JAPAN NRG WEEKLY

DECEMBER 2, 2024

JAPAN NRG WEEKLY

DECEMBER 2, 2024

NEWS

TOP

- JERA launches first commercial sales of power generated with hydrogen fuel, to supply iconic Toho Studios

- KEPCO and RWE plan to build massive 1.68 GW offshore wind farm, with up to 120 turbines

- JX starts production at gas field in Papua New Guinea, project led by Exxon and Santos

- FEPC head calls for more nuclear power in next Basic Energy Plan

- Govt approves economic measures, resumes electricity subsidies

- Osaka Gas to build supply chain for e-methane

- JERA and Tokyo Metro sign virtual solar PPA

- Firms cooperate on solar panel reuse and recycling

- Itochu and Saudi firm to cooperate on water and renewables

- Japan rail firm to test hydrogen-powered vehicles

- New insurance product to cover hydrogen, CCS technologies

- Hokkaido Electric plans a 1.14 GW offshore wind farm

- OCCTO seeks to improve renewable energy forecasting; and revise calculations for penalties in capacity market

- Toho Gas joins capacity market using VPP services

- Osaka retailer secures 17-year loans for merchant BESS

- Power spot market offers down amid declining supply

- JERA announces measures for winter electricity supply

- Yanmar and SMFL create Japan’s largest virtual PPA

- Chiyoda revises contract for Golden Pass LNG in Texas

- Tokyo Gas seeks to optimize real estate portfolio

- LNG stocks dropped from previous week, down YoY

ANALYSIS

CAN JAPAN AVOID A POWER SHORTAGE THIS WINTER?

For winter 2024, the official outlook sees capacity reserve margins exceeding 3% across all regions, signaling stable supply. METI won’t call for energy conservation, but structural challenges underscore lingering vulnerabilities. In addition to volatility in LNG price and supply, sudden cold snaps and natural disasters have affected the power system almost every year this decade. To address these issues, METI is expanding LNG fuel purchasing support and directing power companies to enforce safety protocols and secure additional capacity.

OFFSHORE WIND AUCTIONS BET ON INCREMENTAL IMPROVEMENTS FOR BOOST

As Japan braces for the results of Round 3 offshore wind tenders, industry insiders are growing restless. Small tweaks to the auction process over recent years have sought to address pricing and timeline issues, but many fear these adjustments fall short of the urgency needed to meet the country’s ambitious 2030 sector target. Preparations for Round 4 are adding to the doubts. The timeline for selecting operators has not yet been announced. Uncertainties and supply chain frustrations are giving some developers pause about Japan’s potential.

ASIA PACIFIC REVIEW

This column gives a brief overview of last week’s top energy stories from across the region

EVENTS SCHEDULE

A selection of events to keep an eye on in 2024.

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group

Events

Editorial Team

Yuriy Humber (Editor-in-Chief)

John Varoli (Senior Editor, Americas)

Kyoko Fukuda (Japan)

Magdalena Osumi (Japan

Filippo Pedretti (Japan)

Tim Young (Japan)

Tetsuji Tomita (Japan)

Regular Contributors

Chisaki Watanabe (Japan)

Takehiro Masutomo (Japan)

Mayumi Watanabe (Japan)

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

OFTEN-USED ACRONYMS

|

METI |

The Ministry of Economy, Trade and Industry |

mmbtu |

Million British Thermal Units | |

|

MoE |

Ministry of Environment |

mb/d |

Million barrels per day | |

|

ANRE |

Agency for Natural Resources and Energy |

mtoe |

Million Tons of Oil Equivalent | |

|

NEDO |

New Energy and Industrial Technology Development Organization |

kWh |

Kilowatt hours (electricity generation volume) | |

|

TEPCO |

Tokyo Electric Power Company |

FIT |

Feed-in Tariff | |

|

KEPCO |

Kansai Electric Power Company |

FIP |

Feed-in Premium | |

|

EPCO |

Electric Power Company |

SAF |

Sustainable Aviation Fuel | |

|

JCC |

Japan Crude Cocktail |

NPP |

Nuclear power plant | |

|

JKM |

Japan Korea Market, the Platt’s LNG benchmark |

JOGMEC |

Japan Organization for Metals and Energy Security | |

|

CCUS |

Carbon Capture, Utilization and Storage | |||

|

OCCTO |

Organization for Cross-regional Coordination of Transmission Operators | |||

|

NRA |

Nuclear Regulation Authority | |||

|

GX |

Green Transformation |

NEWS: ENERGY TRANSITION & POLICY

JERA launches commercial sales of power generated with hydrogen fuel

(Company statement, Nov 29)

- Toho Co and JERA launched Japan’s first commercial supply of electricity from a hydrogen-fired power plant, providing energy to Toho Studios in Tokyo.

- The hydrogen-fired unit at the Sodegaura Thermal Power Plant includes a 320 kW gas engine and two 35 kW fuel cells, which are expected to deliver about 1 GWh a year. Hydrogen is delivered via tanker trucks with a total capacity of 12,000 Nm³.

- Toho Studio also purchases electricity from JERA’s solar farms and has set an initial target of sourcing 60-70% of its energy from low carbon sources. The film company wants to rely on electricity from renewables and hydrogen entirely by 2030.

- CONTEXT: Toho Studios is one of Japan’s most renowned and historic film and TV production companies. Established in 1932, it’s been a cornerstone of Japan’s film industry, famous for producing numerous iconic films and franchises such as the Godzilla series.

- SIDE DEVELOPMENT:

MHI milestone: operating ultra-high pressure liquid hydrogen booster pump

(Company statement, Nov 28)- MHI completed 1,200 hours of operation in durability tests for its 90 MPa-class ultra-high pressure liquid hydrogen booster pump, demonstrating reliability in handling large flow rates (160 kg/ hour) at extreme conditions (-253°C).

- The pump will be delivered to a large-scale hydrogen station in Japan by April 2025, marking its first commercial application. It consumes just 25% of the energy needed for gaseous hydrogen boosting, resulting in lower environmental impact.

- Tests confirmed virtually no hydrogen loss owing to boil-off gas.

TAKEAWAY: These are very early days for hydrogen-fired power generation, and there are many unknowns, including how much Toho studios is spending on this system. It’s likely that the publicity is worth more to JERA than margins, at least for now. The bigger test will come when power users try to pass on their improved sustainability as a cost to customers. The transport sector will be one to watch in this regard. However, another point of interest here is the combination of solar with hydrogen, which theoretically covers peak and base load, as well as seasonal variations. Should it prove commercially viable, this will be a large market opportunity.

Source: TM & © TOHO CO., LTD. via JERA

FEPC head calls for more nuclear power in next Basic Energy Plan

(Company statement, Nov 29)

- Hayashi Kingo, chairman of the Federation of Electric Power Companies of Japan (and president of Chubu Electric), urged the govt to promote and support nuclear energy as a “power source to be used as much as possible” in its next Basic Energy Plan.

- He suggested removing the phrase “reduce dependence on nuclear power as much as possible.” Hayashi also wants the promotion of new construction and the replacement of aging nuclear plants with modern ones.

- Hayashi says opinions on energy demand and nuclear energy have shifted since 2021 due to increased importance of decarbonization and economic security.

- CONTEXT: The govt plans to complete the next energy plan in FY2024, setting the power supply composition for 2040. Discussions about reducing nuclear dependence remain contentious.

TAKEAWAY: The opinions of the big power utility lobby and the big business lobby (Keidanren) have changed little in recent years. They are steadfast supporters of a continued reliance on nuclear energy. The question is how much influence they have on the new government. This has become much more difficult to answer with the changed political landscape. So far, indications are that there are more pro-nuclear lawmakers in parliament than anti. The ultimate litmus test, however, will be what happens to the Kashiwazaki Kariwa NPP.

Govt approves economic measures, resumes subsidies for electricity and gas bills

(Denki Shimbun, Nov 25)

- The govt approved a comprehensive economic package on Nov 22, including the resumption of subsidies for electricity and city gas bills from January to March 2025.

