Grid-scale battery energy storage systems (BESS) were the biggest winners in Japan’s first ever long-term decarbonized power auction in January. But how can we be sure that all of the winning projects will come online? And how will these results affect the next auction? Japan NRG examines the rewards and challenges that developers may face.

Until the mid-1990s, Japan’s electric power sector was dominated by 10 regional companies that were responsible for all power generation, distribution and sales. Since then, the nation’s power industry has undergone significant reforms that seek to foster competition. We review the current state of electricity markets, look at the main structures and platforms, and how they are changing.

ASIA ENERGY VIEW

A wrap of top energy news that impacts other Asian countries.

EVENTS SCHEDULE

A selection of events to keep an eye on in 2024.

JAPAN NRG WEEKLY

PUBLISHER K. K. Yuri Group

Editorial Team Yuriy Humber (Editor-in-Chief) John Varoli (Senior Editor, Americas) Mayumi Watanabe (Japan) Wilfried Goossens (Events, global) Kyoko Fukuda (Japan) Magdalena Osumi (Japan Filippo Pedretti (Japan) Tim Young (Japan)

PM Kishida called for a new 2040 energy and climate strategy called ‘GX 2.0’. METI and GX Minister Saito will form the “GX 2040 Leaders Panel” to write it.

Kishida explained that the first iteration of GX, or ‘GX 1.0’ was about setting regulatory, fiscal, tax, market and international certification frameworks for carbon pricing, as well as outlining a ¥150 trillion GX investment program to expand low-carbon power sources, etc.

The next iteration, GX 2.0, will clarify realistic roadmaps to 2040 to cope with the challenges around meeting the nation’s final 2050 carbon neutrality goal.

Issues to address include the expansion of AI data centers that are now seen as a matter of national security. There are unprecedented new requirements to provide high quality decarbonized power supplies in distributed locations in a short timeframe.

Kishida also called for a review of how Japan can accelerate efforts to reduce its reliance on fossil fuels – especially due to an expected increase in the volatility of oil and gas prices, in part caused by “the situation in the Middle East and other factors.”

Kishida mentioned an acceleration of divestments from new upstream oil and coal projects as another factor impacting prices and supply.

Thus, Japan needs to look into carbon pricing, long-term decarbonized power source investments and securing strategic backup power sources, he said.

The GX 2.0 strategy should accommodate changes in industrial structures and their locations, technology breakthroughs, and consumer behavior, coming up with realistic paths to decarbonization that can be shared by the public and private sectors.

CONTEXT: Under the Paris Agreement, governments are required to submit an updated nationally determined contribution (NDC) plan to the UN by 2025. Japan’s present commitment is a 46% cut in emissions by 2030 over 2013’s levels. The next NDC needs to be more ambitious.

TAKEAWAY: The sudden emergence of a GX 2.0, with arguably the first iteration of the plan yet to fully take root, shows PM Kishida feels a sense of urgency. The reasons may be several, from the need to demonstrate positive action domestically amid weak polling numbers and to the international community ahead of the G7 meeting and the latest COP climate summit. However, the biggest driver is likely to be the realization in government that the country’s digital strategy will generate new and substantial new energy demand that may not have been considered within the current GX program. We will cover this issue in more detail in upcoming reports.

On May 15, the Advisory Committee for Natural Resources and Energy officially launched discussions on the 7th Basic Energy Plan, a national energy strategy. The Committee will align with another panel writing the GX 2.0 2040 strategy.

The 2040 strategy will show directions for energy supply security, decarbonization and investments; Basic Energy Plan discussions will focus on energy mix details and strategies for each energy and power source.

Key discussion points include the potential to expand renewable energy sources further, the share of nuclear in the national power mix, and possible increases in green power demand from data centers.

METI set its “2024 Strategy for Technologies to Drive Energy Savings and Shift to Non-fossil Energy”, identifying 28 base technologies that need rapid development.

NEDO will provide financial support for their development. The technologies are applicable to hard-to-abate sectors as well as for transport and homes.

Examples are ferro-coke development in steelmaking, hydrogen-fueled transport, heat pumps and energy management at industrial plants, as well as zero-emission buildings and houses.

CONTEXT: METI annually picks key climate technologies and their development roadmaps. Some of these technologies have been on the GX agenda for a while.

METI Minister held an online meeting with Saudi Arabia’s Minister of Investment and a separate meeting with the Saudi Arabian ambassador to Japan ahead of the May 20 Crown Prince Salman’s visit to Tokyo.

METI launched a 10-member panel to clarify legal issues for emissions trading systems. Tokyo University professor Takamura Yukari chairs the group.

The panel will study how the EU emissions scheme performs if the Japanese systems were applied, and identify legal issues.

The panel won’t design the emissions trading scheme; another panel will be set up to build on the legal issue discussions. It will publish recommendations in September.

Parliament approves CCS, low-carbon hydrogen acts

(Parliament statement, May 17)

On May 17, the Diet passed bills on carbon storage and support measures to promote low-carbon hydrogen.

The Act on Carbon Dioxide Storage defines licensing, exploration and other processes for CCS operations. The Mining Act, Radioactive Substance Disposal Act, Marine Pollution Act, Bankruptcy Act, etc, were also amended to synchronize with the Carbon Dioxide Storage Act.

The Act on Promoting Supply and Use of Low-Carbon Hydrogen for a Smooth Shift to Low Carbon Growth Oriented Economic Structure will allow METI to provide subsidies and regulatory support to parties in the low-carbon hydrogen supply chains.

Central Japan Railway Company, Hitachi and ENEOS inked a basic agreement to develop supply networks to fuel hydrogen train systems.

They chose methylcyclohexane (MCH) compounds as the medium to carry hydrogen at room temperatures.

They will explore transport, storage, fueling of trains, transport of hydrogen on trains and consuming the gas on board.

CONTEXT: The key technology for the supply chain is retrieving hydrogen from MCH that’s not as straightforward as converting hydrogen into MCH, and making compact equipment to perform the chemical reactions, whether to perform them on or off the trains.

Japan plans to accelerate nuclear fusion technology development, to catch up with the U.S., China, and the U.K., all of which have plans to test fusion power by the 2040s.

Japan will bring forward new legislative and testing timelines in its June economic and fiscal policy.

CONTEXT: Fusion technology is more costly than renewable energy and traditional nuclear power. It requires advanced materials and large equipment.

JERA and INPEX will do a preliminary study on capturing CO2 from JERA’s operations in Japan and transporting it to Australia for storage.

