WEEKLY

May 12, 2025

ANALYSIS

BOOMING BESS AND NUCLEAR RETROFITS WIN BIG IN ROUND 2 OF LTDA AUCTION

- The second Long-Term Decarbonized Power Sources Auction confirmed the explosive growth of the battery energy storage market

- The results also reflect the state’s willingness to help cover safety upgrades of NPPs and the importance energy planners put on LNG’s role

ENERGY JOBS IN JAPAN: MAKING THE MOST OF A CHANGE IN COMPANY OWNERSHIP

- Development platforms sponsored by private equity funds typically have a limited investment time horizon in which they seek to maximize portfolio value with a view to exit

- As an employee, how can you act and react to such changes? What opportunities exist in a change of ownership situation? What threats should you be aware of and prepared to navigate?

ASIA PACIFIC REVIEW

This column provides a brief overview of the region’s main energy events from the past week

NEWS

- GHG emissions hit record low; focus on concrete, blue carbon initiatives

- Ex-trade minister Seko comments on Japan-U.S. energy cooperation

- EGC finalizes plan to revise imbalance charges

- Major utilities forecast lower revenue and profit amid rising costs

- Electricity spot market sell-bids hit record high

- Sumitomo extends UAE gas power plant contract

- Marubeni signs offtake from Exxon ammonia plant

- China overtakes Japan in hydrogen patent competitiveness

- TOCOM conducts 1st green hydrogen trial trading

- JOGMEC to launch survey for natural hydrogen

- BESS secures multiple wins in LTDA auction

- ANRE to boost demand for next-gen solar cells

- Nickel-based batteries regain attention for safety and sustainability

WIND POWER AND OTHER RENEWABLES

- Kyuden Group to expand renewables 15-fold

- Eurus inks deal on Japan’s first market-linked project finance for wind farm under FIP

- TEPCO EP sells wind farm naming rights

- MHI discusses NPP replacement with component producers

- Hitachi GE Nuclear Energy to supply equipment for Canada’s first SMR project

- QatarEnergy negotiates long-term LNG deal with JERA and Mitsui

- JERA again mulls joining Alaska LNG Project

- MODEC to produce FPSO vessel domestically

CARBON CAPTURE & SYNTHETIC FUELS

- Japan, Malaysia to cooperate on CO2 storage

- Japanese and Thai firms join for decarbonization

- Japan’s first SAF begins supply flights

EVENTS

June 4-5 Kyushu Innovation Week / Kyushu GX Decarbonization Expo @ Marine Messe Fukuoka

June 4-6 AXIA EXPO 2025 (Hydrogen and Ammonia Next-Generation Energy Exhibition) @ Aichi Sky Expo

June 15-17 G7 Summit @ Kananaskis, Alberta, Canada

June 18-20 Japan Energy Summit & Exhibition ` Tokyo Big Sight

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Chief Editor)

John Varoli (Senior Editor, Americas)

Kyoko Fukuda (Data, Events)

Magdalena Osumi (Renewables & Storage)

Filippo Pedretti (Thermal, CCS, Nuclear)

Tetsuji Tomita (Power Market, Hydrogen)

George Hoffman (Sales, Business Development)

Tim Young (Design)

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

NEWS: GENERAL POLICY AND TRENDS

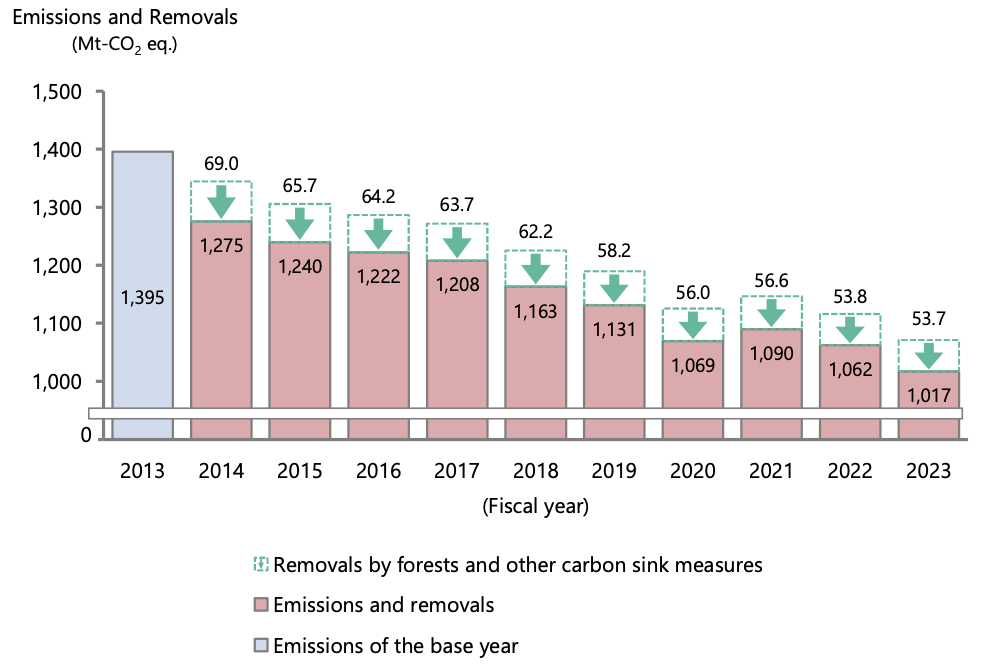

GHG emissions hit record low; focus on concrete, blue carbon initiatives

(Government statement, April 25)

- Japan’s total GHG emissions fell 4.2% YoY to about 1.017 billion tons of CO2 equivalent in FY2023, a record low and a 27.1% drop over FY2013.

- Key factors include increased decarbonization of electricity supply (renewables and nuclear surpassing 30% of total) and reduced domestic manufacturing, says an MoE annual report on National Greenhouse Gas Emissions and Removals.

- Emissions of fluorinated gases (HFCs, PFCs, SF6, NF3) fell 3.9% from the previous year to around 37 Mt, continuing the decline that began in 2022.

- MoE reports that CO2 absorption through forests and blue carbon remained little changed YoY at around 53.7 Mt, covering about 14.2% of total emission reductions since 2013; meanwhile, CO2-absorbing concrete (CCU) expanded significantly to 121 tons from 27 tons in FY2022, with plans to accelerate carbon-credit certification.

- MoE also said that offshore blue carbon initiatives will be expanded. The govt plans to establish a promotion system through the collaboration of the relevant ministries and agencies and public-private partnerships.

TAKEAWAY: Japan NRG has covered CO2-absorbing concrete in several prior Analysis texts and, while it is an interesting technology, the usual issues of cost and consumer-side pressure are yet to be resolved. However, the blue carbon initiative is worth paying attention to and could prove to be a niche but important part of Japan’s strategy to reach NDC targets.

Source: MoE

Ex-trade minister Seko comments on Japan-U.S. energy cooperation

(Facta, April 30)

- CONTEXT: In an interview with the monthly magazine, ex-METI minister Seko expressed optimism about the long-term prospects of Japan–U.S. energy cooperation.

- Seko advocates using gestures, such as visiting sites like Alaska’s LNG fields and publicly expressing interest as a tactic to resonate with President Trump. Seko even suggests the Alaska LNG project might eventually become a Japan–U.S.–Russia trilateral energy initiative, once geopolitical conditions allow.

- Japanese negotiators must prepare theatrical, persuasive responses that appeal to Trump personally. Seko also suggests using visual storytelling – such as maps showing Japanese investment creating jobs in the U.S. and numbers-driven presentations – which was effective during past negotiations.

- To counter trade shocks and possible recession, Japan must be ready with monetary easing, tax cuts, and fiscal spending. Diplomatically, Japan should take the lead in ASEAN and act as a bridge between the EU, TPP, and RCEP to uphold free trade.

- Seko also praised Akazawa’s recent talks with Trump, urging critics to focus on diplomacy and results over appearance.

TAKEAWAY: Japan is mulling further U.S. investments as a way to avoid the potential economic blow of tariffs. One such investment could be in the Alaska LNG, which could also aid broader geopolitical interests, especially defense cooperation and energy competition with Russia. Taiwan has recently agreed to import LNG from a potential future Alaska project and Thailand has made similarly positive noises. This adds pressure on Japan to follow, but how the government and private companies would share the responsibility for such a large project and investment is as yet unclear.

- SIDE DEVELOPMENT:

Sojitz launches carbon credit fund with U.S. firm - (Nikkei Asia, May 1)

- Sojitz is launching a $200 million carbon credit fund in partnership with the U.S.-based Ecotrust Forest Management and others to focus on sustainable forest management in the U.S. Pacific Northwest. It will generate carbon credits.

- The goal is to enhance carbon absorption by optimizing logging and promoting biodiversity. Investors will benefit through carbon credits and financial returns.

