The debate over the economic feasibility of ‘blue hydrogen’ vs ‘green hydrogen’ is approaching a decisive moment, and developments in the State of Texas are at the center of this issue. How it is resolved will impact Japan’s power sector decarbonization in general and Japan’s largest utility, JERA, in particular, as it envisions upgrading coal-powered thermal plants to run on ammonia.

The steel sector will get almost 50% of state green R&D funding over the next ten years. Price is one of the main factors that will influence the next steps in ‘green steelmaking’. In this second part we look at how the steel sector and the government are wrestling with disparities between what they ‘need’ the price of clean steel technologies to look like and what they are in practice.

ASIA ENERGY VIEW

A wrap of top energy news that impacts other Asian countries.

EVENTS SCHEDULE

A selection of events to keep an eye on in 2024.

JAPAN NRG WEEKLY

PUBLISHER K. K. Yuri Group

Editorial Team Yuriy Humber (Editor-in-Chief) John Varoli (Senior Editor, Americas) Mayumi Watanabe (Japan) Wilfried Goossens (Events, global) Kyoko Fukuda (Japan) Magdalena Osumi (Japan Filippo Pedretti (Japan) Tim Young (Japan)

A METI panel on long-term industrial policy published an interim report on strategies through 2040, with a focus on using social issues (health, economic security, green and digital transformations) as growth opportunities.

Since it’s socially and politically more stable than other countries, Japan can play a vital role in global supply chains. Upstream efforts are important for securing base metals such as copper, as well as critical raw materials.

Regarding the GX, the report said that efforts on the 2026 launch of the emission trade (GX-ETS) should continue; incentives and regulatory measures can combine to generate a market that might have linkages with allies.

Japan will build supply chains with allies by coordinating transition investment policies and to advance specific programs for the Asia Zero Emission Community.

CONTEXT: Every June, the govt releases the Basic Policy on Economic and Fiscal Management and Reform, also known as the ‘Big-Boned Policy’. Business lobby groups ask to include a longer term policy scenario in the upcoming policy. This METI paper is likely to be referenced for writing the next Big-Boned Policy.

TAKEAWAY: The paper hints at the potential for Japan’s carbon credit markets to be linked to similar exchanges or programs in other countries. At this point, this is just a mention in a broader strategy paper that has far-off targets and little substance. However, it points to the direction that some in govt and business believe Japan should take – creating an international carbon credits marketplace, which would see CO2 reductions in one place credited / traded in another.

Aomori Pref will draft a new ordinance titled “Towards co-habitation of nature and renewables”; it includes a new tax on operators, establishing zones prohibiting renewables, and calls for dialogue with local stakeholders.

The Aomori governor appointed seven external experts, mostly academics, to the Study Committee. Its first meeting will be on May 2, and several more will be scheduled before the draft is completed.

Possible tax targets are onshore wind and solar operators that are perceived to have had an environmental impact, both new and those in operation.

The ordinance is expected to pass by late FY2024, pending local assembly approval.

CONTEXT: Aomori has 407 onshore wind turbines with a total combined capacity of 910 MW; this is the largest number of onshore wind turbines of any area in Japan. Another 684 more turbines (total capacity 2.53 GW) are in the works. The governor plans a system to allow communities to receive fair economical returns.

In May, Japan and the EU will agree to set common rules on state programs to support net-zero initiatives in the private sector and public procurement.

Japan has a similar framework with the U.S., aiming to reduce reliance on China for products used in EV and offshore wind installations.

Main points are:

Build supply chains based on principles focused on sustainability, etc;

Develop principles on critical materials, but pricing is to be excluded;

Cooperate with the U.S. and other countries sharing the concept;

The principles will be applied to public procurement, subsidies, etc.

The agreement aims to reduce reliance on Chinese supplies for EVs, offshore wind equipment etc., which may be subsidized by the government in Beijing to realize low prices.

TAKEAWAY: It may be possible to exclude some generic or commoditized made-in-China products from the market. But it will be challenging to block Chinese products that are highly innovative and not found in Japan, EU or the U.S. In some sectors, Chinese companies’ R&D spending exceeds that of Japanese businesses even without government subsidies. Even in the more commoditized areas, non-Chinese producers will need to show they have a competitive offering.

Japan’s Information Technology Promotion Agency (IPA) and its EU counterpart inked a MoU to share a database of minerals used in EV batteries.

It will trace the origins and parties involved in deals associated with battery metals, namely lithium, in a bid to facilitate recycling in the Japanese and EU markets. Competition-sensitive data is excluded.

Japan’s database, “Ouranos”, has input from 50 companies and organizations; the EU database “Catena-X”, from 170 companies and organizations.

CONTEXT: The data sharing plan came from the need for Japan’s automotive companies to stay competitive by complying with EU regulations. The agreement includes a mutual authentication of entries in battery metal databases.

TAKEAWAY: In a typical mutual authentication agreement with the EU, the parties review each other’s systems periodically. Extending this framework to hybrid vehicles, as well as drawing a line between “recyclable minerals” and “chemicals with marginal mineral elements that can’t be recycled”, etc. may be possible discussion points.

PM Kishida and Brazilian President Luiz Inacio Lula da Silva are expected to sign the Green Partnership Initiative when they meet in Brazil in early May.

A delegation of about 40 Japanese companies will accompany Kishida. Biofuel tech development and deforestation will be major areas of focus.

CONTEXT: Brazil is this year’s G20 chair, and seeks to be a leader in fighting climate change; in 2025 the country will host COP30.

TAKEAWAY: Japan Biofuels Supply, a JV of five local oil refineries, currently dominates biofuel import trades. Market entries triggered by bilateral initiatives will not only change the trade landscape but will also create a need to explore ways to price biofuel imports. There is no commodity index for the Japanese biofuel market.

The Green Innovation Fund did an annual review of nine projects to develop next-gen power chips, SiC wafers and data storage and energy saving systems for data centers.

The data center project was told to be more focused on AI-derived issues and that a clear business scenario for replacing current DRAM and storage memory devices with nanotube RAM (NRAM) needs to be developed.

Power semiconductor chip designs and development of manufacturing lines begin this year, with work on next-gen central processing unit prototypes in FY2025.

CONTEXT: The goals for 2030 are to achieve 50% power efficiency improvements for electronic devices, and reduce production costs of power chips; and for data centers to realize 40% power savings by deploying opto-electronics based technologies.

The Yokohama municipal govt, TEPCO Power Grid and Ocean Power Grid, a subsidiary of PowerX, signed an MoU on building a power network and a new clean energy supply base in the port of Yokohama, Kanagawa Pref.

The project will examine the possibility of supplying green power derived from offshore wind power to Yokohama’s port and the construction of power supply facilities to cope with increasing demand in the waterfront area.

