When the Japanese Advanced CCS Projects were first announced last year, only two of the seven projects involved overseas CO2 transportation. But METI has added two more international projects. By 2030 most of the planned CCS projects are slated to start commercial operation, yet much of the technology remains stuck in R&D. Project developers are worried about the overall cost assessment of the value chain. Japan NRG explores some of the challenges that the nascent carbon industry is facing in envisioning a CCS value chain to overseas storage sites.

Local and national authorities are looking for emergency backup energy sources that can be utilized quickly and flexibly. Restarting a mothballed coal or oil-fired power plant can take days. That’s why municipalities are turning to batteries, EVs, and other clean energy sources, seeking both lower emissions and a nimbler approach. Japan NRG takes a glance at energy emergency response measures implemented in the wake of major disasters, as well as recent trends showing increased reliance on renewables in the times of emergency.

ASIA ENERGY VIEW

A wrap of top energy news that impacts other Asian countries.

EVENTS SCHEDULE

A selection of events to keep an eye on in 2024.

JAPAN NRG WEEKLY

PUBLISHER K. K. Yuri Group

Editorial Team Yuriy Humber (Editor-in-Chief) John Varoli (Senior Editor, Americas) Mayumi Watanabe (Japan) Kyoko Fukuda (Japan) Magdalena Osumi (Japan Filippo Pedretti (Japan) Tim Young (Japan)

New Energy and Industrial Technology Development Organization

kWh

Kilowatt hours (electricity generation volume)

TEPCO

Tokyo Electric Power Company

FIT

Feed-in Tariff

KEPCO

Kansai Electric Power Company

FIP

Feed-in Premium

EPCO

Electric Power Company

SAF

Sustainable Aviation Fuel

JCC

Japan Crude Cocktail

NPP

Nuclear power plant

JKM

Japan Korea Market, the Platt’s LNG benchmark

JOGMEC

Japan Organization for Metals and Energy Security

CCUS

Carbon Capture, Utilization and Storage

OCCTO

Organization for Cross-regional Coordination of Transmission Operators

NRA

Nuclear Regulation Authority

GX

Green Transformation

NEWS:ENERGY TRANSITION & POLICY

Japan’s next Basic Energy Plan likely to indicate strong electricity demand growth

(Japan NRG, Aug 23)

The next Basic Energy Plan might forecast the nation’s electricity demand to grow about 20% by 2040, driven by the buildout of energy-intensive industries like semiconductor manufacturing, as well as data centers and other digital infrastructure, according to people familiar with govt discussions.

The next Plan is likely to be published in early 2025, with February to April seen as the most likely time.

CONTEXT: Japan’s current edition of the strategic document was published in 2021. The Plan forecasted a 10% drop in electricity demand in Japan over the course of this decade. The Plan is updated every three years or so.

TAKEAWAY: Expectations for a decline in total electricity usage in the country were squashed in the last year after the emergence of mass-market generative AI models. Large Japanese corporations like SoftBank have vowed to build nationwide data center networks and pioneer home-grown genAI systems to support the nation’s competitiveness in the digital age. The quick emergence of AI as the next demand driver has caught the govt by surprise, but it’s now starting to provide its own outlook for the impact of this digital innovation. A 20% growth in 15 or so years is much lower than the numbers forecasted by experts, but it likely takes into account efficiency gains and various constraints on digital asset growth.

Hydrogen subsidy program likely to accept applications in late Sept, say industry insiders

(Japan NRG, Aug 23)

The Contract for Difference (CfD) subsidy program for hydrogen projects will likely start to accept applications from late September or October, according to industry stakeholders.

CONTEXT: Earlier this month, METI began public consultation on its proposal for the subsidies program and for definitions of what can be described as “low-carbon hydrogen”. Feedback is open until Sept 11.

The subsidies and standards follow the passing of the Hydrogen Society Promotion Act by the Diet in June.

Once the consultation period ends, and METI has had time to respond to public comments, pitches for financial support will be made by public-private groups interested in developing local hydrogen supply chains for industry. This will include those seeking to build import terminals and storage facilities.

TAKEAWAY: There are about six such groups at the moment, but another two may emerge by the time the tender closes, say industry stakeholders. METI may then take as much as six months to review applications and select subsidy recipients.

ANRE seeks public feedback on its plan to exempt state-approved low carbon hydrogen and ammonia supply facilities from major earthquake safety requirements.

Feedback is accepted until Sept 19.

CONTEXT: Hydrogen and ammonia storage and production sites are high-pressure gas facilities that would require internal earthquake safety rules reviewed by the local fire department and other authorities.

Chevron and Mitsubishi Power Americas, a subsidiary of MHI, will begin to produce green hydrogen in the state of Utah starting mid-2025.

Intermountain Power Agency (IPA) will source excess solar and wind power volumes from across the U.S. and supply them to ACES Delta.

Chevron is the biggest shareholder in ACES; other investors include Singapore’s sovereign wealth fund GIC, and a Canadian pension fund.

ACES expects to produce 100 tons of hydrogen per day using electrolyzers made by a Norwegian firm in which MHI is an investor. The fuel will be stored in salt dome caverns, a type of underground formation that is also used to store natural gas and oil.

The hydrogen will then be extracted as needed to be used as fuel alongside natural gas in IPA power plants. IPA has plans to add a 840 MW gas-co-firing plant that’s expected to run on 30% hydrogen.

CONTEXT: MHI claims this will be the world’s first large-scale green hydrogen production, storage and power generation project.

TAKEAWAY: The production volumes are quite small compared to the sizes of planned blue hydrogen projects. At such volumes, export of hydrogen makes little sense, while creating a local demand point for the fuel helps to improve energy efficiency and lower costs. Japan’s domestic hydrogen production projects are taking a similar approach. They will make up a smaller proportion of the Japanese hydrogen market but should play an important role in future hydrogen industry development.

Toyota Tsusho and Indonesia’s Pertamina will develop and supply biofuels and green hydrogen to the Patimban Port and industrial park in West Java.

They plan to start demos in 2026 and commercialize the project by 2028.

