WEEKLY

APRIL 21, 2025

ANALYSIS

JAPANESE FIRMS EXPAND SOUTHEAST ASIA LNG PROJECTS AS REGION SHIFTS TO GAS

- Japan is accelerating its LNG push into Asia seeking to capitalize on new markets.

- In the coming years, as domestic demand declines, Japan faces an oversupply of LNG and needs to build ‘secondary’ markets to sell its surplus.

WHAT’S THAT SMELL? E-METHANE PITCHES AN ALTERNATIVE TO THE HYDROGEN SOCIETY

- Japan is putting waste to use in a supply chain to produce synthetic fuels, such as e-methane, a cleaner alternative to fossil fuels.

- The cost of producing hydrogen is a major stumbling block; thus, Japan is testing ways to make e-methane that does not require raw H2 as a feedstock.

ASIA PACIFIC REVIEW

This column provides a brief overview of the region’s main energy events from the past week

NEWS

- Govt experts consider data center sites based on proximity to clean power

- IMO agrees treaty to cut emissions of international shipping

- METI hosts first next-gen geothermal forum, sets ambitious sector targets

- TOCOM power futures trading hits record high

- OCCTO launches 1st FY2025 solar auction

- Regulator mulls reflecting inflation in the wheeling charges

- IHI conducts first green ammonia trial at coal plant in ASEAN

- Mitsubishi Kakoki invests in Japan hydrogen fund

- Sumitomo Rubber launches onsite green hydrogen production

- MoE first round of subsidies to support agrivoltaics and floating solar

- Toa Road launches pilot for solar-powered pavement in Tokyo

WIND POWER AND OTHER RENEWABLES

- METI to set new target for floating offshore wind

- Largest onshore wind farm online in Fukushima

- Tohoku Electric acquires stake in GPI’s wind farm

- TEPCO’s 5th business plan discussions resume

- Niigata rejects NPP restart referendum

- Kyoto Fusioneering sets up subsidiary for demo

- Global gas-fired power generation to grow, MHI to increase production capacity

- OFS opens center in Malaysia as a hub for FPSO

CARBON CAPTURE & SYNTHETIC FUELS

- NEDO selects contractors for technology at CO2 Utilization Site

- INPEX start of pre-FEED for Australian CCS

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Chief Editor)

John Varoli (Senior Editor, Americas)

Kyoko Fukuda (Data, Events)

Magdalena Osumi (Renewables & Storage)

Filippo Pedretti (Thermal, CCS, Nuclear)

Tetsuji Tomita (Power Market, Hydrogen)

George Hoffman (Sales, Business Development)

Tim Young (Design)

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

EVENTS

May 3-6 May Golden Week Holidays

June 4-5 Kyushu Innovation Week / Kyushu GX Decarbonization Expo @ Marine Messe Fukuoka

June 4-6 AXIA EXPO 2025 (Hydrogen and Ammonia Next-Generation Energy Exhibition) @ Aichi Sky ExpoJune 15-17 G7 Summit @ Kananaskis, Alberta, Canada

NEWS: GENERAL POLICY AND TRENDS

NEWS: GENERAL POLICY AND TRENDS

Govt experts consider data center sites based on proximity to clean power

(Government statement, April 15)

- The Cabinet Secretariat set up a working group to discuss measures to implement the GX industry location policy, including attracting investment to regions with abundant decarbonized energy and promoting the new GX-type industries.

- The discussion will help identify locations suitable for high-energy-consuming facilities, such as data centers, and seek to align the discussions with that of the Watt-Bit Council, a new public-private dialogue addressing a similar issue.

- The working group, chaired by Ohashi Hiroshi, VP of the University of Tokyo, will formulate policies by summer 2025. The focus will be:

- Identifying conditions to promote industrial clustering near decarbonized power sources and reduce energy price gaps with other countries;

- Consider measures such as targeted financing, regulatory reforms, and investment incentives;

- Address a shortage of industrial land that is estimated to be at half the level of 1996 and the mismatch between supply and demand across prefectures;

- Benchmark international practices, such as France’s approach to data center location planning, which involves govt designation of 35 areas close to nuclear power plants to support the AI-driven national strategy;

- Attract foreign investment by assessing Japan’s competitive advantages.

- CONTEXT: The GX 2040 Vision formulated in February emphasizes the need to accelerate the clustering of industries with a view to utilize decarbonized power sources in terms of GX industrial location. Supply is needed to cover the vast amount of electricity consumed by AI data centers.

TAKEAWAY: Japan is exploring a similar strategic site-selection method as France, and may designate certain zones as favorable for new data centers based on the availability and proximity of nuclear and renewable energy. This is reminiscent of the Special Economic Zones approach of PM Abe’s govt in the early part of the previous decade.

IMO agrees to treaty amendment for carbon neutrality in international shipping

(Government statement, April 14)

- The MLIT said the International Maritime Organization (IMO) agreed in principle to a treaty amendment jointly proposed by Japan and Europe to achieve carbon neutrality in international shipping. It includes:

- A system for the gradual conversion of ship fuel to alternative fuels with lower GHG emissions;

- A system that provides economic incentives for the deployment of zero emission fuel ships.

- CONTEXT: The 83rd session of the IMO Marine Environment Protection Committee was held in London from April 7-11. It also discussed measures for ships to lessen marine pollution, etc. Shipping accounts for 3% of global emissions.

METI hosts first next-gen geothermal forum, sets ambitious sector targets

(Government statement, April 14)

- METI held its first public-private forum to promote next-gen geothermal power.

- The forum drew participation from more than 70 companies, including INPEX and Chubu Electric. The focus was on investment and state support measures to accelerate deployment of new capacity and technology.

- The goal is to roll out advances such as “closed loop” systems, which generate electricity even without hot water underground, in the early 2030s.

- CONTEXT: Japan has the world’s third-largest potential geothermal resource. Based on today’s conventional tech, about 23.5 GW of power generation capacity could be installed. This number could be augmented by 77 GW with next-gen geothermal tech: 66 GW for high-temperature rock-mass geothermal systems.

- By October, METI plans to draw up specific plans and targets for 2040.

Japan to add undersea cables and satellites to critical supplies list

(Nikkei Asia, April 15)

- Japan plans to expand its list of critical goods to include undersea cables, satellites, rockets, industrial data, and also cover fusion energy and nuclear manufacturing tech.

- METI aims to revise the economic security plan by May. Japan will offer subsidies to bolster domestic capabilities and reduce reliance on imports.

- CONTEXT: This reflects growing concerns over supply chain vulnerabilities. Rivals, such as China, are gaining ground in strategic areas like undersea cables.

- SIDE DEVELOPMENT:

- Mitsui Sumitomo Insurance introduces new service to prevent copper cable theft

- (Company statement, April 17)

- Mitsui Sumitomo Insurance launched a new service to prevent copper cable theft at solar farms. Sensors are placed at vulnerable spots; if an intruder is detected, a security company is automatically alerted.

- CONTEXT: With copper thefts rising due to high prices for the metal, this service aims to protect operators from financial losses. Other insurers like SOMPO and Solvvy also offer theft prevention services using AI and advisory support.

Toshiba ESS to be reintegrated into its parent company

(Company statement, April 15)

- Toshiba will reintegrate its energy arm, Toshiba Energy Systems & Solutions (Toshiba ESS), into the parent company through a merger effective April 1, 2026.

- CONTEXT: This move follows the company’s effort to consolidate key subsidiaries, with Toshiba Infrastructure Systems already merged earlier this year. Toshiba ESS was spun off in 2017 from the company’s energy and nuclear divisions.

NEWS: ELECTRICITY MARKETS

TOCOM power futures trading hits record high in March 2025

(Exchange statement, April 9)

- Power futures trading on the Tokyo Commodity Exchange (TOCOM) surged to a record 12,600 contracts in March, over 2.5 times higher than the previous peak of 4,853 contracts in May 2022.

- A single day’s trading volume on March 13 reached a historic high of 711 GWh, significantly surpassing the prior daily record of 153 GWh on Nov 7, 2024.

- Off-floor transactions dominated activity, accounting for 154 of the total 167 trades. On March 13, annual baseload contracts for the East accounted for 9,720 contracts.

- Smaller-scale futures trades also increased, suggesting growing participation among new power retailers, with trades as small as one contract per month observed.

- CONTEXT: Q1 was particularly strong. February’s trading volumes were 205.7 GWh, a 2.3-fold increase from the previous month. Among the drivers was a concern about the wholesale power price for West Japan.

- SIDE DEVELOPMENT:

Spot electricity prices drop in March as supply eases

(Exchange statement, March 2025)- Spot electricity prices (JEPX) declined across all 9 regions in March over February, driven by mild temperatures, easing heating demand, though volatility rose due to periodic cold snaps and scheduled maintenance outages at thermal plants.

