JAPAN NRG WEEKLY

JANUARY 8, 2025

JAPAN NRG WEEKLY

JANUARY 8, 2025

NEWS

TOP

- Govt unveils draft outlook for energy supply-demand in FY2040; scenarios indicate a preference to pursue all clean tech options

- New GX2040 Vision draft talks up the need to coordinate industry locations with abundant clean power supplies

- Consortiums led by JERA and Marubeni win the offshore wind projects in Round 3 of govt tenders

- Govt presents draft plan for global warming countermeasures

- Sekisui Chemical ready to mass produce perovskite solar cells

- INPEX advances plans for large-scale hydrogen plant in Japan

- Nippon Steel sees breakthrough in hydrogen-based steelmaking

- JERA launches think tank to tackle climate change

- Opinion: Coal remains essential for Asia’s energy security

- Head of TEPCO’s Fukushima HQ discusses progress at the site

- Chubu Electric bets on floating wind for future: President Hayashi

- Tohoku Electric, Chugoku Electric resume operations at nuclear power plants

- TEPCO holds briefing on Kashiwazaki-Kariwa with eye on restart

- JERA, Toho Gas to operate units at LNG-fired power station

- Shikoku Electric makes first overseas renewables investment

- Tokyo Century invests in solar project in Sicily

- Marubeni appoints operator for Yuza Town offshore wind project

- Chubu Electric and others seek to build wind farm in Hokkaido

- Japan’s shipping majors to expand their LNG fleets by 40%

- ENEOS HD unit JX Metals aims to go public in 2025

- LNG stocks down more than 20% YoY near end of December

- Japan’s shipping majors to expand their LNG fleets by 40%

- ENEOS HD unit JX Metals aims to go public in 2025

- LNG stocks down more than 20% YoY near end of December

JAPAN NRG WEEKLY

Events

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Editor-in-Chief)

John Varoli (Senior Editor, Americas)

Kyoko Fukuda (Japan)

Magdalena Osumi (Japan

Filippo Pedretti (Japan)

Tim Young (Japan)

Tetsuji Tomita (Japan)

Regular Contributors

Chisaki Watanabe (Japan)

Takehiro Masutomo (Japan)

Mayumi Watanabe (Japan)

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

OFTEN-USED ACRONYMS

METI | The Ministry of Economy, Trade and Industry | mmbtu | Million British Thermal Units |

MoE | Ministry of Environment | mb/d | Million barrels per day |

ANRE | Agency for Natural Resources and Energy | mtoe | Million Tons of Oil Equivalent |

NEDO | New Energy and Industrial Technology Development Organization | kWh | Kilowatt hours (electricity generation volume) |

TEPCO | Tokyo Electric Power Company | FIT | Feed-in Tariff |

KEPCO | Kansai Electric Power Company | FIP | Feed-in Premium |

EPCO | Electric Power Company | SAF | Sustainable Aviation Fuel |

JCC | Japan Crude Cocktail | NPP | Nuclear power plant |

JKM | Japan Korea Market, the Platt’s LNG benchmark | JOGMEC | Japan Organization for Metals and Energy Security |

CCUS | Carbon Capture, Utilization and Storage | ||

OCCTO | Organization for Cross-regional Coordination of Transmission Operators | ||

NRA | Nuclear Regulation Authority | ||

GX | Green Transformation |

NEWS: ENERGY TRANSITION & POLICY

Govt unveils draft outlook for energy supply-demand in FY2040

(Government statement, Dec 25)

- METI unveiled a draft outlook for energy supply-demand in FY2040, the basis for the draft 7th Basic Energy Plan released on Dec 17.

- Officials noted that while new technologies will play an overwhelming role in 2040, it is almost impossible today to forecast which ones will be dominant. To address this and keep public investment costs in check, METI advocates for a wide variety of measures while maintaining a “technology-neutral approach”.

- Also, METI created five scenarios to model energy supply and demand in FY2040. The first four are based on the idea that Japan’s NDC (emission cuts) targets are met, while the last one does not, assuming the continued use of current technology:

- (1) Scenario in which there is widespread adoption of innovative renewable energy technologies

- (2) Scenario in which there is widespread adoption of hydrogen, ammonia, synthetic fuels, and synthetic methane

- (3) Scenario in which there is widespread adoption of CCS

- (4) Scenario in which all of the above (1-3) are utilized

- (5) Scenario in which the cost of innovative tech (listed in 1-3) is not reduced sufficiently for such tech to become widespread

- In two scenarios, (1) renewable energy and (2) hydrogen/new fuels, the share of renewable energy is forecast at about 50%. Where they differ is the forecast for total electricity supply. In the case of (1), this increases to 1,150 TWh. In the case of (2), it is largely unchanged from today at 1,060 TWh and the lowest of the five options. This is because a diffusion of hydrogen and new fuels is seen as suppressing electrification.

- The scenarios that suggest the lowest electricity demand of the five are (2) hydrogen, new fuels and (3) CCS. Both forecast just 950 TWh of demand and assume a limited expansion of renewables.