The project seeks to make the Yokohama port carbon neutral and to be Japan’s first base to supply onshore power to large cruise ships.

Ocean Power Grid plans to transmit energy derived from offshore wind power using an automated power transfer vessel, which would be the first such attempt in the world.

CONTEXT: Ocean Power Grid is a new, wholly-owned subsidiary of Japanese battery startup PowerX, set up to take over marine and wind power projects and development of specialized tech. It will focus on promoting maritime power transmission utilizing battery tankers. It will own, sell, and operate the battery tankers in Japan and abroad. The completion of the first such vessel and test sail is planned for 2026. It will be developed with Imabari Shipbuilding in Ehime Pref.

Future model of the battery tanker Power Ark 100 Series, Source: PowerX

Mitsui O.S.K. Lines (MOL) became the first Japanese shipping company to raise funds through a syndicated transition linked loan.

The loan is from Sumitomo Mitsui Trust Bank, Development Bank of Japan, and SBI Shinsei Bank, and will support MOL’s environmental investments.

The loan structure adjusts interest rates based on MOL’s progress in meeting predetermined GHG reduction targets.

Okinawa’s caustic soda plant to commercialize hydrogen supply

(Japan NRG, April 22)

In 2026, Okinawa-based Showa Chemical Industries will commercialize hydrogen generated at its caustic soda plant in the city of Uruma.

The plant annually emits 31 tons of hydrogen, and 70% goes unused. The gas will be compressed and stored in a tank to be built by Ryuseki Corp, a gasoline retailer.

The hydrogen is certified as “grade 4” (99.9% purity) under the Japan Industrial Standard. Potential users include Okinawa Electric for co-firing at its thermal power plant. For FCV, the gas needs to be reformed to achieve the required 99.97% purity.

CONTEXT: Presently, Okinawa Electric is conducting field tests of hydrogen-LNG co-firing at its 35 MW Yoshinoura power station. In March, it succeeded in co-firing with 30% hydrogen. The studies will continue until FY2025.

TAKEAWAY: The national govt will fund ¥156 mln for building the hydrogen transport and storage facilities, which equates to ¥354/kg of hydrogen, assuming that the facilities will be used for 20 years. This is just about at the 2030 target cost of ¥30 /Nm3 set by the govt.

In March, the number of EV charging outlets hit 40,323, up from 32,251 a year ago, which is about a 25% increase. ENEOS led with 6,609 outlets.

High-speed charging equipment with 90 kW output or more accounted for about 20%.

This year, subsidies for new charging stations will be doubled to ¥36 billion. The 2030 installation goal is 300,000 outlets.

TAKEAWAY: EV charging outlet growth has outpaced that of EV sales, which were 40,327 units in FY2023, up from 35,559 in the previous period. Sparse charging infrastructure was blamed for slow EV sales, which accounted for only 1.6% of total passenger car sales.

Asahi Kasei will build an integrated plant in Ontario, Canada for the base film manufacturing and coating of wet-process, lithium-ion battery separators.

Asahi Kasei plans to manufacture its Hipore™ microporous membrane that provides a barrier between the positive and negative electrodes in LIBs.

It will be in partnership with Honda Motor. Commercial operation is set for 2027.

Production capacity will be about 700 million m2 per year, as coated film. The project will receive funding from the Development Bank of Japan and support from the Canadian govt and the province of Ontario.

Toyo Engineering, Chubu Electric, Chubu Electric Power Miraiz and Nippon Seisen inked a MoU to develop small-scale crackers to convert ammonia into hydrogen.

Demand for hydrogen as boiler and engine fuel has potential; ammonia could be the best hydrogen carrier as it can be transported and stored with current technology.

Toyo and Nippon Seisen will develop the cracker, and Chubu Electric will study market strategies.

CONTEXT: Hydrogen might be better as fuel than ammonia since it’s more flammable; but ammonia can carry more hydrogen molecules than liquefied or compressed hydrogen, or methylcyclohexane (MCH).

Hokkaido Electric, IHI, Marubeni, Mitsui & Co, Mitsui Chemicals, and Tomakomai Futo will study building an ammonia supply chain in Tomakomai, Hokkaido.

The focus is on facilities required to import, store and deliver ammonia, and its demand in north Japan.

The group will hold consultations with Kushiro Power Station, Nippon Beet Sugar Manufacturing, and Oenon Holdings, which are potential ammonia consumers.

Chugoku Electric became arguably the biggest winner of Japan’s first ever long term decarbonized power auction after it secured funding for 1.31 GW via a single project – Unit 3 at its Shimane Nuclear Power Plant. The 1,373 MWe advanced BWR reactor is currently under construction. Delivery of the capacity is scheduled for FY2027.

A total of 42 decarbonized power projects were chosen: 30 of these were BESS, two biomass, one nuclear, three pumped hydro storage, as well as five projects for thermal turbines modified for co-firing with ammonia and one for co-firing with hydrogen.

The govt also awarded capacity funding to 10 LNG-firing projects with capacities ranging from 463 MW to 615 MW (5.75 GW in total). Operators of those units are: Hokkaido Electric, Tohoku Electric, KEPCO (3 projects), Chugoku Electric, Tokyo Gas, Osaka Gas and JERA (2 projects).

The tender had several sub-categories, which saw allocations for 1.66 GW of capacity in battery and pumped hydro storage; and another 826 MW in co-firing projects (coal or natural gas with ammonia or hydrogen).

In terms of capacity, KEPCO won with two large pumped storage projects for its Okutataragi hydropower station (units 3 and 4), each with an output of 254 MW.

In the BESS category, Tokyo-based Hexa Renewables was granted as many as 11 projects across Japan, with a total capacity of 342 MW including in the cities of Iga (Mie Pref) and Fukuchiyama (Kyoto Pref).

Other firms awarded multiple projects included: BESS developer CHC Japan with four projects (103 MW in total); and Renova with three projects (165.5 MW).

CONTEXT: The auction was held in January 2024 and delivery of the capacity is planned for FY2027.

CONTEXT: Although this is billed as a ‘decarbonization’ tender, LNG projects are eligible to take part in the auction for another two years, with a cap of 6 GW per year versus a total of 4 GW allocated for decarbonized power. The govt has said that this was a way to help procure more baseload capacity for a transition period to lessen the reliance on coal.

TAKEAWAY: Despite renewables industry concerns that nuclear power would benefit the most from this new auction, the greatest capacity allocation (outside LNG) actually went to BESS and pumped hydro. The latter are both geared towards energy storage, rather than generation per se, which highlights the govt’s interest in securing more energy storage to balance the grid amid a wider rollout of variable renewable energy sources.