- Subsidies will focus on peak winter months, reducing low-voltage electricity rates by ¥2.5/ kWh in January and February, and ¥1.3 in March. Standard households are expected to save ¥1,000 monthly on electricity and ¥300 on gas during peak months.

- The plan emphasizes energy resilience, promoting energy efficiency and maximizing the use of renewables and nuclear power for decarbonization.

- Public investment exceeding ¥10 trillion is planned by 2030 for AI and semiconductor sectors, along with infrastructure upgrades to support data centers and increased power demand in regional areas.

Osaka Gas to build supply chain for e-methane

(Nikkei, Nov 30)

- Osaka Gas plans to set up a supply network for e-methane, investing about ¥100 billion in the U.S. to build production facilities and secure hydrogen, the primary raw material, at lower costs compared to domestic sources.

- Leveraging existing infrastructure, Osaka Gas plans to import e-methane and meet over 60% of its domestic introduction target for 2030.

- CONTEXT: E-methane is a next-gen urban gas pivotal to decarbonization; it is synthesized by combining hydrogen and CO2. By utilizing CO2 recovered from industrial sources, the process can offset the CO2 emissions generated when e-methane is burned as city gas, effectively achieving carbon neutrality.

TAKEAWAY: Japan’s gas utilities have pushed e-methane as a decarbonization solution very strongly in the last year or so. One of the attractions for the companies is the ability to blend it into existing gas networks, retaining infrastructure that has taken decades to build up. The current Basic Energy Plan calls for e-methane to account for 1% of city gas by 2030, which is what Osaka Gas investment seems to address. The bigger question is what happens after the end of this decade. Is there an economic and technical pathway for e-methane to play more than a minor role?

JERA and Tokyo Metro ink virtual solar PPA

(Company statement, Nov 26)

- JERA signed a 25-year virtual power purchase agreement with Tokyo Metro, providing environmental value from solar power to reduce Tokyo Metro’s CO2 emissions by approximately 936 tons annually starting in December.

- Through its subsidiary JERA Cross, JERA will supply 2.4 GWh annually of non-fossil fuel certificates, enabling Tokyo Metro to count this energy as renewable without altering its existing electricity contracts.

- Tokyo Metro will be the first in the Japanese railway industry to utilize the renewable energy data management solution provided by Granular Energy (a French startup).

Firms cooperate on solar panel reuse and recycling in Fukuoka Pref

(Nikkei, Nov 25)

- Kitakyushu City (Fukuoka Pref) agreed with Hamada, a recycling company, and Shinryo, a subsidiary of Mitsubishi Chemical Group, to cooperate on solar panel recycling and reuse.

- Hamada collects discarded but operational solar panels. Shinryo takes panels that can’t be reused and extracts the glass, copper, silver, etc.

- Although solar panel reuse has not developed due to quality concerns, Kitakyushu City seeks to pioneer the reuse of solar panels and to create a model for solving the problem of large-scale panel disposal.

- CONTEXT: Solar panel lifespan is estimated to be 20 to 30 years, but in practice, panels are often replaced with more powerful ones every 10 years due to innovations. The number of panels to be discarded is expected to increase fivefold by the 2040s.

- SIDE DEVELOPMENT:

Osaka Gas invests in Australian startup to develop solar thermal systems

(Company statement, Nov 26)- Osaka Gas has invested in Australian startup FPR Energy, a developer of concentrated solar thermal systems that uses ceramic particles as a heat medium.

- FPR’s system uses stable ceramic particles to achieve high-temperature heat transfer (up to 1,200°C) and efficient heat exchange.

- Osaka Gas will combine this tech with its expertise in gas cogeneration and boilers to enhance energy stability.

Itochu signs MoU with Saudi firm to develop water and renewables projects

(New Energy Business News, Nov 26)

- Itochu inked an MoU with Saudi Arabia’s ACWA Power, the Middle East’s largest independent power producer and world’s largest desalination company.

- The agreement focuses on strategic collaboration in water, environmental, and renewable energy projects, particularly in the Middle East, Central Asia, and Africa. The MoU was signed during COP29 in Baku.

- CONTEXT: Based in Riyadh, ACWA Power’s portfolio of about 90 projects in operation and development has an investment value of $86 billion, and a capacity of 55 GW of power and 8 million m3/ day of desalinated water.

JR to test hydrogen-powered vehicles

(Company statement, Nov 26)

- Central Japan Railway Company is developing hydrogen-powered vehicles to replace diesel-powered railcars.

- Based on the HC85 series hybrid system, these vehicles will be able to utilize both fuel cells and hydrogen engines as power sources.

- CONTEXT: Fuel cells are efficient, produce no emissions during use, and they power electric motors through an electrochemical process; typically used for cars and buses. In contrast, hydrogen engines are similar to internal combustion engines; they offer higher energy density and are thus used for heavy-duty vehicles and heavy loads.

- SIDE DEVELOPMENT:

Tokio Marine offers risk assessment in hydrogen and ammonia supply networks

(Nikkei, Nov 29)- Starting December, Tokio Marine & Nichido Fire Insurance will offer a service to analyze risks in hydrogen and ammonia supply networks, including fires, leaks, and explosions, helping businesses stabilize operations and plan safety measures.

- The service will simulate accidents during procurement, transportation, and usage, estimate damage costs, and assist in prevention strategies and evacuation plans.

- The service will focus on ammonia and later expand to hydrogen and CO2 management technologies like CCS and CCU.

NYK Line seeks to develop world’s biggest ship recycling capacity

(Nikkei Asia, Nov 26)

- Nippon Yusen (NYK Line) plans to dismantle ships and large marine structures, and recycle high-purity iron in Aichi Pref starting 2028.

- This initiative aims to establish the world’s largest ship recycling capacity. It could handle 300,000 tons of scrap iron per year.

- The recycled iron will help Japan shift toward electric furnaces in the steel industry.

- CONTEXT: This manual-intensive industry is currently dominated by Bangladesh and India.

NEWS: ELECTRICITY MARKETS

KEPCO and RWE plan to build 1.68 GW offshore wind farm off Hokkaido coast

(Company statement, Nov 25)

- Kansai Electric and RWE Renewables Japan plan to build an offshore wind farm with a capacity of 1.68 GW off Hiyama, Hokkaido. On Nov 25, they released an Environmental Impact Assessment for the project.

- Up to 120 wind turbines, each 14 to 24 MW capacity, will be installed. Foundation types under consideration include monopile, jacket, and gravity-based structures.

- CONTEXT: Hiyama offshore has been designated as a “promising area” by METI. Several other companies plan developments in the same regions such as Cosmo Eco Power and Hokkaido Electric, which announced its plan earlier this week. The govt will upgrade the site to a “promotion zone”, and feed-in-premium (FIP) subsidies will be awarded to projects through a public tender run by METI/MLIT.

- SIDE DEVELOPMENT:

Hokkaido Electric plans a 1.14 GW offshore wind farm

(Company statement, Nov 26)- Hokkaido Electric submitted to METI, and local state agencies, an Environmental Impact Assessment for a wind project off the coast of Hiyama, Hokkaido.

- The offshore wind project spans over 20,000 hectares off the coasts of Setana, Yakumo, Esashi, and Kaminokuni towns. It aims for a maximum capacity of 1.14 GW, with up to 76 wind turbines, each 15–20 MW capacity.

- The firm has not chosen a foundation structure.

TAKEAWAY: Offshore wind developers are pushing METI to start opening up the Hokkaido areas to auctions. The ministry’s reticence so far has been a lack of clarity on when an underwater sea cable would be built to bring this power from Hokkaido seas to the industrial areas of Kanto. However, the development of a semiconductor manufacturing cluster in Hokkaido is proving that there are willing electricity buyers closer to home, which may give officials confidence that some Hokkaido offshore projects can proceed sooner rather than later.

OCCTO will revise method to calculate penalties in capacity market

(OCCTO statement, Nov 25)

- Within the next 12 months, OCCTO will revise a section of the Supply Capacity Provision Notice and the method for calculating penalties.

