JAPAN NRG WEEKLY

MAR 4, 2024

JAPAN NRG WEEKLY

MAR 4, 2024

NEWS

TOP

- METI puts focus on “super perovskite cells” amid change of direction in national next-gen solar strategy

- EGC plans to re-examine power liberalization, seeks to improve monitoring and trading; also, new study around data centers

- TEPCO begins fourth treated water release from Fukushima NPP site, last one for FY2023

- Two more towns consider tax for spent nuclear fuel storage

- LDP lawmakers seek to accelerate nuclear fusion research

- Foreign investors cautious toward new climate transition bonds

- Govt fully discloses GHG reports of 13,300 businesses

- MoU inked for CCS value chain between Japan and Malaysia

- Japan-U.S. study on carbon capture using solid amine is extended

- IHI to add carbon capture capability to methanation system

- IHI, KHI accelerate hydrogen-powered aircraft development

- Record trading on spot electricity market due to Noto earthquake

- New grid line to connect Tokyo to Hokkaido may cost ¥1.8 trillion

- JERA fills up ammonia tank ahead of 20% co-firing at coal plant

- Manies Group and Mercuria to develop solar plants in Taiwan

- Daihen’s new grid storage battery system requires less space

- Toyota affiliate to install first PowerX storage battery

- Tohoku Electric to build dry cask storage at Onagawa NPP

- Hitachi invests €30 mln for transformer operations in Germany

- LNG stocks up slightly last week, but down 12.9% YoY

- Saisan partners with U.S. firm on LP gas sales in Africa

- Japan’s fossil fuel imports drop significantly in January

ANALYSIS

JAPAN’S STRATEGY FOR CARBON CAPTURE AND STORAGE IN SOUTHEAST ASIA

Carbon Capture and Storage is one solution that Japan is betting big on to solve Southeast Asia’s emissions problem. While the technology is still in its infancy and has limited operational capacity globally, Japan is eager to become a frontrunner. Southeast Asian nations show abundant CO2 storage potential because of more suitable geology, but they lack the financial means to develop innovative technologies such as CCS. In this context, Japan and Southeast Asia complement each other and offer possibilities for cooperation and mutual growth in CCS.

THROUGH RENEWABLES, INDONESIA OFFERS JAPANESE FIRMS SIGNIFICANT CO2 CUTS

Indonesia is one country where Japan hopes to create an overseas carbon storage hub to sequester some of its emissions. It’s also a country where Japanese firms seek to reduce their CO2 footprint the most, via the Joint Crediting Mechanism (JCM), a scheme that offsets the costs for Japanese firms looking to introduce clean energy technologies overseas. Now that the JCM has passed the ten-year mark, Indonesia has clearly emerged as a strategic partner for Japan in its approach to carbon markets and management.

ASIA ENERGY VIEW

A wrap of top energy news that impacts other Asian countries.

EVENTS SCHEDULE

A selection of events to keep an eye on in 2024.

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group

Events

Editorial Team

Yuriy Humber (Editor-in-Chief)

John Varoli (Senior Editor, Americas)

Mayumi Watanabe (Japan)

Wilfried Goossens (Events, global)

Kyoko Fukuda (Japan)

Magdalena Osumi (Japan

Filippo Pedretti (Japan)

Tim Young (Japan)

Regular Contributors

Chisaki Watanabe (Japan)

Takehiro Masutomo (Japan)

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

OFTEN-USED ACRONYMS

|

METI |

The Ministry of Economy, Trade and Industry |

mmbtu |

Million British Thermal Units | |

|

MoE |

Ministry of Environment |

mb/d |

Million barrels per day | |

|

ANRE |

Agency for Natural Resources and Energy |

mtoe |

Million Tons of Oil Equivalent | |

|

NEDO |

New Energy and Industrial Technology Development Organization |

kWh |

Kilowatt hours (electricity generation volume) | |

|

TEPCO |

Tokyo Electric Power Company |

FIT |

Feed-in Tariff | |

|

KEPCO |

Kansai Electric Power Company |

FIP |

Feed-in Premium | |

|

EPCO |

Electric Power Company |

SAF |

Sustainable Aviation Fuel | |

|

JCC |

Japan Crude Cocktail |

NPP |

Nuclear power plant | |

|

JKM |

Japan Korea Market, the Platt’s LNG benchmark |

JOGMEC |

Japan Organization for Metals and Energy Security | |

|

CCUS |

Carbon Capture, Utilization and Storage | |||

|

OCCTO |

Organization for Cross-regional Coordination of Transmission Operators | |||

|

NRA |

Nuclear Regulation Authority | |||

|

GX |

Green Transformation |

NEWS: ENERGY TRANSITION & POLICY

METI puts focus on “super perovskite cells” amid change of direction in PSC strategy

(Japan NRG, Feb 28)

- METI plans to provide new funding programs for the development of “super-highly efficient perovskite solar cells”, which will be separate from the Green Innovation Fund, a METI official said in a keynote address at Smart Energy Week in Tokyo.

- The perovskite solar cell (PSC) tech will likely create three markets:

- 1) modules for small devices and for indoor use;

- 2) light and flexible modules installed on walls and roofs with weight constraints; and

- 3) “super-perovskites” for vehicles and aircrafts.

- The present single-junction perovskites cannot be used for transport vehicles with space constraints. Tandem-structured “super-perovskites” with higher performance are needed, and this would require extensive research on interconnection of various chemical layers, etc, that fall outside the traditional perovskite research.

- CONTEXT: This is a change in the direction of the national PSC strategy, which focused on raising energy self-sufficiency by developing silicon-free modules. The tandem “super-perovskites” consist of a perovskite layer made of lead and iodine, but silicon has been the most common material for the second layer. As a result, Japanese companies lag behind the EU and the U.S., where tandem cells are the mainstream.

TAKEAWAY: METI is very successful at creating new funding mechanisms and securing govt finance. But industrial strategies entirely led by METI have a less stellar track record. So, a “super PSC” strategy will hinge on the motivation and efforts of domestic players. PXP Corp and Kaneka are the main tandem PSC developers in Japan. The others, notably Aisin of Toyota group, still need to decide whether to focus on IoT devices and building applications, or to launch tandem development by forming alliances with overseas players. There’s little chance of getting automaker support for developing “not-so-super perovskites”. Another issue is whether the new financing scheme planned by METI will cover foreign companies.

EGC plans to review power retail reforms, seeking to improve trading and monitoring

(Government statement, Feb 27)

- The Electricity and Gas Market Surveillance Commission (EGC) will write new policies to improve monitoring and review of the wholesale electricity market, seeking to ensure fair and more accessible trading conditions.

- The EGC also plans to draft medium-term policies outlining challenges that the surveillance committee should address by 2026. Five meetings will be held this spring to work on the policy, including hearings with experts.

- The EGC outlined three areas to examine: (1) the full liberalization of the power market and institutional reforms; (2) conditions for a level playing field in the wholesale electricity market; and (3) the monitoring, review, and institutional functions in the transmission and distribution (T&D) sector.

TAKEAWAY: The rally in electricity prices in the last few years put a significant number of electricity retailers out of business. According to various surveys, as many as one in six retailers either went bankrupt or decided to pull out of the market. The exits were not always managed well, and the sudden pullback led to a flurry of new customer applications to major power utilities, overwhelming their ability to process the requests. METI, under whom the EGC sits, believes it is important to improve the quality of market players in the electricity retail space and this latest review seems to be part of the process of helping the market mature.

- SIDE DEVELOPMENT:

EGC sets up group to study impact of data centers on grid, power demand

(Government statement, March 1 1)- The EGC is launching a group to study the impact on the grid of new demand factors, such as data centers and quick EV charger stations, and how these will counterbalance with longer-term trends including population decline.