The results also indicate a willingness to grant allocations for smaller-scale BESS projects, which should support the sector as it starts to develop from its low base in Japan. BESS and other energy storage options will likely have even greater allocations from FY2026 when the govt is due to stop accepting bids for LNG-fired capacity. With a 20-year guarantee for fixed revenues, the auction is expected to prove a popular option for BESS operators. While only 24% of BESS bids were successful this time, the fact that 4.56 GW of BESS capacity was tendered bodes well for the sector’s development over the course of this decade.

Decarbonized power projects:

Company name

Project

Category

Capacity (kW)

1

ORIX

Maibara-Minoura battery energy storage project (Shiga Pref)

BESS

96,208

2

Tess Engineering

Shizuoka-Kikukawa Battery Storage System

BESS

22,077

3

Hokkaido Electric

Tomato-Atsuma Power Plant

Modification for ammonia co-firing

132,300

4

KEPCO

Okutataragi Power Station, Unit 3

Pumped storage

254,308

5

KEPCO

Okutataragi Power Station, Unit 4

Pumped storage

254,308

6

Chugoku Electric

Shimane Nuclear Power Plant, Unit 3

Nuclear power

1,315,707

7

CHC Japan

Aomori City Yamaguchi Nogi Battery Storage System

BESS

27,158

8

CHC Japan

Okayama-Mimasaka Battery Storage System

BESS

22,719

9

CHC Japan

Hokkaido-Sapporo Miyanosaka Battery Storage System

BESS

28,060

10

CHC Japan

Rubeshibe Battery Energy Storage System

BESS

25,250

11

Kobelco Power Kobe

Kobe Power Plant, Unit 1

Ammonia co-firing

131,433

12

Kobelco Power Kobe

Kobe Power Plant, Unit 2

Ammonia co-firing

132,000

13

Chubu Electric

Takane No 1

Pumped storage

68,321

14

Renova

Tomakomai BESS

BESS

70,213

15

Renova

Shiraoi BESS

BESS

39,027

16

Renova

Mori-Mutsumi 2 BESS

BESS

56,351

17

Equis Development Japan

Kashiwahara-Tomakomai Biomass Power Station

Biomass

100,000

18

Ishikari Bay New Port Biomass

Ishikari Bay New Port Biomass Power Plant

Biomass

99,258

19

Hexa Renewables

Iga City Kawanishi BESS

BESS

22,531

20

Hexa Renewables

Eniwa-Nishishimamatsu BESS

BESS

23,217

21

Hexa Renewables

Oyabe-Ishinada BESS (Toyama Pref)

BESS

39,983

22

Hexa Renewables

Kumamoto Tatsudamachi-Yuge BESS

BESS

29,615

23

Hexa Renewables

Ikari-Tagawa ② BESS (Fukuoka Pref)

BESS

22,189

24

Hexa Renewables

Shiraoi-Kita Yoshihara BESS

BESS

23,393

25

Hexa Renewables

Shiraoi-Ishiyama BESS

BESS

39,004

26

Hexa Renewables

Fukuchiyama-Araga BESS (Kyoto Pref)

BESS

36,918

27

Hexa Renewables

Matsusaka-Uegawa BESS (Mie Pref)

BESS

28,568

28

Hexa Renewables

Bibai BESS (Hokkaido Pref)

BESS

39,004

29

Hexa Renewables

Otosukebuchi-Yurihonjo BESS (Akita Pref)

BESS

37,597

30

Nozomi Energy

AEJ Oita-Usuki BESS project

BESS

37,019

31

Nozomi Energy

AEJ Fukuoka-Nogata BESS project

BESS

37,019

32

CEFH2

Miike Power Station

Hydrogen co-firing

55,300

33

Battery Park 1

Mie-Taki BESS

BESS

36,222

34

Battery Park 1

FUKO-B1 BESS generation plant

BESS

36,814

35

Higuchi-gumi

Fukushima Nishigo Solar Power Plant, Unit 1

BESS

16,535

36

Fukushima battery storage project company 1

Fukushima Nishigo Solar Power Plant, Unit 2

BESS

16,527

37

Tida Power 110

CS Aomori-Imabetsu BESS

BESS

32,677

38

Tida Power 110

CS Fukushima Ishikawa 2 BESS

BESS

37,997

39

Tida Power 110

CS Yamaguchi-Shin-Mine 2 BESS

BESS

74,669

40

Joyoshoji

Yubari-Naganuma BESS

BESS

37,515

41

JERA

Hekinan Thermal Power Station, Unit 4

Ammonia co-firing

187,334

42

JERA

Hekinan Thermal Power Station, Unit 5

Ammonia co-firing

187,315

LNG projects:

Company name

Project

Category

Capacity (kW)

1

Hokkaido Electric

Ishikari Bay New Port Power Station

LNG

551,217

2

Tohoku Electric

Higashi-Niigata Thermal Power Station, Unit 6

LNG

615,849

3

KEPCO

Nanko Power Plant, Unit 1

LNG

591,812

4

KEPCO

Nanko Power Plant, Unit 2

LNG

591,812

5

KEPCO

Nanko Power Plant, Unit 3

LNG

591,812

6

Chugoku Electric

Yanai Power Station, Unit 2

LNG

463,535

7

Tokyo Gas

Chiba Sodegaura Power Station

LNG

604,831

8

Osaka Gas

Himeji Natural Gas Power Station

LNG

565,780

9

JERA

Chita Thermal Power Station, Unit 7

LNG

589,836

10

JERA

Chita Thermal Power Station, Unit 8

LNG

589,836

JERA Nex and Australia’s Alinta Energy to develop 1GW+ offshore wind farm

(Company statement, April 24)

Newly-established JERA Nex and electricity retailer Alinta Energy plan to develop a wind farm off Australia’s southeast coast, in the Bass Strait.

Known as the Spinifex Offshore Wind Farm, proposed capacity will be 1 GW.

JERA Nex will participate via its EU-based subsidiary, Parkwind.

Australia’s Southern Ocean offshore wind zone was declared in March, though scaled back from the proposed 5,100 km2. Plans call for hosting up to 2.8 GW of offshore wind capacity.

CONTEXT: Parkwind plays a central role in JERA Nex, owning and operating seven wind farms across the globe, including in Belgium, Germany, UK, and Taiwan.

The Ministry of Land, Infrastructure, Transport and Tourism designated Aomori Port and Sakata Port as ‘base ports’ for offshore renewable energy power sites.

So far, Japan has selected operators for offshore wind power projects in a total of eight maritime areas. They are able to use ports that are specifically designated as ‘base ports’ that can handle the transportation of equipment for renewables facilities, such as offshore wind power stations. There were five ports (Akita, Noshiro, Kashima, Niigata, and Kitakyushu) with this classification before the latest decision.

CONTEXT: For the installation and maintenance of offshore wind power facilities, piers must have load-bearing capacity and the space to handle heavy equipment.

