WEEKLY

MAY 19, 2025

ANALYSIS

GEOTHERMAL POWER GAINS STEAM AS JAPAN TALKS UP POTENTIAL

- Geothermal power is on the cusp of a technological breakthrough.

- Some of this tech could increase Japan’s geothermal potential by more than four-fold. Will these plans come to fruition?

WATT-BIT COORDINATION: FUTURE OF INTEGRATED POWER AND COMM INFRASTRUCTURE

- Japan’s drive for digital transformation will boost power demand from data centers by 12-fold over the next decade.

- The Watt-Bit Coordination will play a crucial role in guiding this process, proposing how to integrate the power (Watt) and communications (Bit) facilities.

ASIA PACIFIC REVIEW

This column provides a brief overview of the region’s main energy events from the past week

NEWS

- ANRE mulls more support for energy conservation policies and demand response

- Govt annuls certification for 32 renewables projects due to violations

- Japan to adjust revenue cap system reflecting wage increases, inflation

- Early 2025 data shows surge in nuclear output; mixed trends in thermal and hydro power

- TOCOM trading held strong in April

- Spot market trading saw low prices in West Japan

- European Energy launches world’s largest commercial-scale e-methanol project

- Shiga Pref launches hydrogen hub consortium

- NYK working on second commercial ammonia-fueled vessel to grow low-carbon fleet

- Japan delays bill to mandate solar panel recycling

- Renova to invest up to ¥200 billion in grid-scale battery storage in strategic shift

- Toyota’s Aisin starts solar plants in Turkey

WIND POWER AND OTHER RENEWABLES

- Chiba proposes 4th offshore area for wind power

- MOL buys stake in Taiwan offshore wind project

- NTN signs first virtual PPA utilizing Cosmo Eco

- Kashiwazaki-Kariwa NPP’s selection in LTDA said to boost investment potential

- TEPCO submits report on Kashiwazaki-Kariwa NPP Unit 7 incidents

- Alaska says talks are underway with Japanese firms for LNG project

- ENEOS Power to build new LNG-fired power plant

CARBON CAPTURE & SYNTHETIC FUELS

- KEPCO, MHI begin CC test at Himeji No.2

- NYK Group firm completes methanol-fueled CTV for offshore wind

EVENTS

June 4-5 Kyushu Innovation Week / Kyushu GX Decarbonization Expo @ Marine Messe Fukuoka

June 4-6 AXIA EXPO 2025 (Hydrogen and Ammonia Next-Generation Energy Exhibition) @ Aichi Sky Expo

June 15-17 G7 Summit @ Kananaskis, Alberta, Canada

June 18-20 Japan Energy Summit & Exhibition ` Tokyo Big Sight

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Chief Editor)

John Varoli (Senior Editor, Americas)

Kyoko Fukuda (Data, Events)

Magdalena Osumi (Renewables & Storage)

Filippo Pedretti (Thermal, CCS, Nuclear)

Tetsuji Tomita (Power Market, Hydrogen)

George Hoffman (Sales, Business Development)

Tim Young (Design)

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

NEWS: GENERAL POLICY AND TRENDS

ANRE mulls further support for energy conservation, demand response, etc

(Government statement, May 12)

- ANRE discussed key policies to further promote energy efficiency, non-fossil energy transition, and demand response (DR).

- The main direction for energy demand policies includes comprehensive energy conservation, cost-effective decarbonization, support for small and medium-sized enterprises and households, and integrated approaches.

- Govt will continue to promote the following:

- For industrial sectors – investment for upgrades, support for SMEs, and digital technology utilization;

- For commercial and residential – strengthening energy efficiency standards, support for rollout of high-efficiency equipment, and promotion of non-fossil fuel conversions and DR;

- For transportation – electrification of vehicles, alternative fuels transition, and decarbonization of logistics and transportation.

- CONTENTS: The Energy Conservation Subcommittee is considering measures based on the 7th Basic Energy Plan. Looking ahead to 2040, it will implement measures already outlined in the 2030 Energy Supply and Demand Outlook. In addition, it will comprehensively take into account the level of technological innovation, international developments, and the progress of DX and GX.

- SIDE DEVELOPMENT:

- ANRE reports on Energy Conservation Act measures for factories

- (Government statement, May 14)

- ANRE advanced measures related to the Energy Conservation Act in the working group on Energy Efficiency Standards for Factories.

- The group focused on SAF and spoke with Cosmo Oil from the supply side, and Japan Airlines from the demand side.