This is one of about 70 agreements expected to be signed at the Asia Zero Emission Community (AZEC) ministerial meetings in Indonesia.

CONTEXT: Launched in early 2023, AZEC is a Japanese-led effort to foster agreements that focus on decarbonization across Southeast Asia, involving both state-run and private companies from Japan, Australia, and ASEAN countries.

SIDE DEVELOPMENT: Nitto Denko to fully run boiler on green hydrogen in Q1 2025 (Japan NRG, Aug 21)

In early 2025, Nitto Denko plans to bring online Japan’s first industrial boiler fully fueled by green hydrogen.

Located at its industrial film and tape plant in Miyagi Pref, the boiler will be fueled by its own rooftop solar-derived hydrogen.

The electrolyzer will be operational on weekends when the factory is idle.

JERA Ventures, a unit of Japan’s leading power utility, has invested about $2 million in a U.S. startup called Power to Hydrogen.

Based in Columbus, Ohio, the firm designs and manufactures anion-exchange membrane (AEM) electrolyzers for hydrogen production.

JERA said the startup successfully addresses the key issue of stability for AEM technology with use of a unique electrolyzer configuration that can rapidly respond to changes in electricity input. This pairs it well with intermittent renewables.

Nippon Yusen (NYK) inked a deal to ship green ammonia from India to Japan in collaboration with Kyushu Electric, Sojitz, and a subsidiary of India’s Sembcorp Industries.

Those three companies plan to produce ammonia in India using renewable energy and aim to deliver 200,000 tons a year.

This volume is slated for industrial customers in the Kyushu region.

Toshiba and PLN Nusantara Power ink MoU on CCS in Indonesia

(Company Statement, Aug 22)

Toshiba Energy Systems & Solutions inked an MoU with state-owned PLN Nusantara Power (Indonesia).

The MoU calls for application of Toshiba’s CCS technology at PLN’s Paiton coal-fired power plants, where Toshiba has already supplied turbines and generators.

PLN will provide data from Paiton and other facilities to help with optimization.

CONTEXT: Indonesia relies heavily on thermal power generation, with over 80% of its energy mix coming from such sources in 2022. The country has a goal of carbon neutrality by 2060. Thus, there is increasing demand for low-carbon technologies, particularly CCS, in thermal power plants.

CONTEXT: Toshiba has been supplying steam turbines and other equipment to Indonesia since 1981. It has supplied nine turbines to PLN-operated power plants.

Jasmy, a company specializing in IoT systems, will launch its NCCX carbon credit exchange in late Sept that will be managed by Green Carbon.

It will offer a variety of carbon credit products, including J-Credits and other voluntary credits. The exchange will also support international voluntary credits.

NCCX aims to enhance the speed and efficiency of credit transactions by leveraging blockchain technology to prevent data tampering and double-counting.

Aisin eyes launching perovskite solar farms in Aichi

(Japan NRG, Aug 21)

Aisin is exploring running solar farms with perovskite solar cell modules at its subsidiary CVTEC in the city of Tawara, Aichi Pref.

Aisin has been developing PSC technologies for 20 years and recently installed a system prototype on the walls of its head office. It is studying various applications ahead of product commercialization in about 2030.

CONTEXT: Aisin is a Toyota group company that makes automotive components. CVTEC makes transmission components, but it recently launched an agribusiness following a request from Tawara municipality to step up climate action.

NEDO extended the deadline for a research project proposal on regulations related to building parts and materials integrated with perovskite solar cell modules.

The deadline is now Aug 29 instead of Aug 9. Companies, universities and research institutes are eligible to apply.

CONTEXT: NEDO plans to complete research on regulatory issues and standardizing PSC products by March 2025 in order to industrialize PSC as soon as possible.

Over the next 3 years, West Group (Hiroshima) and digital solutions provider Grid Corp (Tokyo) plan to develop AI-based, grid-scale battery energy storage, totaling as much as 800 MWh.

The first project (1.99 MW/ 10 MWh) will be in Nagato City, Yamaguchi Pref.

CONTEXT: West Group has built around 70,000 solar power facilities of various sizes with a total capacity of 2.3 GW. Grid Corp has worked with power firms on various AI initiatives such as ReNom Charge, an AI storage battery control optimization engine.

TAKEAWAY: As Japan seeks to increase the ratio of renewables in its energy mix, the market for grid-scale BESS is expected to grow. The govt is bolstering support for such projects, such as through the Long-Term Decarbonized Power Source Auctions launched last year. This has led to more utilities opening up their grids to energy storage facilities.

Battery producer NGK Insulators secured an order for sodium-sulphur (NaS) batteries for a demo project.

The batteries will be installed at the Taiwan Power Research Institute in New Taipei City. They’ll be used to absorb long-term electric power load fluctuations, peak shaving, peak-shifting between DT and NT, and also as emergency power sources.

The order is for the advanced type of NaS Battery, NAS MODEL L24 that was released in June 2024. Operation is expected to begin in 2025.

CONTEXT: The move to demo the use of NaS comes amid increasing electricity demand partly driven by the growth of Taiwan’s chip-related industries. NaS batteries have a high capacity that allows for long-term charge and discharge, and their degradation rate is below 1% annually thanks to reduced corrosion in cells.

Haikou Onoda Remicon (HOR), Idemitsu Kosan, and Nippon Concrete Industries were selected for a grant offered by Shiga Pref to trial the use of synthetic calcium carbonate as a construction material.

CONTEXT: Concrete sludge is a byproduct of concrete manufacturing, and consists of cement and water. The project, scheduled from July 2024 to March 2025, aims to promote CO₂ resource recovery technology.

Nippon Concrete Industries will operate the pilot plant and handle the transportation of the material. The goal is to achieve widespread use of this technology by FY 2026.

TAKEAWAY: While several entities are advancing this technology, the commercial use of CO2-derived concrete and similar materials is limited due to high production costs and competition from traditional products.

The Ministry of Land, Infrastructure, Transport and Tourism (MLIT) suspended issuing NOx emission certificates to Kawasaki Heavy Industries because it falsified the emission data of 673 ship engines.