Hitachi eyes growth from energy grid business despite Trump policy risks

(Nikkei, April 28)

- Hitachi expects its power grid business to drive growth over the next three years, despite potential U.S. policy shifts under Trump. In FY2024, its Green Energy and Mobility segment led profit growth, rising 85% to ¥369 billion.

- For FY2025, Hitachi forecasts a 15.3% rise in net profit to ¥710 billion.

- A new three-year plan aims to boost operating margin to 13–15%, and expand services around core businesses like trains and grid systems. It will invest ¥500 billion in data centers, possibly through acquisitions.

TAKEAWAY: Hitachi remains bullish on its grid business despite possible reversals in U.S. clean energy support. The uncertainty of U.S. energy regulations presents a challenge for foreign firms, but Hitachi’s focus on diversified global growth strategies, including digital and green energy, is expected to help mitigate these risks. This also underscores the global momentum behind energy infrastructure upgrades.

Regulator urges utilities to split non-fossil certs pricing from electricity

(Denki Shimbun, April 28)

- Japan’s Fair Trade Commission recommended that major utilities clearly separate prices for electricity and non-FIT non-fossil certificates in internal transactions between generation and retail units.

- The regulator flagged possible antitrust violations if utilities provide these certificates free to their retail units but charge independent power retailers.

- CONTEXT: Of the 10 major utilities, eight already separate pricing, while two continue unified pricing under long-term contracts predating the establishment of the non-fossil market.

- The commission also advised lowering the current minimum bid requirement of 100 MW for renewable energy in long-term decarbonization auctions and supported allowing renewable projects with battery storage to participate in capacity markets.

NEWS: ELECTRICITY MARKETS

EGC finalizes plan to revise imbalance charge system

(Government statement, April 25)

- The Electricity and Gas Market Surveillance Commission (EGC) finalized a proposal to revise the imbalance charge system.

- A key topic was the “Cumulative Price Threshold System,” which lowers the cap on imbalance charges in areas where spot market prices remain high.

- Starting FY2026, the revised system sets imbalance charge caps at ¥50 when reserve rates are at 8%, and ¥300 when below 3%. If spot prices exceed ¥200 in 30 slots over seven days, the imbalance charge cap in that area will drop to ¥100 the next day.

- CONTEXT: The imbalance charge is a unit price that offsets the excess or shortfall of actual supply and demand, and serves as the basis for price signals. This system is designed to impose reasonable costs on those who cause imbalances and to provide appropriate incentives to system users.

TAKEAWAY: Although expanding the system’s coverage to prevent price inconsistencies was discussed, it was deemed unnecessary due to high costs and the low chance of such issues. The revised plan will be open for public comment in May, and the new rules could start in April 2026 after official approvals.

Major utilities forecast lower revenue and profit amid rising costs

(Company statements, Denki Shimbun, May 2)

- Nine of the 10 major regional power utilities (EPCOs) project lower revenue, and eight see profit declines for FY2025, citing higher material, labor, and equipment costs due to inflation.

- Only TEPCO has yet to release a forecast.

- In FY2024, sales reached record highs for Hokuriku, KEPCO, Shikoku, Kyushu, and Okinawa due to increased electricity sales. Operating profits declined at eight, except Shikoku and Okinawa. Still, six companies saw their second-highest profit levels ever.

- In FY2025, lower fuel prices and reduced electricity demand are expected to crimp revenue. Challenges include inflation and competition in wholesale/ retail power. Costs are also rising.

- Kansai Electric faces reduced nuclear plant utilization due to an increased period of time its units will spend in scheduled maintenance.

- Hokkaido Electric sees costs related to restarting Tomari NPP Unit 3.

- Chubu Electric forecasts a decline due to rising grid maintenance costs.

- Hokuriku Electric expects reduced wholesale power sales.

- Shikoku Electric anticipates higher repair costs for thermal plants.

- Most utilities are concerned over potential U.S. tariff impact; Chubu Electric noted that a similar policy in 2019 caused a 2 TWh drop YoY in industrial demand in the region, suggesting possible negative impacts worth billions of yen.

Ordinary income, excluding extraordinary impact (in billions of yen)

EPCO | FY2024 | FY2025 |

Hokkaido | 62 | 33 |

Tohoku | 234.7 | 190 |

Tokyo | 252.4 | – |

Chubu | 264 | 210 |

Hokuriku | 86 | 45 |

Kansai | 532.6 | 380 |

Chugoku | 117.5 | 75 |

Shikoku | 88.1 | 50 |

Kyushu | 184.6 | 158 |

Okinawa | 3.2 | 3 |

Electricity spot market sell-bids hit record high

(Denki Shimbun, April 28)

- Sell-bids on the Japan Electric Power Exchange (JEPX) reached a record daily average of 1.327 TWh in March, up 3.4% from February, driven by subdued demand despite increased plant maintenance.

- Monthly total sell bids were at an all-time high of 41.1 TWh, a 14.4% increase MoM, while buy-bids declined 2.8% to 29.55 TWh.

- Daily average buy-bids fell 12.2% from February to 0.954 TWh, reflecting warmer weather and reduced electricity consumption.

Hokkaido Electric eyes early launch of Ishikari-wan Shinko Unit 3

(Company statement, April 28)

- Hokkaido Electric will move up the start of operations for LNG-firing Ishikari-wan Shinko Power Plant Unit 3 to FY2033, four years earlier than the planned December 2037 start. This follows its successful bid in the second round of Long-term Decarbonized Power Sources Auction, results of which were disclosed on April 28.

- CONTEXT: In 2023, the company delayed the start of Unit 2 to Dec 2034 and Unit 3 to Dec 2037. In 2024, they moved Unit 2’s schedule up to within FY2030. The power plant is being developed with future hydrogen co-firing in mind. It currently has one 569 MW LNG-firing unit in operation.

Mitsubishi’s DGA joins ACEN for early coal-fired power shutdown in Philippines

(Company statement, May 7)

- Mitsubishi Corp and its subsidiary Diamond Generating Asia (DGA) joined ACEN, GenZero, and Keppel Ltd.

- Their goal is to use transition credits for early retirement of a 246 MW coal-fired power plant in the Philippines. Mitsubishi and DGA offer this access to Japan’s trading emission scheme.

- The plant’s operator is South Luzon Thermal Energy Corp. It aims to retire the plant by 2030 instead of 2040, and replace output with clean energy.

- CONTEXT: Transition credits are a new type of high-integrity carbon credit. The award is for replacing coal plants with renewables. This mechanism, approved under Verra’s Verified Carbon Standard, could become a model for more coal-fired power plants to be shut down.

TAKEAWAY: Retiring a coal-fired power plant can prove to be costly, especially in SE Asia. Estimates suggest costs could reach $1 billion. By using transition credits, companies hope to bridge the financial gap generated by the early dismissal.

Nagano village builds microgrid, aims for stable electricity supply and reduced outage

(Nikkei, May 1)

- Ikusaka Village (Nagano Pref) is building a microgrid powered by solar and small-scale hydroelectricity to supply energy to vineyards and public facilities.

- The project includes a hydro plant using dam outflow (100 kW+), and is funded partly by MoE subsidies. It’s expected to be operational by FY2028.

- CONTEXT: Ikusaka faces frequent power outages due to its mountainous location and dependency on electricity from nearby towns. The new grid aims to eliminate these risks while supporting the core grape industry.

TAKEAWAY: Combining local renewables, agricultural support, and disaster preparedness, the project is a model of sustainable development for small communities.

Sumitomo extends UAE gas power plant contract

(Company statement, May 2)

- Sumitomo Corp, TAQA and ENGIE signed a 15-year extension of its PPA with the Emirates Water and Electricity Company. This is for the Shuweihat S1 power plant in the UAE. Launched in 2005, the contract was set to end in June 2025.

- The plant will shift from a combined power and water desalination facility (1.5 GW power, 100 MIGD water) to a gas-fired open-cycle power plant. It will have a reduced capacity of 1.13 GW.

- The new configuration allows the plant to operate only when needed.

NEWS: HYDROGEN

Marubeni signs offtake from and signals investment in Exxon’s Texas ammonia plant

(Company statement, May 7)

- Marubeni and ExxonMobil have signed a long-term agreement for the annual supply of 250,000 tonnes of blue ammonia from ExxonMobil’s planned Baytown, Texas facility. The plant aims to remove 98% of the CO2 emissions from the manufacturing process and produce up to 1 million tons of ammonia per year.

- The ammonia will primarily be supplied mainly to Kobe Power Plant (owned by Kobe Steel), where it will be used for co-firing by 2030.

- Marubeni will also take an equity stake in ExxonMobil’s project, laying the groundwork for a global low-carbon ammonia supply chain.