- Also, ANRE confirmed that data centers will need to set energy efficiency standards.

- CONTEXT: The Energy Conservation Subcommittee is reviewing standards and systems to promote the rationalization of energy use in factories and businesses.

ANRE annuls certification for 32 renewables projects due to violations

(Government statement, May 12)

- Between November 2023 and March 2025, ANRE cancelled 32 renewables project licenses.

- These spanned the work of four firms, including small-scale solar and hydro projects. Key reasons:

- Structural non-compliance (H.D.O., 2 cases)

- Violations of agricultural land laws (Matsuno Concrete Industry, 10 cases)

- Installation at unauthorized locations (Ecokaku, 19 cases)

- Document forgery (Chubu Electric’s Wada Hydropower Plant, 1 case)

- These cancellations reflect stricter enforcement of standards.

Japan to adjust revenue cap system reflecting wage increases, inflation

(Denki Shimbun, May 15)

- The govt will revise the revenue cap system to allow for adjustments in response to wage increases and inflation; this is part of a 5-year plan to boost wages at SMEs.

- The goal is for wage increases to outpace inflation by about 1% annually through FY2029, supporting SMEs by ensuring proper cost pass-through in public procurement, which totals ¥17.4 trillion for local govts and ¥11 trillion for the central govt and state agencies.

- Authorities will prohibit basing the following year’s bidding prices on previous years’ low bids, and will allow contract price adjustments even after agreements are signed if costs rise due to inflation or higher minimum wages.

- Currently, the revenue cap system does not factor in anticipated increases in labor and material costs during the first regulatory period (FY2023–27), raising concerns over negative impacts on businesses, particularly subcontractors.

MoE: Hokuriku Electric should stick to emission targets despite LNG plans

(Government statement, May 9)

- The MoE submitted its opinion to METI on the Toyama Shinko Power Plant Unit 2 project from Hokuriku Electric. It concerns the environmental planning document.

- The utility plans to decommission existing coal and oil units and replace them with a new 600 MW LNG-fired unit.

- MoE emphasized aligning the project with Japan’s long-term climate goals and with global targets. If unable to align, then the utility should scale back or shut the facility.

Honda delays Canada EV plan by two years

(Denki Shimbun, May 16)

- Honda will postpone by 2 years plans for an EV factory and battery factory in Canada, originally scheduled to launch in 2028. The delay is due to slowing EV market growth in North America.

- The EV factory was to have a max annual production of 240,000 units, and the battery factory a max annual capacity of 36 MWh.

Asuene acquires U.S. energy management firm

(Company statement, May 12)

- Carbon accounting software startup Asuene acquired U.S. energy management firm NZero, its first overseas acquisition. This will expand Asuene’s sales in the U.S. by leveraging NZero’s client base and technology.

- NZero, founded in 2019, specializes in energy optimization systems and serves state govts and large energy users like data centers.

Euglena gets METI grant for algae cultivation in Malaysia

(Company statement, April 30)

- Biotech firm Euglena won a METI subsidy to explore the use of palm agricultural residues in Malaysia as a sugar source for microalgae cultivation.

- The project includes biomass resource surveys, sugar extraction trials, and algae cultivation tests.

- CONTEXT: Running until February 2026, this project is similar to a METI-backed SAF supply chain study in Bangladesh. Euglena aims for commercial algae-based bio-crude production in the early 2030s.

NEWS: ELECTRICITY MARKETS

Surge in nuclear output amid mixed trends in thermal and hydro power

(Denki Shimbun, May 12)

- In January, Japan’s total electricity generation increased 2.2% YoY to 79,360 GWh; the first YoY rise in three months.

- The uptick was due to peak winter demand and the restart of Tohoku Electric’s Onagawa Unit 2 and Chugoku Electric’s Shimane Unit 2.

- Monthly nuclear power generation rose 27.1% YoY, reaching about 8,350 GWh. Kyushu Electric saw a 39.7% increase in nuclear output, while Kansai Electric saw a 7.6% decrease. Shikoku Electric recorded a marginal 0.1% increase.

- Thermal power remained the dominant source, increasing 0.5% to 63,160 GWh. In this category, coal-fired generation rose 4.9%. LNG dropped 2.6% and oil-fired generation declined 21.2%.

- Hydropower showed mixed results. Conventional hydropower output decreased 15%, while pumped storage hydro increased 22%.