- This notice covers the period from 18:00 on the previous day until the gates close if the reserve margin for the area falls below 8%.

- OCCTO wants to keep in mind that reserve margins can still be improved if the use of surplus pumped storage capacity is brought forward. In other words, pumped hydro plants are used earlier than initially forecast.

- Operators of stable power sources will be subject to a penalty if they do not participate in market bidding during periods of low reserve margin.

- The current calculation method assumes that a low reserve margin time is 30 hours, based on past performance.

TAKEAWAY: Starting FY2024, pumped storage has been operated by the balancing group (BG) of power generation companies. TSOs can utilize pumped storage within a range of surplus capacity as notified by the BG. If the range of available capacity notified by the BG is small, the reserve margin decreases. Once the reserve margin falls below 5%, operations of pumped storage will switch to TSOs. For this winter, however, there is a provisional measure: the threshold for the switch in operations has been raised to 8%. It is possible that it’ll remain at 8% from now on.

- SIDE DEVELOPMENT:

OCCTO improves renewable energy forecasting

(Denki Shimbun, Nov 27)- OCCTO reported progress on enhancing renewable energy forecasting, which could help reduce the need for tertiary balancing power. The initiative uses a new method called “confidence-level classification forecasting.”

- This method, adopted nationwide in 2023, separates solar forecasting errors into “high” and “low” confidence categories, and adjusts the required balancing power.

- Under a NEDO-backed program (2021–2024), the goal is to cut maximum forecasting errors by over 20%, leveraging specialized weather models.

- These improvements reduced the annual tertiary power requirements by 28% in FY2023, with Kansai Electric leading trials to expand this forecasting technique.

TAKEAWAY: OCCTO has struggled to raise usage of the EPRX balancing market. This effort is about boosting the volume of renewable energy utilized as a balancing reserve, which would give TSOs more flexibility. However, improving the confidence of TSOs is key. The involvement of Kansai Electric should be taken as a good signal for potential adoption in other parts of the country.

Toho Gas to join capacity market using VPP services

(Nikkei, Nov 29)

- Toho Gas is entering the capacity market where it will utilize its virtual power plant (VPP) service, “Waketoku,” that aggregates and controls home storage batteries as a unified power source.

- This marks Japan’s first power purchase service using household batteries as part of a VPP. The secured capacity will be sold to OCCTO and become available four years from now.

- The company’s VPP service, launched in October, aggregates and controls household batteries to function as a single power source. The initiative is run in partnership with electrical equipment manufacturer, Omron Group.

- Targeting households in Aichi, Gifu, and Mie, “Waketoku” remotely controls storage batteries to discharge during tight supply-demand situations, offering a purchase price ¥3 higher per kWh than the standard rate. It is especially used during power shortages.

Osaka retailer to enter BESS sector, secures bank financing for merchant units

(Company statement, Nov 27)

- Osaka based retailer, Energy Power, plans to enter the battery energy storage system (BESS) market by acquiring and commissioning two projects before Sept 2026.

- The projects, located in Asago and Tamba cities in Hyogo Prefecture, will both have 1.979 MW capacity and 8.226 MWh storage, with construction scheduled from February to June 2025.

- The Asago plant (¥809 million acquisition cost) will be built by East Engineering, while the Tamba plant (¥800 million) will be constructed by BS POWER, on 1,151 m² and 1,787 m² sites respectively.

- Energy Power said it secured two 17-year loans totaling ¥748M: a ¥600 million facility from Kiyo Bank and a ¥148 million facility from Japan Finance Corp.

- The two BESS projects will trade power in the wholesale, balancing, and capacity markets to capture demand for grid-stabilizing solutions.

TAKEAWAY: The most impressive part of this news is probably the financing details. These show that the retailer was able to secure long-term bank loans for close to half of the investment amount for BESS that, according to the statement, will be operating a full-merchant model. In other words, it will trade the electricity in the market and not rely on a long-term contract with an anchor buyer or a state subsidy. Banks have so far been hesitant to expose themselves to market risk in the power sector. After a decade of financing solar and wind projects on an FIT basis with predictable cash flows, it will take a while for lenders to adjust to the new risk levels. However, this deal indicates that there is some move in this direction. If this were to happen more widely, more BESS developers may consider options outside of the LTDA and similar subsidy schemes to aim for higher margins.

- SIDE DEVELOPMENT:

Toshiba wins Orix contract to build 134 MW BESS project

(Company statement, Nov 25)- Toshiba Plant Systems & Services won an engineering, procurement, construction, and commissioning (EPCC) contract from an Orix-related SPC for a 134 MW/ 548 MWh grid-connected BESS project in Maihara City, Shiga Pref.

- CONTEXT: This will be one of the largest BESS facilities in Japan once complete. It was the biggest BESS to be awarded a subsidy in Round 1 of the LTDA tenders, the results of which were announced at the start of this year.

- The project is located in the Kansai TSO area and has a 26,000 m2 land plot leased from Maibara City. It involves installing 140 lithium-ion battery containers and is due to be completed in November 2026.

Power spot market offers are down amid declining supply and sustained demand

(Denki Shimbun, Nov 26)

- In October, JEPX reported a 13.6% MoM drop in average daily sell offers, totaling 999.75 GWh; and a 10.7% decrease in buy offers, totaling 893.05 GWh. Despite lower volumes, unseasonably high temperatures led to stronger buying activity early and mid-month as thermal power output declined.

- Compared to October 2023, sell offers rose 0.5%, while buy offers surged 18.4%, reflecting robust demand. The pause on gross bidding, in effect since October 2023, influenced these dynamics.

- Total monthly sale volume fell 10.8% over September to a total of 30.99 TWh, while the buy volume declined 7.7% to 27.68 TWh.

- Peak-hour sell offers dropped 12.9%, with nighttime offers declining the most at 18%.

- Supply tightness eased later in the month as sell offers increased, but earlier mismatches between supply and demand created noticeable gaps in market activity.

- SIDE DEVELOPMENT:

New power companies ranking for May, Tokyo Gas tops the list

(Denki Shimbun, Nov 29)- METI and ANRE reported that the number of new power companies (shin denryoku) was 676, down 15 from the previous month. Of these, 482 have registered sales, down 13 from the previous month.

- Tokyo Gas topped the list for the 14th consecutive month, but its sales dropped significantly. Marubeni New Power Co overtook Osaka Gas to enter the top three.

- The total sales volume of new power companies was 10.37 TWh, down 6.4% from the previous year. Low voltage was down 16.9%; high voltage was up 3.0%; and extra high voltage was up 5.5%.

- Among the top high-voltage companies, Kyuden Mirai Energy (8th place) and CD Energy Direct (9th place) switched places.

- The top ten companies in the extra-high-voltage category remained unchanged.

JERA announces measures for winter electricity supply

(Company statement, Nov 27)

- JERA plans measures to ensure electricity supply during the heavy-load winter, such as scheduled maintenance for thermal power stations in warmer months.

- JERA already enhanced supply with nine new operational units providing 6.53 GW of capacity; also planning to launch the Goi Thermal Power Station Unit 3 in March 2025, and to resume operations at the Taketoyo Thermal Power Station.

- As far as LNG, JERA expects supply constraints to ease due to warm weather and high natural gas stocks in Europe. There are risks from sudden cold snaps, production issues, or international geopolitical changes.

- CONTEXT: Under the Strategic Buffer LNG, JERA will secure one cargo of surplus LNG per month from Dec 2024 to Feb 2025.

TAKEAWAY: The Strategic Bugger was set up in December 2023 by METI, with JERA handling three cargoes in the winter season. The govt already expressed plans to secure not only one cargo per month during the winter season, but also for each month of the year. How much this improves Japanese LNG buyers’ conference is yet to be seen, especially in the offpeak power demand seasons, but it does show the government’s willingness to support marginal LNG purchases.

Mayor visits TEPCO and Tohoku Electric regarding NPP restarts

(Nikkei, Nov 25)

- Hatanaka Toshiaki, mayor of Higashidori (Aomori Pref ), visited Tohoku Electric and TEPCO, requesting the early restart of Tohoku Electric’s Higashidori NPP Unit 1 (BWR, 1.1 GW), as well as resuming construction on TEPCO’s Higashidori NPP Unit 1 (ABWR, 1.39 GW).

