WEEKLY

APRIL 14, 2025

ANALYSIS

WHAT CAN JAPAN’S OFFSHORE WIND SECTOR LEARN FROM OTHER ASIAN COUNTRIES?

- Once seen as one of Asia’s most promising offshore wind markets, Japan is at risk of losing momentum. A complicated auction system and concerns over financial feasibility have made Japan less attractive.

- In contrast, Taiwan and South Korea have had more success in advancing their offshore wind sectors.

FROM IMPORTER TO TRADER: LNG ACTIVITY GROWS DESPITE SHRINKING DOMESTIC DEMAND

- Japan is experiencing a dramatic shift in its energy landscape. LNG imports have been on a downward trend in the past several years due to shrinking domestic demand, and this looks set to continue.

- Major Japanese players are adapting, with ambitions to become key traders in LNG markets across Asia.

ASIA PACIFIC REVIEW

This column provides a brief overview of the region’s main energy events from the past week

NEWS

- China tightens rare-earth export controls, posing risk to Japan’s supply chains

- Kansai Electric raises ¥30 bln via transition bonds for nuclear, hydrogen projects

- TEPCO registers hydrogen system as a primary source for grid balancing; a Japan first

- Capacity market reduces penalties for the power generation side

- Singapore’s Sembcorp to double stake in Senoko, co-owned by Japan’s Lion Power

- JERA, Mitsui & CF Industries to build world’s largest ammonia plant

- Rio Tinto, Mitsubishi, others launch hydrogen-based ironmaking demo plant

- Cement maker to test ammonia-only burner

- Approvals for 80,000 inactive solar projects now revoked

- METI to require rooftop solar targets in energy plans, promoting more adoption

- PowerX secures large order for flagship BESS units

WIND POWER AND OTHER RENEWABLES

- MoE opinion on Happo-Noshiro offshore wind farm

- Eurus Energy plans onshore wind farms

- CNSN approves building Hitachi’s SMR in Canada

- Sumitomo signs MoU with U.S. fusion startup

- Global LNG prices to remain high until at least 2028, says Trafigura CEO

- Osaka Gas expands aggressively into India’s city gas and renewables market

CARBON CAPTURE & SYNTHETIC FUELS

- NYK to build methanol-fueled carrier for Idemitsu

- Tokyo to back use of domestically produced SAF

EVENTS

May 3-6 May Golden Week Holidays

June 4-5 Kyushu Innovation Week / Kyushu GX Decarbonization Expo @ Marine Messe Fukuoka

June 4-6 AXIA EXPO 2025 (Hydrogen and Ammonia Next-Generation Energy Exhibition) @ Aichi Sky Expo

June 15-17 G7 Summit @ Kananaskis, Alberta, Canada

APRIL 14, 2025 & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Chief Editor)

John Varoli (Senior Editor, Americas)

Kyoko Fukuda (Data, Events)

Magdalena Osumi (Renewables & Storage)

Filippo Pedretti (Thermal, CCS, Nuclear)

Tetsuji Tomita (Power Market, Hydrogen)

George Hoffman (Sales, Business Development)

Tim Young (Design)

NEWS: GENERAL POLICY AND TRENDS

China tightens rare-earth export controls, posing risk to Japan’s supply chains

(Nikkei, April 9)

- China has expanded export restrictions on seven additional rare earths, including dysprosium and terbium that are used in EVs and advanced magnets, significantly impacting supply chains for Japanese high-tech sectors.

- Japan and the U.S. together account for 53% of China’s rare-earth exports, making them primary targets of the tightened controls. With these restrictions, procurement delays are already reported as approvals slow down.

- CONTEXT: Amid China’s geopolitical leverage, Japan is accelerating efforts to diversify its rare-earth sourcing. In March, Tokyo announced a €100 million investment in a French rare-earth refining venture to reduce reliance on Chinese processing. Japan also invested in Australian rare-earth projects in the past decade.

- China’s tighter controls follow its 2024 move declaring rare-earth resources state-owned, consolidating their processing strictly within state-backed companies.

TAKEAWAY: This pause raises concerns for Japan’s long-term security in tech sectors. The U.S. is China’s main target with the latest restrictions, and it might ease the restrictions towards Japan as a way to drive a wedge in relations with Washington. Securing supply without hurting relations with either China or the U.S. will be a conundrum for PM Ishiba.

Kansai Electric raises ¥30 bln via transition bonds for nuclear, hydrogen projects

(Company disclosure, April 10)

- KEPCO issued ¥30.7 billion ($200 million) in transition bonds to finance NPP safety upgrades and next-gen fuel projects, including hydrogen.

- The bonds have maturities of 10 and 20 years, with interest rates of 1.766% and 2.367%, respectively; this marks KEPCO’s second set of transition bond issuance following a ¥45 billion offering in July 2022.

- Funds will also support upgrades at existing thermal power plants, such as the Nanko Power Plant in Osaka, in response to rising power demand driven by AI adoption.

- The bond sales were managed by Daiwa and Nomura securities firms, among others.

TAKEAWAY: Transition bonds are a subset of ESG bonds. Last year’s ¥20 billion issuance of transition bonds by JAL was six times oversubscribed. Transition finance is of more interest in Japan than in other markets because many local companies seek capital for energy sources other than renewables. While these projects are important to cutting emissions, and thus consistent with limiting global warming according to the Climate Bonds Initiative, which monitors the integrity of bond issuances, international investors tend to shy away from transition bonds in favor of green finance. It’s interesting to note that KEPCO’s second issuance of transition bonds is smaller than the first one in 2022, but still sizable.

Mitsubishi HC Capital and Sanei to generate J-Credits from solar clients

(Company statement, April 9)

- Mitsubishi HC Capital and Sanei have launched a project that will generate J-Credits based on adoption of solar power.

- The companies will aggregate the CO2 reductions of companies and households that install Sanei’s solar power systems and convert them into J-Credits.

- The first certification, scheduled for March 2026, is expected to generate approx. 100 tons of credits. By 2030, the project aims to create about 900 tons of carbon credits.

- CONTEXT: Japan plans to achieve 15 Mt of its 2030 GHG reduction target through the use of J-Credits.

MoE offers subsidies for firms that lease equipment for decarbonization

(Government statement, April 10)

- The MoE said applications are now open for designated leasing providers and exemplary initiatives under the FY2025 ESG Lease Promotion Program, which supports decarbonization efforts through subsidies for leasing low-carbon equipment.

- More information can be found here.

Toyo to appeal fine imposed in Brazil on bribery suspicion

(Company statement, media reports, April 8)

- Toyo Engineering will file an objection with Brazil’s comptroller general’s office responsible for anti-corruption, after the agency imposed a fine of 560 million reais (about ¥14 billion, or $140 million) on suspicion of bribery.

- Toyo said it was not involved in any wrongdoing. The issue involves a project awarded in 2011 to a consortium that included a Toyo Engineering subsidiary. The project was for construction at a petrochemical complex in Rio de Janeiro state, commissioned by Petrobras.

- Authorities suspect Toyo paid a bribe equal to 1% of the contract to Petrobras execs.

