Weekly

March 31, 2025

ANALYSIS

METI PUSHES FORWARD ON SIMULTANEOUS MARKET TO BOOST RENEWABLES INTEGRATION

- To improve electricity market efficiency and create a system that can accommodate more renewables on the grid, METI is doing a review on introducing a so-called simultaneous electricity market.

- Japan NRG takes a closer look at the simultaneous market debate within the broader context of the country’s evolving electricity market reforms.

JAPAN’S ELECTRICITY COMPANIES ARE CHEAP AND GETTING CHEAPER

- Japanese firms are the cheapest electricity stocks in the G7, making them more of a target for M&A.

- This also significantly hinders their fund-raising capabilities at a time when more investment in the grid and clean energy are imperative.

ASIA PACIFIC REVIEW

This column provides a brief overview of the region’s main energy events from the past week

NEWS

- Agencies list issues around rolling out simultaneous market system

- Govt launches meeting on Watt-Bit Coordination

- Japan asset managers start to exit net-zero alliance

- JERA acquires EDF Trading’s Tokyo desk to expand in Japan’s power trading

- JERA to supply gas-fired power for data centers

- MOL, IHI, others ink MoU for green ammonia in India

- Japan’s first hydrogen co-firing demo to launch in April

- Kansai Electric to build one of Japan’s largest battery storage facilities

- ANRE: control functions of home storage batteries to support demand-response (DR)

- JR Kyushu to tackle abandoned small solar plants

WIND POWER AND OTHER RENEWABLES

- Shikoku Electric launches new hydro plant

- Kanadevia, Taisei, MOL sign deal to accelerate floating offshore wind

- Hokkaido Electric sets out timeline to restart two of the units at nuclear power plant

- NRA gives approval for long-term management plan for Takahama NPP

- JAPEX sets up oil JV in the U.S.

- Ithaca Energy acquires JAPEX UK oil subsidiary

CARBON CAPTURE & SYNTHETIC FUELS

- METI eyes competitive bidding for CCS transport and storage

- Tokyo launches local carbon credit market utilizing blockchain tech

- Japan and Brazil sign MoU on carbon credit market and climate action

EVENTS

| Mar 31 | End of Japan’s fiscal year 2024 |

| May 3-6 | May Golden Week Holidays |

| June 4-5 | Kyushu Innovation Week / Kyushu GX Decarbonization Expo @ Marine Messe Fukuoka |

| June 4-6 | AXIA EXPO 2025 (Hydrogen and Ammonia Next-Generation Energy Exhibition) @ Aichi Sky Expo |

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Editor-in-Chief)

John Varoli (Senior Editor, Americas)

Kyoko Fukuda (Japan)

Magdalena Osumi (Japan)

Filippo Pedretti (Japan)

Tim Young (Japan)

Tetsuji Tomita (Japan)

Regular Contributors

Chisaki Watanabe (Japan)

Takehiro Masutomo (Japan)

OFTEN-USED ACRONYMS

METI | The Ministry of Economy, Trade and Industry | mmbtu | Million British Thermal Units |

MoE | Ministry of Environment | mb/d | Million barrels per day |

ANRE | Agency for Natural Resources and Energy | mtoe | Million Tons of Oil Equivalent |

NEDO | New Energy and Industrial Technology Development Organization | kWh | Kilowatt hours (electricity generation volume) |

TEPCO | Tokyo Electric Power Company | FIT | Feed-in Tariff |

KEPCO | Kansai Electric Power Company | FIP | Feed-in Premium |

EPCO | Electric Power Company | SAF | Sustainable Aviation Fuel |

JCC | Japan Crude Cocktail | NPP | Nuclear power plant |

JKM | Japan Korea Market, the Platt’s LNG benchmark | JOGMEC | Japan Organization for Metals and Energy Security |

CCUS | Carbon Capture, Utilization and Storage | ||

OCCTO | Organization for Cross-regional Coordination of Transmission Operators | ||

NRA | Nuclear Regulation Authority | ||

GX | Green Transformation |

NEWS: GENERAL POLICY AND TRENDS

ANRE, OCCTO list issues to tackle to build simultaneous market system

(Government statement, March 24)

- ANRE and OCCTO experts discussed issues for creating a simultaneous market:

- For the seller side, the issues are: How to bid with self-scheduled power sources (where the plant operator determines the start of the power source by themselves); What mechanism to use when self-scheduled power source bids are restricted; How to register operating parameters; How to bid for power sources other than thermal power; and, How to operate power sources that require one week (or, at least more than one day) to bring online.

- For the buyer side, the issues are: The bid process; and bidding obligation for demand that’s linked to bilateral contracts.

- In terms of power supply security, the issue is how to respond in the event that demand differs from TSO expectations.

- Regarding methods for calculating market prices: There are questions around the price per kWh in a situation when there is grid congestion; how to determine the price per Δ (delta) kW; and How to set individual compensation for power generation costs (uplift).

- In terms of the intraday part of the simultaneous market, the issues are timing and frequency of holding the market, the settlement target, and how to change bidding content.

- For actual supply-demand, the debates are around how to set the price of balancing power per kWh and the imbalance charge.

- To introduce a simultaneous market, the roles of the operating entities will need to be clarified, and a system will need to be established to ensure that they work together.

- Next, the govt study group intends to confirm the current operations and management of JEPX, EPRX and OCCTO, paying particular attention to functions and operations utilized in market management, as well as mechanisms used for information exchange with related organizations.

TAKEAWAY: The Study Group on the Simultaneous Market is charged with finding a way to introduce such a market in Japan. The group has met 12 times since February 2023, and it published an interim report on initial findings in November 2024. For a detailed look at the Simultaneous Market discussions and implications, please see this week’s Analysis section.

Govt launches meeting on Watt-Bit Coordination

(Government statement, March 21)

- The Ministry of Internal Affairs and Communication (MIC) and METI launched a new body, known as the Public-Private Meeting on Watt-Bit Coordination. It brings together members of the power, telecom and data center (DC) industries.

- The govt wants to accelerate the digital transformation (DX) in the country through the rollout of AI, and promote coordination between the electricity and telecom sectors (the Watt-Bit Coordination) with upgraded infrastructure in order to achieve growth, decarbonization and national resilience.

- Working groups will be held and a summary will be produced in June after four monthly meetings for technical and practical discussions.

- CONTEXT: MIC and METI held “Expert Meetings on Development of Digital Infrastructure (DC, etc.)”, and published an interim report on findings in October 2024. It indicated the need for urgent measures to develop digital infrastructure. The GX2040 Vision, approved by the Cabinet in February, underscored the importance of effective coordination between electricity and telecoms to build infrastructure to achieve rapid development of data centers, which require lots of electricity.

TAKEAWAY: As ordered by PM Ishiba to both ministers at the Digital Government and Finance Reform Council on Feb 20, there is a government push to integrate the development of power and telecom infrastructure. The urgency can be seen from how quickly this initiative is moving. From a first meeting in March, the group is expected to deliver a detailed roadmap for future efforts within three months. This suggests there is already a consensus about which direction policy needs to move in to facilitate inter-sector collaboration.

ANRE resumes discussions of measures to promote biodiesel

(Government statement, March 25)

- ANRE listed key issues for introducing biodiesel, and proposed measures.

- Japan’s maximum blending ratio of Fatty Acid Methyl Ester (FAME) in diesel to create biodiesel for trucks, buses and other vehicles is currently 5% (B5). This will be increased to the same level as in Europe, 7% (B7).

- The fuel for construction machinery, etc, is also limited to B5, but following the examples of Europe and the U.S., a new JIS standard for B20 and B30 fuel exclusively for off-road use will be formulated so that it can be introduced in Japan.

- Modern-day biodiesel with HVO (Hydrotreated Vegetable Oil) has the same chemical formula as diesel fuel, but Japan has not as yet established a standard for its handling.

- Since HVO has a lower density than existing fossil-based diesel, it does not fall under the definition of ‘diesel’ for the purposes of diesel tax. So, regulations and operation of the tax on diesel will be reviewed.

- CONTEXT: There is growing momentum towards using biodiesel for construction machinery and as a marine fuel to cut emissions. In addition to demos of high blends of biodiesel, the govt is also promoting biodiesel as part of national policy. The 7th Basic Energy Plan states that biodiesel should be prioritized in transportation. However, issues such as standards and taxation have hindered its spread so far.

TAKEAWAY: As when blending bioethanol with gasoline, discussions about blending biodiesel with diesel began about 20 years ago. It has yet to become widespread due to cost, supply volumes, and product standards. In the past few years, the government has put more priority on supporting hydrogen and ammonia as low carbon fuels, but recent moves show that biofuels are back in favor.

Japan asset managers start to exit financial net-zero alliance

(Nikkei Asia, March 27)

- Tokio Marine Asset Management left the Net Zero Asset Managers initiative formed by leading financial industry players to tackle climate change.

- CONTEXT: This exit begins the outward trickle of Japanese asset management companies, following banks and insurance companies. Most U.S. banks and insurers have also quit NZAM. The world’s largest asset manager, Blackrock, left in January.

TAKEAWAY: These exits were on the cards as soon as Trump called for the U.S. to withdraw from the Paris Agreement, again. Most financial companies that have left NZAM plan to continue with climate and sustainability policies independently. NZAM’s implosion creates an opportunity for new frameworks to emerge, possibly centered on Europe.

NEWS: ELECTRICITY MARKETS

JERA acquires EDF Trading’s Tokyo desk to expand in Japan’s power trading

(Company statement, March 27)

- EDF Trading and JERA Global Markets will merge operations in Japanese power trading. JERA GM will effectively take over the Tokyo desk of EDF Trading.

- CONTEXT: EDF Trading has built up one of the biggest power trading desks in Japan. JERA GM is a JV between JERA (two-thirds owner) and EDF Trading (the rest), and focuses on trading in fuels.

- The two companies launched cooperation in 2008, when EDF Trading was a counterparty with Chubu Electric on coal procurement. (JERA is a 50-50 JV between Chubu Electric and TEPCO).

- The integration of the two trading desks takes effect from April 1, 2025. JERA GM will continue to operate out of the Coredo Nihonbashi building in Tokyo with an expanded team of over 50 staff.

TAKEAWAY: JERA is the world’s largest LNG importer, but in the last couple of years it has also tried to expand into international gas trading that’s not directly linked with the fuel needs of its power plants. JERA has a Singapore office to bolster its global LNG trading while also dipping its toes into the electricity markets at home. The addition of EDF Trading expands JERA’s resources considerably and should help make it a top player in Japan’s fast-growing power derivatives markets.

JERA seeks to supply gas-fired power for data centers

(Nikkei Business, March 27)

- JERA plans to enter the data center market by constructing gas-fired power plants near data centers, or by attracting data centers next to its existing facilities, providing rapid and stable electricity supply through on-site PPAs.

- CONTEXT: Rising demand from IT firms competing in generative AI development has accelerated the expansion of data centers. However, the volume of renewable energy in development lags behind, pushing operators to explore other ways to secure electricity. This is where generators of gas-fired power plants hope to come in, knowing that the availability of electricity from nuclear plants in Japan is limited.