- The final investment decision is expected in 2025, contingent on regulatory approvals and supportive policy.

- CONTEXT: The Bayston facility is expected to be the world’s largest of its kind, capable of daily production of up to 1 billion cubic feet of low-carbon hydrogen.

TAKEAWAY: This is one of the first major ammonia offtake agreements signed by a Japanese firm, following several deals clinched by JERA. It is also the first major deal struck by a non-power sector player. The key point here is that the FID is reliant on government support. This likely refers not only to Japan’s CfD auction but also U.S. IRA credits.

China overtakes Japan in hydrogen patent competitiveness

(Nikkei, May 2)

- For the first time, China has surpassed Japan in global competitiveness in hydrogen-related patents, especially dominating in four of five key areas: production, storage, transportation/ supply, and safety management.

- Utilization is the only area where Japan maintains a lead. The rankings are based on a competitiveness score from 180,000 patents filed globally between 2013 and 2022, analyzed by Tokyo-based data firm Astamuse.

- China’s lead is particularly pronounced in hydrogen production, where its companies benefit from lower costs and large-scale systems. As of 2023, Chinese-made green hydrogen production equipment costs are just one-quarter of those made in Europe. China now has 60% of global electrolyzer capacity, with increasing overseas orders.

- CONTEXT: Following President Xi Jinping’s 2020 carbon peak pledge, China’s annual hydrogen patent filings doubled those of Japan. By 2024, the number of Chinese firms entering electrolyzer production had surged to 100–200, compared to only a few players in Japan (e.g., Asahi Kasei, Toshiba).

Idemitsu lowers profit targets for decarbonization amid delays in H2 projects

(Nikkei, April 29)

- Idemitsu Kosan might revise downward its 2030 profit target for its decarbonization business, citing delays in commercializing next-gen fuels like hydrogen and ammonia.

- Originally aiming for non-fossil fuel businesses to make up over 50% of profits, the company now views a 20–30% share as more realistic.

- President Sakai said the company will focus on balancing stable fossil fuel supply with energy transition goals, with a new mid-term plan due later in FY2025.

- CONTEXT: Despite the shift, Idemitsu continues to prioritize SAF and solid-state EV batteries, while also exploring overseas production options. Fossil fuels still account for around 90% of its profits as of FY2023 (end of March 2024).

TAKEAWAY: Soaring material costs and weak demand, especially in hydrogen, have prompted a rethink similar to that seen among global peers like BP and Shell.

TOCOM holds 1st Tokyo green hydrogen trial trading

(Organization statement, April 30)

- In May, the Tokyo Commodity Exchange (TOCOM) will hold the first Tokyo Green Hydrogen Trial Trading for FY2025.

- This is part of the Tokyo Green Hydrogen Trial Trading Project, implemented by the Tokyo Metro Govt (TMG).

- The bidding method for FY2025 was changed in terms of implementation categories for suppliers and the content of pre-bid notifications to bidders.

- CONTEXT: TMG seeks to expand hydrogen energy demand and accelerate adoption. In FY2024, Tokyo Govt launched the “Tokyo Green Hydrogen Trial Trading” to test a market-based hydrogen trading system using a double auction mechanism, where the selling and buying prices of hydrogen are determined by bidding.

JOGMEC to launch domestic survey for natural hydrogen

(Nikkei, April 29)

- JOGMEC will begin surveying sites in Japan to identify subsurface zones where naturally occurring hydrogen can be economically extracted.

- The study focuses on rock formations like serpentine and peridotite, known to generate hydrogen through chemical reactions with water.

- CONTEXT: Hydrogen emits no CO2 when combusted. The expected production cost of natural hydrogen is as low as $1/ kg, making it much cheaper than green hydrogen.

Tokyo Gas to implement e-methane production test solicited by Tokyo Govt

(Company statement, May 7)

- Tokyo Gas inked a deal for the Tokyo Govt’s “Green Methane Production Project Using Green Hydrogen and CO2 from Sewage”.

- The project will run from April 2025 to March 2027. It involves the production of e-methane using green hydrogen produced in Keihinjima and CO2 derived from mixed gas containing sewage sludge as feedstock.

- This is the first project to produce e-methane by continuously feeding raw materials through pipes without separating CH4 and CO2 from gases generated from sewage.

- CONTEXT: Tokyo Gas Group has held demo tests for e-methane production since March 2022. The goal is to examine the practical application of local production and consumption of e-methane, as well as identify problems, and promote its use.

J-ENG launches full-scale ammonia-fueled engine operation

(Company statement, May 1)

- J-ENG began ammonia co-firing on its first full-scale, low-speed 2-stroke engine.

- Since May 2023, J-ENG has been conducting breakthrough ammonia co-firing tests on a test engine of this class. Over 18 months, the company gathered critical data on stable high-ratio ammonia co-firing and safe ammonia handling.

- The engine will undergo verification and is set for shipment in October.

JRI signs MoU to build hydrogen & ammonia supply chain

(Company statement, April 30)

- JRI inked an MoU with the Chubu Hydrogen and Ammonia Council to develop hydrogen and ammonia supply chains in the region.

- A founding member of the Council, JRI will help design cross-sector model cases for hydrogen utilization.

NEWS: SOLAR AND BATTERIES

BESS secures multiple winning bids in LTDA auction

(Government statement, April 28)

- OCCTO announced results of the second round of its Long-Term Decarbonized Power Sources Auction (LTDA), with a total of 38 projects – 34 in the decarbonized sources category and four LNG projects.

- BESS projects were the biggest winners, with a total of 27 of the 34 decarbonized power sources bids. Of those, six use batteries operating for at least six hours; the other 21 operate for 3-6 hours.

- The largest number of winning bids went to domestic firm Shirokuma Power, with 11 projects and an awarded capacity of 376.6 MW.

- Among the winners were also: three nuclear projects, two pumped-storage projects; one conversion to ammonia-co-firing and one adjustable hydro.

- CONTEXT: All winners are listed in the table in the Analysis section.

- The awarded capacity by type of power generation are as follows:

- Pumped hydro and energy storage (3-6 h) – 961 MW,

- pumped hydro and energy storage (6+ h) – 769 MW,

- ammonia co-firing upgrades — 95 MW,

- nuclear (safety upgrades for existing plants) — 3.15 GW,

- adjustable hydro — 52 MW.

- LNG-fired capacity secured 1.31 GW. Last year, ten LNG projects won their bids.

- CONTEXT: Just ahead of the results, ANRE unveiled a proposal for changes to the LTDA scheme that would apply from Round 3 (FY2025). The gist of the proposal was in the Japan NRG April 28 issue.

TAKEAWAY: Please see this issue’s Analysis section for more details.

ANRE plans to boost demand for next-gen solar cells.

(Government statement, May 7)

- ANRE presented a plan to boost demand for next-gen perovskite solar cells. The goal is to install them on public infrastructure such as roads, airports, and ports, and to encourage large urban areas like Tokyo to set high installation targets.

- The plan focuses on installation of light, film-type PSCs on rooftops; municipalities are encouraged to develop installation plans. A guideline will be this year.

- The govt also plans to support development of tandem-type solar cells, which have higher efficiency than traditional silicon cells.

- CONTEXT: From May to Nov 2024, a public-private council met to promote expansion of PSCs and boost industrial competitiveness. Deployment and price targets for 2040 were discussed, and a “Next-Generation Solar Cell Strategy” was released, setting a deployment target of about 20 GW by 2040.

Kansai Electric to build BESS on site of former thermal power plant

(Company statement, May 7)

- Tanagawa Energy Storage Facility, jointly established by Kansai Electric, Kinden Corp, and Japan Extensive Infrastructure (JEXI) will develop one of Japan’s largest BESS on the site of the former thermal power plant in Misaki-cho, Osaka Pref.

- Construction begins in June, with commercial operation set for February 2028.

- The facility will cover about 20,000 m3 and will use lithium-ion batteries with a rated output of 99 MW and a rated capacity of 396 MWh.

- Kansai Electric will oversee the project, Kinden will procure the storage batteries and build the storage facilities. E-Flow, a subsidiary of Kansai Electric, will operate BESS in the electricity market.

- CONTEXT: JEXI was set up in 2023 to create a virtuous cycle of funds, assets, and capital in the infrastructure sector.

Nickel-based batteries regain attention for safety and sustainability

(Company statement, Nikkei, April 28)

- FDK, a Japanese battery manufacturer, is reviving interest in nickel-based rechargeable batteries – an older tech – as demand grows for safer and lighter power sources in data centers and elevators.

- The company will begin mass production of nickel-zinc batteries in FY2026, aiming to replace lead-acid batteries that are heavy and toxic.

- The new batteries are half the weight and easier to recycle, with a lower risk of fire compared to Li-ion batteries.