NEWS: ELECTRICITY MARKETS

TEPCO to trial hydrogen production for balancing the power grid

(Nikkei, April 10)

- TEPCO HD plans to trial using hydrogen production systems as a rapid-response mechanism for balancing the grid, especially at times of excess solar generation. The company joined the Balancing Market in April.

- TEPCO is partnering with Yamanashi Pref at a Kofu City facility to test how well electrolyzer-based hydrogen systems work as a “demand adjustment valve.” The project is the first in Japan to register hydrogen equipment as a primary adjustment power source (i.e., it must respond within 30 seconds of receiving instructions.)

- The partners have three electrolysers at the Kofu site that can be used for balancing. Each one requires 500 kW of power.

- CONTEXT: TEPCO, Totay Industries, and Yamanashi Pref last year established the Yamanashi Hydrogen Company (YHC) to develop and operate P2G (Power to Gas) systems. The facilities use renewable energy to power electrolyzers that make hydrogen. YHC is also engaged in the storage and transportation of hydrogen.

TAKEAWAY: If successful, TEPCO could turn to hydrogen systems as an alternative to thermal power plants as a regulating power source. PEM electrolyzers are the most responsive of hydrogen-production facilities and have performed well in tests so far. The issue for TEPCO to tackle will be how to operate the electrolyzer systems at scale and ensure that cost remains reasonable even as the equipment is used sporadically.

JEPX spot electricity market marks 20 years, trading volume up 300-fold since launch

(Denki Shimbun, April 8)

- The Japan Electric Power Exchange (JEPX), which began electricity trading in April 2005, celebrated its 20th anniversary, with annual trading volumes increasing nearly 300-fold to about 30% of Japan’s total electricity demand.

- JEPX membership has grown from an initial 27 companies to 320 today, passing the 100-member milestone in 2015, driven by liberalization and new market entrants.

- JEPX, which is is upgrading its transaction systems and organizational capabilities, has maintained consistent trading rules, providing stable power procurement channels for new market entrants (shin denryoku, 新電力, or PPS).

Capacity market reduces penalties for the power generation side

(Denki Shimbun, April 10)

- OCCTO has decided to reduce economic penalties in the capacity market.

- The assumed occurrence time for ‘capacity provision notices’, a factor determining the penalty amount, has been changed from the current 30 hours to 90 hours. Thus, the penalty will be lowered.

- CONTEXT: The frequency of provision notices has increased and the burden on power plant operators grew after FY2024.

- If it’s expected that the wide-area reserve rate will fall below 8% after 6 PM the day before consumption, a ‘capacity provision notice’ is issued to operators who have signed capacity assurance contracts. The notified power plants are required to operate and bid in the spot market, among other obligations.

- Penalties are calculated by multiplying the capacity that did not bid, despite receiving the notice, by a certain ratio (penalty rate). That rate is based on the expected hours in which the wide-area reserve rate is anticipated to be below 8%.

Singapore’s Sembcorp to double stake in Senoko, co-owned by Japan’s Lion Power

(The Straits Times, other media, April 2)

- Sembcorp Industries, a Singaporean state-owned energy firm, signed a sale and purchase agreement that will increase its interest in local electric utility firm Senoko Energy to a maximum of 70%.

- Sembcorp will acquire up to 57.1% in Lion Power, which holds a 70% interest in Senoko Energy.

- Lion Power is owned by a JV comprising Marubeni, KPIC Netherlands, Kyuden International and Japan Bank for International Cooperation. Marubeni holds the remaining 42.9% interest in Lion Power.

- CONTEXT: Lion Power specializes in the design and manufacturing of automated systems and medical devices. Their product lineup includes robot systems, measurement systems and electronics-applied devices.

Eurus Energy launches renewable energy aggregation service

(Company statement, April 4)

- Eurus Energy launched a new integrated power sales support and aggregation service for renewable energy sources.

- The service enables the firm to purchase electricity generated from domestic onshore wind and solar power plants, and manage everything from power supply planning to sales to end-users, retailers, and wholesale electricity markets.

- CONTEXT: On April 1, Eurus Energy merged with Terras Energy, bringing Terras’s ReEra virtual power plant platform into the business. This maximizes the value of the battery storage assets by managing them in tandem with generation assets.

NEWS: HYDROGEN

JERA, Mitsui & CF Industries to build world’s largest ammonia plant

(Company statement, April 10)

- JERA, Mitsui & Co, and CF Industries will build a $4 billion (¥590 billion) ammonia plant in Louisiana, set to begin operations in 2029. The plant will produce 1.4 million tons of ammonia annually, the world’s largest.

- The product made from natural gas, with CO2 sequestered using CCS tech, will be exported to Asia and Europe, mainly for fuel in power generation and shipping.

- JERA will contribute 35% of the total cost and offtake the ammonia.

TAKEAWAY: JERA struck an initial agreement with CF after the initial MoU signed in 2022 on the back of a tender for ammonia supply to Japan. Since then, JERA has broadened horizons and now sees potential to sell ammonia not only in the domestic market. The power utility operates thermal power plants across the world and sees the potential to bring co-firing technology to Southeast Asia, North America, and elsewhere. While other companies have shied away from banking on clean ammonia outside of its traditional use in fertilizers, JERA is determined to establish ammonia as the next-gen fuel for dispatchable power plants.

- SIDE DEVELOPMENT:

- Tsubame BHB and Atvos to launch green ammonia project in Brazil

- (Company statement, April 10)

- Japan’s Tsubame BHB and Brazil’s Atvos signed a letter of intent to produce green aqueous ammonia in Mineiros, Goiás, from 2027. The plant will produce 20,000 tons of green ammonia annually.

- Brazil’s strong renewable energy and high fertilizer demand make it ideal for onsite decentralized ammonia production, according to Atvos. The companies signed the deal during the Brazilian president’s visit to Japan in late March.

- CONTEXT: Aqueous ammonia has lower nitrogen content and is easier to handle for farmers compared to the more widely available anhydrous ammonia (i.e. pure ammonia, without water solution).

Primetals, Rio Tinto and Mitsubishi launch hydrogen-based ironmaking demo plant

(Company statement, April 8)

- Primetals Technologies, voestalpine, Rio Tinto, and Mitsubishi Corp launched a hydrogen-based ironmaking demo plant in Austria.

- It integrates HYFOR (Hydrogen-based Fine Ore Reduction) with an electric smelter, producing hot briquetted iron, hot metal, and pig iron.

- The demo plant is set to begin operations in 2027.

- CONTEXT: HYFOR is the first direct reduction process that uses iron ore without pelletizing. The smelter uses renewable energy to melt the direct reduced iron.

TAKEAWAY: Reduced Iron is particularly needed, for example, for high-grade coal used in car production. Steel-making is a ”hard-to-abate” sector: hence, the industry is eager for advancements in CO2-reduction technology.

KHI wins order for gas engines converted to hydrogen co-firing

(Company statement, April 9)

- Kawasaki Heavy Industries (KHI) received an order for two 8 MW class gas engines to upgrade a system at Nitto Boseki’s Fukuyama Business Center.

- This plant has the world’s highest power generation efficiency of 51% for its class, and future modifications will allow mixing hydrogen with city gas in any ratio up to 30% by volume.