- The monthly average temperature nationwide was 1.13°C above the 30-year average, the seventh highest March since records began in 1898.

- Fuel prices diverged: Crude oil rose ¥2,443/ kl to ¥78,186; coal declined ¥1,689/ ton to ¥21,692; and LNG fell significantly by ¥6,061/ ton to ¥94,310, influenced by geopolitical risks and U.S. tariff policies.

TAKEAWAY: The JEPX wholesale power exchange just had its 20-year anniversary, and market volumes are up over 300-fold since its start. Quite a large part was due to regulatory changes. In March 2013, major power utilities (EPCOs) were mandated to bid on the spot market, and full liberalization of retail electricity sales launched in April 2016, expanding the buyer base. As the interconnector gate capacities expand, there is also more cross-regional electricity trade and more price correlation between markets.

OCCTO opens registration for 1st FY2025 solar power auction

(Government statement, April 11)

- OCCTO opened registration for its 24th solar auction, the first of FY2025, offering up to 79 MW in FIP contracts for non-rooftop solar projects ≥250 kW.

- The price cap is ¥8.90/ kWh. Registration closes May 9. Results on June 20.

- Future round capacities will be adjusted based on bid volumes, but stay above 79 MW. Remaining FY2025 rounds will open on June 23, Sept 24, and Jan 5, 2026.

- CONTEXT: The initial procurement volume was trimmed from 93 MW in the first FY2024 round, prompted by lackluster second and third rounds that year.

EGC discusses reflecting inflation in revenue cap system

(Government statement, April 15)

- At an EGC expert meeting, the Transmission and Distribution Grid Council and TSOs called to adjust the revenue cap system to reflect rising labor costs and inflation.

- Currently, the cap does not allow for inflation-based cost increases, thus requiring companies to absorb rising expenses.

- Experts agreed that such adjustments should be made in the second regulatory period (FY2028-FY2032). Some argued it should also apply retroactively to the first period (FY2023-FY2027), since the cost impact has already been significant, estimated at ¥150 billion in FY2023 alone.

- The EGC will continue to discuss the factors contributing to price increases, as well as the differences in the numbers reported by each operator, and further standardization and refinement of the calculation methodologies.

- CONTEXT: The T&D network usage charge, known as the “wheeling charge,” was previously calculated using the “total cost method”. But from FY2023 it’s calculated using the “revenue cap system”. Operators prepare five-year business plans, and the govt reviews the costs necessary to implement these plans (revenue cap).

Hitachi Energy selected for HVDC to deliver 6 GW of renewables in India

(Company statement, April 3)

- Hitachi Energy won a contract to build a 950 km, 6 GW HVDC transmission link in India. The firm formed a consortium with state-owned Bharat Heavy Electricals, a major engineering and manufacturing firm.

- The consortium will design and deliver HVDC terminals to transmit renewable energy from Bhadla in Rajasthan to the industrial and transport hub in Fatehpur.

- CONTEXT: The system is part of India’s 500 GW renewables transmission program, and will deliver enough clean power for about 60 million households. The project is expected to enhance grid stability, enable bi-directional power flow, and support India’s renewable energy and decarbonization targets.

JERA Cross and Nozomi to supply carbon-free electricity with greater transparency

(Company statement, April 17)

- Nozomi Energy, a renewables developer established by Actis, and JERA’s subsidiary JERA Cross began supplying 24/7 carbon-free electricity to customers using a wholesale supply model and hourly matching to track generation and consumption transparently.

- Power generated at Nozomi’s Maki solar farm in Chiba Pref is used.

- CONTEXT: 24/7 carbon-free electricity ensures every kilowatt-hour consumed is matched in real time by carbon-free generation, certifying to the buyers that continuous clean energy is supplied without relying on offsets. Actis is a global investment firm specializing in sustainable infrastructure.

AT Tokyo enters retail electricity market, supplies own data centers with 100% renewables

(Denki Shimbun, April 18)

- AT Tokyo, a data center operator, has entered the retail electricity business. Since October last year, it has been supplying power to its own data centers in Tokyo.

- Previously, AT Tokyo (which also uses the name @Tokyo) relied on TEPCO EP plans to achieve 100% renewable energy for its data centers. It enrolled in TEPCO EP plans from April 2024 and progressively shifted five data centers to green electricity.

- The company uses both FIT non-fossil certificates and renewable-designated, non-FIT non-fossil certificates, as well as solar power via off-site PPAs.

OCCTO deducts out-of-market balancing capacity from required amount in EPRX

(Agency statement, April 15)

- OCCTO announced its policy to deduct off-market balancing capacity from the required amount in the balancing market, EPRX (Electric Power Reserve Exchange).

- CONTEXT: Out-of-market balancing capacity is reserve capacity held by TSOs and is not traded on the EPRX.

- OCCTO examined the reserve capacity in each area based on actual supply-demand data and found that a certain degree of reserve capacity exists in all areas.

- CONTEXT: Since the start of trading for all products on the EPRX in April 2024, procurement shortfalls have persisted. However, the shortfall is made up by surplus capacity in the wider area.

- SIDE DEVELOPMENT:

- OCCTO treats EPPS as power failure response balancing capacity

- (Agency statement, April 15)

- OCCTO will start to deduct EPPS (Emergency Power Presetting Switch) capacity from the abnormal situation (power failure) response balancing capacity.

- The balancing capacity for abnormal situations in the balancing market is the capacity to suppress frequency drops within a certain range and restore frequency in the event of a power failure.

- CONTEXT: The EPPS has not been a completely reliable tool so far. Energy planners discussed the issue in March and proposed ways to improve it.

OCCTO issues notice to Groove Energy on payment delinquency

(Denki Shimbun, April 18)

- OCCTO gave notice to Groove Energy (Matsuyama City) for delinquent capacity contribution payments, which retail electricity providers are required to pay under the capacity market framework.

- OCCTO demanded full payment of the overdue amount within two weeks and requested Groove Energy to strengthen internal systems.

- This is the second time OCCTO gave such a notice, the first was in January 2021.

- CONTEXT: Since the capacity market entered its actual supply-demand phase in April 2024, retail electricity providers are obligated to pay capacity contribution fees to OCCTO.

TAKEAWAY: If Groove Energy fails to comply, the next step is “sanctions,” which could include reprimands, fines, or suspension of membership rights, as determined by the Disciplinary Committee.

NEWS: HYDROGEN

IHI conducts first green ammonia trial at coal plant in ASEAN

(Company statement, April 16)

- IHI, in collaboration with Indonesia’s state-owned power utility PLN Indonesia Power and fertilizer company Pupuk Kujang, conducted the first green ammonia co-firing test at a commercial coal-fired power plant in the ASEAN region.

- IHI retrofitted an existing non-IHI boiler burner at the Labuan Power Station (300 MW) to allow for ammonia combustion using green ammonia.

- CONTEXT: The project builds on IHI’s earlier 2022 ammonia combustion test in Indonesia’s Gresik plant, which was successful.

Mitsubishi Kakoki invests in Japan hydrogen fund

(Company statement, April 16)

- Mitsubishi Kakoki invested in the Japan Hydrogen Fund, set up by the Japan Hydrogen Association (JH2A) and Advantage Partners.

- The fund supports projects across the entire hydrogen value chain – production, transportation, storage, and usage – to foster a global hydrogen supply network.

TAKEAWAY: As a founding member of JH2A, Mitsubishi Kakoki expects the investment to generate both financial returns and strategic partnerships. The company engineers and builds industrial and chemical plants and sees hydrogen as a new business area.

Sumitomo Rubber launches onsite green hydrogen production

(Company statement, April 15)

- Sumitomo Rubber will produce up to 100 tons of green hydrogen annually at its Shirakawa factory using an electrolysis system developed by Yamanashi Hydrogen Company, powered by renewable energy.

- It is Japan’s largest factory-scale hydrogen facility by a private company and the first hydrogen-powered tire production plant in Japan.

- Located far from hydrogen pipelines and ports, the plant sets a “local production for local use” model for decarbonizing inland manufacturing, reducing reliance on transported hydrogen.

- CONTEXT: Shirakawa Factory is recognized as a Nationally Certified Sustainably Managed Natural Site by the MoE.

iLabo to begin mass production of hydrogen truck engines by 2026

(Company statement, Nikkei, April 15)

- iLabo will mass-produce hydrogen engines for trucks starting in 2026, initially targeting an annual output of 40–50 units.

- The company secured ¥800 million through third-party allocation from Idemitsu Kosan, TPR (piston rings), Kamigumi (port logistics), etc.