- The combined generation of major electric utilities rose 1.8% YoY to 53,370 GWh. Yet, their thermal power output declined 0.5%, with coal increasing 5%, LNG decreasing 2.7%, and oil falling 26.1%.

TOCOM electricity futures trading held strong in April

(Exchange statement, April 2025)

- Electricity futures trading at the Tokyo Commodity Exchange (TOCOM) reached 12,351 contracts in April, slightly below the record 12,600 in March.

- Off-auction trades dominated, particularly large-scale hedges fixing prices for the entire FY2026 (April 2026–March 2027), with East Japan base-load contracts totaling 711 GWh (9,744 contracts), many exceeding 40 GWh each. Seasonal contracts were also prominent.

- The number of transactions jumped to 393, roughly 2.4 times the previous month’s total of 167, reflecting increased participation from both major and smaller-scale market players. Weekly contracts saw a dramatic 17.5-fold MoM increase, reaching about 7.5 GWh (460 contracts).

- Final settlement prices for April 2025 monthly contracts were ¥11.45/ kWh for East Japan baseload, down from ¥15.85/ kWh at initial listing in May 2023, indicating lower forward pricing.

- Open interest at the end of April reached a record high of about 909 GWh, up 30% from the previous month.

April spot market trading saw low prices in West Japan

(Exchange data, media reports, May 16)

- The average daily trading volume on the spot market fell 11.4% MoM to 692.9 GWh in April, marking a second consecutive month of declines. Total monthly trading volume dropped 14.2% from March to 20.79 TWh, accounting for 34.1% of total electricity demand.

- Despite cold weather early in the month driving demand and prices nationwide, warmer days from the second week onward led to a low-price trend in West Japan.

- The monthly average system price (24-hour) dropped below ¥10. The average daily electricity demand across Japan’s nine major grid areas fell 12.3% from the previous month, but was up 1.6% YoY.

MHI’s GTCC sector sees huge growth

(Company statement, May 9)

- MHI released its FY2024 financial results. Data show a strong performance for the GTCC (gas turbine combined cycle) business. There were orders for 25 large frame gas turbine units, with demand high especially in the Americas and Middle East.

- The GTCC segment reported a significant increase in both orders and revenue. Orders reached ¥1,474 billion, up from ¥1,259 billion in FY2023, while revenue rose to ¥791 billion from ¥736 billion in the previous year. Income is balanced between new installations and service contracts.

- MHI is expanding production capacity for gas turbine components.

- CONTEXT: The surge in GTCC orders is due to the transition from coal to gas and growing electricity demand in emerging markets. There’s been a rebound in global gas turbine demand, from 29.2 GW in 2020 to 36.3 GW in 2023, said McCoy Power Reports. Utilities are looking for more gas-fired power to complement renewables.

TAKEAWAY: Similar to competitors in the U.S. and Europe, MHI has booked a big jump in gas turbine and other power equipment orders thanks to grid upgrades, AI-driven rising power demand, and the tilt to renewables. The lead times for items such as transformers, used for power transmission, are said to be up threefold in the last five years; turbine waiting times stretch to the end of this decade. MHI is also preparing its turbines to serve the needs of next-gen fuels. MHI says they can co-fire hydrogen and deliver over 64% thermal efficiency.

Tekoma Energy discloses first PPA with Shikoku Electric

(Company statement, May 12)

- HSBC-backed renewables developer Tekoma Energy inked its first disclosed power purchase agreement (PPA) with Shikoku Electric.

- Tekoma will develop three solar power plants in Shikoku, with a total capacity of 4.5 MW, scheduled to begin operation in 2026.

- Shikoku Electric will procure the output and supply it to JTEKT Corp, a Toyota Group bearings manufacturer, for use at 10 of its domestic facilities.

- This is believed to be the largest physical offsite corporate PPA in the Shikoku region. Tekoma plans to expand its domestic solar portfolio to over 1 GW within three years.

- CONTEXT: Tekoma Energy, founded in 2013 and acquired in 2023 by HSBC Asset Management, received a $50 million investment from ABC Impact in 2024 to accelerate its growth. The firm develops, owns, and operates solar and storage projects in Japan, Taiwan, and South Korea.

J-POWER lines up nuclear bid for next decarbonized power sources auction

(Denki Shimbun, May 12)

- J-POWER President Kanno Hitoshi said the firm aims to bid Ōma NPP in the 3rd Long-Term Decarbonization Power Source Auction. In the first auction (FY2023), Chugoku Electric’s Shimane NPP Unit 3 secured an award.

