JAPAN NRG WEEKLY

JANUARY 20, 2025

ANALYSIS

AMONG GLOBAL UNCERTAINTIES, JAPAN STILL SEES KEY ROLE FOR LNG IN ENERGY SECURITY

- Hoping to boost both domestic energy security and cement its role as a leading LNG trading hub, Japan continues to diversify its suppliers

- Recent energy strategy draft assured support for LNG as a stable power generation fuel, but does that tally with the strategy of Japanese LNG buyers?

JAPAN MUST TAME WIND POWER COSTS; DATA MAY USE 10% OF ALL POWER BY 2030: YERGIN

- On Jan 13, Daniel Yergin shared his thoughts on the shifting sands of energy security, the role of renewables, and the implications of new alliances and rivalries.

- He talked about Japan, Trump, and how Big Tech will determine the future of energy.

NEWS

- ANRE allocates more funds to energy saving, toughens rules for data center consumption

- METI Minister visits Middle East to further cooperation

- Concerns over construction costs of transmission line between Hokkaido and Honshu

- Kyushu Electric to offer additional annual wholesale electricity contracts

- U.S. hydrogen projects among likely winners in Japan’s CfD auction: Argus

- eFuel startup Infinium secures more funding

- TEPCO PG partners with Endeavour Energy to expand distributed energy resources

- Chubu Electric Miraiz, KEPCO, etc. to promote PSC

WIND POWER AND OTHER RENEWABLES

- KEPCO, RWE plan 600 MW wind farm off Hokkaido coast

- Sumitomo inks loan for expansion of Indonesian geothermal project

- KEPCO long-term management plan approved for Takahama NPP

- Tohoku Electric to do geological survey for Onagawa NPP

- MOL and JERA sign deal for new LNG carrier

INPEX wins oil and gas licenses in Norway

CARBON CAPTURE & SYNTHETIC FUELS

- Kanadevia, AIST develop catalyst for LPG synthesis

- Cosmo-led group completes SAF production plant

ASIA PACIFIC REVIEW

This column provides a brief overview of the region’s main energy events from the past week

EVENT

| Jan 6-24 | FIT/FIP solar auction #23 |

| Jan 20 | Japan begins the Long-Term Decarbonization Power Source auction for clean power capacity |

| Jan 21-22 | World Forum Offshore Wind (WFO) Global Summit 2025, Barcelona, Spain |

| Jan 29-31 | Offshore Technology & ENEX Exhibition @ Tokyo Big Sight |

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Editor-in-Chief)

John Varoli (Senior Editor, Americas)

Kyoko Fukuda (Japan)

Magdalena Osumi (Japan

Filippo Pedretti (Japan)

Tim Young (Japan)

Tetsuji Tomita (Japan)

Regular Contributors

Chisaki Watanabe (Japan)

Takehiro Masutomo (Japan)

Mayumi Watanabe (Japan)

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

OFTEN-USED ACRONYMS

METI | The Ministry of Economy, Trade and Industry | mmbtu | Million British Thermal Units |

MoE | Ministry of Environment | mb/d | Million barrels per day |

ANRE | Agency for Natural Resources and Energy | mtoe | Million Tons of Oil Equivalent |

NEDO | New Energy and Industrial Technology Development Organization | kWh | Kilowatt hours (electricity generation volume) |

TEPCO | Tokyo Electric Power Company | FIT | Feed-in Tariff |

KEPCO | Kansai Electric Power Company | FIP | Feed-in Premium |

EPCO | Electric Power Company | SAF | Sustainable Aviation Fuel |

JCC | Japan Crude Cocktail | NPP | Nuclear power plant |

JKM | Japan Korea Market, the Platt’s LNG benchmark | JOGMEC | Japan Organization for Metals and Energy Security |

CCUS | Carbon Capture, Utilization and Storage | ||

OCCTO | Organization for Cross-regional Coordination of Transmission Operators | ||

NRA | Nuclear Regulation Authority | ||

GX | Green Transformation |

NEWS: GENERAL POLICY AND TRENDS

ANRE allocates more funds to energy saving, toughens rules for data center consumption

(Government statement, Jan 10)

- This fiscal year, Japan will allocate over ¥275 billion, including future obligations for multi-year commitments, to upgrade energy-saving and non-fossil fuel equipment at industrial and residential energy systems, especially at SMEs. Demand for subsidies of this kind has been robust, according to METI.

- The support will cover installation of AI and other advanced tech to monitor precise energy usage and dicover ways to reduce losses, as well as money for heat pumps, thermal insulation upgrades, and high-efficiency homes (ZEH-level).

- CONTEXT: The spending is part of a three-year, ¥700 billion program started last year to raise energy efficiency and help smaller businesses to electrify and take steps to decarbonize.

- Part of this program is an effort to curb rising energy consumption at data centers. It applies to businesses that utilize 1,500 kl or more of energy per year (oil equivalent) in the process of data center operations or other kinds of data processing.

- The Govt wants to impose standards on the larger data centers, including:

- Power Usage Effectiveness (PUE) benchmarks; By FY2030, data center operators must achieve an average PUE of 1.4 or below, improving energy efficiency indicators by 1% annually in the medium to long term and submitting periodic reports on long-term plans and progress.

- New data centers, including tenant-based centers, should introduce clearly defined mandatory energy efficiency standards with emphasis on transparency

- a “pledge & review” system.

- All operators will be encouraged to disclose certain data voluntarily.

- The government will monitor and publish information, including naming non-compliant operators and providing aggregate-level data.

- One of the stated aims is to to enhance data centers’ societal acceptance and drive industry-wide improvements.

- SIDE DEVELOPMENT:

- METI Minister outlines Japan’s energy strategy in 2025

- (Japan Atomic Industrial Forum, Jan 7)

- The METI Minister outlined economic and energy strategies in 2025. On GX, he emphasized developing renewables and nuclear energy.

- In December, the govt finalized drafts of the Strategic Energy Plan and GX 2040 vision. Focus points include replacing decommissioned nuclear plants with advanced reactors to ensure safety, as well as the decommissioning of the Fukushima Daiichi NPP.

METI Minister visits Middle East to further cooperation

(Government statement, Jan 15)

- On Jan 11 to 16, METI Minister Muto visited the UAE and Saudi Arabia to further bilateral partnerships, particularly on clean energy.

- Muto and the Saudi Minister of Investment discussed the Japan-Saudi Vision 2030. Several Japanese firms, including startups specializing in AI and IT, signed 13 MoUs with Saudi firms on energy-related initiatives.

- Muto met with the Saudi energy minister to reaffirm the kingdom’s role as a key oil supplier. Muto also attended the World Future Energy Summit in Abu Dhabi.

- ADNOC (Abu Dhabi National Oil Company) reaffirmed its commitment to reducing methane emissions in the LNG value chain under the Japan-led CLEAN Initiative, which includes 35 global energy and resource firms.

- CONTEXT: The UAE is developing new gas fields and LNG plants, with Japanese firms like Mitsui holding stakes in these projects. The Saudi-Japan Lighthouse initiative focuses on clean energy materials. Projects will focus on hydrogen, ammonia, e-fuel, carbon recycling, DAC, critical energy minerals, advanced materials, and research exchange to improve supply chain resilience.