- Officials assume that if the cost of decarbonization technologies does not decrease and the 73% CO2 reduction listed in the NDC is not achieved (as per scenario 5), the share of thermal power will be the largest in the electricity mix and LNG will remain as important as it is today. In contrast, if development of next-gen geothermal and nuclear technologies progresses, Japan will be able to reach its NDC goals.

- As part of the publication of this document, METI partially amended the draft of the new Basic Energy Plan. The following texts were added:

- Promotion of GX will help break away from excessive dependence on fossil fuels and lead to stable supply in the medium to long term

- Promotion of local distributed energy resources will also contribute to regional revitalization

- In the section on hydrogen, technological development of high-temperature gas-cooled reactors was listed as a way to promote the sector.

- Next, the govt plans to gather feedback through a public comments process.

- CONTEXT: In the draft of the Basic Energy Plan announced on December 17, the energy supply-demand outlook was presented only as a reference. This time, the government has clarified the various scenarios that will be used to determine the energy mix for FY2040.

Energy Supply-Demand in FY2040 by Scenario

(1) Renewables | (2) Hydrogen/ New Fuels | (3) CCS | (4) All Innovative Technologies | (5) Existing Technologies | ||

Electricity Demand (TWh) | 1040 | 950 | 950 | 1080 | 990 | |

Electricity Supply (TWh) | 1150 | 1060 | 1070 | 1200 | 1080 | |

|

| Renewables | 580 (50%) | 540 (51%) | 480 (45%) | 580 (48%) | 380 (35%) |

Nuclear | 230 (20%) | 210 (20%) | 210 (20%) | 240 (20%) | 220 (20%) | |

Thermal | 340 (30%) | 310 (29%) | 380 (35% | 390 (32%) | 490 (45%) | |

Govt announces draft GX2040 Vision

(Government statement, Dec 26)

- CONTEXT: This is the last of the three core documents that form the framework of the next national energy strategy. It sits alongside the 7th Basic Energy Plan and the Outlook for Energy Supply-Demand in FY2040.

- The document states that to achieve energy security, economic growth and decarbonization simultaneously, the government will need energy and industrial policies to work in tandem and also maximize the use of renewables.

- In terms of industrial structure, investments in GX fields are expected to create new businesses with innovative tech, including AI. Decarbonization (GX) and a digital shift (DX) are seen as complementing each other.

- In terms of future industry location, the government wants to accelerate the process of concentrating new facilities in hubs with ample clean power sources. Specifically, it will guide the location of data centers to areas where they are ‘suitable’ for the power grid. The govt also plans to promote next-gen communication infrastructure, the development of which should go hand-in-hand with that of the power grid.

- The govt aims to work with other countries to promote GX and contribute to the formation of rules that take into account Asia’s economic and social perspectives. This includes Japan’s Asia Zero Emission Community (AZEC) initiative.

- To accelerate GX, effort will be directed at both the energy sector, industrial users, and citizen lifestyles; there will be sector-specific investment strategies.

- Govt plans a growth-oriented carbon pricing system that combines regulation and support. This emissions trading system will be fully operational from FY2026 and a fossil fuel levy will be introduced from FY2028. An auction system for carbon credits for power generation companies will be introduced from FY2033.

- The govt is keen to ensure that the energy transition is fair and that workers can move into new GX-friendly industries, while Japan retains an active role in advanced supply chains.

- Progress on the implementation of GX-related policies will be reported at the GX Implementation Council and other appropriate venues.

- CONTEXT: The GX2040 Vision is a long-term directive aimed at increasing the predictability of investments in GX in an environment of increasing uncertainty.

TAKEAWAY: Most of the items listed in the draft GX2040 Vision summarize content discussed at the GX Implementation Council and various govt expert groups. In that sense, it is not entirely new material. However, the Vision underscores the determination of the govt to pursue a more aggressive renewables strategy as well as a desire to maintain some control over the industrial and digital development in the country, ensuring new facilities are added where there are clean power sources, rather than the other way around. The ambition of the Vision is large – it aims to be not only an environmental policy framework, but also as a large-scale project to reform Japan’s economic and social structures, as well as a statement to the international community and future generations. How it fares in practice will depend on the funding made available and investor interest.

Govt presents draft plan for global warming countermeasures

(Government statement, Dec 24)

- At a joint meeting on Dec 24, MoE and METI set Japan’s GHG reduction targets at 60% and 73% for FY2035 and FY2040 respectively. These fit the outlines released in the draft Plan for Global Warming Countermeasures on Dec 19 and 20.

- This plan will be reviewed by the Cabinet within the first two months of this year. After that, these GHG reduction targets will be submitted to the United Nations as the Nationally Determined Contributions (NDC).

- There were three opinions on the path to take in order to achieve a 46% reduction by 2030 and net zero by 2050. However, it was decided to connect the GHG targets across the years in a straight line.

- The main text of the draft plan is almost the same as the plan in 2021, but new items and measures have been added based on progress made over the past three years.