The certificates will be issued after MLIT confirms KHI’s compliance. MLIT will also conduct probes.

CONTEXT: This is not the first such violation. There have already been similar cases of data fraud involving KHI industry peers MHI and IHI. In late April, IHI Power Systems was the target of a police raid following suspicions that the manufacturer tampered with data on 4,200 engines.

Hitachi Energy unveiled the world’s first switchgear enabling the long-distance transmission of large flows of electricity while eliminating emissions of sulphur hexafluoride (SF6), which is considered to be one of the most potent greenhouse gases.

The new technology is used in Hitachi’s EconiQ 550 kV circuit breaker that can be used in gas-insulated switchgear (GIS) or dead tank breakers (DTB), as well as the EconiQ 420 kV Live Tank Breaker (LTA).

Electricity transmission firms Hydro One (Canada) and Wesco (America) introduced the new tech at their substations in North America.

As energy markets and power grids expand and transition globally, the high-voltage switchgear market will also see growth, potentially reaching $60 billion by 2050. As much as 80% of total global SF6 emissions come from the power sector.

CONTEXT: SF6 has been widely used in power grid equipment due to its insulating qualities. It’s considered 24,300 times more potent than CO2 as a GHG, and remains in the atmosphere for over a 1,000 years whereas CO2 dissipates after 200 years.

Sumitomo Corp acquired a stake in EEW Offshore Wind EU Holding, a German manufacturer of monopile foundations for bottom-fixed offshore wind turbines.

Sumitomo didn’t disclose details but completion of the deal is set for late December.

Annual EU demand for monopiles is expected to rise from 650,000 tons in 2023 to over 1 million tons in 2026. EEW is the world’s largest supplier of monopiles.

CONTEXT: Sumitomo entered the European wind power business in 2014, and has several offshore wind sites, including near Dusseldorf. Sumitomo is involved in the development and operation of three offshore wind farms in Belgium, two in the UK and two in France. It has a 30% stake in the 219 MW Northwester 2 Offshore Wind Farm off the Belgian coast; a 29.5% stake in two French projects — Le Tréport and Noirmoutier, 496 MW each; and a 12.5% stake in German utility RWE’s Five Estuaries in the UK.

METI and OCCTO issued an interim report on the ‘simultaneous’ market framework.

It outlined the results of technical studies into the start up of power generation facilities and output allocation logic, as well as methods for determining market pricing.

CONTEXT: METI has been conducting a wholesale review of the current market structure for more than a year and a half. It’s keen to introduce a so-called “three-part offer” system, which would consider the three key factors that govern whether you can secure electricity in the market: availability of capacity, availability of volume, and the cost and time involved in getting this electricity to users.

The report showed results of a simulation that incorporated the one-hour-ahead market into the simultaneous market, resulting in lower computational load and time.

Future expert discussions will focus on refining the system by addressing factors like renewable energy forecasting errors and comparing the current auction system with the new proposed framework.

On Aug 22, JEPX began to add tracking information to non-fossil fuel certificates, which will contain key information such as power source type and production area.

CONTEXT: Until FY2023, all FIT non-fossil certificates could be tracked, while non-FIT, non-fossil certificates with a renewable energy designation derived from large hydropower and other sources could only be tracked upon request.

CONTEXT: FIT non-fossil fuel energy certificates have been traded since around the start of the decade. The first auction for non-FIT NFCs was in late 2020. Such certificates can also be sold bilaterally.

The Kiko Network (KN), one of Japan’s leading climate action NGOs, intensified criticism of JERA and its promotion of ammonia co-firing as a clean energy solution.

KN filed a complaint with the Japan Advertising Review Organization (JARO) against JERA advertisements that position the co-firing of ammonia in coal-fired power plants as a “zero-emission thermal power”.

KN and a lawyers’ group asked JARO to stop JERA and other power utilities from claiming co-firing is a technology that doesn’t emit CO2, saying this is misleading.

KN claims that JARO in May declined to investigate the issue because it was beyond its scope of judgment. As a result, the NGO has filed a complaint to the UN Secretary-General and asked for international monitoring.

For FY2023, Chubu Electric Power Grid reported mistakes in renewables generation curtailment — meant to prevent overloading or damaging the grid — at a total of 67 power plants.

It said the mistakes occurred due to omissions in updates or incorrect data input, and resulted in insufficient reduction of power output at 67 power plants.

Chubu Electric will make adjustments to balance the output from FY2024 onwards.

CONTEXT: Curtailment occurs when renewable energy sources, like solar and wind, produce more energy than the national grid can use. This happens when there’s an oversupply of energy, or when there are other constraints like congested transmission lines. Curtailments also mean lost financial opportunities for renewables projects.

On Aug 21, Kyushu Electric Power Transmission and Distribution received up to 350 MW of power from Kansai Electric Power Transmission and Distribution and Chugoku Electric.

The measure was needed because the reserve ratio was expected to fall below the 3% required for stable supply.

Kyushu Electric’s coal-fired Reihoku Power Station No 2 Unit (Reihoku Town, Kumamoto Pref) had to shut due to equipment troubles.

The Japanese big business community is advocating for promotion of nuclear power in the upcoming new energy policy plan, along with the construction of new plants and the replacing of aging facilities with new units, as well as continued development of next-gen reactors.

Business leaders stress the importance of ensuring predictability for investments, and want clear positioning of next-gen reactors in the energy plan.

There are concerns about declining nuclear capacity after 2040 due to aging reactors. Another issue is guaranteeing a stable nuclear fuel supply chain amidst geopolitical tensions.

CONTEXT: The lobbying is from the big three business groups in Japan: the Keidanren, the Keizai Doyukai, and the Japan Chamber of Commerce and Industry.

TEPCO will accelerate a decision on decommissioning Kashiwazaki-Kariwa NPP Units 1-5 in order to reassure the local community.

The decision was originally to be made within five years after the restart of Units 6 and 7, but that will now be shortened to within two years in order to address local concerns about nuclear safety; this is expected to help to advance the restart of the newer Units 6 and 7.