- SIDE DEVELOPMENT:

- Malaysia and Japan to deepen energy cooperation

- (Nikkei Asia, Jan 10)

- PM Ishiba met his Malaysian counterpart in Putrajaya to discuss energy security, such as natural gas and hydrogen projects. The Malaysian PM highlighted his country’s LNG exports to Japan and hydrogen projects in Sarawak that have Japanese support.

- This was Ishiba’s first official overseas tour since taking office. He called Malaysia a “bridge” between Asia and the Middle East.

NEWS: ELECTRICITY MARKETS

Concerns over construction costs of transmission line between Hokkaido and Honshu

(Nikkei, Jan 16)

- Soaring costs to build a transmission line connecting Hokkaido and Honshu, now estimated at ¥1.5 to ¥1.8 trillion, are causing concerns among potential bidders.

- A consortium led by TEPCO might withdraw from the bidding unless conditions improve. On Jan 15, OCCTO held a hearing to confirm the conditions submitted by the TEPCO-led consortium, which highlighted uncertainties in feasibility, financial support, and profitability.

- TEPCO Power Grid vice chief Okamoto said the company can’t commit to the project without resolving these issues, urging the government for support.

- Two groups are bidding for the project: the TEPCO consortium and another led by UK-based Frontier Power. The winner will be chosen by late FY2025.

TAKEAWAY: This transmission line is one of the key parts of the system that will unlock the development of offshore wind power around Hokkaido. Like other large infrastructure projects, this one is suffering from rising EPC costs, a weak yen, and potentially higher financing costs with the Bank of Japan signaling a readiness to raise interest rates. Govt officials have tried to keep costs under control as much as possible but given the inflationary pressures, it’s becoming counterproductive. Expect METI to insert flexibility clauses to allow developers to claw back some cost increases.

Kyushu Electric to offer additional annual wholesale electricity contracts

(Company statement, Jan 14)

- For FY2025, Kyushu Electric will conduct an additional sale of annual wholesale electricity contracts, including base and custom-tailored products.

- Interested businesses must request documentation and applications are open until Jan 31. Contracts will be finalized by March 21.

- CONTEXT: Base products provide 24-hour coverage; custom products allow buyers to set flexible power volumes above a minimum threshold. Pricing includes a two-part tariff with a basic fee and energy charges, and grid division costs are borne by buyers.

Toshiba ESS launches renewable energy trading platform

(Company statement, Jan 14)

- Toshiba Energy Systems (Toshiba ESS) unveiled EneHub, a platform matching renewable energy sellers with buyers such as power retailers and corporate consumers. The site facilitates various contracts, including offsite PPAs.

- EneHub covers solar, wind, hydro, geothermal, and biomass power sources across Japan, including small-scale facilities under 50 kW. Currently, power plants with a combined output of 69 MW are registered.

- The platform supports physical PPAs and virtual PPAs. It accommodates various schemes, including FIP, non-FIP, and excess power purchases.

- Toshiba ESS assumes imbalance risk, manages power output forecasts, and submits operational plans to grid operators.

JERA implements AI management system at thermal power plants

(Nikkei, Jan 15)

- By the end of last year, JERA implemented AI-driven operational management systems at its thermal power plants for anomaly detection and response advice. It has a centralized control center for remote management, reducing response times by 66%. Microsoft collaborated on the development.

- The system has already reduced unplanned outages by 10-20% at pilot sites. It cut repair and fuel costs, with an estimated savings of ¥40 billion per large plant. JERA plans to sell the system to third parties.

Vena Energy signs PPA with LINE Yahoo for renewables supply

(Company statement, Jan 17)

- Renewables developer Vena Energy plans to help Japan’s top social media and e-commerce company, LINE Yahoo, go green. The 20-year agreement will use a virtual PPA model where Vena sells electricity to the Japan Electric Power Exchange (JEPX) while LINE Yahoo purchases only the environmental value.

- The power will come from the 70 MW Maniwa solar farm in Maniwa City, Okayama Pref, that Vena Energy will build and launch in August 2026.

- This marks LINE Yahoo’s first use of the PPA model; its scale will be the largest in Japan for a virtual PPA.

- SIDE DEVELOPMENT:

- Octopus Energy signs PPA in Gunma to supply green energy

- (Company statement, Jan 16)

- Octopus Energy was selected by Gunma Pref as the retail electricity provider for a local production and consumption PPA initiative.

- Starting from April 2025, over a 3-year period Octopus Energy will supply around 280 GWh of electricity generated from hydropower stations owned by the prefecture.

- The electricity, including non-fossil value, will be distributed to 17 designated locations, supporting local green energy usage and regional contribution.

- SIDE DEVELOPMENT:

- Toyoda Gosei inks PPA for renewable energy in North America

- (Company statement, Jan 15)

- The U.S. subsidiary of Toyota Motor, Toyoda Gosei North America (TGNA), inked a PPA with Eurus Energy America, a member of Eurus Energy Group.

- TGNA will purchase renewable energy certificates over 10 years. The certificates have an additionality of 100 GWh/ year that will be generated at a wind farm in Texas.

- This will help cut TGNA’s emissions in the Americas by more than 20% (over FY2023).

METI cites Groove Energy for failed contributions for renewables promotion

(Government statement, Jan 14)

- METI disclosed the name of utility Groove Energy, which failed to pay contributions to OCCTO under the act on special measures concerning procurement of electricity from renewable energy sources by utilities. Groove Energy failed to pay by the extended deadline of Jan 10.

- CONTEXT: Article 34, Paragraph 3 of the act mandates that utilities purchase electricity generated by renewables at pre-determined prices and obligates them to make payments to OCCTO. Groove Energy was supposed to issue the payment by Jan 6. These payments originate from surcharges collected from electricity users as part of the cost-sharing mechanism for promoting renewables under Japan’s FIT system.

- OCCTO informs the utilities that missed the deadline and specifies a new deadline, after which it notifies METI of the failed payments. The METI Minister is obligated to publicly announce names of non-compliant utilities.

Rokkasho partners with firms for local decarbonization

(Government statement, Dec 27)

- Rokkasho Village in Aomori Pref will partner with private firms – Aomori Wind Development, Pacific Power, and Aomori Michinoku Bank to create Rokkasho Energy Management, a regional energy company.

- The JV will engage in electricity sales, generation, transmission, and distribution, as well as renewable energy projects and environmental value trading. It will promote solar power and BESS projects.

- Rokkasho Village holds a 55% stake, while Aomori Wind Development and Pacific Power each hold 21%, and Aomori Michinoku Bank owns 3%.

- CONTEXT: Pacific Power is a specialist in local power companies and has worked with a number of municipalities around Japan.

NEWS: HYDROGEN

U.S. hydrogen projects among likely winners in Japan’s CfD auction: Argus

(Japan NRG, Jan 16)

- U.S. Gulf Coast projects are likely among the winners in Japan’s inaugural Contract for Difference (CfD) auction to provide subsidies for hydrogen, ammonia and related fuels, Argus analysts said as part of their Global Hydrogen Outlook 2025 webinar.