- TPR will handle parts procurement and engine assembly, while JAL Airtech, a Japan Airlines subsidiary, will install the engines into vehicles.

- CONTEXT: iLabo developed the world’s first hydrogen engine truck conversion and was selected by the MoE in 2021.

JGC and Amogy Partner on ammonia cracking for hydrogen production

(Company statement, April 17)

- JGC signed an MoU with U.S. startup Amogy to utilize its low-ruthenium ammonia cracking catalyst, aiming to enhance the efficiency and cost-competitiveness of JGC’s large-scale ammonia-to-hydrogen conversion technology.

- Since 2023, JGC, Kubota, and Taiyo Nippon Sanso have developed this technology under NEDO’s hydrogen supply chain R&D program, with a goal of producing 100,000 tons of hydrogen annually via thermal ammonia cracking.

- Amogy’s catalyst operates at lower temperatures with reduced use of precious metals, offering potentially significant CAPEX reduction and energy efficiency benefits.

NEWS: SOLAR AND BATTERIES

MoE first round of subsidies to support agrivoltaics and floating solar

(Government statement, April 8)

- The MoE launched the first round of subsidy applications to support agrivoltaics (solar sharing) and floating solar projects. The subsidy covers up to half of eligible costs, with a maximum of ¥150 million per project.

- Eligible equipment includes solar panels, stationary batteries, private power lines, and EMS. Applications are accepted until May 8.

- Projects must meet specific cost and technical requirements, and only certain types of farmland and water surfaces qualify.

- CONTEXT: Agrivoltaic initiatives are proliferating in Japan, blending agriculture with solar energy production to optimize land use and support rural revitalization. To promote such dual-use systems, the govt offers feed-in tariffs for local energy production. However, regulations require that at least 80% of the agricultural output be maintained, ensuring that farming remains a primary activity.

JWA launches forecasting service for grid-scale battery operators

(Organization statement, April 14)

- The Japan Weather Association (JWA) introduced a new online service to support operators of grid-scale battery storage systems.

- It provides 30-minute interval forecasts of power market prices and demand to optimize charge/ discharge planning and bidding strategies for power markets.

- The system is tailored to facility size and usage objectives, and it uses data from solar PV systems and battery storage.

- CONTEXT: JWA has previously offered electricity price, demand, and solar output forecasts mainly to renewables operators and aggregators.

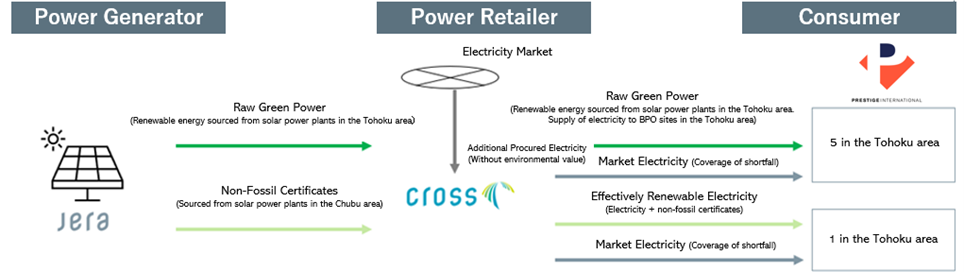

JERA supplies solar power to Prestige International sites via offsite PPA

(Company statement, April 16)

- JERA Cross, a JERA subsidiary, began supplying solar power to six Prestige International sites in Japan through offsite corporate PPAs. Prestige International (PI) is a firm specializing in business process outsourcing (BPO).

- Power from small JERA-owned solar farms in the Tohoku and Chubu regions now supply facilities at PI sites in Akita, Yamagata, and Toyama Prefs, covering about 30% of their electricity needs.

- The remaining electricity will be sourced from solar power plants in the Chubu area or procured from the market. Going forward, JERA Cross will gradually introduce 24/7 carbon-free electricity at all of PI’s sites.

DEI and TESS to work on grid-scale BESS in Kumamoto Pref

(Company statement, April 16)

- Daiwa Energy & Infrastructure (DEI) acquired development rights for a grid-scale battery storage project in Nishiki Town (Kumamoto Pref) from Gotion Japan, a subsidiary of Chinese battery producer Gotion.

- With a planned installed capacity of 25 MW and storage capacity of 100 MWh, the project is scheduled to start construction in 2026 and begin operations in 2028, without relying on subsidies.

- Technical due diligence and business feasibility evaluations are completed, and EPC services were contracted to TESS Engineering for about ¥4 billion, with project completion expected by December 2027.

- CONTEXT: DEI and its subsidiary CO2OS, an O&M services provider, partnered with Gotion Japan in March 2024, aiming to deploy 1 GWh of Gotion batteries in Japan within two years.

Glass substrate maker Kuramoto Seisakusho to enter grid-scale BESS business

(Company statement, April 11)

- Kuramoto Seisakusho, a manufacturer specializing in glass substrates, is entering the grid-scale battery storage sector, inking a partnership with Eiki Shoji, a firm active in environmental energy solutions.

- By August, Kuramoto will complete acquisition of its first BESS project, and begin construction of the storage facility this fall.

- The project will involve participation in the wholesale electricity market (JEPX), the balancing market, and the capacity market.

- CONTEXT: The company began building a PSC production line in 2024, marking its entry into clean energy. The move into BESS is its first step into power infrastructure, reflecting a broader trend of non-energy companies entering the market and linking solar power with storage solutions.

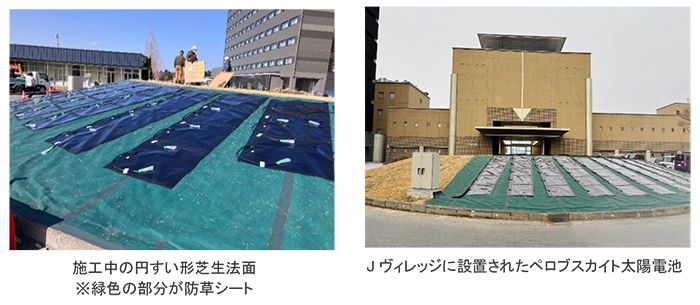

Unitika’s weed-control sheet adopted in PSC panel pilot

(Company statement, April 11)

- A weed-control sheet developed by materials manufacturer Unitika was selected for use in a field test of film-type perovskite solar panels at the J-Village sports training facility in Naraha Town. This is a Fukushima Pref initiative.

- The test will assess whether weeds interfere with power generation and if the installation method provides adequate wind resistance.

- CONTEXT: In Japan, where flat land is limited, slopes and embankments are potential sites for solar deployment. Installing PSCs requires not only weed suppression but also secure, long-term mounting solutions.

- CONTEXT: Unitika specializes in polymers, advanced textiles, etc.

Hankyu Railway installs regenerative energy storage system

(Company statement, April 15)

- Hankyu Railway installed Toshiba’s Li-ion battery system at its Ishibashi substation in Osaka to store regenerative energy from train braking.

- Previously, excess regenerative power was often wasted, but the new system temporarily stores it for reuse. The system can supply power during outages to help trains safely reach the nearest station.

Toa Road launches pilot for solar-powered pavement in Tokyo

(Company statement, April 9)

- The MoE tapped Toa Road’s solar pavement tech for a field test. The system, based on “Wattway” developed in France, integrates solar panels into road surfaces.

- A 34-meter stretch (6 kW capacity) will be installed in Shinjuku Gyoen park starting mid-April 2025, with power supplied to on-site facilities from mid-May.

- CONTEXT: Toa Road is a subsidiary of construction firm Toa, and specializes in the development, manufacture and sales of road pavement materials.

NEWS: WIND POWER AND OTHER RENEWABLES

METI to set new target for floating offshore wind power

(Nikkei, April 16)

- METI will set a new 2040 target for floating offshore wind power deployment. Discussions were due to begin on April 17, with a conclusion expected by summer.

- The plan includes setting domestic procurement and export goals for a supply chain.

- CONTEXT: Floating wind tech is suitable for deep waters, but currently Japan only has under 10 MW installed, including a site off Goto, Nagasaki. The new target will be in gigawatts. With no domestic wind turbine makers, Japan seeks to attract global players like GE Vernova and Vestas, but also build a local supply chain leveraging Japan’s strengths in foundations and cable components.

Japan’s largest onshore wind farm helps revitalize Fukushima area

(Nikkei, April 17)

- The Abukuma Wind Farm began commercial operations in Fukushima Pref’s Abukuma Highlands, an area severely affected by the 2011 nuclear disaster.

- With 46 turbines and a total capacity of 147 MW, it’s now Japan’s largest onshore wind facility. The power is partly used locally through corporate PPAs, supporting businesses like fish farming and local utilities.

