There is growing awareness that various types of seaweed can play a role in mitigating climate change, with Japan promoting usage of so-called ‘blue carbon’ that’s stored in coastal and marine ecosystems. While coastal habitats cover less than 2% of total ocean area they account for about half of all sequestered CO2 in ocean sediments. A new initiative tackles the issue by addressing a blue carbon area that’s received little attention to date.

Hiring companies often want to poach from competitors first, rather than take on the high potential talent who doesn’t yet have the optimal resume. Competition though is fierce, and demand outweighs supply, which can inflate salary offers. Let’s look at whether poaching is the ideal approach – How to do it well, and investigate the alternative approach of hiring for talent rather than direct experience.

ASIA ENERGY VIEW

A wrap of top energy news that impacts other Asian countries.

EVENTS SCHEDULE

A selection of events to keep an eye on in 2024.

JAPAN NRG WEEKLY

PUBLISHER K. K. Yuri Group

Editorial Team Yuriy Humber (Editor-in-Chief) John Varoli (Senior Editor, Americas) Mayumi Watanabe (Japan) Wilfried Goossens (Events, global) Kyoko Fukuda (Japan) Magdalena Osumi (Japan Filippo Pedretti (Japan) Tim Young (Japan)

METI plans to increase the Green Innovation Fund allocation to meet unexpected R&D cost increases for the projects it supports.

The ¥300 billion reserve, set aside for emergencies, will be reduced to ¥100 billion; while the remaining ¥200 billion will be spent for project funding.

The fund is ¥2.76 trillion, and ¥2.27 trillion has already been allocated to projects. The balance will be for future projects such as hydrogen co-firing in gas turbines.

From this fiscal year, companies applying must disclose 2025 and 2030 Scope 1 and 2 emission reduction goals, and to show roadmaps to cut Scope 3 emissions.

CONTEXT: In 2020, METI set up the Green Innovation Fund with ¥2 trillion, assigning its management to the New Energy and Industrial Technology Development Organization (NEDO). GIF provides 10 years of continuous support to business-led decarbonization initiatives, ranging from R&D and demonstration to full implementation, with specific goals shared between the public and private sectors.

TAKEAWAY: As a key program in Japan’s efforts to reach net zero emissions by 2050, bolstering the Green Innovation Fund is crucial in the face of rising costs. Most of the technology needed to make the broader energy transition succeed are still in R&D phase; hence, such funding from METI and other government agencies will prove to be crucial.

METI has asked Japan Wind Development to file a report on its initiatives to improve compliance. This followed JWD submitting a report to ANRE on March 6 that assesses the causes of violations by its former president Tsukawaki Masayuki.

METI also asked JWD to report whether an investigation committee looking into its case involving bribery found whether there were any other cases of concern in terms of compliance with laws and regulations.

CONTEXT: In October 2023, ANRE requested scandal-tainted JWD to provide neutral and objective verification of its legal compliance measures and compliance system in the implementation of power generation projects. In the same statement, METI reported that the agency also asked the Japan Wind Power Association to involve a third-party to review decision-making and activities of the association.

CONTEXT: To expand JWD’s wind business, Tsukawaki provided illegal financial contributions to lawmaker Akimoto Masatoshi to change national wind auction rules. Akimoto has denied the allegations.

TAKEAWAY: Neither JWD, its new parent company Infroneer Holdings, nor METI have disclosed the compliance review reports to date. In comparison, Kansai Electric (KEPCO) has fully disclosed on its website various compliance reports related to the Takahama town bribery case, as well as the names of the external parties conducting the probes. In late 2019, accusations came to light that a former deputy mayor of Takahama town, which hosts one of KEPCO’s nuclear plants, had been bribing company executives for almost three decades.

In 2028, Japan plans field tests for hydrogen production fueled by nuclear power. This comes after a successful safety test of the High Temperature Engineering Test Reactor (HTTR) last month.

The generated heat will produce so-called ‘pink hydrogen’. But the HTTR has limited output and needs many units for scalability.

Japan plans funds for advanced nuclear reactor development. Yet, there’s skepticism over waste disposal.

CONTEXT: After a period of little activity, HTTR technology is now advancing. Japan’s successful test in late March was the second in the world, after those in China.

TAKEAWAY: Hydrogen produced by nuclear power is referred to as ‘pink hydrogen’. Its main advantage is potentially lower hydrogen production costs with a stable, non-CO2-emitting power source. But it’s still too early to judge how this will compete with hydrogen produced using natural gas (‘blue hydrogen’) or renewable energy (‘green hydrogen’).

In the first trilateral summit in Washington on April 11, President Biden, PM Kishida and President Marcos Jr will discuss nickel supplies from the Philippines.

The Philippines seeks a free trade pact with the U.S. to make its nickel eligible for Inflation Reduction Act subsidies.

CONTEXT: U.S. nickel imports from the Philippines are marginal, but strengthening economic ties is a part of U.S. regional security plans. The IRA application on nickel from the Philippines will benefit Japanese companies that run battery plants in the U.S. After China, Japan is the second largest consumer of Philippine nickel.

TAKEAWAY: The Philippines produces battery-grade nickel that’s been used for Toyota’s hybrid vehicles for decades. The IRA would incentivize stakeholders to improve trade, but it would also depend on the type of nickel products the U.S. will include in the IRA framework. Since the U.S. has no nickel processing plants, it can’t utilize Philippine nickel ore directly.