- CONTEXT: Oma NPP is classified as under construction and start of operations was pushed back a number of times, to about 2030 to allow time for further safety tests. Shimane NPP Unit 3 is also under construction.

- Kanno said an LTDA application will also be made for Matsushima Thermal Power Plant Unit 2 (500 MW), which is being converted into an Integrated Gasification Combined Cycle facility. It will switch to coal and hydrogen co-firing.

TG Octopus launches discounted daytime electricity rate for all-electric homes

(Company statement, May 13)

- TG Octopus Energy, a JV between Tokyo Gas and UK-based Octopus Energy, introduced a new electricity pricing plan aimed at all-electric households, offering lower rates during daylight hours to encourage solar power usage.

- The “All-Electric Octopus–Sunshine” plan provides electricity at ¥16.92/ kWh from 9 a.m. to 3 p.m., much cheaper than the ¥26.43/ kWh charged at other times.

- Available in all regions except Okinawa, the plan includes a fuel cost adjustment that raises or lowers rates based on an average fuel price threshold of ¥44,200/ kiloliter.

- SIDE DEVELOPMENT:

- Tohoku Electric to sell electricity to Tokyo-area households via Tokyu Power

(Company statement, May 13)- Tohoku Electric agreed with Tokyu Power Supply to sell electricity to households in the Tokyo metropolitan area, beginning late September 2025.

- Tokyu Power Supply will manage customer contracts and billing under its brand, using electricity supplied by Tohoku Electric.

- The two companies plan to launch bundled packages combining electricity with additional services, with details to be announced around September.

NEWS: HYDROGEN

European Energy launches world’s largest commercial-scale e-methanol supply

(Nikkei, May 14)

- European Energy, a Danish subsidiary of Mitsubishi HC Capital, began supplying e-methanol; it built the world’s first and largest production facility of its kind.

- The facility integrates 304 MW of solar power and 52 MW of water electrolysis capacity, enabling the production of up to 42,000 tons of e-methanol annually. The fuel is expected to be used by global firms including shipping giant A.P. Moller-Maersk, pharmaceutical manufacturer Novo Nordisk, etc.

- European Energy has an extensive renewable energy footprint, operating across 25 countries with 4.5 GW of completed renewables facilities, and over 65 GW in the development pipeline. It also launched a wind-powered green hydrogen plant in Denmark in October 2024, positioning itself as a leader in Power-to-X technologies.

Shiga Pref launches hydrogen hub consortium

(Government statement, May 13)

- The Shiga Hydrogen Hub Formation Consortium has launched to promote hydrogen across energy-intensive industrial sectors.

- As one of Japan’s lead manufacturing regions, Shiga is targeting hard-to-electrify sectors, estimating potential local hydrogen demand at about 200,000 tons per year.

- The consortium includes Sekisui Chemical, Chiyoda, JR West, and Murata Manufacturing (Yasu Plant), along with the cities of Hikone, Yasu, and Maibara.

- The group aims to examine the hydrogen supply infrastructure and link inland demand with coastal hydrogen projects. Maibara is positioned as a potential hydrogen supply hub, given its strategic location.

- A kick-off seminar and founding meeting will be held on June 2, 2025, at the Maibara City Convention Hall.

NYK works on Japan’s second commercial ammonia-fueled ship

(Company statement, May 15)

- NYK is developing a second ammonia-fueled ammonia carrier with Japan Engine, Japan Shipyard, and IHI Power Systems. It will be a 40,000 m3 ocean-going vessel.

- To be delivered in late 2026, this ship aims to reduce a standard vessel’s GHG emissions by over 80%.

- NYK plans to launch 15 ammonia-fueled ships by 2033.

- CONTEXT: In August 2024, Japan launched the world’s first commercially operated ammonia-fueled vessel – a modified tugboat, Sakigake – with support from the NEDO Green Innovation Fund. Originally built as Japan’s first LNG-fueled tug, Sakigake was retrofitted by NYK Line and IHI Power Systems.

NOK Group launches “H2 Project” to expand hydrogen technologies

(Company statement, May 12)

- NOK Group plans to expand in the hydrogen economy, across the entire supply chain — from producing hydrogen via electrolysis to transporting and storing the fuel, and finally to utilizing it in fuel cells for vehicles and power generation.

- CONTEXT: Since the 1990s, NOK has supplied advanced seals for fuel cell stacks, which are essential for containing hydrogen, oxygen, and cooling fluids in high-efficiency fuel cell systems.