- CONTEXT: This project involves replacing two 5 MW class gas engine cogeneration systems delivered by KHI in 2014.

- SIDE DEVELOPMENT:

- Nikkiso wins KHI pump unit order for hydrogen fuel ship

- (Company statement, April 7)

- Nikkiso won a pump unit order for a hydrogen fuel ship from KHI.

- This pump supplies high-pressure hydrogen to large, low-speed two-stroke hydrogen fuel engines. It was designed and made by combining the technologies of products for LNG-fueled ships and hydrogen stations, and is scheduled for delivery in 2026.

- CONTEXT: The project to develop a hydrogen-fueled ship is part of Next-generation Ship Development under the Green Innovation Fund. That is carried out by KHI, Yanmar Power Technology, and Japan Engine.

Chugai Ro supplies ammonia-only burner for test at cement plant

(Company statement, April 8)

- Chugai Ro delivered an ammonia-only burner to UBE Mitsubishi Cement.

- The goal is to reduce CO2 emissions by using ammonia, a clean-burning fuel, as an alternative to pulverized coal, which has traditionally been used as a heat source. This will be a world first for cement production.

- CONTEXT: In January, UBE Mitsubishi Cement began a test using ammonia at the Ube Cement Plant in Ube City, Yamaguchi. The goal is to replace 30% of the coal-fired thermal energy with ammonia.

IHI provides decarbonized electricity generated by ammonia for Osaka Expo

(Company statement, April 11)

- IHI began CO2-free ammonia power generation for the Osaka Expo 2025.

- CONTEXT: In 2022, IHI, together with Tohoku University and AIST, demonstrated CO2-free power generation using a gas turbine that uses 100% liquid ammonia.

- SIDE DEVELOPMENT:

- NTT Anode Energy and Panasonic install hydrogen supply network at Osaka Expo

- NTT Anode Energy and Panasonic installed a hydrogen supply chain model system at the Osaka Expo to power Panasonic hydrogen fuel cells at both pavilions.

- CONTEXT: NTT Anode Energy and Panasonic are lead supporters of the Osaka Expo. (For more details, see the Analysis section of Japan NRG’s April 7 issue).

NEWS: SOLAR AND BATTERIES

Japan revokes approvals for 80,000 inactive solar projects

(Sankei Shimbun, April 5)

- Between FY2022 and FY2024, the govt revoked certification for about 80,000 non-operational solar power projects that were approved under the FIT system but failed to launch.

- Some developers exploited loopholes, securing approvals when purchase prices were high and delaying operations to maximize profits when equipment costs fell.

- CONTEXT: Many stalled projects dated to the early years of the FIT (2012–2014), and some were backed by foreign investors.

TAKEAWAY: The move by the govt aims to promote a healthier solar industry by clearing out inactive or speculative operators, and encouraging new, active ones. This decision is expected to help avoid up to ¥4 trillion in additional costs that would have been passed on to consumers through renewable energy surcharges.

METI to require rooftop solar targets in energy plans

(Company statement, April 3)

- To promote the use of rooftop solar power systems, METI/ ANRE propose energy-intensive businesses to include solar installation targets in their mid- to long-term energy plans, starting FY2026.

- Businesses will also be required to provide details on the roof area, seismic standards, and load-bearing capacity of designated facilities.

- SIDE DEVELOPMENT:

- MoE calls for subsidy applications for community-based solar power systems

- (Government statement, April 8)

- MoE announced a call for applications for a subsidy program supporting the installation of community-based solar power systems tailored to local conditions.

- Applications are accepted until May 8, 2025. More information here.

Trina Solar’s Japan branch and Equinix partner on first renewables PPA

(Company statement, April 1)

- Trina Solar Japan Energy, a branch of Chinese PV firm Trina Solar, said it inked a solar PPA with Equinix, a global data center operator.

- Equinix will receive 30 MW of energy from a solar project in Abira, Hokkaido. The project is set to begin in 2028 and will supply power to Equinix for 20 years.

- This is Equinix’s first renewable energy PPA in Japan, one of the most challenging markets for sourcing renewable energy, according to RE100 members.

- CONTEXT: Equinix already achieved 100% renewable energy procurement for its operations in Japan. However, this deal is expected to enhance the quality of its renewable energy sourcing by adding new capacity to the Japanese power grid.

Tokyo Century to build grid-scale battery storage in Nagasaki City

(Company statement, April 8)

- Tokyo Century will build a grid-scale battery in Nagasaki City, Kyushu Pref. with an output of 15.6 MW and a storage capacity of 64 MWh.

- This project will be developed without any subsidies, a first for the company. Launch is targeted for FY2028.

- The facility will participate in the wholesale, capacity, and balancing markets.

- CONTEXT: The Kyushu area might post a 6.1% renewable energy curtailment rate in FY2024, which ended in March. Grid-scale batteries are needed to provide flexibility. Tokyo Century seeks to develop 300 MW of grid-scale battery storage.

PowerX secures order for 32 units of flagship BESS

(Company statement, April 8)

- PowerX secured an order to supply 32 units of its “Mega Power” battery storage systems for a large-scale grid storage project in Memuro Town, Hokkaido.

- The systems will provide a total storage capacity of 79 MWh and a maximum capacity of 20 MW, with operations to begin in FY2027.

- The project is developed by a JV backed by Tokyo Century and JFE Engineering. The site, adjacent to the Kitamemuro substation, was secured through a land lease granted by Hokkaido Electric Power Network.

- CONTEXT: The project will help stabilize Hokkaido’s supply-demand balance, where both power generation, such as offshore wind projects, and electricity demand from new semiconductor plants and data centers, are expected to grow.

- SIDE DEVELOPMENT:

- JAL partners with PowerX to sell strawberries grown only with renewables

- (Company statement, April 11)

- Starting in July, PowerX batteries will be installed at the JAL Agriport farm in Narita to store solar power, which will be used for greenhouse operations.

- The project will grow and sell strawberries.

TAKEAWAY: Battery storage is making agrisolar a viable and scalable solution by enabling stable, round-the-clock use of solar power for controlled farming. This is especially valuable in a land-scarce country like Japan.

Looop launches BESS, firm’s first grid-scale project

(Company statement, April 3)

- Power retailer Looop launched commercial operations at a grid-connected battery storage facility in Ogawa Town, Saitama Pref. It has a total storage capacity of around 7.68 MWh.

- This marks Looop’s first investment in a grid-scale storage project.

- Looop is already active on the wholesale electricity market, and seeks to participate in the capacity and balancing markets to expand revenue.

- SIDE DEVELOPMENT:

- TESS to build 22 MW grid-connected storage in Shizuoka

- (Company statement, March 31)

- TESS Engineering will develop a 22 MW grid-connected battery storage facility in Kikugawa City, Shizuoka Pref.

- The project is scheduled for completion by March 2027.

- CONTEXT: The project was awarded under the FY2023 Long-Term Decarbonized Power Sources Auction.

Sekisui Chemical to install PSCs at public facilities in Fukushima

(Company statement, March 31)

- Sekisui Chemical and its subsidiary Sekisui Solar Film, which makes perovskite solar cells (PSCs), will join a research project led by Fukushima Pref.

