22.1% of the budget). And over the past few years, the role of foreign interests in JGB trading and other functions has increased, gradually adding pressure on the fiscal system.

Of course, the GX spending is supposed to be financed – in the future – by levies on hydrocarbon fuels and other mechanisms for pricing carbon. But these initiatives are only nascent. It remains unclear whether they will become a credible and consistent source of revenues for GX bond repayment or whether the GX debt will simply be added to the gargantuan pile to be paid down through some combination of inflation and tax increases.

Source: MOF

Hence in the present, Japan’s multiple avenues for investment GX disbursements probably make sense as a means of diversifying risks and maximizing opportunities in a precarious political economy.

ANALYSIS

BY JAPAN NRG TEAM

Modernizing Japan’s Grid: Sharing Power Data as the First Step

For the energy transition to succeed in Japan, the national grid will have to undergo significant reforms and modernization in order to increase efficiency, enhance energy security and reduce environmental impact. Now, the nation’s main power transmission firms have taken a first step in that direction.

A new entity has emerged to act as a central repository for all electricity transmission and distribution data in Japan. As well as opening the door to new business opportunities, it will help to ensure that the nation’s regions are better-connected through a reliable and secure transmission network. The consolidation of data should also boost resilience.

More than any other of its G7 allies, Japan is prone to natural disasters, such as earthquakes and typhoons, which can disrupt power supply. A reformed grid can incorporate advanced technologies to enhance flexibility of power delivery thus minimizing downtime during disasters. Also, it will enable consumers to have more control over their energy usage through smart grids.

While these issues are by no means unique to Japan, the country faces a number of exceptional challenges, the most prominent being the fact that its power transmission system is bifurcated, each half runs at a different frequency. For the country to embrace and support an increased reliance on variable renewable energy, distributed systems, batteries and EVs, among other features, it needs to create a next-generation grid that speaks the same language. It is hoped the central data entity will enable just that.

Background history on power industry liberalization

From 1939 to 1951, the country’s utilities were integrated into a single unit known as Japan Power Generation and Transmission. The U.S. occupational government broke it into nine EPCOs, (later on, 10, when Okinawa Electric was added), which subsequently dominated all aspects of the country’s power supply for more than 60 years.

Led by Tokyo Electric (TEPCO), Kansai Electric and Chubu Electric, the EPCOs developed individual power technologies cooperating with the likes of Toshiba, Hitachi, Mitsubishi Heavy Industries, Mitsubishi Electric, Fuji Electric or Meidensha. EPCO engineers competed amongst each other to develop somewhat different and better technologies.

While TEPCO preferentially ordered power equipment from Toshiba and Hitachi, Kansai Electric cooperated with Mitsubishi Heavy Industries and Mitsubishi Electric. Therefore, the equipment development between suppliers was an extension of the bitter rivalry between TEPCO and Kansai – to have the most effective and efficient power capacity.

This competition helped suppliers to develop highly advanced equipment, which, due to its quality, eventually became in demand across the globe. However, these achievements became a negative for Japan’s power system once the power industry was deregulated, the EPCOs unbundled, and the market opened to new players.

In March 2000, the power market began to be liberalized with retail sales of extra high voltage contracts. Additional deregulation came in April 2004 and then in April 2005 for high voltage contracts. In April 2016, the full liberalization of power retailing began, which culminated in April 2020 when the transmission and distribution (T&D) business of each EPCO was officially broken off from the electricity generation entities in order to secure the neutrality of the grid.

While the generation and retail sectors saw a massive inflow of new players ready to add competition, the market approach could not be replicated in the T&D space. For new entrants to succeed there, they’d need to build an entirely new set of power lines, substations, etc. and the huge investment is unlikely to pay off.

What’s more, a centralized national power grid is more effective to operate than a fragmented one. Therefore, while METI pushed for greater competition in power production and retail, the ministry has gone the other way in the T&D space, seeking to unify the infrastructure and operations across the regions (apart from Okinawa).

Grid consolidation needed to form the All-Japan Power Transmission System

By the end of the 2020s, METI wants to integrate the power grid control system functions of all transmission companies, excluding Okinawa Electric. As a prerequisite for this, all the regional T&D companies are required to unify their power grid control systems. Reliable, real-time data will be key.

For the first step in implementing the consolidation, on August 31, the nine major regional T&D companies jointly established a new entity to integrate the specifications of all grid control systems. This will allow the sharing of data collected from smart meters, including personal data such as power consumption, and anonymous metadata about consumers in each region.

This new company, Transmission and Distribution IT & OT Systems, will play a key role in unifying the power grid control systems. Its Electricity Data Aggregation System utilizes info from smart meters installed in homes, businesses, etc., while ensuring privacy and security. Also, the next-generation intermediate distribution system will allow all transmission firms in each area (excluding Okinawa) to share the central dispatch system that they’ve developed individually.