- Over the next 10 years, a significant amount of new power demand is expected to materialize as semiconductor fabs, telecom and data infrastructure, and EV chargers are rolled out. This increase, however, won’t be evenly distributed across the country; rather, demand is expected to increase locally in certain areas.

- What strategies should be adopted in the face of this trend, including additions to the grid and power generation facilities, will be the subject of the group’s review.

- The group will hold its first meeting on March 1, and finalize its findings in the summer. Its report will be shared with ANRE for policy making.

Onagawa, Ishinomaki consider introducing tax for spent nuclear fuel on NPP premises

(Nikkei, Feb 28)

- The town of Onagawa (Miyagi Pref) and Ishinomaki city began considering a tax for spent nuclear fuel. There are concerns that the temporary storage of spent fuel on an NPP’s premises could be prolonged. For example, Tohoku Electric expects to be able to store more than 10 years’ worth of spent fuel.

- The utility considers dry storage as temporary, but there’s concern that the storage could become permanent.

- CONTEXT: Five municipalities, such as the city of Mutsu (Aomori Pref), have already introduced a nuclear fuel tax based on the amount of spent fuel stored.

TAKEAWAY: According to METI, storage at NPPs nationwide has reached around 80% of total capacity. In theory, Japan’s plan is to send the nuclear spent fuel rods to the Rokkasho Reprocessing Plant, whose launch continues to be delayed. NPP operators need other options, the most viable being temporarily storing the fuel on a nuclear power plant’s premises. This stirs concerns among locals, who fear that the spent fuel will be kept there for a long time. As projects such as the Rokkasho plant and other mid-term storage facilities lag behind, friction between NPP operators and communities increases.

LDP lawmakers announce plans to accelerate nuclear fusion research

(Japan NRG, Feb 28)

- Ruling LDP lawmakers plan to establish a party project team on nuclear fusion to speed up research, according to Omae Takayoshi, a chief strategist at the 35-nation International Thermonuclear Experimental Reactor (ITER) organization.

- Omae spoke at Smart Energy Week in Tokyo.

- Japan’s goal is to build a fusion power plant by 2050. The lawmakers plan to push forward the plant operation to 2040, to align with the goals of the U.S. and the UK.

- CONTEXT: Together with the EU, Japan operates the world’s largest fusion experimental facility, JT60SA, (Ibaraki Pref). In March, the Nuclear Fusion Energy Forum that unites the private sector, govt and academia to develop fusion tech, standards and safety rules, will launch. About 40 companies are ready to join.

TAKEAWAY: Aside from the ITER project, Japan has a relatively large number of startups in the fusion space claiming advanced progress in the technology. Such companies claim a pilot fusion plant could be built by the early 2030s, but there is a big funding gap between their ambitions and reality. An LDP project team is one of the ‘early-stage’ govt efforts that could lead to state funding going into private fusion projects.

Foreign investors show caution toward Japan’s new climate transition bonds

(Nikkei Asia, Feb 27)

- Japan launched the world’s first sovereign climate transition bonds. Widely known as GX bonds, the initial batch totaled ¥800 billion, with plans to sell ¥20 trillion over a decade. They will funnel money to various decarbonization projects and initiatives.

- The bonds benefited from a slim “greenium”, indicating moderate investor demand. There are lingering concerns over the way these bonds will be seen by overseas investors. One of the challenges the govt faces is having the bonds recognized as sustainable despite the difficulty of assessing their direct climate benefit.

- CONTEXT: On Feb 14, the Ministry of Finance announced the results of bidding for the inaugural sale of Japan’s 10-year Climate Transition Bonds. On offer were ¥799.5 billion of bonds. The bidding amount was three times greater: ¥2.32 trillion. These bonds will support CO2 emission reduction in high-polluting sectors. Projects include hydrogen-based steelmaking and carbon-capture.

TAKEAWAY: Climate transition bonds are a new class of bonds created by Japan to promote steps towards CO2 reduction that fall outside of the remit of traditional green bonds, which focus primarily on renewable energy. The bond category will bring financing to hard-to-abate sectors, but not only. Many will be watching these bonds to see whether these sales stimulate interest in a new sub sector of financial instruments related to decarbonization. The problem is, most funds that seek out sustainability investments are interested in ‘green’ instruments and doubt the environmental value of a ‘transition’ product.

- SIDE DEVELOPMENT:

Govt discloses GHG reports of 13,300 businesses for FY2021

(Government statement) - METI and MoE have disclosed full details of the FY2021 greenhouse gas emission reports filed by 13,284 businesses; they released a total of 614 mln tons of CO2 equivalent. Data is available online.

- CONTEXT: Companies consuming over 15,000 kiloliters (75,477 barrels) of crude oil equivalent fuels annually are required to file emission reports, and starting from FY2021 this information should also be provided by individual business units.

ENEOS, Mitsubishi and Petronas ink MoU on CCS value chain between Japan and Malaysia

(Company statement, March 1)

- ENEOS, JX Nippon, Mitsubishi Corp, and Petronas CCS Solutions signed an MoU on CCS to study a potential CCS value chain from CO2 capture in Tokyo Bay to storage in Malaysia. The project aims to capture around 3 mln tons of CO2 per year, with plans to increase that to 6 mln tons per year.

- The roles of the companies include CO2 separation and capture, development and evaluation of storage sites. Then they’ll consider CO2 accumulation, liquefied CO2 transport and govt engagement.

- SIDE DEVELOPMENT

JAPEX, JGC, Kawasaki ink deal with Petronas for CCS project in Malaysia

(Company statement, Feb 29)- JAPEX, JGC, and Kawasaki Kisen Kaisha inked a Storage Site Agreement with Petronas CCS Ventures and Petroleum Sarawak Berhad.

- This agreement focuses on the M3 depleted field in offshore Sarawak, Malaysia. There will be feasibility studies for CO2 storage sites. They plan for development to include onshore terminals and pipelines.

- SIDE DEVELOPMENT:

Chugoku Electric and Nippon Gas Line join JAPEX’s Malaysia CCS project

(Company statement, Feb 26)- Chugoku Electric and LPG carrier Nippon Gas Line Co. agreed to join a project led by JAPEX to create a CCS value chain based in Malaysia.

- JGC, Kawasaki Kisen Kaisha, and JFE Steel are already members of the project, which aims to link facilities for CO2 separation, transportation, and storage. The goal is to begin subsea CO2 injection and storage starting by late 2028.

- Currently, the project is focused on cost review of building facilities such as pipelines to carry CO2 onshore, maritime transport of liquefied CO2 and receiving terminals.

Japan-U.S. studies on carbon capture using solid amine to be extended another year

(Japan NRG, Feb 28)

- Japan Carbon Frontier Organization and Integrated Test Center (U.S.) will extend studies, for one more year, on carbon capture using solid amine adsorbents instead of liquid amine.

- The studies began in 2023, and are held at the 400 MW Dry Fork power station in Wyoming. Solid amine developed by Kawasaki Heavy Industries was used to evaluate performance and environmental impact.

- CONTEXT: Solid amine is believed to be energy efficient since it separates the captured carbon at lower temperatures. Liquid amine also emits substances that might have negative environmental impact.

IHI to add carbon capture capability to methanation system

(Japan NRG, Feb 28)

- IHI has developed a carbon capture system that will be an add-on feature to its methanation system that was commercialized in 2022.

- The methanation system produces synthetic methane from CO2 and hydrogen. The process generates heat, which will be utilized as an energy source to capture carbon.

- The carbon unit will capture 0.6 tons / day of 99% CO2, when integrated with a methanation system with a 12.5 nm3 / day of synthetic methane output capacity.

- The carbon capture unit will be commercialized later this year.