- CONTEXT: The news was covered in Japan NRG’s April 7 issue. The wind farm cost ¥67 billion and spans four municipalities affected by the disaster. Part of the site was within a restricted zone until evacuation orders were lifted on March 31, 2025.

TAKEAWAY: Abukuma’s launch is a milestone not only for Fukushima’s recovery but also for Japan’s broader energy transition. By combining large-scale renewables development with local reconstruction efforts, this project shows how clean energy can revitalize post-disaster areas, stimulate local economies, and create new opportunities for communities.

Tohoku Electric acquires stake in GPI’s wind farm in Iwate

(Company statement, April 16)

- Tohoku Electric acquired an undisclosed stake in the 113 MW wind farm in Iwate Pref, which began operations in May 2023.

- Developed by Green Power Investment (GPI), the project features 27 Vestas turbines (4.2 MW each); with a 20-year FIT contract at ¥22/ kWh, valid through May 2043.

- CONTEXT: Tohoku Electric aims to reach 2 GW of renewables by the early 2030s, while GPI continues to expand its wind portfolio, including offshore projects and a newly-launched ¥61 billion wind-focused fund.

- SIDE DEVELOPMENT:

- Tokyu Land to build wind farm in Iwate

- (Company statement, April 1)

- Major real estate developer Tokyu Land announced the environmental assessment for its 56 MW onshore wind farm near Kuji City, Iwate Pref.

- The project aims to launch by March 2029; construction to start in April 2026.

- It will install up to 13 turbines, (each 4.3 MW capacity), and cover 848 hectares.

Tohoku Electric begins supply of wind and hydro power to TOPPAN via PPA

(Company statement, April 17)

- Tohoku Electric began supplying wind and hydro power to four TOPPAN group sites in Niigata, Miyagi, and Fukushima Prefs under a 20-year off-site corporate PPA.

- The agreement will deliver about 27 GWh of renewables annually. Power is sourced from wind farms owned by HSE’s subsidiary, Kuroshio Wind Power, and small hydro plants operated by the two districts.

JWA launches wind forecast confidence interval service

(Organization statement, April 15)

- JWA launched a new service for wind power operators that adds confidence intervals to its wind speed and power output forecasts.

- This feature will help operators assess the reliability of forecasts and manage the risk of over- or under-estimating power generation, which is crucial for creating accurate generation plans, especially under the FIP scheme.

- The service supports: Reliable power generation planning; Supply-demand balancing in power markets; Procurement planning by retailers; Strategies for aggregators and co-located battery systems; Early risk detection for power supply shortages.

Australian CTVs to serve offshore wind sector

(Company statement, April 15)

- Towage firm Tokyo Kisen welcomed the first of two custom-built crew transfer vessels (CTVs) to service Japan’s offshore wind sector. The two 26-meter CTVs can carry 12 technicians.

- The vessels are designed by Australian marine engineering firm Incat Crowther, and built by Cheoy Lee shipyard in China

NEWS: NUCLEAR

TEPCO’s 5th business plan discussions resume, target for summer completion

(Denki Shimbun, April 18)

- The Nuclear Damage Compensation and Decommissioning Facilitation Corp (NDF) resumed talks on TEPCO’s 5th Comprehensive Special Business Plan. It hopes to complete these issues in summer.

- Key focus includes improving cash flow, and funding must be ensured for decommissioning and compensation (¥500 billion a year). Reducing that amount could signal a lack of commitment. TEPCO cites inflation and safety-related investments as factors straining cash flow.

- There were calls for TEPCO to pursue alliances beyond its JERA venture.

- SIDE DEVELOPMENT:

Niigata rejects referendum on Kashiwazaki-Kariwa restart - (Nikkei, April 18)

- The Niigata Pref Assembly rejected a proposed referendum on restarting the Kashiwazaki-Kariwa NPP. The idea had strong public support.

- Governor Hanazumi, who opposed a simple Yes/No vote, plans to hold public hearings and surveys instead.

- Opposition parties supported the referendum, while the LDP and Komeito argued nuclear policy is a national issue.

TAKEAWAY: The main argument against a referendum was that its binary nature (Yes/No) did not reflect the complex reality of restarting a NPP. Yet, the biggest issue for the govt is that it would have set a precedent for any other nuclear power-related project in Japan seeking local consensus, which is often lacking.

Council for Spent Nuclear Fuel discusses management plans

(Government statement, April 17)

- The Council for the Promotion of Spent Nuclear Fuel Countermeasures discussed expanding storage capacity, both on-site and off-site, and promoting dry and intermediate storage.

- Also, it seeks to advance reprocessing and MOX fuel use, supporting the Rokkasho Reprocessing Plant and MOX Fuel Fabrication Plant.

- There’s also a strong emphasis on reducing plutonium stockpiles by increasing MOX fuel usage in reactors. The goal is for deployment in at least 12 units by FY2030.

- CONTEXT: Of the restarted reactors, only four are using MOX fuel. The goal of having at least 12 units by FY2030 aligns with FEPC goals.

TAKEAWAY: The govt made calls for nuclear power operators to collaborate with local communities and maintain the deadlines. For the former, it cited Kansai Electric, which has been postponing the solution for transporting spent fuel outside Fukui Pref at least since late 2022. For the latter, the focus was on TEPCO and Japan Atomic Power, which have to offer a clear deadline for fuel removal at the Mutsu facility.

Kyoto Fusioneering sets up subsidiary for demo

(Company statement, April 16)

- Kyoto Fusioneering set up a subsidiary, Starlight Engine, to focus on its fusion power demo project, FAST, and to build a dedicated structure.

- CONTEXT: Kyoto Fusioneering plans a demo in the early late 2030s. Site selection is underway. The project will develop a tokamak-type reactor, and must prove Deuterium-Tritium fusion and control of burning plasma.

NEWS: TRADITIONAL FUELS

Global gas-fired power generation to grow, MHI to increase production capacity

(Nikkei, April 16)

- Global gas-fired power generation capacity will grow 1.2 times by 2030 over 2023 levels, from 1,900 GW to 2,300 GW. Asia, especially China and India, will lead the increase. This trend is due to rising electricity demand, including from AI-driven data centers. Also, there is a shift away from coal to natural gas.

- MHI plans to increase gas turbine production capacity 30% by FY2026, and will invest about ¥50 billion to expand output of key components such as turbine blades.

- MHI competes in the gas turbine market with GE Vernova and Siemens Energy. In 2023, MHI led the global market with a 36% share for a second consecutive year.

OFS opens center in Malaysia as a hub for FPSO business

(Company statement, April 16)

- Offshore Frontier Solutions opened a new center in Kuala Lumpur, Malaysia. OFS is an affiliate of Toyo Engineering (TOYO) and Mitsui Ocean Development (MODEC).

- This center will serve as a hub for TOYO’s expanding FPSO (Floating Production, Storage, and Offloading) business. The center will supervise detailed engineering, overseeing construction and integration at shipyards.

- CONTEXT: MODEC and TOYO own 65% and 35% of the company, respectively.

LNG stocks same as previous week, down YoY

(Government data, April 16)

- As of April 13, the LNG stocks of 10 power utilities were 2.13 Mt, exactly the same as the previous week; but down 2.3% from the end of April 2024 (2.18 Mt), and 0.5% down from the 5-year average of 2.14 Mt.

March Oil/ Gas/ Coal trade statistics

(Government data, April 17)

Imports | Volume | YoY | Value (Yen) | YoY |

Crude oil | 10.8 million kiloliters | -13.6% | 805.8 billion | -17.2% |

LNG | 5.2 million tons | -7.2% | 468.5 billion | -11.6% |

Thermal coal | 8.3 million tons | 8.8% | 162.5 billion | -9.9% |

Gasoline prices to drop ¥10 as part of inflation countermeasure

(Nikkei, April 18)

- Starting May, the govt plans to reduce gasoline prices by ¥10/ liter to counter inflation. Subsidies for electricity and gas bills will resume from July to Sept.

- This should help household burdens during the high-cost summer period.

- CONTEXT: Gasoline prices were kept at about ¥185/ liter with subsidies phased out since December 2024 due to falling global crude oil prices. On April 17, the subsidy reached zero, on cheaper oil and a stronger yen.