NEWS: SOLAR AND BATTERIES

Japan delays bill to mandate solar panel recycling

(Government statement, May 13)

- The MoE and METI won’t be able to submit a bill mandating solar panel recycling in the current parliamentary session.

- The delay owes to the Cabinet Legislation Bureau’s request to address inconsistencies with existing laws, particularly who bears the responsibility for recycling costs.

- The proposed bill had aimed to make the manufacturers responsible for recycling expenses. While this is feasible for new panels, it’s difficult to apply retroactively.

- MoE and METI ministers said they’ll revise the bill by referencing other recycling laws, such as for autos and electronic devices, and submit it “as soon as possible”.

- CONTEXT: With most solar panels to reach the end of lifespan in the 2030s, concerns are growing over mass disposal and landfill use. Estimates suggest that annual disposal could peak at around 170,000 to 280,000 tons between 2035 and 2037.

TAKEAWAY: In March, an expert panel suggested that both domestic manufacturers and importers should share recycling costs. However, this contrasts with models like Japan’s end-of-life automobile recycling law, where owners pay, raising legal consistency concerns. The bill was supposed to build on the amendment to the Renewable Energy Act in April 2022, which requires operators of solar power facilities over 10 kW to set aside funds for equipment disposal. The bill’s success will depend on fair distribution of responsibilities, the establishment of a clear legal framework, effective enforcement, and the development of adequate recycling infrastructure. Japan lacks legislation for PV waste management. Also, as the bill stipulates that manufacturers or importers bear recycling costs, while equipment owners cover dismantling, this may disproportionately affect domestic manufacturers, especially if importers of foreign-made panels, notably from China, evade responsibilities.

Renova to invest up to ¥200 billion in grid-scale battery storage

(Nikkei, Company statement, May 12-13)

- Renewables developer Renova plans to invest up to ¥200 billion by 2030 to develop grid-connected battery storage facilities across Japan.

- This marks a strategic pivot from large-scale solar to battery storage as Renova’s growth focus. The shift comes as solar and wind energy have increasingly led to grid strain and output curtailments when supply exceeds demand.

- The firm aims to expand its storage capacity from the current 230 MW (from three sites awarded subsidies via the LTDA) to 1 GW by the early 2030s. It plans to fund 80% of investment via project finance, and is considering JVs and govt subsidies.

- CONTEXT: Renova developed and owns a 1.5 GW portfolio in total generation capacity across multiple energy sources, with total assets worth around ¥500 billion – including solar power (429 MW), onshore wind (346 MW), and biomass (445 MW).

- Battery storage is seen as key to reducing the curtailment of solar farms, particularly in areas like Kyushu, where it reached 6% in FY2025. As of Sept 2024, only 100 MW of grid-scale batteries were connected in Japan.

- Renova said it will invest around ¥340 billion in small-scale solar power, storage batteries, and other areas like onshore wind power by FY2031.

TAKEAWAY: Renova expects increased demand for balancing capacity, and a significant reduction in BESS costs, accelerating faster battery connections to the grid. A focus shift to BESS comes as Renova expects to post its first net quarterly loss since listing, due to issues at its biomass power plants. The latter struggle as Japan moves away from FIT to FIP, which carries explicit market price volatility risk, due to high fixed operating costs. Meanwhile, the BESS market is seen as a blue ocean. If METI’s 2030 forecasts are correct, and the country will have 24 GWh of BESS installed by then, it means the current 100 MW (at an average discharge duration of 3 hours) would need to grow about 80x.

- SIDE DEVELOPMENT:

- TEPCO launches its first grid-connected BESS in Gunma

- (Company statement, May 15)

- TEPCO began operating its first battery energy storage facility in Tsumagoi Village, Gunma Pref. The project received a grant from METI/ANRE.

- Developed with NTT Anode Energy, the 2 MW facility stores electricity during low-price periods and discharges it when prices are high.

- It also aims to support grid stability amid increasing use of renewable energy.

Ecokaku secures order for PV and BESS systems from Mori Building

(Company statement, May 9)

- Ecokaku won an order from urban developer Mori Building for a solar power system with battery storage, valued at ¥2 billion.

- Ecokaku seeks to grow solar-related revenue from ¥12.5 billion in the fiscal year ending January 2025 to ¥21 billion by the January 2027 fiscal year.

- Growth initiatives include expanding solar equipment sales and installation, scaling agrivoltaic projects, strengthening on-site and off-site corporate PPA offerings, and activating the secondary solar market.