TAKEAWAY: In Japan, carbon capture systems have spread slower than methanation tech since companies would rather buy offset credits than make capital investments. Manufacturers believe carbon capture capital and running costs need to fall to ¥1,000 / ton of carbon in order to compete effectively with offset credits. Present CC costs are over ¥3,000 / ton. Some industry members also say state subsidies are needed to spur investment into CC systems.

Kawasaki Heavy to build mid-sized liquefied hydrogen vessel

(Japan NRG, Feb 28)

- Kawasaki Heavy Industries plans to build a mid-sized ship for transporting liquefied hydrogen following the completion of an oceangoing vessel with a 160,000 m3 tank storage space in about 2030. It will have a 80,000 m3 storage capacity, or four 20,000 m3 tanks, and will be for domestic shipping.

- The world’s first hydrogen carrier Suiso Frontier, which was made by KHI, first sailed in 2021. It had a 1,250 m3 tank carrying 75 tons of liquefied hydrogen.

- SIDE DEVELOPMENT:

IHI, Kawasaki Heavy Industries accelerate hydrogen-powered aircraft development

(Japan NRG, Feb 28)- IHI has developed prototypes of the 70 kW turbo blower and other components made of aluminum alloys to feed hydrogen to fuel cells for high-speed hydrogen-powered engines on aircraft. Aluminum was chosen to reduce the component weight.

- IHI’s main premise is the use of gaseous hydrogen. In the last year or so, Kawasaki Heavy Industries has launched R&D on powering airplanes with liquid hydrogen that’s then gasified on board.

TAKEAWAY: Aircraft must be lightweight, so hydrogen in a gas state is seen as more suitable than liquid hydrogen, which would require extra equipment to convert the liquid to gas on board an aircraft and maintain the liquid at -235 C before gasification. A KHI official agreed, but said his company seeks every opportunity to develop new hydrogen applications.

Idemitsu, Mitsubishi, Proman sign ammonia production agreement

(Company statement, Feb 27)

- Idemitsu Kosan, Mitsubishi Corp and Swiss-based Proman agreed to annually produce 1.2 mln metric tons of ammonia in Lake Charles, Louisiana; to start by 2030.

- The plant will use one-step, oxygen-blown reforming technology developed by Denmark’s Topsøe that streamlines ammonia production, as well as use the carbon capture tech “Advanced KM-CDR process” developed by MHI and Kansai Electric.

- The ammonia will be shipped to Idemitsu’s Tokuyama terminal (Yamaguchi Pref), and to Mitsubishi’s Namikata storage facility (Ehime Pref).

TAKEAWAY: Idemitsu’s goal is to build a 1 mln ton / year ammonia supply hub to cover demand in the Chugoku region. Demand will be sufficient if coal-fired power plants owned by local chemical companies shift to ammonia co-firing. Even by 2030, however, Chugoku region’s annual demand is unlikely to hit 1 mln tons since no company has yet announced definite ammonia co-firing plans.

- SIDE DEVELOPMENT:

Tokyo Gas, Miura Co, Gifu Univ to develop ammonia boilers

(Company statement, Feb 26)- Tokyo Gas, Miura Co, and Gifu University will develop boilers and industrial furnaces fueled by ammonia synthesis gas that’s generated in ammonia production.

- The synthetic gas consists of ammonia, nitrogen and hydrogen. The companies plan to identify the optimal gas combustion method and develop a prototype boiler and a furnace by FY2027.

- Research is funded by the Strategic Innovation Promotion Program (SIP) of the Japan Science and Technology Agency.

MOL, Itochu, etc ink MoU on e-fuel and CO2 marine transport using green hydrogen

(Company statement, Feb 27)

- Mitsui O.S.K. Lines (MOL), Itochu, HIF Asia Pacific and JFE Steel signed an MoU on a supply chain for synthetic fuel and CO2 marine transport using green hydrogen. They will conduct a study on CO2 capture, transportation, and e-fuel production.

- Itochu will focus on trading and assessments; HIF on e-fuel business; JFE Steel on CO2 separation; and MOL on ocean shipping.

- CONTEXT: E-fuel is produced from clean hydrogen and CO2. Its usage is facilitated by the fact that it can utilize existing infrastructure and does not require equipment modifications.

Nisshin Kasei to commercialize FC system using silicon waste as feed

(Japan NRG, Feb 28)

- In 2024, Nisshin Kasei plans to commercialize a fuel cell system that uses silicon waste as feedstock to produce hydrogen for power generation.

- One gram of silicon particle generates 1.5 liters of hydrogen. Silicon waste from chip factories is crushed before reacting with an alkaline solution.

- Nisshin Kasei developed an all-in-one fuel cell that produces hydrogen from silicon particles and generates electricity.

- It will first market small 200-300 Watt FC systems for use at remote construction sites, and plans to scale it up to 5 kW.

TAKEAWAY: Manufacturers are targeting small FC systems for use in remote off-grid areas. However, the system loses power if hydrogen runs out. Nisshin Kasei is offering an on-site system that produces hydrogen and power, and easy-to-carry silicon particles as feedstock.

Honda starts online orders for CR-V, Japan’s first plug-in FCEV

(Japan NRG, Feb 28)

- Honda Motor began accepting online orders for CR-V, Japan’s first plug-in FCEV that has hydrogen fuel cells and a plug-in charging system.

- The cars will be imported from the U.S., and delivered to buyers after the summer. The FC system, developed with GM, will be made in the U.S.

- CR-V drives 600 km when fully fueled with hydrogen, and 60 km without hydrogen, to enable travel in areas with no hydrogen refueling station.

- In 2027, Honda and Isuzu Motors plan to commercialize FC trucks mounted with the same fuel cell system. The trucks will likely also be imported from the U.S.

- SIDE DEVELOPMENT:

JR East begins FC train test runs

(Asahi Shimbun, Feb 28)- East Japan Railway Company has begun test runs of Hybari, a train powered by fuel cell and storage battery systems on the Tsurumi Line (Kanagawa Pref). Toyota Motor and Hitachi developed the systems, using Toyota’s FC vehicle Mirai as the base.

- The railway operator plans to start the train in 2030.

Tokuyama to commercialize alkaline electrolyzer in 2025

(Japan NRG, Feb 28)

- In 2025, Tokuyama Corp plans to commercialize its 2 kW alkaline water electrolysis (AWE) system, following tests of its 5 kW prototype electrolyzer.

- The electrolyzer produces 99.97% vehicle grade hydrogen, and would require another step of purification to reach 99.99%, the standard grade in Japan.

TAKEAWAY: Tokuyama might possibly be the second Japanese AWE manufacturer, following Asahi Kasei. AWE’s advantage is its scalability to accommodate GW-sized electrolyzer demand that’s emerging in Australia and the Middle East.

MHI invests in Fervo Energy for geothermal tech

(Company statement, Feb 29)

- Mitsubishi Heavy Industries invested in Fervo Energy, a U.S. startup involved in geothermal technology. This investment was facilitated through MHI America.

- Fervo utilizes technologies from the oil and gas industry to make geothermal energy viable. They particularly focus on untapped locations.

NEWS: ELECTRICITY MARKETS

TEPCO begins fourth release of treated water from Fukushima NPP, last one for FY2023

(Japan NRG, Feb 28)

- TEPCO began releasing the fourth batch of ALPS-treated water from Fukushima Daiichi NPP into the sea. This is the last in FY2023 and consists of 7,800 metric tons.

- TEPCO plans to release 31,200 metric tons of treated water in four rounds in FY2024; the releases will continue for 30 years.

- CONTEXT: The International Atomic Energy Agency will inspect the NPP in March. It recently confirmed that the water release complies with international safety standards for radioactivity. No abnormal tritium levels have been detected in nearby waters after previous discharges. Still, China opposes the release and has banned Japanese seafood imports since the first discharge in August.