- CONTEXT: Higashidori NPP is unique in that it comprises two adjoining sites, one run by Tohoku Electric and the other by TEPCO. Both have Toshiba reactors.

- Mayor Hatanaka said closure of the NPPs negatively impacted the local economy.

- Tohoku Electric president Higuchi Kojiro said Onagawa Unit 2’s restart will benefit the local community. TEPCO president Kobayakawa Tomoaki said work at Higashidori NPP Unit 1 must be accelerated.

- CONTEXT: The restart of Tohoku Electric’s Higashidori Unit 1 has been under NRA review since June 2014. Safety construction deadlines have been postponed six times. The revised completion target is now set for Sept 2025. TEPCO’s Higashidori Unit 1 still doesn’t have a clear timeline for resumption. Construction began in 2011 but was stopped due to the 2011 Fukushima accident.

- SIDE DEVELOPMENT:

Tōhoku Electric to begin commercial operation at Onagawa NPP

(Nikkei, Nov 28)- Tohoku Electric plans commercial operation at Onagawa NPP Unit 2 about Dec 26, waiting for formal approval following inspections by the NRA.

- CONTEXT: When Onagawa NPP Unit 2 resumed on Oct 29, it was the first nuclear reactor in east Japan to restart since the 2011 earthquake. The reactor is now in a planned shutdown for safety inspections before commercial operation.

TEPCO submits revised pre-use inspection application for NPP

(Company statement, Nov 28)

- TEPCO submitted to the NRA a revised pre-use inspection application for Kashiwazaki-Kariwa NPP Unit 6.

- Safety upgrades for Unit 6 are underway. Once the NRA approves, TEPCO plans to load fuel and proceed with post-fuel-loading inspections.

- CONTEXT: Unit 6 has been inactive since March 2012. TEPCO had hoped to restart both Unit 6 and Unit 7, having passed the NRA review in 2017. Approval for construction plans ahead of the restart only came in September.

TAKEAWAY: TEPCO said it plans to load nuclear fuel into Kashiwazaki-Kariwa NPP Unit 6 in June 2025. December 2024 had previously been the target, but the restart date for Unit 6 remains undecided as Niigata Pref has not yet agreed to the resumption, which is also delaying the restart of Unit 7. Discussions between the company and the local govt is ongoing, but a restart does not seem around the corner. The national govt is working with local authorities to address evacuation concerns. There is ongoing public unease about nuclear plant safety in earthquake-prone regions like Niigata.

- SIDE DEVELOPMENT:

MHI wins order to supply MOX fuel assemblies for Ikata NPP

(Company statement, Nov 29)- MHI won an order from Shikoku Electric to supply 24 MOX fuel assemblies for Ikata NPP Unit 3. MHI already supplied 57 MOX fuel assemblies.

- CONTEXT: MHI won a similar order in October from Kyushu Electric for Genkai NPP Unit 3.

- MHI will design the MOX fuel. Components will be produced by Mitsubishi Nuclear Fuel and final assembly will be done by Orano at its MELOX plant in France.

Yanmar and SMFL sign agreement for Japan’s largest virtual PPA with solar

(Company statement, Nov 27)

- SMFL Mirai Partners, Yanmar Holdings, and Yanmar Energy System signed an agreement for Japan’s largest virtual power purchase agreement (PPA) to supply 150 MW of renewable energy.

- The three companies plan to develop 150 MW of renewable energy sources nationwide by 2030.

- A joint special-purpose company (SPC) was established to deliver renewable energy to Yanmar Holdings, with Phase 1 including nine solar power plants (totaling 10.9 MW) supplying environmental value credits starting in December 2024.

- CONTEXT: In 2021, Yanmar sold a 60% stake in Yanmar Credit Service to SMFL.

- SIDE DEVELOPMENT:

All locally-generated renewable electricity is consumed in Iwate Pref

(Nikkei, Nov 26)- All of the renewable electricity generated and sold under the FIT system by the Iwate Enterprise Bureau is consumed within the prefecture.

- This is the first time in the Tohoku area that the entire amount will be consumed within the prefecture.

- A total of 80 GWh will be supplied to the Tohoku Automobile Industry Green Energy Association and Kuji Regional Energy through March 2027.

- The prefecture hopes that Iwate will become a suitable place for industrial and economic activities in terms of decarbonization.

- CONTEXT: The Iwate Public Enterprise Bureau is working to build power plants that use renewable energy sources such as hydropower, wind power, and solar power, and currently operates 20 power plants (total capacity, 176 MW), making it one of Japan’s largest public power companies.

OCCTO awards 56 MW in latest solar power auction

(Government statement, Nov 26)

- Japan awarded 56.44 MW of solar power capacity to 23 successful bidders in its 22nd auction, which offered a maximum of 93 MW.

- The highest capacity was awarded to a private firm, miyagi motoyoshi solar, for a price set at ¥7.5.

- The weighted average bid price was ¥8.17/ kWh, with individual bids ranging from ¥7.05/ kWh to ¥9.04/ kWh, under a cap of ¥9.05/ kWh.

- Two entries from the previous auction – RJ Fain and Solar Grazing were also awarded capacity after their projects were cancelled and plans were revised. In the second case, the firm had failed to secure offtakers.

- Winners in the 22nd solar power tender are:

|

Company name |

Price (¥/ kWh) |

Capacity (kW) |

|

miyagi motoyoshi solar |

7.5 |

19,500 |

|

ECO Kamiken |

7.5 |

450 |

|

ECO Kamiken |

7.5 |

550 |

|

SPC under Renova |

7.97 |

299.7 |

|

Yachiyo Engineering |

7.97 |

600 |

|

Yachiyo Engineering |

7.97 |

500 |

|

Yachiyo Engineering |

7.97 |

400 |

|

Yachiyo Engineering |

7.97 |

300 |

|

Yachiyo Engineering |

7.97 |

300 |

|

YTS-Solar |

7.97 |

400 |

|

GPSS Agri-B |

7.99 |

1,995 |

|

Sustainable Solar 4 |

8 |

9,990 |

|

OTS |

8 |

1,500 |

|

OTS |

8 |

375 |

|

Sirius Solar Japan |

8.95 |

1,000 |

|

RJ Fain |

9 |

1,999 |

|

WAKO |

9.03 |

600 |

|

WAKO |

9.03 |

450 |

|

WAKO |

9.03 |

400 |

|

WAKO |

9.03 |

400 |

|

WAKO |

9.03 |

350 |

|

Solar grazing |

9.04 |

13,332 |

|

Toho Gas facility |

9.04 |

750 |

NEWS: OIL, GAS & MINING

JX starts gas production at field in Papua New Guinea

(Company statement, Nov 27)

- JX Nippon Oil & Gas Exploration Corp (JX) started production at the Angore gas field (Papua New Guinea). It is part of the PNG LNG Project.

- The project includes gas production, processing, and liquefaction facilities across many provinces. It is connected by over 700 kilometers of pipeline. The Angore field has production capacity of up to 350 million cubic feet per day.

- JX’s subsidiary, Nippon Papua New Guinea LNG, holds a 4.7% stake. Major partners include ExxonMobil (33.2%), Santos (39.9%), etc.

Chiyoda revises contract for Golden Pass LNG in Texas

(Company statement, Nov 25)

- Chiyoda Corp reevaluated the extra costs needed to complete the Golden Pass LNG project in Texas. It adjusted mid-to-long-term plans, reaching an agreement with the client on cost-sharing.

- The revisions pertain to the first train of Golden Pass LNG. Of the three trains, building the first train is the most complicated.

- CONTEXT: Chiyoda’s decision followed the bankruptcy of its partner, Zachry Industrial, in May, delaying construction. In FY2023, Chiyoda saw a ¥15.8 billion loss, and drew upon a ¥37 billion provision to cover costs due to Zachry’s failure.

