JAPAN NRG WEEKLY

MAY 27, 2024

JAPAN NRG WEEKLY

MAY 27, 2024

NEWS

TOP

- 150-member public-private “perovskite council” set up to foster investments and manufacturing

- Panasonic plans to more than double domestic production of EV batteries by 2030

- Mizuho Financial Group to provide assistance to shut coal plants in Southeast Asia

- Japan-Saudi leaders talk online about crude, hydrogen, CRMs

- Marubeni, Saudi Power Procurement Co ink PPA

- JERA unveils renewables detection tech to shrink greenwashing

- Minister Takaichi participates in nuclear fusion meeting

- METI publishes preliminary definitions for Direct Air Capture

- Sumitomo to build CO2 underground storage in Canada

- MHI tests pilot CO2 capture unit in Belgium

- Toyota’s liquid hydrogen racing car improves cruising range

- Google signs long-term solar farm deals to power data centers

- UAE’s Mubadala makes first renewables investment in Japan

- OCCTO releases upbeat forecast on summer power reserves

- Orix launches virtual PPA under FIP as more firms switch from FIT

- BESS connection applications growing rapidly nationwide

- Renova to develop very large onshore wind power farm

- JERA, MODEC, etc secure AIP for TLP-type floating wind turbines

- Toshiba develops forecasting tools for wind generation

- Japan, Malaysia leaders discuss decarbonization, rare earth collab

- Zachry goes bankrupt, Chiyoda and US LNG project impacted

- MOL signs long-term charter deal with JERA for LNG carrier

ANALYSIS

AMMONIA OR METHANOL: WHICH IS THE WINNING ZERO-EMISSION SHIP FUEL?

Decarbonizing the maritime transport sector Is one of the most important tasks in the energy transition. Among the proposed clean energy solutions, the main one focuses on which fuel should replace the heavy marine oil now used by vessels. Top candidates include ammonia and methanol. This analysis assesses new shipping fuel candidates in the regulatory, ship development and supply aspects.

JAPAN’S CHIP REVOLUTION IS CHALLENGING FORECASTS FOR DROP IN POWER DEMAND

As state planners seek to update Japan’s energy strategy, they must consider that the push to revive semiconductor manufacturing has yielded fruit. The rapid rise of generative AI usage, as well as Japan’s courting of global data centers, could see power demand for the digital sector alone jump by a factor of 10 in a decade. Without a quick reaction, the next surprise could be energy shortages.

ASIA ENERGY VIEW

A wrap of top energy news that impacts other Asian countries.

EVENTS SCHEDULE

A selection of events to keep an eye on in 2024.

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group

Events

Editorial Team

Yuriy Humber (Editor-in-Chief)

John Varoli (Senior Editor, Americas)

Mayumi Watanabe (Japan)

Wilfried Goossens (Events, global)

Kyoko Fukuda (Japan)

Magdalena Osumi (Japan

Filippo Pedretti (Japan)

Tim Young (Japan)

Regular Contributors

Chisaki Watanabe (Japan)

Takehiro Masutomo (Japan)

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

OFTEN-USED ACRONYMS

|

METI |

The Ministry of Economy, Trade and Industry |

mmbtu |

Million British Thermal Units | |

|

MoE |

Ministry of Environment |

mb/d |

Million barrels per day | |

|

ANRE |

Agency for Natural Resources and Energy |

mtoe |

Million Tons of Oil Equivalent | |

|

NEDO |

New Energy and Industrial Technology Development Organization |

kWh |

Kilowatt hours (electricity generation volume) | |

|

TEPCO |

Tokyo Electric Power Company |

FIT |

Feed-in Tariff | |

|

KEPCO |

Kansai Electric Power Company |

FIP |

Feed-in Premium | |

|

EPCO |

Electric Power Company |

SAF |

Sustainable Aviation Fuel | |

|

JCC |

Japan Crude Cocktail |

NPP |

Nuclear power plant | |

|

JKM |

Japan Korea Market, the Platt’s LNG benchmark |

JOGMEC |

Japan Organization for Metals and Energy Security | |

|

CCUS |

Carbon Capture, Utilization and Storage | |||

|

OCCTO |

Organization for Cross-regional Coordination of Transmission Operators | |||

|

NRA |

Nuclear Regulation Authority | |||

|

GX |

Green Transformation |

NEWS: ENERGY TRANSITION & POLICY

150-member public-private “perovskite council” set up

(Government statement, May 21)

- 150 companies and government organizations have joined the newly established Public-Private Sector Council to Expand Deployment and Strengthen Competitiveness of Next-Gen Solar Cells”. The goal is to promote perovskite solar cell (PSC) technologies.

- The Council seeks to foster large investments, to set up mass manufacturing, to build production plants, and to stimulate demand.

- Council members include scholars who serve on multiple METI advisory panels, manufacturers planning PSC productions, potential users, relevant industry associations, ministries and municipalities. Potential raw material suppliers, such as INPEX and Fujifilm, are not included.

Sectors | Members | Notes |

|

National government |

METI, MoE, Ministry of Land, Infrastructure, Transport and Tourism, Ministry of Agriculture, Ministry of Internal Affairs, Defense Ministry, Education Ministry |

Foreign Ministry (MoFA) is not included, suggesting that PSC application-focused bilateral ties are not yet on the horizon |

|

Manufacturers |

Sekisui Chemical, Toshiba, Aisin, EneCoat Technologies, Panasonic, Kaneka |

Ricoh, PXP Corp, Peccell Technologies not included |

|

Potential users |

Japan Railways group |

NTT Data, and Tokyu Group, one of the first to conduct PSC field studies, are not included |

|

Industry associations |

Japan Chamber of Commerce, Japan Business Federation, etc. |

Covers photovoltaics, housing, real estate development sectors |

|

Municipalities |

Tokyo, Fukushima, Miyagi, Okinawa, Kochi, Saitama, Yamanashi, Nagano prefectures, etc. |

Over 110 prefectures and cities |

- CONTEXT: The PSC modules for power plants are large-sized and more difficult to produce compared to smaller ones for IoT devices. The Council focuses on larger installations, and so it doesn’t include Ricoh that’s developing PSC for lighting and IoT devices. The Council will set 2040 targets for PSC power generation volume and costs. The current cost target is to reach ¥14/ kWh, or less, in 2030.

TAKEAWAY: Almost every govt unit is participating in this effort, which is unprecedented for any part of Japan’s energy sector. If it works, this model of cooperation could be utilized with other new energy solutions. Within just three-four years, PSC has gone from a niche R&D technology to one of the main decarbonization tools touted by the govt.

Panasonic plans to more than double domestic production of EV batteries by 2030

(Nikkei, May 20)

- Panasonic plans to more than double domestic production of EV batteries by 2030, up from the current 12 GWh per year.

- The firm seeks to supply potential customers like Mazda and Subaru.

- CEO Kusumi said the firm plans to modify some domestic production lines for more advanced batteries.

- He added that Panasonic has faced a significant drop in demand for batteries used in car specific models, prompting the firm to slash output from its EV battery factory in Japan; this is mainly due to slowing demand from its key customer, Tesla.

- CONTEXT: Panasonic has been working to boost the energy density of its 2170 cell, which could help reduce an EV’s overall cost. It is also developing another battery that’s thicker and more voluminous, called the 4680 cell. Panasonic is Japan’s top battery maker and a major supplier for Subaru, Mazda and Tesla. Panasonic has vowed to expand production in North America, aiming to one day provide 200 GWh of energy in EV batteries. Its current capacity in the U.S. is around 38 GWh, but EV sales in the U.S. are slowing.