- SIDE DEVELOPMENT:

TEPCO suspends investigation of Fukushima reactor containment vessel

(Nikkei, Feb 29)- TEPCO suspended its internal investigation of the reactor containment vessel of Unit 1 at Fukushima Daiichi NPP. The plan was to film the removal of melted fuel debris, but the robot was unable to reach the target point.

- The goal was to investigate for two days from Feb 28, using four drones and a robot.

- The robot, however, got stuck and was unable to reach the area around the base.

- CONTEXT: In March 2023, TEPCO investigated the lower part of the containment vessel and found that most of the inner wall of the base supporting the pressure vessel was damaged, with exposed reinforcing bars.

January JEPX spot market trading: Record volumes after the Noto earthquake

(Denki Shimbun, Feb 28)

- In January, the JEPX had a daily average volume of 19.05 GWh, a 9.6% increase MoM, surpassing the previous month’s performance for the third time.

- On Jan 2, the day following the Noto Peninsula earthquake, the traded daily volume exceeded 30 GWh. On Jan 24, when the Hokuriku region was hit by a cold snap, volume reached a record high of 44.07 GWh.

- In Hokuriku, the Nanao-Ota Thermal Power Plant was shut due to the Jan 1 earthquake. Power troubles were also observed in other areas, leading to a sharp increase in procurement from the spot market to maintain stable supply.

East Area Interconnection line modernization could cost ¥1.8 trillion

(Government statement, Feb 28)

- ANRE said modernization costs will range from ¥1.5 to ¥1.8 trillion for the interconnection linking the Japan Sea side of the East Region (Hokkaido to Tohoku to Tokyo) with a 2 GW HVDC system.

- Construction will combine offshore and onshore components, and will take six to ten years. Expenses for laying submarine cables, covering about 800 km, would range from ¥870 billion to ¥1.1 trillion. The establishment of converter stations, one in each area, would cost between ¥470 and ¥510 billion, and power access lines ¥170 billion.

- CONTEXT: In contrast to ANRE’s estimate, OCCTO gave a different cost estimate, in the range of ¥2.5 – ¥3.4 trillion.

JERA fills up ammonia tank ahead of 20% co-firing at Hekinan thermal power plant

(Japan NRG, Feb 28)

- JERA filled the liquid ammonia tank at the Hekinan No. 4 coal power station (1 GW) ahead of the 20% ammonia co-firing field study that begins on March 26. The liquid will be gasified inside the power generation facility and mixed with coal.

- On March 29, the ammonia ratio in the fuel will reach 20%. The co-firing test will continue into June.

- The ammonia is stored in the tank for a month-long “cool down” before it’s used for power generation. The pier by the Hekinan power plant complex, built to offload coal, will offload ammonia to be transported to the tank via pipeline.

- The present tank is sized 2,000 m3 and has 1.5 tons of ammonia capacity. JERA plans to build multi-10,000 ton tanks on unused land around the Hekinan complex.

- CONTEXT: Ammonia-coal co-firing is a key net-zero solution promoted by Japan’s power sector, and JERA’s Hekinan field study is the world’s first at a commercial power facility. JERA seeks to commercialize 20% ammonia-coal co-firing before 2030. In addition to JERA, Kyushu Electric has been conducting co-firing tests, and Kobe Steel plans to start before 2030.

TAKEAWAY: Industries are closely watching the Hekinan test, as well as the sail of ammonia-fueled ships in about 2027, to determine whether ammonia is a transition fuel that can serve as a bridge between fossil fuels and hydrogen, or a permanent net-zero solution. The main concerns are safety, cost and NOx release, as cited by climate activists.

- SIDE DEVELOPMENT:

Central Japan Association sees co-firing dominating ammonia demand

(Japan NRG, Feb 28)- Central Japan Hydrogen and Ammonia Association said JERA will dominate regional ammonia demand in 2030, as other companies running coal-fired power plants have shifted to biomass co-firing.

- The Association consists of Aichi, Mie and Gifu prefecture authorities and businesses.

- It forecasts 1.5 mln tons of annual ammonia demand for 2030, and 6 mln tons in 2050. Hydrogen demand is seen at 230,000 tons in 2030; and 2 mln tons in 2050.

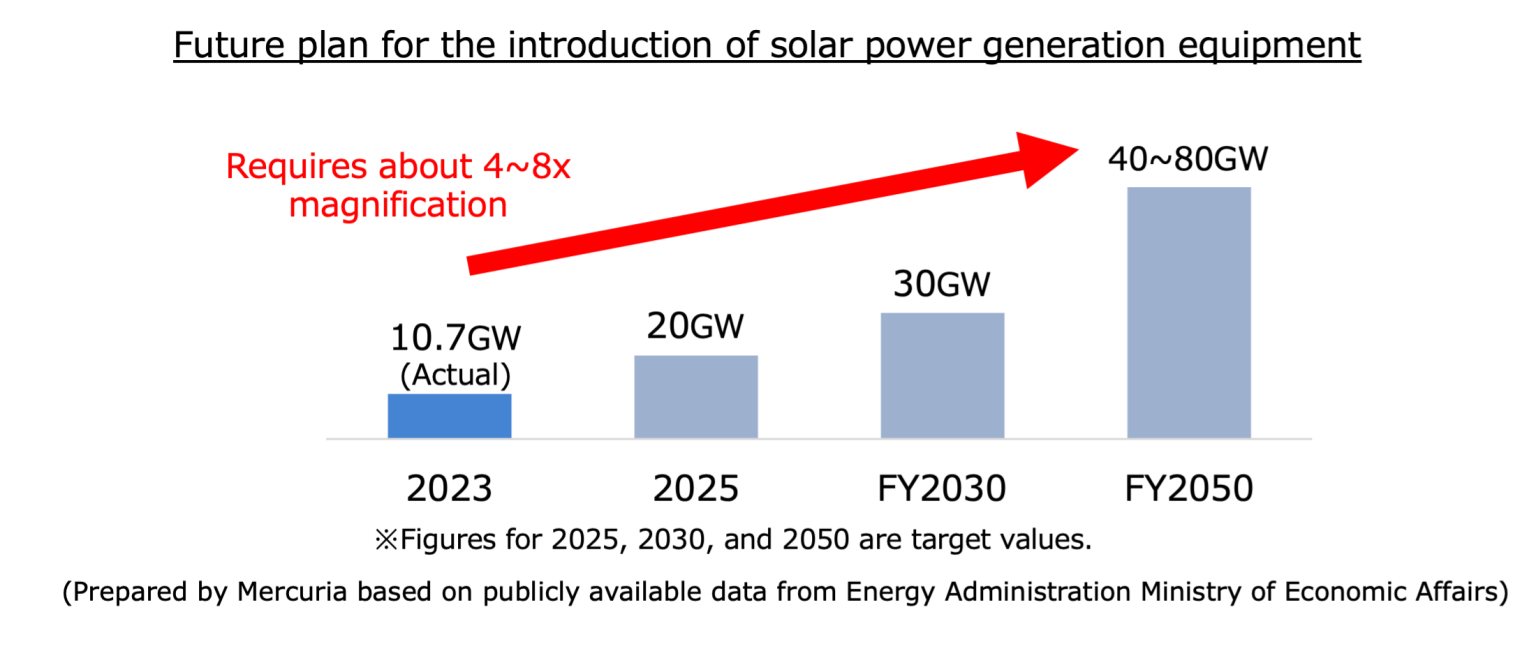

Manies Group and Mercuria Holdings agree to develop solar PV plants in Taiwan

(Company statement, Feb 21)

- Tokyo-based fund management and investment firms Manies Group and Mercuria Holdings inked an alliance to develop solar power plants in Taiwan.