- In line with the revision of the Basic Energy Plan, items such as expanding decarbonized power sources and building next-generation networks were added.

- CONTEXT: The Plan for Global Warming Countermeasures is a comprehensive government document based on the Act on Promotion of Global Warming Countermeasures. As well as GHG reduction numbers, it includes measures to be taken by enterprises, citizens, and the national and local governments in order to achieve the targets. The Plan’s review period is every three years. This time, it was timed to coincide with the submission of the next NDC by February 2025.

Sekisui Chemical to mass produce and commercialize PSC

(Company statement, Sept 26)

- Sekisui Chemical will mass produce perovskite solar cells, branded as “Solafil”, at Sharp’s factory in Osaka that it has bought for ¥25 billion.

- Sekisui Solar Film will operate production. Sekisui Chemical will own 86%, while the remaining 14% will be owned by the Development Bank of Japan.

- The goal is to build a 100 MW production line by April 1, 2027. Investment for this phase is estimated at ¥90 billion. But the firm plans to expand to a 1 GW production with a ¥314 billion investment; half to be subsidized by the Green Innovation Fund.

- CONTEXT: Sekisui has been working on lightweight, flexible PSC tech but has faced challenges in reducing manufacturing costs and expanding production capacity. On Dec 25, the company was selected for METI’s GX Supply Chain Support Project that targets setting up a gigawatt-scale production system by 2030.

INPEX advances plans for large-scale blue hydrogen production in Niigata

(Company statement, Dec 18)

- INPEX completed feasibility studies for a blue hydrogen project in Niigata, leveraging the Nagaoka gas field and Joetsu LNG terminal.

- The project aims to build a hydrogen plant with a 100,000-ton annual capacity, using domestically produced natural gas and LNG.

- CO2 from hydrogen production will be captured and stored underground (CCS), enabling low-carbon hydrogen supply for local energy needs.

- CONTEXT: This is part of INPEX’s goal to have three hydrogen/CCS projects and 10 million tons of CO2 storage annually by 2030.

Nippon Steel claims breakthrough in hydrogen-based steelmaking by cutting CO2 43%

(Company statement, Dec 20)

- Nippon Steel successfully reduced CO2 emissions by 43% using hydrogen reduction in a test blast furnace, surpassing its 40% target and the levels publicized by other steel manufacturers around the world.

- This milestone was achieved at its Kimitsu Works in the last two months of 2024. The Green Innovation Fund, administered by NEDO, helped fund the testing, which had taken place since May 2022, steadily increasing the amount of CO2 that could be reduced through hydrogen injection.

- Nippon Steel now plans to scale the technology known as ‘Super COURSE50’ for larger furnaces, aiming eventually to halve CO2 emissions in steelmaking processes. The key factor will be maintaining a thermal balance in the blast furnace when using heated hydrogen.

- CONTEXT: There are currently around 800 blast furnaces in operation around the world, of which 20 are in Japan. Most of the blast furnaces are in China, which accounts for around half of the world’s crude steel production.

TAKEAWAY: Hydrogen is not the only option for steelmakers looking to swap out coal for a cleaner-burning product. However, this is the fuel that Nippon Steel has focused its tests on the most. The company had previously announced targets of producing “green steel” by the end of the decade, but the technology or approach it will take, as well as the location of the manufacturing, remain unclear.

JERA launches think tank to tackle climate change and energy security

(Company statement, Jan 6)

- On Jan 1 this year, JERA launched the JERA Global Institute think tank, seeking to enhance its research and analysis capabilities on domestic and international energy trends.

- The institute will focus on global and regional energy and environmental issues. The main goal is to support clean energy supply and public infrastructure.

- CONTEXT: Media reports suggest that JERA will employ 30 staff in the center and aims to emulate global energy majors such as Shell, which use similar in-house think tanks to produce reports around long-term demand forecasts and industry trends. Such reports are usually aimed at company senior management, but are also made available to the public.

Opinion: Coal remains essential for Asia’s energy security

(Nikkei, Dec 23)

- CONTEXT: This is an opinion piece by Nishizawa Jun, a visiting researcher at the Institute of Energy Economics. He discussed the new Basic Energy Plan. The current plan, released in 2021, sets a target of 59% non-fossil fuel power sources by 2030.

- Rising power demand, due to AI, could make this target hard to meet. Nishizawa argues that coal is essential for Japan and many Asian countries because it has lower geopolitical risks, and has advantages in storage and distribution.

- Japan’s self-sufficiency in coal development dropped from 53% in 2016 to 22% in 2022. This decline raises concerns about future supply chains.

- Nishizawa argues that Japan has lost momentum in promoting cleaner coal tech, but China continues to expand its coal power sector and the cleaner coal facilities.

- Nishizawa concludes that Japan must accept coal’s importance for developing nations, and should leverage environmental technologies to reclaim a leadership role globally.