- Gas-fired generation supplies 35% of Japan’s electricity, with JERA responsible for roughly 30% of the nation’s total generation. JERA operates gas-fired plants at 26 locations, mostly around urban areas.

TAKEAWAY: The lack of available power for new data centers is starting to push U.S. operators to review other options. Just a few months ago, ExxonMobil said it will design large (1.5 GW or more) gas-fired power plants specifically to serve data centers in the U.S. JERA seems to be the first Japanese company to test interest for similar applications here.

- SIDE DEVELOPMENT:

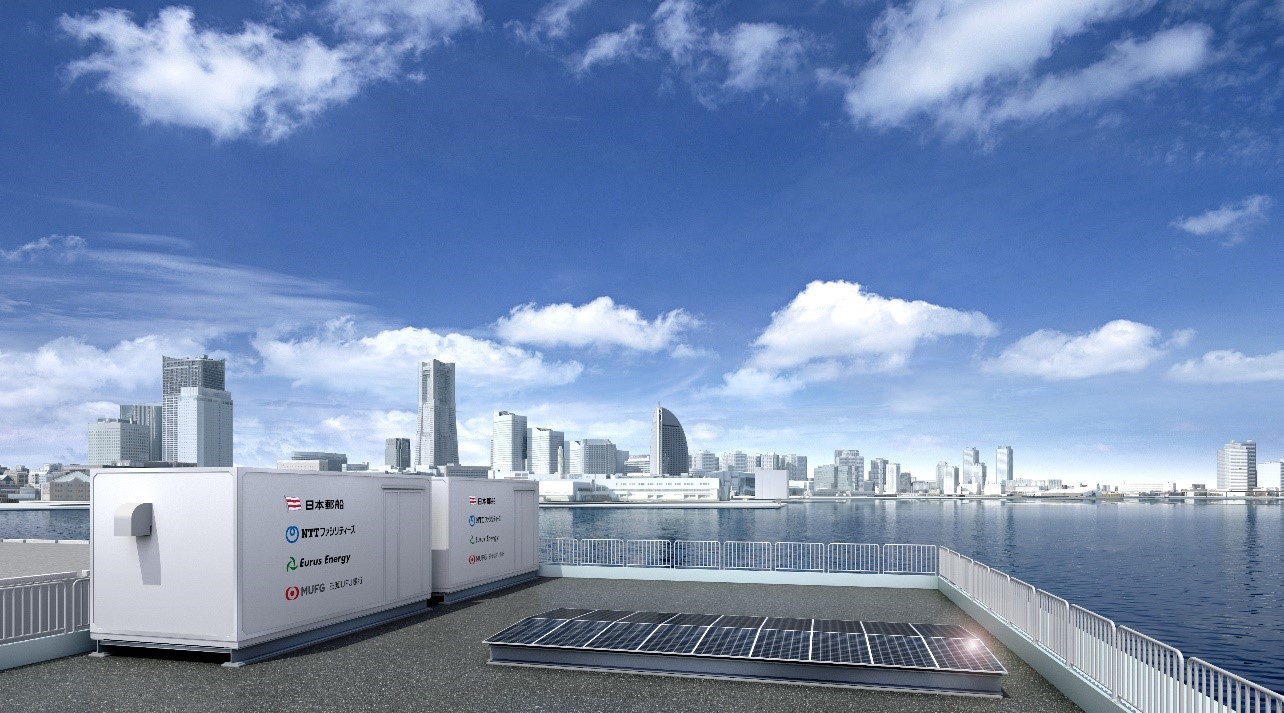

- NYK to begin experiment in Yokohama for offshore data center

- (Company statement, March 27)

- NYK will begin an experiment in Yokohama in autumn to develop an offshore data center powered by renewable energy. A test facility will operate on stored battery power, examining potential issues such as salt damage.

- CONTEXT: NYK, Mitsubishi UFJ Bank, NTT Facilities, Eurus Energy Holdings, and Yokohama City are partners on the project that calls for a container-type data center with solar panels and batteries on a floating mooring facility.

TAKEAWAY: Nuclear power is often regarded as the most reliable energy source for meeting the growing energy demands of data centers, especially given many operators’ preference for non-fossil fuel sources. However, exploring alternatives, particularly battery storage, could offer a viable solution.

Demo of a data center powered with solar

Demo of a data center powered with solar

Artist impression of a future offshore data center powered by floating wind turbines

Artist impression of a future offshore data center powered by floating wind turbines

Source: NYK

Editorial: TEPCO must rewrite path to reconstruction

(Nikkei, March 23)

- CONTEXT: This is an editorial from Nikkei.

- TEPCO held up publication of its revised business reconstruction plan for FY2024 over delays in restarting Kashiwazaki-Kariwa NPP. The restart is essential for improving TEPCO finances, but local approval is uncertain.

- The utility faces rising costs from the Fukushima Daiichi cleanup, with the total now at ¥23.4 trillion, up from an initial estimate of ¥6 trillion. Despite plans to have two Kashiwazaki-Kariwa reactors operating, safety issues caused delays.

- TEPCO expects a loss of ¥520 billion by March 2025, its seventh consecutive year of losses. TEPCO’s fifth business plan must focus on accelerating the plant’s restart, and aim to improve public trust and profitability through restructuring.

- In a provisional update, TEPCO requested an extra ¥1.9 trillion in state aid to cover rising costs. TEPCO’s reliance on public funds continues to grow, raising concerns about the financial burden on taxpayers.

- TEPCO’s attempts at business restructuring and attracting capital have had limited success. The only significant achievement has been JERA. Other efforts to diversify and strengthen revenue have fallen short. To regain financial stability, TEPCO must not only restart Kashiwazaki-Kariwa, but reduce dependence on nuclear power and state support.

OCCTO reports on status of FY2025 supply plan

(Agency statement, March 19)

- OCCTO reported its outlook for power supply in FY2025 (and through FY2034); this includes assumptions around impact of severe weather on supply and demand and the influence of reserve margins on balancing.

- OCCTO says that demand for electricity should continue to increase through FY2034, due to economic growth, and new data centers and semiconductor factories; their impact is expected to be greater than the impact of population decline and energy conservation measures.

- In terms of the supply-demand balance, there’ll be years when supply reliability is not certain in some areas, which will require measures such as additional capacity market auctions and adjustments to the timing of power plant repairs.

- As far as balancing capacity, OCCTO sees annual fluctuations due to the retirement, as well as construction, of thermal power plants; but, overall the balance is expected to remain at FY2024 levels. Also, the power mix of coal, LNG-fired thermal power and pumped storage power is expected to stay largely unchanged.

- In response to robust summer and winter demand, OCCTO expects to secure the minimum required reserve rate of 3% in all areas, taking into account increased supply from thermal power, inter-regional volumes, and dispatchable power sources during periods of high demand.

- The agency expects few changes in supply-demand management in the context of the reserve margins as they stand.

- CONTEXT: Each March, OCCTO publishes the “Supply Plan” in its annual report.

- SIDE DEVELOPMENT:

- OCCTO to prepare long-term policy for cross-regional grid

- (Agency statement, March 21)

- With a view to formulating the third long-term cross-regional grid system policy, OCCTO will examine the following issues:

- Review of long-term outlook for cross-regional grid development

- Update guidelines for renewal of aging facilities

- Evaluate and implement renewals of interconnection facilities

- Study congestion management on trunk and local grids (with an eye on the future needs of a simultaneous market)

- These discussions will be in tandem with ANRE, EGC and TSOs; not just OCCTO.

- CONTEXT: OCCTO has formulated the “Long-term Policy for the Cross-regional Grid System” for the development and renewal of the nationwide grid systems. This includes the ideal state of the nationwide grid systems over a 10-year period and how to achieve it. The first version dates to March 2017; it was reviewed in March 2023. It now must be rethought in light of recent changes, such as the 7th Basic Energy Plan.

Japan retail electricity sales dip; new entrants reach 20% market share

(Denki Shimbun, March 24)

- Total electricity retail sales in December 2024 slid 1% YoY to 64.8 TWh. New market entrant suppliers (shin denryoku) increased sales 17.4% to 13.0 TWh, reaching a market share of 20.1%, up 3.1 percentage points from a year earlier.

- The big power utilities, EPCOs, saw sales decline 4.7% to 51.8 TWh, marking a continued erosion in their market share.

- Total electricity contracts rose 0.2% YoY to nearly 90 million accounts, with new entrants accounting for about 20.4 million contracts (up 3%).

- Regionally, sales by incumbent utilities declined in most areas, notably 7.7% in Tohoku and Kyushu, and 5.3% in Chugoku; while Okinawa saw a 6.2% increase.

NTT Anode Energy inks off-site corporate PPA with NTT Urban

(Company statement, March 26)

- NTT Anode Energy will supply renewable energy through an off-site corporate PPA to four commercial properties owned by NTT Urban Development, including Shinagawa Season Terrace and WITH Harajuku.

- About 9 MW of newly developed solar capacity across multiple sites will supply about 10 GWh annually.

- CONTEXT: The buildings in the deal need between 4 GWh and 17 GWh of a year. The commercial offices sector has been one of Japan’s most active at inking PPA deals and pursuing 100% RE goals.

- SIDE DEVELOPMENT:

- NTT Anode Energy expands solar PPAs

- (Company statement, March 27)

- Starting April 1, NTT Anode Energy will supply 6.2 GWh of renewable electricity annually, from newly developed 5.8 MW solar plants, to battery maker Energywith via an off-site corporate PPA.

- Energywith’s Saitama facility will achieve 100% renewable energy coverage for its total annual consumption of 41 GWh.

NEWS: HYDROGEN

MOL, IHI, etc ink MoU for green ammonia in India

(Company statement, Mar 25)

- Mitsui O.S.K. Lines (MOL), IHI Corp, Hokkaido Electric, Mitsubishi Gas Chemical, Mizuho Bank, and Tokyo Century, inked an MoU to consider investment in green ammonia production in Odisha, India.

- Led by ACME Group, by 2030 the project aims to produce 400,000 tons of green ammonia annually.

- The green ammonia will be shipped to Japan, to supply power producers, chemical manufacturers, and other industrial users. The six firms will explore forming a special-purpose company to invest in and operate the project.

- Mizuho Bank aims to provide ¥2 trillion to build hydrogen and ammonia supply chains by 2030.

Hydrogen co-firing demo to launch at Himeji No. 2

(Company statement, March 28)

- In April, Kansai Electric will begin Japan’s first 30% hydrogen co-firing field test using a large commercial gas turbine at Himeji No. 2 Power Plant.

- The field test uses hydrogen produced via water electrolysis at the plant, to evaluate operation, maintenance, and safety protocols for hydrogen power generation.

KHI begins work on hydrogen liquefaction compressor demo

(Company statement, March 26)

- Kawasaki Heavy Industries began building a demo facility at its Harima Works (Hyogo Pref) for its newly developed centrifugal hydrogen compressor “KM Comp-H2”, designed for hydrogen liquefaction plants.

- CONTEXT: The unit’s manufacturing is ready, and the facility is scheduled for completion November 2025, followed by one year of field testing.

- This world-first compressor for liquefaction plants supports 100% pure hydrogen.