TAKEAWAY: The restart of Kashiwazaki-Kariwa NPP, TEPCO’s only operable NPP, is proving to be complicated. Therefore, the utility is trying to win over public opinion by announcing new commitments on safety.

KEPCO submitted to the NRA a long-term management plan for Takahama NPP Units 3 and 4. It incorporates measures for handling outdated technologies and managing discontinued parts.

The plan runs from June 6, 2025 until the 50th operational anniversary for each unit.

CONTEXT: These two units were already approved for extended operation beyond 40 years — up to 60 years — based on previous evaluations. Yet, the utility must also gain approval for the new long-term facility management plan. This is due to amendments of the Reactor Regulation Act (RRA) that takes effect in June 2025.

KEPCO submitted to the NRA a “Safety Enhancement Evaluation Report” for Takahama NPP Unit 3.

This includes evaluation of the reactor since the end of the periodic inspection, and also relates to the implementation of safety measures based on an improvement plan.

Japan Atomic Power Company (JAPC) will delay completion of safety upgrades at Tokai NPP Unit 2 due to issues found in the seawall construction — reinforcing bars in the foundation were deformed.

The work was originally scheduled to be completed by September, but it’s now planned through December 2026. This is the third postponement.

TAKEAWAY: Tokai NPP is of particular importance to Japan’s national plan to restart NPPs. Completion of safety upgrades have been delayed since 2018, and dissatisfaction is growing among local communities, with officials calling for better planning.

On Aug 19-20, the NRA inspected sites on the Noto Peninsula, focusing on areas affected by the earthquake. Damage from the tsunami was greater than expected.

The findings will be reported at a meeting in September.

The results might impact seismic design standards. Particularly, it could impact the nearby Shika NPP.

Recyclable-Fuel Storage (RFS) and five municipalities neighboring Mutsu City, (Aomori Pref), signed an agreement that calls for information disclosure to local residents and transparency regarding the spent nuclear fuel storage facility.

The agreement is part of efforts to boost safety and build trust with the community.

CONTEXT: This agreement comes just before the start of operations next month at the Mutsu interim storage facility, which will be Japan’s first.

Vena Energy submitted to the prefectural and municipal govts its environmental impact assessment for a 71.6 MW solar farm in Maniwa City, Okayama Pref.

The firm revised the plan and site in response to concerns over potential disaster risk.

In November 2020, the MoE requested environmental preservation measures to minimize the alteration of steep slopes and forested areas, and that the project be designed to properly dispose of trees and waste.

EX4Energy, a provider of communication services for the power industry, raised ¥350 million through a third-party allocation of new shares.

The funds will develop the platform, Public Power HUB, which allows solar power devices and systems to exchange information such as the amount of electricity generated, regardless of manufacturer or power company.

Toyo Engineering inked an MoU with Indonesia’s energy ministry to develop a geothermal master plan for Indonesia.

CONTEXT: Indonesia aims for net-zero by 2060. Toyo is promoting development of geothermal resources by combining different technologies underground and above ground. Toyo serves mainly the hydrocarbon processing and petrochemical sectors.

Seven-Eleven Japan will introduce solar-powered delivery trucks.

They will be deployed first in Kyushu by the end of August.

CONTEXT: The company expects each unit to reduce CO2 emissions by 3.7 tons/ year, and fuel costs by ¥180,000.

TAKEAWAY: Although Japan has made progress in EV development, expansion to rural areas is still a long shot given poor charging infrastructure there. Solar-powered trucks might be an interesting alternative to EVs or FCVs, but their reliability and capacity are as yet unclear.

INPEX Browse E&P won an exploration permit for its wholly-owned Block AC/P71 offshore Western Australia.

The block is near the AC/RL7 Retention Lease, where INPEX holds a 74% stake, and natural gas and condensate fields have been discovered.

CONTEXT: Nearby Block AC/P71 is the INPEX-led Ichthys LNG Project, which plans to produce 8.9 million tons/ year of LNG and 1.65 mln tons/ year of LPG. INPEX has a 67.82% stake in Ichthys.

On Aug 16, TOCOM trading in LNG futures took place for the first time in nearly two years, with 50 contracts executed due to a recently expanded “market maker system”.

The trades involved November contracts, with 20 contracts (20 billion BTU, or 20,000 mmbtu) executed in the morning and 30 contracts (20 billion BTU, or 30,000 mmbtu) in the afternoon. The prices were ¥2,090 and ¥2,110, respectively.

CONTEXT: With TOCOM also offering trading in power futures, the exchange is keen to offer the potential for participants to trade “spark spreads” (which is the price difference between the cost of procuring natural gas to fuel power plants and the price of electricity).

TAKEAWAY: Total contracts traded on Aug 16 would be less than one regular sized LNG ship cargo. At current trading volumes, it would be difficult for the exchange to attract financial players to grow the market, so TOCOM will first need to convince some of the LNG importers to use the platform to build up liquidity.

Nippon Steel and JFE Steel acquired a 20% and 10% stake, respectively, in Australia’s Blackwater coal mine.

The seller is Whitehaven, which holds the remaining 70%.

CONTEXT: The two steelmakers have been customers of Blackwater, which was owned by BHP Mitsubishi Alliance but sold to Whitehaven earlier this year.

TAKEAWAY: This year, JFE Steel closed its steelmaking plant in Kawasaki which will be converted into a liquefied hydrogen import terminal. This investment suggests the Kawasaki plant may be the last closure of coal-consuming blast furnace steelmaking in Japan.

As of Aug 18, LNG stocks of 10 power utilities were 1.92 million tons, 3% less from the previous week (1.98 million tons), but 11.6% up from end August in 2023 (1.72 million tons), and 5% down from the past five-year average of 2.02 million tons.

CONTEXT: JMA continues issuing heat stroke alerts across Japan. Even southwest Hokkaido was alerted. The long-term weather forecast is for higher-than-average temperatures until late October.