- The first project is a solar PV plant (100-150 MW capacity) in the central part of Taiwan. Construction is slated to be completed by late FY2027.

- CONTEXT: The alliance will create opportunities in Taiwanese solar projects for investors from Japan and other Asian countries. Taiwan has a solar PV target of 20 GW installed by 2025; 30 GW by 2030; and 40 to 80 GW by 2050. The govt aims to introduce 3 to 4 GW by 2025 using a method combining fishing and power generation in which solar panels are installed on top of shrimp, clam, and other aquaculture ponds. As of 2023, solar PV capacity was 10.72 GW.

Daihen’s new grid storage battery system uses less space, reduces costs

(Company statement, Feb 26)

- Daihen developed what it calls the first unit-type power conditioner for grid-scale storage batteries that reduces space needed for installation. It can be connected to 1500V-compatible high-energy-density type storage batteries.

- The system uses silicon carbide (SiC) power semiconductors that increase the voltage a storage battery can handle by 1.5 times in transitioning between DC and AC.

- CONTEXT: As grid storage batteries become larger in scale, finding adequate space is a serious challenge, and this drives costs upward.

Toyota Motor-affiliated parts manufacturer to adopt first PowerX storage battery

(Company statement, Feb 21)

- Tokai Rika, a Toyota Motor-affiliated producer of components such as switches and shift levers, ordered its first container-type stationary storage battery from Japanese startup PowerX.

- The batteries will be installed for the purpose of peak shaving at factories and optimization of surplus power from solar PVs, as well as to help increase the use of renewable energy and reduce electricity costs.

Tohoku Electric to build dry cask storage for spent fuel at Onagawa NPP

(Company statement, Feb 27)

- Onagawa NPP plans to build dry cask storage for spent nuclear fuel from Unit 2.

- Unit 2 is expected to restart around September 2024, and its spent fuel pool will reach capacity four years after that. Thus, as a solution, two facilities for dry cask storage will be created; one will open for operations in March 2028, and the second in June 2032.

- CONTEXT: Dry cask storage is the way that most utilities store used nuclear fuel if they do not intend to ‘recycle’ it to create new fuel. The approach is the default option in the U.S., where utilities have used dry cask storage for decades. Once spent fuel is cooled in a pool for at least a year, it is loaded inside a cask that is sealed to protect any radiation from escaping.

- SIDE DEVELOPMENT:

Tohoku Electric petitions for construction of dry storage at Onagawa NPP

(Company statement, Feb 28)- Tohoku Electric submitted a request for prior consultation to Miyagi Pref, Onagawa Town, and Ishinomaki City to build a spent fuel dry storage at Onagawa NPP Unit 2.

Hitachi Energy invests over €30 mln to expand transformer operations in Germany

(Company statement, Feb 22)

- Hitachi Energy will invest over €30 million to expand and modernize its power transformer manufacturing facility in Bad Honnef, Germany.

- Expected to be completed in 2026, the project will address rising demand for transformers to support Europe’s clean energy transition.

- CONTEXT: The Bad Honnef facility is one of Hitachi Energy’s key production sites in Europe, producing large power transformers that are critical components of the electrical grid in voltage level adjustment for efficient transmission and distribution.

JRC and Wakachiku to cooperate on Japan’s first gangway system for SEP vessels

(Company statement, Feb 21)

- Japan Radio (JRC), a wireless communication company and Wakachiku Construction inked a deal to develop Japan’s first motion-compensated gangway for self-elevating platform (SEP) vessels, to be used in offshore wind installations.

- Its biaxial compensator reduces bridge sway when the vessel shakes heavily.

- CONTEXT: Small and medium-sized SEP vessels used for offshore wind surveys and harbor construction often need to operate amid intense waves, and require lifting a platform. Workers routinely travel back and forth between land and SEP vessels by small traffic vessels. But intense waves often impact their motion, causing severe swaying that inhibits transfer to and from the SEP vessel.

NEWS: OIL, GAS & MINING

LNG stocks up slightly to 2.13 mln tons, but down 12.9% YoY

(Government data, Feb 28)

- LNG stocks of 10 power utilities was 2.16 million tons as of Feb 25, up 3.3% from 2.09 mln tons a week earlier. This is 12.9% down from the end of Feb 2023 (2.48 mln tons), and 1.4% above the 5-year average for this month.

- CONTEXT: Over the past week, there were big temperature swings in the Tokyo area. While some days had double-digit temperatures, March might see some snowfall.

Saisan partners with Jibu on LP gas sales in Africa

(Nikkei, Feb 29)

- Saisan is expanding its LP gas sales network to Africa, particularly Rwanda. Together with the U.S. company Jibu, which is known for bottled water sales in Rwanda, Saisan plans to introduce LP gas sales.

- Saisan and Jibu are setting up a JV, with Saisan holding 51% and Jibu 49%; they’ll invest about ¥100 million.

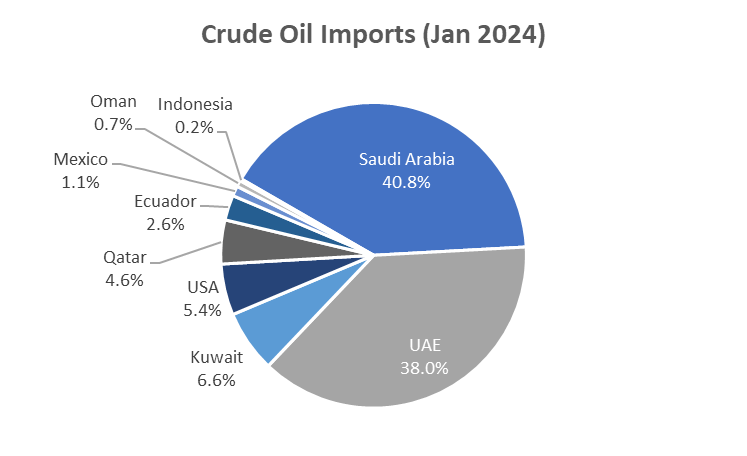

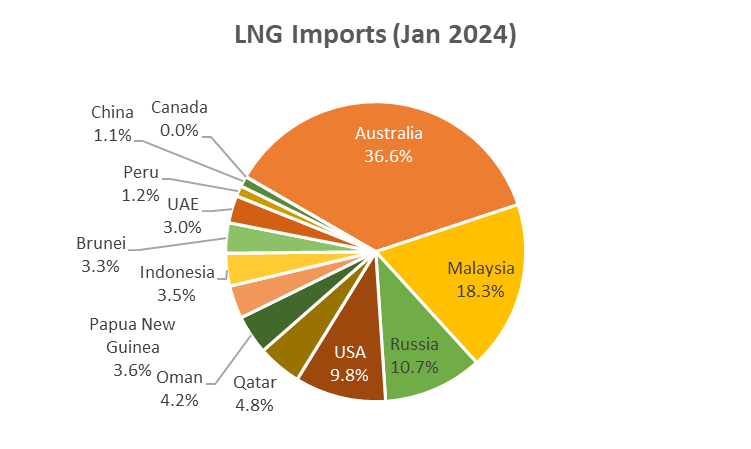

January Oil/ Gas/ Coal trade statistics

(Government data, Feb 28)

|

Imports |

Volume |

YoY |

Value (Yen) |

YoY |

|

Crude oil |

11.8 million kiloliters |

-14.2% |

¥916.3 billion |

-9.2% |

|

LNG |

6.1 million tons |

-10.5% |

¥622.4 billion |

-28.7% |

|

Thermal coal |

10 million tons |

-6.8% |

¥243.2 billion |

-53.6% |

- January crude oil imports declined to the level of Sept-Oct 2023. Over 90% came from the Middle East, with the top 3 countries unchanged from the prior months – Saudi Arabia, UAE, and Kuwait.