Japan, the U.S. and the Philippines will cooperate in areas such as semiconductors, digitalization, communication networks, clean energy and critical minerals, PM Kishida told Nikkei ahead of a three-way summit in Washington next week.

“We need the U.S. to remain engaged in the Asia-Pacific region,” Kishida said. “We also face the reality that China is increasing its presence in the region.”

CONTEXT: Japan has been closely aligned with the U.S. for decades but the Philippines move closer to Washington, and away from China, is a more recent development. Kishida will hold separate talks with Biden the day before.

East Japan Railway (JR East) and Tokyu Land set up Sandia, a ¥10 billion renewable energy fund to develop and acquire renewable energy power plants.

The companies will also deepen collaboration in acquisition, development, asset management, etc, and expand the fund to ¥100 billion over the next 10 years.

The firms plan to develop solar power generation and other projects, aiming to build five sites within about five years.

Toyoda Gosei’s hydrogen tank, mounted on fuel cell vehicles and trucks, will be installed on a fuel-cell powered passenger ship operated by MOTENA-Sea.

The tank applies hydrogen storage technologies developed for Toyota Motor’s FC vehicle MIRAI.

Sumitomo Corp, American Bureau of Shipping, CALAMCO, Fleet Management, and TOTE Services began feasibility studies of ammonia ship-to-ship bunkering at the Port of Oakland, Benicia and other ports in the U.S. West Coast.

The studies include safety assessment of ammonia as a marine fuel.

Tokuyama launched production of magnesium hydride tablets that absorb and store hydrogen. The output capacity is 30 tons / year.

The tablet, sized 72 x 72 x 18 mm, captures up to 75 kg/m3 of hydrogen. The tablet size inflates by 10% after absorbing the gas.

CONTEXT: Various metal hydrides, ranging from aluminum to nickel alloys, have been developed to store hydrogen at room temperature. But, this requires capital investments: equipment to capture hydrogen into the metal, a separate device to retrieve the gas, and a hydrogen refining system capable of attaining over 99.99% purity, are required.

TAKEAWAY: The hydrogen-contained magnesium tablets are light enough to be hand carried, but the other equipment is not. Tokuyama says its product accommodates 90%-purity hydrogen, but the storage capacity declines as a result.

Panasonic Energy began talks with Indian Oil Corp to form a JV to produce cylindrical lithium-ion batteries.

They’ll conduct a feasibility study on the use of battery tech, hoping to finalize details on collaboration by summer.

CONTEXT: India anticipates a significant increase in demand for batteries for two- and three-wheel vehicles and energy storage systems. IndianOil is the country’s largest state-owned oil production firm and has set a net-zero goal by 2046.

Idemitsu Kosan took a stake in graphite producer Graphinex in Queensland, Australia.

Graphinex aims to be an integrated producer of battery anodes. It owns a graphite mine in Croydon and plans to set up an anode production plant in Townsville.

Japan Green Investment Corp for Carbon Neutrality (JICN), a MoE-backed fund, has invested ¥300 mln into LINK-US, a Yokohama-based firm providing metal welding solutions using ultrasonic wave technologies.

Ultrasonic waves are less energy intensive compared to lasers. LINK-US applies the technologies for EV battery production.

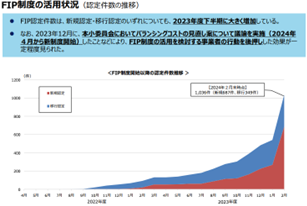

Renewables generation capacity under the Feed-in-Premium (FIP) system increased by 150% from October 2023 through late February, METI said.

Certified capacity under the FIP of both new FIP projects and existing ones that shifted from the Feed-in-Tariff (FIT) totaled 1.507 GW.

Meanwhile, the number of newly certified renewables projects under the FIP rose 3.8 fold between October and February.

In October, the total capacity stood at 986 MW, with 275 certified projects.

The highest number of both new and existing projects were for PV power, but the data also showed an increasing trend in the use of hydro under new certifications, and biomass power in projects shifting from FIT to FIP (details below).

CONTEXT: The Feed-in-Premium scheme was introduced in 2022 to offer financial support to renewables producers as an evolution of the FIT scheme. Under FIP, generators sell electricity to the market, as opposed to the fixed price guaranteed under the FIT.

TAKEAWAY: The number of renewables projects (excluding PV for housing) still operating under FIT was 753,543, with a total capacity of 94.7 MW. The number of projects under the FIT reflect their smaller scale as only those PV installations that are under 50 kW are still eligible for the FIT certification. Still, the increase in FIP certifications reflects the market’s growing acceptance that it needs to adapt to the new system to continue developments.

Type of power source

New projects

Projects shifting from FIP

Total

Capacity

(MW)

Number of projects

Capacity

(MW)

Number of projects

Capacity

(MW)

Number of projects

Solar power

371

654

147

301

518

955

Wind power

212

5

205

15

416

20

Geothermal

2

1

0

0

2

1

Hydropower

170

26

68

6

238

32

Biomass

10

1

322

27

332

28

Total

765

687

742

349

1,507

1,036

Increasing use of FIP certifications for renewables projects from FY2022 and FY2023 with newly certified projects marked in red and FIT-to-FIP transitions in blue.

Research by Teikoku Databank found that as of March 15 a total of 119 new electric power firms left the market or went bankrupt; that’s 43.3% up from the previous year.

The number rose sevenfold from March 2022 and accounts for 20% of a total of 706 new electric power firms registered in April 2021.