NEWS: ELECTRICITY MARKETS

Consortiums led by JERA and Marubeni win offshore wind projects in 3rd round tender

(Government statement, Dec 24)

- Two separate consortiums led by Japan’s largest utility JERA and trading house Marubeni have been awarded large-scale offshore wind power projects in the sector’s Round 3 tender. The long-awaited results were announced on Dec 24.

- Key information on the projects awarded in R3 include:

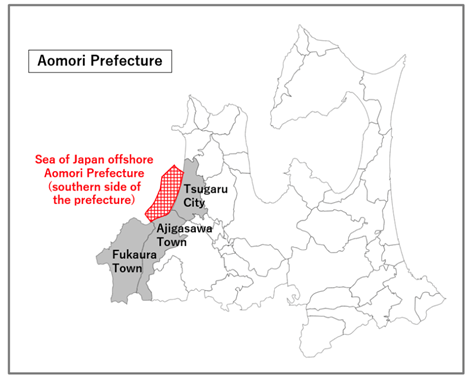

Location: Aomori South (south Japan Sea off Aomori Pref)

Winner: JERA, Green Power Investment, Tohoku Electric;

Planned capacity: 615 MW

Turbines: 41 Siemens Gamesa units, 15 MW each;

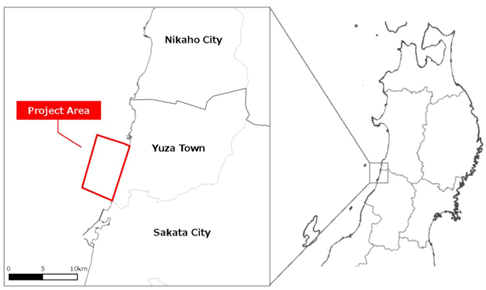

Location: Off the coast of Yuza Town, Yamagata Pref

Winner: Marubeni, KEPCO, BP Iota, Tokyo Gas, construction firm Marutaka;

Planned capacity: 450 MW

Turbines: 30 Siemens Gamesa units, 15 MW each.

- In total, five overseas firms participated: bp’s unit BP Iota; Vena Energy (HQ in Singapore), CI IV Coöperatief, a subsidiary of Danish CIP; Norwegian Equinor; and, SSE Pacifico (a JV between SSE Renewables, part of UK-listed SSE, and Pacifico Energy, a major Japanese renewables developer.

- CONTEXT: BP Iota is the third overseas winning participant after Germany’s RWE and Spain’s Iberdrola.

- Both winning consortiums bid at ¥3/ kWh, a “zero premium” level under FIP. Such bids are awarded the full points in the price evaluation category, meaning that developers agree not to seek subsidies beyond the market price for electricity.

- While prices for losing bids were not disclosed, the fact that all participants were given full marks in the price evaluation category shows that all bids, including losing bids, were priced at the zero premium level or at ¥3/ kWh or below.

- All participants submitted plans with operations scheduled to begin June 30, 2030. Detailed feasibility assessment of each plan shows the winning bids were superior in nearly all categories and areas subject to review.

- CONTEXT: Bids were evaluated in two main categories – price and feasibility; with the maximum score of 120 each, and a total of 240 points. In terms of feasibility, METI/MLIT considered factors such as the planned speed of execution; foundation type; track record of the firms; funding plan; and the details of the construction process, as well as risk scenarios after the start of operation, measures to ensure stable supply of electricity, efforts at communication and relations with local communities (fisheries, etc ) and impact on the local economies.

TAKEAWAY: In Round 3, the feasibility category became the main competitive factor in the overall project assessment. Assessors seemed to have focused most on detailed construction and risk scenarios after the launch of operations, as well as the availability / nature of off-take agreements.

In terms of expanding the international nature of the sector, it’s a positive to see another win for a non-Japanese firm, following the successes of RWE and Iberdrola. However, BP Iota’s win is as much a win for JERA as it is for the UK energy major since the announcement of a global offshore wind JV between the two companies at the end of last year. As such, JERA can now claim to be one of the leaders in Japan’s offshore wind sector, rivaling the influence of Mitsubishi Corp, which since its Round 1 blitz has barely featured. Reports in the Japanese magazine Diamond at the very end of 2024 suggest Mitsubishi’s reluctance to delve further in the sector is due to the trading house potentially facing valuation writedowns on some of its three Round 1 projects. While Diamond‘s speculation that Mitsubishi might go as far as selling its projects is highly unlikely, it does illustrate the issue of cost inflation affecting all developers. METI is now looking at ways to provide additional support for the sector.