Tokyo Gas seeks ways to optimize real estate portfolio

(Bloomberg, Nov 28)

- Tokyo Gas is exploring ways to optimize its extensive real estate portfolio, including potential sales of underutilized assets. This follows pressure from activist investor Elliott Investment Management.

- CONTEXT: Elliott recently disclosed a 5% stake in Tokyo Gas, urging the company to divest properties such as the Shinjuku Park Tower.

- The company plans to exceed its current mid-term return-on-equity goal of 8%. This is part of its broader strategy to enhance shareholder returns.

LNG stocks down 9.7% from previous week, down 4.6% YoY

(Government data, Nov 27)

- As of Nov 24, the LNG stocks of 10 power utilities were 2.06 Mt, down 9.7% from the previous week (2.28 Mt), down 4.6% from end November 2023 (2.16 Mt), and 3.3% down from the 5-year average of 2.13 Mt.

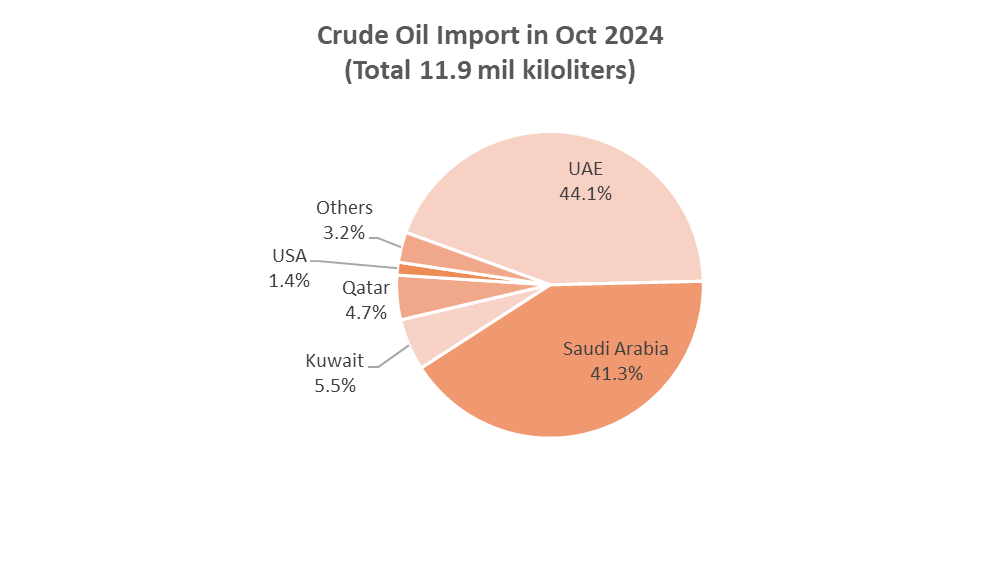

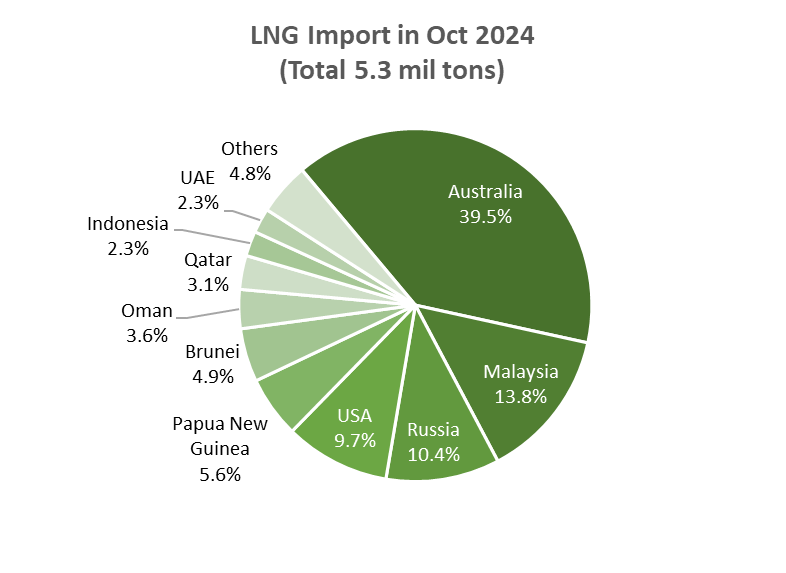

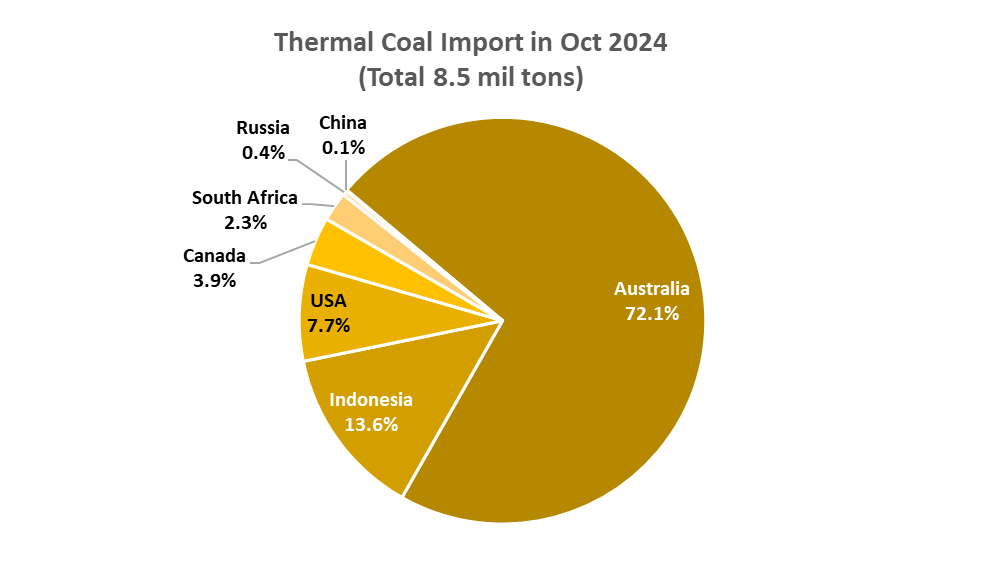

October Oil/ Gas/ Coal trade statistics

(Government data, Nov 29)

|

Imports |

Volume |

YoY |

Value (Yen) |

YoY |

|

Crude oil |

11.9 million kiloliters |

1.5% |

¥871.5 billion |

-14.2% |

|

LNG |

5.3 million tons |

-2.2% |

¥482.6 billion |

-2.9% |

|

Thermal coal |

8.5 million tons |

-0.9% |

¥193.5 billion |

-21% |

- Japan imported 11.9 million kiloliters of crude oil in October, which is 11% more than in September and 1.5% more YoY. Once again, over 95% of the total crude oil imports came from the Middle East. As December approaches, the temperature will drop sharply and an increase in oil imports is needed to prepare for heating devices (kerosene) after processing and refining crude oil.

- LNG imports in October totaled 5.3 Mt, which is down 2.5% over September (5.4 million tons) and 2.2% less YoY. Australia is the biggest exporter of LNG to Japan, and its volume was up 16.2% over September (from 1.8 Mt to 2.1 Mt ). Japan imported LNG from Canada for the first time this year.

- Thermal coal imports in October decreased to 8.5 Mt, down 20.6% from September. About 30% of Japan’s coal-fired thermal power plants are less than 20 years old, and their average life is 40 years. This makes it difficult for Japan to exit entirely from thermal coal sooner than other countries.

ANALYSIS

BY TETSUJI TOMITA

Can Japan Avoid a Power Shortage This Winter?

This past summer, Japan faced soaring electricity demand due to record heat, straining the nation’s power grid. However, disruptions were averted through interregional electricity transfers and increased thermal plant output.

For winter 2024/25, METI expects a calmer situation. The official outlook by OCCTO, which was made last month, sees capacity reserve margins exceeding 3% across all regions, signaling stable supply. Consequently, METI will not call for energy conservation measures.