In March, as many as 69 new firms cancelled new contracts, down 38.4% YoY.

CONTEXT: New power companies (the shin denryoku) tend to offer customers lower rates than major power utilities EPCOs. That worked as a strategy in the first few years after market liberalisation but came unstuck as prices surged in recent years and grew more volatile. Today, new entrants are in a situation where they need to raise prices or adjust their plans to market rates.

The Electric Power Reserve Exchange (EPRX) acquired legal entity status, starting operation with its revised structure on April 1.

The board of directors consists of general managers from nine transmission and distribution firms (excluding Okinawa). The nine set up EPRX in March 2021 as the operating entity of the Balancing Market.

Regarding the first two auction results disclosed in late March, EPRX’s Secretary General Fukumoto Naoyuki called the failure to receive bids a big challenge in the supply-demand adjustment (i.e. balancing) market. He pledged to increase the number of trading members and revitalize the market.

CONTEXT: Setting up a new legal entity is expected to stabilize operations and ensure transparency and neutrality.

Mercuria Energy Group is preparing to begin trading in Japan’s spot market amid the sector’s rising volatility.

Ahead of the move, Mercuria reportedly hired Kato Masayuki, formerly one of Itochu’s top electricity traders.

CONTEXT: The move follows other European energy companies, including BP, which joined the market last fall, as well as Danske Commodities and Engie earlier this year. Goldman Sachs-backed InCommodities is another firm in the process of getting a license for physical trading.

TAKEAWAY: Following the govt’s recent reform of the market, spot power trading has seen a significant volume increase in the physical electricity market compared to derivatives, drawing interest from overseas firms interested particularly in decarbonization projects.

METI suspended grants to nine solar power generation firms engaged in unauthorized development on forest land. This is the first time the measures were applied since being introduced this month.

The goal is to encourage operators to make effort to gain the understanding of local communities in areas selected for renewables projects.

Under the revised Renewable Energy Special Measures Law that came into force April 1, METI can suspend the government’s FIT and other subsidies for wrongdoing.

All nine firms were found to have violated the Forest Act and their FIT grants were suspended. The names of the firms have not been disclosed but the cases include those where solar panels were installed without permission.

CONTEXT: In relation to the installation of solar panels, there have been a number of cases of landslides and other disasters caused by operators who do not comply with the law and cut down more forest than necessary. The govt’s response to developers who have caused problems with local residents has been limited to issuing them with administrative guidance.

By mid April, Tokyo Gas plans to acquire 13.04% in Renova for ¥17.82 billion.

Renova aims to expand total renewable power capacity from its current 1.18 GW; including building more solar farms, onshore wind projects both in Japan and abroad, as well as solar and battery ventures overseas.

CONTEXT: Tokyo Gas and Renova have been jointly working on the 75 MW Ishinomaki Hibarino biomass-fired power plant that began commercial operations on March 28. Tokyo Gas holds a 34% stake in the project, while Renova owns 38%.

Marubeni, PT Pertamina and Sojitz began commercial operations at the Jawa1 gas-fired IPP plant. It is Indonesia’s first large-scale gas-to-power initiative.

It includes a 1.76 GW gas-fired power plant and a floating storage and regasification unit (FSRU) with a storage capacity of 170,000 m3. It will supply electricity to PT PLN under a 25-year power purchase agreement.

Mitsui O.S.K. Lines (MOL) began commercial operation of the FSRU, Jawa Satu, to service Indonesia’s Jawa 1, Asia’s first gas-to-power project utilizing an FSRU.

The FSRU is owned by MOL through PT Jawa Satu Regas (JSR). It receives LNG from carriers via ship-to-ship transfer. It stores gas, regasifies it, and supplies it to PT Jawa Satu Power that operates the LNG-fired power plant.

JERA ignites Hekinan ammonia co-firing test boiler

(Japan NRG, April 5)

On April 1, JERA began the combustion of fuel composed of 20% ammonia and 80% coal at the test boiler facility in the No. 4 Hekinan power station. The combustion followed test runs of the ammonia dispensing unit in March.

The test, which will run until the end of June, will have three phases:

In April, focus will be on ensuring stable ammonia combustion and control of the NOx release within the environmental standard;

In early May, loads will change to see if parameters will adjust accordingly;

From the second half of May to late June, various load scenarios will be studied to identify the best operational flow for the entire power station.

Co-firing won’t continue 24/7; it will be suspended depending on needs.

Prior to the test, JERA did safety training with the local authority, fire department, police and hospitals.

Test results won’t be disclosed as it’s competition-sensitive information.

KEPCO released the 2023 results for its NPPs. Total electricity generated rose to about 44.2 billion kWh from 27.9 billion kWh in 2022. The utilization rate of NPP facilities rose to about 76.6% from 48.5%.

CONTEXT: The increase was due to the restart of two units at Takahama NPP last summer; now, all seven of the company’s units are in operation.

KEPCO’s financial statement for FY2023 posted the highest net profit ever.

The Japan Bank for International Cooperation and Sumitomo Mitsui Banking Corp will loan $560 mln to the Singapore arm of Trafigura.

JBIC will provide $390 mln, and SMBC $170 mln.

The loan is for LNG supply stability, to allow a Japanese utility to import the gas.

The statement doesn’t name the Japanese utility buying gas through Trafigura.