Project Aomori

SouthProject off Yuza Town, Yamagata Pref

Winning bids in R3 auction

Project Name | Project Capacity and Bid (¥ / kWh) | Operation Starts | Project Members | Wind Turbine Manufacture, number of units |

Aomori South | 615 MW (¥3) | June 2030 | JERA, Green Power Investment, Tohoku Electric | SGRE 15 MW × 41 SG DD-236 |

Off the coast of Yuza Town, Yamagata Pref | 450 MW (¥3) | June 2030 | Marubeni, KEPCO, BP Iota, Tokyo Gas, Marutaka Corp | SGRE 15 MW × 30 |

Losing bids in R3 auction

Project Name | Project Capacity and Bid (¥ / kWh) | Operation Starts | Project Members | Wind Turbine Manufacture, number of units |

Aomori South | 495 MW Zero Premium (¥3 or lower) | June 2030 | CI IV Transfer Coöperatief U.A., Tokyu Land, Hokuriku Electric, Toda | GE 16.5 MW × 30 Haliade-X250 |

517 MW Zero Premium (¥3 or lower) | June 2030 | Vena Energy | Vestas 15 MW × 38 V236-15MW | |

Off the coast of Yuza Town, Yamagata Pref | 480 MW Zero Premium (¥3 or lower) | June 2030 | Eurus Energy, Equinor Japan, ENEOS Renewable Energy, Toyota Tsusho, Toda | SGRE 15 MW × 32 SG DD-236 |

480 MW Zero Premium (¥3 or lower) | June 2030 | TEPCO Renewable Power, Sumitomo Corp, Mitsui Fudosan, East Japan Railway Company | Vestas 15 MW × 32 V236-15MW | |

495 MW Zero Premium (¥3 or lower) | June 2030 | Kyuden Mirai Energy, SSE Pacifico, JAPEX | SGRE 15 MW × 33 SG DD-236 |

- SIDE DEVELOPMENT:

- Marubeni appoints operator for Yuza Town offshore wind project

- (Company statement, Dec 24)

- Marubeni-led consortium appointed Yamagata Yuza Offshore Wind, a special purpose company to operate the offshore wind farm off the coast of Yuza Town, Yamagata Pref, awarded in the Round 3 offshore wind tender.

- The SPC was set up through a joint investment by Marubeni, KEPCO, bp Iota, a 100% owned subsidiary of energy firm bp, Tokyo Gas and Marutaka.

- The project involves the construction, maintenance, and operation of a 450 MW bottom-fixed offshore wind farm.

Chubu Electric, Hokkaido Electric and Kanadevia seek to build wind farm in Hokkaido

(Company statement, Dec 23)

- Chubu Electric, Hokkaido Electric and Kanadevia (formerly Hitachi Zosen) plan to build an onshore wind power project in Kaminokuni, Hokkaido.

- The project could have a maximum capacity of 183 MW, with up to 30 turbine units with a capacity between 4.2 MW and 6.1 MW.

- The firms submitted the draft environmental considerations statement as part of the Environmental Impact Assessment process to METI, the Gov of Hokkaido, and the Kaminokuni Town Mayor. The plan is available for viewing until Jan 31.

- SIDE DEVELOPMENT:

- GPI unveils EIA for Tsugaru wind farm

- (Company statement, Sept 27)

- On Dec 27, Green Power Investment released an environmental impact assessment for the Tsugaru offshore wind farm (Aomori Pref). The firm, along with JERA and Tohoku Electric, was selected by the government as operators.

- This project aims for a max capacity of 600 MW. Construction is set to begin in 2028, with commercial operation expected in June 2030. The firm plans to use a monopile fixed-bottom structure.

Chubu Electric bets on floating wind as pillar of Japan’s renewables: President Hayashi

(Nikkei, Jan 1)

- Chubu Electric President Hayashi has stressed the need to strengthen the development of floating offshore wind power, naming it as a key area for growth.

- The firm’s current projects include an offshore wind farm off Goto City, Nagasaki Pref, and a demonstration project off Tahara City, Aichi Pref, through its subsidiary C-TECH.

- Among other critical measures for Japan’s decarbonization, Hayashi named the restart, rebuild, and construction of nuclear power plants, as well as technologies to reduce CO₂ emissions from thermal power.

- Regarding the utility’s Hamaoka NPP in Shizuoka, Hayashi said that regulatory safety reviews typically take around two years, with additional time required for restarting operations.

- CONTEXT: Chubu Electric aims to increase renewable energy capacity by 3.2 GW by 2030 (compared to FY2017). As of Sept 2024, the increase measured just 1.03 GW.

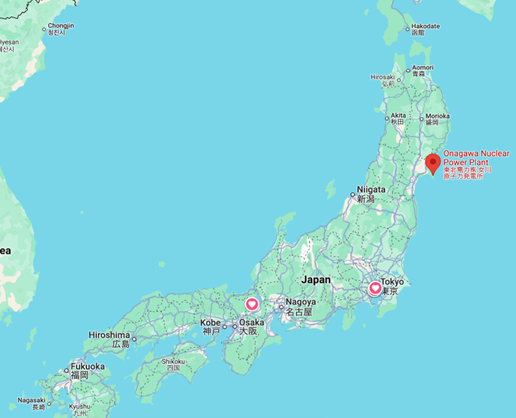

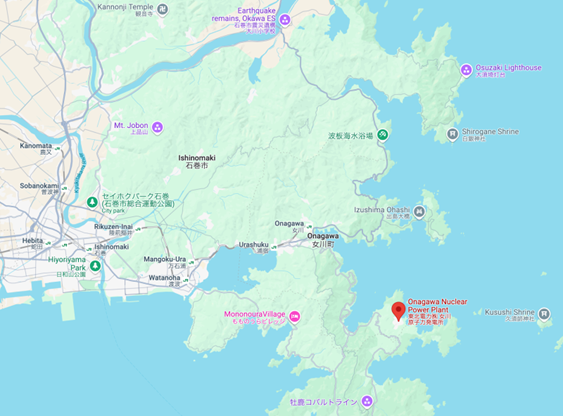

Onagawa NPP Unit 2 resumes commercial operations

(Company statement, Dec 26)