Still, structural challenges – aging thermal plants and risks of equipment failures – underscore lingering vulnerabilities in Japan’s power system. In addition to volatility in the price and supply of LNG, sudden cold snaps and natural disasters have affected the electricity system almost every year this decade. Only the occasional nuclear reactor restart in the past two years has avoided technical glitches and delays.

To address these issues, METI is expanding LNG fuel purchasing support and directing power companies to enforce strict safety protocols and secure additional capacity. This will build on the measures that worked well last winter, 2023/24, when electricity price and supply volatility remained moderate. The upcoming winter, however, promises a different weather pattern.

Reserve margin forecasts for FY2024 winter

(Unit: %)

|

Area |

At Maximum Demand |

At Minimum Reserve Margin | ||||||

|

Dec |

Jan |

Feb |

Mar |

Dec |

Jan |

Feb |

Mar | |

|

Hokkaido |

26.5 |

11.3 |

13.0 |

12.3 |

23.8 |

11.6 |

13.5 |

13.1 |

|

Tohoku |

26.5 |

11.3 |

13.0 |

23.8 |

23.8 |

11.6 |

13.5 |

22.0 |

|

Tokyo |

26.5 |

11.3 |

13.0 |

23.8 |

23.8 |

11.6 |

13.5 |

22.0 |

|

Chubu |

15.5 |

11.3 |

13.0 |

23.8 |

15.5 |

11.6 |

13.5 |

23.0 |

|

Hokuriku |

15.5 |

11.3 |

13.0 |

23.8 |

15.5 |

11.6 |

13.5 |

23.0 |

|

Kansai |

15.5 |

11.3 |

13.0 |

23.8 |

15.5 |

11.6 |

13.5 |

23.0 |

|

Chugoku |

15.5 |

11.3 |

13.0 |

23.8 |

15.5 |

11.6 |

13.5 |

23.0 |

|

Shikoku |

18.1 |

17.1 |

30.5 |

26.3 |

16.3 |

17.2 |

30.2 |

26.3 |

|

Kyushu |

15.5 |

11.3 |

13.0 |

23.8 |

15.5 |

11.6 |

13.5 |

23.0 |

|

9 Areas |

20.2 |

11.5 |

13.5 |

23.5 |

19.2 |

11.8 |

14.1 |

22.3 |

|

Okinawa |

48.5 |

34.5 |

40.4 |

40.9 |

48.5 |

34.5 |

40.4 |

40.9 |

|

10 Areas |

20.4 |

11.7 |

13.7 |

23.6 |

19.4 |

12.0 |

14.3 |

22.5 |

Source: OCCTO

Ensuring stable supply

OCCTO conducts rigorous evaluations of supply-demand conditions ahead of high-demand periods: summer and winter peaks. Its October 2024 report assessed both the supply-demand situation during summer 2024 and the outlook for winter. The primary metric used is the reserve margin, which indicates the level of surplus capacity relative to peak demand. A reserve margin of at least 3% is considered the minimum for a stable power supply under extreme conditions, such as the coldest weather recorded in the past decade.

For this winter, OCCTO has factored in potential risks, including unplanned outages and fluctuations in renewable energy output. It has set the expected unplanned outage rate at 2.6% across all regions, accounting for potential equipment failures. Supply capacity estimates also exclude nuclear plants preparing for restarts, such as Onagawa NPP Unit 2 (825 MW) in Tohoku and Shimane NPP Unit 2 (820 MW) in Chugoku. Both are anticipated to begin commercial operation by January 2025, which would bolster reserve margins in their respective regions.

Renewable energy sources, particularly solar and wind, have been evaluated using historical performance data. Solar output is calculated as the average on peak demand days over the past decade, while wind and hydroelectric power assessments incorporate adjustments for natural variability. These refinements reflect the growing importance of accurately predicting the performance of renewables, especially during evening hours when solar output diminishes.

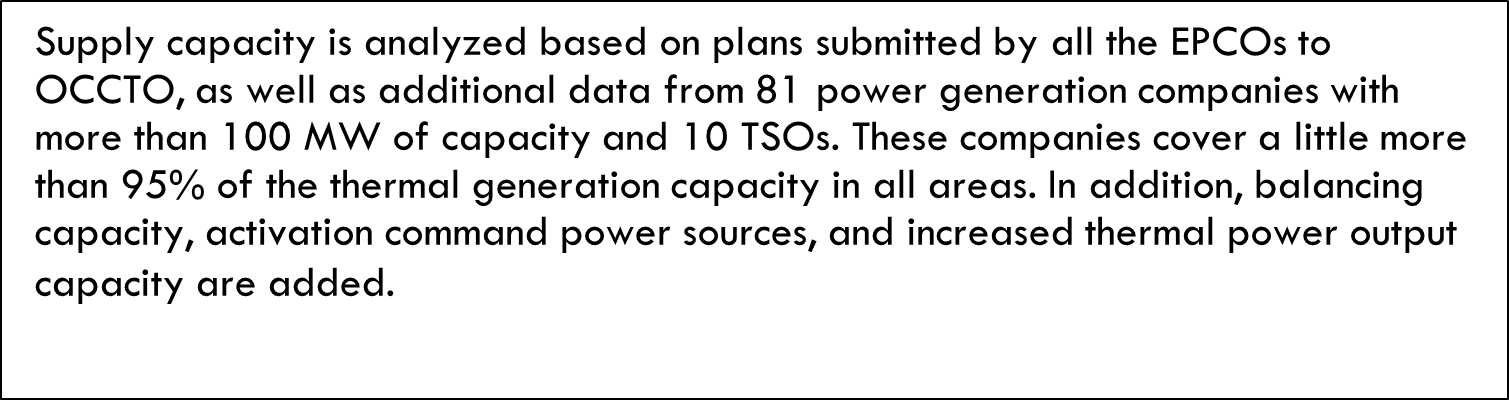

Supply capacity is analyzed based on plans submitted by all the EPCOs to OCCTO, as well as additional data from 81 power generation companies with more than 100 MW of capacity and 10 TSOs. These companies cover a little more than 95% of the thermal generation capacity in all areas. In addition, balancing capacity, activation command power sources, and increased thermal power output capacity are added.

Comparison with past winters

The winter of FY2023 was unseasonably mild, resulting in lower-than-expected electricity demand nationwide. Maximum demand was the lowest in five years, and reserve margins remained robust, peaking at 14% and never falling below 11.4%. Even on the coldest days, all regions maintained reserve margins above 9%, ensuring stable supply.

In contrast, FY2022 experienced harsher winter conditions. Maximum demand in three regions — Hokkaido, Tohoku, and Chubu — exceeded forecasts based on the coldest days in the past decade. Nationwide reserve margins dipped to 10.5%, significantly tighter than the previous year but still sufficient to avoid disruptions. Interregional electricity transfers played a critical role in maintaining stability, particularly during peak demand periods.

Unplanned outages have also varied significantly between years. In FY2023, outage rates averaged 2.8%, rising to 3.1% during January’s cold snap, partly due to disruptions from the Noto Peninsula earthquake. By comparison, FY2022 saw lower outage rates, averaging 1.9% annually and 1.8% during peak demand. These fluctuations underscore the system’s vulnerability to natural disasters and the importance of robust contingency planning.