- Japanese firms inked agreements to potentially invest in several Gulf Coast ammonia and hydrogen projects over the past year or so, and together with U.S. subsidies, these projects should be among the most competitive, Argus analysts said.

- CONTEXT: Among the U.S. projects with Japanese partners are ExxonMobil’s Baytown Complex as a blue ammonia source (JERA, Mitsubishi Corp, Idemitsu); a hydrogen plant by MVCE Gulf Coast (ENEOS); as well as blue ammonia facilities planned by CF Industries (Mitsui, JERA) and Yara (JERA).

- Outside of the U.S., other attractive regions might include Australia, Argus said.

- Last year, green hydrogen costs rose faster than blue hydrogen, widening an already large cost gap between the two. The gap widened to as much as five times that of the delta between blue and grey. Still, global investments into capacity based on Final Investment Decisions are evenly split between blue and green.

TAKEAWAY: Last year, the U.S. Gulf became the lowest-priced blue ammonia delivery region in the world, according to S&P Global. Prices dropped to the $470s/ metric ton of blue ammonia in late spring / summer. The U.S. enjoys the same advantage in blue and green hydrogen, according to Argus. How long the U.S. can remain at the forefront will depend in part on subsidies in producer countries. Australia is moving towards establishing an incentive to producers of green hydrogen that would offer $2/ kg for a decade from as soon as 2027. As Australia looks to solidify its position, that of the U.S. is seen in the short-term as more uncertain due the incoming Trump administration. Meanwhile, production from India, the Middle East, and a couple of other regions is flying under the radar, but is likely to vie for attention in Japan’s CfD auctions.

Japan-backed eFuel startup Infinium secures more funding

(Company statement, Jan 16)

- California-based startup Infinium completed the purchase of gas conversion firm Greyrock Technology alongside the first tranche of its Series C Preferred Stock fundraise, led by Brookfield Asset Management.

- New investors include Japan Hydrogen Fund, Mitsubishi Corp, and Japanese state-backed resources firm JOGMEC, joining major backers like Amazon, SK, and NextEra Energy Resources.

- The funding will support Infinium’s eFuels project pipeline and market expansion; its Pathfinder facility in North America already supplies ultra-low carbon eFuels to U.S. and European customers.

- CONTEXT: eFuels are synthetic fuels that can be utilized in existing combustion engines. They aim to reduce lifecycle GHG emissions by over 90% because eFuels are made with recycled CO2 and clean hydrogen. Such fuels are already used in the U.S. by firms such as Amazon and American Airlines.

TAKEAWAY: This seems to be the first publicly announced investment for the $400 million Japan Hydrogen Fund, which was created last year by mostly private Japanese firms to assist the The Japan Hydrogen Association developing a supply chain for the hydrogen sector. TotalEnergies was the only initial non-Japanese investor, joining Toyota Motor, Iwatani, Sumitomo Mitsui Banking Corp, MUFG Bank, Tokyo Century, Bank of Fukuoka, and the MoE-backed state corporation, the Japan Green Investment Corp. for Carbon Neutrality. Private equity fund Advantage Partners manages the fund. It’s interesting that the Fund’s first money is going into eFuels – a topic that no doubt delights manufacturers like Toyota Motor that do not believe that all future transport will be electrified

Nagano Pref advances green and white hydrogen

(Nikkei, Jan 16)

- A demo plant using artificial photosynthesis developed by Nobel Prize nominee Professor Kazunari Domen will be built in Nagano’s Iida City. It uses sunlight and photocatalysts to produce hydrogen without CO2 emissions, scaling up from a prior experiment that generated 1,300 liters of hydrogen daily on a 100 m² system.

- The new plant, covering 3,000 m² and to be the world’s largest, launches in 2026. Hydrogen produced will fuel buses and other regional applications.

- CONTEXT: Nagano (specifically Hakuba Village) is home to Japan’s only confirmed source of natural hydrogen. Found in the Hakuba Happo Onsen hot springs, this “white hydrogen” is believed to form continuously underground via rock and geothermal water reactions, offering a potentially ongoing, low-cost energy resource.

Sojitz invests more in Hycamite, turquoise hydrogen company in Finland

(Company statement, Jan 9)

- Hycamite TCD Technologies, a Finnish startup specializing in methane decomposition for “Turquoise Hydrogen,” raised €44 million.

- Sojitz led the investment, becoming Hycamite’s largest shareholder, alongside MOL PLUS, Mitsui O.S.K. Lines’ venture capital arm.

- Sojitz will accelerate projects using this technology in Japan and overseas.

- Hycamite’s process pyrolyzes methane at low temperatures, producing hydrogen and solid carbon. This method reduces CO2 emissions compared to conventional hydrogen production and leverages natural gas as a resource-efficient feedstock.

- The funds will support Hycamite’s demo plant in Finland that’s set to produce 2,000 tons of turquoise hydrogen annually (2,880 Nm³/h), one of Europe’s largest.

- CONTEXT: Hydrogen produced by thermal decomposition of methane is called “turquoise hydrogen”; “green hydrogen” produced by the electrolysis of water.

Mitsui & Co. and Itochu invest billions in ammonia supply

(Nikkei, Jan 15)

- CONTEXT: This is a wrap of already publicized projects and ongoing activities.

- Mitsui & Co, together with Mitsui Chemicals, IHI, and others, is spearheading projects to build ammonia storage facilities in Osaka, Hokkaido, and Fukushima.

- These facilities are set to be operational by FY2030, with investments estimated in the tens of billions of yen per site. Itochu is pursuing a similar project in Kitakyushu, focusing on importing and distributing ammonia.

- By 2027, Mitsui & Co plans to produce 2 million tons of ammonia annually in the UAE and the U.S., with exports directed to Japan.

- Mitsubishi Corp and Idemitsu Kosan will repurpose existing LPG storage facilities in Ehime and Yamaguchi Pref to create cost-effective ammonia receiving bases.

Itochu invests in UK green hydrogen startup

(Company statement, Jan 10)

- Itochu will invest in Protium Green Solutions, a green hydrogen production and supply company in the UK that provides advice on local production and consumption.

- Since March 2023, Protium has been supplying green hydrogen to UK companies in the industrial and transport sectors.

- CONTEXT: In the UK, large-scale support for domestic environmental projects, including green hydrogen, will be implemented through 2029. Itochu seeks access to Protium’s knowledge and expertise of hydrogen solutions.

- SIDE DEVELOPMENT:

- Mitsui invests in UK green hydrogen startup

- (Company statement, Jan 10)

- In tandem with Itochu, Mitsui has also acquired a stake in Protium Green Solutions.

JERA invests in new tech for hydrogen production

(Company statement, Jan 9)

- JERA invested about $2 million in Advanced Ionics, a U.S. firm developing a new class of water-vapor electrolyzer tech that produces hydrogen from water using electricity and thermal energy.

- The tech uses low-cost materials and harvests heat in the range of 100–650°C, a range no other electrolyzer covers.

- This tech could significantly reduce the power and cost needed to produce hydrogen.