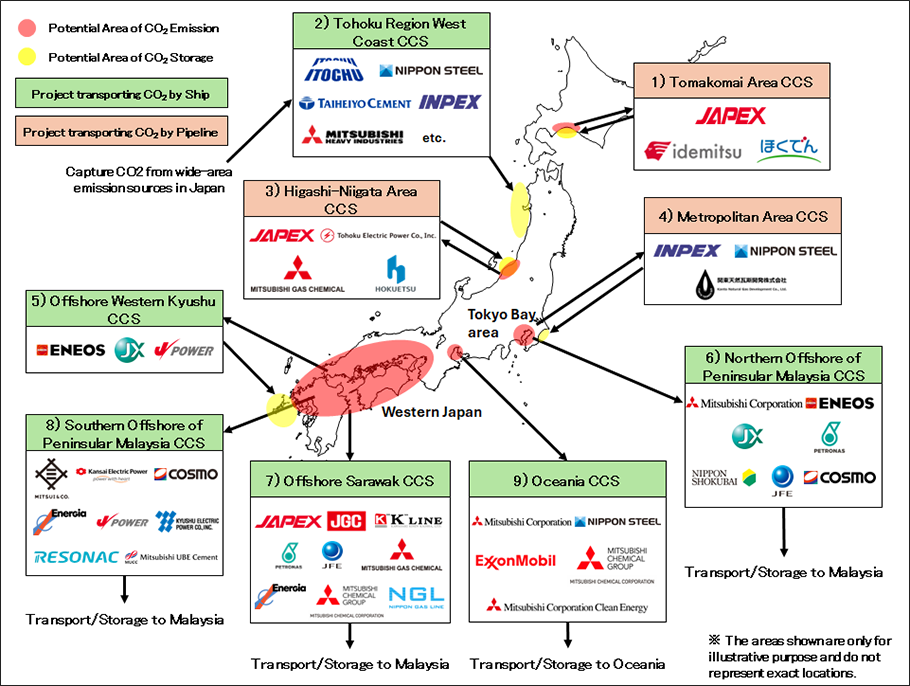

Can Japan Transform CO2 Sea Transport From Waste Management to Profit?

When the Japanese Advanced CCS Projects were first announced last year, only two of the seven projects required overseas CO2 transportation. But recently, METI added two more international projects, bringing the total to nine.

Now, of these nine, six will require marine transportation of CO2 — four to overseas locations and two to domestic sites.

JOGMEC has stated that shipping CO2 from Japan to overseas storage sites will be vital. Transportation of liquefied CO2 (LCO2) by ship is the obvious solution for the CCS value chain, and this will require grappling with both engineering and cost issues.

Most storage sites are expected to be in Southeast Asia, as well as Australia, which means long shipping routes that bring additional complications than if the CO2 was stored at home. Clarifying on how most efficiently to transport CO2 will be imperative.

By 2030 most of the planned CCS projects are slated to start commercial operation, yet much of the technology remains stuck in the R&D stage. Project developers are worried about the overall cost assessment of the value chain, urging the industry to move from its current engineering phase to more practical tests and applications.

Japan NRG explores some of the challenges that the nascent carbon industry is facing in envisioning a CCS value chain to overseas storage sites.

New CCS advanced projects

The two newly added international projects are located in Malaysia, adding to the other two overseas projects already included in the original list of seven – 1) the Offshore Sarawak CCS involving JAPEX, K-Line, JGC Holdings, Petronas CCS Ventures, etc, and which could store between 1.9 to 2.9 million tons of CO2 per year from industries in Setouchi region (Okayama Pref) such as steel, power plants, and chemical factories.

The second one is the Southern Malaysian Offshore Project that includes Mitsui & Co, Chugoku Electric, Kansai Electric, and others. Plans call for storing around 5 million tons of CO2 each year, targeting different industries such as power, cement, chemicals, etc in Kinki, Chugoku and Kyushu. Both projects, according to METI, will involve ships as well as pipelines for transportation.

Japanese Advanced CCS Projects

Source: JOGMEC

The two principal methods for mass CO2 transportation are by pipeline and ship. The first is most cost-effective when dealing with shorter distances, but as the distance increases, ships become necessary. A report by the Intergovernmental Panel on Climate Change (IPCC) claims that the financial break-even point is 1,000 km, but in Japan that figure can be lowered to 200-300 km, according to NYK and MHI.

Needless to say, this CO2 transportation method is not limited to the Japanese Advanced CCS Projects alone. Recently, Chubu Electric and BP told Japan NRG about plans for a major CCUS project at the Port of Nagoya and Indonesia’s Tangguh gas field. It seeks to annually capture 5 to 20 million tons of CO2 emissions that will be transported on 20 liquefied CO2 ships to Tangguh. Operations are targeted to begin by 2030, although the business model is still uncertain, and it will have to depend on government subsidies. The two companies will now proceed with a more detailed study before making a final investment decision.

Launching the CCS value chain

Marine transportation of CO2 is just one part of the overall CCS value chain. The first step is, of course, to capture CO2 from an emitting source. After that, a complete CCS value chain comprises the following phases:

Liquefaction

Temporary storage

Loading

Marine transportation

Heating

Boosting

Injection

In the final step, CO2 is injected directly into a offshore reservoir, or through a floating barge, or in an offshore terminal (and then into a reservoir). As with any other value chain, in order to be successful, minimizing the related costs is of crucial importance.

When it comes to the technical side of LCO2 ship transportation and its cost assessment, an important point to consider is the pressure method, of which there are three: Elevated Pressure (EP), Medium Pressure (MP), and Low Pressure (LP).

In March, NYK, in partnership with Chiyoda Corp and Knutsen Group, revealed the results of their studies on the three methods. Temperature and pressure specifications for the three look like this:

Mode

Temperature

Pressure

EP

from 0 to 10 C

34 to 45 bar

MP

from -30 to -25 C

15 to 18 bar

LP

from -50 to -45 C

6 to 10 bar

Considered were parameters such as operational risks, cost and energy consumption, and the type of tanks for CO2. According to circumstances, one method may prove to be better than another. In most situations, however, EP proved to be more cost effective when considering capital expenditure and operating expense. The cost stood between $52/ ton-CO2 (EP); and $59.9 (LP) for domestic transportation. In the case of overseas (from Japan to Australia), it rose to $90.3 (EP); and $103.6 (LP).