Japan-Saudi leaders talk online about crude output, hydrogen and critical minerals

(Government statement, May 21)

- Saudi Arabia’s Crown Prince Mohammed bin Salman postponed his visit to Japan and instead held an online meeting with PM Kishida on May 21.

- Kishida urged Saudi Arabia to raise crude oil output, and called for deeper cooperation in hydrogen and ammonia global supply chains, and mineral resource development using Japanese technologies.

- The Prince said Saudi Arabia remains committed to stable crude supplies and would like to enhance cooperation in clean energy and other areas.

- SIDE DEVELOPMENT:

Marubeni, Saudi Power Procurement Co sign PPA

(Government statement, May 22)- Marubeni Corp inked a power purchase agreement (PPA) with Saudi’s largest wind power project run by SPPC.

- This is the first deal involving a Japanese company in the Saudi wind sector.

TAKEAWAY: Japan sees Saudi Arabia as potentially a strong partner in developing new sources of critical raw materials unconnected to China, which has come to dominate the processing of these key elements. Saudi Arabia and several countries in Africa are potential locations for this collaboration in critical raw materials.

JERA unveils renewables detection tech to minimize greenwashing

(Nikkei, May 22)

- JERA is launching a service that detects, on an hourly basis, whether the electricity used by a company was derived from renewable sources.

- The tech will enable businesses to generate more accurate data than existing methods that only give rough estimates of CO2 emissions based on monthly or annual calculations. Hence, it could help prevent and eventually eliminate greenwashing.

- The system will help companies disclose electricity usage to external parties and store that history on a secure blockchain.

- Since the system will accord with international standards, it could be used globally.

- JERA is considering offering the system to electricity utilities to establish a national power management framework.

- CONTEXT: Electricity used at night often comes from fossil fuel sources, boosting CO2 emissions by up to double from daytime levels. This means that firms using electricity at night might emit more CO2 than they currently estimate. Energy derived from fossil fuel sources accounted for over 70% of Japan’s power source mix in 2022, with renewable energy providing more than 20%. Similar systems have been developed and are already in use outside of Japan.

TAKEAWAY: Japan lags behind regarding plans to monitor CO2 emissions; systems similar to JERA’s new tech were developed and are already in use in other countries. Discussions on greenwashing also began much later in Japan than in other parts of the world. Japan has no penalties for false claims. To tighten the crackdown on greenwashing, Japan may need stricter rules that require firms to show proof to support their claims.

Minister Takaichi participates in nuclear fusion meeting in Tokyo

(Nikkei, May 21)

- Minister of State for Economic Security Takaichi Sanae attended a meeting to promote nuclear fusion that was organized by the Japan Fusion Energy Industrial Council (J-Fusion).

- She emphasized the importance of nuclear fusion for Japan’s energy security and industries, saying that a stable power supply is needed to meet demand from the country’s growing number of data centers.

- CONTEXT: The J-Fusion council comprises around 50 companies from various sectors. It aims to accelerate plans to realize nuclear fusion power in Japan.

TAKEAWAY: In 2022, Minister Takaichi announced that the govt intended to create a roadmap for nuclear fusion energy. A draft was then published in April 2023. As allied G7 nations forge ahead with fusion energy programs, Japan’s effort is in need of funding both from the private and public sectors.

METI publishes preliminary DAC definitions

(Government statement, May 17)

- METI published preliminary definitions of direct air capture (DAC) and its carbon accounting methodologies. An expert panel will put together a social implementation roadmap by late June.

- METI specified that DAC is the act of removing carbon from air outdoors and indoors; this is in contrast to Swiss-based carbon removal company Climeworks, which says that DAC only relates to outdoor air capture.

- METI will refine DAC methodology, aiming to make it applicable to earn J-Credits and other carbon offset credits.

Sumitomo joins project to build CO2 underground storage in Canada

(Nikkei, May 23)

- Sumitomo Corp will join a project to build an underground CO2 storage facility in Canada. When launched in 2026, each year it will store nearly 3 million tons of CO2. That figure could eventually expand to 10 million tons/ year.

- Sumitomo will work with the local developer, Reconciliation Energy Transition Inc (RETI), to build the hub, including a compression facility and pipelines

- The companies are considering using the captured CO2 to produce SAF.

- CONTEXT: The project, which will be located near Calgary, will be one of the world’s biggest hubs for capturing and storing CO2 when completed. It will likely store carbon from a nearby natural gas power plant, as well as others in the area. Marubeni is also participating in a carbon capture project in the vicinity of Calgary.

- SIDE DEVELOPMENT:

MHI tests pilot CO2 capture unit in Belgium

(Company statement, May 21)- MHI is testing a pilot carbon capture unit at its Gent steelmaking site to assess the feasibility of full-scale deployment.

- The unit will operate for up to two years, capturing CO2 from blast furnaces and reheating emitted gasses.

- CONTEXT: The EU has set an annual target of 50 million tons of CO2 storage by 2030. The IEA claims that CCUS technology must be applied to at least 37% of primary steel production by 2050 in order to meet climate goals.

Toyota’s liquid hydrogen racing car improves cruising range

(Company statement, May 24)

- Toyota Motor has improved the cruising range of its liquid hydrogen-fueled racing car by 50% to up to 135 km.

- A new dual-drive crank mechanism was developed to improve durability of the pump that sends the hydrogen to the engine.

- CONTEXT: The racing car, a Corolla model, is due to take part in the Super Taikyu Fuji Race held over May 24-26.

MHI receives order for 12 units of outer vertical target for ITER

(Company statement, May 20)

- MHI secured a contract from Japan’s National Institute for Quantum Science and Technology (QST) to produce 12 more outer vertical target units for the ITER fusion reactor in France.

- CONTEXT: ITER is an international nuclear fusion research and engineering project aimed at creating energy through a process similar to that of the Sun. It’s located in Cadarache, France, and the goal is to prove the feasibility of fusion as a large-scale and carbon-free source of energy.

- This brings MHI’s total for ITER to 18 out of 54 units. Deliveries will begin in 2026.

- CONTEXT: The divertor is a critical component of the tokamak fusion reactor. It discharges unburned fuel and impurities to maintain plasma stability. In 2023, MHI also produced five of the 19 toroidal field coils for ITER.

Chubu Electric, Miura agree to develop ammonia boilers

(Company statement, May 21)

- Chubu Electric and Miura Co signed an R&D contract to develop small industrial boilers fueled by city gas and ammonia. They’ll also study the possibility of Chubu Electric Power Miraiz marketing the boilers.

- The research will focus on reducing NOx emissions and ammonia flammability in high temperatures.

Osaka Gas completes methanation demo facility

(Company statement, May 17)

- A methanation demo project by Osaka Gas, in conjunction with Osaka City and the Osaka Wide Area Environmental Facilities Association, has been completed.

- The demo aims to build a methane supply chain by combining hydrogen from renewable energy and biogas from food waste. Methane is then transported via pipeline for use in urban gas consumption devices.

- The project aims to manufacture 5 Nm3/h of e-methane from 1 ton/ day of food waste-derived biogas and renewable energy-derived hydrogen.

- Tests at the facility will continue until July. Then, the methanation demo equipment will be moved to the Osaka Expo site.

NEWS: ELECTRICITY MARKETS

Mizuho Financial Group to provide assistance to shut down coal plants in SE Asia

(Nikkei Asia, May 21)

- Starting July, Mizuho Financial Group (MFG) will offer funding to coal plant operators to repay loans or pay dividends early, helping with the shutdown of these plants.