- One third of January LNG imports came from Australia, but overall, the supply from the top four nations (i.e., Australia, Malaysia, Russia, and U.S.) was slightly down; while the share from countries such as Papua New Guinea, Qatar, Oman, and Brunei slightly increased.

ANALYSIS

BY FILIPPO PEDRETTI

What is Japan’s Strategy for Carbon Capture and Storage in Southeast Asia?

In 2020, Southeast Asia was responsible for about 6.5% of global energy-related carbon dioxide emissions, a more than twofold increase from 2.8% in 1990. This undesirable trajectory underscores the need for rapid action to reduce the carbon footprint.

Japan hopes its multifaceted decarbonization plan, which consists of several key vectors, can help rectify this situation. Carbon Capture and Storage (CCS) is one solution that Japan is betting big on to tackle the region’s emissions problem. While the CCS technology is still in its early stages and has limited operational capacity worldwide, Japan is eager to become a frontrunner in its deployment.

Last year, Japan Organization for Metals and Energy Security (JOGMEC) launched seven Advanced CCS projects, and METI proposed a CCS Business Act to regulate it. The Act has swiftly moved forward to gain Cabinet approval. However, Japan’s CCS strategy is limited by the country’s geography, lacking suitable sites for large-scale CO2 storage capacity due to the frequency of earthquakes across the country and little history of hydrocarbon exploration.

On the other hand, the rapidly emerging economies in Southeast Asia show abundant CO2 storage potential because of their more suitable geology and ample used oil and gas wells. However, they lack the financial and engineering capacity to develop nascent technologies such as CCS.

In this context, Japan and Southeast Asia complement each other and offer ample possibilities for cooperation and mutual growth in the CCS sector.

CCS in Thailand and Malaysia

In early January, Thailand’s state-owned PTT Exploration and Production (PTTEP) announced a study on the carbon storage potential of Thailand’s Northern Gulf. Such a study will be carried out jointly with INPEX and can count on the support of Thailand’s Department of Mineral Fuels (DMF) and JOGMEC.

The project’s goal is to gather geological data on the area’s potential storage capacity. If the results are positive, then a CCS hub will be promoted in the Eastern Economic Corridor (EEC), a special zone covering about 13,000 square km that comprises three Thai provinces. PTTEP has been in charge of the relevant feasibility study.

PTTEP’s goal is to use CCS technology and the region’s storage potential for reducing CO2 emissions from their sites in Rayong and Chonburi provinces, where the feasibility study is in progress. The provinces are home to several industrial clusters.

The clusters contain traditionally heavily polluting industries. They include four power plants by Global Power Synergy (GPSC); three petrochemical, refinery and power plants run by IRPC, PTT Group’s chemical flagship operation GC and Thaioil; as well as a gas separation plant operated by PTT. The idea is to capture CO2 from these facilities and collect it in a central terminal (the CCS Hub).

From there, the CO2 would be transported through a pipeline to a PTTEP CO2 storage site, to be located offshore in the gulf. The company aims to start the CCS Hub operations in 2033, with a storage capacity of 6 Mtpa.

Source: NANOTEC, NSTDA

In February, Mitsui also inked an MoU with Chugoku Electric to study the potential for a CCS value chain around a storage site in offshore Malaysia.

The project envisages the separation, capture, liquefaction, and temporary storage of CO2 from a Chugoku Electric coal-fired thermal power plant. Then, the CO2 in liquefied form would be transported to Malaysia for permanent storage. Floating offshore temporary storage facilities would also be utilized.

In addition, in June 2023, TotalEnergies and Malay Petronas began developing a site for underground CO2 sequestration in Peninsular Malaysia, planning for CO2 storage by 2030. The Malay region has already been involved in several oil and gas exploration activities and is geographically closer to Japan. Thus, JOGMEC sees the area as having high storage potential once the necessary logistics and port facilities are established.

JOGMEC’s exploration and screening

Last year, JOGMEC’s overseas exploration team released an initial regional site screening for CCS storage in Southeast Asia. They evaluated factors such as plate tectonics, formation rock pressure, and temperature, and analyzed the reservoir resources of a dozen sedimentary basins.

Based on the presence of reservoir rocks and seals, reservoir depth and tectonic movements, five areas were selected, including the Gulf of Thailand and Offshore Malay Peninsula.

High-rating potential CO2 storage sites selected by JOGMEC

|

Indonesia |

Java, Sumatra |

|

Thailand |

Gulf of Thailand |

|

Vietnam |

Northern offshore region |

|

Malaysia |

Offshore Malay Peninsula |

|

Malaysia |

Offshore Sarawak and Sabah |

Source: JOGMEC

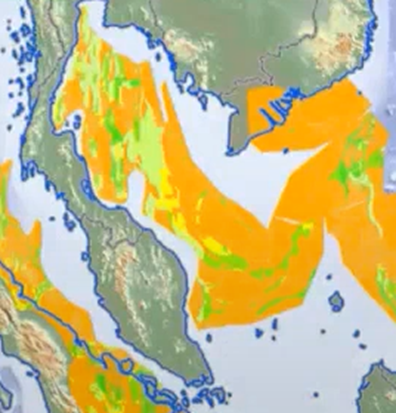

CO2 storage potential in the Gulf of Thailand and Offshore Malay Peninsula.

Source: JOGMEC

The areas in the Gulf of Thailand possess other traits making it suitable, according to JOGMEC. One is the presence of oil and gas fields, which can utilize injections of CO2 to boost output or, once depleted, provide large, well-explored caverns that are suitable for carbon storage.

Indeed, PTTEP has some experience with CCS thanks to its initiative at the Arthit gas field. In a first such project in Thailand, PTTET captures CO2 from gas reservoirs using membrane-based gas separation technology, and then, after compression, transports it to the injection platform, where it’s stored in saline aquifers and depleted reservoirs, at a depth of 1 to 2 km.

Arthit upstream CCS project operations are scheduled to start in 2027. According to the company’s expectation, the project will help to annually reduce up to 1 million tons of CO2 in atmospheric emissions.

Global and national regulations

When it comes to cross-border CO2 transportation, there are certain challenges for both the customer and receiving countries. The former face the high costs of capture, liquefaction, and transportation of CO2. The latter need strong regulatory frameworks that clarify long-term liabilities, port access, as well licensing and contracting for storage.

Currently, The London Protocol is the global agreement that specifically deals with CO2 cross-border transportation and storage. CO2 is considered as “waste”, and its subsea storage is regarded as “dumping”. However, storage from capturing processes is exempted from the dumping prohibition.

As for Thailand and Malaysia, neither have specific CCS regulation at the national level. The state of Sarawak has rules that cover CC for its local jurisdiction, but Malaysia more broadly seeks to develop three CCUS hubs in its National Transition Roadmap. Meanwhile, the Thai government has set a target of collecting up to 40 Mtpa of CO2 annually by 2050, and 60 Mtpa by 2065.

The proposed CCS Business Act in Japan, (which has received Cabinet approval but is now due to be discussed in the House of Representatives in the coming weeks), does not deal in detail with CO2 shipment abroad. It also does not touch on the issue of the vessels used for its transport even though JOGMEC has already said that it will support Japanese companies in acquiring CO2 storage concessions overseas.

So, what regulations will the Japanese firms use? One document that is likely to serve as the basis for cross-border CO2 transport is the guideline for GHG inventories set out by the UN Intergovernmental Panel on Climate Change.

Let’s consider a case of CO2 captured in Country A and stored in another, Country B.