- On Dec 26, Tohoku Electric resumed commercial operation of Onagawa NPP Unit 2 following the completion of the comprehensive load performance test.

TAKEAWAY: The restart prompted discussions among neighboring municipalities on disaster preparedness and nuclear fuel taxes. Five municipalities within the 5–30 km Urgent Protective Action Planning Zone (UPZ) established a council, planning to request increased allocations of nuclear fuel tax grants from Miyagi Pref. 10% of the nuclear fuel tax collected by the prefecture from Tohoku Electric is allocated to Onagawa and 5% to Ishinomaki. The five municipalities received a total of ¥6.5 million for the first time in FY2024. The tax revenue will now increase, as the plant begins operations. The five municipalities argue that they bear costs for evacuation planning and disaster drills. Onagawa and Ishinomaki are preparing to impose their own taxes on spent nuclear fuel stored at the plant’s facilities.

- SIDE DEVELOPMENT:

- Chugoku Electric resumes power generation at Shimane NPP Unit 2

- (Company statement, Dec 23)

- Chugoku Electric resumed power generation at Shimane NPP Unit 2 (BMW, 820 MW). It plans the restart of commercial operations on Jan 10.

- CONTEXT: The restart will improve financial performance by ¥40 billion per year. primarily due to reduced fuel costs for thermal power generation. It is the 14th reactor to restart in Japan since the Fukushima Daiichi disaster.

- SIDE DEVELOPMENT:

- TEPCO holds briefing on Kashiwazaki-Kariwa NPP

- (Nikkei, Dec 21)

- TEPCO held a new type of event on Dec 21 in Nagaoka City, Niigata Pref, explaining to locals its efforts to restart the Kashiwazaki-Kariwa NPP.

- Topics included radiation risk evaluation and energy policies to curb electricity costs. TEPCO executives also addressed questions from attendees. Of the 61 questions submitted, 36% were about the plant’s restart.

- CONTEXT: Nagaoka neighbours Kashiwazaki. Most of the city is within a 30 km radius from the NPP. Similar events were held in Nagaoka and surrounding places in the summer of last year.

TAKEAWAY: With the restart of Shimane NPP, there are now five utilities in Japan operating a nuclear power plant – Kansai, Kyushu, Shikoku, Chugoku and Tohoku EPCOs. The same number of utilities have nuclear facilities that have not operated since at least May 2012 – twelve and a half years ago.

While the 14 restarted reactors have added 13.3 GW of power capacity to the grid (about half of the operable capacity of South Korea’s nuclear plants), a further 19.8 GW remains offline. Almost half of that idle capacity is at one location: the Kashiwazaki-Kariwa NPP (TEPCO, 8.2 GW).

Among the 14 units allowed to restart, 12 use PWR technology and 2 use BWR tech (the same as the reactors at the Fukushima Daiichi NPP). Of the 19 yet to restart, 4 are PWRs and 15 are BWRs.

The next restart may be one of the units of the Kashiwazaki-Kariwa NPP. Each date set by operator TEPCO for the restart has been exceeded and the latest guidance from the local authorities is that no restart is possible within this fiscal year (ending March 31, 2025). As such, the next likely restart window is likely to be May or June.

Other unit restart plans are either uncertain or slated for 2026/27. That suggests that despite the steady gains in bringing back online nuclear capacity, it’s unlikely to add much more than 10% this year.

KEPCO seeks approval of long-term management plan for Takahama NPP Unit 2

(Company statement, Dec 25)

- KEPCO applied to the NRA for approval of a long-term facility management plan for Takahama NPP Unit 2. The plan addresses measures for aging management as the plant approaches 50 years of operation.

- The degradation evaluation confirmed that the plant can remain sound beyond 50 years. KEPCO will supplement current maintenance activities with extra measures for certain components. The plan also outlines strategies to address obsolescence.

- CONTEXT: Amendments to the Reactor Regulation Act take effect on June 6.

Head of TEPCO’s Fukushima Revitalization HQ discusses future plans

(Nikkei, Dec 25)

- CONTEXT: Nikkei interviewed Akimoto Nobuhide, head of TEPCO’s Fukushima Revitalization Headquarters. He discussed local opinions on the decommissioning of Fukushima Daiichi NPP. He said TEPCO will increase dialogue, such as plant tours.