- PSC panels will be installed at public facilities to assess feasibility and performance.

- This initiative is part of the Fukushima Plan for a New Energy Society to explore the potential for deploying lightweight, flexible solar tech, particularly in areas with limited load capacity like rooftops, walls, and curved surfaces.

- The generated electricity will power equipment such as batteries and digital signage. The project will test suitability of installation sites, mounting methods, etc.

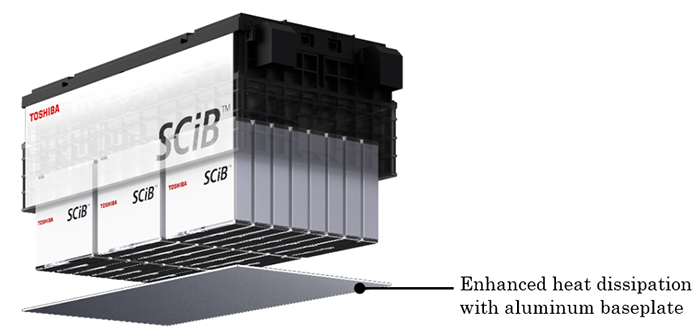

Toshiba launches Li-ion module with double the heat dissipation

(Company statement, April 8)

(Company statement, April 8)

- Toshiba developed a new Li-ion battery module for its SCiB series, featuring an aluminum base plate that doubles the heat dissipation performance.

- The new module, designed for use in EV buses, electric ships, and stationary storage applications, will be available in Japan and overseas from mid-April 2025.

NGK Insulators’ Polish subsidiary signs first VPPA with local solar power firm

(Company statement, April 7)

- NGK Ceramic Poland, a subsidiary of NGK Insulators, inked its first virtual PPA with Helios Renewable Energy (Poland). This is the NGK Group’s first virtual PPA.

- Under the 10-year contract (April 2026-March 2036), NGK will procure only the environmental value (carbon credits) from additional solar power generation.

NEWS: WIND POWER AND OTHER RENEWABLES

MoE opinion on Happo-Noshiro offshore wind farm, calls for further assessments

(Government statement, March 28/ April 9)

- The MoE gave an opinion on the environmental assessment for the 356 MW Happo-Noshiro offshore wind farm (Akita Pref), planned by a JV comprising ENEOS Renewable Energy, Iberdrola Renewables Japan and Tohoku Electric.

- During a meeting with the MoE, operators addressed concerns by local communities. The MoE called for clear and thorough post-construction monitoring to assess the environmental impact on marine life and birds such as ospreys and herring gulls. The officials want further studies to ensure that post-project surveys use “appropriate” equipment and methods.

- The project will consist of 25 monopile-foundation turbines. Operations are planned to launch in June 2029.

- CONTEXT: The Happo Noshiro site was awarded to a consortium led by Japan Renewable Energy (now ENEOS Renewable Energy) through Japan’s 2023 offshore wind tender. JRE became a subsidiary of ENEOS in 2022.

Eurus Energy plans onshore wind farms in Fukushima and Aomori

(Company statement, March 28)

- Eurus Energy plans two onshore wind farms:

- 80 MW in Iwaki City, Fukushima Pref

- 60 MW in Mutsu City, Aomori Pref

- The plans include installation of:

- 19 turbines, 4-6 MW each, for the Iwaki wind farm; construction is expected to start after 2031, with operations to begin after 2034.

- 14 turbines for the Mutsu wind farm (each 4-6 MW); construction begins in April 2030, with trial operations in December 2032, and commercial operations in April 2033.

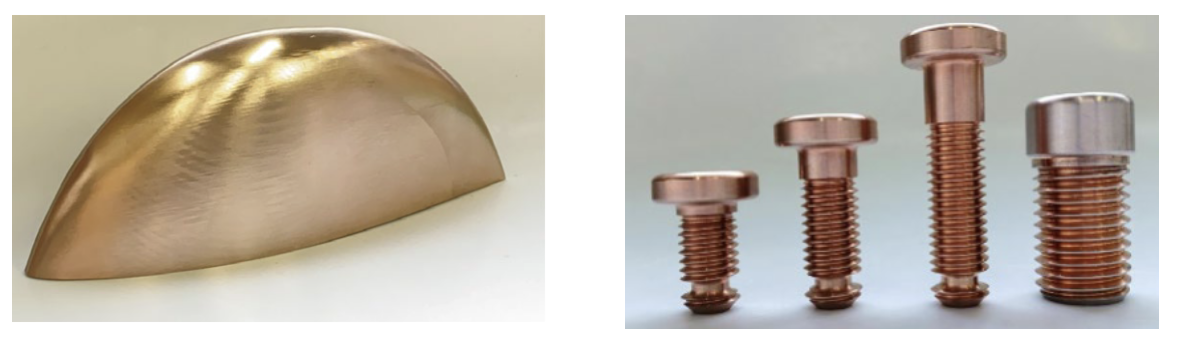

Meidensha develops lightning protection component for wind turbine blades

(Company statement, March 31)

- Meidensha, a Japanese producer of wind power generation equipment, has developed a “receptor,” a wind turbine component to protect turbine blades from lightning strikes. The firm plans to bring the product to market in FY2027.

- Designed with high conductivity and mechanical strength, it reduces blade damage and downtime, ultimately boosting energy output and lowering maintenance costs

- The receptor is installed at the blade tip to attract and safely receive lightning.

- CONTEXT: Blade damage from lightning is especially problematic for offshore wind turbines, where maintenance costs are significantly higher than onshore.

From left to right: Chip receptor and rod receptors.

Source: Meidensha

Panasonic Energy inks off-site corporate PPA for geothermal power

(Company statement, April 8)

- Panasonic Energy began procuring geothermal power from Kyuden Mirai Energy via an off-site PPA, securing around 50 GWh/ year.

- Kyuden Mirai Energy has eight geothermal plants, acquired from Kyushu Electric in April 2024 (totaling 224 MW).

- CONTEXT: This deal follows Kyuden Mirai’s first geothermal PPA with Sumitomo Mitsui Banking in February 2025. Geothermal PPAs remain rare. The only other known deal is a 22.8 MW virtual PPA via Digital Grid.

TEPCO RP and Hulic sign off-site physical PPA for hydroelectric power plant

(Company statement, March 31)

- TEPCO Renewable Power and real estate firm Hulic Group inked an off-site physical corporate PPA (C-PPA). This is TEPCO RP’s first C-PPA outside the TEPCO Group.

- Starting in April 2026, TEPCO RP will supply renewable energy generated from its Shimofunato Hydroelectric Power Plant (6.6 MW capacity, 40 GWh annual generation) in Niigata Pref to selected Hulic Group facilities.

- CONTEXT: The deal will cover 10% of Hulic’s total energy use, with the hydro power complementing solar to provide round-the-clock renewable energy.

(Company statement, April 2)

- Toho Gas joined the Floating Offshore Wind Technology Research Association (FLOWRA), becoming its 21st member. Its goal is to promote floating offshore wind tech in Japan.