NEWS: CARBON CAPTURE & SYNTHETIC FUELS

NEDO selects contractors for technology at CO2 Utilization Center

(Organization statement, April 11)

- NEDO selected contractors for tech development at the CO2 Utilization Center:

- Japan Carbon Frontier Organization: operation and research support;

- Tokai National Higher Education and Research System (Nagoya Univ), Kawada Industries: pioneering carbon recycling using ammonia and plasma;

- Tohoku University, Sumitomo Corp: carbon recycling type SiC synthesis using advanced resource utilization tech for silicon-based waste;

- Institute of Microalgal Technology, Nippon Steel: carrier culture tech for microalgae and productization of biomass for carbon recycling;

- Sekisui Chemical, Univ of Tokyo, Tokyo Institute of Science: Large-scale production tech for hydrogen-free, highly energy-efficient conductive carbon materials derived from CO2;

- Algal Bio: CO2 tech using microalgae and production of useful chemicals;

- Chugoku Electric, Fuji Oil Group: development of gas-to-lipid bioprocesses;

- ENEOS Globe: catalyst performance enhancement and production processes for carbon recycling LPG;

- CONTEXT: NEDO set up the R&D and Demonstration Base for Carbon Recycling in Osaki-kamijima (Hiroshima Pref) as a hub for activities by multiple companies and universities aiming to achieve a carbon-neutral and decarbonized society. The facility supports the development and demonstration of basic carbon recycling technologies using CO2 generated from an adjacent Integrated Gasification Combined Cycle (IGCC) CO2 capture and recovery demo plant.

INPEX starts pre-FEED for Bonaparte CCS

(Company statement, April 17)

- INPEX started the pre-FEED phase for the Bonaparte CCS Project offshore of Australia, about 260 km from Darwin. The project is developed through INPEX Browse E&P, TotalEnergies, and Woodside Energy.

- The pre-FEED phase follows a comprehensive evaluation phase, which included a 3D seismic survey covering 1,800 km² and drilling of two CCS appraisal wells.

- Results confirmed the presence of high-quality saline aquifer reservoirs and thick sealing formations. This is suitable for permanent CO2 storage.

- CONTEXT: The project will store over 10 Mt of CO2 a year. Injection will start about 2030. The project is now progressing toward applying for a GHG injection license. INPEX’s Ichthys LNG Project, also owned by TotalEnergies and Woodside, will likely be a major CO2 supplier for this CCS project.

Mitsui & Co invests in U.S. synthetic fuel company

(Company statement, April 16)

- Mitsui & Co invested in Infinium Holdings, a U.S.-based provider of gas conversion solutions and developer of synthetic fuel tech and projects.

- This is Mitsui’s second investment in the synthetic fuel area, following Twelve Benefit Corp in February.

- CONTEXT: Mitsui is advancing efforts across the carbon value chain, including CO2 recovery, storage, and utilization for synthetic fuels and carbon credits.

TAKEAWAY: By fostering collaboration among synthetic fuel firms, Mitsui aims to expand its carbon-neutral fuel business, integrate clean energy sources, and meet diverse fuel needs.

BY FILIPPO PEDRETTI

Japanese Firms Expand SE Asia LNG Projects as Region Shifts to Gas

Japan’s top utilities and energy companies are accelerating their LNG push into Asia as they seek to capitalize on new markets for the fuel. Southeast Asia is of particular interest and a key component of METI’s 2020 international energy strategy.

As of today, Japanese firms including JERA, Tokyo Gas, and KEPCO are active in about 30 projects across Asia-Pacific that span the entire value chain, from distribution infrastructure and regasification terminals, to gas-fired power plants. The proposed generation capacity of projects with Japanese involvement has climbed to about 60 GW.

The context is that Japan faces an oversupply of LNG in the coming years and needs to build ‘secondary’ markets to sell its surplus. Long-term offtake agreements with Australia, Qatar, Malaysia, and the U.S. helps to protect Japan’s security of supply but also lock buyers into volumes that the domestic market seems no longer able to absorb. Should METI’s own 2040 national energy mix forecasts materialize, demand will wane further.

Despite softening domestic demand, the government sees it as imperative to defend Japan’s position as one of the top players in the LNG sector. That means finely balancing new investment in supply and the demand side within an industry often susceptible to economic and political changes.

Japan NRG takes a look at the significant LNG-related projects with Japanese involvement in Southeast Asia, as well as at the region’s overall outlook in this sector.

JERA and Tokyo Gas

As Japan’s major LNG traders, JERA and Tokyo Gas are leading related infrastructure expansion in Asia. JERA has set a goal of introducing LNG to Asia’s coal-and-oil reliant countries, while Tokyo Gas seeks to develop a specifically South-Asian LNG chain.

The driver is straightforward: Japan wants to diversify its LNG supply sources to improve energy security. This necessitates creating new overseas markets for the fuel in places like Vietnam, Indonesia, and the Philippines. With more Asian nations turning to LNG, Japanese firms can play the role of re-seller, or trader of the fuel. And, if Japan suddenly runs short, there would in theory be more LNG cargoes in the region to buy or swap.

Source: Tokyo Gas

Of course, the opportunities for Japanese players are not limited to trading the molecules.

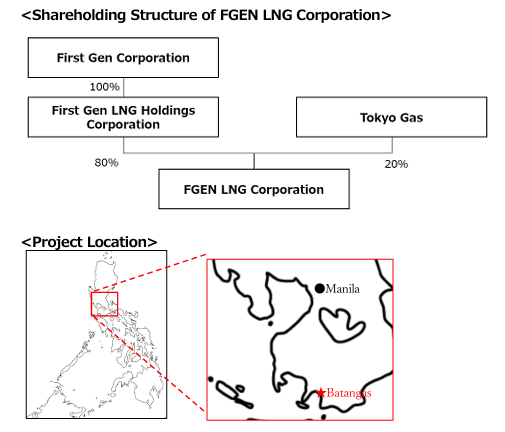

In February 2025, Tokyo Gas made its first investment in an operational overseas LNG terminal. It acquired a 20% stake in FGEN LNG Corp, which owns and operates a floating LNG terminal in Batangas City in the Philippines. Tokyo Gas said it will support the facility’s operations and maintenance, leveraging its experience of managing LNG terminals in Japan.

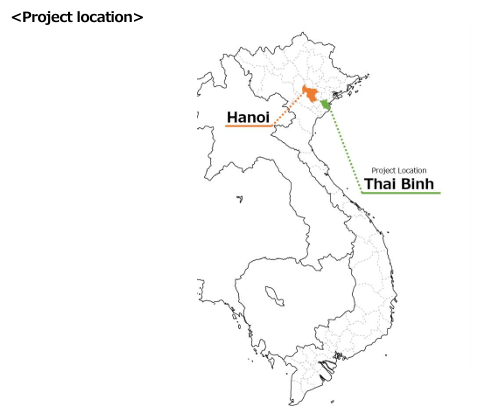

Further downstream, Tokyo Gas is involved in a LNG-to-power project in Thai Binh Province, Vietnam, that includes a 1.5 GW gas-fired power plant and an offshore LNG receiving terminal. The 2024 investment partners the Japanese gas utility with Truong Thanh Viet Nam (TTVN) and an overseas unit of Kyushu Electric – Kyuden International Corp. The goal is to start power operations by 2029.

The above has built on another Vietnamese LNG-to-power project Tokyo Gas launched in 2022. The $2 billion project involves bringing gas-fired power to the Quang Ninh Province, with operations slated for the latter half of the 2020s.

The arrival of gas-fired power and LNG imports to Southeast Asia is a recent phenomenon.

The Philippines and Vietnam only began importing LNG in 2023, as did Hong Kong. The first LNG cargoes reached Cambodia and Myanmar just a few years before that.

Population and economic growth, however, are pushing a very steep demand trajectory. Petrovietnam’s PV Gas estimates that the nation’s LNG imports will reach 9 million tons per annum (MTPA) by 2030 and 15 MTPA by 2035, for a total value of $7.2 billion. Despite this, Vietnam has not secured any long-term LNG contracts; the same for the Philippines.

Source: Tokyo Gas

This means Japanese firms are not only playing the role of LNG sellers – they are helping to prepare the institutional and logistical networks for Southeast Asia to lean into the fuel. In December 2023, JERA signed an MoU to assist with the introduction of LNG in the Philippines. For value chain development, JERA also signed an MoU with a subsidiary of Indonesia’s state-owned electricity company PLN for collaboration.

Previously, JERA proposed a 4.5 GW LNG-fired power plant and import terminal with ExxonMobil in Vietnam. Should it go ahead, that project alone would require imports of about 6 MTPA. Such volumes would complement JERA’s sales in its domestic market and allow it to redirect LNG vessels to balance surpluses / shortages in Japan.

The origin of much of this LNG is likely to be Australia and the U.S. JERA sees U.S. LNG as an attractive option: there is abundant supply, relatively low costs, and now with Trump in the White House – strong support from the government. At the very least, this indicates that U.S. projects would get faster approval for construction and exports compared to Australia.