- The funding will be limited to operators transitioning to low-carbon energy projects.

- CONTEXT: Coal plants in Asia have a much younger average age than the coal plants in Europe or North America. In countries such as Indonesia and Vietnam, early shutdowns can cost up to $300 million. The UN asked OECD countries to phase out coal by 2030, but other nations have a 2040 target. While 70% of OECD coal capacity will retire by 2030, only 6% outside the OECD will retire by that year.

TAKEAWAY: Japanese banks, including MFG, pledged to cut coal financing by 2040. MFG has already reduced its coal sector financing from ¥300 billion in 2019 to ¥236 billion in 2022. MFG has come under criticism from NGOs since it is ranked as the biggest private lender for new coal power plants worldwide. It made $16.8 billion in direct loans to coal plant developers in 2017-2020. There have also been online campaigns targeting MFG. The other major Japanese banking groups, Mitsubishi UFJ Financial Group and Sumitomo Mitsui Financial Group, have faced similar criticisms. Investments in coal power plants were focused in Vietnam, Indonesia, and Bangladesh. Now MFG is trying to improve its image and decarbonization efforts.

Google signs long-term solar deals to power data centers

(Japan NRG, May 24)

- Google inked deals with renewables providers to build dedicated solar farms for its data centers in Japan.

- This includes corporate PPAs with Clean Energy Connect (CEC) and Shizen Energy.

- CEC will invest ¥10 billion through 2026 to build around 800 solar farms that will provide about 70 MW of capacity.

- The virtual PPA signed with Shizen will provide Google with environmental attribute certificates derived from a 20 MW AC solar project developed by Shizen.

- The solar plant will be built on a former golf course near Google’s data center in Inzai City, Chiba Pref. Operation is expected to start in 2027.

- Google will decarbonize its operations in Japan by using “non-fossil certificates,” which will confirm that none of the electricity is derived from fossil fuels.

- CONTEXT: By 2030, Google wants 100% of electricity consumed at its data centers and offices to be sourced from renewables. While renewables account for about 90% of Google’s power consumption in some U.S. states, in Japan that figure is 16%. Google is expected to also set up data centers in Hiroshima and Wakayama Prefs.

- CONTEXT: Google isn’t the only tech giant pursuing PPAs in Japan. Amazon cooperates with trading house Mitsubishi, CEC and other firms to supply solar energy to its Japanese data centers and other facilities. Microsoft signed a corporate PPA with Shizen, and its dedicated solar plant launched in February.

UAE’s Mubadala makes first renewables investment in Japan, to focus on solar

(Company statement, May 20)

- UAE state-owned Mubadala invested in Hong-Kong-based PAG’s Asia Pacific renewable energy platform that mainly focuses on supplying solar power to companies across Japan.

- The platform – PAG REN I – aims to operate across developed economies in APAC. The fund will invest in renewable energy assets in Asia, with solar generation in Japan a priority.

- The platform will use Japan’s corporate PPA framework to help businesses purchase electricity directly from renewables suppliers on a long-term basis.

- CONTEXT: While the investment size has not been disclosed, PAG says it raised $500 million from investors including Mubadala, which seeks to help Japan meet its ambitious target to install 108 GW of solar capacity by 2030.

OCCTO releases upbeat update on power reserve margins forecasts for the summer

(Denki Shimbun, May 22)

- OCCTO released a draft electricity supply and demand verification report that includes forecasts for summer supply and demand (July to Sept).

- The report forecasts that the minimum required reserve ratio of over 3% can be secured in all areas by factoring in the supply capacity of power sources that can be activated on command (i.e. dispatchable) and flexible power supply. This calculation also assumes weather similar to the hottest year in the past 10 years.

- During July and August, the reserve ratio will be in the 4% range in some areas based on measures to secure available capacity through the capacity market framework and other means.

- CONTEXT: The latest forecast is an update on the one presented on March 16. It takes into account the fact that several thermal plants such as the Kawasaki Station 1 Unit 1 (LNG, 490 MW) and Joetsu Station 2 Unit 2 (LNG, 585 MW) are not yet available due to repairs.

Orix launches virtual PPA under FIP as more firms switch from FIT

(Company statement, May 24)

- Orix is set to use the Feed-in Premium (FIP) program to launch a virtual PPA initiative for the trading of environmental value in renewables.

- This initiative will launch using a solar power system on the rooftop of a logistics facility in Atsugi (Kanagawa Pref) completed in April, and owned by Orix Group.

- The environmental value of excess electricity generated will be sold to offices and facilities owned and managed by Orix Real Estate.

- CONTEXT: The initiative is linked to Orix’s efforts to promote corporate PPAs in which it borrows the land or roof of an electricity consumer, installs power generation systems there, and supplies the electricity generated to the consumer.

TAKEAWAY: Since developers can use FIPs to reduce the cost of corporate PPAs, we can expect an increase in firms seeking to enter such contracts to benefit from the FIP system, which attributes the environmental value to power producers.

BESS connection applications rapidly expand, reaching 27 GW

(Denki Shimbun, May 24)

- With the expansion of renewable energy, applications for connection to BESS (Battery Energy Storage System) are growing.

- According to ANRE, the total capacity in nine areas nationwide reached 27 GW by late 2023, almost tripling YoY. Particularly notable was Hokkaido, Tokyo, and Kyushu, all of which exceeded 5 GW in applications.

- As the number of balancing power suppliers rises, more companies are starting to commercialize BESS.

- Not all connections considered will lead to actual contracts or grid connections. But out of a total of 27 GW of applications in nine areas nationwide, (excluding Okinawa), Tokyo has the most with capacity total of 5.35 GW, followed by Hokkaido with 5.24 GW, Kyushu with 5 GW, and Tohoku with 4.6 GW.

- Of the total applications, 2.93 GW of capacity has progressed to the more secure step of applying for a connection contract. It takes about two years from contract to installation.

- CONTEXT: BESS has been rapidly introduced in the past two years because the increase in variable renewable energy has made dealing with surplus electricity an urgent issue; the capacity and balancing markets have begun full-scale operation, and the applications for electricity storage are expanding.

- SIDE DEVELOPMENT:

ANRE considers new contract form for BESS and pumped storage hydropower

(Denki Shimbun, May 23)- ANRE held a meeting with experts to explore ways to improve the utilization of pumped hydro and BESS (Battery Energy Storage System), and to ensure that these facilities are able to operate in a more flexible and reliable manner to cover the nation’s growing reliance on variable renewable energy sources.

- Currently, there are issues including failed pumped storage bids in the Balancing Market, operated by EPRX.

- In response, the energy agency will look at new contract forms or compensation schemes for operators of pumped hydro and BESS, which would be options alongside revenue from balancing and ancillary services markets.

- Additionally, the agency presented a policy to make the Intraday Market operate under a system similar to the balancing and ancillary services platforms. The changes may introduce new bidding processes for both contracted and non-contracted power sources, ensuring that additional power can be sourced as needed.

- CONTEXT: Officials are looking to offer more options to market operators to manage their energy storage facilities, but also to ensure the energy system’s overall efficiency and stability is maintained or improved.

Renova to develop 240 MW onshore wind power farm

(Company statement, May 20)

- Renova plans to develop an onshore wind farm in Higashidori Village (Aomori Pref). In early May, the firm released an environmental impact assessment outline for the project, with a planned maximum output of 240 MW.

- Construction is set to begin in August 2029, with commercial operation to begin in August 2034.

- CONTEXT: There are two other projects planned in the area by ENEOS Renewable Energy and Cosmo Eco Power.