- Other members include ENEOS Renewable Energy, JERA and Mitsubishi. FLOWRA seeks measures to reduce the cost and risks of floating offshore wind.

- A few days ago FLOWRA unveiled a partnership with World Forum Offshore Wind.

NEWS: NUCLEAR

CNSN approves construction of Hitachi’s SMR in Canada

(Government statement, April 9)

- The Canadian Nuclear Safety Commission approved construction of a GE Hitachi Nuclear Energy BWRX-300 at the Darlington Nuclear Station in Ontario.

- OPG, the site operator, plans to build up to four SMRs at Darlington.

- CONTEXT: The BWRX-300 is a boiling water reactor co-developed by Hitachi-GE Nuclear Energy and its U.S. subsidiary.

Sumitomo signs MoU with U.S. fusion startup

(Company statement, April 9)

- Sumitomo, via its U.S. arm, Sumitomo Corp of Americas, signed an MoU with SHINE Technologies to deploy fusion-derived technologies and medical isotopes in Japan and other Asian markets.

- It includes studies for commercialization, regulatory and logistical assessments, and distribution of products. If the studies confirm market potential, Sumitomo will act as a sales agent in the region.

- CONTEXT: SHINE Technologies is a leader in fusion-derived applications. With over $800 million in funding, it has a track record of commercialization success in neutron imaging and isotope production. Sumitomo has invested in fusion startups, such as TAE Technologies (U.S.) and Tokamak Energy (UK).

Helical Fusion partners with MiRESSO on beryllium supplies for fusion reactor

(Company statement, April 10)

- Helical Fusion inked a partnership with MiRESSO, based in Misawa, Aomori to develop and secure beryllium, a rare metal critical for fusion reactor components.

- MiRESSO has developed a low-temperature purification technology, which allows low-cost, energy-efficient beryllium production. This is a world-first.

- CONTEXT: Beryllium serves as a neutron multiplier in the blanket, which enables both tritium production and energy extraction. By increasing the number of neutrons, beryllium improves tritium production. Yet, global beryllium supply is expensive and limited. A single fusion reactor could need more than the total global output.

Niigata takes cautious stance on referendum for Kashiwazaki-Kariwa NPP

(Japan NRG, April 10)

- Niigata Governor Hanazumi Hideyo gave an official opinion on a citizen-proposal to hold a referendum on Kashiwazaki-Kariwa NPP’s restart.

- He expressed a cautious stance, not stating whether he supports or opposes the ordinance itself. The prefectural assembly will likely vote on the ordinance during an extraordinary session on April 18.

- Meanwhile, Kobayashi Ken, Chairman of the Tokyo Chamber of Commerce and Industry, visited the plant. He urged TEPCO to resume operations as soon as possible.

- CONTEXT: Holding a referendum for a NPP restart would be a first in Japan. It would set a precedent for other restarts and nuclear power-related projects.

- CONTEXT: Kobayashi’s visit follows recent inspections by heads of the Keidanren (Nov 2024) and Japan Association of Corporate Executives (March 2025). There is growing pressure from Japan’s major business lobbies to restart the plant. Even the head of the IEA, Fatih Birol recently visited the plant and encouraged its restart.

NUMO to hold a forum in Genkai on nuclear waste site selection

(Company statement, April 7)

- On April 17, NUMO will hold the first “Dialogue Forum” in Genkai Town (Saga Pref), to discuss the literature survey for nuclear waste disposal sites.

- CONTEXT: Genkai Town is home to Genkai NPP and is under consideration for a high-level radioactive waste disposal site. NUMO is charged with selecting such sites. Previous attempts at site selection faced public resistance in other regions.

NEWS: TRADITIONAL FUELS

Global LNG prices to remain high until at least 2028, says Trafigura CEO

(Nikkei, April 11)

- Trafigura CEO Richard Holtum expects LNG prices, currently around $11 per million BTU for Asia, to remain elevated until at least 2028, citing sustained European demand following reduced Russian pipeline gas supplies.

- Significant new U.S. LNG production capacity will likely not come online fully until after 2028 due to typical construction delays, prolonging current high prices.

- A substantial decline in LNG prices would occur only if Russian pipeline gas returns to Europe at pre-invasion levels, though Holtum sees this as highly unlikely due to physical pipeline damage and political barriers.

- Despite geopolitical tensions and trade disputes under Trump, Holtum emphasized continued global trade flows and urged Japan to diversify energy sources by securing both renewable energy and fossil fuels, including LNG.

- CONTEXT: In spring 2024, JBIC and Sumitomo Mitsui Banking Corp agreed a $560 million loan to help an unnamed Japanese utility to import LNG from Trafigura over an extended period of time.

Osaka Gas expands aggressively into India’s city gas and renewables market

(Nikkei Asia, April 8)

- Osaka Gas, through its 2021 investment in Singapore-based AG&P Group, secured exclusive gas distribution rights covering 10% of India’s land area, targeting annual sales of 3.5 billion m3 by 2030 – more than half its Japanese gas sales volume.

- The company is laying a 100 km gas pipeline in Chennai and announced a JV with India’s Clean Max Enviro Energy Solutions to supply solar and wind power, aiming for 400 MW of capacity by 2028 – 2.5 times its current overseas renewable assets.

- CONTEXT: India is a critical overseas market for Osaka Gas, which saw non-Japan revenue surge from ¥18.7 billion in FY2016 to ¥116.4 billion in FY2024, driven by aggressive foreign investment amid Japan’s shrinking domestic market.

- Osaka Gas also sees potential in India for next-gen fuels, including hydrogen and renewable-based e-methane, as the country’s favorable climate and strong state support present opportunities beyond traditional gas infrastructure.

NGOs urge Japanese companies to withdraw from Mozambique LNG project

(NPO statement, April 9)

- 74 civil society organizations are urging Japanese shipping companies and Korean shipbuilders to withdraw from TotalEnergies’ Mozambique LNG project, due to human rights and environmental concerns.

- Mitsui OSK Lines, NYK, and K-Line, together with Greece’s Maran Gas Maritime, are set to operate 17 LNG carriers that are worth over $3 billion and built by Samsung Heavy Industries and Hyundai Samho.

- Critics warn the vessels will lock in fossil fuel infrastructure for decades. Japanese firms, which control 13% of the global LNG carrier fleet, face particular scrutiny.

Inpex starts engineering design for Indonesia’s Abadi LNG project

(Reuters, April 9)

- Inpex Corp began the front-end engineering design process for its Abadi LNG project in Indonesia, as the govt has put pressure on the company to accelerate development.

- CONTEXT: The Abadi LNG project faced years of delays due to requests by the previous govt to move the LNG plant onshore from an earlier offshore plan, as well as Shell’s exit from the project and a push to include CCS.

LNG stocks down from previous week, down YoY

(Government data, April 9)

- As of April 6, the LNG stocks of 10 power utilities were 2.13 Mt, down 4.5% from the previous week (2.23 Mt); down 2.3% from end April 2024 (2.18 Mt); and 0.5% down from the 5-year average of 2.14 Mt.