Japan-Korea hold follow-up hydrogen & ammonia dialogue

(Government statement, March 27)

- Japan and South Korea held the 2nd Hydrogen and Ammonia Cooperation Dialogue on March 26 in Tokyo, agreeing to deepen collaboration in supply chains, certification, international standards, and safety.

- The countries will establish a Japan-Korea platform led by private organizations to promote hydrogen and ammonia supply chain development and utilization.

Cosmo Energy, Shizuoka Univ study green hydrogen by seawater electrolysis

(Company statement, March 26)

- Cosmo Energy Holdings and Shizuoka University began a joint study of green hydrogen production using seawater electrolysis.

- If successful, the project could produce green hydrogen at less cost.

- CONTEXT: Cosmo Energy is working to develop CCS and CCU. The company uses large amounts of seawater in oil refining and has seawater pumping facilities. Shizuoka University has developed and patented technology for producing hydrogen by electrolyzing seawater.

TAKEAWAY: Seawater electrolysis is a process where electricity is used to decompose seawater (H2O + dissolved salts) into its constituent elements: hydrogen (H2) and oxygen (O2). Using seawater could be a boon because of the abundance of the resource as compared to limited freshwater resources, but corrosion from salty water has prevented this development to date. Still, the need for switching to seawater has been questioned by many sources due to the additional costs involved, the additional energy use, and other challenges.

Ammonia-fueled tugboat completes successful demo

(Company statement, March 28)

- NYK Line and IHI Power Systems completed a 3-month demo of the world’s first ammonia-fueled tugboat, Sakigake, achieving up to 95% GHG emissions reduction.

- This validates ammonia as a viable next-gen marine fuel.

- CONTEXT: A second ammonia-fueled vessel, an ammonia carrier, is under joint development by NYK, IHI, Japan Engine Corp, and Nippon Shipyard, and is scheduled for delivery in November 2026.

JAEA applies for upgrade to HTTR to connect a hydrogen facility

(Company statement, Dec 28)

- JAEA asked the NRA to upgrade the HTTR (High-Temperature Engineering Test Reactor) at the Oarai Research Institute, to connect a hydrogen production facility. This goal is to verify hydrogen production technology using reactor-generated heat.

- CONTEXT: HTGRs offer improved safety and can supply high-temperature heat without CO2 emissions; thus it’s a promising source for large-scale hydrogen production.

NEWS: SOLAR AND BATTERIES

Kansai Electric to build one of Japan’s largest battery storage facilities

(Company statement, March 25)

- Kansai Electric plans to build two large-scale battery storage facilities in Sapporo, with a combined output of 100 MW and a total storage capacity of 351 MWh, which would be among Japan’s largest.

- The facilities, named SGET Sapporo 1 and SGET Sapporo 2, will each have 50 MW of volume and 175 MWh of capacity. The lithium-ion battery containers will be supplied by Sungrow Power (China).

- Construction begins in March 2026, with operations set for April 2028. Partners include Sparx Group and JA Mitsui Leasing; Toshiba Energy Systems will oversee construction and battery procurement.

ANRE: control functions of home storage batteries to support DR

(Government statement, March 21)

- ANRE proposed control functions for home storage batteries that would support demand response (DR).

- For communication, an appliance will be able to link with the gateway in the same way as a heat pump, and with the DR server using a structured data format.

- For external control functions, the DR server will be able to issue charge/ discharge commands with target values and durations for power to the appliance, as well as monitoring the amount of charge, and returning the appliance to its own mode after DR control. The server would also monitor the amount of power needed for backup.

- As with heat pumps, the appliance must pass security requirements and be on the labeling system (JC-STAR).

- CONTEXT: The “DRready Study Group” was launched in June 2024 to examine the DR requirements for equipment and appliances. Because DR requirements vary by each appliance, discussions began with heat pump water heaters, which are expected to become more prevalent and consume large amounts of electricity.

JR Kyushu leads initiative to tackle abandoned small solar plants

(Company statement, March 25)

- JR Kyushu, Mitsubishi UFJ Trust Bank, Fuyo General Lease, and Girasol Energy have launched “Hyakunen Solar Kyushu,” a business initiative aimed at acquiring and consolidating small to medium-sized solar power plants in Kyushu to ensure their stable, long-term operation and address abandonment risks.

- Hyakunen Solar Kyushu plans to acquire 10 MW of solar power capacity in the Kyushu region by 2027.

- The project will be funded with investments from the four companies, alongside financing from regional banks such as Higo Bank.

- CONTEXT: Small and medium-sized solar power plants, with a capacity of less than 1 MW, account for 90% of Japan’s total, but there are concerns that they will be abandoned after the 20-year FIT period expires.

Japan mulls 12-hour daily limit for battery charging to ease grid integration

(IT Media, March 20)

- CONTEXT: The govt is discussing how to speed up connection of more energy storage batteries to the grid. There is concern that adding a lot of new battery capacity at once could destabilize the energy system’s flow.

- One idea is a standard daily maximum for charging, at 12 hours nationwide. Operators that agree would then see their grid applications processed faster.

- Under the proposed guidelines, battery storage operators subject to these restrictions would retain eligibility to participate in capacity and balancing markets, although failure to meet market requirements due to charging restrictions won’t exempt operators from penalties.

- Grid operators in turn will be asked to provide, in advance, battery storage developers with detailed hourly grid-flow data, enabling accurate assessments of potential charging limitations before finalizing connection agreements.

TAKEAWAY: METI is reviewing a number of strategies that would give grid operators leeway with how they treat BESS in times of network congestion. These include the use of “non-firm” contracts through which battery facility operators agree to restrictions on charging at times of grid congestion. METI wants to avoid making restrictions excessive, otherwise BESS won’t be able to play its role in balancing the market. However, officials also seem keen to retain a degree of control, especially over peak periods. Where BESS facilities are unable to meet their obligations in the capacity / balancing markets explicitly due to grid issues, the onus may fall on the grid operator to invest in network upgrades.

Smart Energy enters battery maintenance business

(Nikkei, March 27)

- Smart Energy entered the battery storage maintenance business. It will maintain three large BESS at the JRE Fukuchi Daisan solar farm in Fukuoka Pref.

- As of January, Smart Energy was maintaining 4.6 GW of solar power capacity. By the end of FY2025, it targets contracts to maintain 300 MW of battery storage.

Solar/ BESS developer TRENDE raises ¥1 bln, adds Tokyo Century to investors

(Company statements, March 19)

- TRENDE, a Tokyo-based provider of zero-initial-cost solar power and battery-storage installation services, raised ¥1.07 billion to fund expansion.

- Investors include Tokyo Century, National Federation of Agricultural Cooperative Associations, Zen-Noh Energy, and Toshiba Infrastructure; they join existing shareholders Idemitsu Kosan, Itochu, and Forward Ventures.

- TRENDE plans collaboration with Tokyo Century in finance and asset management.

- It also wants to expand nationwide a project linking vehicle-to-everything (V2X) systems and P2P power trading in collaboration with Toshiba Infrastructure.

NEWS: WIND POWER AND OTHER RENEWABLES

Kanadevia, Taisei, MOL sign MoU to accelerate floating offshore wind

(Company statements, March 27)

- Kanadevia, Taisei Corp, and Mitsui OSK inked an MoU to share expertise, aiming to reduce costs and risks associated with floating offshore wind projects.

- The collaboration will focus specifically on improving construction methods for floating foundation manufacturing, as well as efficient towing and mooring.

GPI publishes environmental assessment for 95 MW wind project

(Company statements, March 11)

- Green Power Investment released its environmental assessment for a 95 MW wind farm in Kazuno City, Akita Pref. Public feedback is accepted until April 24.

- The project spans 1,302 hectares, (up to 22 turbines, 4.2 MW to 6.1 MW capacity)

- Construction to start around 2030, with commercial operations in Feb 2033.

Morimura SOFC Tech develops compact, high-efficiency mono-generation SOFC system

(Company statement, March 27)

- Morimura SOFC Technology has developed a compact, high-efficiency mono-generation solid oxide fuel cell (SOFC) system.

- This system fosters energy conservation and CO2 reduction by maximizing high power generation efficiency (65%); the system is greatly reduced in size and weight.

- The prototype has been installed at the Niterra Komaki plant and is in trial operation; the company aims to commercialize the product in FY2027.

- CONTEXT: Morimura SOFC Technology is a JV established in 2019 by four ceramic companies of the Morimura Group: Noritake, TOTO, NGK Insulators, and Niterra. In 2021, Morimura Bros joined the venture.

Shikoku Electric launches new hydro plant

(Company statement, March 24)

- Shikoku Electric began commercial operation of the Kurofuji River Power Plant, with a maximum output of 1.9 MW

- CONTEXT: By 2030, Shikoku Electric seeks to develop 500 MW of renewable energy capacity in Japan and overseas.

NEWS: NUCLEAR

HEPCO plans to restart Tomari NPP 1-2

(Nikkei, March 26)

- Hokkaido Electric (HEPCO) revealed plans to restart Tomari NPP Units 1 and 2 in the early 2030s. By FY2035, HEPCO aims to achieve an operating profit of over ¥90 billion. If the restarts go forward then HEPCO expects electricity rate reductions.

- As for Unit 3, HEPCO completed the explanations for regulatory approval, and it expects approval within the year, aiming to restart Unit 3 in early 2027.

- HEPCO also announced its investment strategy through FY2035. It will allocate ¥400 billion over the next decade for carbon-neutral initiatives. It will allocate ¥250 billion for next-gen energy sources like hydrogen and ammonia.

- CONTEXT: The combined capacity of Tomari Units 1,2,3 is 2.07 GW; they covered over 40% of Hokkaido’s electricity demand before the Fukushima accident. Since then, all units have been offline. By FY2035, HEPCO plans for nuclear power to account for 60–70% of its energy mix.

TAKEAWAY: As TEPCO’s example shows, nothing can be taken for granted in these plans for nuclear reactor restarts. HEPCO’s numbers look promising and could make it one of the most valuable power utilities in the country (see this week’s Analysis section for more details), but the company’s applications for a restart of Tomari NPP have been repelled by the regulator multiple times. As covered in previous Analysis texts by Japan NRG, no nuclear reactor restarts are likely within the next two years. HEPCO’s early 2027 guidance seems overly optimistic.

NRA gives approval for long-term management plan at Takahama NPP

(Company statement, March 27)

- KEPCO received NRA approval for its Long-Term Facility Management Plan for Takahama NPP Unit 1. The plan addresses aging measures.

- CONTEXT: Nuclear reactors operating beyond 30 years must be assessed every 10 years, at which point a Long-Term Facility Management Plan must be produced and accepted by the NRA. Takahama began commercial operations in November 1974, turning 50 years old. It is one of Japan’s oldest operating reactors.

Chugoku Electric consent for anti-terrorism facility at Shimane NPP

(Company statement, March 25)

- Chugoku Electric received prior consent from Shimane Pref for an anti-terrorism facility at Shimane NPP Unit 2 (BWR, 820 MW).