TAKEAWAY: Slowly, the govt is expanding the number of logistical facilities that the offshore wind sector can utilize, which helps to expand the number of projects that can be developed at any one time in the country.

Tokyo Gas will partner with Eku Energy to launch a grid-scale energy storage business on the island of Kyushu.

The project will have two facilities, (total capacity 55 MW). Tokyo Gas will build a 25 MW /50 MWh grid-scale energy storage facility in Oita City (Oita Pref), to be developed by its wholly-owned subsidiary Nijio.

Tokyo Gas also signed a 20-year offtake agreement with Eku Energy that grants operational rights for a planned 30 MW asset in Miyazaki City (Miyazaki Pref).

Eku Energy’s asset will have a 4-hour duration (120 MWh). The firms plan to begin construction later in FY2024; commercial operations begin in FY2026.

CONTEXT: The project seeks to utilize electricity generated from renewable power sources that would otherwise go unused; this is a way to prevent electricity curtailments that are a common solution for balancing energy surplus on Kyushu.

ANRE decided to hold capacity market auctions in FY2024 (for FY2025 supply capacity). Bids open on May 10 and run to May 22.

Officials seek to have about 184 GW of capacity potentially available in the power system this fiscal year and 184.2 GW in FY2025. However, it is estimated that in Hokkaido, Tokyo and Kyushu areas there are potential shortfalls on the supply side based on annual plant outage assessments.

According to ANRE’s estimates, the three areas need additional available supply of:

TOCOM has seen trading in futures contracts for this summer jump more than 8 times the volume of last month thanks to the introduction of a market-maker system. There were 2,126 contracts traded in the first 24 days of April.

The exchange is trialing the system through June, hoping to encourage more hedging transactions during the summer’s peak electricity demand period.

CONTEXT: Market makers step into the market as a counterparty to ensure those providing bid and ask prices have a trading partner in case there are none available. As of April, six companies are participating in TOCOM’s electricity futures market.

JEPX spot prices halved in 2023 as demand headed downward

(Denki Shimbun, April 23)

The JEPX spot market saw contracted volume for FY2023 fall by 17.9% YoY, to 261.49 TWh.

This was due to the impact of the end of gross bidding from Oct 2023. The ratio of contracted volume to electricity demand also fell below 30%.

The yearly average price fell by ¥9.67 to ¥10.74. The highest monthly average system price was ¥14.20 in November. While demand increased due to lower temperatures, many power supply facilities were undergoing inspections and repairs during the off-season.

There was also a noticeable drop in electricity demand, YoY, which was 5.1% lower in December, 4.3% lower in January, and 0.1% lower in February.

Prices showed a clear trend of being higher in the east and lower in the west. Prices in east Japan ranged from ¥11.33 to ¥12.20, and in west Japan from ¥9.14 to ¥11.14.

Prices in the nine areas peaked on Sept 20-23 at ¥50 due to a decrease in solar power from stormy weather; also, summer heat was severe and demand did not fall even in the evening.

A consortium comprising trading, power and gas firms plans to invest ¥5 billion in startup Enechain, which runs an online electricity exchange.

The goal is to lower wholesale prices and create an environment suitable for small power retailers. The companies plan more trading on the exchange, as well as to have affiliated power retailers buy electricity using it.

The consortium comprises: JERA, Tokyo Gas, Osaka Gas, KEPCO and Chubu Electric groups, Sumitomo and Mitsubishi Corp. It also includes Soros Capital Management, Minerva Growth Partners and Ireland’s Energia Group.

The group will take a 14% stake through a private share placement.

CONTEXT: Over the next three years Enechain seeks a tenfold increase in the amount of electricity traded on its platform to 500 TWh / year, about 60% of Japan’s power demand. The exchange employs mainly forward contracts and provides service to more than 250 firms.

Genkai Town mulls putting hand up to host nuclear waste final disposal site

(Japan NRG, April 26)

Genkai Town (Saga Pref) is reviewing a petition to put its hand up as a candidate to host the country’s future final nuclear waste disposal facility. Genkai hosts a NPP owned by Kyushu Electric and it would be the first municipality with a nuclear station to also be reviewed as a site for waste storage.

The town’s special committee and then its assembly both voted to move forward with the initiative, which now has to be approved by the mayor before it is submitted to the national authorities. Mayor Wakiyama Shintaro has told local media he will decide on this in early May.

Saga Pref Governor holds a negative stance on the matter.

CONTEXT: Submitting the town as a potential candidate for the site begins a lengthy review process. The first stage of that is documents-based research. It’s conducted by the Nuclear Waste Management Organization of Japan (NUMO). During this phase, NUMO considers previously documented data on the area’s geological features.

TAKEAWAY: Since NUMO started the search for a final disposal site more than 20 years ago, only two localities (Suttsu and Kamoenai, both in Hokkaido) have started the process. The Hokkaido municipalities are now in the second stage of the review process.

Accepting the survey brings state funding to the municipality, which helps revitalize the local economy. Yet, according to a state map indicating potential waste storage site locations, Genkai is not suitable. Even if the town’s authorities overcome any opposition from residents and the prefectural governor, and the survey goes ahead, there’s no guarantee it will ever be completed. The entire three phases could easily take more than 10 years, leaving space for cancellation.

Chugoku Electric began geological excavation surveys to explore building a spent nuclear fuel interim storage facility in Kaminoseki, Yamaguchi Pref.

CONTEXT: Since August 2023, the company has been conducting preliminary literature research. This first step studies records of earthquakes, tsunami, and factors like humidity and climate. In December, the company submitted a forest clearing notification to Kaminoseki and began cutting the forest.

TAKEAWAY: The Kaminoseki interim storage facility is crucial for both Chugoku Electric and KEPCO. If the surveys continue and the facility is built, Chugoku Electric could use it for its Shimane NPP. Also, it can help KEPCO fulfill promises to ship spent nuclear fuel out of the prefecture – promises that underpin its current NPP operations.

Nomura Research Institute assessed the economic impact of restarting Units 6 and 7 at Kashiwazaki-Kariwa NPP. It analyzed three scenarios: restart, decommissioning, and complete shutdown.

Restarting the plant could bring ¥440 billion in economic gains over 10 years; compared to ¥298 billion if there’s a shutdown; and ¥126 billion if decommissioned. Over 10 years, revenue from taxes and subsidies totalled ¥322 billion in the first scenario.

Niigata Pref’s governor said these surveys are important for discussions, but economic profits are not the only thing to consider.

KEPCO said most of Mihama NPP Unit 3 meets long-term operations standards.

The International Atomic Energy Agency also agreed, with a review conducted by its long-term operation team SALTO. Yet, it had recommendations for more inspections and some improvement works.

While compliance with SALTO safety standards is not a condition for operation, KEPCO had requested it.