Reserve margins during winters in FY2022 and FY2023

(Unit: %)

|

Area |

FY2022 |

FY2023 | ||||||

|

Max Nationwide (Jan 25, 2023) |

Max in Each Area |

Max Nationwide (Jan 24, 2024) |

Max in Each Area | |||||

|

Maximum Demand |

Minimum Reserve Margin |

Maximum Demand |

Minimum Reserve Margin |

Maximum Demand |

Minimum Reserve Margin |

Maximum Demand |

Minimum Reserve Margin | |

|

Hokkaido |

9.5 |

12.5 |

9.5 |

12.5 |

16.1 |

14.2 |

10.1 |

9.7 |

|

Tohoku |

6.2 |

5.6 |

6.2 |

5.6 |

42.6 |

20.7 |

21.6 |

9.6 |

|

Tokyo |

10.9 |

10.3 |

8.8 |

8.2 |

12.9 |

12.2 |

10.7 |

10.4 |

|

Chubu |

9.1 |

7.2 |

9.1 |

7.2 |

9.5 |

8.1 |

9.5 |

8.1 |

|

Hokuriku |

6.2 |

11.9 |

7.4 |

11.9 |

10.9 |

12.3 |

14.6 |

15.8 |

|

Kansai |

14.8 |

15.1 |

12.7 |

14.0 |

9.1 |

9.0 |

9.1 |

9.0 |

|

Chugoku |

10.9 |

8.9 |

8.0 |

8.0 |

9.6 |

9.6 |

9.6 |

9.6 |

|

Shikoku |

11.7 |

6.8 |

11.7 |

6.8 |

9.3 |

8.4 |

9.3 |

8.4 |

|

Kyushu |

6.8 |

5.7 |

6.8 |

5.7 |

10.0 |

8.6 |

10.1 |

8.6 |

|

9 Areas |

10.2 |

9.6 |

13.8 |

11.2 | ||||

|

Okinawa |

57.6 |

44.6 |

33.7 |

34.5 |

43.0 |

31.3 |

31.3 |

31.3 |

|

10 Areas |

10.5 |

9.8 |

14.0 |

11.4 | ||||

Source: OCCTO

Risks and uncertainties

Despite the optimistic supply outlook, several risks could disrupt the balance. Extreme weather events, such as cold waves or heavy snowfall, could drive up electricity demand beyond current forecasts. The Japan Meteorological Agency predicts average temperatures nationwide this winter. Colder-than-usual conditions are expected in western Japan due to La Niña that typically strengthens pressure patterns, bringing cold air southward, and increasing the likelihood of heavy snow and lower temperatures in some regions.

Natural disasters remain another significant threat. Earthquakes, typhoons, and other disasters can damage infrastructure and reduce supply capacity. While OCCTO assumes a 2.6% unplanned outage rate in its calculations, recent events like the Noto Peninsula earthquake have shown that actual rates at times can exceed this assumption.

Renewable energy also introduces unique challenges due to the weather-reliant output of solar and wind farms. While advances in forecasting and grid integration are helping to mitigate these variables, the growing share of renewables in Japan’s energy mix requires continued innovation to ensure reliability and much more energy storage than is available in the system today.

Measures to address tight supply-demand

In the event of a tight supply-demand balance, OCCTO has a tiered response system to prevent shortages. If reserve margins fall below 3%, then ANRE will issue a Power Supply-Demand Alert urging businesses and households to conserve electricity. For reserve margins below 1%, rolling blackouts may be implemented, with affected areas receiving at least two hours notice.

New measures introduced in FY2024 include daily updates on reserve margin forecasts, published via the Cross-Regional Reserve Margin Web Publication System. This real-time information aims to improve preparedness on both the supply and demand sides, giving stakeholders more time to respond to potential shortages.

Efforts to strengthen Japan’s power system are also underway through capacity market reforms to enhance grid resilience. However, as covered in the Nov 11, 2024 issue of Japan NRG, these measures are a work in progress, with gaps in implementation limiting their immediate impact.

Lessons from past reforms

Japan’s current electricity system has its roots in reforms initiated after the Great East Japan Earthquake of 2011. That disaster exposed critical vulnerabilities, including overreliance on large power plants and the lack of a unified response framework. As a result, the government launched a three-phase reform process to fully liberalize the electricity market, enhance grid connectivity, and ensure stable supply.

The reforms have made progress and are in their final stages. These include the legal separation of power generation and transmission, the establishment of a capacity market, and the introduction of power balancing mechanisms. But due to the tightness of power supply-demand in recent years and its increased vulnerability to disasters, global fuel markets, and greater forecast uncertainties, the earlier stages are also being reviewed. The main goal today seems to be to introduce much more flexibility into the power system – at all stages.

METI’s and OCCTO’s forecasts for this winter suggest that Japan is well-prepared to meet electricity demand under normal conditions. However, the system’s vulnerabilities to extreme weather, natural disasters, and renewable energy fluctuations mean that risks cannot be entirely eliminated. Continued vigilance, combined with ongoing reforms and technological innovation, will be essential to ensuring a stable and resilient power supply in the years ahead.

Additional supply capacity measures for this winter

|

Activation Threshold Reserve Margin Index |

Measures |

Notes |

|

Less than 8% |

Switch control of pumped storage capacity from generation companies to TSOs |

Threshold has been temporarily changed from 5% to 8% for this winter |

|

Supply surplus power from stable sources by TSO directive |

– | |

|

Start up additional power sources based on a surplus utilization contract with TSOs |

Threshold has been temporarily changed from 5% to 8% for this winter | |

|

Less than 5% |

Activation of power sources by TSO directive |

Threshold was changed from 8% to 5% in Sept 2024 |

|

Conduct increased power operation or peak mode operation of power sources based on a surplus utilization contract with TSOs |

Threshold has been temporarily changed from 8% to 5% for this winter | |

|

Request to increase generation of in-house power |

– | |

|

Supply hydropower to other areas by switching frequency conversion |

– | |

|

If it could be less than 3% |

Inter-regional power transfer by OCCTO directive |

Conducting just before actual supply-demand |

|

Less than 3% |

Transfer power through use of interconnection line margins or expansion of operating capacity |

– |

|

Ensure supply capacity by reducing the voltage of the supplied power |

– | |

|

Use black start power capacity to recover from power outages |

– |

Source: METI, OCCT

ANALYSIS

BY MAGDALENA OSUMI

Offshore Wind Auctions Bet on Incremental Improvements to Boost Sector

As Japan braces for the outcome of Round 3 offshore wind tenders, industry insiders are growing restless. Incremental tweaks to the auction framework over recent years have sought to address pricing and timeline issues, but many worry that these measured adjustments fall short of the urgency needed to meet the country’s ambitious 2030 sector target.

So far, Japan has made only modest progress in offshore wind development, with a total installed capacity of 153.5 MW by the end of 2023. This includes a mix of both fixed-bottom and floating turbines, but just two wind farms account for the bulk of that capacity.

A best-case scenario would see about 5.7 GW of offshore wind projects operating in Japan by the end of FY2030 – based on the capacity awarded in the first three rounds of tenders. But, this is almost half of the original 10 GW national target. More importantly, it risks presenting Japan as a less attractive market for developers at a time when others in Asia are embarking on ambitious offshore wind programs.

Preparations for Round 4 are adding to the doubts. The three sites expected to be involved are currently at a preliminary stage of readiness, and require environmental and foundational assessments before they can be opened to full-scale bidding. The timeline for selecting operators has not yet been announced.

Despite efforts by METI and MLIT to refine regulatory frameworks and streamline the bidding process, the uncertainties and supply chain frustrations are giving some developers pause about Japan’s potential. Will the government be able to bring the industry back on track?

Upcoming auction

The government is now preparing for Round 4 of the offshore wind auctions, focusing on newly designated “preparation areas” that cover the following locations:

- A site off the coast of Akita Prefecture (Oga City, Katagami City, and Akita City),

- Two sites off the coast of Wakayama Prefecture (eastern and western areas).

For Round 4, METI is revising criteria for evaluating offshore wind power project bids to ensure faster development timelines and financial stability. The new standards that come into effect from Round 4 include lead time for operations with a six-year benchmark.

This is how it’s expected to work. Projects are evaluated on a 240-point scale, with 20 points allocated for the lead time to start operations. For instance, a standard development period of six years will earn 18 points. Projects completing in five years and six months will receive the full 20 points. Conversely, delays beyond six years will incur penalties: a deduction of two points for each six-month delay. The six-year benchmark reflects the average timeline proposed during Round 2.

To enhance focus on projects with robust financial and risk management plans, METI will increase points for financial stability from 10 to 14, recognizing that significant investments are required to finalize the projects with long-term forecasts. On average, such investments are estimated at hundreds of billions of yen. The goal is to ensure that projects are resilient against inflation and exchange rate fluctuations.