- CONTEXT: The company submitted a request for prior consent to Shimane Pref and Matsue City in 2016. In the same year, it applied to the NRA for reactor installation modification approval. In 2024, it received reactor installation modification approval from the NRA. Also in 2024, it received consents from the relevant local govts.

Fukui Gov gives nod to KEPCO’s spent fuel roadmap

(Company statement, March 24)

- Governor of Fukui Pref endorsed KEPCO’s spent fuel management roadmap.

- CONTEXT: The roadmap outlines more spent fuel shipments to France’s Orano, doubling MOX fuel to 400 tons. Plans call for the Rokkasho plant to start operations in FY2028. Japan NRG covered the topic in the Nov 20, 2023 issue.

TAKEAWAY: Also in FY2023, KEPCO proposed a roadmap for transporting spent nuclear fuel outside the prefecture. The governor’s approval of such a roadmap allows the continued operation of the utility’s three NPPs in Fukui. Their operations are tied to a future removal of spent fuel from the region, but concerns remain due to repeated delays at Rokkasho.

JACE visits Kashiwazaki-Kariwa NPP

(Company statement, March 24)

- Niinami Takeshi, representative director of Japan Association of Corporate Executives, visited the Kashiwazaki-Kariwa NPP, and inspected the central control room, Unit 7 operating floor, and seawall.

- After the visit, he said that the plant has a “high level of safety”.

- CONTEXT: Since 2023, JACE has advocated for nuclear power. This visit marks the first time in 10 years that a JACE director inspected Kashiwazaki-Kariwa. Niinami stressed the need to share economic benefits with local communities, and he called for a national framework to foster industries in those areas.

TEPCO gets report from Nuclear Security Committee

(Company statement, March 24)

- TEPCO received the 6th evaluation report from the Nuclear Security Expert Evaluation Committee assessing TEPCO’s own efforts.

- The report found no new issues at Kashiwazaki-Kariwa NPP. Future evaluations will focus on monitoring progress every six months.

Kyushu Electric shuts down Genkai reactor for regular inspection

(NHK, Nikkei, March 26)

- The 18th regular inspection at Genkai NPP Unit 3 began on March 28. It is expected to be turned back online in early June with regular power generation operation expected around June 30, 2025.

- CONTEXT: Genkai NPP Unit 3 (output 1.18 GW) is operated by Kyushu Electric. During the inspection period, it will replace some of the 193 fuel assemblies. Unit 4 at the same NPP is still in operation and is scheduled to undergo regular inspection in late July.

NEWS: TRADITIONAL FUELS

JAPEX sets up oil JV in the U.S.

(Company statement, March 26)

- JAPEX founded Peoria Resources through its overseas subsidiary, JAPEX (U.S.)

- JAPEX is developing projects, including oil production and the Freeport LNG project. To expand its U.S. business, it’s considering acquiring operating assets.

- CONTEXT: The venture will handle the full process, from acquiring mining sites to extraction. The goal is to secure its first site by around 2026.

Ithaca Energy acquires JAPEX UK

(Company statement, March 25)

- Ithaca Energy acquired Japex UK (JUK) from JAPEX for $193 million. JUK holds a 15% stake in the Seagull oil field in the North Sea.

- This deal will increase Ithaca’s stake from 35% to 50%, matching bp’s stake.

LNG stocks up from previous week, up YoY

(Government data, March 26)

- As of March 23, the LNG stocks of 10 power utilities were 1.83 Mt, up 17.3% from the previous week (1.56 Mt), up 23.7% from end March 2024 (1.48 Mt), and 9.9% down from the 5-year average of 2.03 Mt.

- CONTEXT: Unseasonal snowfall in the past 10 days depleted LNG stocks, pushing utilities into the spot market to prop up reserves. Temperatures remain volatile but there is a general warming trend.

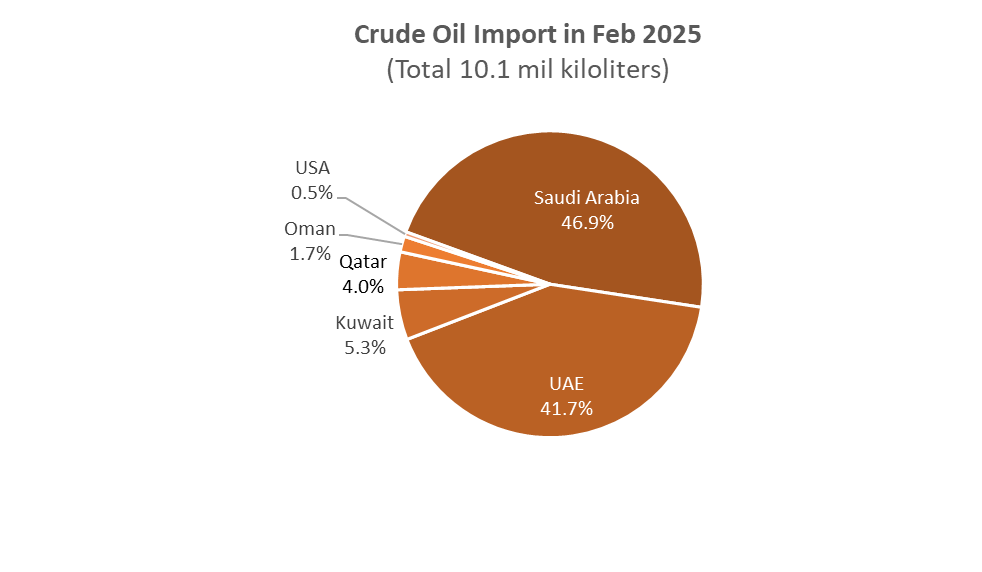

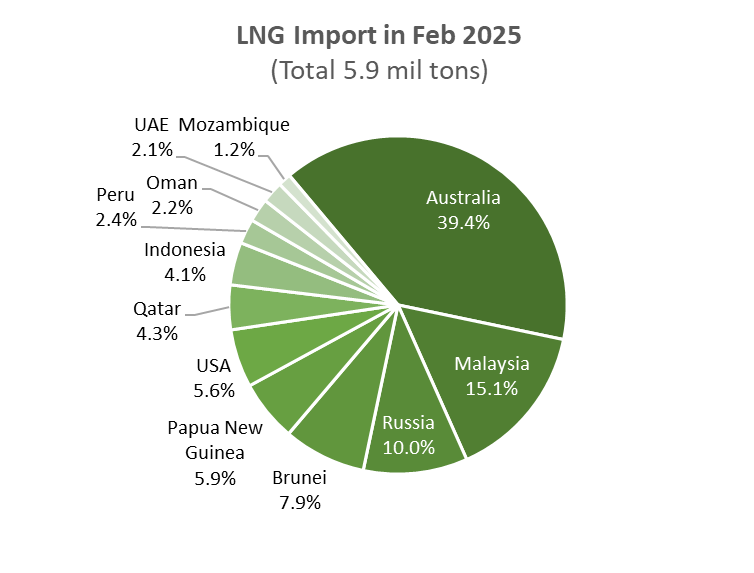

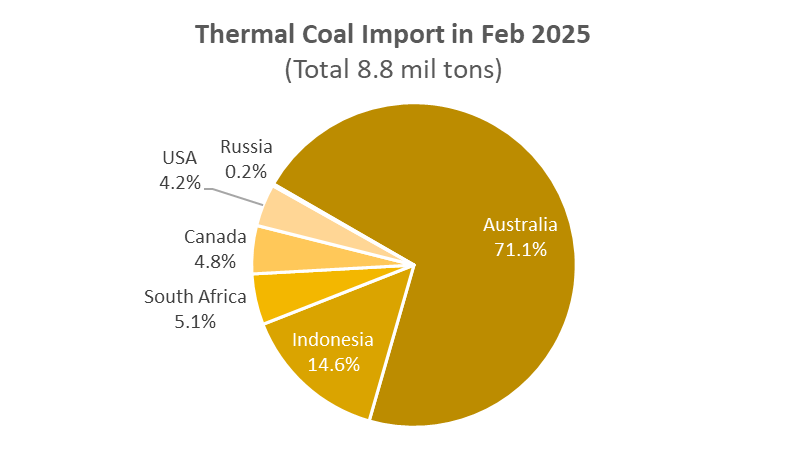

February Oil/ Gas/ Coal trade statistics

(Government data, March 28)

Imports | Volume | YoY | Value (Yen) | YoY |

Crude oil | 10.1 million kiloliters | -13.1% | 789.5 billion | -12.9% |

LNG | 5.9 million tons | -2.5% | 554.1 billion | -7.2% |

Thermal coal | 8.8 million tons | 13.1% | 191.6 billion | -2.3% |

- In February, Japan imported 10.1 million kiloliters of crude oil, 22% less than in January and 13.1% less YoY. February is the month that consistently shows a decrease in imports. Almost all the oil came from the Middle East, except 0.5% from the USA. In 2021, crude oil was sourced from 24 countries. In 2022, that number dropped to 19, then to 16 in 2023; and 14 in 2024. This year, Japan imported from only 8 countries.

- LNG imports in February totaled 5.9 Mt, down 11.5% over January (6.6 Mt), and down 2.5% YoY. Australia remained Japan’s top LNG source.

- Thermal coal imports in February decreased to 8.8 Mt, down 15% from January (10.4 Mt), and up 13.1% YoY (7.8 Mt). As usual, Australia and Indonesia are the two major suppliers of thermal coal to Japan.

NEWS: CARBON CAPTURE & SYNTHETIC FUELS

METI eyes competitive bidding for CCS transport and storage

(Government statement, March 28)

- The latest meeting of the METI working group on how best to support the carbon capture and storage (CCS) sector suggested the govt considers introducing a competitive auction system to allocate funding for CCS transportation and storage projects. The aim is to reduce costs and foster market competitiveness.

- Consortiums would consist of emitters and transportation/ storage operators bidding on a per-ton of CO2 transportation and storage fee. Carbon capture costs at emission sites, which vary significantly by industry, wouldn’t be included in auction criteria.

- Auctions could be held annually, beginning in the early 2030s, to slowly scale up CCS projects. Maximum bid prices would be capped to reflect realistic costs, expansion potential, and project risks.

- The govt should seek to introduce a transparent funding framework to supports CCS operators based on the difference between CCS costs and so-called industry-standard CO2 mitigation expenses, aiming to eventually phase out state support as the CCS sector costs become competitive.

TAKEAWAY: The development of business models for CCS in Japan is still at a very early stage. Early signs indicate that METI is keen to deploy more of contract-for-differences and actions approaches used for other energy sources. The annual auction cycle would give predictability for CCS operators.

Tokyo launches local carbon credit market utilizing blockchain tech

(Government statement, March 25)

- Tokyo launched Japan’s first municipally run carbon credit trading platform, the “Tokyo Carbon Credit Market,”.

- The system seeks to facilitate fee-free trading of J-Credits and voluntary credits from overseas issuers, helping SMEs in Tokyo pursue decarbonization goals.

- Utilizing blockchain technology to ensure secure transactions and prevent fraud, it enables companies to buy credits through an e-commerce style interface.

Japan and Brazil sign MoU on carbon credit market and climate action

(Nikkei, March 25)

- MoE Minister Asao Keiichiro met with Brazil’s Minister of Environment and Climate Change to sign an MoU for cooperation on climate action.

