JAPAN NRG WEEKLY

OCT 30, 2023

JAPAN NRG WEEKLY

Oct 30, 2023

NEWS

TOP

- JAEA nuclear fusion project generates super-hot plasma, milestone for clean energy effort

- Japanese and Danish PMs met in Tokyo to promote floating offshore wind power, establish global standards

- MoE subsidies to push power-hungry data centers toward increased renewable energy use

- Subsidies to mitigate energy hikes will be reduced in May 2024

- Energy sector seeks to move away from Chinese supplies

- METI 2050 hydrogen outlook too conservative: H2 Association

- Mitsubishi Power delivers equipment for green hydrogen project

- Itochu, Orascom to develop ammonia bunkering in Suez Canal

- Isuzu, Toyota collaborate on hydrogen-powered truck

- Mitsubishi Motors invests €200 million in Renault’s EV subsidiary

- Idemitsu, FOMM ink MoU to study EV collaborations

- SoftBank to build data center with Japan’s largest power demand

- Mitsubishi Corp proposes changes in offshore wind auctions, FIP

- Kobe Steel plans ammonia co-firing at captive power stations

- IHI, GE explore ammonia combustion compatibility in Singapore

- Kyushu Electric invests in JERA assets, expanding LNG, RE ties

- Aomori governor: scale down the 150 MW Noushi wind farm

- Nikkei: 90 solar panel incidents in 8 years due to stronger winds

- TEPCO completes second discharge of Fukushima treated water

- Mitsui, Mitsubishi and others extend stakes in Oman LNG

- JERA returns to profit, says it secured enough LNG for winter

- Japan’s reliance on Middle East oil imports slightly declines

- Opinion: Japan, South Korea and India should cooperate on oil

ANALYSIS

IRIDIUM’S CHALLENGE

IN THE AGE OF GREEN HYDROGEN

Negotiations on Japan’s FY2024 budget are underway, with the Ministry of Finance squaring off against METI, the MoE, and others. The need to invest big in clean energy is substantial. The amount of funds, and for which pathways, will determine where Japan sits mid-way through a decade during which it vowed to slash emissions by half. This budget will be the biggest yet and will struggle to satisfy all parties. Who are the likely winners?

JAPAN’S LONG ROAD

TO NUCLEAR WASTE DISPOSAL

The disposal of nuclear waste is a critical challenge for countries that rely heavily on nuclear energy. Japan, however, is struggling to convince municipalities to house the infrastructure for nuclear waste disposal. All hope rests with the two candidate spots in Hokkaido with more than a few challenges. Finding a way around the roadblocks, or another town to volunteer as a host, is now center stage in Japan’s nuclear industry.

GLOBAL VIEW

A wrap of top energy news from around the world.

EVENTS SCHEDULE

A selection of events to keep an eye on in 2023.

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group

Events

Editorial Team

Yuriy Humber (Editor-in-Chief)

John Varoli (Senior Editor, Americas)

Mayumi Watanabe (Japan)

Wilfried Goossens (Events, global)

Kyoko Fukuda (Japan)

Filippo Pedretti (Japan)

Tim Young (Japan)

Regular Contributors

Chisaki Watanabe (Japan)

Takehiro Masutomo (Japan)

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

OFTEN-USED ACRONYMS

| METI | The Ministry of Economy, Trade and Industry | mmbtu | Million British Thermal Units | |

| MoE | Ministry of Environment | mb/d | Million barrels per day | |

| ANRE | Agency for Natural Resources and Energy | mtoe | Million Tons of Oil Equivalent | |

| NEDO | New Energy and Industrial Technology Development Organization | kWh | Kilowatt hours (electricity generation volume) | |

| TEPCO | Tokyo Electric Power Company | FIT | Feed-in Tariff | |

| KEPCO | Kansai Electric Power Company | FIP | Feed-in Premium | |

| EPCO | Electric Power Company | SAF | Sustainable Aviation Fuel | |

| JCC | Japan Crude Cocktail | NPP | Nuclear power plant | |

| JKM | Japan Korea Market, the Platt’s LNG benchmark | JOGMEC | Japan Organization for Metals and Energy Security | |

| CCUS | Carbon Capture, Utilization and Storage | |||

| OCCTO | Organization for Cross-regional Coordination of Transmission Operators | |||

| NRA | Nuclear Regulation Authority | |||

| GX | Green Transformation |

NEWS: ENERGY TRANSITION & POLICY

JAEA nuclear fusion project generates super hot plasma, milestone for clean energy

(Nikkei Asia, Oct 25)

- Japan’s fusion power project at the JT-60SA research center has generated super hot plasma, marking a breakthrough. This means it generated a high-temperature cloud of ionized atoms, taking a step closer to the goal of creating an experimental fusion reactor.

- This program is run by the Naka Fusion Institute of the Japan Atomic Energy Agency (JAEA).

- JT-60SA in the city of Naka is one of the world’s largest plasma research facilities; it aims to harness fusion as a clean energy source using heavy hydrogen from seawater and generating less radioactive waste compared to fission reactors.

- CONTEXT: Fusion, the process that powers the sun, involves merging atomic nuclei to produce energy, unlike fission, which splits atoms. For 37 years Japan’s nuclear fusion program has centered around JT60 and its successor, JT60SA, (short for Japan Torus-60).

TAKEAWAY: In 2022, PM Kishida said nuclear fusion is part of his clean energy strategy, and he allowed startups in the field to claim state support. However, fusion energy projects remain highly experimental. At best, optimistic experts only expect it to be commercially viable by 2035. Meanwhile, more pessimistic experts doubt it will ever be commercially viable because, they say, the technological challenges are so great that the vast development and operational costs would make it unprofitable as a commercial energy source.

Japan, Danish PMs meet to promote floating offshore wind, establish global standards

(Nikkei, Oct 24)

- The Danish PM visited Tokyo to meet PM Kishida, and offshore wind was one of the main topics they discussed.

- Denmark and Japan plan to focus on floating offshore wind power generation, and want to come up with global standards for the sector.

- Experts from both countries’ industry and academia will work together to find ways to reduce development costs and electricity generation.

- Japan is attractive for Danish companies; it has shipbuilding technology needed for floating equipment, and it promises to be a major offshore wind market. Japanese companies with expertise in floating structures include Japan Marine United, Modec and Hitachi Zosen.

- CONTEXT: Denmark is a leader in offshore wind power, home to giants like wind turbine maker Vestas and Orsted, the world’s leading wind turbine operator. Floating offshore wind platforms will be located much further from shore than stationary offshore wind farms, allowing them to harness more powerful winds. Another advantage is that there will be much fewer potential conflicts with local communities.

TAKEAWAY: Floating offshore wind is still highly experimental and in its nascent stage. Globally, in 2020, its total installed capacity was a mere 17 MW. But about a dozen countries, such as Japan, are placing much hope in floating offshore wind as part of efforts to decarbonize their energy sector. Japan’s GX calls for 30-45 GW of offshore wind power capacity by 2040, with floating turbines seen as taking over the wind sector once it gets fully established in the 2030s.

Japan’s energy sector seeks to move away from Chinese supplies after detention

(Japan NRG, Oct 25)

- Battery and magnetic motor manufacturers will step up the shift away from Chinese supplies on the news of Beijing detaining a Japanese company employee in March, industry sources told Japan NRG.

- The detained employee is a Chinese national working for a nonferrous metal trading firm. He was believed to be dealing with rare metals.

- Japanese businesses are canceling trips to China, which may possibly lead to termination of contracts with Chinese suppliers.

TAKEAWAY: The detention was not an isolated incident. Earlier in October, China formally arrested a senior Japanese executive at pharma company Astellas after detaining him since March on espionage charges. The executive had spent a large part of his career in China and was on the brink of retirement. Earlier this year, China had revised its legislation to broaden the range of activities it considers to be espionage.