TAKEAWAY: The JBIC decision is unusual as Trafigura is a trading house rather than an upstream developer, but direct financing of production projects is a govt priority. Trafigura’s impact is not limited to the volume of its LNG transactions; it also has influence on prices. Unlike Japanese trading houses, Trafigura bids in spot trades and influences international price trends, which are often based on spot market moves.

Mitsui to produce its first lithium in Q4 when mine launches in Brazil

(Japan NRG, April 4)

In Q4, Mitsui & Co will begin its first lithium production, when the Minais Gerais mine launches in Brazil.

The mine’s total output will be 300,000 tons / year of spodumene concentrate, a lithium raw material; Mitsui will take 15,000 tons / year. The offtake volume will increase to 60,000 tons / year as output expands.

Mitsui & Co has a 12% stake in Atlas Lithium, a U.S. mining company that operates Minais Gerais and other battery metal projects in Brazil.

CONTEXT: Atlas is Mitsui’s first lithium investment. It also plans to produce nickel, graphite and rare earths in Brazil. Mitsui did not elaborate on the chemical composition of its spodumene.

TAKEAWAY: The mining operation at Minais Gerais has a low carbon footprint as it is fully powered by renewables. But neither Mitsui nor Atlas own any facilities to process lithium carbonate or hydroxide for delivery to battery makers. Control of emissions throughout the lithium value chain is important, which may vary depending on the method to extract the lithium out of the spodumene.

LNG stocks of 10 power utilities were 1.48 mln tons as of March 31, down 2.6% from 1.52 mln tons a week earlier. This is 36.5% down from March end (2.33 mln tons) in 2023, and 30.8% down from the past 5-year average of 2.14 mln tons.

The LNG stock level has been decreasing for five consecutive weeks.

CONTEXT: Low stockpiles are encouraging spot purchases by Japanese buyers for the summer, but interest is still speculative.

The LNG bunkering vessel Keys Azalea was delivered and will be operated by Keys Bunkering West Japan Corp.

Keys is a JV set up by Kyushu Electric, NYK Line, Itochu Enex, and Saibu Gas.

The ship is equipped with dual-fuel engines, able to use both LNG and heavy oil.

ANALYSIS

BY CHISAKI WATANABE

Japan Ramps Up ‘Blue Carbon’, Betting on Sea Vegetation to Reduce CO2

Kelp and other types of seaweed are not merely staples in the Japanese diet. There are growing expectations that they can play a role in mitigating climate change, with the government promoting the usage of so-called ‘blue carbon’ that’s stored in coastal and marine ecosystems.

Blue carbon is a sister of sorts to ‘green carbon,’ which refers to carbon stored in terrestrial ecosystems (i.e., forests, peatlands, and grasslands). Blue carbon began to gain attention following a 2009 report by the United Nations Environment Program (UNEP) that defined it as a new option for carbon sink measures to remove CO2 from the atmosphere.

The ocean is among the world’s largest carbon sinks, along with soil and forests. Coastal habitats like seagrass lands, mangroves, and salt marshes cover less than 2% of total ocean area, but they account for about half of all sequestered CO2 in ocean sediments, according to the Blue Carbon Initiative (BCI), which brings together governments, research institutions and NGOs.

Coastal blue carbon ecosystems, however, are also among the most endangered, according to BCI, which estimates that 340,000 to 980,000 hectares are destroyed every year. Up to 67%, and at least 35% and 29% of the global coverage of mangroves, tidal marshes, and seagrass meadows, respectively, may have been lost so far. Furthermore, when degraded or lost, these ecosystems can release significant amounts of CO2 that’s been stored for centuries.

A new inter-ministerial initiative in Japan is starting to tackle the issue by addressing a blue carbon area that’s received little attention to date.

Background

Seaweed species, however, have been largely excluded from the blue carbon umbrella, according to Conservation International, a U.S. environmental organization and one of the organizers of the Blue Carbon Initiative. In fact, the 2009 UNEP report made no mention of seaweeds.

A 2023 study by Conservation International and the University of Western Australia estimated that the protection, restoration and improved management of kelp and seaweed forests globally could provide mitigation benefits in the range of 36 million tons of CO2, equivalent to the CO2 capturing capacity of as much as 1.6 billion trees.

Quantifying just how much CO2 seaweed forests can absorb is important in reducing total emissions toward net-zero targets. Every year, countries need to report to the UN their inventories of man-made emissions by sources, as well as removals by natural GHG sinks.

In 2013, a supplement to the 2006 IPCC Guidelines for National Greenhouse Gas Inventories was published, expanding the scope of wetlands covered to include coastal areas. That clarified how to organize inventories on seagrass beds, mangroves, and tidal marshes. However, seaweed species were not included in the supplement.

In November 2023, Japan, which has been working on a system to calculate how much seaweed beds can sequester and absorb carbon, published its own guidelines to measure carbon removals by seaweed beds. The MoE says that it’s ready to report on carbon removal by both seagrass and seaweed – about 360,000 tons annually – and the information will be included in an upcoming submission to the UN, due by April 15.