Country A must report captured amounts, emissions from transport, and exported CO2. Country B reports imported CO2 and emissions from injection and storage sites. In case of leakage in Country B, Country A should handle the reporting of emissions it anticipates. This implies bilateral arrangements between countries for monitoring and mitigation. In case of many countries sharing a storage site, reporting responsibilities are based on storage site location.

Furthermore, as per Japan’s proposed CCS bill, operator liability is a sensitive topic. Who should bear responsibility for any accident during the storage phase, both for intentional and unintentional damages, is hotly debated. Government officials claim there has to be a sensible division of liabilities, but that is too vague for project operators to move ahead. After all, CCS operators will need insurance coverage for their infrastructure and final CO2 storage sites, and the uncertainties translate into extra costs on top of the already significant expected outlays.

Particularly on the issue of subsea CCS regulations, MoE and METI have been locked in talks for weeks. Some argue that a CCS project’s overall carbon impact on the marine environment must be assessed, which would widen the scope of liabilities beyond CO2 leakage.

Providing economic viability to the CCS value chain requires policies such as grants, tax credits and low interest loans. Especially for customer countries, strong government incentives are needed in order to profit from a CCS project.

The storage phase alone may be possible for $40/ ton of CO2. But, on top of this comes the costs of capture, liquefaction and transport. Since carbon markets are still developing, there are concerns that the various costs of CCS will require significant government support, which will lead to higher taxes and energy prices.

On the positive front, a stable CCS ecosystem would also benefit the hydrogen industry, of which Japan is a strong advocate. It will broaden opportunities to capture and store CO2 from hydrogen production (the so-called ‘blue hydrogen’ made from natural gas), and open the door to creating synthetic fuels based on the combination of clean hydrogen and CO2.

Despite the many challenges, there does exist a vision around which potential CO2-exporter Japan and CO2-receiving countries could rally. As the two sides sit down to work through the details of regulation, liabilities, financing and operations, Southeast Asian nations will get a chance to decide over how much – and for how much – they are willing to commit.

ANALYSIS

BY JAPAN NRG TEAM

Through Renewables Indonesia Offers Japanese Firms Significant CO2 Cuts

Indonesia is one of the countries where Japan hopes to create an overseas carbon storage hub to sequester some of its emissions. Yet it’s also the country where Japanese firms have committed to reducing their CO2 footprint the most, via a specialist bilateral carbon credits mechanism.

Interestingly, both countries launched national carbon trading markets in the fall of 2023, and data indicates that the cost of carbon reduction is considerably lower in Indonesia. This opens a pathway for Japanese companies with overseas assets, especially in manufacturing, an option to bring down their CO2 footprint for less while “greening” their supply chain.

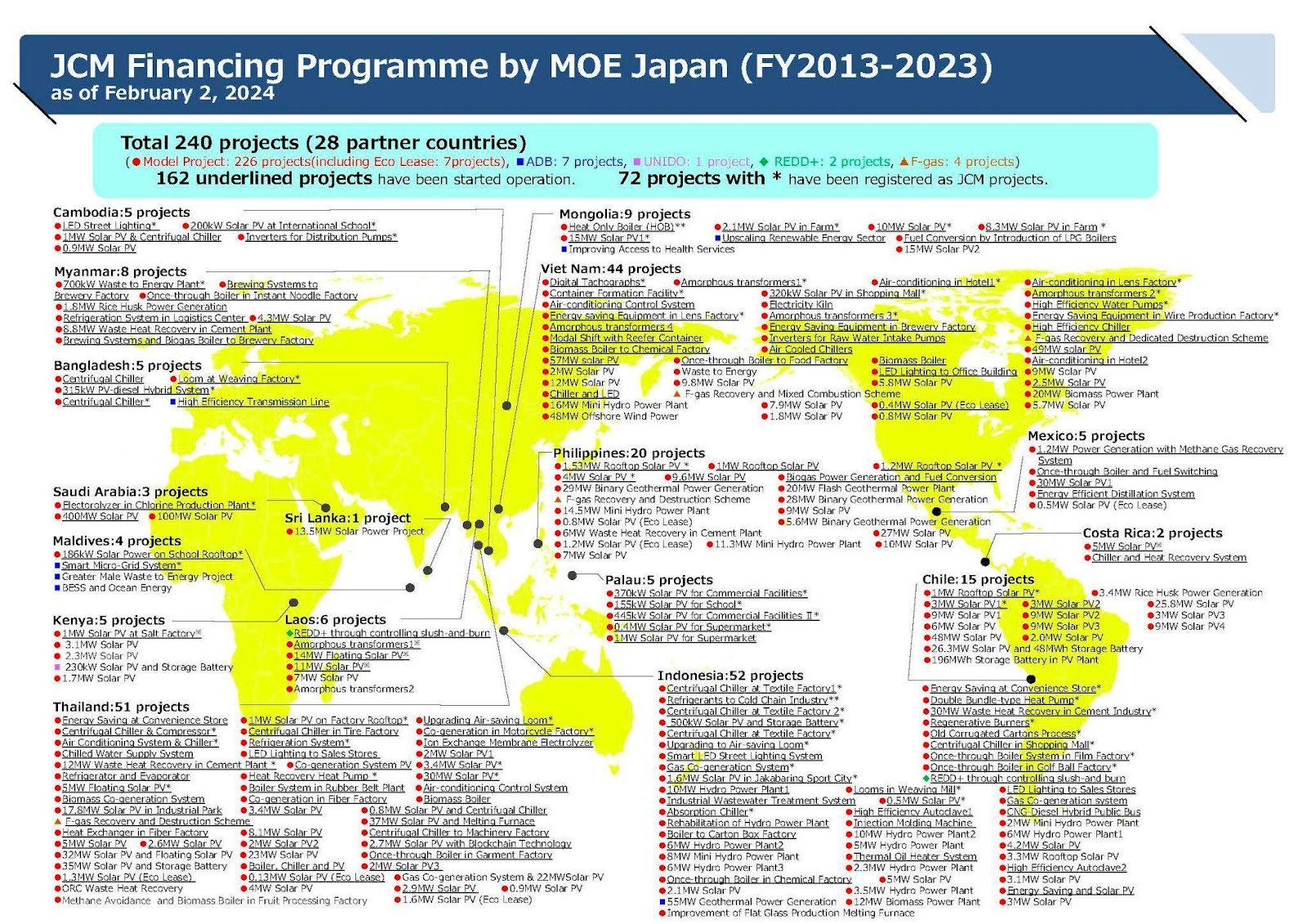

Last month, the Ministry of the Environment in Tokyo published the latest allocation of funding support via the Joint Crediting Mechanism (JCM), a scheme that offsets the costs for Japanese firms looking to introduce clean energy technologies overseas.

In return for funding projects in one of the 29 nations where Tokyo has a JCM agreement, Japan is able to claim around half of the CO2 reduction as its own. At the end of February, Ukraine became the 29th country to join the Joint Crediting Mechanism, the second European country to do so.

Some recently selected projects are in Chile, Sri Lanka and the Philippines, covering the installation of a solar farm, a hydropower plant and a battery storage unit. But the standout JCM project of fiscal year 2023 so far is a 55 MW geothermal power generator that will be built by Tokyo-based JFE Engineering in West Java. That facility alone is expected to deliver almost 10% of the annual CO2 reduction total of all JCM projects to date.

Some recently selected projects are in Chile, Sri Lanka and the Philippines, covering the installation of a solar farm, a hydropower plant and a battery storage unit. But the standout JCM project of fiscal year 2023 so far is a 55 MW geothermal power generator that will be built by Tokyo-based JFE Engineering in West Java. That facility alone is expected to deliver almost 10% of the annual CO2 reduction total of all JCM projects to date.