In the commodities business, the sharing of data is often part of the process of creating a market. Publishers of international energy price indices rely on market participants voluntarily disclosing details of their deals. Not many Japanese companies take part in the process, but those few who do might now recheck price publisher data management policies. Businesses are improving measures to protect employees as well as data. However, according to Japanese experts speaking at the recent Tokyo-Beijing Forum, there is now uncertainty about where Chinese legal lines lie.

Subsidies intended to mitigate energy price hikes will be reduced in May 2024

(Denki Shimbun, Oct 25)

- The govt’s draft for a comprehensive economic package stipulates that measures to alleviate the drastic hikes in electricity and gas prices will continue at their current level until late April 2024.

- These measures were set to expire in December. While they will now continue, the extent of such support will nevertheless be reduced starting in May 2024, but details are not yet known.

- Since September, measures to alleviate the drastic changes in electricity and gas prices have been subsidized at ¥3.5/ kWh for low voltage, and ¥1.8 for high voltage.

- For urban gas, the subsidy is ¥15/ cubic meter for households and companies with annual contract quantities of under 10 million cubic meters.

METI 2050 hydrogen outlook too conservative: Japan Hydrogen Association

(Japan NRG, Oct 25)

- METI’s 2050 hydrogen demand outlook of 20 million tons is far too conservative; the Japan Hydrogen Association sees a potential demand at 69.45 million tons, an association official told a hydrogen safety panel.

- Demand from the power sector alone will account for 16 million tons and from other industries around 35 million tons. It will all be in the form of green hydrogen.

Potential hydrogen demand breakdown (million tons)

| Sector | Hydrogen demand |

| Power | 15.75 |

| Transport | 16.01 |

| Industry (manufacturing) | 3.13 |

| Industry (heat source) | 31.58 |

| e-fuel | 2.98 |

Mitsubishi Power delivers equipment for U.S. green hydrogen project

(Company statement, Oct 26)

- Mitsubishi Power Americas made its first equipment delivery for the Hydaptive hydrogen production plant that’s part of the Advanced Clean Energy Storage Hub (ACES Delta Hub) in Utah.

- The ACES Delta Hub, a collaboration between Mitsubishi Power Americas and Chevron, aims to produce, store, and supply green hydrogen. Once operational, each day it will convert 220 MW of renewable energy into nearly 100 tons of green hydrogen, storing it in two vast salt caverns.

- A pipeline from the hub will supply hydrogen to the InterMountain Power Agency’s power plant, whose turbines will use up to 30% hydrogen blended with natural gas at start-up, with a goal of transitioning to 100% hydrogen by 2045 or sooner.

Itochu and Orascom to develop ammonia bunkering in Suez Canal

(Company statement, Oct 25)

- Itochu signed an MoU with Orascom Construction to develop ammonia bunkering in the Suez Canal. This is a step toward building a global ammonia supply chain and the development of ammonia-fueled ships.

- Itochu is also developing ammonia bunkering hubs in Singapore, Spain, various other European ports, the Panama Canal, and Japan.

- The company’s decarbonization strategy includes building ammonia-powered ships, and participating in green ammonia production.

Isuzu and Toyota collaborate on hydrogen-powered truck for green logistics

(Nikkei Asia, Oct 25)

- Isuzu Motors and Toyota will collaborate to mass-produce a hydrogen-powered fuel cell truck, with the goal of competing with electric trucks.

- The vehicle will combine Isuzu’s light truck body with Toyota’s fuel cell technology. Its production location is yet to be determined.

- FCVs offer longer ranges and cargo capacity compared to electric trucks.

- CONTEXT: The market for commercial FCVs is expected to grow as logistics companies aim to reduce their carbon footprint. Challenges include the cost of hydrogen and the need to expand the hydrogen filling station network.

Mitsubishi Motors invests €200 million in Renault’s EV subsidiary ahead of public listing

(Company statement, Oct 24)

- Mitsubishi Motors will invest €200 million in Ampere, an EV and automotive software company founded by Renault Group in late 2022.

- By the end of this year, Ampere plans to go public. The company has pledged to produce 1 million EVs annually by 2031.

- With this investment, Mitsubishi Motors aims to improve its EV development technology.

- CONTEXT: Renault seeks to become a “next-gen automotive company”. Mitsubishi Motors is a member of the Alliance with Renault and Nissan, and in 2009 it launched the i-MiEV –the world’s first mass-produced EV, followed by the Outlander PHEV – the world’s first plug-in hybrid electric SUV in 2013.

Idemitsu, FOMM ink MoU to study EV collaborations

(Company statement, Oct 26)

- Idemitsu Kosan and First One Mile Mobility (FOMM) inked an MoU on cooperation.

- This might include the launch of EV-related services at Idemitsu gasoline service stations, such as converting small engine vehicles to EVs by replacing engines with electric motors, battery replacement and maintenance services of FOMM EV models.

- CONTEXT: Founded in 2013 by a former Suzuki Motor engineer, FOMM is an emerging automotive maker focused on EVs. Its newest service will allow gasoline-powered car owners to convert their vehicles into electric ones by remodeling and installing a battery and motor.

TAKEAWAY: In 2021, Cosmo Energy signed a similar agreement with EV manufacturer ASF. While Idemitsu’s MoU with FOMM doesn’t include investments, the final agreement will reveal Idemitsu’s ultimate ambition in the EV space: Does it aim to evolve into an automotive manufacturer, or focus on batteries? The company has ties with Toyota Motor in solid battery production.

Recent service station related agreements

| Oil refineries | Partners | Projects |

| Idemitsu | FOMM | Engine-to-EV conversion services, maintenance of FOMM models, battery replacement. |

| Delta Electronics | New charging station | |

| ENEOS | NEC | Charger system management, payment systems |

| HW Electro | Maintenance and sale of commercial EVs | |

| Cosmo | ASF | Maintenance of ASF models at Cosmo service stations |

Source: Company statements

Cosmo Energy and Toyo Engineering to study production of methanol from CO2

(Company statement, Oct 23)

- Cosmo Energy and Toyo Engineering inked an agreement to study direct synthesis of CO2 into methanol using a catalyst, including its commercial feasibility.

- There is much interest in “g-methanol”, Toyo’s proprietary technology that directly synthesizes methanol from hydrogen and CO2 emissions at oil refineries.

- CONTEXT: CO2 can be used as a direct feedstock to produce methanol efficiently without going through multiple processes.

Cosmo Oil and MOL will develop CCS value chain

(Company statement, Oct 27)

- Cosmo Oil and Mitsui OSK Lines (MOL) signed an MoU to study ocean transport for development of the CCS value chain.

- The two companies will consider specifications of liquefied CO2 carriers for long distance, estimate ocean transport costs, and collaborate on potential carbon capture, utilization, separation, storage, transport, etc.

- CONTEXT: Japan has named seven CCS storage sites, two of which are located outside Japan. Transporting liquefied CO2 is costly and much more work needs to be done to make it commercially-viable.

Cosmo Energy and CRRA to study CCU

(Company statement, Oct 26)

- Cosmo Energy and the Carbon Recovering Research Agency (CRRA) will study carbon capture and utilization (CCU) by way of microalgae such as Spirulina.

- CRRA has been promoting bioethanol production using CO2 from direct air capture and the process to ferment microalgae in a CO2-absorbed alkaline solution.

Toyota Tsusho delivered biodiesel fuel to container liner in Fukuyama Port

(Company statement, Oct 24)

- In a trial, Toyota Tsusho is providing biodiesel fuel made from used cooking oil (UCO) to the container liner, Integrative Earth, at Fukuyama Port.

- The UCO is sourced within Toyota Group and Toyota Tsusho Group companies.

ENEOS and Toshiba collaborate on e-fuel production

(Company statement, Oct 25)

- ENEOS and Toshiba Energy Systems and Solutions plan to collaborate on synthetic fuel (e-fuel) production.