- Over 1,200 local firms participated in decommissioning in the past five years.

- As for compensation, the fifth round of extra payments began in 2023 and has reached 90% of eligible claimants. It covers around 1.3 million cases. Compensation related to the release of treated water remains contentious.

- CONTEXT: Developments in 2024 included the first removal of melted fuel since the 2011 accident. The decommissioning roadmap is set for completion by 2051. Still, there was a radioactive water leak in Feb and a cable-cutting incident in April. It halted the release of treated water, and a three-month cooling failure in the spent fuel pool of Unit 2 due to corroded pipes. These incidents caused public anxiety.

- SIDE DEVELOPMENT:

- TEPCO to attempt second fuel debris retrieval at Fukushima

- (Nikkei, Dec 26)

- TEPCO plans a second test retrieval of nuclear fuel debris from Fukushima Daiichi NPP Unit 2 in March–April 2025. It will use the same rod-like retrieval device as before. TEPCO aims to collect about 0.7 grams of debris, like the first attempt.

- CONTEXT: The debris retrieved in November is now under analysis at a national research institute. The initial retrieval encountered setbacks due to a camera malfunction leading to a halt.

JERA and Toho Gas to develop and operate Units 7 and 8 at Chita Power Station

(Company statement, Dec 23)

- JERA and Toho Gas will develop and operate Units 7 and 8 of the Chita Thermal Power Station. Operations are scheduled to begin in FY2029. The project involves building an LNG-fueled gas turbine combined cycle power plant.

- Total capacity will be 1.3 GW and thermal efficiency of about 64%. The ownership will be 75% JERA Power Investment and 25% Toho Gas.

Shikoku Electric takes stake in Indonesia’s HGI, first investment in overseas renewables

(Company statement, Dec 19)

- Shikoku Electric acquired a 25% stake in Hero Global Investment (HGI), a renewable energy operator in Indonesia. The stock purchase agreement marks Shikoku Electric’s first investment in an overseas renewable energy company.

- HGI runs two hydropower and one biogas power plant. Electricity is sold under long-term contracts with the Indonesian state-owned power company.

- The firm’s plans include development of new hydro, solar, biogas, and biomass power projects and achieving a target capacity of about 100 MW of renewables by 2030. Shikoku Electric will support HGI from the design and construction stages.

Tokyo Century invests in solar project in Sicily

(Company statement, Sept 26)

- Tokyo Century invested in a solar power project developed and built by Capital Dynamics, a Swiss firm that manages over 2 GW of clean energy assets, mainly in the UK, Italy, and Spain.

- The 189 MW project will be in Palermo and Trapani cities in Sicily. Construction began in fall 2024, with operations set to begin in July.

- CONTEXT: Italy’s energy mix relies heavily on imported natural gas, which has prompted the govt to expand solar capacity from 25 GW in 2022 to 80 GW by 2030.

- CONTEXT: As part of overseas expansion, Tokyo Century recently acquired stakes in existing solar power plants in the UK, and invested in a North American renewables fund.

NEWS: OIL, GAS & MINING

Japan’s shipping majors to expand their LNG fleets 40% by 2030

(Nikkei, Jan 5)

- Mitsui O.S.K. Lines (MOL): Plans to increase its LNG carrier fleet to 140 vessels by FY2028, aiming for 150 by 2030. Current holdings include 97 vessels, making MOL the top global owner of LNG transport. Expected additional investment: ¥500–600 billion.

- Nippon Yusen Kaisha (NYK): Targeting a 30% fleet expansion to reach 120 vessels by FY2028, supported by ¥250–300 billion in investments.

- Kawasaki Kisen Kaisha (K-Line): Will grow its fleet by 60%, from 47 to 75 vessels, by FY2030, investing ¥250–300 billion.

- Investments reflect rising LNG demand, expected to grow to 624 million tons annually by 2035, driven by decarbonization and energy diversification. All three companies expect to share the LNG vessel construction costs with their overseas partners, in order to keep their investment down.

- CONTEXT: The market price for an LNG carrier is said to be ¥30-40 billion.

TAKEAWAY: While the role of natural gas as an energy transition fuel continues to be debated, investments in more LNG demand-side facilities continue apace. As Japan NRG has detailed in prior analyses, the shipping sector looks willing to step in and pick up the slack in power sector demand, seeing the CO2 reduction impact from LNG (~30% compared to regular bunker fuel) as worth it. The shipping sector is also seen as a major potential demand hub for ammonia producers, but at this point the investment allocation to vessels powered by hydrogen carriers is unclear.

ENEOS HD unit JX Metals aims for semiconductor growth with public listing

(Nikkei Tech Foresight, Jan 7)

- JX Nippon Mining & Metals will list in 2025, targeting 80% of operating profit from semiconductor materials by 2040.

- The firm, which sits under the ENEOS Holdings umbrella, will expand its market presence with molybdenum precursors for chip production and advanced packaging for AI semiconductors. It aims to scale its new CVD/ALD materials business to generate ¥10 billion in operating profit, with production facilities in Japan and Germany.