- CONTEXT: Nickel-based batteries were first made in Japan over 60 years ago but lost prominence to Li-ion tech in the 1990s. They’re now being re-evaluated for their durability and safety in harsh environments. As Chinese and Korean firms dominate Li-ion battery markets, Japan sees renewed hope in alternative tech like solid-state batteries and safer nickel-based solutions.

- CONTEXT: FDK, originally part of Toshiba and now under Taiwan’s PSA Group, is also developing improved NiMH batteries, including a model that operates at –40°C.

NEWS: WIND POWER AND OTHER RENEWABLES

Kyuden Group to expand renewables 15-fold

(Nikkei, April 24)

- Kyuden Mirai Energy, a subsidiary of Kyushu Electric, will significantly expand its renewables sales, seeking to boost non-FIT renewable capacity to 4 GW by 2030 – 15 times the FY2025 level.

- This will be achieved by trading in electricity markets, handling third-party power sales, and investing in storage.

- Starting FY2025, KME will use market-based sales for its geothermal and wind power, including 270 MW of non-FIT assets and battery storage coming online. Starting FY2026, it will begin selling renewables generated by other firms.

- With the addition of hydro from Kyushu Electric, KME will have about 1.6 GW of renewable capacity and become one of Japan’s top green power providers.

- KME plans to manage around 150 power sources by 2030, including third-party assets. Leveraging its operational expertise and AI-based trading systems, the firm seeks to optimize profits, accelerate renewable deployment, and become the only domestic provider with a balanced portfolio of all five major renewable sources: solar, wind, biomass, hydro, and geothermal.

- CONTEXT: KME began handling geothermal power from Kyushu Electric in April 2024. This marks the company’s entry into market-based electricity sales, alongside auction and bilateral contracts.

Eurus inks deal on Japan’s first market-linked project finance for wind farm under FIP

(Company statement, April 30)

- Eurus Energy signed a project finance agreement for its wind farm in Date City (Hokkaido) with grid capacity at 10 MW, based on the FIP. This is the first project finance deal in Japan for a wind power project using the FIP.

- The Eurus Date Wind Farm has been operational since November 2011. From May 1, the wholesale electricity price for Eurus Green Energy – a power retail firm within the Eurus group – has been linked to the electricity market.

- CONTEXT: Unlike the FIT, this project relies on electricity market revenues. FIP premiums are more complex and risky due to higher cash flow volatility.

TEPCO EP sells wind farm naming rights and green electricity

(Company statement, April 25)

- TEPCO Energy Partner began supplying electricity bundled with environmental value from local wind generation to 19 Shizuoka Bank branches starting April 1.

- The renewable attributes come from TEPCO Renewable Power’s 18.4 MW Higashi-Izu Wind Farm (renamed “Shizugin Wind Park Higashi-Izu” after Shizuoka Bank acquired the naming rights).

- The power is effectively 100% renewable through FIT non-fossil fuel certificates linked to the wind farm.

- A portion of Shizuoka Bank’s rights payment will fund local projects; this is the first time a domestic company acquired naming rights for a wind farm over 10 MW.

TAKEAWAY: Sale of naming rights for wind farms – or other renewable energy facilities for that matter – is very rare in Japan. In late 2023, Kansai Electric sold the naming rights for a hydro power plant near Uji City, Kyoto Pref, to Sumitomo Mitsui Banking Corp, which was described as the power utility’s first such deal. The funds were also due to go into local community projects. The value of the naming rights is unclear, but it shows there’s a market for ‘green branding’ in Japan, and with clients largely in the financial and insurance sector.

Vestas partners with Mitsubishi Electric and Fuji Electric on wind turbine components

(Company statement, April 25)

- Vestas agreed with Mitsubishi Electric and Fuji Electric to develop wind turbine components.

- The Japanese firms will make equipment for generators and power chips, aiming to supply them for Vestas turbines deployed in Japan and abroad.

- Mitsubishi Electric will develop a new switchgear system for offshore wind turbines, to be installed in projects planned by major Japanese utilities JERA and J-Power.

- Fuji Electric will develop power semiconductors for both onshore and offshore wind.

- CONTEXT: Since entering Japan in 1993, Vestas has supplied over 1.5 GW of wind turbine capacity, including for the first large-scale commercial offshore wind farm at Akita Port and Noshiro Port.

Looop forms alliance with Tokyu Land to expand renewables

(Company statement, April 25)

- Electricity retailer Looop signed a capital and business partnership with Tokyu Land, which already participated in a third-party allotment of Looop shares in 2021. This is an additional investment.

- The goal is to boost power sales capabilities by combining Tokyu Land’s experience in renewables development and corporate electricity supply with Looop’s expertise in the residential market, where it holds some 340,000 contracts.

- The agreement was formalized on March 31. Details such as the investment amount and ownership stake have not been disclosed, but Tokyu Land will not become Looop’s largest shareholder.

- CONTEXT: Tokyu Land entered the renewables business in 2014 and, as of March 2025, owns nearly 2 GW of renewable energy capacity. The firm runs a renewable energy business under the ReENE brand, which is a fully-owned subsidiary focused on power sales to corporate clients.

Toyoda Gosei invests in agrivoltaics startup Agritree

(Company statement, April 25)

- Toyota Corp’s subsidiary Toyoda Gosei has invested in Agritree, a Fukuoka-based startup promoting agrivoltaics.

- Toyoda Gosei will explore purchasing renewable electricity and environmental value generated on farmland.

- Agritree also plans to set up a local subsidiary in Vietnam to explore use of agrivoltaics in mitigating climate change impact.

- CONTEXT: Agritree, founded in 2018, offers consulting, design, installation, and management of solar sharing systems, combining renewables generation with farming. In Vietnam, it will collaborate with several universities to conduct field trials and develop guidelines and JCM methodologies.

TEPCO Group acquires firm in power and railway sectors

(Company statement, May 8)

- TEPCO’s investment subsidiary acquired CSD, a systems development company in Kawasaki City.

- CSD develops infrastructure systems used in electricity, railways, and media. TEPCO aims to strengthen its capabilities in power system development across the group.

- CSD is expanding into renewables, including solar power monitoring and storage.

NEWS: NUCLEAR

MHI discusses aging NPP replacement with component producers

(Nikkei, May 6)

- MHI is in discussions with over 200 component manufacturers to replace aging NPPs. The company is developing the Innovative Light Water Reactor (ILWR), aiming for practical use in the 2030s. About 150 out of 200 key components are currently procurable, including advanced safety valves.

- MHI is working to maintain a robust domestic supply network amidst some firms exiting the nuclear business. The latter include KHI in 2021, and the closure of Japan Casting & Forging Corp.

- In its 7th Basic Energy Plan, the govt changed policy to allow reactor replacements on existing nuclear plant sites. About 400 firms are involved in the domestic nuclear supply chain.

- CONTEXT: Japan has not built new reactors since the 2011 Fukushima disaster. As a consequence, the supply chain for components is at risk of weakening.

Hitachi GE Nuclear Energy to supply equipment for Canada’s first SMR project

(Company statement, May 9)

- Hitachi GE Nuclear Energy will supply key reactor components for Unit 1 of Canada’s first SMR project. With GE Vernova Hitachi Nuclear Energy, they will take part in Ontario Power Generation’s Darlington New Nuclear Project.

- This project is North America’s first SMR deployment. It will use the BWRX-300, a small light water reactor developed by Hitachi GE and GE Vernova Hitachi.

NRA confirms Tomari NPP Unit 3 meets safety standards

(Tokyo Shimbun, April 30)

- The NRA approved a draft safety review confirming that Tomari NPP Unit 3 meets safety standards. This is the 18th reactor at the 11th plant to pass NRA safety review.

- Hokkaido Electric aims to complete safety upgrades, including a seawall, by March 2027. Before final approval, there will be a public comment period and consultation with METI. Final approval will be in summer 2025. It is still necessary to get local consent and regulatory approvals of equipment design and operational rules.

- CONTEXT: Tomari NPP Unit 3 began operation in December 2009. It is Japan’s newest nuclear reactor. The approval was delayed by debates over whether a fault beneath the site was active. Reviews of Units 1 and 2 are still ongoing.

TAKEAWAY: The restart of Tomari NPP Unit 3 is at the center of Hokkaido’s energy discussions. Many expect Rapidus’s semiconductor plant and SoftBank’s data center to drive up Hokkaido’s electricity demand by 50% in a decade. Renewables and batteries will play a role, but many fear that without Tomari NPP Unit 3 there will be supply shortfalls.

NEWS: TRADITIONAL FUELS

QatarEnergy negotiates long-term LNG deal with JERA and Mitsui

(Reuters, May 2)

- QatarEnergy is negotiating a long-term LNG supply deal with Japanese firms, including JERA and Mitsui. At stake is 3 Mt a year from its North Field expansion.