- ENEOS has developed a catalyst that produces liquid hydrocarbons from carbon monoxide (CO) and hydrogen. Toshiba ESS leads the world in carbon electrolysis to convert CO2 into CO. They will conduct joint tests.

Yanmar delivers first fuel cell system to shipping company

(Company statement, Oct 26)

- Yanmar delivered its first fuel cell system to Motena-Sea, a Mitsui OSK Lines company operating passenger ships. The system will be mounted on Hanaria, a hybrid “carbon neutral” vessel fueled by biodiesel and FC systems.

- The ship will carry two FC systems, each with a 240-kW output; and 99.97% purity hydrogen will be used.

Tokyo Gas to launch carbon recycling at customer sites

(Company statement, Oct 26)

- Tokyo Gas will launch the country’s first on-site carbon recycling service, capturing CO2 and converting it to potassium carbonate at customer sites.

- CarbinX, a compact carbon capture equipment developed by Canada’s CleanO2, will be the technology used to capture and convert CO2 into carbonate.

- The first target customers will be industrial plants that use potassium carbonates.

Asuene unveiled AI-based cloud service to help customers reduce emissions

(PR Times, Oct 24)

- Tokyo-based climate tech startup Asuene unveiled a new cloud-service, “Asuene AI”, that advises customers how to reduce their emissions by analyzing their individual consumption patterns.

- “Asuene AI” uses ChatGPT and generative AI.

MLIT and U.S. CalSTA co-host symposium on green shipping and port decarbonization

(Company statement, Oct 20)

- The Port Decarbonization and Green Shipping Corridor Symposium, co-hosted by MLIT and the California State Transportation Agency (CalSTA), brought together leaders from major seaports in California and Japan to discuss efforts to transition to zero-emission port operations and establish green shipping corridors.

- California showcased its commitment to reducing port-related pollution, with investments in zero-emission infrastructure, while Japan highlighted its leadership in hydrogen technologies and its initiative to decarbonize terminal operations.

NEWS: POWER MARKETS

MoE subsidies to push data centers toward increased renewable energy use

(Japan NRG, Oct 25)

- The MoE will expand subsidies to push data centers toward increased renewable energy consumption, said Kato Daisuke, deputy director of the Climate Change Projects Office, during Japan IT Week in Chiba.

- The subsidies began in FY2021, funding data centers that introduce on-site renewable energy systems. So far, about 25 projects have received subsidies. Kato aims to expand the plan to include battery installations, building-integrated solar systems and energy-efficient cooling systems starting in FY2025.

- CONTEXT: Data centers are purchasing green power and non-fossil fuel certificates but the MoE wants to change this. It forecasts the data center sector’s power consumption rising to 150 TWh in 2030, up from 16 GWh in 2017, and there may not be enough certificates.

TAKEAWAY: Data center power consumption is likely to exceed the MoE’s forecast. Covid-19 led to an increase in data traffic, especially with more video streaming. That traffic will only increase because video is going 3D with the rise of the metaverse and AI-driven “XR” (virtual, augmented and mixed reality) technologies.

- SIDE DEVELOPMENT:

Mibai City to expand carbon neutral data center

(Japan NRG, Oct 25)- Mibai City (Hokkaido) plans to expand its carbon-neutral data center that uses snow to cool servers. The data center was built in 2021 with 20 racks of servers consuming 3,000 tons of snow.

- One ton of snow cuts 10 liters of oil-equivalent energy consumption. Water from melted snow is transported to the data center through pipelines. The city is considering biogas and solar power as the data center’s main power sources.

- The extent of the expansion depends on the number of interested users.

- CONTEXT: New Chitose International Airport (Hokkaido) and Imperial Hotel (Tokyo) use snow-based systems to control building temperatures.

TAKEAWAY: Snow does not cost the data center anything, but the labor and fuel cost of collecting and transporting it has an impact, a city official told Japan NRG. Meanwhile, another data center operator said that customers seek resilience against earthquakes and floods, and that emissions are still a low priority.

Carbon neutral data centers

| Operator | Location | Power capacity | Energy types |

| Kyocera Communications | Ishikari City (Hokkaido) | 2 MW (400 racks) | Solar; plans wind and biomass |

| Agata | Tomioka City (Gunma) | 300 kW | Solar |

| Amazon | NA | NA | Offsite PPA |

Source: MoE

SoftBank to build data center with Japan’s largest power demand

(Nikkei, October 20)

- SoftBank seeks to build a large-scale data center in Hokkaido by FY2026. The company has applied for a subsidy from METI for half the construction costs, which are expected to be in the range of ¥40 to ¥60 billion.

- The volume of data is expected to grow rapidly with the spread of AI and other tech. There are concerns that clusters of data centers in Japan’s urban areas will increase power consumption, which is why companies seek decentralized data center projects.

- SoftBank estimates it will need 300 MW of power capacity for the Hokkaido center, which would make it Japan’s biggest power consumer in the sector. It also wants the electricity to come from renewable energy sources so that the data center is “green”.

- The site is planned for Tomakomai City.

TAKEAWAY: A report earlier this month estimated that the catchment area served by TEPCO also will require 7 GW of new power capacity over the next ten or so years to meet demand from new data centers. One of the biggest clusters for such new facilities is forming in the city of Inzai, Chiba Pref, which has a population of just over 100,000 but will require 2.5 GW of new capacity by 2035 to meet data center needs. That’s equivalent to building two and a half nuclear reactors. Softbank’s choice of location in Hokkaido should help to support new solar, wind and battery capacity in the region. But the site near Tomakomai will also need to compete for green energy with a new semiconductor hub that the govt plans to establish in nearby Chitose City.

Mitsubishi proposes changes in offshore wind auction and FIP systems

(Government statement, Oct 27)

- A unit of Japan’s biggest trading house, Mitsubishi Corporation, made offshore wind policy recommendations to the METI Power Tariff Committee, saying high costs are impacting projects overseas and Japan could find itself facing the same issues.

- The company suggested that future project auction price caps should reflect prevailing market conditions, and called for the introduction of a new mechanism in the Feed-in-Premium system that allows increased flexibility in setting the govt purchase rates for electricity from offshore wind farms.

- If auction cap prices are below the leveraged cost of electricity (LCOE), future offshore wind auctions may not draw any participants, the company warned.

TAKEAWAY: For years, governments around the world have scaled back the price offered at wind and solar auctions to benefit from over a decade of cost reductions in both sectors. But the last two years or so have seen a marked reversal in costs due to inflation, rising raw materials prices, and supply constraints. In Japan, the cost of wind power is up by almost a third in this time and the industry supply chains are still at an early stage of development. Mitsubishi is clearly trying to get the officials in Tokyo to notice the situation in Europe. Last month, the UK saw no bids entered in its latest round of offshore wind auctions last month after industry players felt the price cap proposed by the government was too low to allow for a profit.

There is another factor worth noting in this development. After Mitsubishi won all three of the major offshore wind projects in Round 1 of Japan’s auctions for the sector, intense lobbying by competitors led to a change of auction rules. One of the main actors in the lobbying was the Japan Wind Power Association (JWPA). Recently, Mitsubishi has left the JWPA. Should the govt accept Mitsubishi’s proposals, it may weaken the negotiating heft of the industry association.

Kobe Steel plans ammonia co-firing at four coal power stations

(Company statement, Oct 26)

- Kobe Steel plans 20% ammonia co-firing by 2030 at the Kobe Unit 1 and Unit 2 coal power stations, (each 700 MW capacity). At a later date, co-firing will start at Units 3 and 4, (each 650 MW capacity).

- By 2050, all four power stations will be running fully on ammonia.

- The company plans to set up a supply chain for ammonia, which will be imported.