- They will focus on carbon credit markets and GHGs emission measurement, and to strengthen cooperation ahead of COP30 in Brazil (Nov 2025).

- SIDE DEVELOPMENT:

- Japan and Brazil ink economic partnership for biofuels, green ammonia, etc

- (Asia Nikkei, March 27)

- Japan and Brazil inked a 5-year partnership on climate, economy, defense, etc.

- PM Ishiba and President Lula da Silva agreed to reciprocal leadership visits every two years, the launch of a new dialogue on defense and foreign affairs, etc.

- Projects include decarbonization initiatives leveraging Brazil’s biofuels and Japan’s auto technology. Agreements include Japanese startup Tsubame BHB and Brazil partners seeking to produce green ammonia fertilizer via sugarcane-based bioethanol.

JFE Steel and partners test carbon-recycling supply chain in industrial complex

(Government statement, March 24)

- JFE Steel, Mitsubishi Gas Chemical, and Mitsubishi Chemical signed an MoU for supply chain testing to realize a carbon recycling society at the Mizushima Industrial Complex in Kurashiki City, Okayama.

- From FY2026, JFE Steel will supply by-product gas from its steelworks to Mitsubishi Gas Chemical, which will use the by-product gas as a raw material to produce methanol at a newly constructed demonstration plant.

- This test is a new initiative in which difficult-to-abate industries will work together to produce chemicals by utilizing CO2 in the by-product gas generated in steelmaking.

- CONTEXT: The Mizushima Industrial Complex, where the three companies have their business bases, is densely concentrated.

Finnair signs first SAF supply agreement in Japan with Cosmo Oil

(Company statements, March 26)

- Finnair inked its first sustainable aviation fuel supply agreement with a Japanese company, Cosmo Oil Marketing, to buy 233 tons of SAF in 2025.

- The SAF will be produced almost entirely from domestically collected waste cooking oil at Cosmo Oil’s Sakai Refinery in Osaka Pref.

BY JAPAN NRG TEAM

METI Forges Ahead on ‘Simultaneous Market’ Plans to Boost Renewables Integration

To improve electricity market efficiency and create a system capable of reliably accommodating greater renewable energy penetration, METI is conducting an in-depth review on introducing a simultaneous electricity market (同時市場) – a fundamentally new approach to power trading in Japan.

In a simultaneous market, generation and consumption of electricity are balanced in real-time, optimizing dispatch and pricing through a centrally coordinated system. This approach integrates electricity supply and balancing services into a unified framework capable of effectively managing real-time volatility in both production and demand. Additionally, it facilitates better coordination among various ancillary and reserve services, potentially reducing the costs associated with balancing power procurement.

Implementing such a system will necessitate significant structural changes in electricity bidding processes, market offers, and methods for securing adjustment volumes. Although inspired in part by the PJM (Pennsylvania-New Jersey-Maryland) system – the largest independent system operator (ISO) in the U.S. – METI’s deliberations on the simultaneous market are already entering their third year. Nevertheless, recent discussions indicate increasing confidence that Japan can successfully adapt and implement this market structure.

The most recent METI committee meeting, held last week, focused extensively on detailed presentations regarding market design options, international comparisons, and strategic implementation considerations. Japan NRG takes a closer look at the simultaneous market debate within the broader context of Japan’s evolving electricity market reforms.

What is PJM and its impact on Japan?

The PJM system operator utilizes a nodal pricing system (also known as locational marginal pricing or LMP) to determine wholesale electricity prices. This reflects the cost of supplying an extra unit of energy at a specific location (node), considering grid constraints.

Under this system, each node on the grid can have a different electricity price, influenced by factors such as generation availability, transmission capacity, and congestion. PJM centrally coordinates dispatch using detailed real-time data, enabling economically efficient operations and clearer price signals for investment in generation and transmission infrastructure.

Traditionally, Japan has utilized a regional-based market system rather than nodal pricing. Prices are uniform across broad geographical zones, and detailed locational constraints (congestion and transmission limitations) are typically managed through administrative measures rather than direct market signals.

The introduction of a simultaneous market in Japan would represent a shift from that broader, regional price approach to more granular, node-based price signals. It essentially means using market-based solutions over administrative interventions to alleviate network constraints.

Background: Market reforms

Before METI started power market liberalization, Japan’s electricity system was a vertically integrated monopoly, with 10 regional power companies (EPCOs) controlling the entire process of generation, transmission, and distribution of electricity.

This system’s advantage was that with exclusive control over their regional areas, the EPCOs ensured a stable power supply. The downside was that it inhibited competition. Pricing and investment decisions were regulated by METI, and consumers had no choice of electricity provider.

Japan fully liberalized retail electricity sales in 2016, which has allowed over 700 new companies to enter the power market and compete with the EPCOs, mostly on the retail side. Market-based platforms to trade electricity were rolled out, primarily on the Japan Electric Power Exchange (JEPX), which manages the Spot Market, Intraday Market, Baseload Market, and Non-Fossil Fuel Value Trading Market.

Later, other platforms were added to mimic physical power systems. The OCCTO-operated Capacity Market helps to secure availability of power plants several years from now. This system was expanded two years ago with a Long-Term Decarbonization Power Source Auction and Standby Power Source System, expanding the option of securing capacity to the short-, middle- and long-term. Finally, in 2024 the Electric Power Reserve Exchange (EPRX) took on the trading of all balancing power services, which cover last-minute adjustments to available supply to ensure it meets demand.

Even with these reforms, challenges still persist. For example, generators say they need stronger investment incentives, especially for low-carbon capacity, and for improving system stability. The EPRX was designed to help Transmission System Operators (TSOs) buy balancing reserves more efficiently in a competitive setting, instead of relying only on their own resources; but major TSOs, particularly Tokyo and Chubu, largely avoid using the platform.

Instead, the big utilities continue to secure balancing reserves using traditional methods such as internal power adjustments or direct contracts. They claim that this is down to:

- Difficulty in predicting power demand and supply, especially with solar generation;

- Existing contracts that do not assume full use of EPRX;

- Preference for internal control instead of relying on an external system.

Recent updates in power market reform

On January 27, 2025, METI proposed an action plan to review the power market reforms so far and set future directions. A special working group will be created under the Electricity and Gas Basic Policy Subcommittee to review new necessary regulatory and policy changes, including possible amendments to the Electricity Business Act.

The reform plan is divided into three major areas:

Mid-to-Long-Term Supply Security Mechanisms

- Increasing investment incentives for new power generation

- Strengthening mechanisms such as the Feed-in-Premium (FIP), Long-Term Decarbonization Power Source Auction (LTDA), and the capacity market to ensure adequate power volumes

- Encouraging investment in renewable energy and battery storage to improve long-term stability

Development of New Electricity Price Indexes and Trading Markets

- Creating futures markets, forward contracts, and bilateral Power Purchase Agreements (PPAs) to provide more price predictability for electricity retailers and generators

- Developing stable procurement methods to reduce price fluctuations and help financial planning for market participants

Short-Term Trading and Balancing Markets

- Strengthening spot and balancing markets to increase operational efficiency.

- Introducing the Simultaneous Market

- Considering integrating the capacity market with the balancing market to improve procurement efficiency

The discussions cover a broad range of issues, but METI expects them to lead to formal policy recommendations by late FY2025, with possible law revisions taking place in 2026.

Simultaneous Market discussions

The METI study group that seeks how to set up a simultaneous market (同時市場) has now held two meetings, the latest on March 24. The group spent much of early deliberations reviewing the broader market reforms in the country and how a simultaneous market would fit within that. Even today, one of the key areas of debate is around pinning down the precise definition of what such a market is and how far its reach should be.

As an example, one of the areas under review is what to do with self-scheduled generation (自己計画電源) – power plants whose start-up/ shut-down and output is determined independently by their operators, rather than by market dispatch instructions. As such, operators have discretion whether to submit information on their status.

As TSOs seek to optimize dispatch and run the grid efficiently, avoiding congestion, they’d like to incentivise self-scheduled generation to report the details of their operations. But some of these self-scheduled generators work under bilateral contracts.

Mandating the generators to bid on the simultaneous market (and share their operations) would raise transparency but also create legal and accounting issues. For example, how would they account for the difference between the market and the contract prices? Even if the generators simply share the plant status information without selling power via the market, new rules will be required to ensure compliance with grid reliability and operational constraints.

The above is one of a plethora of discussion points outlined by METI’s study group, but it shows how the group’s workings has started delving into the practical matters that all market participants will face once a simultaneous market opens.

METI’s group has explored how the mechanism works overseas, referencing similar markets established in Europe and North America, particularly Germany and the U.S.; international experience shows differences in application across jurisdictions.

So, while a simultaneous market would be designed to balance real-time supply and demand, there is a debate over the exact scope of services this market should cover. Should it include services such as frequency control (周波数調整) and synchronous reserve (同期予備力)? Or act as a comprehensive framework capable of quickly and flexibly managing short-term imbalances? Even the application of a real-time market (リアルタイム市場) has to take into account the specific grid infrastructure and regulatory environment of Japan.

The group also has concerns about fairness and transparency, cautioning against scenarios in which established players might gain undue advantages, or where price mechanisms might unintentionally discourage market entry by innovative renewable energy producers. These require adjustments to the regulations, clearer price signals, and ways to encourage the market entry of innovative new technologies.

Of course, one thing is clear: the introduction of a simultaneous market would require more sophisticated real-time information systems, advanced monitoring and control technology, as well as significant upgrades to the electricity grid. The cost of such upgrades have yet to be estimated but they will be substantial.

Challenges and next steps

Given the size and scope of the changes, a major challenge will be convincing all the public and private stakeholders of the cost-benefit of this shift. The study group recommended pilot projects and phased implementation strategies to test, refine, and gradually demonstrate the market’s effectiveness.

As for the next steps, the group plans to conduct detailed simulations and economic modeling to quantify potential market impacts and benefits, while keeping an eye on best practices abroad.

The group recognizes the significant potential benefits of enhancing grid reliability in Japan with an eye to greater renewable energy integration, and more market-driven signals, but their outlook is one of optimistic caution due to the significance of the reforms.

The lackluster performance of the EPRX and the backup reserve markets shows how important incentives are to ensure a broad set of market players buy in. Even in the more popular markets, like the LTDA, there are tensions between big utilities like JERA and the government.

Often, it seems like reforms of this scale move along at a snail’s pace, with the adoption of the simultaneous market not expected for another three or more years. Given what’s at stake, the steady nature of the deliberations may well be justified. And the time to engage with METI on the planning should be now.