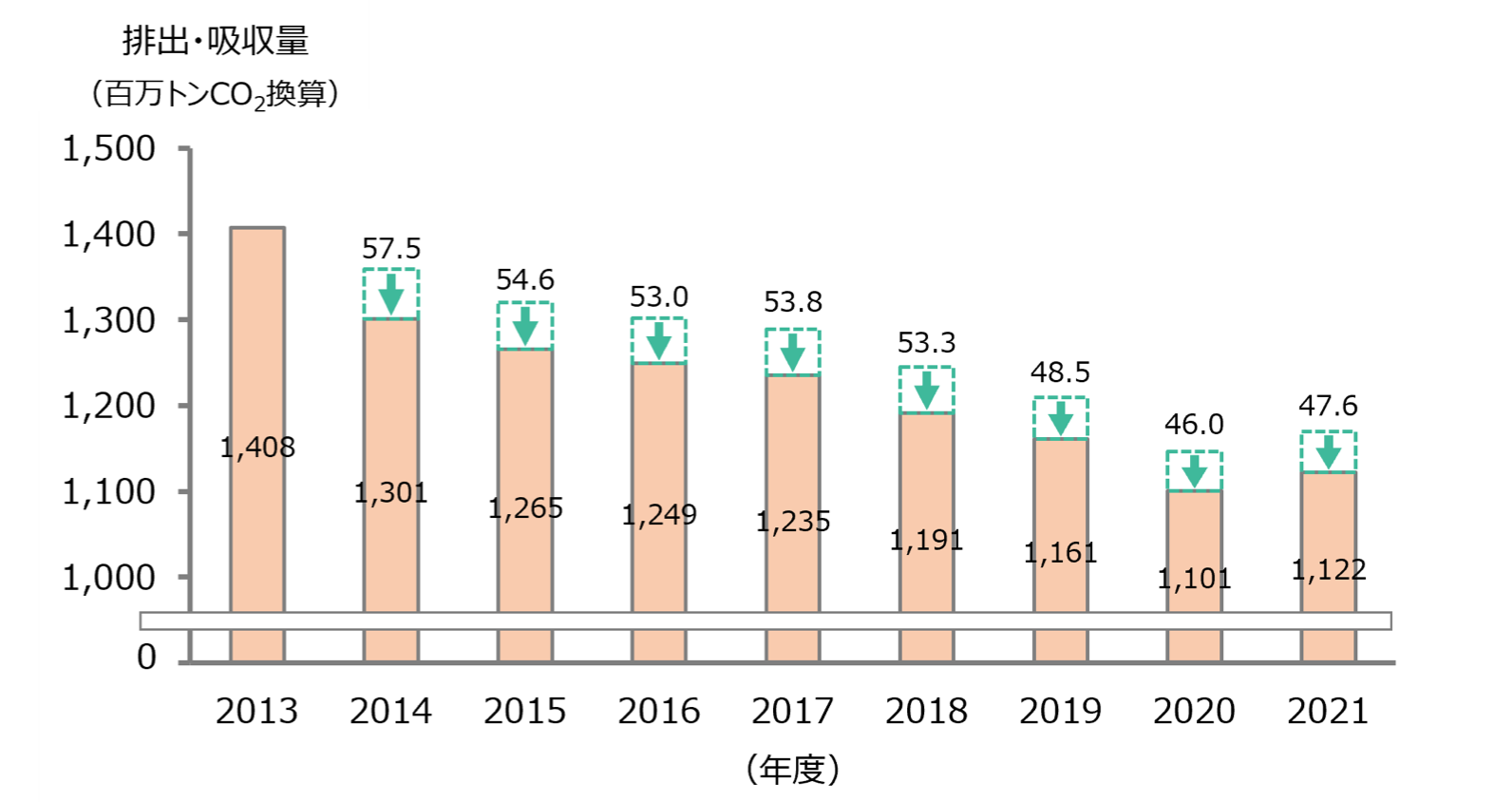

Figure 1 Japan’s GHG emissions and removals

Source: MoE

Potential in Japan

Japan’s FY2021 carbon removals totaled 47.6 million tons and most is attributed to forests – trees capturing CO2. For the reporting of FY2021 results in April 2023, for the first time Japan also included contributions by mangroves, though that was very small, at 2,300 tons of CO2.

Only four other countries – Australia, the U.S., the UK, and Malta – have included blue carbon in their inventories. Australia is the only country that includes seagrass, in this case reporting their loss, which contributes to more CO2 emissions. Because no country has reported on seaweed, the MoE says the upcoming inventory will make Japan the first country to officially list the aquatic vegetation’s carbon removal abilities.

Chart 1: Types of blue carbon inventories reported by countries (both losses and restoration of carbon sinks)

IPCC guidelines

Australia

US

UK

Malta

Japan

Mangroves

Yes

Yes

Yes

Yes

No

Yes

Wetlands (such as salt marshes)

Yes

Yes

Yes

No

Yes

No

Seagrass

Yes

Yes

No

No

No

Planned for April

Seaweed

No

No

No

No

No

Planned for April

Source: MoE

Any contribution from a new carbon sink would help Japan reduce its reported emissions just as its ability to have carbon absorbed by forests rapidly declines as human-bred trees grow older and absorb less CO2, says the MLIT.