- SIDE DEVELOPMENT:

J-Power ninth wind power farm begins operation in Hokkaido

(Company statement, May 20)- J-Power Group’s wholly owned subsidiary, J-Wind Kaminokuni, launched its Kaminokuni No. 2 Wind Farm in Hokkaido.

- Output is 43 MW, using 10 SE Gamesa turbines, each with 4.3 MW.

Taiwan’s HDRE increases presence in Japan with new subsidiary, to focus on LTDA

(Company statement, May 24)

- Taiwan’s HD Renewable Energy (HDRE) set up a subsidiary in Japan.

- HDRE recently secured two contracts in Japan’s first long-term decarbonized power auction for energy storage projects with capacity totaling 73 MW in Mie and Fukuoka Prefs, with operations expected to begin in 2027.

- The firm’s GM has been quoted as saying the firm aims to establish 1.5 GW of storage systems in Japan within 3 years. With the win, HDRE has become the first Taiwanese company to penetrate the Japanese storage system capacity market.

- CONTEXT: LTDA refers to the Long-term Decarbonized Power Auction run by OCCTO under METI.

Toshiba develops tech to predict amount of electricity generated by wind farms

(Company statement, May 22)

- Toshiba has developed technology to forecast the amount of electricity generated by wind power plants.

- With a proprietary AI, and by using weather forecasting that calculates wind power based on a power plant’s topography, Toshiba says it achieved high accuracy in its estimation of electricity volumes.

- The tech will be installed in Toshiba Energy Systems’ renewables balancing system, REBSet, and the service will be launched by the end of FY2024.

- Toshiba ESS and Toshiba Next Craft Berkeley verified the tech under a METI project, and the results showed the average forecasting error for wind power generation in the morning of the previous day at 10.1%, an improvement from the 17.3% average error in the previous year.

JERA, MODEC, etc secure AIP for TLP-type floating wind turbines

(Company statement, May 21)

- A group comprising JERA, MODEC, construction firm Toyo Construction and electric equipment firm Furukawa Electric secured an Approval in Principle for their project on cost reducing tech for TLP floating wind turbines.

- CONTEXT: AIP refers to an assessment scheme to confirm the technical feasibility of a system design in its early stages, based on drawings and documents from the perspective of existing regulations.

- The project is run under NEDO’s Green Innovation Fund.

- The firms aim to establish component tech for TLP floating, mooring, and subsea power transmission systems to commercialize floating wind farms in the early 2030s.

- CONTEXT: TLP or Tension Leg Platform is a floating structure moored by tendons connecting the structure and anchors on the sea bottom. This system ensures stability of the platform under extreme environmental conditions. It is expected to reduce the cost of power generation because the high stability of tension mooring with a seafloor foundation enables installation of large 15 MW-class wind turbines. These are expected to become mainstream on compact floating platforms.

MOL group completes O&M training facility for offshore wind

(Company statement, May 21)

- Mitsui O.S.K. Lines (MOL) and its group firm Hokutaku, Japan’s largest wind turbine maintenance company, completed construction of a training facility specializing in practical operations and maintenance for offshore wind power generation.

- The firms will provide maintenance training based on Hokutaku’s expertise and case studies from Europe.

NRA approves change to Chugoku Electric’s decommissioning plan for Shimane NPP

(Company statement, May 17)

- Chugoku Electric secured NRA permission to alter its decommissioning plan for Shimane NPP Unit 1.

- CONTEXT: The decommissioning plan was approved in April 2017. Work began in July of the same year.

- SIDE DEVELOPMENT:

KEPCO resumes operation at Takahama NPP Unit 4 after inspections

(Company statement, May 21)- Full-scale operations resumed at KEPCO’s Takahama NPP Unit 4 (PWR, electric output 870 MW, thermal output 2.7 GW); periodic inspection began on Dec 16, 2023.

- The restart was delayed by 21 days because of damage to the heat transfer tube in the steam generator.

Toshiba completes new 300-mm wafer fabrication facility for power chips

(Company statement, May 23)

- Toshiba completed a new 300-mm wafer fabrication facility for power chips in Ishikawa Pref. The firm plans to start mass production in the second half of FY2024.

- The firm says that energy from renewable sources and solar panels on the facility’s roof (onsite PPA) will allow it to meet 100% of its power demand.

- Toshiba expects to receive a grant from METI to subsidize its investment.

Hitachi Energy to invest an additional $1.5 bln to ramp up transformer production

(Company statement, May 23)

- Hitachi Energy will invest over $1.5 billion to boost its global transformer production capacity in response to growing demand amid clean energy expansion.

- This investment in capacity will run through 2027.

- CONTEXT: Hitachi Energy is the world’s largest transformer manufacturer in terms of installed base, portfolio range, manufacturing capacity, and market coverage, with over 60 transformer factories and service centers across the world.

- The investments will span Europe, the Americas, and Asia. For example, around $180 million will be invested in a new state-of-the-art transformer factory in Finland.

- CONTEXT: The $1.5 billion is in addition to the $3 billion that has been invested globally in manufacturing and engineering, R&D and partnerships. Hitachi integrates more than 150 GW of HVDC links into power systems across the globe.

NEWS: OIL, GAS & MINING

Japan, Malaysia leaders discuss decarbonization, rare earth collaborations

(Government statement, May 23)

- PM Kishida met with PM Anwar of Malaysia who visited Japan. In addition to defense issues, they discussed collaboration in energy, decarbonization, securing of rare earths and other critical minerals, etc.

- CONTEXT: Starting 2023, Malaysia has introduced more control over rare earth exports, allowing only processed product exports and not the sale of raw materials.

Zachry Holdings goes bankrupt, Chiyoda and US LNG project impacted

(Bloomberg, May 22)

- Construction company Zachry Holdings filed for bankruptcy due to rising costs at the “Golden Pass” LNG project in Texas. Building work on the project began in 2019 but geopolitical issues and the pandemic disrupted progress, which created severe financial strains, according to Zachry, which now plans to exit the project.

- The project is 70% owned by QatarEnergy and 30% by ExxonMobil; it had planned to start operations by mid-2025.

- CONTEXT: Chiyoda was in charge of the project’s design phase, and then teamed up with Zachry and McDermott to build the three LNG trains.

MOL signs long-term charter deal with JERA for LNG carrier

(Company statement, May 22)

- Mitsui O.S.K. Lines (MOL) announced a contract for a long-term charter for a LNG carrier, signed with a vessel operation management company financed by JERA.

- This is the seventh contract of its kind. The new vessel will be built at Samsung Heavy Industries’ Geoje Shipyard in South Korea. Delivery is planned for 2026.

LNG stocks increased 6.6% from the previous week

(Government data, May 22)

- The LNG stocks of 10 power utilities were 2.26 million tons as of May 19, up 6.6% from the previous week (2.12 million tons). This is 6.2% down from end May 2023 (2.41 million tons), and 7.1% up from the past 5-year average of 2.11 million tons.

- CONTEXT: Rainy season is about to start in a week or so; hot and humid days are ahead.

April Gas/Coal Trade Statistics

(Government data, May 22)

|

Imports |

Volume |

YoY |

Value (Yen) |

YoY |

|

Crude oil |

12.3 million kiloliters |

-3.9% |

1,006.5 billion |

13.1% |

|

LNG |

5.3 million tons |

16.7% |

468.9 billion |

12.5% |

|

Thermal coal |

7.6 million tons |

5.0% |

189 billion |

-33.4% |

ANALYSIS

BY MAYUMI WATANABE

Ammonia or Methanol: Which is the Winning Zero-Emission Ship Fuel?