One reason is that EP is less energy intensive. Unlike MP and LP, CO2 is kept at ambient temperature in EP, not requiring refrigeration. Furthermore, EP allows for CO2 of less purity and usage of Knutsen NYK Carbon Carriers’s Cargo Tank Cylinders (CTC) tankers, two factors that make re-liquefaction unnecessary at the receiving terminal. One future goal for KNCC is to lower the cost of CTC tankers, which can handle 12 m3 of CO2 at a time.

CO2 density is actually a disadvantage for EP, since it’s lower than for the other methods. This means that larger tanks or more trips will be required in case of EP deployment. While this issue can be mitigated, it is one example of the factors that impede the possibility of establishing one method as superior to the others. Proceeding on a case-by-case basis remains essential.

Building the LCO2 carriers

LCO2 transportation by ship is a new industry, and the only notable CCS project involving shipping is Greensand in Denmark, which demonstrated crossborder CO2 storage, with CO2 captured in Antwerp transported by ship to Esbjerg, and then stored in a depleted oil field in the North Sea.

In April, Dalian Shipyard launched the first two LCO2 carriers with a 7,500 m3 capacity for the Northern Lights project in the North Sea, placing itself at the forefront of this industry. Before that, the only notable LCO2 carriers were four small-sized (1,000-2,000 m3) LCO2 carriers operated by Larvik Shipping built between 1999 and 2005.

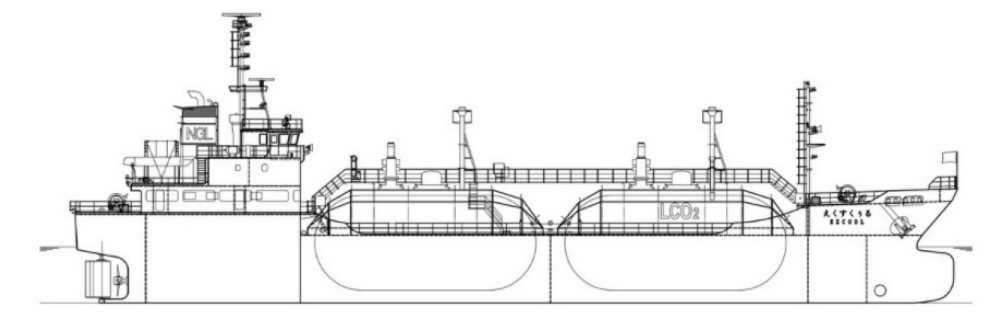

As for Japan, in February METI unveiled the LCO2 transportation ship Excool built by Mitsubishi Heavy Industries. It has two tanks with a total capacity of 1,450 m3, and starting October it will transport CO2 from KEPCO Maizuru Power Station in Kyoto Prefecture to Tomakomai, Hokkaido.

General Arrangement of Excool

Source: Mitsubishi Heavy Industries

With LCO2 carriers still few in number, one of the next challenges is to build an entire fleet. From the time of contract signing, two to three years is needed to deliver a finished vessel. Still, securing the required port facilities and CO2 tanks could be a more daunting challenge.

JOGMEC’s view

Japan NRG reached out to JOGMEC regarding its expectations for CO2 transportation by ship, and the answer was that it will be a key method for enhancing the feasibility of CCS projects. JOGMEC recognizes the challenges that need to be overcome in order to launch the industry in a cost-efficient and sustainable manner.

First, current domestic construction capacity for storage tanks and ships is not sufficient. These challenges were made clear last year in a feasibility study, which pointed out the necessity for increased capacity. JOGMEC intends to further explore the matter with the newly announced projects.

One of the key issues to address is the standardization of liquefied CO2 ship transportation in CCS projects. As this new industry emerges, common rules, guidelines and technical standards are lacking, and they need to be established together with the necessary infrastructure (such as facilities at ports). Furthermore, JOGMEC is considering collaborating with the government to develop support measures to resolve these issues.

Conclusion

Ironically, the greatest challenge faced by CO2 transportation is CO2 itself. As a product without inherent value, handling it is basically waste management. Therefore, finding the most cost efficient way to dispose of it will be a top priority. Technical details such as choosing the best transportation method, or enabling the production of sufficient tanks and ships, are all part of the solution to the big question – “How can we make this tech work?”

The next question could be: Is CCS worth the effort and resources? A CCS chain could turn out to be far more costly than emitters and receivers would like to hear. The best solution would be to turn waste into a valuable product (i.e., CO2 utilization), but this alone won’t impact the amount of CO2 that abatement projects aim to capture. Therefore, efficient storage remains essential.

CO2 will have to prove itself as a convenient product in sectors where it’s considered to be a candidate for utilization. The CCS business model currently has little benefit from a carbon credits market that is voluntary, as is the case in Japan. Those businesses and investors that are voluntarily interested in ‘going green’ tend to prefer to put money into options further removed from oil and gas.

The most powerful catalyst for a CCS value chain will likely be found in carbon crediting under a compulsory market and with a carbon tax framework. This will require careful governmental intervention, both in terms of funding and regulation.

METI’s 2030 deadline for commercializing the CCS projects is approaching, and it’s time for the businesses involved to decide what to do before the day of reckoning arrives. Positioning CCS as an effective industry that fosters decarbonization goals will require settling technical matters and, perhaps most importantly, guaranteeing profits for those involved. Few will pay for CCS on a voluntary basis.

ANALYSIS

BY MAGDALENA OSUMI

Japanese Municipalities Aim for Increased Use of Clean Energy in Emergencies

A series of natural disasters this summer, from an earthquake in south Japan to Typhoon Ampil along the coast of greater Tokyo, served as a reminder of the need to make energy systems resilient even in times of extreme crises.

Efforts to mitigate ensuing risks now extend to energy generation with a growing number of municipalities across the country seeking to switch from fossil fuels to renewable energy in order to secure power supply during emergencies.

The issue of securing backup sources is becoming more important as the mainstay of Japan’s energy system are aging thermal plants. This is a factor that even METI minister Saito recently underscored, noting that periods of extreme weather, such as this summer’s heat, are putting undue strain on domestic energy systems.