- CONTEXT: Among the EPCOs, JERA, Kyushu Electric, Chugoku Electric, Shikoku Electric and Tohoku Electric plan to introduce coal-ammonia co-firing. Among non-EPCOs, Tokuyama and Tosoh will also use it.

TAKEAWAY: The two 700 MW units will consume 700,000 tons/ year of ammonia at 20% co-firing. JERA and Kyushu Electric plan 20% co-firing at 1 GW plants, consuming 1 million tons/ year of ammonia combined. If all coal plants in the country did 20% ammonia co-firing, Japan would need 27 million tons/ year. In 2022, the global ammonia market was 170 million tons in 2022, according to ChemAnalyst, which predicts that it will almost double in the next 10 years or so.

IHI and GE explore ammonia combustion compatibility in Singapore power generation

(Company statement, Oct 25)

- IHI Corporation (IHI) and GE Vernova’s Gas Power, in collaboration with Singapore’s Semcorp, signed an MoU to explore the modification of a Gas Turbine Combined Cycle (GTCC) power plant on Jurong Island, for ammonia combustion.

- This marks the first time that IHI and GE plan to implement their jointly developed technology for ammonia-exclusive combustion in an actual power plant.

- In 2022, IHI and Semcorp inked an agreement on green ammonia that covers the development of infrastructure from ammonia production to utilization. The companies are considering whether to use green ammonia at this power plant.

- By 2030, IHI and GE plan to develop ammonia-exclusive combustion technology for large-scale gas turbines. While hydrogen is an option for introducing decarbonized fuels into gas turbines, both companies anticipate that ammonia will be more cost-effective for maritime transportation and direct combustion.

TEPCO completes second discharge of Fukushima treated water, plans for third discharge

(Company statement, Oct 24)

- On Oct 23, TEPCO announced completion of its second ocean discharge of treated water from the Advanced Liquid Processing System (ALPS) at the Fukushima Daiichi Nuclear Power Plant.

- A total of 7,810 cubic meters of water was discharged from one of the three tank systems over about 17 days. Following this, inspections and verification work on the equipment and operations will be done.

- Preparations for the third discharge already began.

- CONTEXT: On Oct 19, TEPCO released test results of radioactive isotope concentrations in samples taken from the tanks in July. In FY2023, TEPCO plans to discharge into the ocean a total of 31,200 cubic meters of treated water. The total tritium discharge is expected to be about 5 trillion becquerels, well below the acceptable level of 22 trillion becquerels.

- SIDE DEVELOPMENT:

IAEA says water release has no technical concerns, proceeding as planned

(Agency statement, Oct 27)- The discharge of treated water from the Fukushima Daiichi NPP is “progressing as planned and without any technical concerns,” the Task Force set up by the IAEA confirmed after a two-month review into the safety standards.

- The agency and its experts from around the world will continue to monitor the marine environment, equipment and approach of TEPCO as it carries out the release.

JERA and Kyushu Electric expand collaboration on renewables and thermal power

(Denki Shimbun, Oct 24)

- JERA and Kyushu Electric inked an MoU to develop new power capacity, including renewable energy and thermal power. Kyushu Electric will acquire from JERA a 6.67% stake in the revamped Goi Thermal Power Plant (Chiba Pref, LNG, 780 MW x 3 units) that’s jointly owned by JERA and ENEOS.

- Kyushu Electric will sell LNG to the Goi plant, facilitating optimal LNG consumption. A company official said the goal with the Goi investment is to secure a stable sales outlet for LNG already procured by the company.

- The Goi plant is under reconstruction to replace all three gas-fired units with combined cycled LNG-firing capacity, which will start operations by March 2025.

- JERA and Kyushu Electric are also considering collaboration with Chugoku Electric, Shikoku Electric, Tohoku Electric Power, Hokuriku Electric, and Hokkaido Electric in jointly procuring ammonia and hydrogen fuel.

- CONTEXT: JERA and Kyushu Electric already collaborate on LNG trading. Moreover, in 2022, they signed a similar MoU about the development and expansion of supply chains for hydrogen and ammonia for use as power generation fuels.

Kagoshima assembly nixed referendum on Sendai NPP operation extension

(Nikkei, Oct 26)

- The Kagoshima Prefectural Assembly rejected a proposed ordinance for a referendum concerning the extension of operations at the Sendai Nuclear Power Plant (NPP). The majority, including the faction from the Liberal Democratic Party, opposed the proposal, ensuring that the referendum wouldn’t take place.

- This call for a referendum was spearheaded by civic groups, who have criticized the decision to extend the plant’s operations. Governor Koichi Shiota expressed reservations about the referendum, stating that decisions regarding nuclear energy should fall under the jurisdiction of the national government.

- The Sendai NPP units will reach their 40-year operational limit in 2024 and 2025.

Aomori governor hints at need to scale down the 150 MW Noushi wind farm

(Government statement, Oct 24)

- The Aomori Pref governor asked Cosmo Eco Power to consider scaling down the 150 MW Noushi wind farm in order to mitigate the environmental impact.

- The governor asked for data on the cumulative impact from other nearby wind farms.

- Possible impact on nearby forests and wetlands needs to be taken note of.

- CONTEXT: The governor made his comments following public consultations on Cosmo Eco Power’s proposed environment impact assessment methodology.

Nikkei investigation: Nearly 90 solar panel incidents in 8 years due to stronger winds

(Nikkei, Oct 23)

- CONTEXT: This data comes from a freedom of information request by the Nikkei, Japan’s biggest business daily newspaper, to METI’s regional offices, and also from interviews / surveys carried out by the paper.

- From 2015 to 2022, about 90 accidents nationwide were caused by or involved solar panels, according to Nikkei’s research, but less than 10% of all incidents are reported.

- The probe focused on damage caused to panels from strong winds that scatter and sometimes even shatter the equipment. The reason for the incidents is said to be the fact that solar farms are exempted from the Building Standards Act, which was done to accelerate the rollout of renewables. The survey found cases of poor foundations for the panels and water drainage issues.

- Until 2020, operators of facilities with a 50 kW capacity or less had no obligation to report accidents. Even after the regulation was revised in 2021, there is no report requirement for installations under 10 kW.

- As a result, big insurers like Tokio Marine & Nichido Fire have started to vary their premiums based on risk assessments of solar facilities by third-party organizations.

Kyuden takes 40% stake in U.S. renewables developer Enfinity Global

(Company statement, Oct 26)

- Kyuden International, part of the Kyushu Electric Group (KG), will acquire a 40% stake in renewables developer Enfinity Global, which has 28 solar power generation facilities in California, Idaho, and North Carolina with combined capacity of 400 MW.

- Enfinity Global will retain the 60% stake. This acquisition is KG’s first in the U.S. renewables sector.

- KG’s overseas power generation capacity is now around 3 GW.

Hokkaido Bank and Bansyo Ito-gumi plan a 250 kW biogas power station

(New Energy Business, Oct 23)

- Hokkaido Bank will provide ¥730 million to Bansyo Ito-gumi to build a 250-kW biogas power station via its “Hoku-Hoku Sustainable Finance” at Nakashibetsu town in Hokkaido Pref.

- The plant collects livestock manure from farms, and uses biogas through methanation as fuel to generate power. The electricity will be sold via Feed-in-Tariff (FIT). The plant expects to start operation in April 2024.

Cosmo Oil to help Kawasaki City source a quarter of its power from renewables

(Company statement, Oct 25)

- Starting Nov 1, Cosmo Oil Marketing will supply 100% renewable electricity with non-fossil certificates to 207 schools and public buildings in Kawasaki City.

- This means that 54 MWh of electricity during the course of the year will be sourced from renewables, or a quarter of total city electricity consumption.