BY YURIY HUMBER

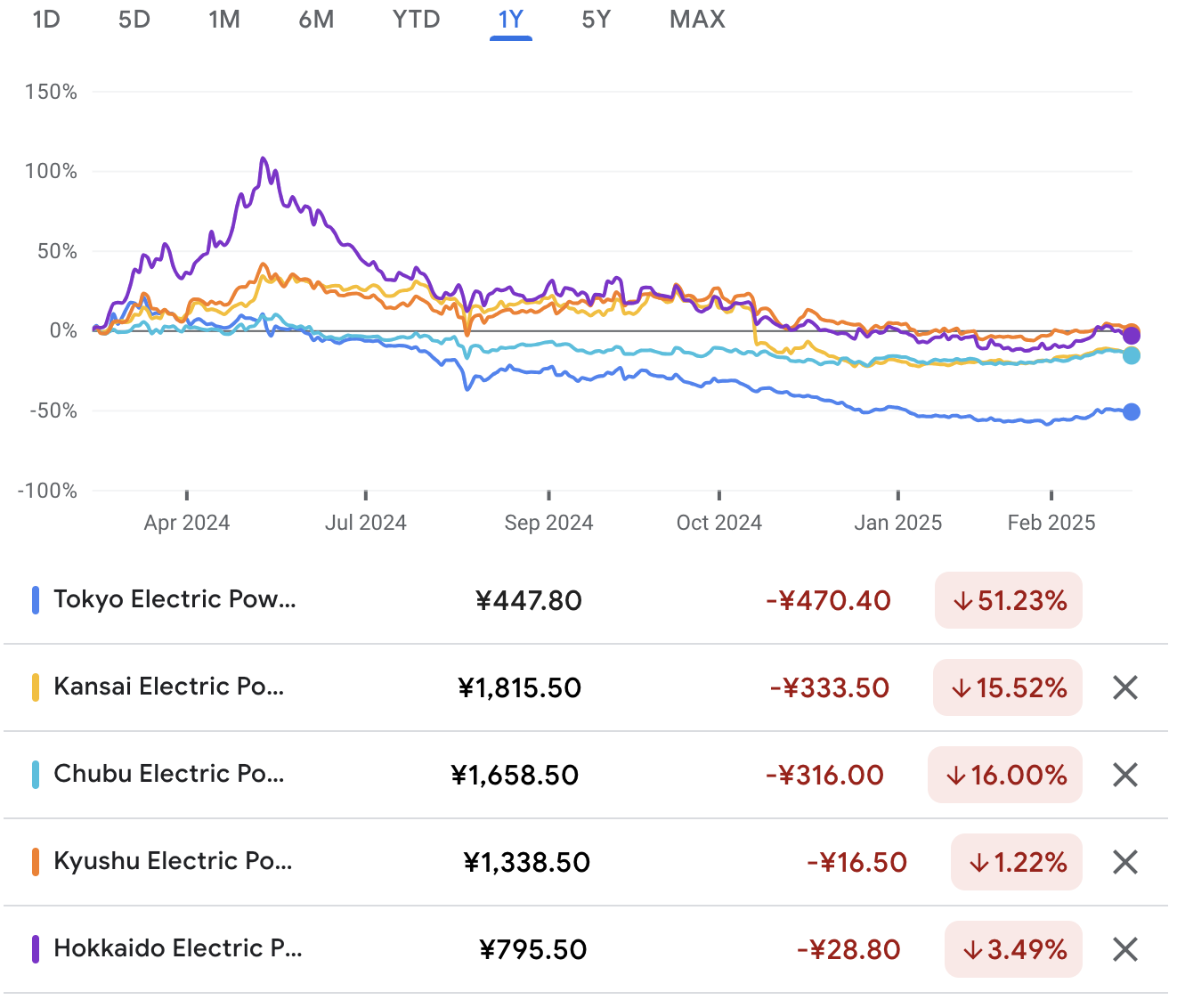

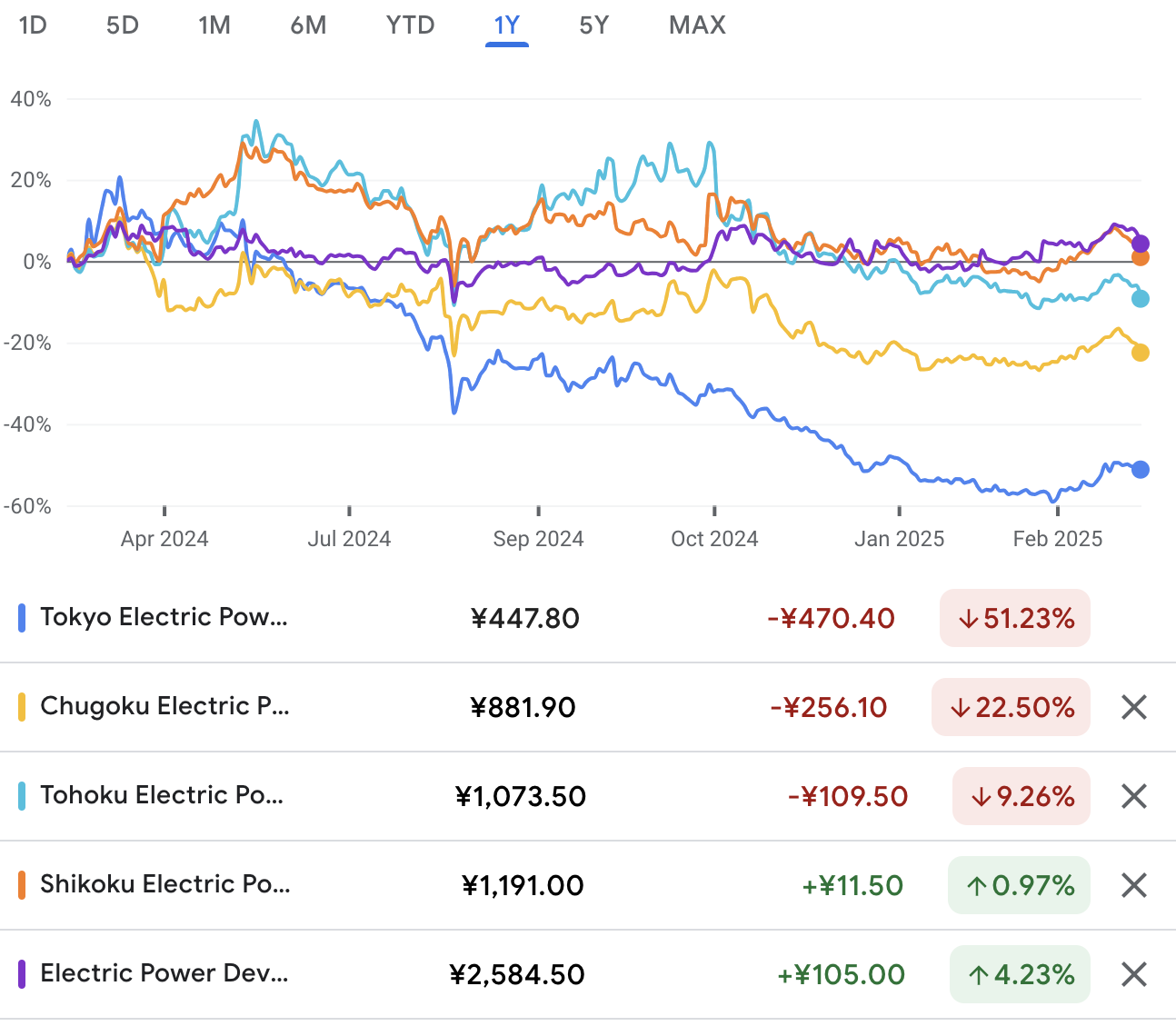

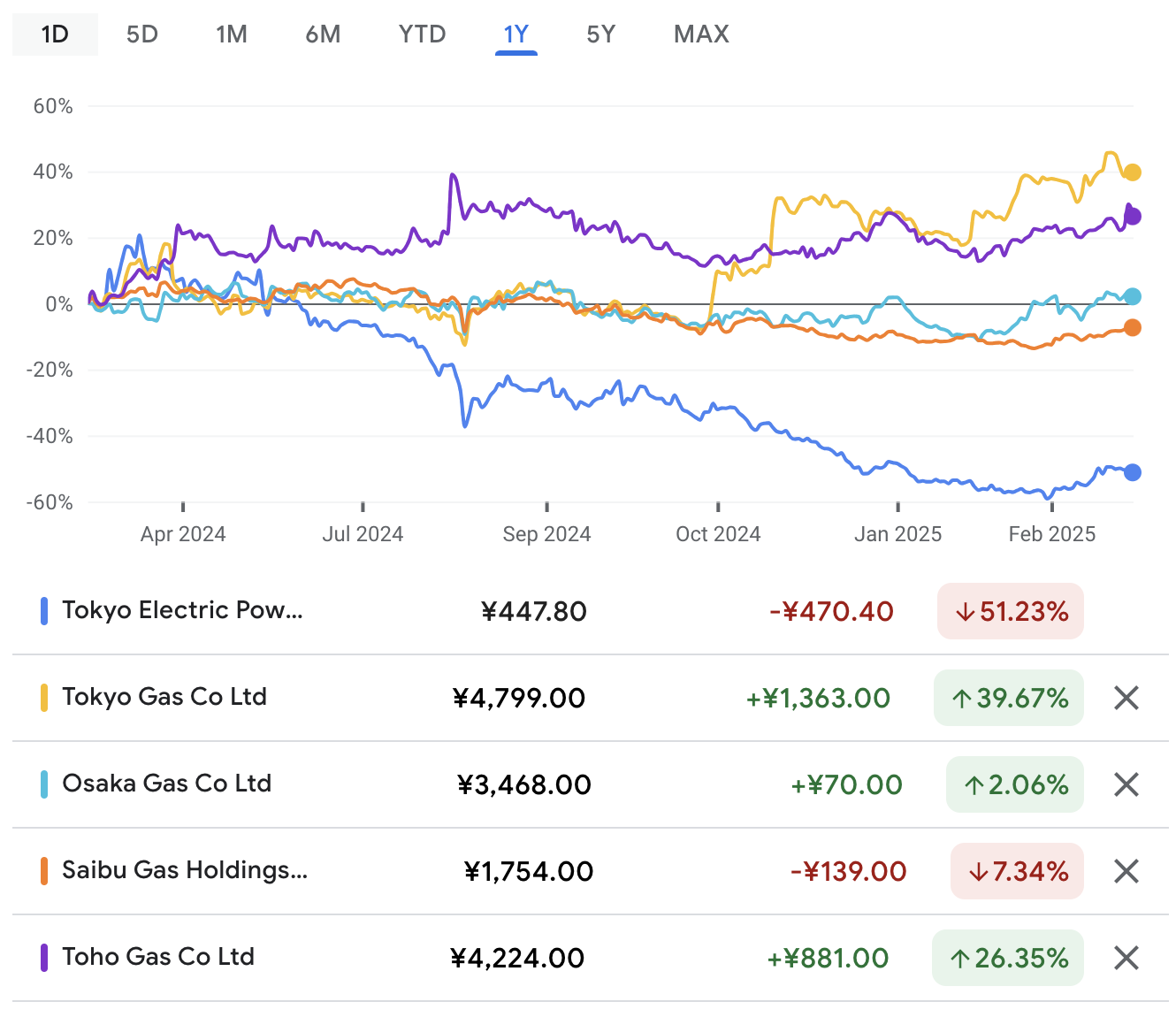

Japan’s Electricity Companies Are Cheap and Getting Cheaper

Japanese firms are the cheapest electricity stocks in the G7 — and the gap in market values is widening.