The study will examine the entire value chain, from CO2 separation and capture in Japan to transportation and storage in Australia.

CONTEXT: Australia has geographical sites suitable for CO2 storage, and is working on regulations to develop CCS businesses and receive CO2 from abroad.

TAKEAWAY: While Australia has been fostering international cooperation on CCS, limited funding and a lack of infrastructure impede plans for a Japan-Australian CCS value chain.

The European Commission granted PCI status to a CO2 capture and transportation project called the CCS Baltic Consortium — it includes Mitsui O.S.K. Lines (MOL), SCHWENK Latvija SIA, etc.

The goal is to create a CCS value chain in the region. The PCI status will facilitate the project’s start, with operations to begin in 2030.

Mitsui O.S.K. Lines (MOL) reported the successful performance of the world’s first coal carrier equipped with its Wind Challenger hard sail wind propulsion system.

In 18 months it made seven round-trip voyages from Australia, Indonesia, and North America to Japan on behalf of Tohoku Electric.

The Wind Challenger system reduced daily fuel consumption by up to 17% and achieved an average of 5% to 8% savings per voyage.

CONTEXT: Wind Challenger was developed by MOL and Oshima Shipbuilding. It employs a telescoping hard sail to use wind power for propulsion.

Asahi Kasei brought on-stream an alkaline water electrolysis (AWE) testing facility in its Kawasaki Works, to develop AWE systems of over 100 MW.

In 2025, the company will start accepting system orders. Its largest system so far, the 60 MW AWE, will be delivered to Malaysia-based Gentari Hydrogen.

NEWS: ELECTRICITY MARKETS

Sumitomo Electric starts building £350 mln factory in Scotland to make subsea cables

(Japan NRG, May 15)

Sumitomo Energy began construction of a subsea transmission cables factory at the Port of Nigg in Scotland.

The £350 million factory should be operational in 2026, and will be Sumitomo’s first cable factory in Europe and the first HVDC cable factory in the UK.

It will manufacture cables to connect and deliver electricity from renewables facilities, including offshore wind.

CONTEXT: The UK ranks second in the world in terms of nameplate capacity for offshore wind power (22% share of the global total). Therefore it’s a lucrative market for companies like Sumitomo Energy.

JERA announced its 2035 growth strategy for decarbonization and the energy transition, with three key areas: LNG, renewables, and hydrogen & ammonia.

As for LNG, it aims to have transactions in the fuel for over 35 million tons by 2035. In the renewables sector, the goal is 20 GW of capacity by the same year. Finally, for hydrogen and ammonia, it targets 7 million tons of volume.

By 2035, JERA aims for a net profit of ¥350 billion and an EBITDA of ¥700 billion. Plans call for investing ¥5 trillion in LNG, renewables, and hydrogen & ammonia.

JERA plans to reduce CO2 emissions 20% by 2030, total CO2 emissions 60% by FY2035, and achieve zero emissions by 2050. It plans to phase out coal-fired power by FY2030. It will convert remaining coal-fired power to ammonia by the 2040s.

TAKEAWAY: JERA is Japan’s biggest power company and top trader of LNG. Its strategy will likely be followed by other major power utilities and suggests that in the domestic market the major players may seek to balance LNG as a baseload power source with a stronger renewables business, while looking for ways to transition the coal fleet to ammonia or hydrogen.

JERA President Hisae Okuda said the company will postpone a decision on the construction of new Units 7 and 8 at the Chita Thermal Power Plant (Aichi Pref) that won in the long-term decarbonized power supply auction.

A company that withdraws from a winning bid faces a financial penalty.

JERA President Okuda noted that under the auction rules, 90% of fixed costs are returned but variable costs are not compensated. For an LNG-fired plant, there are uncertainties around future fuel costs, power demand, and whether the facility will be used as a baseload power source, or not, Okuda said.

JERA will discuss the issue with the government, Okuda said.

Units 1, 2, 3, and 4 at the Chita power plant were shut in 2017. Only Units 5 and 6 are now operational (total capacity 1.7 GW); both run as combined cycle plants that are fueled by LNG.

CONTEXT: At the end of April, Japan had its first ever long-term decarbonized power auction. A total of 42 decarbonized power projects were chosen, the majority were for battery projects and energy storage, but the biggest winners in terms of total capacity were gas-fired power plants.

TAKEAWAY: As reviewed in the Analysis section of this week’s report, there are a number of uncertainties stemming from the new auction. While there may be financial penalties for not delivering the capacity, these are thought to be relatively small and not an obstacle for developers to renege on their construction plans should the economics of their project change. However, if a number of winning bids fail to deliver the promised capacity, auction rules will most likely be tightened going forward.

March data from JEPX show the daily average Sell bids (i.e. supply volume) was at 1.03 TWh, down 15.3% from the previous month. Buy bids (i.e. demand volume) and 889.5 GWh, down 0.4%.

The period between March 27-29 March saw several of JERA’s thermal power plants shut due to fuel constraints, but the impact on prices was limited. Instead, the market saw waves of fluctuation in supply and demand.

For comparison, April data show Sell volumes rose slightly to 1.09 TWh; but Buy volumes declined to 789.7 GWh.

The total monthly volumes for March were: Sell bids down 9.5% YoY to 32.13 TWh; Buy bids up 6.4% YoY to 27.57 TWh.

Average supply volume per product was 21.6 GWh, down 15.3% YoY. Of this, daytime supply was down 12.2%; peak hours was down 10.3%; and evening supply was down 20.6%. Demand volumes were little changed, apart from peak times (down 2.7%).

ANRE reported that the number of new players in the electricity market (known as shin-denryoku) rose to 694 as of December 2023.

Of that total, 513 actually had sales, three fewer than a year ago. Tokyo Gas took the top spot for the 9th consecutive month in terms of total electricity sales.

CONTEXT: While a large number of companies have a retail license, some have either never used it or are not currently using it. Even of those that posted sales results, only about a fifth are understood to be retailing electricity outside of their group entities.

Overall power volume sold by new market entrants rose 16.4% YoY to 11.02 TWh, mainly due to increased heating demand in winter. Low-voltage sales increased 24.5% YoY, high-voltage sales increased 10.6% YoY, and extra high-voltage sales decreased 0.5% YoY.

In the low-voltage category, Daiwa House reached the 10th spot after posting a 34.6% YoY jump in sales. Many new market players booked bigger sales in the high-voltage category.

TAKEAWAY: After several years of aggressively taking market share from EPCOs (the major power utilities), new entrants saw their positions eroded in the past two years due to price spikes and higher volatility. More stability in the market recently is helping non-EPCO players to revive their business, but the upcoming summer peak demand period will be another test for the retailer business model.