- This would reinforce Qatar’s presence in Japan amid rising competition from the U.S., UAE, and Oman, which offer more flexible contracts. While JERA and Mitsui confirmed ongoing talks, they did not disclose details.

- By 2030, Qatar plans to boost LNG output from 77 to 142 Mtpa.

- CONTEXT: Japan has reduced its LNG imports from Qatar after restarting nuclear reactors over the past few years. Volumes fell from over 15 Mtpa a decade ago to under 3 Mtpa in 2024.

- SIDE DEVELOPMENT:

JERA mulls joining Alaska LNG Project - (Bloomberg, April 28)

- JERA is considering joining the proposed Alaska LNG Project.

- Executive officer Maekawa Naohiro said this is important for energy security.

- CONTEXT: Trump has been pushing to revive the $44 billion Alaska LNG project, and raised the topic during a U.S.-Japan summit in February. Today, only 10% of JERA’s LNG is sourced from the U.S., while over half is from Asia and Oceania.

MODEC to produce FPSO vessel domestically, first in 8 years

(Nikkei, April 9)

- Mitsui Ocean Development & Engineering (MODEC) will partially produce a Floating Production, Storage, and Offloading (FPSO) vessel at Sumitomo Heavy Industries’ Yokosuka Shipyard in Kanagawa Pref.

- This is the first FPSO domestic production in about eight years. They’re built in China or Singapore.

- MODEC will build only the front section in Japan; the rear will be made in China.

- The order is for a Shell subsidiary offshore oil development project in Brazil.

- CONTEXT: An FPSO is a vessel-shaped facility used to produce oil from subsea fields, store it in onboard tanks, and transfer it to tankers.

ANRE finalizes guidelines for responding to city gas supply shortages

(Government statement, April 28)

- ANRE finalized guidelines for responding to city gas supply shortages. Initially, gas and power companies will cooperate to share resources.

- If a crisis worsens, pipeline operators will assess supply and demand based on information from LNG suppliers and issue warnings as needed. Retailers will ask consumers to conserve gas and may negotiate reductions with large users.

LNG stocks down from previous week, down YoY

(Government data, April 30)

- As of April 27, the LNG stocks of 10 power utilities were 2.05 Mt; down 3.3% from the previous week (2.12 Mt); down 6% from end April 2024 (2.18 Mt); and down 4.2% from the 5-year average of 2.14 Mt.

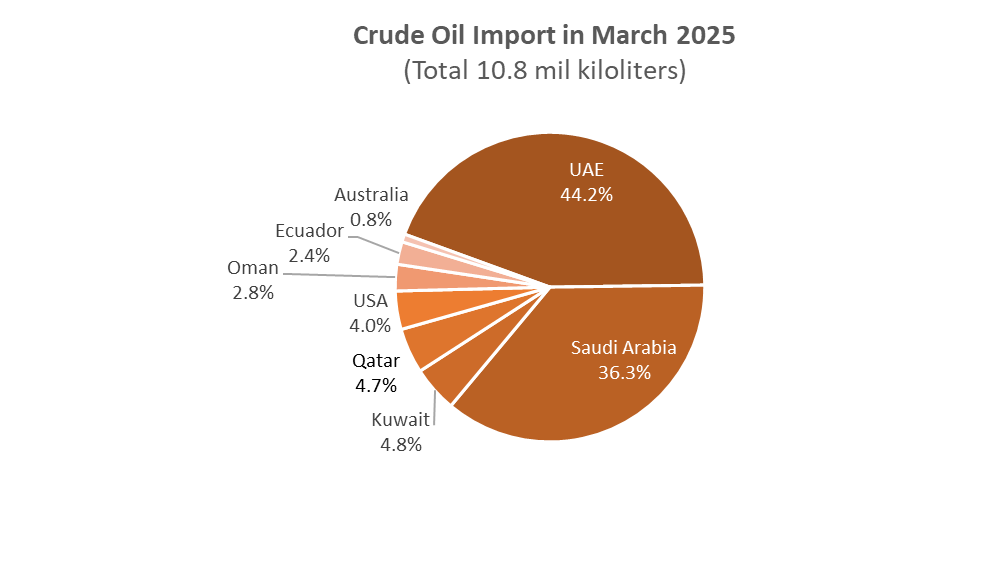

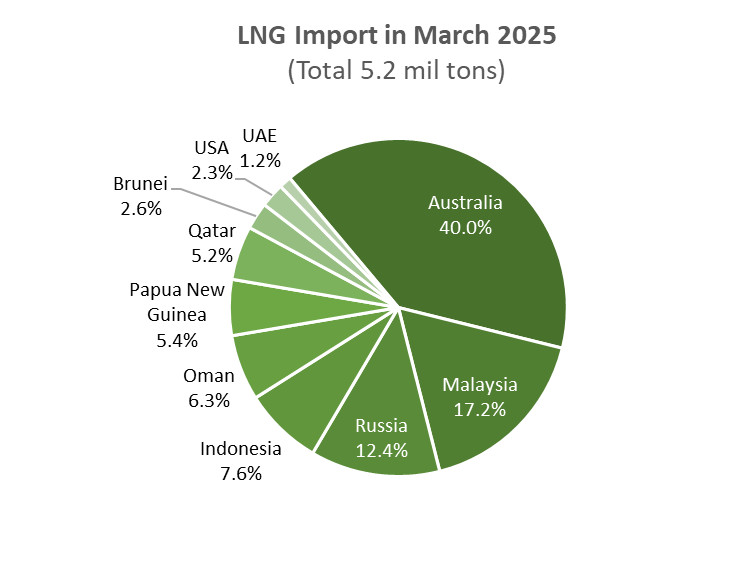

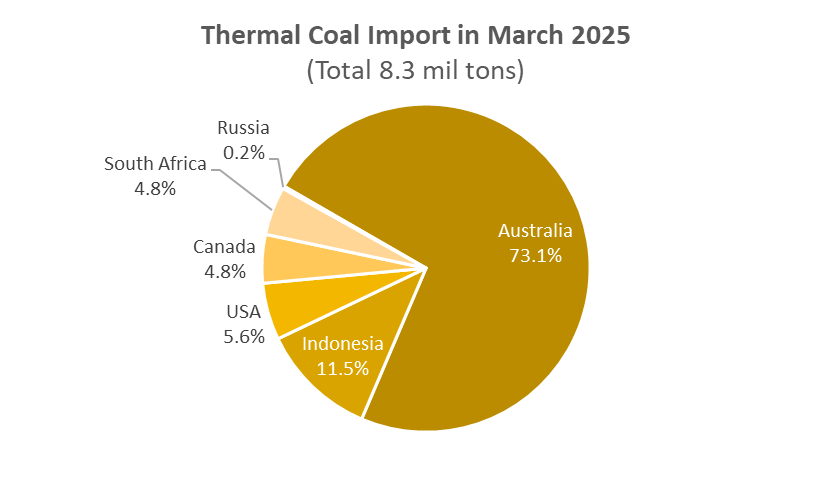

March Oil/ Gas/ Coal trade statistics

(Government data, April 25)

- In March, Japan imported 10.8 million kiloliters of crude oil, 6.7% over February (10.1 million kl) but down 13.6% YoY (11.6 million kl). About 93% of total crude imports came from the Middle East, with the UAE the top supplier. One major change is that imports from the U.S. jumped 8.6-fold over the previous month – from 0.05 to 0.43 million kiloliters.

- March LNG imports totaled 5.2 Mt, down 12.3% over February (5.9 Mt), and down 7.2% YoY (5.5 Mt).

- March thermal coal imports decreased to 8.3 Mt, down 5.9% over February, but up 8.8% YoY. No significant change in the exporting country list, and volumes were more or less on a monthly average. Electricity demand usually drops in April and May due to the mild climate, as heating or cooling devices are not used. Import volumes will most likely show a downward trend in coming months.

NEWS: CARBON CAPTURE & SYNTHETIC FUELS

Japan and Malaysia to cooperate on overseas CO2 underground storage

(Nikkei, April 28)

- Japan and Malaysia will cooperate on an overseas CO2 underground storage project, Japan’s first such initiative abroad. It will launch around 2030.

- CO2 captured from Japan’s thermal power plants will be liquified and transported by ship for injection in depleted offshore gas fields in Malaysia.

- Mitsui & Co, KEPCO, and Malaysia’s Petronas are leading the project. Three sites are in progress, with a total storage capacity of up to 10 Mt of CO2 annually.

- Japan is also exploring partnerships with Australia. Interested companies include INPEX and Chubu Electric. The govt estimates ¥4 trillion investment over the next ten years for CCS development, to be raised via green transition bonds, etc.