- CONTEXT: JX Metals has a 60% global share in sputtering (the adding of an ultra-thin layer on materials) and makes some of the highest purity copper in the world. The metals side of the business has always been a separate division of ENEOS, which started as an oil and gas company.

LNG stocks down 7.2% from previous week, down 23.3% YoY

(Government data, Dec 25)

- As of Dec 22, the LNG stocks of 10 power utilities were 2.07 Mt, down 7.2% from the previous week (2.23 Mt), and down 23.3% from end Dec 2023 (2.16 Mt), and down 4.2% from the 5-year average of 2.1 Mt.

- The latest figures will be released today, January 8.

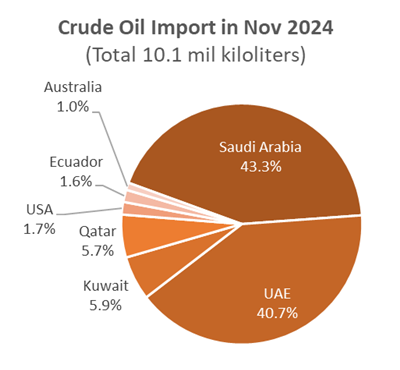

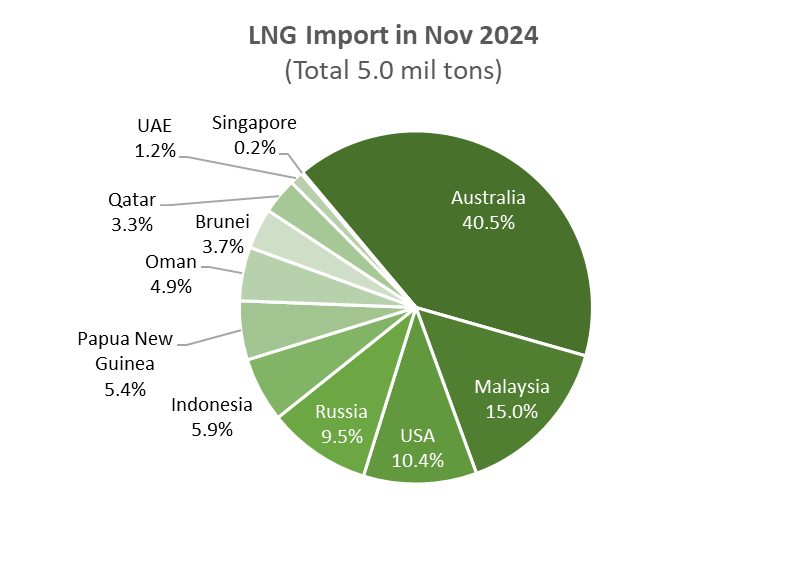

November Oil/ Gas/ Coal trade statistics

(Government data, Dec 26)

Imports | Volume | YoY | Value (Yen) | YoY |

Crude oil | 10.1 million kiloliters | -17% | 761.7 billion | -29.7% |

LNG | 5.1 million tons | -5.3% | 483.4 billion | 2.5% |

Thermal coal | 8.5 million tons | 2.2% | 200.4 billion | -10.2% |

- In November, Japan imported 10.1 million kiloliters of crude oil, 14.6% less than in October, and 17% less YoY. As usual, more than 95% of the total crude oil imports came from the Middle East.

- The imported volume decreased, but refining companies boosted output to supply fuels for heating, increasing production 4.7% over the previous month.

- LNG imports in November totaled 5 Mt, down 4.6% over October (5.3 Mt) and down 5.3% YoY. Australia is the main exporter of LNG to Japan; its volume was up 16.2% over September (from 1.8 Mt to 2.1 Mt).

- November thermal coal imports, 8.5 Mt, were about the same as in October, only a 0.2% decrease; but a 2.2% increase YoY. Japan boosted purchases in September (10.7 Mt) in preparation for winter, but weather was relatively warm until early December. Japan has enough coal stocks and imports may stay relatively low.

2025 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

Month | Date | Event |

January | 6 | First market trading |

6-24 | FIT/FIP solar auction #23 | |

21-22 | World Forum Offshore Wind (WFO) Global Summit 2025, Barcelona, Spain | |

29-31 | ENEX 2025 / DER Microgrid Japan 2025 / Renewable Energy 2025 / Offshore Tech Japan 2025 / InterAqua 2025 / Green Infrastructure Industry @ Tokyo Big Sight | |

February | 19-21 | Smart Energy Week 2025 / H2 & FC Expo / PV Expo / Battery Japan / Smart Grid Expo / Wind Expo / Biomass Expo / Zero-E Thermal Expo / GX Management Week / Decarbonization Expo / Circular Economy Expo @ Tokyo Big Sight |

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Hulic Ochanomizu Bldg. 3F, 2-3-11, Surugadai, Kanda, Chiyoda-ku, Tokyo, Japan, 101-0062.