Chubu Electric completed its investment in Hollandse Kust West Site VI, an offshore wind power project (760 MW capacity) in the Netherlands. The utility now has a 30% stake in Ecowende, which operates the project.

This is the first time Chubu Electric has directly invested in an offshore wind project.

The project aims to start operation in 2026.

TAKEAWAY: The investment will enable Chubu Electric to use the experience in offshore wind power generation, as well as the know-how on ecosystem protection initiatives, in future projects in Japan and abroad.

Chubu Electric and OSCF, a Tokyo-based construction firm focused on renewables projects, said they canceled plans to build a 86 MW onshore wind farm straddling Shinshiro City and Shitara Town in Aichi Pref.

Poor wind conditions are the main reason for cancellation.

Erex, which trades electricity and runs several biomass power plants, has formed an alliance with JFE Engineering to develop biomass-fueled generation facilities in Japan and overseas.

The firm plans to raise about ¥11.8 billion through a third-party allotment of new shares to four firms: JFE Engineering, construction and engineering firms Toda and Kyudenko, and Sumitomo Mitsui Finance & Leasing.

About ¥8.3 billion will fund the growth of the overseas business, including a biomass power plant in Vietnam; about ¥3.4 billion will go to reducing interest-bearing debt.

Erex will issue 1.48 million shares of common stock and plans to allocate 4.39 million shares to JFE Engine and Toda, respectively; and 3.56 million to Kyudenko, and 2.5 million to Sumitomo Mitsui Finance & Leasing.

Precision components maker MinebeaMitsumi plans to significantly expand its solar power generation onsite at its Thai factory and expand renewables procurement at other Southeast Asia locations. It hopes this will cut electricity costs and also CO2 emissions.

The firm’s Thai factory premises currently have 16.5 MW of solar capacity installed, but the manufacturer now wants to grow this to 154 MW and to add batteries. This will allow MinebeaMitsumi to procure more than 50% of its Thai electricity needs from renewable energy sources. On a group-wide basis, it will mean that 12.5% of the company’s electricity is green.

MinebeaMitsumi wants to oversee similar transformations across its Southeast Asia operations and become more involved in the renewables generation and procurement business. It plans 8 MW of solar facilities at the Cebu Plant site in the Philippines, and 50 MW of solar as a new factory in Cambodia.

In total, MinebeaMitsumi aims to have 228 MW of solar capacity at its overseas sites.

NEC opened two data centers that run on renewable energy generated at its facilities outfitted with solar PVs in Sagamihara, Kanagawa and Kobe.

The data centers feature energy-saving measures that separate cold and heat.

CONTEXT: The data centers are newly built within two complexes established in 2014 (Kanagawa) and 2016 (Kobe). The expansion aligns with NEC’s goal for 2030 to reduce its overall GHG emissions by 55% compared to 2017 levels.

Tokyo Gas acquired Furuko Holdings, which installs residential PV systems and storage batteries.

Tokyo Gas aims to boost business for households under the “IGNITURE” brand.

SIDE DEVELOPMENT: National Police Agency launches team to probe thefts from solar PV farms (Japan NRG, May 13)

The National Police Agency set up a special unit to investigate thefts of metal parts from solar PV farms. It also seeks to institute preventive measures and step up measures to detect such thefts.

CONTEXT: The decision was made in response to the spike in the number of such thefts nationwide, hitting a record high in 2023, at 16,276. Japan NRG covered this issue in detail in an analysis text in the Oct 16, 2023 report.

Electric power equipment manufacturer Daihen will unveil a new solar power storage system for use at factories, and at half the price of conventional systems.

The system will use a mechanism to store electricity at a higher voltage. Manufacturing costs will be lower.

The system has a storage capacity of 407 kWh. It combines lithium-ion batteries with a power converter and transformer.

It also incorporates a silicon carbide (SiC) power semicon in the power converter that can withstand twice the voltage of conventional devices. This makes it possible to store electricity at higher voltages.

CONTEXT: This new product is a response to growing demand at factories to use electricity from renewable energy sources.

TAKEAWAY: More factories will likely aim to secure their power from PV generation facilities installed on-site. Storage systems that maximize these efforts should generate solid interest.

Mitsubishi Electric will begin development of next-gen energy storage devices with Musashi Energy Solutions.

The two firms will also develop next-gen energy storage modules and battery management systems (BMS) for the railroad industry.

The device will be able to achieve a high output density greater than lithium-ion batteries, as well as a higher capacity density than hybrid supercapacitors (HSC).

The energy storage module is an upgraded compact model with added vibration resistance and insulation/waterproofing to significantly improve performance.

In the future, the module is expected to optimize power storage for hydrogen fuel cell hybrid trains, diesel hybrid trains, overhead line-less trains, etc.

In October, TEPCO hopes to restart Kashiwazaki Kariwa NPP Unit 7.

This will be the first time post-Fukushima that TEPCO operates a nuclear reactor in compliance with the new stringent safety regulations.