NEWS: CARBON CAPTURE & SYNTHETIC FUELS

NYK to build and charter methanol-fueled carrier for Idemitsu

(Company statement, April 7)

- Nippon Yusen (NYK) signed a contract for the long-term charter of an eco-friendly very large crude oil carrier (VLCC) capable of using methanol as fuel for an Idemitsu Tanker that will be built at Nihon Shipyard.

- This ship is 340 meters long, 60 meters wide, a full-load draft of 21 meters, and a deadweight tonnage of 310,000 tons. It is powered by methanol and heavy oil.

- CONTEXT: NYK, Idemitsu Tanker, Iino Kaiun, and Nippon Shipyard have a consortium to research and develop a large crude oil tanker using methanol.

- CONTEXT: Methanol is expected to contribute to the International Maritime Organization’s strategy for reducing GHG emissions, and it can reduce CO2 emissions by about 15% compared to when conventional heavy oil is used.

TAKEAWAY: In addition, it is possible to reduce CO2 emissions to virtually zero by using green methanol, such as bio-methanol produced from biomass and synthetic methanol (e-methanol) produced using hydrogen from renewable energy and captured CO2.

Tokyo to promote use of domestically produced SAF

(Government statement, April 7)

- The Tokyo Govt launched the “Domestic SAF (Sustainable Aviation Fuel) Utilization Promotion Project” in its 2050 Tokyo Strategy.

- A subsidy is available to companies that supply SAF produced in Japan to airlines at Haneda Airport; the difference in supply prices between SAF produced in Japan and SAF produced overseas is subsidized.

- Applications are accepted until April 21, and grant decisions will be made in May.

- CONTEXT: The 2050 Tokyo Strategy will be implemented by 2035 in three areas – “Diversity”; “Smart City”; and “Safe City” – to realize a future of Tokyo in the 2050s.

Mitsubishi Shipbuilding receives AiP for its Onboard CCS

(Company statement, April 4)

- Mitsubishi Shipbuilding received Approval in Principle from Japan’s classification society ClassNK for its Onboard Carbon Capture and Storage system.

- This system captures, liquefies, and stores CO2 from ship exhaust gases. It is developed using MHI’s onshore carbon capture technologies.

BY MAGDALENA OSUMI

What Can Japan’s Offshore Wind Sector Learn from Other Asian Countries?

Japan is preparing to launch the fourth round of offshore wind power auctions under its public tender scheme, which has so far allocated around 3.1 GW of capacity. However, uncertainties over upcoming amendments to the system are raising doubts about the long-term viability of the country’s offshore wind development.

Once seen as one of Asia’s most promising offshore wind markets, Japan is at risk of losing momentum. Several international developers recently opted out of tenders, turning their focus to other Asia-Pacific markets. A complicated auction system and concerns over financial feasibility have made Japan less attractive for offshore wind investment.

In contrast, Taiwan and South Korea have had more success in advancing their offshore wind sectors due to adjustments that have created more transparent and investor-friendly auction systems, which are drawing significant competition and funding. This situation offers clear lessons for Japan as it seeks to rebuild confidence and revive interest.

Offshore wind is still Japan’s main pathway for adding dozens of GW of green capacity in the 2030s, according to the nation’s energy strategy. Developers want officials to act in ways that confirm this commitment.

Background: Challenges in the bidding system

Japan’s offshore wind sector faces a myriad of challenges, including complex permitting procedures, limited sea space, and constrained grid access. These issues are compounded by an auction system that in the early auction rounds overly focused on price, which led to unsustainably low bids.

A case in point is the Mitsubishi Corp-led consortium, which was awarded three large-scale projects in Round 1, but which has threatened to walk away from the developments and the sector unless the government can accommodate the increase in costs it has seen over the past three years due to higher materials and EPC costs, and a weaker yen.

While the auction rules were amended after Round 1 to put more attention on the timescale of project development, the next two rounds saw developers bid at a “zero premium” price level. This means, the project would not receive a top-up payment from the state for the electricity it produces and would rely on sales to the market and to anchor clients under PPA contracts to recover the investment.

Since the bids were made, costs have continued to rise while electricity buyers under PPA deals are reluctant to agree to higher prices, squeezing developers. This has made some reluctant to participate in new auctions until there is a better pricing environment in place either via the state or with offtakers. Few developers are ready to fight for new capacity based on low project costs that leave little margin to correct for unforeseen expenses or delays.

The impasse has dire consequences. Expected CO2 emission reductions from the rollout of offshore wind farms are baked into Japan’s NDC commitments. And at this early stage of the sector’s development, both the developers and the electricity buyers expect the government to take the lead in resolving the issues.

METI has stepped up, promising a number of changes from Round 4 that take into account the variables in cost, and has regularly met with industry participants to source both feedback and details of how similar issues were addressed in other countries.

So far, however, a degree of skepticism, especially from non-Japanese developers, remains over the effectiveness of the proposed reforms. Developers want more specifics on future auction size and timelines, a roadmap of the areas where new wind farms will be allowed, and more flexibility on supply chain and project management. In this sense, the markets near Japan offer useful case studies.

The value of a centralized approach

South Korea and Taiwan demonstrate how centralized, transparent frameworks can create a stable investment environment.

In South Korea, the proposed Special Act, submitted in June 2024, aims to reform the fragmented permitting system by introducing a one-stop-shop model led by a dedicated Offshore Wind Power Development Committee.

This move mirrors successful European systems, such as those in Denmark and the Netherlands, and could significantly reduce project risk, improve predictability, and shorten development timelines currently stretching to seven to nine years.

South Korea also benefits from strong fundamentals: high energy demand, advanced infrastructure, and a robust industrial base. Combined with ambitious renewable energy targets – 21.6% by 2030, and 32.9% by 2038, and contributing to a 120 GW total renewable energy goal – the country is flagging its long-term opportunities for investors.

Taiwan’s shift toward flexibility and openness

Taiwan is also adapting to changing market conditions. In the latest Round 3.2 auction, the government introduced more flexibility in how winning projects can be developed. The goal is to address implementation challenges experienced by both local and European developers.

In a landmark policy shift, Taiwan pledged to eliminate localization requirements from future auctions. Once a major barrier for international players, these will no longer be included as eligibility conditions or award criteria. The move followed a WTO consultation initiated by the EU in July 2024 that challenged Taiwan’s local content rules as discriminatory.

It stands in striking contrast with Japan’s plan to raise its domestic procurement goal for offshore wind farms to roughly 70% in 2040 from the current 60%. The move is aimed at building up the local supply chain to potentially reduce costs of wind turbine imports. A decision is expected by this summer.

Taiwan’s Ministry of Economic Affairs reaffirmed the country’s commitment to offshore wind as a pillar of its 2050 net-zero goal and energy security strategy. The focus is now on ensuring timely grid connection and project execution over rigid industrial relevance plans.

Starting 2025, Taiwan will adopt a more liberalized, developer-friendly framework. With the removal of local content mandates, the market is expected to attract broader international participation to revive the sector on the island. As elsewhere, Taiwan has faced a combination of policy instability, near-zero feed-in tariffs, and infrastructure bottlenecks, which in recent years saw several major players exit the market.