CONTEXT: KEPCO has resumed operation of Unit 3, which in 2021 was Japan’s first NPP to exceed 40 years of service.

Chugoku Electric obtained NRA approval for changes to safety regulations on aging equipment for Unit 2 at the Shimane NPP.

This approval follows the establishment of a long-term facility management policy.

CONTEXT: Unit 2 has been shut since 2012, and Chugoku Electric plans to restart operations in August. When operating a NPP for more than 30 years, approval for safety regulations must be obtained every 10 years.

Mitsui & Co. is exploring whether to join a $7 billion LNG project in Ruwais, UAE. This would be in collaboration with ADNOC and other international partners.

The project will begin operations by 2030, producing about 10 million tons of LNG per year. It could cover 15% of Japan’s yearly demand.

Mitsui’s investment could be 10%, with ADNOC owning 60%. Other partners include Shell, BP, and TotalEnergies. They’ll sell the LNG to customers in Europe and Asia.

CONTEXT: Recently, ADNOC inked a deal with Germany’s SEFE for 1 Mtpa of LNG over 15 years. This follows a similar deal with China’s ENN Natural Gas.

TAKEAWAY: After Nikkei reported the discussions of this deal, Mitsui issued a statement saying a final decision has not been made. One is likely to be made in May. If so, it would mark a slight resurgence in Japanese LNG investment over the past six months or so. In early April, Mitsui’s biggest domestic rival, Mitsubishi Corp, agreed to invest in MidOcean Energy, an LNG firm owned by U.S investor EIG and with stakes in a number of Australian LNG projects. In February, JERA committed $1.4 billion to the Scarborough gas project in northwest Australia that’s being developed by Woodside Energy, following a $880 million investment in the same project by LNG Japan, the JV between trading houses Sumitomo Corp and Sojitz. Mitsui itself extended its involvement in an Oman LNG project just in October 2023.

Such a concerted effort to invest in new and existing projects, which has included several in the U.S., suggests that Japanese buyers see a slightly different demand picture to the one painted in the country’s Basic Energy Plan. The current version of the Plan says LNG use in power generation will drop by half by the end of this decade in Japan. The Plan is due to be revised this year.

METI’s long-term refined oil products demand forecast over FY2024-2028 showed that steep declines of 16.3-19.1% are expected from sulfur fuel oil, also called heavy oil; with a decline of only 1.4% for jet fuel and naphtha.

The energy transition, as well as declining population, will propel the shift away from fossil oil. IMO rules on ship fuel, changes in freight industry practices, and the shift away from plastics, will also have an impact.

In FY2028, the total oil products demand is seen at 132 million kiloliters (829 million barrels), down 7.6% from 143 million kl in FY2023. The figures do not include liquefied petroleum gas.

As of April 21, LNG stocks of 10 power utilities were 2.05 mln tons, up 26.5% WoW (1.62 mln tons). But this is 16% down from the end of April (2.44 mln tons) in 2023, and 1.49% down on the past five-year average of 2.02 mln tons.

Golden Week began and many companies will close their offices from April 27 to May 6. During May to July, the temperatures are expected to be higher than average, especially in southern Japan and Okinawa, with sunny and dry days. The rainy season is forecast to begin in June, except in the Tohoku and Hokkaido areas.

ANALYSIS

BY JOHN VAROLI

Blue vs Green Hydrogen and its Impact on JERA

The debate over the economic feasibility of ‘blue hydrogen’ versus ‘green hydrogen’ appears to be approaching a decisive moment in the global conversation about clean forms of energy. And developments in the U.S., specifically the State of Texas, are at the center of this issue.

Those espousing green hydrogen say that the best solution is to focus on total emission reductions from the very start. Meanwhile proponents of blue hydrogen say that it’s more important to allow low-carbon facilities and infrastructure to be built and scaled quickly.

In the past few months, private opinions have made their way into the public realm, with directors of major legacy energy companies criticizing green hydrogen as economically infeasible because of high production costs.

Instead, they’re pushing for blue hydrogen as a low-carbon solution to meet current market demands. Blue hydrogen is made from natural gas, while green hydrogen, which has more backing from G7 governments, relies on electrolyzing water with solar or wind power. Hydrogen and ammonia do not emit CO2 when burned.

How this issue pans out will impact Japan’s power sector in general and Japan’s largest utility, JERA, in particular, as it envisions upgrading coal-powered thermal plants to run on ammonia. JERA needs the ammonia to have as little carbon footprint as possible to claim that its strategy is “clean”. But it also needs the new fuel to be affordable and available at scale. As such, the outcome of the debate in Texas will have a bearing on both the economics and the optics of Japan’s power sector decarbonization.

Ammonia co-firing with coal

JERA, which is a 50/50 joint venture between TEPCO and Chubu Electric, produces nearly 30% of all electricity in Japan. The company has 26 coal-fired power plants, mostly in and near the cities of Tokyo, Kawasaki, Yokohama, and Nagoya.

At the start of this month, JERA started what it claims is a world-first demonstration of the co-firing of ammonia and coal at a large-scale, commercial thermal power plant. Should it go well, by 2027 JERA aims to implement ammonia co-firing on a regular, commercial basis at its Hekinan power station.

In 2028, the ratio of ammonia in the fuel mix at one of the units of the Hekinan power station would be raised to 50%. JERA wants to gradually increase the ammonia ratio, eventually reaching 100% in all its coal power plants at home, and possibly export the technology to countries in Southeast Asia. The timeline on these plans extends into the 2030s.

While JERA is also actively expanding into renewable energy, and launched its brand new global renewables subsidiary JERA Nex earlier this month, the company’s decarbonization strategy largely rests on shifting existing thermal plants from fossil fuels to clean-burning ammonia or hydrogen. To do that, JERA needs to create a global ammonia supply chain since the vast majority of the ammonia produced today is used to make fertilizer and there’s little spare capacity at existing facilities.

Toward that goal, JERA has inked a number of deals with major ammonia producers. Of these, just one is for green ammonia – the agreement with India’s ReNew E-Fuels. The scale, however, is relatively small: just 100,000 tons of ammonia / year.

All the other projects that JERA has explored to date are based on the ‘blue’ approach, which involves steam reforming of natural gas, and capturing the CO2 that’s created in the process.

In the blue ammonia space, JERA has many more options in terms of suppliers and volumes. JERA is in talks with the world’s top ammonia producer, CF Industries in the U.S., and Yara Clean Ammonia, a unit of Norwegian chemicals giant Yara International. Both are planning new ammonia production lines situated along the U.S. Gulf coast, each possibly producing more than one million tons annually.

JERA might take a stake in the Gulf coast projects, as well as sign an offtake contract for as much as half a million tons of ammonia a year. JERA Chairman Kani said that he’d like to see “at least double-digits” stakes when investing in U.S. ammonia projects.