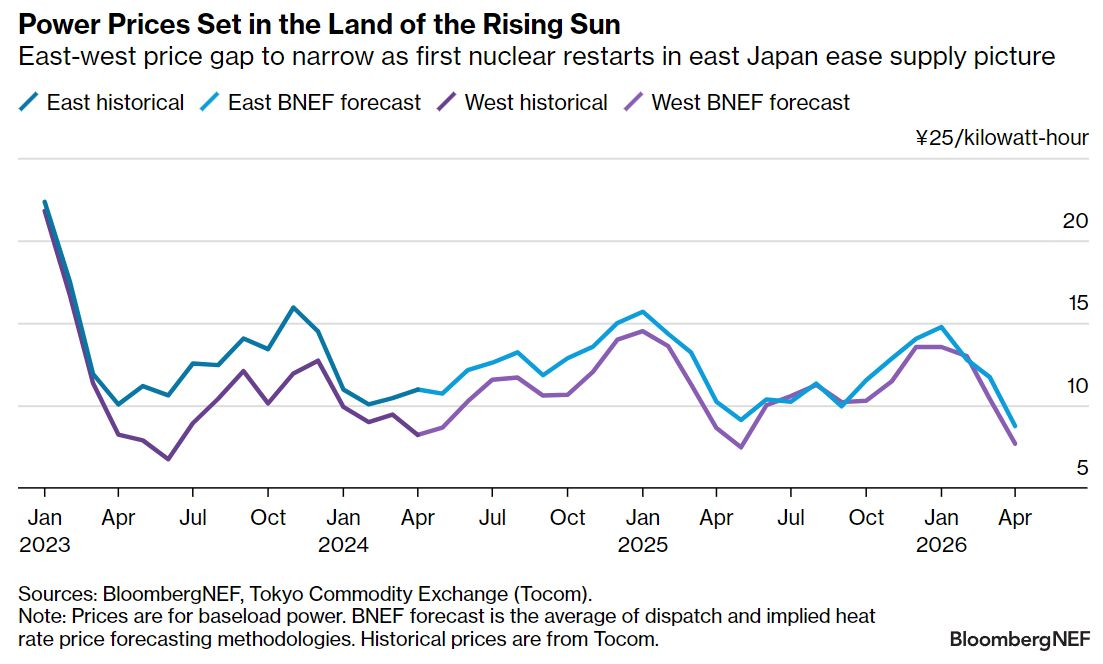

According to consultancy BNEF, average electricity prices in Japan will decrease 11% in 2024, due to sluggish demand and increased supply from nuclear and renewables, which will deepen duck curves and intraday volatility. BNEF sees power prices averaging ¥11-12/ kWh in the coming two years.

CONTEXT: Before the March 2011 Fukushima disaster, the 1,000 acre Kashiwazaki Kariwa NPP was the largest nuclear generating station in the world by nameplate capacity, at about 8 GW.

TAKEAWAY: Japan aims to bring five more reactors online by 2025. This alone will not be enough for nuclear generation to account for 20% of the power mix by 2030, as per the govt’s plan. Japan will have to accelerate the restart of operable nuclear capacity in the second half of the decade to hit its power targets and also to meet interim emission reduction goals.

The mayor of Genkai Town (Saga Pref) accepted a literature survey to select a final disposal site for high-level radioactive waste.

The mayor cited the town’s economic challenges as justification for his decision.

Residents are concerned about population decline and reputational damage. The population has decreased 16% over ten years, and the mayor seeks local revitalization.

CONTEXT: Over the past year Japan has accelerated efforts to restart nuclear reactors to boost carbon-free energy production. Restarting NPPs of course requires solutions in place to dispose of nuclear waste. Genkai is the third municipality to accept a survey for a waste disposal site; the others are Muttsu and Kamoenai (Hokkaido).

TAKEAWAY: The Genkai decision is unlikely to lead to its selection as host of a final nuclear waste disposal facility. The entire process requires a decade of surveys; and what’s more, previous studies showed that Genkai is unlikely to be geologically suitable for such a site.

Idemitsu Kosan, Japan’s second-biggest oil refiner, will increase its Fuji Oil Co. stake to 20% and make it an equity method company. Idemitsu and Fuji are considering collaborations that include jointly procuring raw materials.

The reorganization resembles one proposed in 2021 by an activist fund related to Murakami Yoshiaki, which at the time was Fuji Oil’s biggest shareholder. The fund pressured Fuji Oil to become part of Idemitsu, said an industry source, but the firm wanted to stay independent.

Back then, Idemitsu felt there was a reputational risk due to the association with Murakami, according to a source in the company. But ultimately, Idemitsu took the path of increasing its stake in Fuji Oil by acquiring stock from JERA and Sumitomo Chemical.

CONTEXT: The domestic fuels market has been in fundamental decline for over a decade due to the shrinking of the population and a switch to cleaner alternatives. For Idemitsu, industry consolidation avenues, however, are slim. Fuji Oil has supplied petroleum products to facilities now owned by Idemitsu since at least 2005.

Mitsui O.S.K. Line subsidiary, MOL Energia Pte, inked a time charter contract with CSSA Chartering and Shipping Services that’s owned by TotalEnergies. The contract is for two new LPG dual-fuel very large gas carriers (VLGCs).

Hyundai Samho Heavy Industries in South Korea will build and deliver the vessels in 2026. They can run on LPG or conventional heavy oil, as well as transport ammonia.

As of May 12, the LNG stocks of 10 power utilities were 2.14 million tons, up 6.5% from May 5 (2.01 million tons). This is 11.2% down YoY (2.41 million tons), and 1.4% more than the past five-year average of 2.11 million tons.

For the past several weeks, LNG stock levels have hovered around the five-year average but slightly less than the 2023 level.

The JMA (Japan Meteorological Agency) said that the rainy season will begin in the first week of June. Thus, electric companies will start to prepare for increasing power demand from cooling devices.

ANALYSIS

BY MAGDALENA OSUMI

Japan’s First Long-Term Decarbonized Power Auction is a Boost for BESS, Foreign Investors

Grid-scale battery energy storage systems (BESS) were the biggest winners in Japan’s first ever long-term decarbonized power auction, which was held in January, showing that investments in the innovative green technology are well worth the risk.

That first auction, which was conducted under the auspices of the Organization for Cross-regional Coordination of Transmission Operators (OCCTO), proved to be most profitable for BESS and pumped hydro storage developers. The government had allocated over 1.6 GW of capacity for 30 such projects.

Nevertheless, even though the government introduced the scheme to promote and finance a shift away from fossil fuels, it supported the co-firing of ammonia or hydrogen with coal. Also, the auction had a separate category for gas-fired capacity from LNG. Such an approach initially raised concerns that METI would use the scheme to prop up thermal generation.

Contrary to speculation, however, the auction results announced on April 26 showed that officials are not trying to slow the transition to renewables. In fact, the low-commitment auction criteria left both the government and developers with room for second thoughts.

So, how can we be sure that all of the winning projects will come online? How will the results affect the next auction? Japan NRG looks at the results of Japan’s first long-term decarbonized power auction (LTDA) and examines the rewards and challenges that developers may face.

LTDA as optimal platform for BESS expansion

A total of 42 decarbonized power projects were chosen in the first LTDA – 30 were BESS, two biomass, and one nuclear; in addition, three were for pumped hydro storage and five for thermal turbines modified to co-fire coal with ammonia, and one to co-fire with hydrogen.

The contracts guarantee 20 years of revenue covering fixed costs as long as developers or BESS operators make the capacity available over a long-term period, 20 years in principle. This offers a safety net for a whole wave of BESS projects as the government supports the build out of a battery storage sector from a very low base.

The wide range of companies from abroad that applied for BESS contracts indicates that developers are aware of Japan’s high and rising level of renewable energy curtailment.

Battery storage systems offer flexibility with peak shaving, self-consumption optimization, and backup power in the event of outages. They are crucial to ensure stable power supply when there is a high proportion of variable renewables like wind and solar.