NEWS: SOLAR AND BATTERIES

TEPCO PG partners with Endeavour Energy to expand distributed energy resources

(Company statement, Jan 15)

- TEPCO Power Grid, which manages power grids around the Kanto region, has partnered with Endeavour Energy, a major Australian distributor, to expand the introduction of distributed energy resources.

- In eastern Australia, where Endeavour Energy operates its distribution network, there has been an increase in small-scale clean energy sources, such as solar power, which has raised challenges related to regional supply-demand balancing.

- CONTEXT: Small-scale solar power systems and household storage batteries installed near electricity consumption areas are collectively referred to as distributed energy resources.

TAKEAWAY: The decentralization of energy resources is expanding in Japan, particularly as a way to create power supply in times of natural disaster and on remote islands. TEPCO aims to leverage Endeavour Energy’s expertise to facilitate its further adoption in Japan. Other domestic utility firms, such as KEPCO and Chubu Electric, are also investing in distributed energy tech, microgrids, and renewable projects to strengthen local energy resilience.

Chubu Electric Miraiz, KEPCO, etc to promote PSC

(Company statement, Jan 15)

- Chubu Electric Miraiz, Aisin, and KEPCO proposed the “Perovskite Solar Cell Deployment Expansion Project” to Aichi Pref’s Carbon Neutral Strategy Council.

- Aichi plans to launch its own perovskite solar cell promotion council in spring. Its goal is to scale PSC regionally and encourage investment by PSC producers and power firms, positioning Aichi as a leader in this tech.

- CONTEXT: With national policy on PSC now in place, it’s the turn of the local and regional governments to create the practical frameworks to accommodate projects.

JR East signs off-site PPA for solar power from JERA

(Company statement, Jan 16)

- JERA agreed with JR East to use an off-site corporate PPA for 2 MW of solar power to supply JR East Group’s commercial facilities (Oimachi, Lumine Yokohama).

- The plan involves JERA Cross acting as an aggregator to bundle the 42 existing solar power plants owned by JERA in the Kanto region, and then JR East Trading, a retail electricity provider, supplying electricity to the two commercial facilities.

- SIDE DEVELOPMENT:

- JR East aims to cut emissions on bullet trains

- (Company statement, Jan 15)

- JR East will begin operating its Akita and Yamagata bullet trains on renewable energy in partnership with Tohoku Electric.

- The power will be generated at a solar plant dedicated to JR East and supplied through Tohoku Electric’s grid.

JERA and furniture retailer to mull joint solar power development

(Company statement, Denki Shimbun, Jan 10)

- JERA and its subsidiary JERA Cross may jointly develop 60 MW of solar power by 2030 with Ryohin Keikaku, operator of the “MUJI” retail brand, via virtual power purchase agreements (VPPAs).

- The initial phase would see ¥3.6 billion invested in the next year to develop 12 MW of solar capacity, providing Ryohin Keikaku with environmental value credits.

- The collaboration aligns with Ryohin Keikaku’s target to achieve 100% renewable energy for its stores by 2030 as part of its 2050 carbon neutrality goals.

- JERA will offer expertise in solar power development and maintenance, while JERA Cross will supply the environmental value of the generated electricity.

PXP is developing lightweight, flexible solar panels for greenhouses

(Company statement, Jan 16)

- PXP, a green tech startup based in Sagamihara, Kanagawa Pref, is developing lightweight, flexible solar panels designed for installation on greenhouses.

- PXP estimates that facility-based solar farming could provide over 10 GW of renewable energy.

- CONTEXT: Due to Japan’s high solar density new applications beyond open fields and rooftops are needed. Greenhouses can host solar panels without harming crops and often have temperature control systems for on-site power use.

SOMPO group firm offers service to prevent theft of copper cable

(Company statement, Jan 16)

- SOMPO Risk Management, a subsidiary of one of Japan’s largest insurance agencies SOMPO Holdings, is set to launch a new service offering theft prevention advice for businesses operating solar power plants.

- Employees from SOMPO Risk Management will visit power plant sites to examine factors such as location, surveillance camera placement, and equipment conditions. They will identify areas at risk of theft and propose countermeasures.

- CONTEXT: Copper cables are used to connect solar panels; along with control systems, power reception equipment, and storage batteries, they are targeted for theft due to the high resale value of copper. According to the National Police Agency, 4,161 thefts were reported in the first half of 2024. At this pace, the annual total would exceed 1.5 times the 5,361 cases recorded in 2023.

NEWS: WIND POWER AND OTHER RENEWABLES

KEPCO, RWE plan 600 MW wind farm off the coast of Hokkaido

(Company statement, Jan 14)

- KEPCO and RWE Renewables Japan, a subsidiary of Germany’s RWE, plan to build a wind farm off the coast of Shimamaki Village, west Hokkaido Pref.

- The firms submitted a draft environmental impact statement to METI and the Hokkaido govt. The draft is available for viewing until Feb 14.

- The project, with a maximum capacity of 600 MW, would use up to 43 wind turbines. Fixed-bottom foundations are being considered.

- SIDE DEVELOPMENT:

- Invenergy plans wind farm in Hokkaido

- (Company statement, Jan 19)

- Invenergy plans to develop a 140 MW onshore wind farm in Shimamaki Village, Hokkaido, through its subsidiary, Shimamaki Wind Joint Venture.

- The project will have up to 33 wind turbines (4.2 MW to 6.1 MW each). Construction is scheduled to begin in early 2031; operations in late 2035.

- CONTEXT: Other firms such as Cosmo Eco Power also plan similar projects nearby. Hokkaido is becoming a key hub for wind power development – both onshore and offshore – due to its large open spaces, strong and consistent winds, and relatively low population density. METI supports grid enhancement in the region due to Hokkaido’s frail electricity transmission system.

Windpal completes Japan’s first CPT survey with Ammonite system

(Company statement, Jan 14)

- Windpal completed Japan’s first Cone Penetration Testing (CPT) survey using the Ammonite system at Akita Port.

- Windpal is a Japan-based consortium of European companies providing integrated solutions for offshore wind project developers in Asia.

- Ammonite is a crawling seabed CPT system for offshore wind geotechnical surveys. It was introduced to the Asian market in summer 2024 by Seafloor Geotech.

- The system can work in harsh conditions and eliminates complications with collection of data in shallow waters and deep sea locations for floating wind projects.

- CONTEXT: The government has set targets to develop 30-45 GW of offshore wind capacity by 2040. Policies supporting this include designated promotion zones, streamlined permitting processes, and subsidies to attract investment. Key areas like Akita, Aomori, and Hokkaido are focal points for large-scale offshore wind projects, leveraging Japan’s coastal geography.

TAKEAWAY: The quality of seabed surveys and other kinds of geotechnical surveys in Japan has been questioned by some industry players. Rushed and inaccurate surveys were cited as a reason for cost blowouts for at least one of the Mitsubishi Corp-led offshore wind projects. As Japan’s offshore wind sector adds scale, however, more specialist firms from Europe and elsewhere are entering the market to offer services. Seafloor exploration in Japanese waters is a sensitive area due to national security issues. Still, the government may be keen to support projects like Windpal’s to help reign in costs within the offshore wind sector.