- CONTEXT: Japan aims to store 120–240 Mt of CO2 annually by 2050, roughly 10–20% of its FY2023 emissions. Japan also began developing domestic storage sites, including one at Tomakomai in Hokkaido, set to start commercial operations this year. Still, most domestic sites are in early R&D stages.

- SIDE DEVELOPMENT:

- Japanese and Thai firms join forces for decarbonization

- (Nikkei, April 29)

- Japanese firms including Isuzu, Toray, and Kao inked an MoU with Thai firms such as PTT, CP Group, and local universities to promote decarbonization in Thailand.

- The initiative aligns with the Japan–Thailand Energy and Industry Dialogue held the same day. The partnership aims to help decarbonize Thailand’s lagging supply chains and train next-gen talent, especially in the automotive sector.

- Projects include:

- Isuzu and a Mitsubishi Corp subsidiary piloting battery-swapping EVs with local logistics partners.

- Toray and PTT developing bio-based nylon for automotive use.

- CONTEXT: Thailand targets carbon neutrality by 2050. However, CO2 emissions remain high due to reliance on fossil fuels and lack of mandatory reduction policies. With over 6,000 Japanese firms in Thailand, especially in the automotive sector, Tokyo’s cooperation is vital to Thailand’s decarbonization efforts and as a way to strengthen Japan’s influence amid rising Chinese presence.

Japan’s first SAF begins supply for commercial flights

(Company statement, May 7)

- Saffaire Sky Energy, a JV of JGC Holdings and Cosmo Oil, began supplying sustainable aviation fuel (SAF) made from waste cooking oil.

- CONTEXT: This is the start of regular supply of domestically produced SAF. Previous batches were made as one-off batches for pilot projects.

- The first delivery was provided to a Japan Airlines (JAL) commercial flight departing Kansai International for Shanghai.

- Annual production at Cosmo Oil’s Sakai refinery will reach 30,000 kiloliters starting FY2026, supplying five domestic airports, including Kansai, Narita, and Haneda, for airlines like JAL, ANA, Delta Air Lines, and DHL Express.

TAKEAWAY: The cost of using SAF will be higher than regular fuel. Suppliers like JGC say they expect business travelers to choose ‘SAF-powered’ flights, but this is far from certain especially if the global macro environment sours. It’s possible the govt will provide a certain level of subsidies to help SAF break into the market.

NYK inks deal with Climeworks for CDR purchase

(Company statement, May 7)

- NYK signed a three-year deal with Swiss company Climeworks to buy a portfolio of carbon dioxide removal (CDR) credits starting in FY2026. This makes NYK the first Japanese company to obtain Climeworks’ CDR credits in a portfolio format.

- The credits derive from methods like biochar, BECCS, and enhanced rock weathering. They’ll offset NYK’s residual emissions, including Scope 1.

KEPCO subsidiary took in ¥2.3 billion in overcharges

(Nikkei, May 2)

- KANSO Technos, a KEPCO subsidiary, took in ¥2.3 billion over seven years in overcharges on govt-commissioned projects. It includes CCS-related work.

- The overcharges included fake labor costs for employees not involved in the projects. The misconduct relates to a CCS project commissioned by the MoE in FY2023. The findings came from an internal investigation led by external lawyers.

BY MAGDALENA OSUMI

Booming BESS, Nuclear Retrofits Win Big in Round 2 of Japan’s LTDA Auction

The second Long-Term Decarbonized Power Sources Auction (LTDA) confirmed the explosive growth of Japan’s battery energy storage (BESS) market, as such projects dominated both successful and unsuccessful bids.

The results underscore the technology’s growing role in enhancing grid flexibility and supporting the integration of variable renewables like wind and solar. Additionally, among the winners announced at the end of April were two pumped-storage hydro plants, one ammonia co-firing retrofit, and one adjustable hydro project.

In the FY2024 round, total bids reached 13.61 GW, with 6.34 GW — roughly 47% — awarded. Of this, 5.03 GW (worth ¥346.4 billion per year) went to projects ranging from BESS and thermal plant retrofits to other decarbonized solutions.

An additional 1.31 GW was secured by four dedicated LNG-fired plants under a separate category, reflecting the importance that energy planners put on LNG’s role as a lower-carbon, dispatchable power source.

The auction also reflects government willingness to help cover safety upgrades of nuclear plants, as four utilities secured awards for 3.15 GW. This is seen as progress in the effort to restart long-idled reactors such as Tomari NPP Unit 3 and Kashiwazaki-Kariwa NPP Unit 6.

CCS-equipped plants, synthetic methane, and ammonia co-firing projects – while technically eligible – were excluded from this LTDA round due to pricing and technical readiness.

Japan NRG examines the LTDA results in detail.

Big win for BESS

This year’s LTDA auction saw strong participation from both Japanese and international players, especially in energy storage. As Japan boosts its renewable energy capacity, battery storage is moving from a supporting role to center stage. With solar and wind power growing rapidly – and regularly getting curtailed in the hours when supply exceeds demand – adding more flexibility and balance to the grid has become a national priority.

The latest LTDA auction results reflect this urgency. BESS projects dominated the number of submissions. There were 27 BESS project winners and a total awarded capacity of 1.73 GW.

In terms of project numbers, for the second year running the biggest winner was Shirokuma Power. Last year, it helped Hexa Renewables score the most awards as an EPC partner. This year, Shirokuma Power, founded in 2016 to develop and operate solar plants, managed to secure 11 projects (total capacity of 377 MW) through its various special purpose vehicles (SPCs) such as SRE and Aoba. The company is believed to have submitted over 30 bids.

A joint venture between U.S.-based Stonepeak and Singapore’s CHC and Taiwan’s HD Renewable Energy were awarded five BESS projects each. Stonepeak and CHC’s venture captured a total of 284.23 MW. The duo won 131 MW in the previous FY2023 auction. This year, the venture also partnered with Shizen Energy on one grid-scale project operating for six hours or more.

HD Renewable Energy secured around 300 MW (1.5 GWh) of BESS projects across Aomori, Fukushima, and Hokkaido, with the largest of these nearing 100 MW. The Taiwanese firm also secured 73 MW of capacity for two projects in Mie and Fukuoka Prefectures last year.

Bison Energy, active in Japan’s solar market since 2016, won three projects totaling 197.75 MW, including a 129.79 MW long-duration facility in Fukushima.

Auction winners included big international utility names. France’s EDF Group secured 119.26 MW, the second largest capacity for a single BESS project.

UK-based Eku Energy was awarded 119.26 MW for its 150 MW/ 600 MWh Eshi project in Okayama, one of Japan’s largest planned BESS facilities, expected online by 2030. The contract is recorded as 119.27 MW after applying an efficiency adjustment. The second win follows its first project, the 30 MW Hirohara BESS in Kyushu.

The strong showing by BESS operators is not surprising given the surge of enthusiasm most showed in the LTDA last year. The big gap between the size of bids and awarded capacities is what prompted the government to expand the energy storage allocation of the LTDA to 1.5 GW for Round 2.

Overall, only a fifth of the submitted BESS bid capacity (6.95 GW) ended up as winners. These were further split into 3–6 hour and over 6-hour systems as Round 2 encouraged longer duration storage. Each of these sub-categories had price caps, but uptake in the 6+ hour category was low due to its perceived higher risk and longer development time.

Just six of the winning BESS projects from Round 2 will operate for over 6 hours. One more long-duration project – pumped hydro – was also selected.

Safety updates for nuclear power as new addition

Last year’s LTDA auction surprised by allocating a sizable 1.3 GW of capacity allocation to Chugoku Electric to build a third reactor at Shimane NPP. This year, the nuclear credits went to three existing facilities that need funding to complete safety upgrades:

- Tokai No. 2 (1.056 GW)

- Tomari No. 3 (902.1 MW)

- Kashiwazaki-Kariwa Unit 6 (1.195 GW)

All three have approval to restart from the Nuclear Regulation Authority, yet Tomari’s green-light arrived just a couple of days after the auction results were published, leading some to question the role that the government wants LTDA to play in the nuclear sector.

Still, the main challenge for the nuclear winners will be meeting their LTDA requirements. After all, approval from the NRA is not enough to guarantee that a reactor can restart. There is also the need for local consent, which remains uncertain amid persistent public opposition to nuclear energy and complex facility upgrade processes.

Tokai No. 2, for example, faces restart delays due to seawall construction and a 2021 court ruling citing inadequate disaster preparedness. The plant must also coordinate evacuation plans for 940,000 residents across 14 municipalities.

Kashiwazaki-Kariwa Unit 6 faces financial and trust challenges. Fuel loading is scheduled for June 2025, but full restart may slip to FY2026 or later if public support and compliance with new counterterrorism requirements aren’t secured.