METI-affiliated OCCTO assigned 1.09 GW of BESS capacity across 30 projects. The winning bids accounted for only 24% of all projects in the category.

Renova, which brands itself as Japan’s only listed pure-play renewables developer, and with assets in other parts of Asia, won three contracts for projects totalling 215 MW.

The single biggest BESS contract award was for 96.2 MW to a business run by financial services company Orix for its Maibara City Koto Energy Storage.

Nozomi Energy, a renewables developer founded by global investment group Actis, won bids for two BESS projects that each offer an initial installed capacity of close to 200 MWh.

Among the successful bids, however, were mostly small-scale projects, which could be interpreted as the authorities’ cautious approach towards the new technology, or a desire from developers to start small in a burgeoning field. With weak penalties for non-delivery, there are also questions over whether all the contracted BESS projects will come online.

LTDA winners could use their contracts to secure financing, but review the business model if better review streams become available. In this, the LTDA may act almost as a hedging tool for developers. But a high cancellation rate would almost certainly push METI to alter future auction criteria.

New platform for non-Japanese investors and businesses

Winners have since said that key to securing contracts were the competitive rates of their proposed capacity payments. Those with experience in other national markets seemed to have the edge, with international developers snagging at least 20 LTDA project contracts.

This openness to overseas players in the first auction of its kind came as a contrast to the way the offshore wind tenders have played out. In Round 1, all winners were domestic companies. In Round 2, German utility RWE and Spain’s Iberdrola were, separately, members of some of the winning consortiums.

The list of winners in the LTDA includes Canadian Solar that secured as much as 13.3% of the total capacity for its three BESS projects. The firm’s projects, promising 193 MW of capacity, are located in Aomori, Fukushima, and Yamaguchi prefectures. They will feature the SolBank 3.0 system launched by the company’s subsidiary e-STORAGE, and are expected to begin commercial operation between 2027 and 2028.

Winners also included:

Singapore-based CHC Energy (with input from U.S. asset manager Stonepeak);

A JV between Chinese battery giant Contemporary Amperex Technology (CATL) and Cathay Fortune Company, as well as New York-based Hartree Partners;

Canadian Solar-backed Teeda Power;

Hexa Energy Services, supported by I Squared Capital.

Hexa Renewables bagged the highest number of projects with 11. Singapore-based Equis, which develops renewables and waste infrastructure, was the only winner in the biomass category, picking up contracts for two projects in Hokkaido. Both are 112 MW – one in Ishikari, and another near Tomakomai City. Equis already has several operational biomass plants in Japan, one of which is run jointly with Tohoku Electric.

Nuclear and hydro

The LTDA proved most popular among BESS developers, as 4.56 GW of proposed capacity was offered, exceeding the limit allocated for the entire renewables section (4 GW). But other energy sources also did well during the auction.

OCCTO awarded 1.3 GW to nuclear power capacity, opening up the possibility that major utilities will utilize this scheme to help finance ongoing NPP construction. There are three reactors in Japan officially listed as “mid-construction”. The long lead time for new nuclear plants would make it difficult to utilize LTDA in its current form.

The auction’s entire nuclear allocation went to Chugoku Electric, which is building Unit 3 at its Shimane NPP. The 1.37 GW advanced BWR reactor is obligated by LTDA rules to make its capacity available from FY2027. However, four days after the LTDA announcement, Chugoku Electric said that it aims to complete the reactor only in FY2028, with operations likely to begin in FY2030.

Unit 3 at Shimane began construction in 2006, but work was frozen after the Fukushima disaster. Any start of operation is dependent on winning approval from the nuclear regulator and a green light from the local community. Both have proved tricky challenges for NPP restarts in the past decade.

Chugoku Electric’s Shimane nuclear power plant

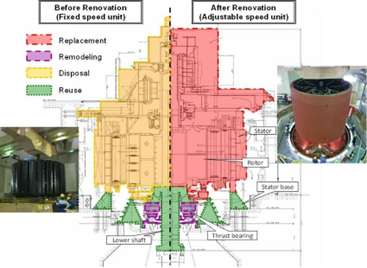

Meanwhile, OCCTO also awarded contracts for 577 MW of pumped hydro storage. Kansai Electric (KEPCO) was among the recipients, securing contracts for two large pumped storage projects at its Okutataragi hydro station in Asago, Hyogo Prefecture. The winning contracts will apply to Units 3 and 4, (each 254 MW output), but these aren’t for new facilities. Launched in 1975 and with a maximum total output of 1.9 GW, Okutataragi is Japan’s largest pumped-storage hydropower station.

To reduce fossil fuel costs and improve generation efficiency in partial load, KEPCO decided to enlarge the station’s LFC (Load Frequency Control) capacity through renovation of an existing pumped-storage power station from fixed speed to adjustable speed. The funding in the FY2023 LTDA will enable KEPCO to complete the renovation work on two units.

LNG – the quiet winner

The biggest allocation in terms of capacity, however, went to ten LNG-firing plants with capacities ranging from 463 MW to 615 MW (5.75 GW in total). Operators of those are: Hokkaido Electric, Tohoku Electric, KEPCO (3 projects), Chugoku Electric, Tokyo Gas, Osaka Gas and JERA (2 projects).

LNG projects are eligible to take part in the LTDA for another two years, with a cap of 6 GW per year versus a total of 4 GW for renewables. METI has explained this inclusion as driven by the need to create replacement baseload capacity and phase out older thermal stations.

How will the auction pan out in the next few years?

With the phaseout of LNG from FY2026, the auction will open up several GW of capacity for other energy sources. Some see this as an opening for larger BESS projects to capture funding. This year’s results also indicate that projects may not need to start exactly four years from the auction to qualify, and that renovations of existing capacity will compete alongside new ones.

Market players also expect a gradual tightening of auction rules to mandate the completion of winning projects, as per the conditions for similar tenders overseas. This time, OCCTO asked bidders to register for the auction several months before the bids were even due. This kind of long-term commitment to the LTDA will make more sense for developers that want to see the project to completion, which would cover the time and resources invested.

While most expect the BESS capacity allocation to grow, some agree with the government’s gradual opening up of the sector, warning that awarding too many contracts at once would lead to over-build in certain areas and affect either grid connections or project economics.

There are also few battery facilities now in operation in Japan, which means data on long-term battery performance, degradation, and synchronization with generation assets is thin. With the phase out of LNG from the LTDA, and limited scope for new and even updated pumped storage capacity in Japan, the biggest rivals to BESS in future auctions may come from nuclear and co-firing facilities.