South Korea’s offshore wind gains speed

In October 2024, South Korea’s Ministry of Trade, Industry and Energy (MOTIE) launched a long-awaited 2.8 GW renewable energy tender, which includes 1.5 GW of offshore wind. This proved to be a major step for the offshore wind sector.

Of the 1.5 GW allocated, 1 GW is dedicated to bottom-fixed, and 500 MW to floating wind. The government set a uniform price cap of KRW 176.565/ MWh ($128) for both types, a move that surprised analysts due to floating wind’s higher costs. However, floating wind projects benefit from higher renewable energy certificate (REC) multipliers, which could help balance the economics.

The auction also introduced a balanced scoring system – 50% price, 50% non-price – covering industrial benefits, grid connection, community acceptance, and project readiness. For the first time, ceiling prices were made public, reflecting a 5% increase from 2023 to account for inflation. This transparency is another positive signal to investors.

These developments show South Korea’s confidence in the rapid innovation of floating wind technology, which is especially significant when compared to Japan, where floating wind turbines remain in the early demonstration phase, with just 34 MW installed.

Lessons learned

Japan stands at a crossroads. While it was once seen as a regional frontrunner, its rigid auction structure, permitting delays, and policy uncertainty are driving developers to explore more predictable markets.

The progress made by Taiwan and South Korea illustrates key lessons:

- Flexibility and transparency attract investors and support project execution.

- Centralized permitting can reduce delays and administrative burdens.

- Balanced auction criteria help prevent overly aggressive bids and improve long-term viability.

- Removing localization mandates opens markets to global supply chain players, which lowers cost through increased competition.

South Korea’s centralized permitting reforms and balanced auction structure, combined with strong domestic demand and industrial capacity, has set a new standard in Asia. Taiwan’s removal of local content barriers and focus on timely project delivery also demonstrate how government responsiveness can reignite investor interest.

If Japan can implement similar reforms – streamlining approvals, increasing transparency, and focusing on execution over cost minimization – it has the potential to re-establish itself as a regional leader in offshore wind. That’s important to secure the ships, human resources, and capital needed to develop offshore wind energy in Japan.

Recent METI statements indicate that the role of renewable energy in Japan has come to be recognized as not only one of reducing emissions but also as a means of achieving greater energy security. That factor should motivate officials to find the compromises the industry seeks to move forward and unlock the nation’s green potential.

BY FILIPPO PEDRETTI

From Importer to Trader: LNG Activity Grows Despite

Shrinking Domestic Demand

Japan is experiencing a dramatic shift in its energy landscape. LNG imports have been on a downward trend in the past several years due to shrinking domestic demand, and this looks set to continue. Total LNG imports in 2024 were 65.9 million tons, around the same volume as FY2023, when there was a slight decrease from the previous year.

By 2030, total LNG demand could drop to 50 million tons, with more aggressive estimates suggesting even 30 million tons. In response, major Japanese players are adapting to these new market conditions, with ambitions to become key traders in LNG markets across Asia.

None of this is accidental. In 2020, METI unveiled its “New Strategy for International Resources” that set a target to handle 100 million tons of LNG a year by FY2030. That target includes LNG volumes to be traded to third countries amid the building of a strong international sales network.

Such plans come at an opportune time for Japan. Global LNG demand is set to rise, and if production doesn’t meet this new demand, prices will of course rise. In order to better understand the situation and forecast the future, Japan NRG takes a closer look at recent developments and strategies in the LNG market.

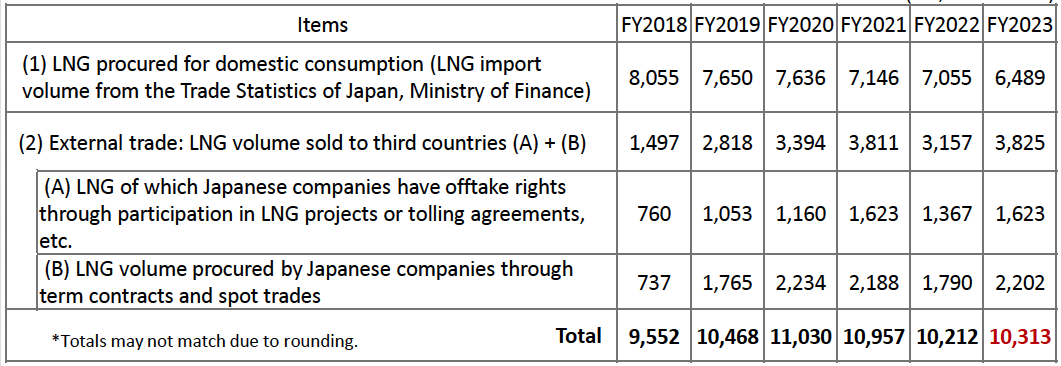

Hedging excess supply through trading

According to JOGMEC, in both FY2019 and FY2020 Japan handled over 100 million tons of LNG, peaking at 110 million tons in FY2020 and FY2021. Since then, the total has decreased to 103 million tons. The major change in LNG for domestic consumption registered a sharp decrease. That figure dropped from a little over 80 million tons in FY2018 to about 65 million tons in FY2023.

In 2023, Japanese utilities were reselling about 37% of the LNG they purchased, up from 16% in 2018. By FY2023 the LNG for external trade grew to 38 million tons, up from just under 15 million tons in FY2018.

New long-term contracts inked by Japanese companies was a major factor in this significant new stage in LNG trading. Nevertheless, as domestic demand continues to drop, more supply will have to find new markets. Breaking long-term contracts means incurring hefty penalties: therefore, Japanese traders might be tempted to re-sell LNG at lower prices in order to offload supply; unless global demand takes a sudden jump in the coming years.

In this regard, it’s worth comparing Spot Asian LNG prices and Japan LNG import prices, which roughly accounts for 80% of long-term contracts linked to crude oil prices and 20% from spot contracts, leaving it less susceptible to the volatile spot market.

Results of JOGMEC’s FY2024 survey on LNG handling volumes by Japanese companies.

Source: JOGMEC

In February, spot Asian LNG prices hit $16.10 per million British thermal units (mmBtu: 1 ton of LNG equals to around 52-53 mmBtu), before dropping to $13.50. It stood at $8.30 at the same time last year, and for the most part has hovered around $13/mmBtu in the past few months. As for Japan NRG data, the LNG import price for February 2025 stood at ¥94,314 / ton, or a little more than $12/mmBtu (leaving some margins for conversions).

JERA, Tokyo Gas and raising global demand

Each year, JERA handles about 30 to 35 million tons of LNG, and has set a target of handling 35 million tons a year by 2035. Part of that total is sold to Asian countries, but JERA doesn’t specify how much. Toward this goal, it plans to invest ¥1 to ¥2 trillion in infrastructure.

Tokyo Gas handles from 13 to 19 million tons of LNG a year, with a target of 5 million tons of LNG to be sold off to third parties each year by 2030, up from 3 million tons today. The company plans to handle 20 million tons by 2030, and to trade around one quarter of that LNG. Tokyo Gas is eyeing Southeast Asia for LNG supply chain development as that regions’ energy consumption is on track to rise rapidly in the coming decade; but the company is also eager to source LNG from Australia and the U.S.