Source: MoE

So far, in the greater scheme of decarbonization the role of the JCM program has been small. Yet the size of projects that it is funding is starting to increase. Now that the JCM has passed the ten-year mark, Indonesia has clearly emerged as a strategic partner for Japan in its approach to carbon markets and management.

JCM background

JCM projects provide developing countries with low-carbon technologies, products, services, and infrastructure. Japan, through the JCM Financial Assistance Program, helps subsidize the cost of installing equipment and software for renewables and energy conservation and then measures and certifies the reductions in greenhouse gas emissions. Via this scheme, the Japanese government claims a portion of the credits representing CO2 cuts to meet Japan’s own GHG reduction targets. The bilateral nature of the credit exchange is in accordance with international climate agreements and backed by Article 6 of the Paris Agreement.

Since the system launched in 2013, a total of 240 JCM-funded projects have been adopted across Asia, Latin America and the Middle East, but the ASEAN countries are leaders. For example, Indonesia and Thailand alone account for nearly half the total number of JCM projects.

As for the allocation and distribution of emission reductions, Japan earns at least one-half of the credits generated by a JCM project. The rest of the allocation is spread among the partner country, Japanese companies, and partner country companies based on each party’s contribution.

So far in FY2023, which ends on March 31, only 15 new projects have been selected for the JCM. While that’s a lot less than the 38 selected last fiscal year, the average annual emission reduction forecast per project is close to 30,000 tons of CO2, almost double the previous year’s total, according to Japan NRG calculations.

That scaling trend will need to continue if the MoE is to meet its goal of securing about 20 million tons of CO2 in annual reductions by FY2030. After 11 years in operation, the 240 projects selected to date only offer annual cuts of 2.84 million tons of CO2 in total.

Indonesia in the lead

Of all the countries in the JCM mechanism, Japanese firms have found especially favorable conditions in Indonesia, which is home to 52 JCM projects. Thailand comes in a close second with 51, but even then, the size of CO2 reductions in Indonesia tends to be larger.

In terms of individual project size, Indonesia also provides the biggest CO2 cuts, trailing only Saudi Arabia in this category. In that Middle Eastern country, Marubeni Corp has a 400 MW Solar power farm that will have an estimated 475,000 tons of CO2 reduction each year.

In Indonesia, state-owned PT Geo Dipa Energi’s Patuha Unit 2 (55 MW) geothermal power project will have an estimated 274,000-ton reduction each year. At the moment, the year of commissioning has not been stated. The Japan Fund Joint Crediting Mechanism (JFJCM) provided an investment grant for the equipment that will reduce emissions. JFE Engineering is leading in the design and construction of the plant.

JFE has said it sees more opportunities in geothermal in Indonesia, which is keen to tap more of this renewable energy source. That bodes well for coining future JCM credits.

However, there are opportunities across the broader energy sector in Indonesia. In 2014, the JCM’s second year, JFE Engineering built a power plant (waste-heat recovery generator at a cement factory) that offers annual CO2 reductions of about 149,000 tons.

The JCM is helping NiX Group to build the $14 million Tongar mini hydro power plant in West Sumatra. The 6.2 MW capacity facility is expected to generate annual sales of $2.5 million. This is the first overseas hydroelectric power project that the NiX Group has undertaken, and is a rare case in which a Japanese company built its own hydro power plant in Indonesia as a majority shareholder.

Also, AURA Green Energy utilized JCM funding to build its 12 MW biomass power plant in Aceh Province of Indonesia. The facility was commissioned last year.

Indonesia carbon market launches

While the JCM scheme is separate from the J-credits that started trading on the Tokyo Stock Exchange last year, the Japanese government is keen to expand the scope of carbon trading. Officials have signaled that other carbon credits may be allowed to trade in Tokyo in the future.

That could be a future business opportunity for Japanese firms active in the JCM scheme in Southeast Asia. Just as Tokyo welcomed the start of nationwide carbon trading last fall, on September 26, Indonesia launched a carbon market of its own (IDXCarbon). On the first day, credits representing a reduction of 459,000 tons of CO2 were traded. At that volume, the entire CO2 reduction of JCM could exchange hands within a week.

The evolution of carbon markets and their potential future interoperability should open the door to arbitrage opportunities. According to local media, the Indonesian trading price per ton of emission reductions on September 26 was 77,000 rupiah (about ¥733). This is four times cheaper than the cost of a 1-ton carbon credit linked to renewable energy introduction that trades in Tokyo.

Should regulations and carbon accounting rules allow it, Japanese manufacturers could be offshoring not only their factories but also decarbonization efforts in the future.

ASIA ENERGY REVIEW

BY JOHN VAROLI

This weekly column focuses on energy events in Asia and the Pacific, and all that impact markets in the region.

Asia / Grid expansion

Asia will be at the forefront of grid expansion, with China accounting for nearly 30% of the predicted global grid investments of about $374 billion in 2024. According to Rystad Energy, by 2030 the world will need $3.1 trillion in grid infrastructure investment to support the energy transition and limit global warming to 1.8 C.

China / Coal power

In 2023, China accelerated coal permitting, approving 106 GW of coal power projects and began construction of 70 GW, possibly derailing the country’s climate targets for 2025. Global Energy Monitor said that in 2023 China also began operations of 47 GW of coal projects, and announced 108 GW more.

China / Solar power

In 2023, China boosted global shipments of solar modules by over a third from its 2022 total, according to Ember. In 2023, total Chinese exports, which account for about 80% of global solar exports, totalled about 220 GW of generation capacity, up by 55 GW from 2022.

India / Coal imports

This year, thermal coal imports are expected to fall for the first time since 2020 due to increasing domestic output and record high inventories. Experts predict that thermal coal imports could fall as much as 6%. In 2023, India imported 176 mln tons of thermal coal, driven mainly by demand from power plants.

India / Electricity

In 2023, electricity demand rose 7% over 2022’s figure of 149.7 TWh. The increase was due to greater consumer and industrial usage, said a report by the International Energy Agency.

Indonesia / Critical raw materials

Indonesia says its nickel production will be more than sufficient to meet demand and keep global prices low; the price of the EV battery metal will stay below $18,000 a ton, reported Bloomberg. Recent sharp drops in nickel prices have hit producers across the globe.

LNG demand

In 2024, global LNG demand will rise, with top buyer China leading the way, and EU consumption rising, said a TotalEnergies official. Last week, Asia spot LNG prices hit their lowest levels in nearly three years due to weak demand in Asia and Europe.

Qatar / Natural gas

Qatar will increase natural gas production despite a recent drop in global prices. The country is betting on rising demand in Europe and Asia. QatarEnergy chief Saad al-Kaabi said a new expansion of its LNG production will add 16 mtpa to its plans, bringing the total to 142 mtpa.

Southeast Asia / Renewable energy

While the region’s renewable energy capacity develops slowly, “renewable energy certificates” (RECs) are growing rapidly. From 2019 to 2023, solar and wind REC issuances in Southeast Asia rose almost 13-fold, according to data from international registries.

Vietnam / Wind power

Electric Wind Power, a subsidiary of Shanghai Electric, inked a deal to provide wind turbines to Hai Anh Wind Power for its wind farm in Quang Tri Province. The project will cover 855 ha, with a 40 MW capacity, and operate Electric Wind Power’s WH5.25-172 wind turbine unit, to date the largest onshore wind turbine diameter in Vietnam.

2024 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

Newly added as of Feb 22, 2024

|

January |

|

|

February |

|

|

March |

|

|

April |

|

|

May |

|

|

June |

|

|

July |

|

|

August |

|

|

September |

|

|

October |

|

|

November |

|

|

December |

|

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Hulic Ochanomizu Bldg. 3F, 2-3-11, Surugadai, Kanda, Chiyoda-ku, Tokyo, Japan, 101-0062.