Flexible contract terms in the U.S. market are another big selling point for Japanese firms like JERA that have ambitions to trade LNG in the Asia region. JERA is leveraging the flexibility of American contracts to push Australian suppliers to do the same.

Main proposed LNG-related activities in Southeast Asia by Tokyo Gas and JERA, 2019-2025.

Company | Location | Details |

Tokyo Gas | Philippines | LNG Terminal in Batangas City (with FGEN LNG Corp) |

Tokyo Gas | Vietnam | 1.5 GW Gas Power Plant and LNG receiving terminal in Thai Binh Province (with TTVN and KIC) |

Tokyo Gas | Vietnam | 1.5 GW Gas Power Plant and LNG receiving terminal in Quang Ninh Province (with Marubeni, PV Power, Colavi) |

Tokyo Gas | Thailand | Launching of Gulf WHA MT Natural Gas Distribution Company Limited (private gas distribution) |

Tokyo Gas | Indonesia | Stakes in city gas distributors PT Energy Mina Abadi and PT Super Energy |

JERA | Vietnam | 4.5 GW LNG-to-power project + Ca Na I LNG plant (1.5 GW) and Ca Na LNG terminal (97,000 tons) |

JERA | Vietnam | Establishment of JERA Energy Vietnam to promote LNG-to-power project |

JERA | Philippines | Agreement with the Association for Overseas Technical Cooperation and Sustainable Partnerships (AOTS) for LNG infrastructure development |

JERA | Philippines | Stake in Aboitiz Power Corporation |

JERA | Indonesia | Subsidiary PT JERA Energi Indonesia (JERA EI), aiming for LNG supply |

JERA | Bangladesh | Stake in Summit Power International Limited (Power generation, LNG supply) |

Source: Tokyo Gas, JERA, IEEFA, JOGMEC.

Asia’s LNG landscape

Global LNG demand is expected to grow to 630-718 MTPA by 2040, up from the 407 MTPA in 2024, with Asia the main driver behind this 60% growth, according to Shell. By 2030, Shell forecasted a growth of 170 MTPA.

Analysts at the environmental think-tank IEEFA are more circumspect. Such a boom in LNG implies a shift away from coal and no serious competitive threat from other energy sources. Meanwhile, coal’s share of the energy mix hit a record (62%) in Indonesia in 2023 – similar to levels in the Philippines. Plus, the average age of coal-fired power plants was just 11 years when the IEA last reported the data in 2021.

Another issue is the slow progress of many Southeast Asia LNG projects, primarily in terms of contracting and negotiation. For example, Tokyo Gas and Pertamina in 2015 worked on an LNG terminal in Indonesia, but it was deferred due to uncertain demand.

What’s more, Japan is not the only LNG powerhouse in Asia anymore. Looking at the Asian market, there are at least two major competitors to Japan’s LNG export strategy: China and Singapore. China has overtaken Japan as the world’s largest LNG importer, and with its U.S.-origin cargoes now under the cloud of tariffs, Chinese trading volumes are rising.

Still, Japan’s state energy firm JOGMEC believes that Tokyo’s strategy has every chance of success. When asked by Japan NRG, JOGMEC noted that while Chinese imports this year are at the lowest levels since 2019, intensified LNG trading activity by China and Japan is likely to be complementary. The two can inject liquidity and volumes in the Asian market, supporting the trend rather than directly competing with each other.

Singapore is also positioning itself as a major LNG trading hub thanks to its hosting of many financial institutions, oil companies, and trading platforms. Most of the Japanese firms have also opened LNG trading desks in the city.

Japan cannot compete with the financial infrastructure of Singapore but it has made a start. The Tokyo Commodity Exchange, for example, launched yen-denominated LNG futures in 2022, though growth in trading volumes has been slow. Expanding this market will be crucial to Japan’s ability to hedge against price fluctuations.

Conclusion

For Japanese firms, securing a foothold in Southeast Asia by participating in infrastructure projects allows them to retain leverage in price negotiations. The LNG market is projected to expand in the region, and Japan’s industry veterans smell a business opportunity.

Still, Japan claims that its LNG strategy is not only about economic advantage, but also a matter of energy security. As the country looks to buy more LNG from the U.S., so as to appease the Trump administration, the plan of reselling LNG to Asian countries gains further strategic significance amid shrinking domestic demand.

Through recent initiatives such as the Asia Zero Emission Community (AZEC), Japan has laid the political groundwork to promote LNG as a critical bridge fuel in the transition to a lower-carbon future. For this, critics accuse Japan of locking Asia into another fossil fuel.

Yet with few other actors coming into the region to finance major shifts to other energy sources, Japan’s offer may be the most pragmatic on the table.

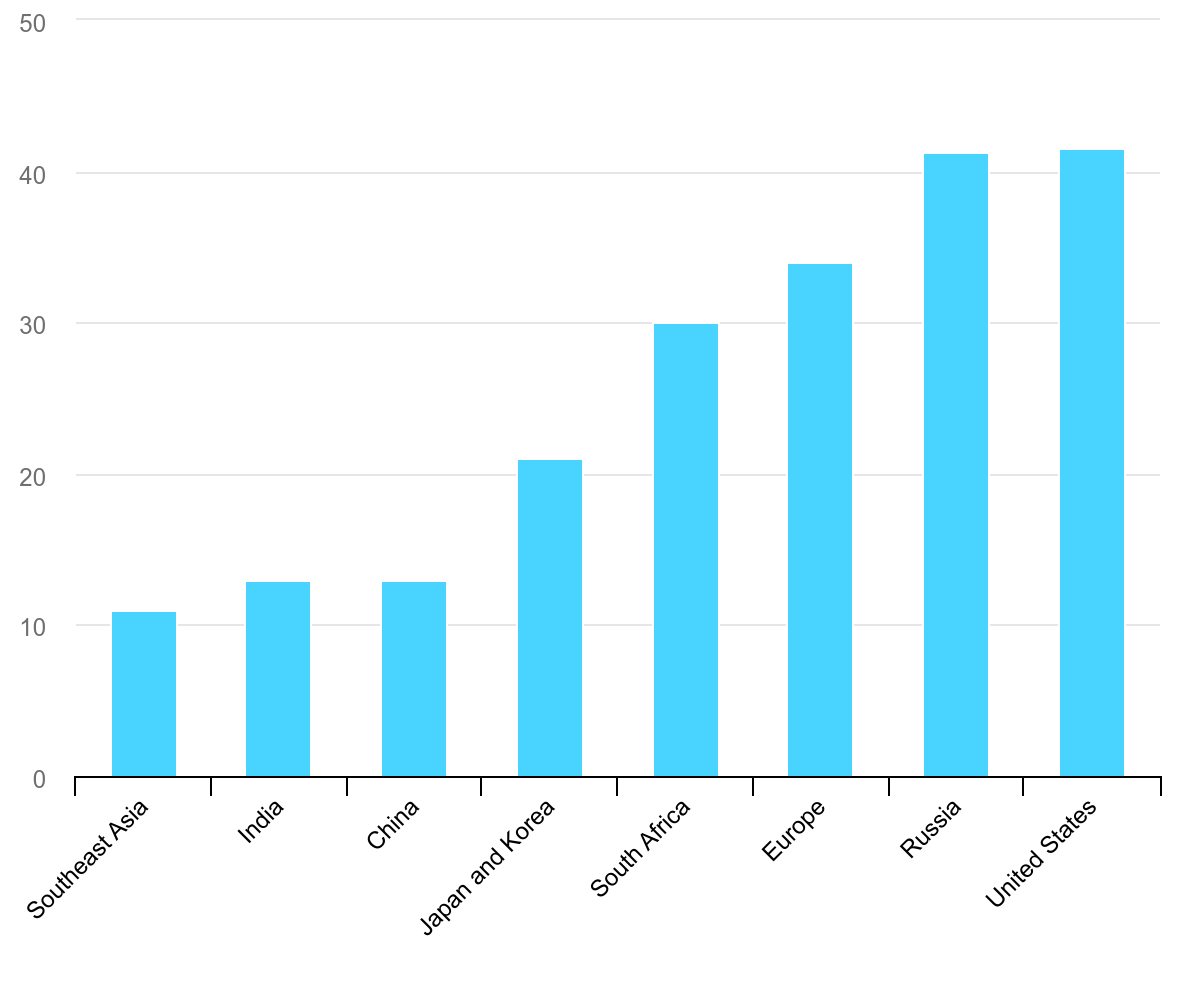

Average age of existing coal power plants in selected regions in 2020

Source: IEA

BY TETSUJI TOMITA

What’s That Smell? E-Methane Pitches an

Alternative to the Hydrogen Society

Japan has created artificial islands using landfill waste. One such plot in Tokyo Bay even has the cheerful name “Dream Island.” Now, the country is putting waste to use in a supply chain that offers a cleaner alternative to fossil fuels.