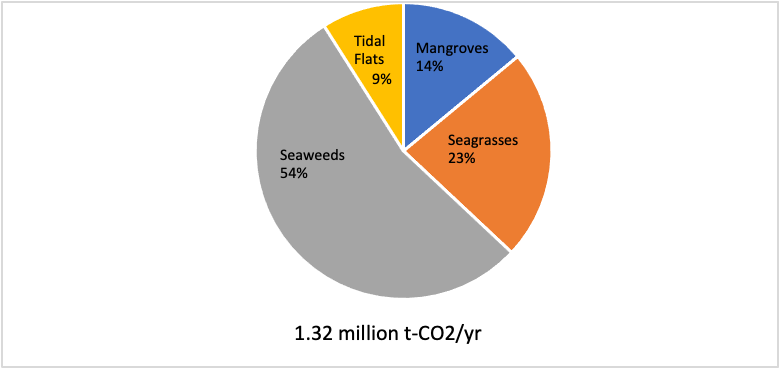

One study shows that the share of blue carbon in total carbon removals will double from 6% in 2019 to 12% in 2030. Japan’s annual blue carbon removal totals 1.32 million t-CO2 on average, with seaweed accounting for more than half.

Figure 2: Breakdown of Japan’s blue carbon estimates

Source: “Nationwide estimate of the annual uptake of atmospheric CO2 by shallow coastal ecosystems in Japan” — Kuwae, et al, (2019)

Efforts public and private

Efforts in this space by Japan’s ministries include the development of carbon-free ports by the MLIT where blue carbon can be utilized to offset/reduce emissions and guidelines set by the Fishery Agency to protect seaweed beds.

To make sure there is greater inter-government collaboration on blue carbon, in January 2023, an inter-ministerial taskforce was set up for this area, bringing to the same table representatives from the MoE, MAFF (including the Fishery Agency), and MLIT.

Activity isn’t limited to national government big-picture policy discussions. Companies, local governments, and fishery co-ops are also part of the push for blue carbon. A list by the MoE includes 45 projects conducted by entities such as Hokkaido Electric, Nippon Steel, and several local governments promoting blue carbon.

Some of the noteworthy blue carbon projects in Japan are as follows:

1) Nippon Steel has been conducting research and pilot projects since 2004 to study what causes the degradation of seaweed beds; it is working with fishery unions in Hokkaido, Miyagi, and Mie prefectures. The steel company aims to improve the ocean ecosystem by installing rocks and blocks for seaweeds to grow on, and by restoring seaweed beds with fertilizer it developed from steel slag, a byproduct of metallurgy.

2) Urchinomics is working to improve seaweed beds in Yamaguchi and Oita prefectures by removing sea urchins that prey on seaweeds. The sea urchins are then grown and sold.

3) J-Power has developed an alternative material for concrete blocks, called J Blue concrete, made mainly from coal ash and copper slag. They have been installed as wave-dissipating blocks serving as seaweed beds.

4) ENEOS announced in December that it has begun a study on the large-scale production of blue carbon with research institutes such as the National Institute of Advanced Industrial Science and Technology (AIST) and the University of Tokyo. ENEOS said it aims to produce more than 1 million tons of blue carbon, without specifying a timeline.

The payoff

Some of these projects can yield credits called J Blue Credits. The Japan Blue Economy Association is in charge of certifying and issuing the credits. In FY2023, 29 projects were approved to issue credits worth 2,170 t/CO2. Projects by Nippon Steel and J-Power are among those that have received J Blue Credits.

Chart 2: Japan ‘blue credits’ issued

FY

Number of certified sites

Volume certified (t-CO2)

Areas certified (ha)

Credits (¥/t-CO2)

2020

1

22.8

10.6

13,157

2021

4

80.4

30.0

72,816

2022

21

3733.1

1100.4

65,567

2023

29

2170.3

1683.1

– – –

Source: Japan Blue Economy Association document

Other countries are also counting on blue carbon. The International Partnership for Blue Carbon (IPBC) was launched in 2015 at the UN climate talks (COP21) in Paris. It was set up for the protection, management and restoration of global coastal blue carbon ecosystems that can contribute to climate change mitigation, adaptation, biodiversity, ocean economies and livelihoods of coastal communities.

Japan’s MoE joined the partnership in August 2023. Australia serves as the coordinator, and NGOs, government agencies, and research institutes are among the 55 members.

While promoting blue carbon has just begun, protecting ocean ecosystems has many benefits, with the removal of CO2 that can be commoditized into transferable credits as one of them.

Further out, seaweed farming has the potential to provide a substitute or supplement for food, animal feed and biofuels; which in turn can lessen agriculture’s overall GHG emissions. The exploration of the sea’s carbon economy is just getting started.

ANALYSIS

BY ANDREW STATTER

Energy Jobs in Japan: Plug & Play, or Invest in Potential?

Client: “We want young, ambitious, bilingual talent with a mix of technical skills as well as solid commercial acumen, who has worked for years with our direct competitor; will match with our culture and is motivated to work for us.”

Agent: “Yep, I’m sure you do. The only issue is that so do all of your competitors.”

I’m slightly exaggerating, but there has been a shift in certain areas of the energy talent ecosystem. Today, there’s a recently developed pool of talent that has led to an attitude shift among hiring companies to consider poaching from competitors first, rather than hire the high potential talent who doesn’t yet have the optimal resume. Offshore wind, energy storage, corporate PPAs, carbon accounting, and various front and mid office roles in power markets are those in which this trend is now prevalent.

Poaching is certainly possible, and successful cases are increasing. Competition though is fierce, and demand outweighs supply, which can inflate prices and give suboptimal offers to acceptance results. Let’s look at whether poaching is the ideal approach – How to do it well, and investigate the alternative approach of hiring for talent rather than direct experience.