While there are diverse forecasts, it’s safe to say that 2030 global LNG demand will be around 550 million tons. If Japan can keep its goal of handling 100 million tons of LNG, this would be a little less than 20%; currently Japan handles almost a quarter of global demand.

JERA and Tokyo Gas account for about 50% of the total volume handled by Japan. In 2030, considering their target goals, the volumes of JERA’s contracts would be 6% (down from the current 8%) of global demand, and around 3.6% for Tokyo Gas (down from 4.5% today).

Besides Japan’s shrinking position in the market, media such as Reuters, noted that significant growth in LNG global demand could also lead to oversupply and subsequent falling prices, a risk for LNG resellers.

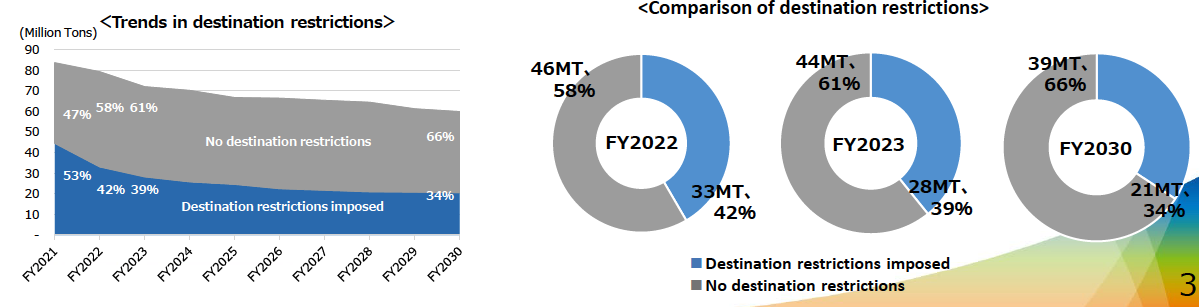

Destination clauses and LNG prices

A significant hurdle in Japan’s LNG strategy has been the use of destination clauses in long-term LNG contracts; they restrict the resale of LNG, limiting the flexibility of Japanese companies to trade surplus gas. A goal of 2020’s plan was working to remove these clauses from contracts, allowing for more fluid trade. Another option supported by the government is to buy LNG on a free-on-board (FOB) basis.

JOGMEC published the results of a survey on LNG transactions, and contracts with destination clauses accounted for 42% of all contracts in FY2022, but declined to 39% in FY2023. When taking an ever broader look at the data, contracts with destination clauses nearly halved in less than a decade, from 75% in FY2016, to 39% in FY2023. By FY2030, such contracts are set to fall to 34%.

Percentage of LNG contracts by Japanese companies with destination clauses from FY2016 to FY2023.

FY2016 | FY2018 | FY2020 | FY2022 | FY2023 |

75% | 65% | 57% | 42% | 39% |

Source: JOGMEC

JOGMEC told Japan NRG that LNG sourced from the U.S. has no destination restrictions. American LNG exports are expected to reach an annual volume of 180 million tons by 2030, which should account for one-third of global supply. Combined with the increase in trading volume and market participants, this has played a role in enhancing market liquidity. JOGMEC also said it expects the U.S. to increase LNG supply through 2030, with 55% of the global LNG supply growth from 2025 to 2030 most likely to be sourced from the U.S.

Conclusion

Japanese involvement in LNG infrastructure development across Asia is expanding (as Japan NRG will show in next week’s issue). But if the LNG global sector sees the gigantic growth in demand that some analysts foresee, Japan’s overall market presence will diminish.

As LNG sellers, Japanese targets for 2030 probably won’t keep pace with the global volumes; while as an importer, Japan’s declining domestic demand is already considered a given.

In a broader perspective, there seems to be a contradiction in Japan’s LNG strategy. On the one hand, Japan justifies its increased LNG trade volumes as a matter of energy security. If its companies secure a strong position as resellers, then they can sell the gas overseas in case of excess supplies, averting a glut.

On the other hand, for the same energy security reasons, Japan launched the Strategic Buffer (SBL), a state-backed LNG reserve program for obtaining emergency supplies amidst demand peaks, with JOGMEC covering financial risks.

In other words,while the private sector secures LNG volumes for overseas trading, the domestic energy security burden falls on the government. The government should be more explicit when advancing its LNG strategies, clarifying the country’s energy needs, its role and that of corporate players when it concerns securing supplies.

ASIA ENERGY REVIEW

BY JOHN VAROLI

A brief overview of the region’s main energy events from the past week

Australia / BESS

The State Electricity Commission in Victoria said that developer OX2 is building the 200 MWh SEC Renewable Energy Park, which will see a 100 MW/ 200 MWh battery energy storage system (BESS) co-located with a 119 MW solar PV power plant.

China / LNG from the U.S.

For over 60 days, China hasn’t imported LNG from the U.S.; this is the longest gap in five years, according to analytics firm Kpler. Zero LNG trade between China and the U.S. is likely to continue for the rest of 2025 due to Trump’s tariffs.

China / LNG resales

Meanwhile, Chinese buyers of LNG are re-selling U.S.-sourced cargoes as tit-for-tat tariffs drive up import costs. The trend is set to accelerate as new multi-year supply deals kick in this month and domestic demand weakens, said Rystad.

China / LPG

Chinese liquefied petroleum gas buyers have prompted a price surge as they seek to replace U.S. supplies of the fuel following Beijing’s response to Trump’s tariffs. Buyers are trying to swap U.S. cargoes with alternatives, including LPG from the Middle East.

Coal Power

The world saw its lowest coal power increase in two decades, with just 44 GW of new capacity added in 2024, according to Global Energy Monitor. The coal fleet rose less than 1% in 2024, a net increase of 19 GW; in the EU, 25 GW of capacity was retired last year.

India / Energy tax

The world’s third-largest oil consumer increased its special additional excise duty on gasoline to 13 rupees (15 cents) a liter, up from 11 rupees. The duty on diesel will be raised to 10 rupees a liter from 8 rupees, said the finance ministry.

India / Green hydrogen

Bharat Petroleum Corp and Sembcorp Green Hydrogen India inked a deal to explore renewable energy and green hydrogen projects across India.

India / Renewable power

In March, India issued around 5.1 GW of renewable energy tenders, according to JMK Analytics. One tender was from NHPC for a 1.2 GW solar project with a 600 MW/ 1.2 GWh energy storage system.

Indonesia / Waste energy

Waste-to-energy (WtE) processing businesses are attracting interest from foreign investors, particularly from Singapore, Japan, and China. In response, the govt is working to simplify regulations and promote ease of doing business, especially involving capital and technology.

Renewable energy

In its Renewable Capacity Statistics 2025 report, IRENA said renewables grew 15.1% in 2024, adding 585 GW, representing 92.5% of new capacity. Solar and wind energy continued to lead the expansion, both accounting for 96.6% of all net renewable additions in 2024. Total global renewable power capacity rose to 4,448 GW.

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Hulic Ochanomizu Bldg. 3F, 2-3-11, Surugadai, Kanda, Chiyoda-ku, Tokyo, Japan, 101-0062.