Last year, a demonstration project in Osaka City, currently host to the World Expo, utilized raw garbage and renewable energy to produce e-methane, a synthetic gas that promises to recycle CO2 without adding to the global carbon footprint, all while utilizing existing gas infrastructure. A similar pilot is in operation just south of Tokyo, in the city of Yokohama. And while small, the tests indicate the potential for mass scale production already by the end of this decade.

Capturing the gases emitted from burning waste is just one of the pathways Japan is trialing to form the outline of a next-generation, low-carbon gas system. While electrification is expected to shift some of the energy demand from molecules to electrons, the country is still one of the top importers of natural gas via LNG. Almost half of those volumes are deployed in heating and industrial equipment – areas that are harder to electrify and abate. That suggests a substantial market for cleaner gas substitutes.

Traditionally, the process of methanation involves synthesizing methane from hydrogen and CO2. The latter is recovered from the atmosphere or industrial emissions. When the hydrogen is made with renewable energy, the end-product is called e-methane. Like the liquid synthetic fuels (e-fuels), e-methane is touted as the future lynchpin of energy systems because it does not increase atmospheric CO2 levels over its lifecycle and has higher heating value per unit than hydrogen or ammonia when combusted.

One of the biggest stumbling blocks to creating an energy system based on synthetic fuels like e-methane, however, has been the cost of producing hydrogen (H2). This is why Japan has started testing several ways to make e-methane, some of which do not require H2 as a feedstock.

Current gas needs

In Japan, the majority of natural gas is imported as LNG, and the consumption ratio (in FY2022) was 54% for electricity, 35% for city gas, and 10% for other uses. The breakdown of city gas use by sector was 59% for industrial, 23% for residential, and 10% for commercial.

Industrial use is primarily as a fuel for heat source equipment, such as steam boilers and furnaces, and as a fuel for power generation. Residential and commercial use is primarily for heat source equipment such as kitchens, water heaters, and space heaters.

To reduce GHG emissions, various firms have developed gas turbines and boilers, etc that can switch to hydrogen or ammonia, and some electrified options are also starting to appear. Still, in cases where there’s a need for high temperatures and/or large equipment, retaining existing gas-based supply chains and infrastructure but switching to a cleaner fuel is seen as ideal.

R&D Trends in e-Methane

Methanation methods can be broadly divided into chemical and biological reactions. The former relies on the Sabatier reaction (CO2 + 4 H2 → CH4 + 2 H2O) with a catalyst, but the scale of the output needs to be grown. Much of Japan’s R&D in this area is focused on finding more efficient synthesis through discovering better catalysts.

Methanation using biological reactions (bio-methanation) swaps the catalyst for methane-producing bacteria. However, its scale at this point is even smaller than for a chemical reaction.

e-Methane Production Technologies

Reaction | Methanation | Reaction Temp. | Energy Efficiency | Feature | Development Organizations | |

Chemical | Conventional | Sabatier | around 500°C | 55-60% | fundamental technology | INPEX IHI Kanadevia |

Innovative | Hybrid Sabatier | around 220°C | over 80% goal) | no H2 requiredhigh efficiency (waste heat use) | Tokyo Gas JAXA | |

PEM CO2 | around 80°C | over 70%(goal) | no H2 required reduce equipment costs (1-step reaction) larger size | Tokyo Gas | ||

SOEC | around 800°C | 85-90% (goal) | no H2 require high efficiency (waste heat use) | Osaka Gas AIST | ||

Biological | Methanation by Microbial Function | – | – | laboratory level efforts | Tokyo Gas Osaka Gas | |

Source: METI

Pilot projects

E-methane as a clean energy solution has drawn interest from numerous sectors including shippers, heavy duty transportation (i.e., trucks and buses), high-temperature industrial processes (steel, cement, and ceramics), as well as the chemical industry.

The main companies driving the development of e-methane in Japan, however, are the two large gas utilities from Tokyo and Osaka, the oil and LNG producer INPEX, and the top engineering group, Mitsubishi Heavy Industries (MHI).

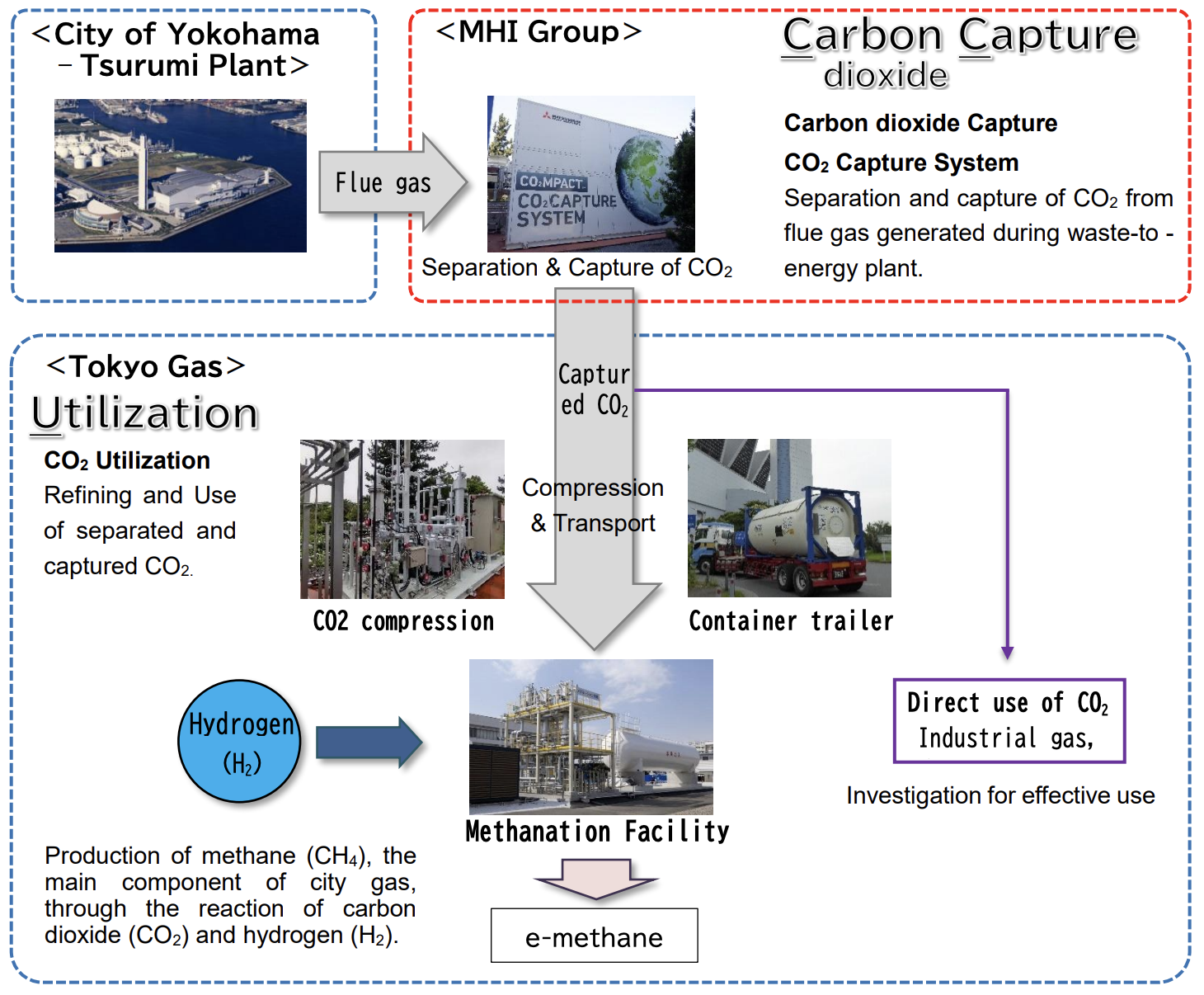

Tokyo Gas started small-scale methanation tests in 2021, which progressed into a pilot project that pools together several players into a fully contained local supply chain. Thanks to an agreement with Yokohama City in 2022, MHI installed a system to capture flue gas at a municipal waste-to-energy facility (Tsurumi Plant) that is then transported to the Tokyo Gas Yokohama Techno Station for methanation using the Sabatier method.

The pilot operates at a rate of 400-500 Nm3 of e-methane per hour. In the 2030s when the technology is deemed mature, this is expected to ramp up to tens of thousands of Nm3/ h.

Assuming a methanation facility with a nameplate capacity of 10,000 Nm3 is able to run nonstop year-round, its annual output would be close to 88 million Nm3. This would help Tokyo Gas get close to its requirement of substituting 1% of city gas sales with e-methane by 2030, as per the national target. (Based on a m3 to Nm3 conversion that assumes the gas is transported at near atmospheric pressure and at standard temperature.)