Another significant modification is the proposed reference price cap based on the national average market price for wind power over the past three years, currently estimated at ¥14/ kWh. Bidding price, set at an average capture price, would enable bidders to secure maximum points. Prices higher than that would, on the other hand, make bidders score lower with the point difference smaller than under the existing rules.

In order to balance cost efficiency, ensure project feasibility while considering public cost implications and encourage fair competition between “zero-premium” and “near-zero premium” bidders, METI also proposes a scoring model for project feasibility (out of 120 points) that uses an average 16-point gap observed in previous auctions. This suggests that bidders at the near-zero premium level require a feasibility score of 104 points or higher to compete effectively.

The zero premium level represents a scenario where no additional financial support (premium) is provided on top of the market price for electricity generated by the offshore wind farm. Meanwhile, the near-zero premium level introduces a slightly higher price point than the zero premium, allowing some flexibility for projects that might face additional costs or challenges but are deemed competitive in the open market.

The government is proposing a linear evaluation method for prices that fall between the zero-premium and near-zero premium levels. For prices that exceed the near-zero premium level, the evaluation may follow the maximum supply price cap set by the guidelines under the act on promotion of renewables (e.g. ¥18/ kWh for monopile-based projects in Round 3 and ¥29/ kWh for jacket-based projects in Round 2).

These changes seek to encourage earlier project completion and improve the financial resilience of offshore wind projects.

Winning bids

In Japan, several offshore wind power projects have been approved in previous tender rounds. For example, in Round 2, four projects were awarded:

- Happo-Noshiro (Akita Prefecture): 356 MW capacity, won by a consortium led by Japan Renewable Energy, Iberdrola Renewables Japan, and Tohoku Electric Power. Operations are expected to begin in 2029.

- Oga-Katagami-Akita (Akita Prefecture): 336 MW capacity, awarded to a group led by JERA, J-Power, and Itochu.

- Murakami-Tainai (Niigata Prefecture): 700 MW capacity, secured by a consortium of Mitsui, RWE, and Osaka Gas, targeting operations by 2028.

- Saikai-Enoshima (Nagasaki Prefecture): 424 MW capacity, awarded to Sumitomo Corp and TEPCO Renewable Power, with operations planned for 2029.

Meanwhile, in Round 3, areas in the Sea of Japan (Aomori Prefecture) and Yuza (Yamagata Prefecture) with capacities of 600 MW and 450 MW, respectively, are still in the process of bidding. Results are expected in December 2024.

These projects continue to face challenges such as gaining community support, particularly from local stakeholders, addressing supply chain limitations, and adhering to tight construction and operational timelines. The interplay of regulatory revisions, stakeholder negotiations, infrastructure constraints, and environmental requirements has collectively slowed the progress of Japan’s offshore wind projects.

Regulatory framework

Although the government has improved auction rules and introduced incentives, one major issue is the lengthy and complex permitting process. Developers must navigate multiple requirements, including obtaining approvals from various ministries and local stakeholders.

These factors, along with technical and logistical challenges in developing floating wind farms, mean that while Japan is making strides, it is likely to face delays in reaching its national renewable energy goals.

Based on the lessons learned from the previous rounds, the government has implemented several regulatory and procedural changes to address industry concerns and to promote a fairer and more efficient bidding process. This is taken positively by developers as it shows a willingness by the government to work with the sector to improve its operation.

The speed of implementation, however, has been admittedly slow. After broad industry concerns about monopolistic tendencies post Round 1, when Mitsubishi Corp made a clean sweep of the three main projects on offer, METI introduced a cap of 1 GW on the total capacity any one consortium can win in a single tender. While this has opened the auctions awards to more companies, it took a year of deliberations to implement.

Additionally, the government has been revising evaluation criteria such as price factor and timeline prioritization. Under the revised rules, all bids below a certain market price threshold will now receive the same score, discouraging unrealistically low pricing tactics. This ensures that projects are economically viable.

Higher scores have also been awarded for faster project delivery timelines, to encourage operators to speed up project execution. The revised rules aim to make the bidding process more attractive and transparent for international developers. Round 2 finally saw two non-Japanese companies share the spoils: Iberdrola and RWE.

Conclusion

The updates to the bidding process and the regulatory framework for Round 4 auctions are the most promising steps toward fostering competition, enhancing financial stability, and ensuring faster project completion.

Industry insiders, however, are pushing the government to go beyond fine-tuning and offer a bigger pie, especially since previous rule changes mean that the annual expansion for a developer is already limited to 1 GW or less.

So far, the government’s response has been to tout the sector’s potential once wind power generation moves further out to sea, into the Exclusive Economic Zone. That will certainly require floating technology, much of which is still either at the R&D or pilot stages.

Still, the message from state officials is that today’s gentle breeze could and should eventually become a transformative gale. If and when it does, those who are toiling today will be invited to enjoy the expanded power generation scale of tomorrow.

ASIA ENERGY REVIEW

BY JOHN VAROLI

This weekly column focuses on energy events in Asia and the Pacific

Australia / Battery storage

New South Wales approved the $1 billion Mount Piper battery energy storage system, one of Australia’s biggest, which will store excess energy from the electricity grid during non-peak periods. The project is being developed by EnergyAustralia and will use the company’s existing electricity infrastructure. It will store up to 500 MW / 2,000 MW/h of power, enough for over 200,000 homes during high demand.

China / Coal

Coal power permits fell 83% in the first half of this year, with no new coal-based steelmaking projects approved. Also, 52% of experts surveyed by the Centre for Research on Energy and Clean Air in Finland, and the International Society for Energy Transition Studies in Australia, said they expect China’s coal consumption to peak next year.

China / Ocean energy

China General Nuclear Power Group (CGN) plans to build an integrated facility that will experiment with deep-sea renewable energy off the coast of Guangdong province. CGN will lead a tech consortium to build an offshore “integrated energy island,” which is regarded by scientists as one of the country’s 10 most challenging engineering projects.

India / Green hydrogen

India is facing challenges in the rollout of green hydrogen. According to CareEdge Ratings, the estimated levelised cost of green hydrogen, which includes both capital expenditure and operational expenditure per unit of production, is currently around 1.75 times that of grey hydrogen and around 1.50 times that of brown hydrogen.

India / Solar power

India will add 22.4 GW of solar capacity in 2024, according to JMK Research. This includes 17 GW from utility-scale projects, 4 GW from rooftop solar installations, and 1.4 GW from off-grid systems. In the wind sector, about 3.6 GW of new capacity is projected this year. From January to September 2024, India added 13.2 GW of utility-scale solar capacity, a 161% YoY increase.

India / Renewable energy

Tata Power and the Asian Development Bank inked a MoU to allocate $4.25 billion for the company’s renewable energy projects in India. Financing for some projects will be evaluated. These include a 966 MW solar wind hybrid project and pumped hydro storage project, as well as others that focus on the energy transition, decarbonisation, and battery storage.

LNG

The second term of Donald Trump will benefit LNG markets as he is expected to accelerate the expansion of LNG infrastructure in the U.S. through deregulation and fast-permitting. This will reverse the Biden administration’s regulatory pauses and increase leases on federal land for gas production.

Philippines / Renewable energy

Meralco PowerGen Corp (MGen) said it plans to increase its power generation portfolio through the addition of 1.5 GW of renewable energy.

Singapore / SMRs

Singapore should avoid becoming a test bed for small modular reactors (SMRs) in a push to diversify its energy mix away from oil; the problem with SMRs is their high cost and safety risks, according to energy analysts.

Thailand / Renewable energy

The Asian Development Bank and Gulf Renewable Energy inked an $820 million loan to build 12 renewable energy projects; this includes eight ground-mounted solar PV plants with contracted capacity of 393 MW and four ground-mounted solar PV plants with battery energy storage that have contracted capacity of 256 MW and 396 MW/h of energy storage.

2024 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

|

November |

|

|

December |

|

|

January 2025 |

|

|

February |

|

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Hulic Ochanomizu Bldg. 3F, 2-3-11, Surugadai, Kanda, Chiyoda-ku, Tokyo, Japan, 101-0062.