NEWS: OIL, GAS & MINING

Mitsui, Mitsubishi and others extend stakes in Oman LNG project

(Company statement, Oct 24)

- Shareholders in the Oman LNG project – among which are Mitsui & Co, Mitsubishi Cop, Itochu, as well as TotalEnergies and Shell Gas – signed an amended shareholders’ agreement extending the business beyond 2024.

- Local partners are Oman LNG (OLNG) and Qalhat LNG (QLNG).

- Mitsui holds a 2.77% stake in OLNG, which has an annual production capacity of 7.6 mmt, while QLNG produces 3.8 mmt.

- Oman has pledged to supply natural gas to OLNG until 2034.

JERA returns to profit, says it secured enough LNG for the winter

(Reuters, Oct 27)

- JERA reported a net profit of ¥291 billion for the first half of FY2023, a big improvement from a ¥214 billion loss the previous year. This was due to reduced fuel costs, higher electricity rates, and profits from overseas ventures like the Formosa 2 wind power project.

- JERA expects a full-year profit of ¥350 billion, with savings from resumed LNG imports from the Freeport LNG plant in Texas. However, earnings from its trading unit, JERAGM, will decrease as last year’s energy crisis subsided.

- Concerning conflict in the Middle East, JERA’s Yoshida Tetsuo said the company is closely monitoring the market and that JERA has enough LNG for the winter. Meanwhile, Chubu Electric, JERA’s parent company, reported a net profit of ¥311.5 billion for the same period and raised its full-year net profit forecast to ¥330 billion.

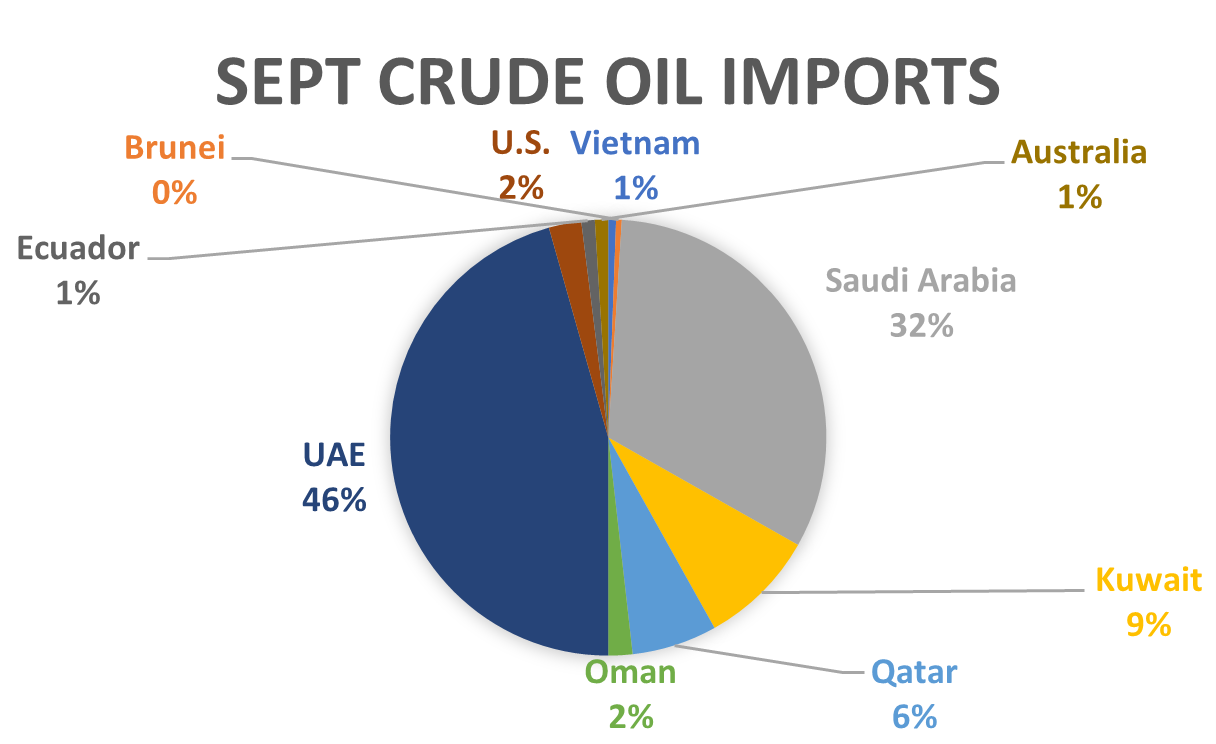

Nearly 95% of Japan’s oil imports sourced from Middle East; Sept total down 16.7%

(Japan NRG, Oct 27)

- Japan imported 10.6 million kiloliters (73.3 million barrels) of crude oil from Middle Eastern countries in Sept, accounting for 94.6% of the total.

- The largest exporter was the UAE, supplying 5.1 million kiloliters, followed by Saudi Arabia at 3.6 million kiloliters.

- Middle East dependence was lower in September. From January to September, crude oil from the region accounted for 95.8% of Japan’s total imported oil.

- Japan’s total oil imports were 11.2 billion kiloliters in September, down 16.7% YoY.

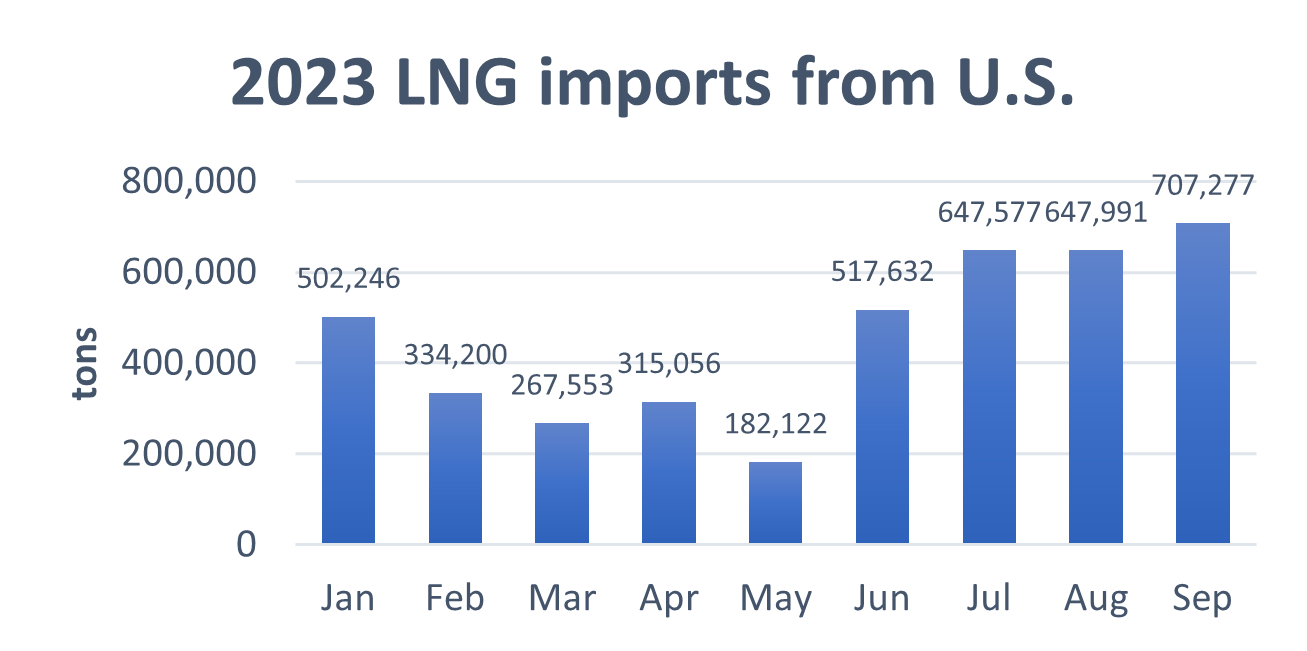

September LNG imports from U.S. at a monthly high; total LNG imports up 3.8%

(Japan NRG, Oct 27)

- In September, Japan imported 0.7 million tons of LNG from the U.S., the highest monthly amount this year. The U.S. had a 12.8% import share, third place after Australia and Malaysia.