Process of the e-methane supply chain that Tokyo Gas is building

Source: Tokyo Gas

Osaka Gas and INPEX have a similar scale Sabatier methanation project (400 Nm3/ h) that aims to use the synthetic fuel in the local gas pipeline system. Gas extracted from one of Japan’s largest gas fields, in Nagaoka, Niigata Pref, will be sent to a methanation facility due to be commissioned this (FY2025) fiscal year.

Source: INPEX

To spread public awareness of methanation as a future clean energy pathway, Osaka Gas has also created a small-scale pilot to coincide with the World Expo, which kicked off April 13 in the company’s home city.

The project is deploying the Sabatier method to extract biogas from household waste (CH4), supplement it with CO2 collected through Direct Air Capture, and bind it to hydrogen made with renewable energy. Kanadevia supplied the methanation equipment.

Other approaches

The Green Innovation Fund has seeded a number of projects to develop other methanation methods, such as a “hybrid Sabatier” approach, which relies on PEM electrolyzers (the “PEMCO2 Reduction” system), and new technologies that work at low temperatures.

The hybrid Sabatier process claims not only to improve efficiency (from 50% to 80%) by more effectively utilizing waste heat from electrolysis (an endothermic reaction), but also promises to make devices smaller and at a lower cost. Among potential future demand centers is Japan’s space agency. JAXA and MHI are developing a liquid methane-fueled engine for a next-generation rocket that is expected to take off around 2030.

Electrochemical reduction (PEMCO2) is a technology that reacts at low temperatures (about 80°C), eliminating the need for thermal management, which is a problem with the Sabatier reaction. PEMCO2 is also a much simpler industrial structure, making it cheaper. The main proponent of this approach is MHI’s domestic rival IHI Corp, which sees this tech as capable of manufacturing from tens to several hundred Nm3/ h by FY2030.

The most interesting approach, however, may be pursued by Osaka Gas. The west Japan utility is backing the development of bio-methanation and Solid Oxide Electrolysis Cell (SOEC) – this methanation process uses Solid Oxide Fuel Cell (SOFC) technology. First, water and CO2 are electrolyzed using an SOEC electrolyzer to produce H2 and CO using renewable energy. Next, methane is synthesized from these in a catalytic reaction. Not requiring hydrogen as a raw material is a key feature.

In addition, electrolysis at high temperatures (around 700-800°C) reduces the amount of renewable energy required. By effectively utilizing the heat generated during methane synthesis, it is possible to achieve a world-leading energy conversion efficiency of 85-90%. The result could significantly reduce the cost of producing e-methane.

Together with the National Institute of Advanced Industrial Science and Technology, Osaka Gas hopes to develop SOEC methanation-related technologies into a unified supply chain by 2030.

International cooperation

The domestic projects offer glimmers of technological progress, but for volume, Japanese companies are looking elsewhere. A Japan-U.S. consortium including Tokyo Gas, Toho Gas, Mitsubishi Corp and Sempra Infrastructure is promoting the ReaCH4 Project on the Gulf Coast of the U.S.

The aim is to build the world’s first large-scale e-methane supply chain that will be capable of producing 180 million Nm3 of e-methane (close to 130,000 tons) in FY2030. Sempra refers to e-methane as e-natural gas and intends to use its Cameron LNG terminal in southwest Louisiana for liquefaction of the gas before its transport to Japan.

In November 2023, Tokyo Gas and Santos announced plans to conduct a feasibility study on a project to produce e-methane in the Cooper Basin in central eastern Australia. The Australian energy firm has developed gas fields in the area for decades. The project aims to export 60,000 tons of e-methane per year (equivalent to 80 million m3 of city gas) to Japan from 2030, with a view to scaling that up even further.

Osaka Gas is conducting feasibility studies across several regions but especially in America, Australia and Southeast Asia, looking to build on existing natural gas and LNG facilities. The utility is keen on establishing an e-methane hub in either Nebraska or western Wyoming where it can source cheap hydrogen, and then send the product by pipeline to Texas to ship to Japan.

The utility is ready to invest as much as ¥100 billion in the U.S. e-methane projects and wants to import as much as 200,000 tons of the synthetic fuel by 2030. Work on basic project design started earlier this year.

To build the sector’s visibility, in October 2024, Japanese firms founded an international alliance called e-NG Coalition to pool together firms that promote e-methane (aka e-natural gas). They want to create a global market by standardizing GHG emission calculation and certification standards.

The nine founding companies were Tokyo Gas, Osaka Gas, Toho Gas, Mitsubishi Corp, Engie, RWE, Sempra Infrastructure, Tree Energy Solutions Belgium (TES) and Totalenergies. Since then, the membership has increased to 20 with IHI and INPEX among the new faces.

How to pay for this?

As with e-fuel, the biggest issue for e-methane is reducing production costs, which are typically five times that of LNG. According to some producer’s calculations, the cost of synthetic methane (CIF price) is currently ¥250/ Nm3 using the Sabatier method. The plan is to reduce this to about ¥120/ Nm3 by FY2030, and to ¥50/ Nm3 by FY2050 through better technology and lower hydrogen feedstock.

Even that price trajectory requires additional fees. For now, Japan is considering a number of approaches to cover the price gaps including some form of an e-methane marketplace, or by further expanding quotas from the current 1% by 2030.

The latter would still require a way for the buyers to pass on the higher costs compared to LNG. These may be addressed either through a contract for difference (CfD) support scheme, as already initiated late last year on the back of the Hydrogen Society Promotion Act. Another alternative is the gas wheeling charges system.

It’s likely that several of the above will need to be put into place within the next three years or so to enable e-methane to gain a foothold in Japan’s energy system. The results of this year’s CfD – which allows the subsidies to cover e-methane – may be the first indication of which way the sector will develop commercially.

ASIA ENERGY REVIEW

BY JOHN VAROLI

A brief overview of the region’s main energy events from the past week

Australia / Renewables

ACEN Australia completed its AU$750 million portfolio debt financing to support renewable energy expansion. The financing will support the 400 MW Stubbo Solar project in New South Wales.

Australia / Solar power

Octopus Australia will soon start construction on the AU$300 million Fulham Solar Farm. The project will have an 80 MW solar farm and a 128-MWh battery project.

China / Coal

Coal production set a new monthly record of 441 Mt in March, as the country focuses on increasing domestic output and reducing reliance on imports. Coal production has totalled 1,203 Mt so far this year, up from 1,106 Mt in the same period in 2024, and surpassing the previous record of 1,153 Mt in 2023.

Data Centers/ Electricity demand

Electricity demand from data centers worldwide is projected to more than double by 2030 to around 945 TWh, said the International Energy Agency. Electricity demand from AI-optimized data centers alone will more than quadruple by 2030.

India / Hydro power

The Central Electricity Authority approved six hydro projects – Upper Indravati (600 MW) in Odisha; Sharavathy (2 GW) in Karnataka; Bhivpuri (1 GW) in Maharashtra; Bhavali (1.5 GW) in Maharashtra; MP-30 (1.9 GW) in Madhya Pradesh; and Chitravathi (500 MW) in Andhra Pradesh.

India / LPG

India plans to end taxes on U.S. ethane and liquefied petroleum gas (LPG) imports as it looks to reduce its trade surplus and ease its tariff burden.

India / Renewables

India continues to expand renewable energy capacity, installing nearly 30 GW of solar and wind power in FY2025. According to JMK Research, compared to 2024, installations for both solar and wind increased 58.5% to 23.8 GW and 27.9% to 4.1 GW, respectively.

Indonesia / LPG

Indonesia proposed increasing imports of crude oil and LPG from the U.S. by $10 billion as part of tariff negotiations, said energy minister Bahlil Lahadalia.

Singapore / Power grid

Singapore is stepping up efforts to strengthen its power grid and diversify energy sources, with natural gas — currently powering 95% of the country’s electricity — still playing a major role. As the city-state targets GHG emissions of 45 Mt to 50 Mt by 2035, authorities face the dual challenge of meeting rising energy demand while decarbonising the grid.

Vietnam / Power plan

The latest amendments to the Power Development Plan, approved by the govt earlier this week, call for the nation to more than double total generating capacity by 2030 over 2023 levels, with the aim of increasing capacity nearly 10-fold by 2050. Solar and wind power will be key. To meet these targets, Vietnam needs a total investment of $136 billion by 2030.

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Hulic Ochanomizu Bldg. 3F, 2-3-11, Surugadai, Kanda, Chiyoda-ku, Tokyo, Japan, 101-0062.