Sumitomo inks loan for expansion of Indonesian geothermal project

(Company statement, Jan 14)

- Sumitomo is participating in the Supreme Energy Muara Laboh (SEML) geothermal power project in West Sumatra, Indonesia through a JV with INPEX and PT Supreme Energy, an Indonesian private power project developer.

- SEML inked loan agreements with a syndicate of banks for international cooperation for the project’s expansion.

- The syndicate comprises JBIC, the Asian Development Bank, Mizuho Bank, Sumitomo Mitsui Banking Corp, MUFG Bank, and the Hyakugo Bank.

- Total project costs will be about ¥70 billion.

- In this expansion, a second unit will be built on a site adjacent to the existing unit in operation since Dec 2019. The generating capacity will increase to around 170 MW.

- The main equipment such as the geothermal steam turbine and generator will be supplied by Fuji Electric.

NEWS: NUCLEAR ENERGY

KEPCO long-term management plan approved for Takahama NPP

(Company statement, Jan 17)

- KEPCO received NRA approval for the long-term facility management plan of Takahama NPP Units 3 and 4. The plan outlines measures for maintaining the NPP’s safety and reliability.

- CONTEXT: A long-term facility management plan must be approved by the NRA when a NPP operates beyond 30 years. This includes conducting technical evaluations of equipment degradation every 10 years.

- The plan covers the operational period from June 6, 2025, to Jan 16, 2035, for Unit 3; and until June 4, 2035, for Unit 4.

Tohoku Electric to do geological survey for Onagawa NPP

(Company statement, Jan 16)

- Tohoku Electric will make a geological survey around the reactor building of Onagawa NPP Unit 3, as part of compliance with new regulatory standards.

- This includes borehole drilling to clarify fault characteristics and geological structure around the reactor building. The work begins next week and will last two years.

- CONTEXT: Onagawa NPP stopped operation following the 2011 earthquake. Unit 2 resumed commercial operation in December 2024.

TAKEAWAY: Attention is now focused on the potential restart of Higashidori NPP Unit 1 and Onagawa Unit 3. Still, there is a long way to go before the units can restart. The company said it’s not considering submitting an application for review or restart within the next two years.

Communication device malfunction at Kashiwazaki-Kariwa NPP

(Nikkei, Jan 14)

- A communication device used for emergency contact malfunctioned at TEPCO’s Kashiwazaki-Kariwa NPP, causing Unit 7 to deviate from the ”operational limits stipulated by safety regulations”.

- The plant’s operations were not affected. Since Unit 7 already contains nuclear fuel, it must follow safety regulations.

Kokubu Group and TEPCO to partner on Fukushima products promotion

(Company statement, Jan 17)

- TEPCO and Kokubu Group agreed to promote the distribution of Fukushima products to support market expansion, increase consumption and assist local businesses.

- CONTEXT: TEPCO has to mitigate reputational damage to Fukushima products since the March 2011 accident. Efforts included establishing a “Fukushima Distribution Promotion Office”. Also, they formed a dedicated team in 2023 to address issues related to ALPS-treated water discharge.

TAKEAWAY: This marks a significant step toward rebuilding local trust, as it’s the first collaboration of its kind. Also, compensation to fishery businesses and others who suffered damage to their reputations as a result of the release of treated water have totaled ¥52 billion.

NEWS: TRADITIONAL FUELS

MOL and JERA sign long-term deal for new LNG carrier

(Company statement, Jan 15)

- Mitsui O.S.K. Lines (MOL) signed its eighth long-term charter contract with JERA for a new LNG carrier. Samsung Heavy Industries in South Korea will be the builder.

- Delivery is set for 2026. The vessel will have a 174,000m³ membrane tank. MOL will manage it to transport LNG for JERA.

TAKEAWAY: Japan is expanding its LNG fleet. This agreement by MOL and JERA, underscores a race to dominate the global LNG shipping market amidst rising demand. Japan has over 30% of the global LNG carrier share. It is leveraging its import energy dependence to secure an unshakable position in the low-carbon energy transition. Still, this expansion is a bold bet on LNG’s longevity in a decarbonizing world, locking Japanese firms into fossil fuel infrastructure for at least the next two decades or so.

INPEX wins oil and gas licenses in Norway

(Company statement, Jan 15)

- INPEX Idemitsu Norge AS (IIN), participated in Norway’s 2024 Awards in Predefined Areas (APA) round. IIN secured exploration licenses for eight areas in the northern North Sea and the northern Norwegian Sea.

- Two of these licenses, PL 1263 and PL 1264, were acquired with IIN as the operator, increasing its total operator licenses to three. The APA round promotes further exploration in areas with previous exploration activities. Applicants can bid on open blocks within predefined areas.

- CONTEXT: This acquisition brings INPEX’s licenses in Norway to 44. IIN holds many licenses in the North Sea, Norwegian Sea, and Barents Sea, with production from fields such as Snorre and Fram. The region has many areas where CO2 can be stored, such as depleted gas fields. INPEX invested in Europe’s first CCS project in Norway in 2024.

LNG stocks up 12.8% from previous week, down 1.9% YoY

(Government data, Jan 15)

- As of Jan 12, the LNG stocks of 10 power utilities were 2.11 Mt, up 12.8% from the previous week (1.87 Mt), but down 1.9% from end January 2024 (2.15 Mt), and 7.7% up from the 5-year average of 1.96 Mt.

- CONTEXT: Temperatures have been fluctuating significantly between warm and cold, which in turn has made energy consumption erratic and difficult to predict. Spot purchases are expected to increase.

NEWS: CARBON CAPTURE & SYNTHETIC FUELS

Kanadevia and AIST develop innovative catalyst for LPG synthesis

(Company statement, Jan 14)

- Kanadevia, with the National Institute of Advanced Industrial Science and Technology (AIST), developed a catalyst and process to synthesize LPG from CO2 under low-pressure conditions (below 1 MPa).

- They use green hydrogen and CO2 from industrial emissions, passed through the catalyst, to produce green LPG.

- A demo plant capable of producing 3–4 tons of LPG a year will be operational by spring 2025, with a year-long trial planned.

- CONTEXT: This innovation builds on Kanadevia’s expertise in CO2-to-methane (e-methane) synthesis. The green LPG market in Japan is projected to grow to 2 million tons by 2035 and 8 million tons by 2050. The project stems from a collaboration established in April 2023.

Cosmo Oil-led group completes SAF production plant

(Company statement, Jan 10)

- Construction is completed on the SAF production plant at Cosmo Oil’s Sakai Refinery in Sakai City, Osaka Pref.

- Cosmo Oil, engineering firm JGC, REVO International, an operator of fuel development businesses, and their JV firm SAFFAIRE SKY ENERGY, aim to establish large-scale domestic production of SAF, the first of its kind in Japan.

- The firms will utilize 100% used cooking oil (UCO) as the raw material. They plan to supply around 30,000 kL of SAF/ year through this facility.