The average major electricity company in Japan is worth 10 times less than one in Europe, and 1/15th the value of one in the U.S., according to a review by Japan NRG. The market capitalization of the top American utility, NextEra Energy, is enough to buy all 10 Japanese regional power holdings — as well as the country’s top electricity wholesaler — three times over.

The differences are not due to the size of generation assets. NextEra Energy has only about 12% more capacity than TEPCO Holdings, the main supplier to the Tokyo area, but it’s 30x more valuable. NuScale Power, a U.S. firm that has yet to build a single working reactor, is worth 30% more than Kyushu Electric, utility with four reactors (total capacity 4.14 GW) online today, as well as dozens of thermal and renewables assets.

In the past twelve months, this divergence has accelerated with Japanese power utility stocks losing value, despite lower fuel costs, while peers in Europe and the U.S. gained. This potentially makes Japanese firms more of a target for M&A as well as significantly hindering their fund-raising capabilities at a time when investments in the grid and clean energy are imperative.

Top 10 Power Utilities in Each Region*

U.S. Firms | MCAP (USD) | European Firms | MCAP (USD) | Japanese Firms | MCAP (USD) |

NextEra Energy | 141.05 | Iberdrola | 100.2 | Tokyo Electric | 4.8 |

Southern Co | 96.22 | Enel | 79.4 | Kansai Electric | 13.6 |

Duke Energy | 90.13 | SSE | 18.4 | Chubu Electric | 8.5 |

Constellation Energy | 71.08 | Terna | 18.0 | Tohoku Electric | 3.7 |

American Electric | 54.7 | EDP | 13.9 | Kyushu Electric | 4.3 |

Dominion Energy | 45.03 | Endesa | 26.3 | Shikoku Electric | 1.7 |

Vistra | 44.84 | Redeia | 10.4 | Chugoku Electric | 2.3 |

Sempra | 45.02 | Fortum | 15.0 | Hokkaido Electric | 1.1 |

Exelon | 43.17 | Orsted | 144.1 | Hokuriku Electric | 1.3 |

Xcel Energy | 39.03 | Verbund | 12.2 | J-Power | 3.2 |

TOTAL | 670.3 |

| 437.7 | 44.5 | |

AVERAGE | 67.0 | 43.8 | 4.5 |

* Stock prices as of March 26, 2025, at the close of Japan trading day. All stock price data taken from public exchanges and other open public sources. The currency conversations – as per public sources on March 26, 2025 – were 1 USD = 1.08 EUR and 1 USD = 0.0066 JPY.

NOTE ON METHODOLOGY: Companies selected based on featuring as the top 10 constituents of sector-relevant indices in each region. In the U.S., we used the S&P’s Dow Jones U.S. Utilities Index. In Europe, it was the STOXX Europe Total Market Electricity Index, although consideration was also made for the larger STOXX Europe 600 Utilities index. In Japan, we referred to the Japan Exchange Group’s Electric Power & Gas sector index and to the Topix-17 Electric Power & Gas index, picking out the largest 10 regional EPCOs but replacing Okinawa Electric with J-Power.

1-Year Stock performance*

*NOTE: Due to publication of this article in today’s, March 31, 2025 edition of Japan NRG, the below graphs actually cover the period of one day less than a full year. They show performance for April 1, 2024 to March 28, 2025.

U.S. MARKET

S&P’s Dow Jones U.S. Utilities Index (White) vs S&P’s 500 Index (Blue)

Year-on-Year Return: 19.2%

- U.S. utility stocks enjoyed a robust rally over the past year, easily outperforming their global peers. The S&P 500 Utilities sector index climbed roughly +20% in price from a year ago and as much as +25–27% total return including dividends. This surge made utilities one of the best-performing S&P 500 sectors in the timeframe.

- Drivers:

- As the Federal Reserve paused and eventually began signaling rate cuts, bond yields stabilized or fell from 2023 highs. This made the utilities’ relatively high dividend yields attractive again, sparking investor interest in defensive, income-producing stocks.

- Unlike in Europe, the U.S. economic outlook in late 2024 included some growth concerns (raising recession odds) – this actually helped utilities, as investors rotated into defensives in anticipation of a slowdown

- Company-specific boosts included NextEra raising dividends, Consolidated Edison selling non-core assets, and Duke Energy streamlined operations by exiting foreign markets

EUROPEAN MARKET

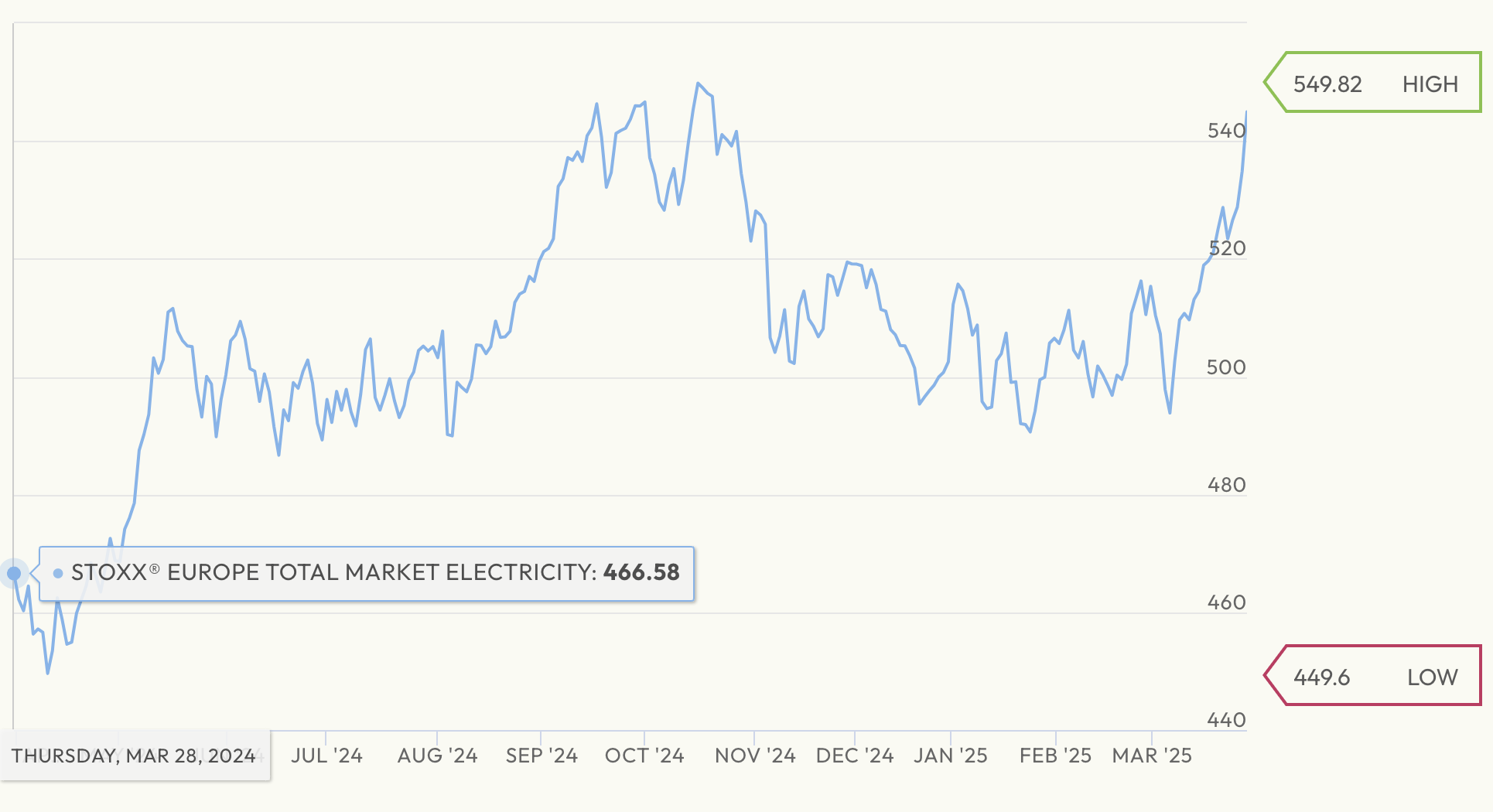

Europe Total Market Electricity Index

Year-on-Year Return: 16.8%

STOXX Europe 600 Utilities Index

STOXX Europe 600 Utilities Index

Year-on-Year Return: 13.9%

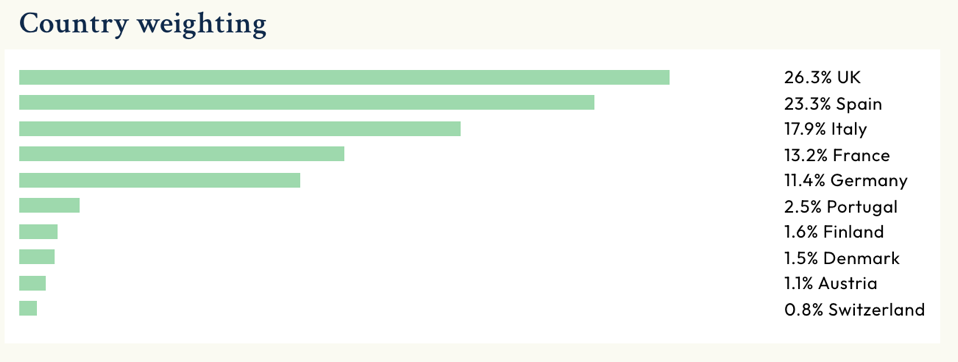

Country Weighting in the STOXX Europe 600 Utilities Index

Country Weighting in the STOXX Europe 600 Utilities Index

Source: Stoxx

- European utility stocks have been rocked by a number of factors over the past year, both in terms of the region’s macro outlook and global energy policy turbulence. Still, a recent rally in Europe pushed the biggest utility index, the STOXX Europe 600 Utilities, close to the YoY gains of the U.S. market as Germany’s willingness to relax its debt ceiling and optimism on trade led gains.

- Drivers:

- Unlike the U.S., Europe’s rate hikes persisted through 2023 (ECB rates peaked in mid-2024), which raised borrowing costs for utilities (typically heavy debt issuers) and made their high dividends less attractive. When the outlook shifted to economic recovery and central banks began signaling rate cuts, investors rotated away from defensives like utilities toward cyclicals.

- Fuel prices, especially for natural gas, stabilized in 2024 and even receded in the latter half of the year thanks also to a milder winter 2023/24. This led to lower input costs but also lower retail prices, reducing revenues at a time when some of the European energy firms were still dealing with windfall profit taxes and price caps.

- EU policy support for green energy (e.g. faster permits for renewables, EU Green Deal investments) benefited utilities pivoting to wind/solar. And while firms such as Orsted faced setbacks on large offshore wind projects due to higher costs and financing challenges, European governments started to raise the subsidies offered via capacity auctions.