Given the difficulty in accurately predicting extreme weather impact, never mind the occurrence of a natural disaster, local and national authorities are also looking for emergency backup energy sources that could be utilized quickly and flexibly. Restarting a mothballed coal or oil-fired power plant would take days, even if it had received regular maintenance. That’s another reason why municipalities are turning to batteries, EVs, and other clean energy sources, seeking both lower emissions and a more nimble approach.

JapanNRG takes a look at some energy emergency response measures implemented in the wake of major disasters, as well as recent trends showing increased reliance on renewables in times of emergency.

Push for use of renewables-derived power in emergencies

The national government is urging municipalities to take the lead in introducing renewable energy to public facilities as part of measures for evacuation centers that are designated for use in disasters.

The goal to transition from thermal power to renewables-produced electricity during times of crises was included in the MoE’s disaster plan in 2020. The MoE allocated ¥2 billion in FY2024 on top of the ¥2 billion in the FY2023 supplementary budget for related initiatives. The amount covers subsidies for a portion of the cost of the installation of renewable energy generation facilities, cogeneration systems (CGS), and their ancillary facilities such as storage batteries, charging and discharging facilities, and CO2 reduction assets.

Perhaps the first example of when a local government in Japan reached for clean energy following a major disaster came in September 2018 when Hokkaido Prefecture procured power for some areas in the wake of an earthquake. Damage had led to a halt at Units 1, 2 and 4 at Hokkaido Electric’s coal-fired 1.65 GW Tomato-Atsuma Power Plant.

Early on Sept 8, the prefecture began to procure backup power using a redox flow grid-scale battery system at Hokkaido Electric’s Minami-Hayakita substation. That site paired solar power with batteries.

The Minami-Hayakita BESS, with a capacity of 51 MWh, and able to provide 17 MW for three hours, had been developed by Sumitomo Electric for Hokkaido Electric. The system, which is now in operation, was only launched at its current commercial scale in April 2022. However, it had already been installed in demo mode in 2015. At the time of the disaster, it was able to deliver power for four hours, at a rate of 15 MW.

Nissan lends a charge in emergencies

EVs are another solution to secure backup power during outages. In recent years, with a spate of natural disasters such as typhoons, torrential rains, and earthquakes, EV manufacturers have faced many requests to assist with their vehicles, including from municipal local governments.

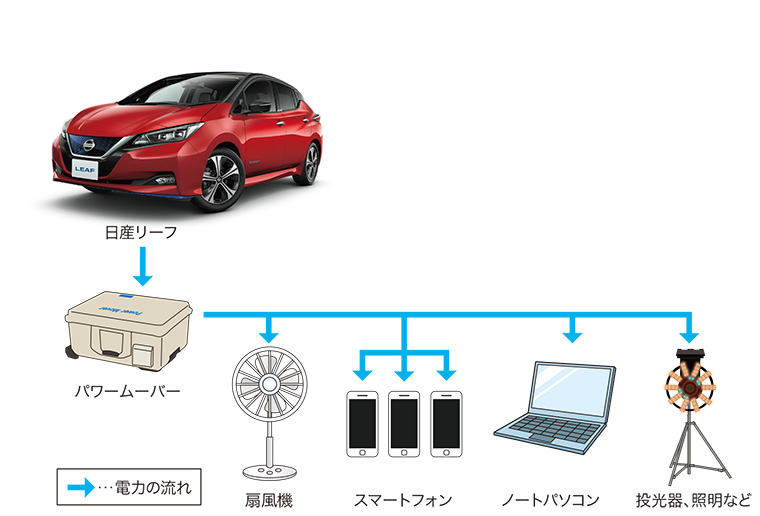

Towards that goal, in 2020, Nissan unveiled a 100% electric emergency response car concept, designed to provide a mobile power supply following natural disasters or extreme weather conditions.

The RE-LEAF prototype is based on the Nissan LEAF passenger car. Alongside modifications to navigate roads covered in debris, the car features weatherproof plug sockets mounted directly to the exterior of the vehicle, which enable 110- to 230-volt devices to be powered from the car’s high-capacity lithium-ion battery.

In 2019, Sapporo agreed with Nissan Motor to supply electricity from EVs at evacuation centers and other facilities in case of a disaster. Nissan LEAF – the world’s first mass-produced EV – can be lent to evacuation centers for use as emergency power in the event of a major outage.

Sapporo also agreed with other car manufacturers to enable households using vehicle-to-home technology to use power from EVs even during blackouts.

During a power outage, the car can power:

Electric jackhammer – 24 hours – 36 kWh

Pressure ventilation fan – 24 hours – 21.6 kWh

10-liter soup kettle – 24 hours – 9.6 kWh

Intensive care medical ventilator – 24 hours – 3 kWh

100-watt LED floodlight – 24 hours – 2.4 kWh

Cogeneration among the options

In Tokyo, the metropolitan government has decided to diversify power supplies through a wider outreach to include independent and decentralized energy sources, such as high-efficiency cogeneration systems.

The Tokyo Metropolitan Government (TMG) is also installing solar power systems for medical institutions and emergency evacuations facilities in Tokyo. This effort was included in the revised 2023 plan for disaster response in Tokyo in 2023.

Tokyo’s efforts to expand renewable energy usage is influencing its wider activities. For example, the TMG is providing a range of subsidies for welfare organizations to build or refurbish their facilities and equipment to accommodate renewable energy sources for help in times of disasters. The authorities are offering up to ¥4 million for introducing portable storage batteries and up to ¥13 million for vehicle-to-home appliances that are used in connection with EVs.

Despite efforts to expand the use of renewables, the amount of electricity generated from green sources in Tokyo in FY2022 was estimated at about 166 TWh, while the amount consumed was estimated at 758 TWh; meaning that renewables provided roughly 22% of the capital’s power.

To expand this further, municipalities will need to be more creative not only in supplying the funds but also in infrastructure planning. Backup fossil fuel generation systems have been in place for decades and have evolved to have clear standards, processes, storage and transport infrastructure for moving fuel. Now the same will need to be put into place to accommodate EVs, grid batteries, and other clean energy sources.