JGC Group and startup PXP test new lightweight solar panels in Yokohama

(Company statement, May 15)

- JGC Holdings and solar startup PXP began a one-year demo of a new type of lightweight, flexible thin-film solar panel on a facility roof in Yokohama.

- The panel combines perovskite and chalcopyrite solar cells to generate power from a range of light wavelengths.

- The duo is testing a new, simplified installation method. The system has a 1 kW capacity, weighs around 20 kg, and covers 10 square meters. The goal is to enable long-term use over 20 years.

Toyota’s Aisin starts solar plants in Turkey

(Company statement, May 7)

- Aisin’s Turkish subsidiary launched two solar power plants (7 MW and 2.7 MW) in Malatya Province, Turkey. Aisin is a Toyota group’s auto components manufacturer.

- All of Aisin’s production sites in Europe now operate on 100% renewable energy.

NEWS: WIND POWER AND OTHER RENEWABLES

Chiba Pref proposes 4th offshore area for wind power development

(Company statement, April 24)

- Chiba Pref govt submitted information on a fourth offshore area – about 3 km off Asahi City – as part of Japan’s offshore wind promotion process.

- This follows previous submissions for waters off Choshi City (already selected for development by the consortium led by Mitsubishi), Isumi City, and Kujukuri Town.

- The central govt will review the new area with input from a third-party committee and may classify it as a “promising”, or “preparation” zone before moving to formal designation through stakeholder discussions.

MOL buys stake from CIP in Taiwan offshore wind project

(Company statement, May 9)

- Mitsui O.S.K. Lines (MOL) will pay ¥25 billion to acquire a 10% stake in a Taiwan offshore wind project from Copenhagen Infrastructure Partners. The 495 MW project is set to be completed by the end of 2027.

- Located off Taichung, the project will install 33 Vestas turbines, each 15 MW.

- The electricity will be supplied to six companies, including Google and leading Taiwanese semicon foundry United Microelectronics Corp, through existing PPAs.

- CONTEXT: This is MOL’s second involvement in Taiwan’s offshore wind sector, following its participation in the Formosa 1 project.

NEDO identifies new promising sites in Tohoku for supercritical geothermal power

(Nikkei, May 14)

- NEDO named three promising sites in the Tohoku region – Kakkonda (Shizukuishi Town, Iwate Pref), Hachimantai City (Iwate Pref), and Southern Yuzawa (Akita Pref) – for supercritical geothermal power generation.

- Each has the potential to host one of Japan’s largest geothermal plants, with a capacity of 100 MW and a 30-year operating life.

- CONTEXT: Supercritical geothermal systems tap into heat at depths of up to 5 km, where water reaches 500°C and exists in a supercritical state (with higher temperature and pressure than conventional geothermal that operates at 1–3 km depth).

- Construction-related surveys could begin as early as FY2026.

- METI aims for early commercialization of the tech by the 2030s and will release a roadmap by October 2025. Drilling surveys may begin as early as FY2026–2027.

TAKEAWAY: Supercritical geothermal recently gained strong interest in a number of countries, including the U.S., with a number of technologies emerging such as closed-loop systems and CO2-injection geothermal. Japan, as a volcanically active country, has strong potential. Japanese firms already hold 67% of the global market in geothermal turbines, making this a rare renewable sector where Japan leads. See this week’s Analysis section for a deep dive on the geothermal sector.

NTN signs first virtual PPA utilizing Cosmo Eco Power’s wind farm

(Company statement, May 9)

- Bearings manufacturer NTN inked its first virtual PPA with Cosmo Eco Power to procure 10 GWh of renewable power annually from the Chuki Wind Farm in Wakayama Pref.

- The 16-year agreement marks the first such deal for both companies, with the wind farm using NTN’s bearings and monitoring systems.

- Installed capacity is 48.3 MW (23 turbines, 2.1 MW each).

Japan launches panel to advance artificial photosynthesis tech

(Japan NRG, May 14)

- Japan launched a govt-led panel to advance artificial photosynthesis, a tech that mimics plants in converting CO2 into resources using sunlight. MoE Minister Asao likened it to a “Japanese Apollo Project.”

- While Japan leads in research, challenges remain in efficiency and cost. Experts will draft a roadmap by this autumn for real-world implementation.

- CONTEXT: Artificial photosynthesis is a promising approach to reducing GHGs that uses CO2 emitted from factories and power plants as a raw material for chemical products while using clean hydrogen. In the process, solar power is used to split water and make hydrogen. This hydrogen, combined with CO2 from factories, can produce olefin, turning a process that used to emit CO2 into one that absorbs it.