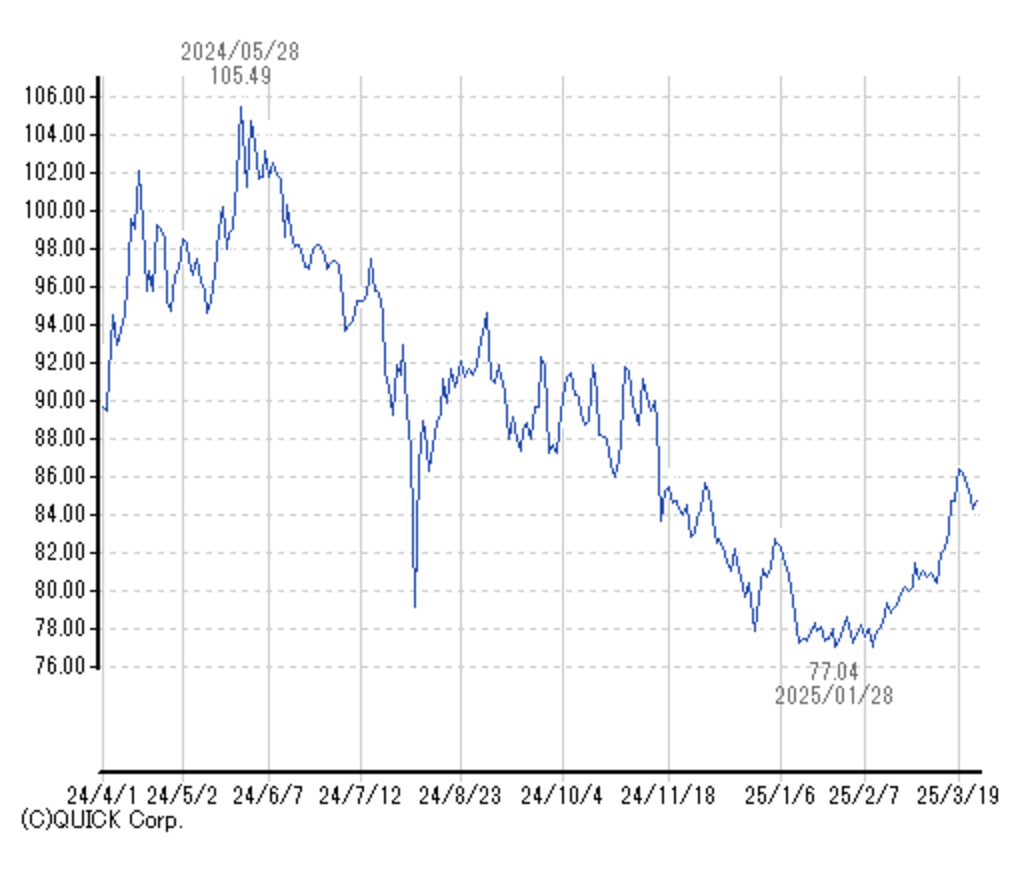

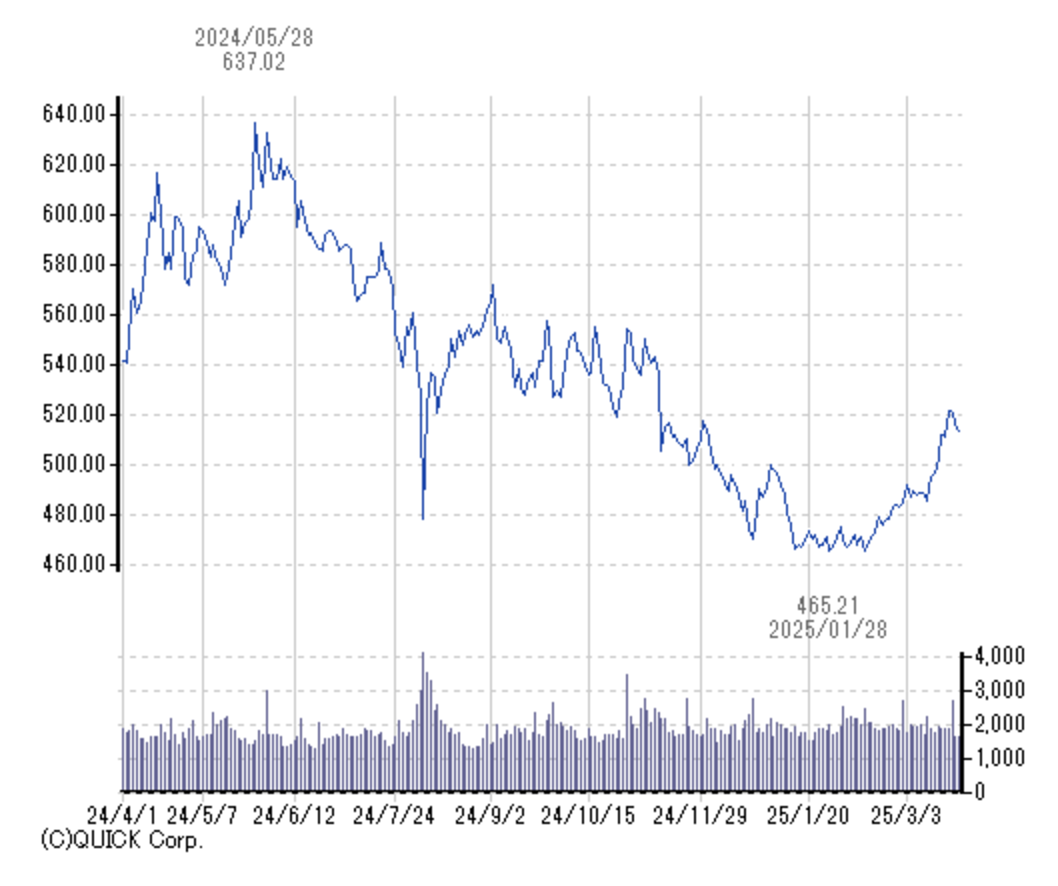

JAPANESE MARKET

Year-on-Year Return: -5.5%

TOPIX-17 Electric Power & Gas Index

TOPIX-17 Electric Power & Gas Index

Year-on-Year Return: -5.4%

JPX Electric Power & Gas Index

- Japanese utilities had a bad year, with nearly all EPCOs losing value over the past 12 months. One major headwind for power indices has been the performance of Tokyo Electric (TEPCO), which has lost about half of its value in the last year due to the further deterioration of its financial condition. Still, TEPCO is not the only utility to suffer in the past 12 months. The shares of Kansai Electric, now Japan’s most valuable power company, are down 14% YoY despite the utility operating all of its nuclear reactors. Other large power firms also saw double-digit drops with only Shikoku Electric and J-Power (previously known as Electric Power Development Co) able to post a positive return. The Nikkei 225 Index is down 7.6% in the past 12 months – less than the drop for most power utilities.

- Drivers:

- Oddly enough, most of the drivers for EPCOs are positive, which makes their share performance even stranger. The introduction of favorable wheeling charges and changes to the Balancing Market rules are expected to improve the profitability of the major power companies, which control about 80% of the electricity supply in Japan.

- Fuel costs declined during 2024: LNG prices in yen terms were down 1.5% YoY and thermal coal prices down 6.2% in January while the dollar-yen exchange was largely unchanged at about ¥150. Meanwhile, most of the EPCOs raised rates in March 2025.

- The big drag on the sector remains TEPCO. Tokyo’s main utility is unable to restart its only operable nuclear power plant while continuing to pay out vast sums each year for decommissioning work at the Fukushima Daiichi NPP and for disaster compensation. Earlier this month, TEPCO published a new business plan that forecasts a ¥960 billion shortfall over the next two years despite an expectation that profit will double. The erosion of TEPCO’s capital base is at a level where it continues to operate solely at the discretion of the state. The government took a controlling stake after the Fukushima disaster.

The power sector’s performance contrasts with that of gas utilities. Tokyo Gas has shot up by 40% YoY thanks to an expanded shareholder returns policy and an investment in the company by the activist fund Elliott Management. But other large gas firms have recorded positive growth on the back of improving financials and expectations of higher demand for the fuel from industry.

The power sector’s performance contrasts with that of gas utilities. Tokyo Gas has shot up by 40% YoY thanks to an expanded shareholder returns policy and an investment in the company by the activist fund Elliott Management. But other large gas firms have recorded positive growth on the back of improving financials and expectations of higher demand for the fuel from industry.

Japan Power Sector Outlook

The Bank of Japan is due to raise rates even further this year, which traditionally would have been a drag on power stocks as utilities tend to raise capital through bond sales. However, the arrival of higher rates is helping to revive investor appetite for utility bonds, which until now offered miserly returns.

What’s more, power companies may be willing to switch their capital raising to equity. Kansai Electric raised over ¥379 billion through a secondary share offering in November 2024, seeking capital for investments in data centers, renewables assets and overseas operations. That’s an unusual move in the sector and may now be echoed at other companies.

The biggest event in the sector remains the often-promised initial public offering by JERA, the top utility by generation capacity and the biggest Japanese importer of LNG. As JERA approaches investors, however, it hopes to persuade them that its valuation should be based in reference to utilities overseas rather than domestic peers.

Asia Energy Review

BY JOHN VAROLI

A brief overview of the region’s main energy events from the past week

Australia / Green hydrogen

Australia will inject $511 million into the 1.5 GW Murchison Green Hydrogen project that is led by Copenhagen Infrastructure Partners (Denmark).

Australia / Solar power

Danish renewable energy developer, European Energy, inaugurated a 58 MW solar PV plant and started construction of a second project, a 106 MW solar park, in Victoria, Australia.

China / Power regulation

Nvidia’s business in China might suffer if Beijing implements energy efficiency rules more strictly. The National Development and Reform Commission is advising Chinese groups to use chips that meet stricter requirements in new data centers.

India / Coal

On March 20, India’s coal production reached one billion tons, which is 11 days ahead of last fiscal year’s total output of 998 Mt, said the Coal Ministry. Coal accounts for 55% of India’s energy mix, with 74% of electricity generated from coal-based power plants.

India / Power transmission

Adani Energy Solutions has won a $3.2 billion power transmission project in Gujarat to supply green electrons for manufacturing green hydrogen and green ammonia.

India / Thermal power

The State of Odisha plans to add 10 GW of thermal power capacity in the next six years. The state currently has 20 GW of operational capacity.

Indonesia / Energy transition

Funding isn’t an issue for the energy transition; the problem is project viability, said Elrika Hamdi, deputy head of the Just Energy Transition Partnership. State electricity firm PLN slowed renewables deployment. Investors should back captive power instead of grid-based projects, she added.

Malaysia / Oil & Gas

A $230 million bailout of Sapura Energy, a major oil and gas services company, has triggered a debate over PM Ibrahim’s pledge to end bailouts of troubled companies using public funds.

Philippines / Solar power

Taiwan-based Giga Solar Materials Corp, through its renewable energy subsidiary, Wholesun Energy, has partnered with Wyn Power Corp to develop a 50-MW solar farm in Batangas.

Singapore / Methanol bunkering

Following finalization of the methanol bunkering licensing framework and standards, the Maritime and Port Authority has opened applications for licensees to supply methanol as a marine fuel.

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Hulic Ochanomizu Bldg. 3F, 2-3-11, Surugadai, Kanda, Chiyoda-ku, Tokyo, Japan, 101-0062.