- CONTEXT: The facility was built as a subsidized project approved by NEDO. JGC oversees the construction of the supply chain; Revo International manages raw material procurement; SAFFAIRE SKY ENERGY handles SAF production. The Cosmo Energy Group is responsible for manufacturing aviation fuel by blending the SAF with traditional fossil-based fuels and sales.

TOA and Sanwa Energy eye production of biodiesel from UCO

(Company statement, Jan 14)

- General contractor Toa and Sanwa Energy launched a study for biodiesel fuel production and distribution in the Yokohama area, with a supply network across Tokyo Bay by FY2026 and a monthly production capacity of 500–600 kL.

- The biodiesel fuel will be made from used cooking oil, Fatty Acid Methyl Ester, or FAME, made by methyl esterification. FAME can be used as a substitute for light and heavy oil in existing diesel engines, either as is or with minor modifications.

- CONTEXT: The current supply infrastructure for alternative fuels, particularly for ships, is considered inadequate, posing challenges to CO2 reduction efforts.

- SIDE DEVELOPMENT:

- Seven-eleven Japan, ENEOS, etc to reuse UCO as BDF and SAF

- (Company statement, Jan 15)

- Chiba Pref launched a pilot to collect used cooking oil, initially refining it into biodiesel fuel (BDF) and potentially using it for sustainable aviation fuel (SAF).

- As part of the initiative, a group of seven firms is set to collect UCO for reuse in biodiesel fuel. The group comprises store chain Seven-Eleven Japan, ENEOS, Mitsui Fudosan Residential, Sumitomo Mitsui Banking Corp, etc.

- CONTEXT: ENEOS plans to start SAF production in 2027.

Suzuki Motor to use cow feces for biogas fuel in India

(Company statement, Dec 25)

- Suzuki Motor seeks to produce biogas fuel for automobiles using cow feces in India.

- Suzuki inked an investment agreement with NDDB Mrida, a subsidiary of India’s National Dairy Development Board (NDDB).

- Suzuki plans to collaborate with dairy cooperatives nationwide through NDDB Mrida to establish and manage its biogas plants.

BY FILIPPO PEDRETTI

Among Global Uncertainties, Japan Still Sees Key Role for

LNG in Energy Security

Hoping to boost both domestic energy security and cement its role as a leading LNG trading hub, especially for Southeast Asia, Japan continues to diversify its source of suppliers across the globe for the super-chilled fuel. The country has also launched its own strategic LNG reserve to cover any emergency or rapid surge in demand.

Casting a wide net for diversified oil and gas sources has long been a cornerstone of Japan’s energy policy. In 2024 alone, LNG arrived from 20 countries. This trend of risk-hedging supply through diversity is expected to continue and is a clear statement that the government still sees a key role for fossil-fuel generation at home and abroad.

In recent decades, Japan has been one of the world’s leading importers of LNG, and volumes jumped even further in the wake of the March 2011 Fukushima disaster. When the nation’s entire fleet of nuclear reactors was idled soon after, LNG (and coal) filled the gap.

In recent years, however, factors such as economic stagnation, nuclear plant restarts, market liberalization, and the installation of more renewables capacity have led to a decline in Japan’s LNG demand.

For key LNG suppliers to Japan – Australia, the Middle East, the U.S. and Russia – the market remains highly attractive even if today China has become the world’s top importer. The Japanese government’s recent energy strategy draft assured its support for the chilled gas as a stable power generation fuel amid an energy transition and global market turmoil. But does that marry with the strategy of Japanese LNG buyers?

Giving birth to the Strategic Buffer

While Japan today relies on LNG for around 29% of its power generation, overall demand has been decreasing steadily since 2015, when imports totaled 85 million tons. Consumption has dropped about 23%, from 88 million tons in 2014 to 68 million tons in 2022. Despite this decline, the utilization rate of regasification facilities has increased, rising from 35% in 2020 to 37% in 2021.

In 2021, METI calculated that LNG was the cheapest form of energy in the national energy mix. However, LNG has since lost this primacy due to added CO2-reduction related costs. In the latest Basic Energy Plan, the share of LNG in the country’s energy mix for 2040 isn’t clearly specified (for 2030 it’s forecast at 20%), with overall thermal power targeted for 40%.

LNG optimists will see this as METI giving the LNG sector carte blanche to eat into coal’s market share. Skeptics note that the 2030 forecast market share for coal and LNG is largely unchanged from the 40% “thermal” benchmark for 2040. But either way, with power demand in Japan also forecast to grow through 2040 thanks to tech demand, a return to LNG import volume growth is on the cards.

If METI forecasts are accurate, they will reverse a multi-year slump in LNG purchases, with 2023’s volumes down 8.1% over 2022 to 66.15 million tons.

Hedging the bets

The problem for buyers is that following forecasts that turn out to be wrong is costly, especially when a single LNG cargo can easily be a couple of hundred million USD. Overstocking is also not an option from the buyers’ side: LNG can’t be held long in long-term storage, unlike oil; it evaporates.

Typically, Japan has two power demand peaks – summer and winter. Preparing for the demand peaks is complicated by the fact that Japan has limited LNG storage capacity of around 12 billion cubic meters at its 31 LNG receiving terminals – about a month of consumption. That’s not much, but with buyers keen to avoid being left with excess fuel on their hands, METI has proposed financial support for securing extra storage tanks in order to boost storage capacity.

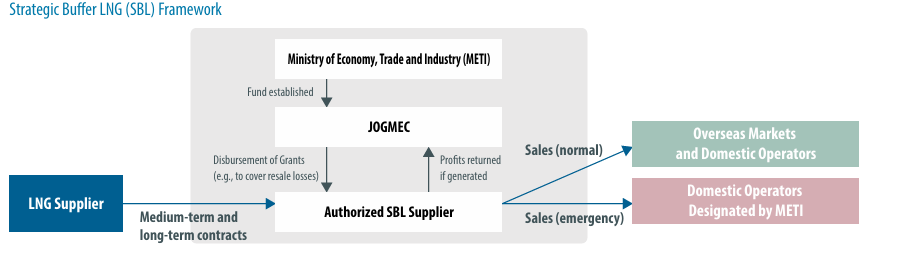

Thus, METI launched the Strategic Buffer in December 2023 to provide a reliable reserve of LNG in case of emergencies at home and in the region, as well as to cover peak demand periods. Originally, it entailed at least one LNG cargo (about 70,000 metric tons) available for each month over the winter months.

Under the scheme, Japanese firms ink contracts with LNG suppliers, selling it overseas or domestically during normal conditions. During crises, METI directs the strategic reserve to supply domestic firms. A JOGMEC fund covers losses from emergency sales, while retaining profits (if any).

SBL Framework. Source: JERA, ANRE

Expanding the Strategic Buffer

Even when the idea was first conceived in 2022, the SBL framework was anticipated to grow from covering only the winter months, to the whole year. In late November 2023, then METI minister Nishimura announced the approval of JERA’s plan to secure surplus supply of LNG, while also approving the SBL under the government’s Economic Security Promotion Act.

JERA, with its 20 LNG carriers and managing around 40 million metric tons of LNG per year, is Japan’s leading power generator, and became the first company tapped to manage the SBL cargoes.