The project that has perhaps become the focal point in the blue versus green ammonia / hydrogen discussion, however, is ExxonMobil’s Baytown Complex in Texas, where JERA is also exploring participation. That project hopes to produce 900,000 tons of hydrogen per year, which would be used to produce about one million tons of ammonia.

ExxonMobil claims that the Baytown Complex will be the world’s largest facility of its kind, and hopes to begin production as soon as 2028. But the multi-billion-dollar investment decision on the project depends in large part on how much the operator can secure in U.S. subsidies. According to ExxonMobil, it needs the subsidies for its blue project to be closer to what the government offers for green projects.

If Exxon wins, this could help decide the outcome of the blue versus green ammonia debate, at least for the near-term. If they lose, companies like JERA might slow their shift from coal to ammonia, fearing a lack of adequate (and affordable) supply.

Color hydrogens do battle

When JERA announced plans to start commercial-scale co-firing at one of the units of its Hekinan coal power plant, it put out a contract offer in 2022 for 500,000 tons of ammonia supply per year. This was possibly the largest ever ammonia contract outside of the fertilizer sector. And yet, this volume would only cover one year of operations at one unit of one thermal power plant at the co-firing ratio of 20% ammonia – 80% coal. Effectively, ammonia would fuel 200 MW of capacity.

For the power company to ramp up to 50% ammonia firing, and to spread the technology to other thermal power plants, it will need to lock in a serious amount of fuel supply. Projects like the Baytown Complex offer this kind of scale, but according to Exxon it needs tax credits for it to work commercially.

The U.S. government’s Inflation Reduction Act (IRA) was passed to address this exact issue – of bridging the cost gap with existing fuel sources. However, the IRA strongly favors green hydrogen. Under the IRA, the amount of tax credit declines as CO2 emissions increase during production. Exxon wants the IRA to treat blue and green hydrogen as equals.

Move now or wait for Green H2?

Over the past several months the heads of major companies such as Exxon, Saudi Aramco and trading company Gunvor have gone public with their thoughts that the high cost of green hydrogen production will prevent it from displacing oil and natural gas any time soon. And waiting for green H2 to arrive would delay the energy transition.

Saudi Aramco CEO Amin Nasser says that the cost of green hydrogen is equivalent to $400 for a barrel of oil, which is roughly four times the current price. To make green H2 work, it needs sizable state incentives and offtake agreements of at least 15 years.

Meanwhile, Exxon CEO Darren Woods told the CERAWeek energy conference that clients were not yet prepared to pay for the costs associated with emissions reductions. As such, Woods said he could only see Exxon producing hydrogen if the IRA guidelines were amended to allow tax credits for methane-derived hydrogen.

International fertilizers and chemicals giant OCI Global said resolutely that it will move forward with hydrogen, but in its ‘blue’ format. The company is building one of the world’s largest blue hydrogen-derived ammonia plants in Texas, to cost nearly $1 billion.

“We’re not going to pause our business just to wait for this technology [green hydrogen] to scale, which we think will take five or ten years,” said Bashir Lebada, head of OCI’s methanol and fuels business.

Conclusion

As a buyer, rather than producer, JERA and other Japanese companies that are keen to use ammonia are largely agnostic on the colors of hydrogen and the production methods. At the same time, Japanese buyers can only invest in and sign offtake deals with projects that are deemed feasible and that deliver at scale.

Whether blue ammonia or hydrogen emerges victorious in the U.S. thanks to the lobbying efforts of Exxon is not something that Japanese buyers will affect. Still, the desire of JERA and others to move to ammonia firing sooner, rather than later, could play a role in the debate.

The irony of ever greater pressure on companies to decarbonize quickly may be that it brings more ‘blue’ options to the fore as realistic pathways, while pushing ‘green’ options into a supporting role.

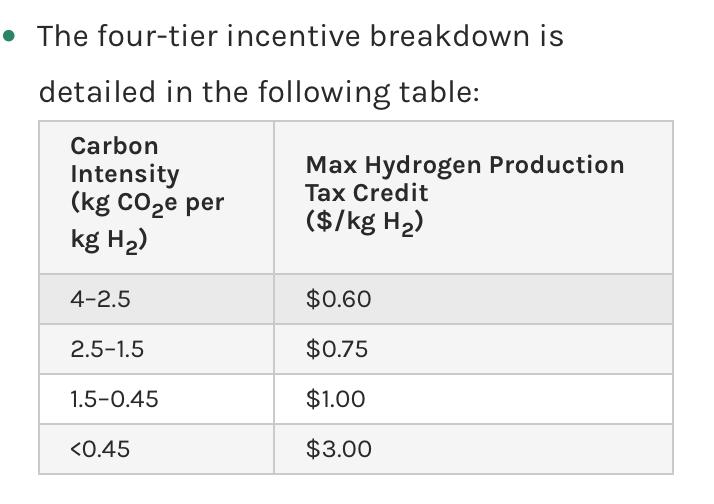

BOX: The math of subsidies

The Department of Energy has said it will award up to $8 billion in grant funding to develop several hydrogen hubs across the U.S. In December of last year, the IRA set up a Clean Hydrogen Production Credit program that has four technology-neutral credit tiers based on the emissions rate of various hydrogen production processes.

To qualify, hydrogen must be produced with less than four kilos of CO2-equivalent per kilo of hydrogen. The guidelines on production, however, only refers to green hydrogen.

The credits are offered only to projects that can begin construction by 2033, and are valid for 10 years starting when a hydrogen production facility enters service. The credit ranges from $0.60 to $3 per kilo of hydrogen produced, depending on the lifecycle emissions of the hydrogen production.

The U.S. energy strategy calls for hydrogen to be produced for $1 per kilo by 2031. Today, the levelized cost of green hydrogen is over $4 per kilogram, according to Bloomberg New Energy Finance, but it could meet the national target should the project qualify for the maximum credit amount.

In the case of blue hydrogen, however, most projects would only be able to qualify for a tax credit of up to $1 per kilo, bringing the cost range of blue H2 to $1.0-$1.5 per kilo. As such, the U.S. Department of Energy estimates that most blue hydrogen will exceed the $1 target by 2031. The DOE also casts doubt on whether most blue projects will meet the criteria for ‘clean hydrogen’ and thus qualify for credits.

The saving grace for blue hydrogen, however, may be an additional tax credit known as 45Q, which provides up to $85 per ton of CO2 that’s captured and permanently stored. Making the subsidies math work will be Exxon’s priority in the coming year or so.

ANALYSIS

BY MAYUMI WATANABE

How Japanese Steel is Turning Green Part II : Reducing the Problem to its Core

If Japan’s fully behind a hydrogen economy, then it’s even more fully behind a net-zero shift in steelmaking. For all the headlines around the ‘hydrogen economy’, the steel sector is due to get almost 50% more government green R&D funding (¥427 billion) over the course of the next ten years.