For the moment, too much of the momentum for shifting emergency power sources from oil-based diesel generators is in the hands of the national and prefectural governments. Both set policy and distribute budgets but they’re usually not in charge of installing energy facilities.

And yet, giving more emphasis to the decarbonization of emergency power sources in the next iteration of the Basic Energy Plan should be able to motivate more municipalities to be active in this space.

ASIA ENERGY REVIEW

BY JOHN VAROLI

This weekly column focuses on energy events in Asia and the Pacific

Australia / Solar power

Environmental approval was granted for a $19 billion solar power project to export electricity to Singapore. The Australia-Asia Power Link is planned to generate 6 GW of renewable energy, one-third of which would be sent to Singapore via an undersea cable.

Australia / Wind power

Collgar Renewables, which operates the largest wind farm in Western Australia, said it plans to boost its portfolio by building five new wind projects across the state, with a total capacity of 1.7 GW.

China / Coal power

China, the world’s largest builder of coal-fired power stations, cut the number of permits for new plants by nearly 80% in the first half of 2024, said Greenpeace East Asia.

China / Nuclear power

Nuclear power accounts for under 2% of China’s total installed energy capacity but has increased at 5% per year since 2018 compared with a total national capacity growth of 9% per year. China plans a major nuclear reactor expansion that should boost capacity and generation significantly in the next decade.

India / Natural gas

India is unlikely to meet its goal of increasing the share of natural gas in the national energy mix to 15% by 2030, said Spencer Dale, BP’s chief economist, adding that the country will reach only about 8%.

India / Nuclear power

Nuclear Power Corp of India said that Unit 4 of the Kakrapar NPP achieved full operation at 700 MW, becoming the country’s second domestically built nuclear reactor to reach full capacity.

Indonesia / Energy minister

Outgoing president Joko Widodo reshuffled the cabinet and replaced the country’s energy minister, just weeks before leaving office. Bahlil Lahadalia will replace Arifin Tasrif as the Minister of Energy and Mineral Resources.

Marine bunkering

Global maritime trade is set to grow 40% by mid-century, while total global marine fuel sales are expected to grow 2% between now and 2030. Marine bunkering in Asia Pacific is set to grow 3 percentage points between now and 2030, increasing its global market share to 51%. However, that market’s volume might begin shrinking in the early 2030s due to increased fuel efficiency.

Offshore wind power

Global offshore wind installations grew 7% in 2023 and is expected to expand, surpassing 520 GW by 2040, (excluding China), according to Rystad Energy. Europe will drive most growth since it will heavily depend on floating wind to meet national targets. The continent is expected to account for more than 70% of global floating wind installations by 2040.

Southeast Asia / solar power

Southeast Asia’s solar industry boom could be threatened by looming U.S. tariff hikes of up to 50% as the U.S. and EU attempt to check China. Four countries are targeted: Malaysia, Thailand, Vietnam and Cambodia. They account for over 40% of solar module production outside China, though many Chinese firms are setting up shop in the region.

2024 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

January

First market trading day (Jan 4)

IEA “Renewables 2023: Analysis and Market Forecast to 2028” released (Jan 11)

Renewable Energy Exhibition (Jan 31 – Feb 2)

Taiwan presidential election (Jan 13)

Japan’s Diet convenes

IEA “Electricity 2024 / Analysis and Forecast to 2026” released (Jan 24)

February

CFAA International Symposium (Feb 2)

India Energy Week 2024 (Feb 6-9)

Lunar New Year (Feb 10-17)

Indonesia presidential election (Feb 14)

Japan-Ukraine Conference for Promotion of Economic Reconstruction (Feb 19)

FIT/FIP solar auction (Feb 19 – March 1)

Smart Energy Week (Feb 28-Mar 1)

March

Announcement of auction result for Offshore Wind Round 2 (for Akita Happo-Noshiro Project)

Onshore wind auctions (March 4-15; results on March 22)

International LNG Congress (LNGCON) 2024, Milan, Italy (March 11-12)

Russian president election (March 15-17)

World Petrochemical Conference, Houston, TX, USA (March 18-22)

IAEA Nuclear Energy Summit @ Belgium (March 21)

Ukraine presidential election (due before March 31)

Happo Noshiro, Murakami-Tainai, Oga-Katagami-Akita and Saikai-Eshima wind project auctions close (June 30)

July

Tokyo governor election (July 7)

7th Basic (Strategic) Energy Plan draft published (expected)

August

7th Basic (Strategic) Energy Plan draft presented to Cabinet (expected)

September

Global Offshore Wind Summit Japan 2024, Sapporo, Hokkaido (Sept 3-4)

The United Nations Summit of the Future (Sept 22-23)

Gastech 2024, Houston, TX (Sept 17-20)

IAEA General Conference

GX Week in Tokyo (expected late Sept to October)

Asia Green Growth Partnership Ministerial Meeting

Asia CCUS Network Forum

International Conference on Carbon Recycling

International Conference on Fuel Ammonia

GGX x TCFD Summit

October

IEA World Energy Outlook 2024 Release

BP Energy Outlook 2024 Release

Innovation for Cool Earth Forum (expected)

Connecting Green Hydrogen Japan 2024 (Oct 16-17)

Japan Wind Energy 2024 Summit (Oct 16-17)

Solar Energy Future Japan 2024 (Oct 16-17)

Japan Mobility Show (Oct 25-Nov 5)

November

US presidential election (Nov 5)

COP 29 in Azerbaijan (Nov 11-22)

Abu Dhabi International Petroleum Exhibition Conference (ADIPEC) 2024, Abu Dhabi, UAE (Nov 11-14)

APEC 2024 @ Lima, Peru

International Conference on Nuclear Decommissioning (TBD)

G20 Rio de Janeiro Summit (Nov 18-19)

Offshore Energy Exhibition & Conference (OEEC) 2024, Amsterdam, the Netherlands (Nov 26-27)

Biomass & BioEnergy Asia Conference (TBD)

European Biomethane Week 2024

December

Last market trading day (December 30)

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.