Decarbonizing the maritime transport sector counts as one of the most important tasks in the energy transition. Each year, global shipping leaves an emissions trail greater than that of the world’s passenger car fleet. To green this sector, the maritime industry is seeking the most effective and viable solutions.

In FY2022, Japan’s CO2 emissions from the shipping sector were 10.1 million tons, which excludes oceangoing vessels that are not included in the national greenhouse gas inventory. Oceangoing shipping accounts for about 2% of total global emissions.

The International Maritime Organization (IMO) has set a goal to cut emissions by 40% in 2030 from 2008 levels. According to ClassNK, in order for Japan to meet this target, a quarter of its shipping fuel needs to avoid creating a CO2 footprint; and, the country needs new ‘zero emission’ ships.

Among the various clean energy solutions considered, the main one focuses on which fuel should replace the heavy marine fuel oil currently used by vessels. Candidates include ammonia and methanol, but there’s also talk of shifting to synthetic methane and bio-derived fuel options.

Among fuel alternatives, the degree of carbon reductions differ, as does the speed at which they can be introduced to the market. This analysis assesses the readiness of new shipping fuel candidates in the regulatory, ship development and supply aspects.

Agreements in place, but logistics are not

In the past six-months, Japan’s shipping sector has moved to accelerate the shift to ammonia and methanol from fossil fuels. In December last year, the city of Yokohama and Mitsubishi Gas Chemical signed a Memorandum of Understanding (MoU) with global shipping firm Maersk to explore green methanol bunkering in the port of Yokohama.

In April, the world’s second largest methanol-fueled container vessel, owned by Maersk, made a port call. In June, NYK Lines will begin operation of the world’s first ammonia-fueled tugboat in the Tokyo Bay area, which includes Yokohama.

Japan has 932 ports, and any ship fueled by ammonia or methanol is able to enter any port, and offload and load cargoes. While port authorities have no right to block the entry of such ship entries, they won’t be able to re-fuel. Presently, most ports only have the capacity to supply marine residual fuel. About 4 million kiloliters/ year (25 million barrels) of marine residual fuel is used for ships in Japan.

Japan has no facility to serve other fuels, including LNG, and there are only two vessels for LNG bunkering. Onshore storage facilities and bunkering vessels for ammonia and methanol can’t be built because of a lack of clear operational and safety rules specific to filling ammonia and methanol into ship fuel tanks.

Compared to methanol or methane, ammonia has low flammability but it’s hazardous, causing death if direct exposure exceeds 5,500 ppm. Methanol is highly flammable, but its health risk is much lower compared to ammonia.

Ammonia, methanol, methane data

|

Ammonia |

Methanol |

Methane | |

|

Flammability limit |

15% |

6% |

1-6% |

|

Minimum ignition energy |

8 mJ |

0.14 mJ |

0.274 mJ |

|

Health risk |

Death or respiratory problems at 5,500 ppm dosage |

Drowsiness, muscle pains, etc. |

Skin and eye irritation, etc. |

Regulatory information gap

Relevant laws on ship refueling are the Ship Safety Act, the Act on Port Regulations and the Act on Prevention of Marine Pollution and Maritime Disasters. In 2013, the Ministry of Land, Infrastructure, Transport and Tourism (MLIT) wrote LNG bunkering guidelines to supplement those first written almost 90 years ago. The guidelines were updated in June 2023.

Following consultation with the Japan Coast Guard, which has oversight over the Act on Port Regulations, the MLIT is expected to write similar guidelines for ammonia and methanol bunkering.

In 2022, ClassNK published proposed guidelines on ammonia and methanol ships that could serve as the basis for MLIT’s guidelines. It recommended fuel tank design, piping, ventilation, alarm systems, etc that are relevant to ship structures, but they don’t address issues outside ship design, for example specifying mandatory reporting.

Availability of ships

Municipalities with ambitions to build ammonia supply chain networks by winning national government subsidies are hoping for the early release of ammonia bunkering guidelines. Some industrial stakeholders, however, believe that methanol bunkering could be more practical. ClassNK said that since ammonia is highly toxic, all possible risks must be considered; while other fuels won’t require intensive risk analysis.

As opposed to liquid ammonia that’s stored at -33 C, methanol is stored at room temperature. Present facilities for fuel oil storage and delivery could be used for methanol, which greatly reduces costs. Another methanol advantage is that merchant fleets are already using the fuel for commercial operations.

Major methanol-accommodated shipbuilding contracts in 2023

|

Contractor |

Builder |

Delivery timeframe |

Ship description |

|

NA |

Tsuneishi Shipbuilding |

NA |

Four dual-fuel container vessels each with 5,900 twenty-foot equivalent unit (TEU) capacity |

|

Evergreen Marine Asia |

Nihon Shipyard, Samsung Heavy Industries |

About 2027 |

24 dual-fuel container vessels each with 16,000 TEU capacity |

NYK Bulkship owns three dual-fuel ships that will operate on marine residual fuel oil and methanol. Although small, there is demand that’s poised to grow as orders for dual-fuel ships continue to rise.

Meanwhile, developments on the ammonia front are also making progress. In June, Sakigake, the world’s first ship fueled by ammonia will make its first sail in Tokyo Bay. Sakigake is a tug boat owned by NYK Lines with a gross tonnage of 272 tons.

It was originally an LNG-fueled vessel, converted to ammonia specifications by IHI Power Systems. Marine residual oil (grade-A heavy fuel oil) will ignite the engine and then Sakigake will be fueled entirely by ammonia during its journey.

Shin Nippon Kaiyosha, a NYK group company, will operate Sakigake, with its crew of two or three. The market, however, will have to wait until 2028 to see construction of a fully-fledged ammonia-fueled ship that’s completed and ready to sail.

Fuel availability

Currently, over 90% of the world’s methanol production uses natural gas as feed. While it is effective in reducing sulfuric and nitrogen oxide emissions, its carbon footprint is only 15% lower than that of fuel oil. It would need to be replaced by ‘green’ methanol, which is either bio-based methanol or made from renewables-derived hydrogen.

One shipbuilder told Japan NRG that the global green methanol supply chain is not as robust as for ammonia, and that if demand outstrips supply then methanol for zero emission maritime fuel might not be economically sustainable.

Japan has 1 million tons/ year of domestic ammonia production, and it imports all of its methanol requirements of 1.8 million tons/ year. Each year the country will need about 7 million tons of green methanol in order to replace the current annual consumption of 4 million k of fuel oil.

Using CO2 and hydrogen from chemical plants, Japan’s leading methanol manufacturer, Mitsubishi Gas Chemical, plans to produce green methanol in the Mizushima industrial zone (Okayama Pref). The goal for annual output is 100,000 tons by 2030.

Will the government offer the same level of support to build a global green methanol supply chain like it is doing for ammonia and hydrogen? That will depend on international trends, said a MLIT official.

As methanol gains traction in the global shipping industry, Japan will seek to expand its market share there. But for the time being, the government will also continue to support the growing penetration of ammonia, pinning hopes that either one or both of the fuels – with Japanese technology embedded in the supply chain – will turn out to be a game changer.

ANALYSIS

BY YURIY HUMBER

Mo’ Power, Mo’ Problems? Japan’s Chip Revolution is

Reversing Power Demand Picture

As Japanese energy planners sit down this spring to update the nation’s strategy, there’s one key assumption they need to rethink entirely. The sixth iteration of the Basic Energy Plan, ratified in October 2021, forecasted that electricity demand would fall 10% this decade thanks to greater efficiency and more conservation. Few would argue that today.