- Mitsubishi Chemical participated in an artificial photosynthesis project conducted by NEDO and has been pushing forward with development in partnership with domestic chemical manufacturers, universities, national institutes, etc.

NEWS: NUCLEAR

Kashiwazaki-Kariwa NPP’s selection in LTDA to boost its investment potential

(Nikkei, May 16)

- TEPCO president Kobayakawa supports state backing for decarbonized energy sources, saying it enhances investment predictability for financial institutions.

- The govt selected TEPCO’s Kashiwazaki-Kariwa NPP Unit 6 in the long-term decarbonized power sources auction.

- CONTEXT: The program targets facilities that need support from FY2027 onward. They include existing NPPs needing safety upgrades.

TEPCO submits report on Kashiwazaki-Kariwa NPP Unit 7 incidents

(Company statement, May 12)

- TEPCO submitted to the NRA its findings on four incidents at Kashiwazaki-Kariwa NPP Unit 7; it includes causes and related improvement measures.

- The four incidents occurred at Unit 7 between Nov 2024 and Jan 2025, such as failure of satellite phones, which constituted violations of operational limits. Thus, on April 30, the NRA changed the plant’s response category from Level 1 to Level 2.

- The company has since secured backup phone systems.

- SIDE DEVELOPMENT:

- One worker at Genkai NPP exposed to radiation

(Company statement, May 11)- At Genkai NPP Unit 3 one reactor maintenance worker was exposed to a low dose of radiation. Inspection confirmed no surface contamination.

- The cause is still under investigation. The plant is undergoing regular inspection.

NEWS: TRADITIONAL FUELS

Alaska says talks are underway with Japanese firms for LNG project

(Nikkei, May 13)

- Alaska Governor Mike Dunleavy said discussions are underway with several Asian countries on the Alaska LNG project. These include Japan, South Korea, and India.

- Talks with several Japanese companies, including Mitsubishi Corp, already took place. Discussions are in early stages.

- CONTEXT: Japanese energy companies and trading firms are considering involvement. Still, they have concerns about profitability. The project will likely cost at least $44 billion due to high pipeline construction expenses. This is raising doubts about feasibility.

- Dunleavy suggested breaking up the project to reduce the financial burden.

TAKEAWAY: The U.S. side is said to have split the project into three stages, offering potential stakeholders more digestible investment portions and extending payment over a broad period of time. Part of the piped gas would also be diverted for local needs, which is touted as an early-stage revenue stream. What will push the currently exploratory discussions into more concrete contracts, however, is unclear. Japanese companies likely are waiting on state guarantees and other backing from the govt. PM Ishiba’s Cabinet will likely weigh its involvement based on progress in trade talks with the U.S. In that sense, we may see signing of MoU-like terms in June.

ENEOS Power to build new LNG-fired power plant

(Denki Shimbun, May 14)

- ENEOS Power will build a new LNG-fired power plant (750 MW) in Kawasaki City. Another LNG plant, co-owned with Tokyo Gas, is already operational there.

- The new plant will use a gas turbine combined cycle (GTCC) system, aiming to start operations in early 2033. Construction will begin in the first half of 2029, with equipment installation around 2031, trial runs in 2032, and full operation in 2033.

- ENEOS submitted the Environmental Considerations Report that mentions participation in long-term decarbonized power sources auctions, but does not disclose financing plans.

- SIDE DEVELOPMENT:

- Gas leaks at ENEOS’s Sakai Refinery results in one death

- (NHK, May 17)

- Three people were hospitalized and one died after a gas leak at ENEOS’s Sakai Refinery in Sakai City (Osaka).

- The three workers collapsed after likely inhaling leaked hydrogen sulfide. The leak may have occurred after a pipe was removed during repair work.