ANALYSIS

BY MAGDALENA OSUMI

Understanding the Complexities and Nuances of Japan’s Power Markets

From the 1950s until the mid-1990s, Japan’s electric power sector was dominated by 10 regional companies that were responsible for all power generation, distribution and sales. Since then, the nation’s power industry has undergone a variety of significant reforms that seek to foster competition among companies selling electricity to end-users.

In this article, JapanNRG reviews the current state of electricity markets that now involve 1,133 generation firms, 729 retailers and 55 transmission operators. We look at the main market structure in place today and how they are changing.

Background

Japan’s electricity industry and market reforms started in the early part of this century, but a full retail market liberalization had to wait until 2016. The goal was to create a more vibrant market that would naturally lower prices.

The reforms sought to ensure competitive neutrality on the basis of stable supply. But with the original 10 power utilities, known as EPCOs, still dominant and the government keen to protect households and big industrial energy users from price volatility, the power market has evolved into a hybrid structure that combines market trading and tariffs.

The government has also introduced more trading and auction platforms to mirror the fragmentation of the electricity industry across regions, generation sources, business models and consumer demands. And yet, disparities remain.

The latest policy discussions within METI and its expert panels reflect a growing sense of the need to reverse market fragmentation. Recent proposals talk of the need to eliminate state tariffs altogether, while integrating various market platforms to bind spot and futures trading. Market purists want physical, derivative, and standby/ backup trading to be all connected so that it better reflects the realities of operating power facilities.

Speaking to officials, it seems that all options are on the table, as long as they lead to stable prices and resilient power companies and systems. The following are the main power trading platforms in Japan.

Wholesale electricity market

JEPX (Japan Electric Power Exchange) acts as an intermediary for electricity sales between producers and retailers, facilitating transactions linked to physical delivery. It is a private exchange managed by a general incorporated association of electric power companies and other such entities.

Established in 2003 and launched in 2005 as a market for the commodity trading of electric power, JEPX serves as an intermediary for electricity spot trading, forward transactions, non-fossil value transactions, indirect power transmission right transactions and base load transactions.

It serves as a platform for three types of markets :

Spot day-ahead, which is the main market where electricity is traded for delivery on the following day;

Intraday market, or same-day market, for electricity supplied on a day when the spot market is closed; it enables members to trade electricity until one hour prior to actual use; and

Forward fixed-form market to trade electricity that will be delivered after a certain period of time, even years into the future.

Trading in the Spot and Intraday markets splits a calendar day into 48 time frames (30 minute-slots). It offers two more contract options: the Day-Ahead Day Time (slots between 8 a.m. and 10 p.m.), and Day-Ahead Peak Time (1 p.m. to 4 p.m.).

To trade on JEPX, membership as an affiliate is required. Separate pricing is set for each of Japan’s nine major grid areas (excluding Okinawa): Hokkaido, Tohoku, Tokyo, Chubu, Hokuriku, Kansai, Chugoku, Shikoku and Kyushu. The price is formed on the basis of contracted transactions, rather than bids. Participants cannot see the bids of other parties.

Until 2016, trading volumes on JEXP were small, accounting for just 2% of Japan’s total generation. This changed dramatically in 2016 both due to full market liberalization, which saw new retail-focused entrants in the market, and thanks to the concerted efforts of METI. The ministry asked major utilities to sell part of their generation volumes via the exchange.

Trade volume reached 318.5 TWh last year, equivalent to 40.1% of all electric power sold nationwide in FY2023. JEPX is a private exchange managed by a general incorporated association of electric power companies and other such entities.

Futures market

Trading in electricity futures was introduced to hedge the risk of electricity price fluctuations. Tokyo Commodity Exchange, or TOCOM, was the first to launch an electricity futures marketplace in Japan in September 2019. It’s now a subsidiary of the Japan Exchange Group (JPX), which handles all equity trading and is now pioneering carbon credit trading.

Alongside power futures, TOCOM offers futures and options contracts for rubber, gold, silver, crude oil, gasoline, gas oil, kerosene, platinum and palladium. The exchange handles mainly physically delivered transactions, but in the case of futures contracts, physical delivery does not take place.

TOCOM’s start in electricity futures was followed by a similar offering from the European Energy Exchange (EEX). While the German exchange operator launched its Japan futures marketplace a year later, it has been able to expand the business much faster, in part thanks to its international background and the experience of running power futures in a number of EU countries and elsewhere, introducing clients from other markets to its Japanese offering.

As a result, EEX had a 92% market share for electricity trading as of 2023. It features a wide range of products for power trading on derivatives markets.

Within three years of running its Japan operations, EEX has established a dominant position in electricity futures, and as of May 16, 2024 it has managed to grow the number of trading participants to 74 with 40 international companies among the registered trading members. These are almost evenly split between domestic power utilities and overseas traders, utilities, financial companies and others. Japan is the first derivatives platform that the EEX has built in Asia.

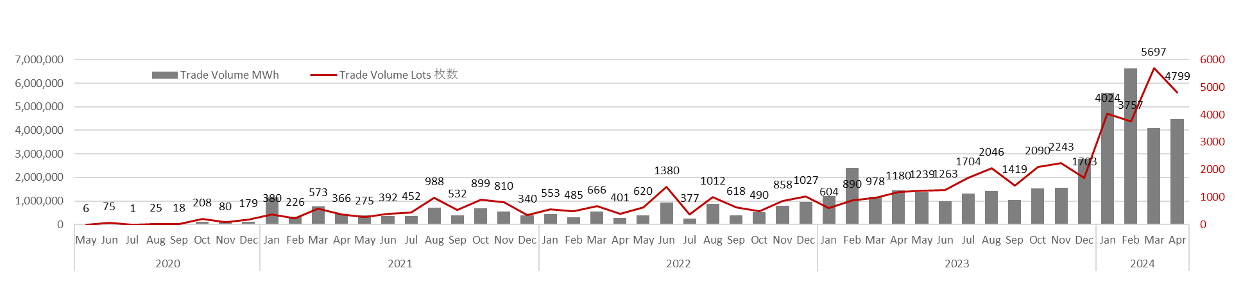

The EEX trading volume in Japan power futures nearly doubled during 2023 from the previous year and hit a record in February 2024, when around 6.5 TWh was traded in a single month. The exchange has facilitated close to 20.8 TWh of trades in the year to date as of April 24. That’s already more than the entire volume traded on the EEX in 2023 (18.3 TWh). In the course of 2020-2022, EEX volumes were just 13.9 TWh, so the growth has been extremely robust.