In the last two years, an ambitious state push to revive semiconductor manufacturing in Japan has yielded fruit. The world’s biggest chip maker, Taiwan’s TSMC, opened its first fabrication plant in Japan in late February. As if by coincidence, after 24 straight months without electricity demand growth, March 2024 saw national power consumption tick up. And again, in April.

Within three years, at least two more major semiconductor fabs will open in Japan. Many more facilities that produce components, materials, and equipment for the chip plants are also in the works. That, and the rapid rise of generative AI usage, as well as Japan’s courting of global data centers, could see power demand for the digital sector alone jump by a factor of 10 in a matter of a decade, according to early estimates.

While Prime Minister Kishida’s government has fully backed the semiconductor and AI push, there’s been much less effort to grasp how this will impact the electricity system. Japan’s success at attracting chipmakers and data centers may even have come as a slight surprise. Today, officials are furiously updating their industrial and energy roadmaps. Without a quick reaction, the next surprise could be energy shortages.

Chips ahoy

A leading producer and innovator of semiconductor chips in the second half of the 20th century, Japan’s influence in the sector waned significantly in the 1990s. As a result, many of its facilities shuttered or curtailed output.

Major players, such as Toshiba, which invented flash memory, sold chip-related assets or exited the business. Toshiba Memory was sold in 2018 to private equity firm Bain Capital to help its parent firm survive severe financial straits. The Bain-controlled entity is now known as Kioxia, with Toshiba Corp remaining a minority shareholder.

The fortunes of Japan’s semiconductor manufacturers have turned around in recent years as the geopolitical tensions between the U.S. and China favored a shifting of supply chains to allied territories. As well as tempting industry-leader TSMC to open its first ever fab in Japan, METI has engineered the creation of a new semiconductor champion in the country – Rapidus Corp.

Rapidus has set an extremely ambitious target of catching up with leading global chip makers in a matter of a few years. The company started construction of its first fabrication plant in Hokkaido last year, and hopes to launch a pilot manufacturing line in 2025. Mass production is due to follow a year or two later.

These are not the only semiconductor facilities in the works. TSMC has already announced plans for a second factory in Kyushu, at the same location as its first, and is mulling a third. A rival chip-maker from Taiwan, PSMC, has joined with Japanese conglomerate SBI to build a fab in Miyagi Pref. Kioxia, the former Toshiba unit, has two new manufacturing expansion projects. And there are at least a dozen other new factories planned in Japan for various kinds of chips.

Major semiconductor investments planned in Japan

|

Company |

Location |

Description |

|

Rapidus |

Chitose, Hokkaido Pref |

Construction of No. 1 fab began in September 2023. Pilot production scheduled to start in 2025. |

|

TSMC (JASM) |

Kikuyu, Kumamoto Pref |

Aims to start full-scale operation by late 2024. Construction of No. 2 fab in Kumamoto finalized. |

|

PSMC |

Ohira, Miyagi Pref |

Constructing a foundry in the Sendai area in partnership with major financial institution SBI. |

|

Mitsubishi Electric |

Kikuchi, Kumamoto Pref |

Renovating the Shisui plant and constructing a pre-process plant for SiC devices. Scheduled to go online in April 2026. |

|

Nishi Ward, Fukuoka City |

Constructing a new post-process plant for power semiconductors as part of the Power Device Works in Fukuoka. | |

|

Rohm |

Kunitomi, Miyazaki Pref. |

Acquired the land and buildings at Solar Frontier’s Kunitomi Plant in November 2023. Will mostly produce SiC devices. Scheduled to go online in 2024. |

|

Kiyotakecho, Miyazaki City |

Expanding SiC device production at Lapis Semiconductor’s Miyazaki Plant. Scheduled to commence operations in October 2024. | |

|

Fuji Electric |

Goshogawara, Aomori Pref. |

Increasing SiC device production by Fuji Electric Tsugaru Semiconductor. Scheduled to start mass production in FY2024. |

|

Renesas Electronics |

Kai, Yamanashi Pref. |

Kofu Factory scheduled to restart in 2024 to mass-produce IGBT on a 300 mm line. |

|

Takasaki, Gunma Pref. |

In 2025, will start mass-producing SiC power semiconductors using a 6-inch line at the Takasaki Factory. | |

|

Micron Technology |

Higashihiroshima, |

Spending up to ¥500 bln in the next few years on Micron Memory Japan’s Hiroshima Plant. |

|

Sony Group |

Koshi, Kumamoto Pref. |

Acquired ~270,000m2 of land ~800m west of the Kumamoto Technology Center. |

|

Kioxia |

Kitakami, Iwate Pref. |

Constructing a second production center at Kioxia Iwate. Originally scheduled to go online in 2023, but postponed to no earlier than 2024 due to memory market conditions. |

|

Kaga Toshiba Electronics |

Nomi, Ishikawa Pref. |

Constructing a power semiconductor production building. Scheduled to go online in FY2024. |

|

Toshiba Electronics Devices & Storage |

Taishi, Hyogo Pref. |

Constructing a new building at the Himeji semiconductor plant to double post-process production capacity for automotive power devices. Scheduled to go online in or around spring 2025. |

|

Hamamatsu Photonics |

Higashi Ward, |

Constructing a 200mm-compatible pre-process plant for photo diodes and other products at the company’s main plant. Scheduled to go online in December 2025. |

|

Kita Ward, |

Constructing a new building at the Miyakoda Factory to expand post-process capacity for LiDAR semiconductor lasers and other products. Scheduled to go online in October 2024. | |

|

Minami Ward, |

Constructing a new building at the Shingai Factory, a post-process center for optical semiconductors. Scheduled to go online in May 2025. | |

|

Sanken Electric |

Ojiya, Niigata Pref. |

Renting a building at JS Foundry’s Niigata Plant to increase production of automotive power modules. Mass production scheduled to start in late 2024. |

|

Phenitec Semiconductor |

Yusui, Kagoshima Pref. |

Expanding the clean room floor area at the Kagoshima Plant. Scheduled to go online in FY2024. |

Source: Bungei Shunjū, company statements

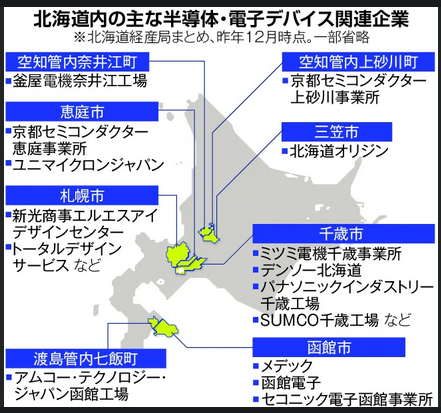

Of course, a semiconductor fab does not exist by itself; manufacture is reliant on at least two dozen or so suppliers of materials, components, equipment, and post-processing, the capacities for which also need to increase in Japan.

Eco-system for chips and electronic devices in Hokkaido (Dec ’23)

Source: Hokkaido Shimbun, Hokkaido Bureau of Economy, Trade, and Industry

How much energy does a chip need?

In 2025, at the stage of a pilot manufacturing line, the Rapidus semiconductor fab in Hokkaido will need access to about 100 MW of capacity, according to the firm’s own estimates. Once it ramps up to mass production, full capacity needs might escalate to 600 MW. That’s more electricity generation capacity than either of the first two units of the Tomari Nuclear Power Plant in Hokkaido, which has been offline and under inspection by the nuclear regulator for over a decade.