In December 2023, Japanese utilities, led by JERA, called for an enlarged SBL. While fuel inventories were reported to be sufficient (METI reported 2.33 million metric tons for electric utilities and 2.4 million tons for city gas suppliers), they still claimed that a bigger SBL was needed to ensure resilience against potential supply disruptions.

In October 2024, the government announced expanding the program fourfold in the latter half of 2020s, seeking to store at least 840,000 metric tons of LNG a year, to address both winter and summer demand peaks. The need also stemmed from uncertainties over nuclear power capacity, as well as reducing dependence on coal and oil.

Diversifying LNG suppliers

With concerns over energy supply disruptions, Japan is also reshaping its global partnerships as more supply comes to market, seeking greater diversification of LNG source by geography, as well as contract terms.

Japan remains highly dependent on far-flung allies for supplies, such as Australia, the U.S. and Qatar. Unfortunately for Japan, relations are tense with its closest neighbor, Russia, which supplies just under 10% of the LNG imports. While Russian volumes trail that of those from allies, transportation costs and time are obviously much smaller due to proximity of the Sakhalin-2 project to Japan.

Nevertheless, relations with Australia and the U.S. have been clouded by pressure from those keen to quickly phase out all fossil fuels production, even the volumes slated for export. Of course, with Donald Trump entering the White House, the American natural gas spigot promises to flow generously.

As far as Qatar, the relationship continues to be marred by a long-standing disagreement over “destination clauses” that Qatar insists on, and which prevents Japanese buyers from reselling the natural gas to regional partners.

The Persian Gulf country has been a reliable supplier of LNG to Japan for decades, also providing emergency shipments following the 2011 Great East Japan Earthquake. Yet, imports from Qatar fell to 4% in 2022 from 12% in 2021, following the expiry of over 7 million metric tons per year of Qatargas 1 contracts.

At the end of 2024, Qatar held talks in Tokyo with Japanese energy companies including JERA, Chubu Electric, Kansai Electric, Tohoku Electric, Mitsui, Marubeni, and shipping firms Mitsui O.S.K. Lines, NYK Line, and “K” Line. Japan’s contracts for Qatari LNG, such as JERA’s 700,000 million metric tons per year are set to expire in 2028 and Kansai Electric’s 500,000 million metric tons per year in 2027. Still, cooperation between the countries continues, for example through Japan’s support for Qatar’s North Field expansion project.

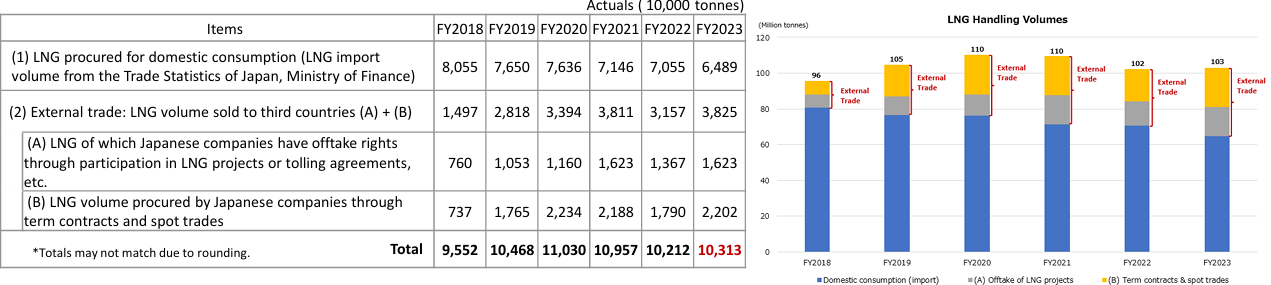

LNG handling volumes for FY2024, JOGMEC’s survey results. Source: JOGMEC

From importer to trader

Even though domestic LNG demand is declining, Japan remains an active international LNG trader, with state-owned entities like the Japan Bank for International Cooperation (JBIC) and Nippon Export and Investment Insurance (NEXI) providing financial support for LNG supply and trade.

Judging by JOGMEC data, one could argue that Japan’s LNG strategy is more focused on business expansion outside the country than securing the fuel for domestic use. While LNG procured for domestic consumption stood at a little over 80 million tons in 2018, by 2023 it had fallen to around 65 million tons. LNG volumes linked to external trade grew from 14 million tons to 38 million tons in the same time frame as firms like Kansai Electric, JERA, and others either opened or expanded a Singapore office dedicated to LNG trading.

Within this context, the SBL can also be considered as a way for the government to take on the responsibility of prioritizing domestic supplies in case of emergencies on behalf of the rather overseas-oriented private sector.

Officially, Japan considers LNG as a transition energy source, eventually to be substituted by ammonia and hydrogen. But the lack of a clear roadmap to phase out fossil fuel is criticized by environmentalists who question how Japan can meet net zero emissions goals by 2050 if this ongoing support for LNG purchases continues.

It’s no secret that many top METI bureaucrats still believe that LNG is the most reliable and cost-effective energy source, and feel indebted to the global LNG community for coming to Japan’s aid in the aftermath of 2011. For the LNG sector to prosper and grow, however, it has to take market share from plants that run on coal while keeping at bay fossil-fuel critics and persuading other Asian nations to embark on coal-to-gas switching.

One way or another, LNG continues to enjoy ample support in Japan’s public and private sector, which suggests that its central role in the national energy mix is here to stay.

ANALYSIS

BY JOHN VAROLI

Japan Must Tame Wind Power Costs; Data May Use 10% of

All Power by 2030: Yergin

Daniel Yergin is a name synonymous with energy expertise. A Pulitzer Prize-winning author and vice chairman of S&P Global, Yergin has spent decades mapping the intricate interplay between energy, geopolitics, and the global economy. His seminal works, including The Prize and The New Map, have become essential reading for policymakers and industry leaders navigating an era of energy transition and geopolitical upheaval. With his signature ability to distill complex dynamics into clear insights, Yergin has earned a reputation as one of the foremost voices in energy analysis.

On Jan 13, in Washington DC, Yergin met with a small audience to share his perspectives on the shifting sands of energy security, the role of renewables in decarbonization, and the implications of new alliances and rivalries shaping the global energy landscape. He talked about Japan, Trump, and how Big Tech will determine the future of energy.

Daniel Yergin Q&A at the Atlantic Council in Washington DC on January 13

How has the global energy landscape changed since The Prize was written?

It was striking for me to see what I call the ‘enduring lessons’ of The Prize, and also to see what it didn’t cover. We can go through the lessons that stand out and the two things that really were not in the book – one is the importance of energy security, which is so strong [today]. Secondly, energy is fundamentally now a strategic commodity. Third, there’s the element of innovation and constant change in technology. And one more thing, there are hundreds of characters in The Prize, but there are only two characters that matter – one is called Supply and the other is Demand. You see that over and over again. I was kind of struck going back and reading about gasoline prices. The [government] hearings that took place in the 1920s sounded as if they could have been taking place in the 21st century. There is a failure to recognize that Supply and Demand, and not machinations, determine market price.