Monthly Number of EEX Trades and Traded Volume in Lots and MWh

Source: EEX, Japan NRG’s Data Book

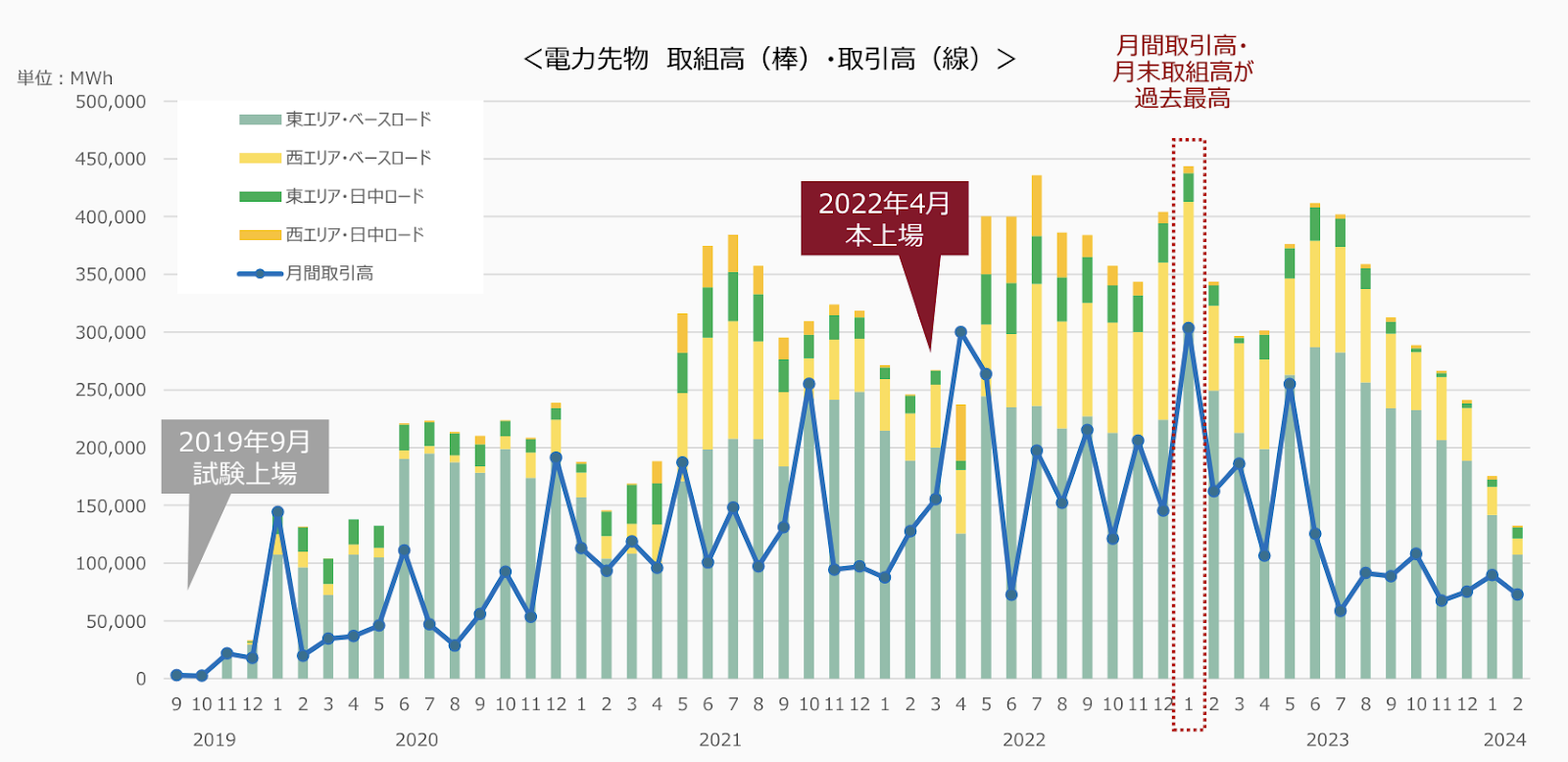

TOCOM splits its futures into baseload and peak load contracts, and also East and West grid areas. The exchange has daily and weekly contracts, as well as the monthly offerings that attract most of the attention.

While TOCOM has lagged EEX in volumes, it also saw a surge in trading this spring after introducing the so-called Market Maker System. Several financial and trading institutions, acting as providers of liquidity, helped to promote more active dealmaking for the July-September 2024 contract period when demand for electricity will be at its peak, which increased liquidity by a factor of more than eight.

Monthly Electricity trading volumes on the TOCOM (MWh)

Source: TOCOM

TOCOM currently has 44 trading participants in its power futures markets, most of which are major power utilities such as Itochu Marubeni and Mitsui & Co. Last year’s trading volume was 15,374 lots, a drop from 24,746 in 2022. It is unclear what this translates into on a kilowatt-hours basis as TOCOM does not disclose this information. However, based on the monthly trading volume graph TOCOM presented to METI earlier this year, the exchange saw annual volumes little changed last year compared to 2022. In contrast, TOCOM’s share of the electricity futures market seems to have declined from over 30% in 2022 to around 1% in late 2023.

Products

Number of traded lots 2023

Number of traded lots in 2022

West Area Baseload Futures

2,382

5,276

West Area Peak Load Futures

563

3,371

East Area Baseload Futures

9,968

11,341

East Area Peal Load Futures

2,461

4,758

Total

15,374

24,746

Capacity market

Trading in the capacity market, where transactions are made to secure overall supply capacity for the future, began in 2020. The market is overseen by the Organization for Cross-regional Coordination of Transmission (OCCTO) that was established in 2015, one year prior to market liberalization.

Transactions in the capacity market, which are auction-based, are made four years before the actual trade. The contract price is set at the intersection of the supply and demand curves, with bidding prices arranged in ascending order. Capacity contracts for 2024, signed in 2020, totaled 167.69 GW in volume and were priced at ¥14,137/ kW. Most of the tender winners since 2020 have been thermal power generators.

From the start of this year, OCCTO also launched an offshoot capacity auction system for low carbon generation sources. The conditions of that auction are different in that they offer a fixed 20-year contract, but ask successful bidders to return 90% of the profit made from other income streams. This new Long-Term Decarbonization Power Source auction is for clean energy facilities that are not subjected to the FIT or FIP regimes.

OCCTO also operates a balancing market to manage supply and demand. This platform was established in FY2021 to facilitate procurement and operation of cross-regional reserve balancing capacity. With participation of renewable energy generators, the market serves as a platform to procure electricity that balances out miscalculations in estimates for energy supply and demand.