What’s more, Rapidus management vowed to procure all their electricity from clean energy sources, since their clients are likely to be major IT firms with net-zero commitments. This allows Rapidus to procure from renewable energy sources or nuclear. At present, Tomari NPP isn’t available. But even if its 912 MW Unit 3 is finally allowed to restart, local power demand won’t be sated.

Near the Rapidus fab will operate various suppliers as part of a planned semiconductor cluster. How much power they’ll require in total is still unclear, but according to U.S. experts, every $1 billion spent on new chip manufacturing leads to about $300 million in primary electricity purchases. That expenditure ratio doubles with data centers, said Mark P. Mills, the executive Director of the National Center for Energy Analytics, in recent testimony to the U.S. Senate.

In Kyushu, TSMC has not yet publicly articulated its energy demand, but its new semiconductor plant in Arizona, U.S. will require 200 MW at the first phase and then 1 GW at full capacity, the CSIS think-tank said last month, citing filings for the local transmission system expansion. The Taiwanese company used about 21 TWh of electricity in 2022. That’s equivalent to about 2.4% of Japan’s national total, or 40% of the volume generated by nuclear plants in FY2022.

Moving the needle, already?

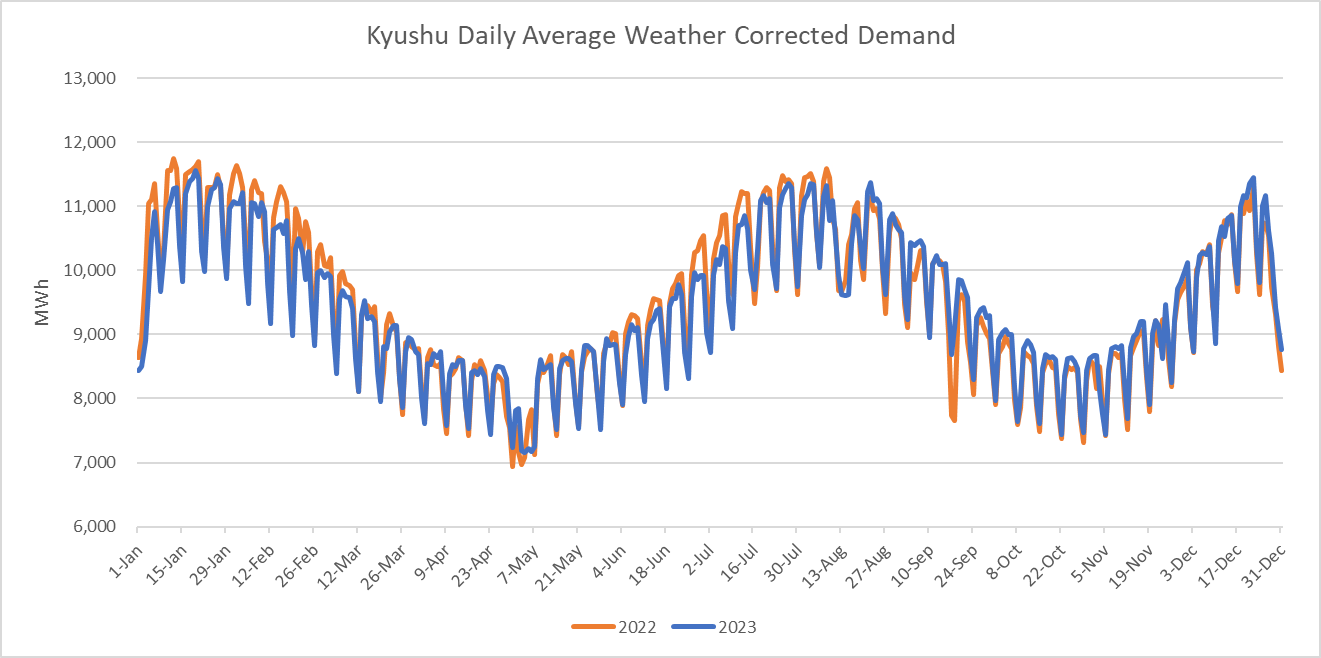

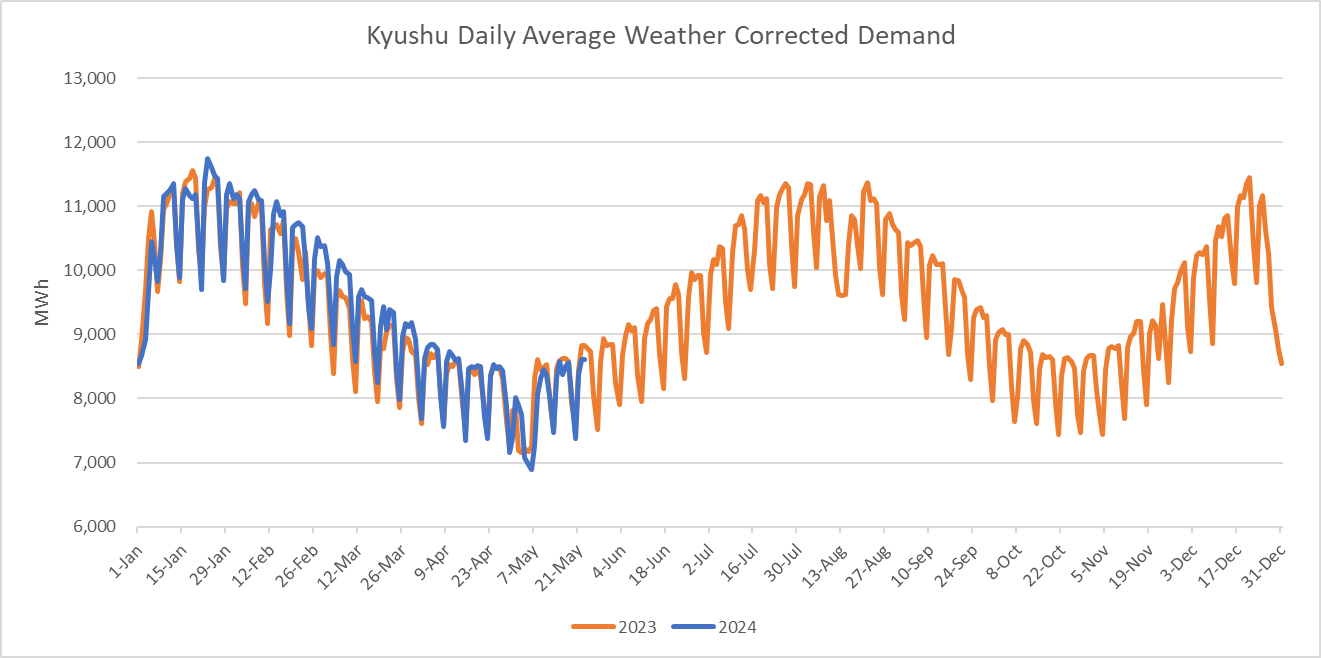

TSMC’s first factory in Japan has operated for only a couple of months, so it’s too early to make definitive conclusions. However, several trends are already visible, according to data provided to Japan NRG by energy forecasting specialist, Yes Energy.

On a national level, YoY electricity demand has been 0 or negative between March 2022 and March 2024. This is based on Yes Energy data that filters out weather impact on power demand; the data covers all the major grids in Japan apart from Okinawa. In March 2024, the demand was up 1.9% on a year earlier; in April, it was 0.1%.