Two big things left out – 1) China. It was striking to me that China hardly appeared in the book then, at that time China was a tiny oil exporter, sending oil to Japan to pay for imports in its first stage of industrialization. And though I mentioned that climate was going to be a big issue, even though I mentioned this, it really doesn’t figure prominently in the book.

As we look ahead, what does the new U.S. leadership need to focus on?

It’s going to be a dramatic change in terms of policy. There’ll be a reversion to the first Trump administration but in a more thoughtful and experienced way. For all countries and the IEA it will be a process of rethinking. I am puzzled about Europe – you are starting to see the shift in the politics and a move toward the right. You are seeing a “greenlash” against climate policies. And European policy makers will have to think more about deindustrialization and competitiveness. Climate policies don’t exist in a vacuum and you have to look at the big picture.

What are your primary advice and counsel to the Trump administration?

Top of the agenda is permitting. On average, globally it takes 20 years to get a mine going, but in the U.S. it takes 29 years. We need to rationalize the permitting process and that will be at the top of the agenda to get things done. And that goes for everything in the energy sector.

As far as LNG – what struck me is the scale of LNG now in the U.S…. The first exports only began in 2016. This is a very significant new export industry for the U.S. Very important. U.S. energy exports have been one of the sources to building better relationships [globally]. This gives the U.S. and any future administrations a strategic advantage in the global arena.

Trump has an energy dominance goal – how would you advise Trump on the energy transition?

It’s pretty clear that Trump is going to focus on energy in general, and he’s going to again withdraw from the Paris Agreement. This will throw climate negotiations into a period of uncertainty. The Europeans are uncertain what to expect from Trump and his use of tariffs for a whole host of things.

Competition between the U.S. and China – are there ways to find success on both sides of the Pacific?

The relationship between the U.S. and China is the great question for the rest of the 21st century. We are more integrated economically than people realize. But there’s also competition on AI, chips and militarily. There’s competition on critical raw materials; in 2019, this wasn’t even on the agenda. People weren’t thinking about critical raw materials then. But then people started to look at the amount of minerals needed for the energy transition. An EV uses 2.5 times more copper than a conventional car, and then you add those numbers up, and you look at who is doing the mining – there’s a global competition now for mining. Brazil certainly is oriented towards China with its exports of raw materials. China is important for Latin American economies in a way that we [the U.S.], as a country, haven’t focused on.

And these requirements of the energy transition and economic growth will become more urgent with the new administration. The Chinese have built up formidable positions, in a concentrated way. There is the issue of ports. The U.S. doesn’t have an international port company like China does. We are seeing a return to the Great Power competition.

As far as costs, I’ve heard from a few Asian companies, who said that they can build a solar panel plant in the U.S. but it will cost them six times as much. One was a Chinese company and the other Korean. So how do you balance costs? This is not simple.

Does the EU need to rethink the energy transition?

We hear the phrase over and over again that we need “More Ambition”. But there’s a need to rethink the energy transition for a host of reasons. A lot of the thinking of the transition congealed during Covid when demand was down, energy prices were down. And now we’ve had a couple of years of experience. In 2023, wind and solar were at their highest levels ever, but so were oil and coal, and there’s a message there that needs to be thought about.

The Prime Minister of Malaysia said that his country will address climate but not according to what Europe and America told them, because he has to worry about economic growth and development and poverty issues. I think that the North-South divide is coming to the fore.

Economics of the energy transition – What are your expectations in terms of driving down the costs of these technologies.

We’ve certainly seen solar costs down 90%; that’s true. Wind costs have come down substantially, but for Japan trying to do offshore wind, those costs are high. The supply chain problems have really driven up costs, and we see that in offshore wind in the U.S., where the matter is facing rethinking. The supply chain issues for offshore wind are very significant. Of all the countries it was Japan that’s long been focused on energy security. Now since the war in Ukraine this issue has become clear to everyone.

How will the surge in demand by AI impact the energy landscape?

Our numbers indicate that within five years, between 7 to 10% of U.S. power demand could just be coming from data centers. For decades, we’ve had very slow growth in energy demand, but now you take data centers, EVs, reshoring of manufacturing, and now that sharp growth is there, and it is really changing the landscape. Suddenly the Big Tech companies are big players in the energy sector because they are worried about reliable energy supplies. They are driving the new interest in nuclear power. Yet, Big Tech seems divided – those who think renewables can handle the rising demand; while others look to nuclear, but that’s not coming online until the 2030s; and yet others think natural gas will do the job, demand for which is surging. I think that natural gas will meet this demand.

Also, the retirement of existing coal plants will slow down, because reliability is the most important thing in terms of electricity supply.

ASIA ENERGY REVIEW

BY JOHN VAROLI

This column provides a brief overview of the region’s main energy events from the past week

Australia / Nuclear power

Grace Stanke, Miss America 2023, was hired to bolster public approval of nuclear power in Australia. Ms Stanke works for Constellation Energy, which operates the largest fleet of reactors in the U.S. Through public speaking tours and social media, she tries to make nuclear power more acceptable and addresses concerns about safety.

China / Power transmission

In the first 11 months of 2024, spending on power transmission rose 19% to 529 billion yuan ($72 billion), said the National Energy Administration. This year, State Grid Corp of China, the nation’s largest operator, promised to boost spending, as well as China Southern Power Grid, the other major operator.

China / Solar power

China plans to build a 1 km wide solar power station in space that will beam energy back to Earth via microwaves. If completed, the new project would be akin to moving the Three Gorges Dam to a geostationary orbit 36,000 km above the Earth.

India / Power demand

By 2035, one-third of power demand growth is expected to belong to EVs and data centers, which today account for a negligible share of power demand in India. The country has a goal of 500 GW of renewable energy capacity by 2030.

Philippines / Renewable energy

Masdar, the United Arab Emirates state energy giant, inked a $15 billion renewable energy deal with the Philippines to develop solar, wind and battery energy storage systems that could total 1 GW of clean power capacity by 2030.

South Korea / Nuclear power

Nuclear power plant operator Korea Hydro & Nuclear Power and state utility Korea Electric Power Corp agreed with Westinghouse to end their intellectual property dispute.

South Korea / Oil and gas

The country plans to import more U.S. oil and gas to diversify energy sources amid tensions in the Middle East, the industry minister said. The government may need to increase support for the purchase of non-Middle East oil, he added.

Taiwan / Solar power

The Ministry of Economic Affairs said that it will reach its 20 GW target of deployed solar by late 2026. Taiwan’s solar power installation capacity currently stands at 14.22 GW, leaving about 6 GW to reach the government’s 20 GW target.

Vietnam / Energy policy

Vietnam is revising its National Power Development Plan VII, which will be submitted to the prime minister for approval by March 1.

Vietnam / LNG and oil

Russian PM Mishustin traveled to Hanoi and offered help to develop Vietnam’s nuclear power sector and provide it with crude oil and LNG. The countries also agreed to continue to facilitate oil and gas projects on each others’ continental shelves.

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Hulic Ochanomizu Bldg. 3F, 2-3-11, Surugadai, Kanda, Chiyoda-ku, Tokyo, Japan, 101-0062.