Further reforms

METI is currently discussing ways to integrate some of the trading platforms and wants to link the futures and spot transactions in the electricity market. There are tentative plans to launch a one-stop trading mechanism by the end of 2025 involving TOCOM and JEPX. The new service, currently titled JJ-Link, would allow JEPX spot transactions to mirror TOCOM future positions.

The mechanism depends on TOCOM receiving contract data from JEPX, facilitating the matching of spot and futures positions, and alerting the power companies concerned. If this works, it would allow the placement of orders for JEPX power delivery trades via TOCOM, thus improving its trading efficiency and increasing liquidity.

JJ-Link is also a way of correlating power futures, a hedging tool, with current accounting practices in Japan. Proponents say that it would make hedge accounting applicable to futures transactions.

With this effort to unify markets, METI is looking to improve the efficiency and liquidity of Japan’s electricity trading, aiming to make it an ecosystem suitable for both energy specialists and financial institutions. The market’s growth is seen as a way of incentivizing new investments in clean energy sources while smoothing out disruptions to power supply due to weather, technology, politics or corporate action.

ASIA ENERGY REVIEW

BY JOHN VAROLI

This weekly column focuses on energy events in Asia and the Pacific

Asia / Oil

The profit from turning a barrel of crude oil into fuels in Asia is at the lowest in seven months, leading refiners to turn away from expensive Middle East grades and seek cheaper alternatives from the Americas.

Australia / Renewable energy

The government allocated about A$14 billion in its 2024-25 budget to help the country become a “renewable energy superpower” over the next decade.

China / Azerbaijan

Azerbaijan’s Minister of Energy met with a Chinese delegation led by the head of China Energy Engineering Group and the head of China Energy International Group. The meeting focused on cooperation in renewable energy.

China / Fossil fuels

In 2023, in order to meet rising electricity demand due to poor hydropower conditions, China generated 65%, or 6,102 TWh, of its electricity from fossil fuels, said energy think tank Ember. About 60% of China’s total power generation came from coal, which is above the global average of 35%. China accounted for over half of total global coal generation.

China / LNG

China’s LNG imports could hit record levels in 2024. The country is already the world’s top LNG importer, and this year will buy up to 80 MMT, driven by high demand from the industrial and commercial sectors.

India / Coal

The share of coal in the country’s power sector dropped to less than 50% for the first time since the 1960s. In Q1, India added a record-breaking 13.67 GW of power generation capacity, with renewable energy accounting for 71.5% of this new capacity.

Nuclear power

In 2023, nuclear power globally rebounded from a five-year low, increasing 1.8% YoY to reach 2,686 TWh. The U.S. was the largest electricity producer from nuclear at 775 TWh; China (435 TWh), and France (336 TWh). These three account for 58% of the global total.

Pakistan / Renewable energy

Oracle Power and its green energy developer firm, Oracle Energy, will develop 1.3 GW of renewable energy, to be located in Jhimpir, Sindh Province. It comprises 800 MW of solar and 500 MW of wind power.

Singapore / Oil

Shell will sell its Bukom refinery, one of the world’s largest oil refining and trading centers, to a JV of Indonesian chemicals firm PT Chandra Asri and global trading house Glencore.

Taiwan / Renewable energy

Taiwan completed the review of 2024 renewable energy feed-in tariffs. The rates for solar PV dropped slightly from last year, while wind and hydropower remained the same or rose slightly.

2024 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

January

First market trading day (Jan 4)

IEA “Renewables 2023: Analysis and Market Forecast to 2028” released (Jan 11)

Renewable Energy Exhibition (Jan 31 – Feb 2)

Taiwan presidential election (Jan 13)

Japan’s Diet convenes

IEA “Electricity 2024 / Analysis and Forecast to 2026” released (Jan 24)

February

CFAA International Symposium (Feb 2)

India Energy Week 2024 (Feb 6-9)

Lunar New Year (Feb 10-17)

Indonesia presidential election (Feb 14)

Japan-Ukraine Conference for Promotion of Economic Reconstruction (Feb 19)

FIT/FIP solar auction (Feb 19 – March 1)

Smart Energy Week (Feb 28-Mar 1)

March

Announcement of auction result for Offshore Wind Round 2 (for Akita Happo-Noshiro Project)

Onshore wind auctions (March 4-15; results on March 22)

International LNG Congress (LNGCON) 2024, Milan, Italy (March 11-12)

Russian president election (March 15-17)

World Petrochemical Conference, Houston, TX, USA (March 18-22)

IAEA Nuclear Energy Summit @ Belgium (March 21)

Ukraine presidential election (due before March 31)

Happo Noshiro, Murakami-Tainai, Oga-Katagami-Akita and Saikai-Eshima wind project auctions close (June 30)

July

Tokyo governor election (July 7)

7th Basic (Strategic) Energy Plan draft published (expected)

August

7th Basic (Strategic) Energy Plan draft presented to Cabinet (expected)

September

Global Offshore Wind Summit Japan 2024, Sapporo, Hokkaido (Sept 3-4)

The United Nations Summit of the Future (Sept 22-23)

Gastech 2024, Houston, TX (Sept 17-20)

IAEA General Conference

GX Week in Tokyo (expected late Sept to October)

Asia Green Growth Partnership Ministerial Meeting

Asia CCUS Network Forum

International Conference on Carbon Recycling

International Conference on Fuel Ammonia

GGX x TCFD Summit

October

IEA World Energy Outlook 2024 Release

BP Energy Outlook 2024 Release

Innovation for Cool Earth Forum (expected)

Connecting Green Hydrogen Japan 2024 (Oct 16-17)

Japan Wind Energy 2024 Summit (Oct 16-17)

Solar Energy Future Japan 2024 (Oct 16-17)

Japan Mobility Show (Oct 25-Nov 5)

November

US presidential election (Nov 5)

COP 29 in Azerbaijan (Nov 11-22)

Abu Dhabi International Petroleum Exhibition Conference (ADIPEC) 2024, Abu Dhabi, UAE (Nov 11-14)

APEC 2024 @ Lima, Peru

International Conference on Nuclear Decommissioning (TBD)

G20 Rio de Janeiro Summit (Nov 18-19)

Offshore Energy Exhibition & Conference (OEEC) 2024, Amsterdam, the Netherlands (Nov 26-27)

Biomass & BioEnergy Asia Conference (TBD)

European Biomethane Week 2024

December

Last market trading day (December 30)

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.