Once we zoom into the electricity demand picture in the Kyushu region, however, things are even more stark. Kyushu’s YoY demand growth turned positive in September 2023. While that particular month’s consumption is ‘artificially’ inflated because of the power outages in Sept 2022 due to Typhoon Nanmadol, the rest of fall and winter 2023/24 shows positive weather-corrected demand growth even as nationwide figures are negative.

The leadup to the TSMC factory opening is a possible contributing factor, according to Mark Todoroff, business development director at Yes Energy. The demand switch starts to be seen after the August Obon holidays and continues into 2024, apart from two weeks in early January.

Source: Yes Energy

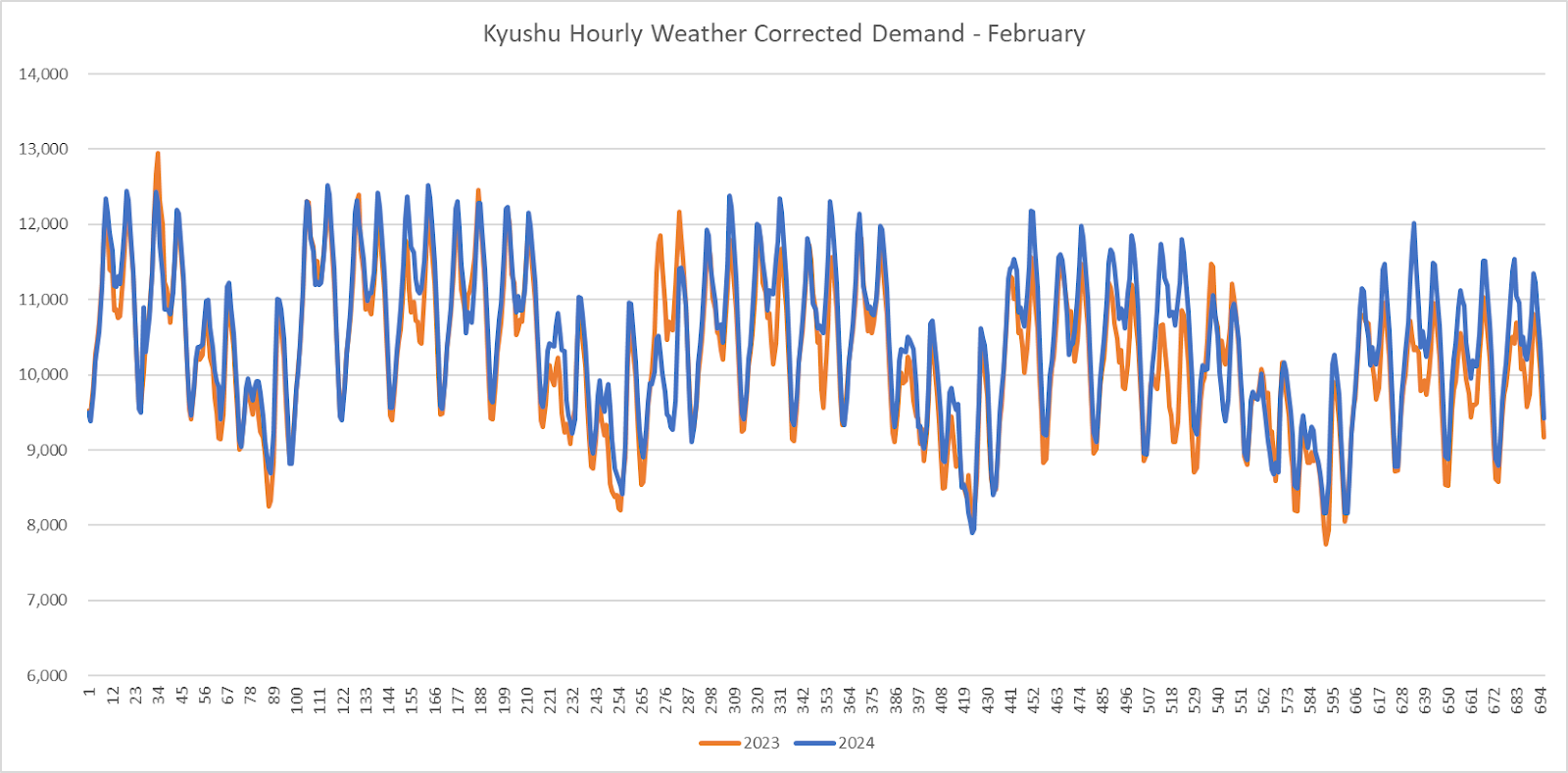

The demand uptick can be seen even more clearly when we zoom into the hourly demand picture.

Source: Yes Energy

Judging by the rollout of new semiconductor facilities nationwide, similar changes are coming to Hokkaido, Tohoku, and some parts of Kansai.

The nation’s energy planners thought this decade would be dedicated to replacing fossil fuels in a shrinking electricity system. Now they’ll need to consider how to shift to cleaner sources in an expanding market.

ASIA ENERGY REVIEW

BY JOHN VAROLI

This weekly column focuses on energy events in Asia and the Pacific

Australia / LNG

Shell expects that its Australian supplies of LNG will help meet demand from emerging markets in south and SE Asia. Philippines, Thailand, Vietnam and Bangladesh are expected to be key growth markets.

Australia / Nuclear power

The cost of nuclear power is six times higher than renewable energy, making it the most expensive energy source in Australia, according to the Clean Energy Council, adding that nuclear power stations are expensive and must run non-stop to break even.

BESS

Battery energy storage systems (BESS) are projected to be the most competitive power storage type because of the sharp decline in its cost due to innovation in technology and manufacturing. BMI reported that since 2010, the average installation costs dropped by 90%, making its price lower than pumped-hydro storage.

China / Oil and gas

Sinopec and TotalEnergies signed a strategic cooperation agreement to cover oil and gas development, LNG value chain, refining and chemicals, engineering and trading, and new energy.

China / Hydropower

A report by Cornell University claims that China’s decarbonization plan could negatively impact crucial river systems and farmland, especially due to hydropower expansion in the Mekong and Salween basins. Potential problems include river fragmentation and altered flood cycles.

LNG

Last week, Asian spot LNG prices rose to the highest levels since January; hot weather spurred demand for the fuel. In May, Asia remained the preferred destination for U.S. free-on-board LNG, with India, Japan, and South Korea resuming their buying.

South Korea / Hydrogen power

The country launched the world’s first auction for clean-hydrogen-fired power, for up to 6,500 GWh of electricity produced annually over a 15-year period, starting 2028. The 15-year contracts are for 100% H2-based electricity generation (using turbines or fuel cells), ammonia co-fired in coal power plants, or hydrogen co-fired at natural gas power plants.

Taiwan / Offshore wind

Copenhagen Infrastructure Partners (CIP) completed construction of the 600 MW Changfang-Xidao offshore wind project. It comprises 62 Vestas V174 turbines.

Thailand / SMRs

Thailand’s EGAT and EDF (France) discussed collaboration on developing Small Modular Reactor (SMR) technology. The goal is to diversify clean electricity production options, supporting Thailand’s carbon neutrality goals.

Vietnam / Renewable energy

Việt Nam Electricity reported that, to date, 29 renewable energy projects with a total capacity of more than 1.58 GW have been supplying energy to the national power grid.

2024 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

|

January |

|

|

February |

|

|

March |

|

|

April |

|

|

May |

|

|

June |

|

|

July |

|

|

August |

|

|

September |

|

|

October |

|

|

November |

|

|

December |

|

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Hulic Ochanomizu Bldg. 3F, 2-3-11, Surugadai, Kanda, Chiyoda-ku, Tokyo, Japan, 101-0062.