Of course, hydrogen will play a vital role in the transformation of steelmaking from the centuries-old process based on coking coal. But it’s not the only component in what is widely touted as the age of ‘green steel’. A number of innovations are in the works in Japan’s steel factories, both in heat control, emissions absorption, and power sources.

Nearly all the new technologies proposed and tested are still in the pilot and demonstration stage, but the development is further advanced than most realize. One of the biggest factors that will influence the next steps in ‘green steelmaking’ is the persistent conundrum of price. After all, technological breakthroughs will mean nothing if they can’t find willing clients and supportive governments.

In this second part of the “Green Steel in Japan” series, we look at how the steel sector and the government are wrestling with obvious disparities between what they ‘need’ the price of clean steel technologies to look like and what they are in practice. The next few years require radical mind shifts, either on the side of producers or buyers, or both.

Another way to make steel

In the first part of this series, we looked at the way the majority of steel is produced in Japan – via iron ore use in blast furnaces. There is another steelmaking process that involves hydrogen that’s known as direct iron reduction (DRI). This approach uses shaft furnaces, which operate at a lesser temperature than the blast furnaces, but still require 900-1,000 C.

The DRI method relies much more on hydrogen as the sole agent for iron reduction. In this approach, the natural gases in the furnace comprise 60-80% hydrogen. Presently, around 10% of the world’s steel is made using natural gas as a reducing agent. It’s especially popular in the Middle East and the U.S. where natural gas is abundant.

In Japan, JFE Steel tested natural gas-triggered reduction two decades ago but stopped due to economic reasons. However, Japanese steelmakers have access to this technology overseas. Kobe Steel’s U.S. affiliate Midrex Technologies is the world’s largest shaft furnace builder. Kobe acquired Midrex in 1983.

Last year, the Japanese steel sector became more active in examining how DRI could be more widely used. Kobe Steel tested how the technology can be applied to its Japanese blast furnace-dominated facilities. The company used DRI at its Kakogawa furnace, deploying the method to pre-treat iron instead of iron ore. As a result, Kobe Steel reported a 25% CO2 reduction compared to the usual process of treating iron ore from scratch.

Meanwhile, JFE Steel has started construction of a small 15 kg of iron ore per hour shaft furnace at its Chiba Works, and plans to begin test runs in FY2024. In 2025, Nippon Steel will set up a 1 ton per hour shaft furnace at the Hasaki R&D Center.

Quality issues

Ore quality is a major challenge for Japanese steel firms keen to employ DRI. Ore with a high iron content of 62-65% fits DRI better. Such ores are found in the Nordic regions and South America. Japanese firms, however, tend to import Australian and Brazilian ores of grades that are in the region of 58-65% iron content, and these are less suitable for DRI.

The above is one region where European competitors such as Thyssenkrupp and SAAB have raced ahead in green steelmaking. With better access to DRI-ready ores, Thyssenkrupp and SAAB say they can commercialize green steel that uses hydrogen as early as 2026-27.

Barring a complete switch of iron ore supplies, which would be a multi-year and vastly expensive process, Japanese steelmakers need to make the DRI process work with the raw materials that they can already access. As such, JFE Steel has embarked on experimentation of DRI with ores of lower iron content (i.e., 58-62%). It has been the most adventurous of Japan’s steel firms in this regard, trialing tactics such as directly feeding low-grade chromite and molybdenum concentrates into the furnaces to compensate for weaker iron concentration.

Unfortunately for JFE, this approach has not yet yielded fruit. It has resulted in massive releases of sulfuric gas, and so the steelmaker has to find other options.

Other technological steps also need revising. The process after removing oxygen from iron ore also needs a re-think. After heating, the metallic iron in blast furnaces melts and becomes more malleable. The hot near-liquid metal can be easily moved to the next process of refining, rolling and shaping. Meanwhile, iron created with hydrogen treatment is not as easily manageable.

Last year, a new project was added to the Green Innovation Fund program, which is to develop a new furnace called a “melter” for treating the iron after DRI. Over the past winter, the government solicited proposals from companies keen to develop such a new furnace, and in April awarded the project to Nippon Steel and The Japan Research and Development Center for Metals.

FY2028 is the deadline to complete development of an 880,000 ton per year DRI production process and equipment. GIF will provide ¥23 billion. By 2030, the Super Course50 method should be operational at Nippon Steel’s Kimitsu Works and Course50 elsewhere.

Calculating H2 demand

Whichever approach Japanese steelmakers use – DRI, Course50, or similar – the common component underpinning the plans is hydrogen.

The Japan Iron and Steel Federation (JISF) believes that steelmakers will need 1,000 Nm3 (90 kg) of hydrogen for one ton of steel in blast furnaces, while DRI would require an additional “several hundred Nm3”.

These numbers are higher than the estimates for hydrogen-based green steelmaking in Europe, with the EU studies quoting figures as low as 50 kg. However, each company’s furnaces are set up differently, and the quality of iron ore, as well as other processes, can impact hydrogen requirements.

– Assuming that Nippon Steel fully switches its 5.7-million-ton a year Kimitsu Works to the Super Course50 method, it would require about 500,000 tons of hydrogen a year.

– Based on JISF guidance, Japan NRG assumes that the DRI process in Japan would require 1,300 Nm3 (117 kg) for one ton of steel. That would mean that a one-million ton per year shaft furnace needs 100,000 tons per year of hydrogen.

These numbers are, of course, a maximum projection. Actual demand would be much lower since blast furnaces with current Japanese technologies would not run on 100% hydrogen.

Cost

JISF also says that the steel sector needs hydrogen prices at ¥8/ Nm3, which is less than half of the already low ¥20/ Nm3 government target for 2050. The numbers are completely divorced from the current prices offered by hydrogen producers, which see even the government’s target as already unrealistic under today’s costs.

One way that the market and steel companies may bridge this gap, however, is by changing the criteria for what kind of hydrogen is needed for steelmaking.

Blast furnaces are inhibited by various gases. As such, unlike fuel cells, furnaces do not require hydrogen of 99.97-99.99% purity. They may tolerate 80% hydrogen so long as it is sulfur-free. This opens opportunities for producers to make cheaper, low-purity gas that would create a new tier in the hydrogen market.

If this tier gains momentum, through being accessible in price for Japanese steelmakers, this could become the hydrogen product that is more likely to drive near-term demand, and thus act as a benchmark for both low and high-purity hydrogen contracts in Asia.

It’s likely that the European and North American markets will evolve differently, due to their widespread plans for DRI based on higher iron ore grades. Still, even those steel producers will have to adapt. The world’s iron ore deposits tend to average 56-57%.