The price of talent in Japan has increased

As has been well publicized in recent months, the age of deflation in Japan is finally at its end. Real estate prices have been steadily increasing for the better part of a decade now, peaking with a 30% increase across the Tokyo metropolitan area in 2023. Salaries have lagged behind, but are now moving, with a 3.8% average increase across all TYSE listed firms in 2023, and similar predictions for 2024. Tax incentives are in place for large firms offering 7% or greater wage hikes, and 4% or greater for SMEs, both of which are occurring at rates not seen since the bubble era in 1980s to early 1990s.

These statistics are aligned with Titan’s internal data, where we track talent that we’ve supported to change companies at 1, 2 and 3-year intervals and have seen an average wage increase of 3% over the past 3 years (not including promotions).

The real cost is compounded by the strong performance and record profits from a number of trading houses, energy majors and oil & gas firms, resulting in actual bonus payouts exceeding the theoretical amount, with many cases in the range of 1.5 ~ 2x of target.

Based upon a healthy annual wage increase, coupled with a 1.5x payout of a typical variable bonus of 25% of base salary, the cost of the same talent increased >20% over the past 3 years.

Paying the poaching premium

Talent working for a direct competitor has the strongest appeal for hiring firms. Their knowledge of the market or technology, connections with clients / vendors and up to date regulatory knowledge are all desirable. Their ability to plug into the role with minimal time loss and investment in training and development is also appealing, and can lower both opportunity and T&D costs. Most hiring companies recognise this, and build in a premium rate to attract such talent. Historically, this has hovered around 10%, with 5% variability either side.

Poaching passive talent from competitors comes with the added challenge for the hiring company to offer professionals something they do not already have in their current firm. In some cases, it can be the chance to work on a new technology, or a project that has been recently won. Without this, the candidate is more than likely to demand a step up: a shift to management, a promotion to Director level, etc.

With an increasingly diverse set of players in today’s energy market, illustrated by continued new market entry of foreign players, more aggressive investment by Japanese industry and a slowly growing start-up innovation ecosystem, competition for talent has increased. This compounds the challenge of meeting the candidate’s demands with the need to win a bidding war to secure the services.

As an illustration of this trend, the most recent four changes that Titan has facilitated to direct competitors, with competition for the talent in question, have resulted in total package increases of 18%, 33%, 50% and 21%.

Clear and hidden benefits of investing in potential

In 2011, domestic renewable energy was virtually non-existent. The earthquake and then tsunami striking Fukushima Dai-ichi and the subsequent shutdown of all nuclear plants changed this. With around 24% of generating capacity knocked out overnight, Japan set about promoting renewable energy growth with one of the most lucrative Feed-in-Tariff systems globally.

Both domestic and international investors and developers raced to get a piece of the market, even though there was close to zero experienced talent to hire. Those early years of the solar boom saw developers hiring from module makers, real estate brokerages, ski resort developers, general contractors and even ramen and chocolate entrepreneurs (true story…). Everyone learned the business from scratch, with varying levels of success, of course. However, the moral of the story remains. If you have an attractive business, people will invest their time to jump in, learn and can become industry leaders.

As the primary motivation of this talent pool is to shift into your company and / or industry sector rather than primarily financial, they typically have a mindset to invest in themselves and demand a lower increase, or in some cases can be hired for the same or less as their previous incomes. Depending on the demand for their transferable skills in both your competing industry and the wider market, you may also avoid the bidding war inflation effect as well.

On one hand, this talent will take a bigger front-end investment from the employer to train and develop, however you have the benefit to mold them to fit your business and avoid any undesirable habits. Breaking negative habits and ingrained methods of working can often take longer than the training and formation of new skills.

Employee referrals reduce cost of hire and lower risk

What percentage of your hires annually come via employee referrals? We have seen attractive energy tech start-ups adding upward of 50% of their workforce from internal referrals, to global giants struggling to get into double figures.

When you consider the cost of an internal talent acquisition team, plus all overheads, social insurances etc. or paying Japan level agency fees (typically 35 ~ 40% for expert service), the savings from promoting an employee referral program are significant.

Other benefits include:

Hire a known quantity; your employees won’t bring in the ‘problem child’ from their prior organizations.

Cultural integration; the new hire already has a buddy in your firm.

Less competition; with a 15~18% market penetration across LinkedIn and major Japanese job boards combined, your employee referral has a >80% chance to not be interviewing all over town.

Financial gain is not the key motivator to move, reducing the premium.

Internal equity dilemma, bring your crew along

As an agency, we have cases at offer negotiation time where the current and expected package cost of the candidate that our client wants to hire becomes an internal equity issue. How can the company justify paying the new, unproven hire more than the loyal employee who has been performing well for a number of years?

Fair question. Let’s revisit one of the first points in this column – Japan is not in deflation anymore, and salaries are increasing. Did you increase across your team in the last few years? Your competition most likely did. This not only will cause headaches for both the business and HR departments at the offer stage around internal equity, it also leaves you wide open for attack from competitors who realize you are a great place to find a bargain….

Review your team and wider market trends regularly, benchmark against competitors and ensure that you are in a position to be competitive to hire and protect yourself from guys like us (sorry!).

Andrew Statter is a Partner at Titan GreenTech, an executive recruitment agency focused on the clean energy space.

ASIA ENERGY REVIEW

BY JOHN VAROLI

This weekly column focuses on energy events in Asia and the Pacific, and all that impact markets in the region.

Bangladesh / Coal power

Coal will overtake natural gas as the country’s primary electricity source. Local power firms more than doubled coal-fired electricity generation in 2023 over 2022 levels to a record 17 TWh. In the same period, natural gas-fired electricity output only increased 4.7% to 47.44 TWh.