- The U.S. exported a total of 4.1 million tons from January to September, up 25% YoY.

- Japan’s total LNG imports were 5.5 million tons, up 3.8% YoY.

LNG weekly stocks rise to 2.23 mln tons, up 3.7%

(Government data, Oct 25)

- LNG stocks of 10 power utilities stood at 2.23 million tons as of Oct 22, up 3.7% from 2.15 million tons a week earlier. METI initially reported the Oct 15 stocks as 2.16 million tons but revised the figure.

- The end-October stocks last year were 2.53 million tons. The five-year average for this time of year was 2.01 million tons.

Opinion: Japan, South Korea and India should collaborate on energy security

(Nikkei Asia, Oct 23)

- CONTEXT: This is an opinion piece by Kabir Taneja, a research fellow at Observer Research Foundation’s strategic studies program in New Delhi.

- The author emphasized the heavy reliance of Asian economies on Middle Eastern energy imports, particularly crude oil.

- The author suggests that India, Japan, and South Korea collaborate on improving Middle East maritime security. These countries have already conducted joint exercises and are part of regional naval partnerships.

ANALYSIS

BY MAYUMI WATANABE

Iridium’s Challenge in the Age of Green Hydrogen

In June, Japan’s hydrogen strategy took a decisive green turn when METI rewrote the 2017 Basic Hydrogen Strategy in order to reflect the International Partnership for Hydrogen and Fuel Cells that seeks to reduce hydrogen’s carbon footprint. METI’s previous stance was that hydrogen of any color was useful in cutting emissions, but now, it leans towards green hydrogen as the optimal solution.

The revised Basic Hydrogen Strategy also introduced a new target for green hydrogen production: 15 GW of renewable-driven electrolyzer capacity by 2030. This is a major leap from the present 14 MW. However, the 15 GW goal brings significant challenges.

One of the most widespread electrolysis technologies globally is proton electrolysis membrane (PEM), but one crucial item in this process is provided by the precious metal iridium. Cost is not even the main issue. The most serious problem is iridium’s severe scarcity amid rapidly growing global demand. In order to satisfy its appetite for PEM systems, Japan alone will need one third of the current total global mined iridium production.

Another problem is the significant carbon footprint of iridium mining, an inconvenient fact that many would prefer to sweep under the rug. It’s estimated that there’s 3,289 tons CO2-equivalent emissions for one ton production of platinum group metals, which includes iridium. Finding solutions to iridium supply and emissions will be fundamental challenges in the growth of green hydrogen in Japan and globally.

Hydrogen investment boom

“Hey, are you investing in hydrogen? The government is giving away money.” These words can now be heard often since the Green Transformation (GX) Act was passed in May, allowing the government to issue ¥20 trillion GX bonds to finance the energy transition, as well as to raise ¥150 trillion more through public and private efforts.

The immediate goal is to fund 15 GW in electrolysis capacity building by issuing GX bonds. This capacity will produce 300,000 tons/ year of hydrogen from renewable energy and water. That is 10% of METI’s goal for 3 million tons of hydrogen supply by 2030. ANRE began internal discussions on funding criteria, which will be finalized by year’s end.

In Japan, the hydrogen production process using water electrolysis has been utilized by the semiconductor industry for two decades or so. There are two technologies: the proton exchange membrane (PEM), also known as polymer electrolyte membrane, and alkaline water electrolysis (AWE).

In PEM systems, water particles pass through the membrane and separate into hydrogen and oxygen after electricity is applied. Iridium is used on the cathode and platinum on the anode. In AWE, sodium hydroxide or potassium hydroxide solution is used. The solution separates into hydrogen and oxygen after electricity is applied. Steel is used as cathode and anode. PEM’s use of precious metals makes it expensive, but it’s capable of accommodating volatile changes in the electricity volume. AWE is cheaper to build but there are questions on how well it copes with sudden changes in output from variable renewable power sources, and if sodium or potassium solution-based systems could be managed easily.

Presently, AWE accounts for two thirds of Japan’s electrolysis capacity owing to a single 10 MW capacity in Fukushima, which is the oldest green hydrogen system operational since 2020. All other recent projects have PEM systems.

Electrolysis capacities in operation

| Project name | Electrolyzer capacity | Electrolyzer maker | Technology

| Energy |

| Fukushima FH2R | 10 MW | Toshiba Energy Systems, Asahi Kasei | AWE | Solar |

| Yamanashi H2-YES | 2.3 MW | Hitachi Zosen, Toray | PEM | Solar |

| Ohbayashi Oita geothermal plant | 0.05 MW | NA | PEM | Geothermal |

| Ishikari City Atsuta Microgrid | 0.005 MW | Takasago Thermal Engineering | PEM | Solar |

| Hokkaido Electric Tomato Atsuma | 1 MW | Hitachi Zosen | PEM | Solar, wind |

Source: Companies information, Japan NRG

In the national hydrogen strategy, METI has positioned PEM and AWE as the main technologies, setting 2030 cost targets: ¥65,000/ kW for PEM; and ¥52,000/ kW for AWE. Japan NRG estimates the present cost to be around ¥500,000-550,000/ kW, based on the amount of the government subsidy given to Hokkaido Electric for its 1 MW electrolyzer.

There are different views on which technology will capture a greater share by 2030. The equipment manufacturers are expanding both PEM and AWE systems, assuming each will have almost equal shares, but with 5-10% also going to novel technologies through the end of the decade.

Supposing that PEM accounts for 40% of the 15 GW capacity to be added – Japan will need to secure as much as 4.2 tons of iridium, over one third of the total globally-mined production, which is between 7 to 8 tons annually. Japan’s electrolysis capacity is seen to account for 10% of the global total.

Japan’s iridium demand in 2030

Data varies on how much iridium a PEM system requires. The World Platinum Investment Council says 400 kg of iridium is required for 1 GW of electrolysis power. Some experts said the iridium requirement could be as much as 700 kg/ GW. Also, iridium electrodes do not last forever, and might end their life cycle after 10 years and need to be replaced.

Based on the conservative estimate of 400 kg consumption for 1 GW, and applying the present market rate of ¥22,900/ gram, the iridium materials cost for 1 kW comes to ¥9,160. This is already 14% of the 2030 target cost of ¥65,000/ kW. The PEM system will also require 0.3 grams of platinum per kW, which comes to ¥1,304.

Iridium is a platinum group metal (PGM), the crude ore of which typically contains roughly 80% palladium and platinum. Iridium’s ratio might be only 1%. South African mining companies Anglo American, Impala, Sibange Stillwater, and Northam account for over 80% of global iridium production.

Iridium suppliers in PEM alliances

| Mines | Intermediate players | End-users, others | Project detail |

| Impala Platinum | — | South African government, academia | R&D of green hydrogen applications |

| Sibanye- Stillwater | Heraeus Precious Metals | — | R&D on cutting iridium catalyst consumption |

| — | Heraeus.

BASF | — | JV in China to recover iridium and other metals from scrapped cars |

| BASF | ZeroAvia | R&D of PEM for aviation | |

| — | Furuya Metal | Toshiba | Building iridium supply chain |

Source: Company press releases

To build reliable supply chains companies are joining forces. In October, Toshiba Energy Systems and Solutions and Furuya Metal, a PGM trader and recycler, inked a MoU to build an iridium supply chain. Furuya Metal is a Mitsubishi group company with a top global share of ruthenium in terms of trading volume. It also runs a recycling plant in Japan and is one of the few companies capable of recovering iridium from industrial scrap.