Similarly, there is a lack of clarity over the type of hydrogen required for DRI that JFE Steel plans to explore in its studies around low-grade iron ores.

Japanese steelmakers building DRI-enabled shaft furnaces may use natural gas as the reduction agent in the interim until hydrogen prices reach realistic levels. This could lead the steel sector to pursue a similar kind of dual-fuel strategy to that currently tested by the power generation sector.

High hydrogen costs could also push steelmakers to increase their reliance on carbon capture. According to the 2021 Japan Science and Technology Agency policy proposal, the estimated cost of carbon capture and separation is ¥15/ kg, provided that carbon released at blast furnaces is captured fully.

The cost of pig iron production, without carbon capture, was ¥40-50/ kg. Reducing the capture cost will definitely help make Japanese steel greener.

Conclusion

With so many variables, it’s too early to call what ‘green steelmaking’ will eventually look like, with many regional and company variations. The multitude of approaches shows that there are at least a few pathways to reducing the CO2 footprint of the steel sector and that these may be more local than global.

Japan’s steelmakers are likely to continue signaling their intent to move towards a hydrogen-based future for their industry. But they know that they have (and must pursue) other options. The technological battle is still wide open.

ASIA ENERGY REVIEW

BY JOHN VAROLI

This weekly column focuses on energy events in Asia and the Pacific

ASEAN / Energy transition

Regional collaboration through power interconnectors, hydrogen networks and energy storage could reduce the cost of decarbonisation among ASEAN member states by $800 billion, says a report by DNV.

Australia / Renewable energy

The govt launched a 6 GW renewable energy tender for the National Electricity Market under the Capacity Investment Scheme, the country’s largest renewables tender. About 2.2 GW of capacity, which could power over one million households, is planned for New South Wales.

China / Carbon market

Fitch Ratings said that China’s government could reduce the free emission allowance for key emitters and place a cap on the quote that can be carried over to 2025. The expected tightening of China’s national carbon market could drive demand for renewable energy.

China / Coal power

China’s coal-fired power sector is set for another year of profit as coal prices drop, reports S&P Global Ratings. Spot coal prices domestically and internationally were down by about 11% due to abundant supply. In Q1 of 2023, the average spot price was 4% to 5% lower than 2023’s annual average.

EVs

In 2024, EV sales in China are projected to reach 10 million, about 45% of total car sales. In the U.S., about 11% of cars sold are expected to be EV. In Europe, despite the phase-out of subsidies, EVs might account for about 25% of cars sold.

Indonesia / Energy transition

The country’s sovereign wealth fund, the Indonesia Investment Authority, will invest up to $1 billion in 2024. Green energy will be a priority, such as investment in the EV ecosystem and geothermal energy, and financing early retirement of coal-fired power plants.

Malaysia / Oil & Gas

Malaysia’s Sapura Energy will sell its entire 50% stake in oil and gas upstream company SapuraOMV to TotalEnergies for $705 million. The deal, which includes a cash payment of $530 million, will leave TotalEnergies as the sole owner of SapuraOMV

Offshore wind

The global offshore wind sector added an additional 9.8 GW capacity in 2023, across 25 new offshore wind farms, according to World Forum Offshore Wind. In 2022, that figure was 9.4 GW. Now the total global offshore wind capacity is 67.4 GW.

South Korea / Oil & Gas

The Korea Energy Terminal, a JV between Korea National Oil Corp (KNOC) and utility SK Gas, launched a new oil and gas import facility. Located in the Ulsan Free Economic Zone, the facility will also become a center for hydrogen technology development.

Taiwan / Offshore wind

Ørsted launched the Greater Changhua 1 and 2a offshore wind farm, with a total installed capacity of 900 MW, making it East Asia’s largest offshore wind project.

2024 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

January

First market trading day (Jan 4)

IEA “Renewables 2023: Analysis and Market Forecast to 2028” released (Jan 11)

Renewable Energy Exhibition (Jan 31 – Feb 2)

Taiwan presidential election (Jan 13)

Japan’s Diet convenes

IEA “Electricity 2024 / Analysis and Forecast to 2026” released (Jan 24)

February

CFAA International Symposium (Feb 2)

India Energy Week 2024 (Feb 6-9)

Lunar New Year (Feb 10-17)

Indonesia presidential election (Feb 14)

Japan-Ukraine Conference for Promotion of Economic Reconstruction (Feb 19)

FIT/FIP solar auction (Feb 19 – March 1)

Smart Energy Week (Feb 28-Mar 1)

March

Announcement of auction result for Offshore Wind Round 2 (for Akita Happo-Noshiro Project)

Onshore wind auctions (March 4-15; results on March 22)

International LNG Congress (LNGCON) 2024, Milan, Italy (March 11-12)

Russian president election (March 15-17)

World Petrochemical Conference, Houston, TX, USA (March 18-22)

IAEA Nuclear Energy Summit @ Belgium (March 21)

Ukraine presidential election (due before March 31)

Happo Noshiro, Murakami-Tainai, Oga-Katagami-Akita and Saikai-Eshima wind project auctions close (June 30)

July

Tokyo governor election (July 7)

7th Basic (Strategic) Energy Plan draft published (expected)

August

7th Basic (Strategic) Energy Plan draft presented to Cabinet (expected)

September

Global Offshore Wind Summit Japan 2024, Sapporo, Hokkaido (Sept 3-4)

The United Nations Summit of the Future (Sept 22-23)

Gastech 2024, Houston, TX (Sept 17-20)

IAEA General Conference

GX Week in Tokyo (expected late Sept to October)

Asia Green Growth Partnership Ministerial Meeting

Asia CCUS Network Forum

International Conference on Carbon Recycling

International Conference on Fuel Ammonia

GGX x TCFD Summit

October

IEA World Energy Outlook 2024 Release

BP Energy Outlook 2024 Release

Innovation for Cool Earth Forum (expected)

Connecting Green Hydrogen Japan 2024 (Oct 16-17)

Japan Wind Energy 2024 Summit (Oct 16-17)

Solar Energy Future Japan 2024 (Oct 16-17)

Japan Mobility Show (Oct 25-Nov 5)

November

US presidential election (Nov 5)

COP 29 in Azerbaijan (Nov 11-22)

Abu Dhabi International Petroleum Exhibition Conference (ADIPEC) 2024, Abu Dhabi, UAE (Nov 11-14)

APEC 2024 @ Lima, Peru

International Conference on Nuclear Decommissioning (TBD)

G20 Rio de Janeiro Summit (Nov 18-19)

Offshore Energy Exhibition & Conference (OEEC) 2024, Amsterdam, the Netherlands (Nov 26-27)

Biomass & BioEnergy Asia Conference (TBD)

European Biomethane Week 2024

December

Last market trading day (December 30)

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.