LNG as a transitioning fuel

While the LTDA system primarily targets decarbonized power sources, it also includes a limited provision for LNG-fired power. Dedicated LNG plants are permitted to bid through the third round (FY2025), provided they commit to full decarbonization by 2050.

Under this scheme, LNG is seen as a transitional solution to help stabilize the grid and prevent short-term supply-demand imbalances. As the government obviously doesn’t deem LNG as a ‘decarbonized’ source, only dedicated LNG-fired projects – offering relatively low CO2 emissions and grid flexibility – are eligible to bid in the LTDA. These projects must also begin decarbonization efforts within 10 years of starting operations.

In the FY2024 round, LNG-fired capacity secured 1.31 GW at ¥45.6 billion per year. Four projects were awarded this year, with the category’s total allocation capped at 2.24 GW.

One notable winner in this year’s auction is Hokkaido Electric, which secured a contract for its 569.4 MW Ishikariwan Shinko Power Station Unit 3 in Otaru City. As the final unit in a 1.7 GW, three-unit LNG complex, Unit 3’s commissioning was accelerated from FY2037 to FY2033. The Ishikariwan plant – Hokkaido Electric’s first LNG facility – is central to the utility’s move away from coal. Unit 2, awarded in the FY2023 LTDA round, is scheduled to come online in FY2030.

How LNG will fare as a fuel as Japan continues to decarbonize is unclear, and this likely explains the weak interest in the LNG category this year. There were only four bids and all were successful; but, even so,this left 2.69 GW unallocated. This year’s LNG category was capped at 2.24 GW.

Future bids and challenges ahead

Ahead of announcing R2 auction results, the government disclosed proposals for changes to the LTDA framework, set to apply from FY2025. The updates aim to address rising construction costs and encourage investment in new power sources.

The introduction of differentiated Weighted Average Cost of Capital (WACC) by technology type is also planned, reflecting varying risk profiles. These changes aim to better support long-term decarbonization projects and encourage the sector’s stable growth.

Key updates planned for the subsequent LTDA tenders are:

- Adjusted business return rates: The standard business return rate of 5% will be modified based on the construction period.

- Increased bid price cap: The maximum bid price was doubled from ¥100,000/ kW to ¥200,000/ kW to reflect increased construction costs.

- Higher price cap for emerging technologies: The maximum price for hydrogen, ammonia, and thermal power with CCS will be raised.

- The proposal comes with new categories such as CCS and long-duration energy storage (LDES) on the table.

| Company name | Project | Category | Capacity (kW) | |

1 | Japan Atomic Power Company | Tokai No. 2 | Nuclear Power (safety measure investments for existing nuclear facilities) | 1,056,000 |

2 | Hokkaido Electric | Tomari No. 3 | Nuclear Power (safety measure investments for existing nuclear facilities) | 902,107 |

3 | KEPCO | Okuyoshino Power Station No. 1 | Pumped-storage (operation duration of 6+ hours) | 180,323 |

4 | KEPCO | Okuyoshino Power Station No. 2 | Pumped-storage (operation duration of 6+ hours) | 180,323 |

5 | Shikoku Electric | Saijo Power Station No. 1 | Conversion to ammonia co-firing | 94,600 |

6 | Kyushu Electric | Morotsuka Power Station | General hydropower (adjustable type) | 51,800 |

7 | Shizen Energy and Stonepeak/CHC | Shizen-601 Grid-scale BESS project | BESS (Operating duration: 6 hours or more) | 47,226 |

8 | TEPCO | Kashiwazaki-Kariwa Reactor N0. 6 | Nuclear Power (safety measure investments for existing nuclear facilities) | 1,195,000 |

9 | Bison Energy | Battery No.22 ESS (Fukushima Pref) | BESS (Operating duration: 6 hours or more) | 129,797 |

10 | Bison Energy | Battery No.31 ESS (Niigata Pref) | BESS (Operating duration: 3 to less than 6 hours) | 37,827 |

11 | Bison Energy | Battery No.32 ESS (Fukui Pref) | BESS (Operating duration: 3 to less than 6 hours) | 30,129 |

12 | BS Holdings (100% subsidiary of Sumitomo) | BS Namie | BESS (Operating duration: 3 to less than 6 hours) | 49,905 |

13 | Japan Energy Storage (Eku Energy) | Eshi BEES1 | BESS (Operating duration: 3 to less than 6 hours) | 119,266 |

14 | EDF Japan | Suginomiya Grid-scale BESS | BESS (Operating duration: 3 to less than 6 hours) | 88,654 |

15 | Risu Energy Development Holdings – Stonepeak/CHC | Risu-101 ESS | BESS (Operating duration: 3 to less than 6 hours) | 78,922 |

16 | Risu Energy Development Holdings – Stonepeak/CHC | Risu-203 ESS | BESS (Operating duration: 3 to less than 6 hours) | 40,705 |

17 | Risu Energy Development Holdings – Stonepeak/CHC | Risu-301 ESS | BESS (Operating duration: 3 to less than 6 hours) | 77,545 |

18 | Risu Energy Development Holdings – Stonepeak/CHC | Risu-502 ESS | BESS (Operating duration: 3 to less than 6 hours) | 39,832 |

19 | Aoba Power (SPC) – Shirokuma Power | Aoba 1 BESS | BESS (Operating duration: 3 to less than 6 hours) | 29,195 |

20 | Aoba Power (SPC) – Shirokuma Power | Aoba 2 BESS | BESS (Operating duration: 3 to less than 6 hours) | 25,953 |

21 | Aoba Power (SPC) – Shirokuma Power | Aoba 5 BESS | BESS (Operating duration: 3 to less than 6 hours) | 25,953 |

22 | Aoba Power (SPC) – Shirokuma Power | Aoba 6 BESS | BESS (Operating duration: 3 to less than 6 hours) | 25,784 |

23 | Rechargeable Energy (SPC) – Shirokuma Power | Muroran BESS | BESS BESS (Operating duration: 6 hours or more) | 46,270 |

24 | Rechargeable Energy (SPC) – Shirokuma Power | Ishinomaki BESS | BESS (Operating duration: 3 to less than 6 hours) | 25,953 |

25 | SRE (SPC) – Shirokuma Power | SRE Hokkaido G | BESS BESS (Operating duration: 6 hours or more) | 46,270 |

26 | SRE (SPC) – Shirokuma Power | SRE Yamagata Pref B | BESS (Operating duration: 3 to less than 6 hours) | 29,195 |

27 | SRE (SPC) – Shirokuma Power | SRE Akita Pref B | BESS (Operating duration: 3 to less than 6 hours) | 38,930 |

28 | Shirokuma Power 02 (SPC) | Shirokuma 03 | BESS (Operating duration: 3 to less than 6 hours) | 36,554 |

29 | Shirokuma Power 02 (SPC) | Shirokuma 04 | BESS BESS (Operating duration: 6 hours or more) | 46,591 |

30 | Star 1 (SPC) – HDRE | Fukushima Tomioka 2 ESS | BESS (Operating duration: 3 to less than 6 hours) | 40,582 |

31 | Star 1 (SPC) – HDRE | Aomori Towada ESS | BESS (Operating duration: 3 to less than 6 hours) | 40,566 |

32 | Star 1 (SPC) – HDRE | Aomori Hashikami ESS | BESS (Operating duration: 3 to less than 6 hours) | 40,501 |

33 | Star 2 (SPC) – HDRE | Aomori Hachinohe ESS | BESS (Operating duration: 6 hours or more) | 92,548 |

34 | Star 4 (SPC) – HDRE | Hokkaido Kitami ESS | BESS (Operating duration: 3 to less than 6 hours) | 39,383 |

| Company name | Project | Category | Capacity (kW) | |

1 | Hokkaido Electric | Ishikariwan-Shinko Power Plant (Ishikari Bay New Port Power Station) Unit 3 | LNG | 551,217 |

2 | Shikoku Electric | Sakaide Power Station Unit 5 | LNG | 561,263 |

3 | Zero Watt Power | Zero Watt Power Ichihara Power Station | LNG | 100,550 |

4 | Toho Gas | (Provisional) Gas-fired Power Plant | LNG | 101,614 |

Conclusion

While the FY2024 LTDA auction results highlight the growing importance of battery energy storage systems (BESS) in integrating variable renewable sources into the grid, the auction also saw progress in nuclear energy with awards for safety upgrades to existing plants. Still, challenges remain in restarting these reactors due to local approval and safety concerns.

Meanwhile, LNG continues to draw some attention as a transitional fuel, but future changes in the auction framework suggest an interest from officials in incentivizing other low-carbon sources, such as ammonia, etc. Yet, with BESS an oversubscribed power source for two years in a row, it’s possible that the government will launch an entirely separate auction for it.