Furuya can increase Toshiba’s supplies by improving the recovery rate of iridium from wastes in the PEM system production. For its part, Toshiba claims to have developed sputtering technologies that reduce iridium consumption by one tenth.

Recycling kills two birds with one stone

According to Heraerus, only 20-30% of end-of-life products that contain iridium are recycled. However, if the recovery rate is raised to 80% then global supply can increase by four tons or more.

Iridium recycling is very challenging technologically since only a few grams are used in any one item and the process isn’t easy to scale. In Japan, studies reveal that spark plugs with iridium are sold as ferrous scrap for less than ¥200/ kg since recyclers can’t tell which plugs contain the precious metal.

Recycling also resolves iridium’s other problem: a high carbon footprint due to the fact that its crude ore is smelted in temperatures of 1,500°C, and the work area needs to be cooled. In 2022, Impala Platinum reported to the UK-based CDP, a climate monitoring body for investors, that its Scope 1 and 2 emissions were 354,367 tons for 107.74 tons of PGM production, which comes to 3,289 tons CO2-e per ton of production.

In comparison, hard-to-abate steel scored 1.41 tons CO2-e/ ton of steel, according to the IEA. Heat treatment of recovered iridium occurs at lower temperatures of 1,000°C. Canada’s iridium recycler, McCol Metal, estimates that recycling’s carbon footprint is one third of mining. But 1,000 tons of CO2-e per ton of iridium recycled is still high.

Scientists are exploring chemical processes at lower temperatures, for example the use of solid aqua regia (a mixture of nitric acid and hydrochloric acid) to separate iridium at 500 °C. Another challenge is building an efficient process where different end-of-life products could be treated at once. If successful, then recycling could resolve both iridium supply and carbon intensity problems.

Recycling technology breakthroughs will not happen overnight. On the other hand, cheaper electrolysis technology may emerge unexpectedly. Betting on a single solution would be risky and it is important to keep eyes on other approaches, such as the potential of other platinum group metals to act as iridium substitutes. Other options include reducing iridium consumption, exploring untapped deposits in South Africa, Canada and Australia, and reprocessing mine tailings that may still contain some elements of iridium.

Effective and cost-efficient solutions will have to be found. Otherwise, there won’t be much of a green hydrogen future in Japan, or elsewhere.

ANALYSIS

BY FILIPPO PEDRETTI

Japan’s Long Road to Nuclear Waste Disposal

The proper disposal of nuclear waste is a critical challenge for countries that rely heavily on nuclear energy, such as Japan. Prime Minister Kishida’s pledge to revitalize the nation’s slumbering nuclear industry, shuttered by the March 2011 Fukushima disaster, underscores the necessity of finding a solution this decade.

More than 20 years ago, Japan began a structured approach toward the geological disposal of nuclear waste and formed the Nuclear Waste Management Organization (NUMO) to manage this issue. Since then, the government has struggled to convince suitable municipalities to house the necessary infrastructure.

In recent months, there seemed to be positive momentum around locating a definitive waste storage location. A debate on whether to potentially host such a facility has unfolded on an islet in western Japan. The locality of Tsushima would have been the third to raise its hand as a host candidate in the last three years. However, in the end, turbulent local politics resulted in a stalemate.

Now, all hope rests with the remaining two candidate spots. Both are small settlements in Hokkaido with more than a few challenges, the biggest of which is legislation that effectively bans the movement of nuclear waste into the region. Finding a way around this roadblock, or another town to volunteer as a host, is now center stage in Japan’s nuclear industry.

Legislative and practical issues

After the Fukushima Daiichi nuclear disaster in March 2011, all of Japan’s 17 nuclear power plants, with a total of 54 reactors, were shut down. At the moment, there are 24 reactors scheduled for decommissioning or in the process of being decommissioned.

The Basic Energy Plan sets a target to secure 20% of Japan’s electricity supply from nuclear power by FY2030. To maintain this 20% contribution from nuclear power by 2050, it’s estimated that 10 to 20 new reactors need to be built by mid-century.

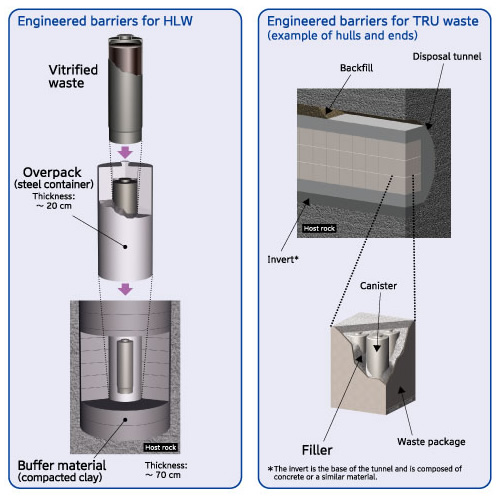

In 2000, Japan enacted the Designated Radioactive Waste Final Disposal Act and set up NUMO to manage the geological disposal of both high-level radioactive waste (HLW) and transuranic waste (TRU) generated from Japan’s nuclear fuel cycle. This waste results from reprocessing spent nuclear fuel, wherein reusable uranium and plutonium are separated, leaving HLW and TRU waste.

The HLW is vitrified and encased in stainless steel, preparing it for geological disposal. This entails placing the waste in stable underground locations at least 300 meters deep. The final disposal site surface will cover about 2 km², with underground facilities storing over 40,000 glass pillars containing nuclear waste.

Source: NUMO

Wanted: Volunteer sites for nuclear waste disposal

There’s a three-stage investigation for selecting a final disposal site. The first stage, termed “Literature survey,” entails NUMO collecting region-specific geological data, maps, and academic papers. Next, they assess the geological stability of potential sites by checking for significant vulnerabilities such as volcanic or fault activities, or weak geological layers that could hinder underground construction.

The second step is an “Overview survey” during which boring and other related tasks are made at candidate sites. Finally, a “Detailed survey” is made, coinciding with setting up an underground research laboratory at the planned sites. These three steps can take as long as 20 years in total.

In 2002, NUMO began inviting Japanese municipalities to volunteer as locations to host a nuclear waste storage site. In 2007, Toyo town (Kochi Pref), led by Mayor Tashima Yasuoki, stepped forward. However, his decision was made without consulting the Toyo assembly, which in the end stirred up significant local opposition. The next election was won by a candidate opposing the storage plan, which led to the withdrawal of Toyo’s application.

Just putting up one’s hand can be a windfall for a locality because accepting a survey comes with significant financial incentives. The first phase provides municipalities with up to ¥2 billion, and no obligation to pay it back in the event of subsequent withdrawal. The second phase can involve a total grant of up to ¥7 billion. Despite the lucrative payout, about 15 years have passed without any other municipality stepping forward as a candidate site.

| Survey Phase | Activities | Grant amount | Duration |

| Literature survey | Research using maps, academic papers, etc. | Up to ¥2 billion | About 2 years |

| Overview survey | Bedrock and geology investigation through boring | Up to ¥7 billion | About 4 years |

| Detailed survey | Underground facilities construction | To be determined | About 14 years |

Final site selection process

To spur momentum into the search, in 2017 the central government produced the Nationwide Map of Scientific Features, which delineates areas deemed scientifically and geologically suitable for a final storage of nuclear waste.