Last month, TEPCO became the first Japanese company to supply the new entity with monthly and daily data. The other companies will start to do so within FY2024. Real time data will be collected after the first half of 2025.

The operation of the new entity will be led by the Transmission & Distribution Grid Council (TDGC), which is made up of members from the nine major T&D companies.

Market impact

By unifying all of the nation’s balancing systems, each regional power system can secure higher power system resilience, as well as procure the cheapest balance power from a much wider area, compared with the current system in operation.

The integrated power grid system can also forecast the balancing power needed at times when excessive volumes of renewable energy are generated and there’s a need for curtailment; or when the local power grid is overloaded.

Moreover, the new national system will strengthen grid resilience by “duplicating” the power system; that means, it will build and operate two circuits in case an accident knocks one of them offline for some reason. This will reduce the risk of a ‘perfect storm’ type of situation where multiple disasters and setbacks hit simultaneously and there’s the threat of a blackout.

On the business side, the value of pooling real-time power usage data in one place could be immense. As of October 2023, the government has dropped restrictions on the use of data by non-electricity companies, and according to Nikkei, over 20 companies including Daiwa House Industry and Toshiba are already eager to introduce services based on this data.

Some Japanese startups see the data as a gateway to installing more residential rooftop solar and battery units and persuading people to buy energy management systems, which promise to improve energy efficiency and cut their power bills.

While certain fees and user permissions may be required, access to nationwide electricity usage data – rather than data sets that only cover a particular region – will create valuable business opportunities. In terms of smart meters alone, Japan has more installed (80 million units) than the U.S. or European countries.

Some of the proposed services could potentially even save lives. Chubu Electric and trading house Mitsubishi are said to be considering a real-time power monitoring service that would aim to detect abnormalities in the routines of the elderly living alone. In a country facing a demographic crisis, that’s an energy-data business that could earn even more than the sale of electricity.

GLOBAL VIEW

BY JOHN VAROLI

Below are some of last week’s most important international energy developments monitored by the Japan NRG team because of their potential to impact energy supply and demand, as well as prices. We see the following as relevant to Japanese and international energy investors.

Australia/ LNG

Chevron Australia and workers at its two LNG plants reached an agreement, ending an impasse that led to threaten renewed strikes. The Gorgon and Wheatstone projects in Western Australia supply around 6% of the world’s LNG.

CRMs

Prices for key EV battery materials have fallen sharply this year – lithium is down almost 70%; nickel down 40%; and cobalt faces a glut with prices almost at record lows. Much of the decline is due to slower growth for EV demand in China.

EU/ Electricity market

Germany agreed to allow France to use state subsidies for nuclear power plants, and thus unblock a long-stalled reform of the EU electricity market. Germany has worried that French subsidies for nuclear plants would give French industry an advantage with lower energy prices.

India/ Coal power

Coal inventories at power plants in the first half of October fell 12.6%, with electricity demand boosting imports as fuel use outpaced supply. Very dry weather and a rise in economic activity has boosted consumption; but there’s also been a seasonal decline in generation from renewable sources such as wind and solar.

Netherlands/ CCS

Construction of Europe’s largest carbon capture and storage facility begins in the Rotterdam port area. The €1.3 billion “Porthos” project will be operational by 2026. CO2 emitted by refineries and chemical plants will be transported to empty gas fields under the North Sea, 20 km off the Dutch coast.

Qatar and Netherlands/LNG

Shell will buy up to 3.5 mtpa of LNG from Qatar for the Netherlands, as per two 27-year purchase agreements. Starting in 2026, QatarEnergy will supply LNG sourced from its North Field East and North Field South projects. Shell has stakes in both.

Scotland/Offshore wind

The govt will invest up to £500 million in the next five years in the offshore wind supply chain. The funding would act as a catalyst for private investment in Scottish ports and harbors, encouraging domestic companies to seek opportunities.

South Africa/Energy transition

The country plans to raise $60 billion over the next five years to switch to green energy. South Africa will set the terms and time frame of its energy transition, said deputy president Paul Mashatile, adding that “We recognize the need to reduce carbon emissions, but we’re also committed to economic development.”

Uganda/Oil pipeline

A $4 billion crude oil pipeline to link Uganda and Tanzania has settled a disagreement with Chinese investors. The 1,443 km pipeline should start in 2025, with a capacity of 246,000 barrels daily at peak. TotalEnergies has a 62% stake. Tanzania Petroleum Development Corp and Uganda National Oil each have a 15% interest, while the rest is owned by CNOOC.

U.S./Oil

Fundraising across equity markets rose this year, particularly among independent oil exploration and production groups and oilfield services companies. Senior bankers said they expect this trend to persist as the oil price will remain high.

Venezuela/Oil exports

In an effort to ease global oil prices, the U.S. issued a six-month license authorizing sales in Venezuela’s energy sector after a deal was reached between the govt and the political opposition regarding the 2024 elections.

2023 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

ASEAN-Japan summit to mark 50 years of cooperation

Last market trading day (December 30)

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.