The allocation of power to a variety of sources, including LNG, also raises questions over the role of the LTDA as a tool to specifically support decarbonization. Still, with green capital increasingly uncertain where to deploy, Japan has the opportunity to burnish its credentials as a safe haven.

BY ANDREW STATTER

Energy Jobs in Japan: Making the most of a change in company ownership

Mergers and acquisitions in the energy sector are common. These range from a strategic merger such as BP and JERA’s offshore wind businesses, as well as targeted acquisitions to build capability as in the cases of Seajacks to Marubeni or Electroroute to Mitsubishi. Or, as increasingly seen in the market, it might be corporate acquisitions targeting the clean energy portfolio as illustrated by NTT’s majority acquisition of Green Power Investment.

In fact, many companies in the energy space begin with the end in mind. Development platforms sponsored by private equity funds typically have a limited investment time horizon in which they will maximise portfolio value with a view to exit at a certain time.

As an employee, how can you act and react to such changes? What opportunities exist in a change of ownership situation, and what threats should you be aware of and prepared to navigate?

Which side are you on?

A jumping off point for this inquiry would be whether you are with the acquiring or the acquired (or the majority or minority shareholder). Advantages on the acquiring / majority side are:

- Tendency for upper management positions to be filled by majority stakeholders providing fast-track, career step-up opportunities;

- Strategic direction, company culture, rules and benefits are usually shaped by the acquiring company;

- The inevitable impacts of change within the business will be lesser;

- Opportunity to become exposed to new technologies, projects, and business without changing your company.

Does this mean that if you are on the side of being acquired or taking a minority stake that you should be looking for the exit doors as soon as you catch wind of the news? Discretion must be exercised, but we should bear in mind potential benefits that can roll to the minority side as well.

- Management independence. An acquisition does not necessarily mean total assimilation into the proverbial ‘Borg’. Seek to understand whether the intent is to allow your company to remain independent, and self-manage.

- Potential career growth opportunities. It is not a given that the new management team will be made up exclusively from the acquiring side.

- Financial upside. Equity payouts, shares in the new company, structured earn-outs may be on the table. However, even without these you may have the opportunity to renegotiate favourable terms.

Knowledge is power

The more you know about the deal before it happens, the more informed you will be and better able to shape your strategy. Understanding the deal structure itself to identify ownership structure, management plan and potential payouts is key. Beyond this, take the time to learn about the company culture, working style, benefits and promotion pathways on offer at the new firm. At a more granular level, study and assess the strengths and weaknesses of the team you’ll be joining and assess your future value to strategically position yourself in the new environment.

This can be relatively easy to do as negotiations take months and may be transparent to an extent. However, in other cases the decision is made far above your pay grade and you could wake up Monday morning to an announcement of new ownership!

Rule #1, prepare to stay and thrive:

Often, not all the answers to the questions we’ve explored above will be clear until after the deal is done and well into the post-merger integration phase. Be prepared for the best. Blind optimism is not what I am advocating for here; rather, control and influence what you are able to.

Identify the key actors. As the management structure becomes clear, identify who are the leaders, how they see success in the business, and what challenges they are benchmarked against. Build a picture of not only the business’ general direction, but the pressures that those above you are under. With this, you can position yourself to align and be most useful. Side note on this: be mindful of actors who may have been displaced and become disgruntled. It’s usually better to avoid being pulled into political battles, and instead focus on results.

Create your strategic value. This can be a great opportunity for you to step up. By identifying where your particular knowledge, technical skill-sets, relationships and experience are strong, you can position yourself as a key asset. Assess and benchmark yourself against people from the other side who may be in a similar role. A post-merger risk is that duplication of roles is likely to emerge, especially in cases of similar businesses combining.

Proactively solve problems. Despite the best intentions of motivated buyers, incentivised sellers and experienced consultants, no integration has been perfectly smooth. Problems will occur, friction will be an issue, cultures will clash and systems will be a mess.

Challenges = opportunities. If you are able to identify and lean into solving the inevitable issues that come up, you will be viewed favourably by leadership, and potentially create new promotion and growth pathways for yourself.

Rule #2, develop an exit strategy:

Not everyone will thrive in this environment. Especially at upper management levels where positions are limited, and in roles where duplication occurs an exit may be necessary. Even if your position or authority is not eliminated or diminished, the working style, new management, and career prospects may no longer be desirable.

Preparing an exit strategy in parallel with doing what you can to thrive is the best strategy. In any job change, people will factor in the trifecta of timing, role and conditions. If you can eliminate timing from the equation and focus on securing an exit that is an ideal position in a desirable firm at compelling conditions, it is ideal. In the case that you wait too long and the company pushes for your exit, timing becomes your overwhelming priority.

When should you start talking to your network and touching base with reputable recruitment agents? Early is always better. You do not need to have made up your mind to leave to initiate discussions with potential new employers. Be honest in discussions, manage expectations of both potential employers and professionals supporting you. You will not burn bridges by having conversations with potential employers and opting not to join them, provided you manage expectations wisely. Conversely, being viewed as passive talent will give you greater leverage in negotiations compared to someone who is clearly desperate to escape.

Negotiate

In almost any situation in an acquisition situation, you can negotiate to improve your position. Here are a few examples:

- Regardless of which side of the deal you are on, look to negotiate a promotion or broadening of your responsibilities.

- If you’re on the side being acquired, this is a chance to renegotiate your package to the new firm. More cash and stock options are the obvious targets; however in some cases the acquiring company needs the human resources of the target and are willing to offer cash retention bonuses to keep talent.

- If you have an equity stake, the opportunity often has negotiable pieces. Partial early payouts, transfer of stock value to that of the acquiring company, increase in equity portion for the purposes of retention or building in a lucrative earn-out clause.

- If you are to be laid off, the acquiring firm has a vested interest for this to go smoothly and for people to leave happily and not cause issues. Leverage this into a strong severance package to buy you time to find your next opportunity.

In summary – be proactive, not reactive:

All too often we see people simply go along with the flow and accept what comes down the line. The deal happened for the interests of leadership / owners / investors upstream of where you sit; so it is on you to look after your own self-interest.

Post-merger integration creates competition and challenge. Be a player, not a spectator.

Andrew Statter is a Partner at Titan GreenTech, an executive recruitment agency focused on the clean energy space.

ASIA ENERGY REVIEW

BY JOHN VAROLI

A brief overview of the region’s main energy events from the past week

Australia / Pumped hydro

Energy major AGL Energy acquired two pumped hydro energy storage sites in NSW, totalling 14 GWh. The two early-stage sites, which are both 10-hour durations, were acquired from renewable energy developer Upper Hunter Hydro Top Trust.

China / Oil refiners

Recent U.S. sanctions on two small Chinese refiners for buying Iranian oil have created difficulties receiving crude. So, they sold the products under other brand names.

China / Clean energy

The Longdong-Shandong project has launched; it’s China’s first “wind, solar, thermal and storage integration” energy base delivery system. More than half of the electricity transmitted by this UHV is clean power such as wind, PV, and energy storage.

China / Oil shipping

China is widening its clandestine supply chain that carries Iranian crude. A tanker identifying itself as Global discharged about 2M barrels of Iranian oil at a Shandong port in late April. However, the vessel was in fact a very large crude carrier called Gather View that’s sanctioned by the U.S. and that took over the identity of a previously scrapped ship.

India / Energy security

As the conflict with Pakistan intensifies, India is boosting security at key energy sites, such as power stations, refineries and LNG terminals.

India / Green hydrogen

Coal India Ltd plans to invest around $3 billion to set up about 4.5 GW of renewable energy capacity, significantly bolstering India’s green hydrogen and ammonia production.

Indonesia / Coal

The world’s largest exporter of coal for power generation shipped out 150 MT of thermal coal over the first four months of 2025, said Kpler; this is the lowest in three years for that same period. The drop was caused by weak demand in China and India – the world’s two largest coal consumers.

Indonesia / Oil products

Indonesia will cut its fuel imports from Singapore and source supplies from the U.S. and Middle Eastern countries, hoping to find better prices. SE Asia’s largest economy will gradually eliminate shipments of oil products from Singapore, which account for more than half its imports, said Energy Minister Bahlil Lahadalia.

Philippines / Floating offshore wind

All three offshore wind projects developed by BuhaWind Energy secured Dept of Energy approval. This allows prioritized permitting across various national and local state agencies. Copenhagen Energy and PetroGreen Energy Corp founded BuhaWind Energy in 2022.

Vietnam / Electricity prices

Vietnam’s retail electricity price climbed 4.8%. Since early 2023, electricity prices in Vietnam were hiked four times: 3%; 4.5%; and two times consecutively, at 4.8%.

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Hulic Ochanomizu Bldg. 3F, 2-3-11, Surugadai, Kanda, Chiyoda-ku, Tokyo, Japan, 101-0062.