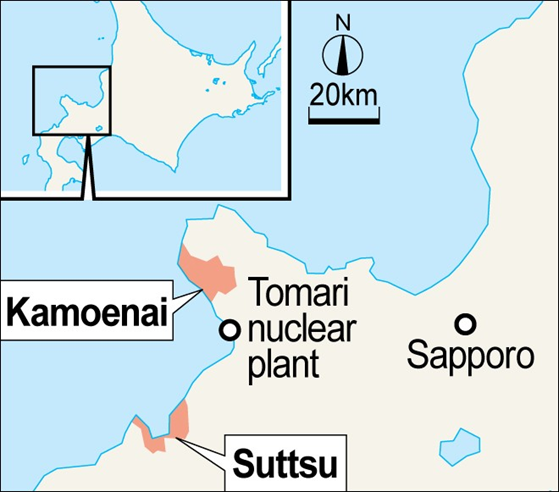

Finally, as the impact of the Covid pandemic hit local economies, two municipalities in Hokkaido suddenly stepped forward. In late 2020, survey work began in the town of Suttsu and the village of Kamoenai that applied for a “Literature survey.” Suttsu, with a population of 2,838, and Kamoenai with about 870 residents, resemble many other peripheral Japanese towns with dwindling populations and industries in need of financial resources.

Following METI’s approval of the two towns’ applications, NUMO began surveys in both locations on November 17.

Location of Kamoenai and Suttsu.

Source: Asahi Shimbun

Kamoenai, however, isn’t an ideal place for a storage facility. According to the map, it sits near an active volcano, which leaves only a small southern portion of the village as suitable ground. Suttsu looks more promising. Still, as far as NUMO is concerned, both locations were within areas deemed as potentially suitable based on the 2017 Nationwide Map of Scientific Features. That’s why the agency says it went ahead with the surveys.

Recent developments

Despite NUMO hosting explanatory meetings and a publicity campaign targeting about 160 locations nationwide, the only concrete interest so far has been limited to the two places in Hokkaido. This led to a revision of the Designated Radioactive Waste Final Disposal Act in April 2023, aiming to enhance information-sharing and discussions among the government, NUMO, power utilities, and local municipalities. Starting July, a team of representatives from government and power companies began a nationwide tour in order to expand the regions where the literature review could be conducted.

The group seemed to sway the mood in Tsushima (Nagasaki Pref), a small islet north of Kyushu. The Tsushima City council discussed acceptance of the literature survey, with a pro-acceptance group submitting a petition. After an initial rejection, on September 12 the petition was adopted with a majority of 10 to 8 in favor. However, the final decision on whether to welcome the survey rested with the mayor.

On September 27, the mayor decided not to accept the preliminary survey, citing several reasons such as insufficient local support, concerns about reputational damage to tourism and the fisheries industry, and the inability to eliminate risks from unforeseen factors. NUMO responded to Japan NRG to say that it takes the mayor’s decision seriously, and that nothing has been decided at the current time.

Things seem to be progressing in Hokkaido, however. Initially slated for a two-year duration, the literature surveys in Suttsu and Kamoenai were extended by about a year. What’s more, the local political support seems to remain in place, at least for now.

On October 3, an election was held for the Suttsu town council. Five candidates supporting the survey were elected, ensuring a majority. The town also elected four council members that oppose the survey. Although not directly involved in the survey process, the council, alongside the mayor, will likely have a big influence on how the town’s residents feel about moving to the second stage of the survey process.

What’s next?

Suttsu’s Mayor Kataoka plans a referendum on whether to proceed with the second “overview survey” stage of the process. But even if the residents approve, the town will also need to battle with the Hokkaido governor.

While not required for the first stage, the governor’s approval is necessary to proceed to the second, and Hokkaido Governor Suzuki Naomichi is not a supporter. Suzuki can defend his position by pointing to a Hokkaido Prefectural ordinance that strongly advises that no nuclear waste should be brought into the region.

Interestingly, Hokkaido is the only prefecture with a clear anti-nuclear waste stance. Its ordinance doesn’t prevent municipalities from conducting surveys, but it hints at potential roadblocks that will impede waste importation.

Of course, ordinances and laws can be rewritten if there’s enough reason to do so. If research confirms the sites as suitable locations, then the national government can work on persuading the Hokkaido governor to lessen the prefecture’s opposition.

When the survey began three years ago, both Mayor Kataoka and then-Minister of Industry Kajiyama Hiroshi backed it, saying that the initial phase did not automatically lead to the second stage, and that the literature survey did not contradict the ordinance. This appeared to sidestep the issue and postpone the problems, playing for time.

The stalling tactics could easily backfire. As local mayors wrestle with the dilemma of winning lucrative grants against likely anger from local fisheries and the tourism industry, the chances of a town performing a U-turn on its candidacy are not small. And the further the survey process extends, the more time will be “wasted” if at some point during the 20-year review period the local leadership withdraws its candidacy. Such a turnaround could easily be sparked by personal conflicts or local politics.

The government’s softly-softly approach looks good enough to reach ‘first base’. But to score a ‘home run’ and secure a viable long-term solution, officials may have to alter their tactics.

GLOBAL VIEW

BY JOHN VAROLI

Below are some of last week’s most important international energy developments monitored by the Japan NRG team because of their potential to impact energy supply and demand, as well as prices. We see the following as relevant to Japanese and international energy investors.

AI/Energy demand

According to Schneider Electric, (with the exception of China) AI consumes about 85-134 terawatt-hours (TWh) of electricity across the globe each year, which is about as much as the Netherlands’ energy consumption. This figure could grow five-fold by 2028.

China/Renewable energy

China’s renewable energy expansion can’t keep pace with demand even though the country added 226 GW of generating capacity in 2023 – solar (129 GW); thermal (39 GW); wind (33 GW); and hydro (8 GW). Thermal plants are generating far more hours on average (3,344 hours) than hydro (2,367 hours), wind (1,665) and solar (1,017 hours), according to the National Energy Administration.

France/Hydrogen power

Air Liquide, one of the world’s largest hydrogen producers, plans to invest €3.4 billion over the next 12 months, with half going to projects in the U.S. where it plans to become a leader.

Italy/CCS

Gas grid Snam and Eni plan to capture CO2 and store it in depleted gas fields, betting that French companies, such as cement and steel makers, will store their CO2 in the Italian hub instead of Norway’s CCS facilities. The first phase launches by early 2025 to store 25,000 tons of CO2 a year in depleted gas fields offshore Ravenna.

Qatar/Natural gas

QatarEnergy inked a deal to sell 1 mtpa of LNG supply to Italy’s Eni for 27 years starting 2026. The volumes will be sourced from expansion of the North Field East (NFE), one of the world’s largest gas fields, which will increase LNG production from 77 mtpa to 110 mtpa. With the North Field South (NFS) phase, Qatar plans a capacity of 126 mtpa by 2027.

Russia/Natural gas

Gazprom will supply extra gas to Hungary this winter, and will provide China with an additional 600 million cubic meters this year on top of contractual obligations. President Putin met the leaders of both countries during a trip to China last week.

Offshore Wind

General Electric expects its offshore-wind operations to post annual losses of about $1 billion for this year and in 2024 as the industry struggles with rising costs. Next year, the company expects offshore will have similar losses but “substantially improved cash performance.”

Singapore/Natural gas

Singapore will set up a single buyer of natural gas for its power-generation sector to improve energy security. This entity will aggregate gas demand from the power-generation companies (gencos), then import the gas required, and sell it to the gencos.

Sweden/EV batteries

Northvolt, Europe’s largest battery maker, could go public next year, but the plans are still preliminary. The Swedish battery maker has invited investment banks to pitch for roles in the deal that could value the company at about $20 billion.

Venezuela/Oil

A U.S. judge will hold an auction of Houston-based Citgo, which is owned by Venezuela. For the past four years, the U.S. protected oil refiner Citgo Petroleum from creditors seeking to seize Venezuela’s foreign crown jewel for billions of dollars in claims.

U.S./Oil

Chevron will buy rival Hess for $53 billion; the deal reflects energy companies’ bid for oil and gas assets. The deal intensifies competition between Chevron and Exxon, but they’ll now be partners in Guyana’s booming oil fields expected to produce 1.2 mbpd by 2027.

2023 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Hulic Ochanomizu Bldg. 3F, 2-3-11, Surugadai, Kanda, Chiyoda-ku, Tokyo, Japan, 101-0062.