China / EV charging

Oil company Sinopec is installing thousands of battery recharging sites across China. EV sales in the world’s largest auto market are expected to account for 40% of the 23 million sold this year. China’s gasoline demand is expected to peak in 2025 and then halve by 2045.

China / Natural gas

GCL Holdings is rebuilding a natural gas business after selling hundreds of solar installations to set up gas import capacity. It will join the tier-two LNG players in China such as city-gas companies ENN and Beijing Gas Group that seek to ramp up imports.

China / Solar power

Consolidation in China’s crowded solar power sector is pushing smaller players out of the market. Excess production capacity could keep global prices low for years. China accounts for 80% of solar module production capacity.

Global oil refining

More than 20% of global oil refining capacity might shut, claims Wood Mackenzie. Europe and China have the greatest number of high-risk sites – 11 in Europe, and 7 in China. This is based on estimates of net cash margins, cost of carbon emissions, strategic value, etc.

India / Hydropower

Main reservoirs hit their lowest March levels in five years, impacting hydropower availability this summer. Affected are major economic centers such as Bengaluru. The 150 reservoirs that supply water for hydro-electricity were filled to just 40% of capacity.

India / Renewable energy

Adani Green Energy exceeded 10 GW of operational renewable energy portfolio, India’s first company to do so.The capacity breaks down as 7.39 GW solar, 1.4 GW wind, and 2.14 GW wind-solar hybrid capacity.

Indonesia / Mining

The world’s top nickel producer will expand output despite a glut that’s forcing rivals to shut mines. Indonesia’s production capacity for battery-grade nickel is expected to quadruple to 1 million tons by 2030. This will keep prices low and protect long-term demand for the metal crucial to EV batteries

LNG / Spot prices

Asian spot LNG prices were unchanged this week, as demand from buyers continued shoring up prices. The average LNG price for May delivery into northeast Asia held at $9.50/mmBtu, the same as the previous week, which was its highest level since February 9.

Russia / LNG

The Chinese ship HunterStar delivered the final liquefaction module for Novatek’s Arctic LNG 2 facility. Novatek, the Arctic LNG 2 project itself, and the Belokamenka construction yard near Murmansk have all been sanctioned by the U.S. The transfer of technology used for liquefaction of natural gas has also been banned by the EU.

2024 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

January

First market trading day (Jan 4)

IEA “Renewables 2023: Analysis and Market Forecast to 2028” released (Jan 11)

Renewable Energy Exhibition (Jan 31 – Feb 2)

Taiwan presidential election (Jan 13)

Japan’s Diet convenes

IEA “Electricity 2024 / Analysis and Forecast to 2026” released (Jan 24)

February

CFAA International Symposium (Feb 2)

India Energy Week 2024 (Feb 6-9)

Lunar New Year (Feb 10-17)

Indonesia presidential election (Feb 14)

Japan-Ukraine Conference for Promotion of Economic Reconstruction (Feb 19)

FIT/FIP solar auction (Feb 19 – March 1)

Smart Energy Week (Feb 28-Mar 1)

March

Announcement of auction result for Offshore Wind Round 2 (for Akita Happo-Noshiro Project)

Onshore wind auctions (March 4-15; results on March 22)

International LNG Congress (LNGCON) 2024, Milan, Italy (March 11-12)

Russian president election (March 15-17)

World Petrochemical Conference, Houston, TX, USA (March 18-22)

IAEA Nuclear Energy Summit @ Belgium (March 21)

Ukraine presidential election (due before March 31)

Happo Noshiro, Murakami-Tainai, Oga-Katagami-Akita and Saikai-Eshima wind project auctions close (June 30)

July

Tokyo governor election (July 7)

7th Basic (Strategic) Energy Plan draft published (expected)

August

7th Basic (Strategic) Energy Plan draft presented to Cabinet (expected)

September

Global Offshore Wind Summit Japan 2024, Sapporo, Hokkaido (Sept 3-4)

The United Nations Summit of the Future (Sept 22-23)

Gastech 2024, Houston, TX (Sept 17-20)

IAEA General Conference

GX Week in Tokyo (expected late Sept to October)

Asia Green Growth Partnership Ministerial Meeting

Asia CCUS Network Forum

International Conference on Carbon Recycling

International Conference on Fuel Ammonia

GGX x TCFD Summit

October

IEA World Energy Outlook 2024 Release

BP Energy Outlook 2024 Release

Innovation for Cool Earth Forum (expected)

Connecting Green Hydrogen Japan 2024 (Oct 16-17)

Japan Wind Energy 2024 Summit (Oct 16-17)

Solar Energy Future Japan 2024 (Oct 16-17)

Japan Mobility Show (Oct 25-Nov 5)

November

US presidential election (Nov 5)

COP 29 in Azerbaijan (Nov 11-22)

Abu Dhabi International Petroleum Exhibition Conference (ADIPEC) 2024, Abu Dhabi, UAE (Nov 11-14)

APEC 2024 @ Lima, Peru

International Conference on Nuclear Decommissioning (TBD)

G20 Rio de Janeiro Summit (Nov 18-19)

Offshore Energy Exhibition & Conference (OEEC) 2024, Amsterdam, the Netherlands (Nov 26-27)

Biomass & BioEnergy Asia Conference (TBD)

European Biomethane Week 2024

December

Last market trading day (December 30)

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.