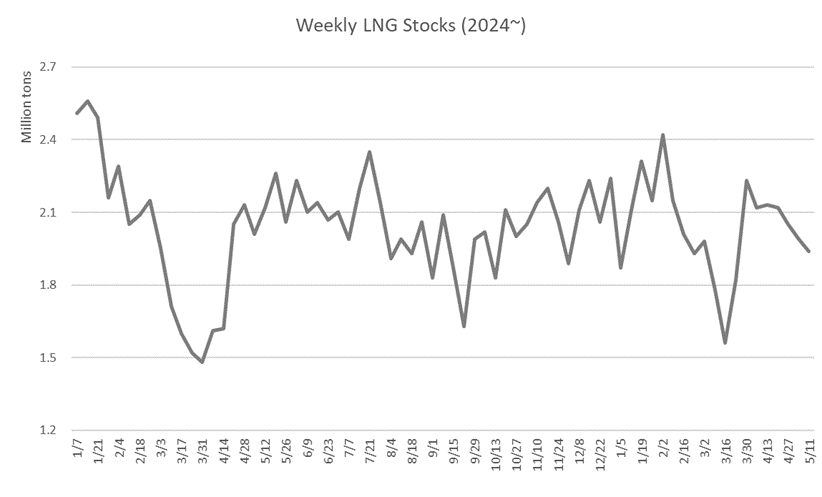

LNG stocks down from previous week, down YoY

(Government data, May 14)

- The govt published data for the past two weeks. The inventory was calculated as of May 11 and data for May 4 was also added.

- The LNG stocks of 10 power utilities were 1.99 Mt as of May 4, and 1.94 Mt as of May 11. That is down 5.4% from April 27 (2.05 Mt), down 6.3% from end May (2.07 Mt), and down 11% from the 5-year average of 2.18 Mt.

- The graph below shows the weekly LNG stocks for the past 16 months. The utilities tend to adjust their stocks at the end of March and September, which are the last months of the 1H and 2H of a fiscal year.

- There are seasonal fluctuations in the stocks in summer and winter. This means LNG stocks will show upward trends in coming weeks to prepare for the summer heat.

NEWS: CARBON CAPTURE & SYNTHETIC FUELS

KEPCO, MHI begin test of CC at Himeji No.2 Power Plant

KEPCO, MHI begin test of CC at Himeji No.2 Power Plant

(Company statement, May 14)

- KEPCO and MHI completed a pilot CO2 capture facility at Himeji No. 2 Power Plant.

- The facility uses a liquid amine-based CO2 separation and capture system, and has a daily capacity of 5 tons of CO2. The goal is to develop a CO2 capture process suited for combined cycle power plants.

- CONTEXT: The project targets combined cycle power plants using LNG, now a mainstream power generation method, considered to have a higher efficiency and lower CO2 emissions. The Himeji No.2 Power Plant comprises 6 units, each with a capacity of 486 MW.

JFE Engineering firm completes food biogas power plant in Hokkaido

(Company statement, May 16)

- Sapporo Bio Food Recycle, a part of JFE Engineering Group, completed Hokkaido’s largest food biogas power plant in the Sapporo Recycling Complex.

- The plant uses microorganisms to ferment food waste to produce methane gas, which is then used to generate electricity.

- The electricity is sold through the FIT program and Urban Energy, a subsidiary of JFE Engineering, aiming for local production and consumption of renewable energy.

- CONTEXT: Sapporo City created its Second Basic Environmental Plan in 2018 and is actively working toward becoming a zero-carbon city by 2050.

NYK Group firm completes methanol-fueled CTV for offshore wind

(Company statement, May 9)

- Northern Offshore Services, a part of NOG, which in turn is part of the NYK Group, built a methanol-fueled crew transfer vessel (CTV).

- It will be used for offshore wind power operations in Europe.

- This is the world’s first CTV to operate exclusively on bio-methanol.

- CONTEXT: In January, NYK acquired a majority stake in Sweden-based NOG, a pioneer in CTV operations for offshore wind power. NOG is the leading CTV operator in Europe, operating more than 60 CTVs at offshore wind power sites.

- SIDE DEVELOPMENT:

- NYK Group firm completes first methanol dual-fuel bulk carrier

- (Company statement, May 13)

- NYK Bulk & Projects Carriers held a delivery ceremony for a methanol dual-fuel bulk carrier at Tsuneishi Shipbuilding Factory in Fukuyama, Hiroshima.

- This is the NYK Group’s first bulk carrier equipped with a dual-fuel engine that can run on both methanol and heavy oil.

- CONTEXT: Methanol has a lower environmental impact than heavy oil; and the use of bio-methanol, or e-methanol made from renewable hydrogen and captured CO2, can significantly reduce GHG emissions.

ANALYSIS

BY CHISAKI WATANABE

Geothermal Power Gains Steam as Japan Talks Up Potential

In his first policy speech, it wasn’t solar or offshore wind power that Prime Minister Ishiba mentioned as a renewable energy source with high potential. As Japan’s 102nd premier took office in October 2024, he counted geothermal power among promising energy sources to address Japan’s energy constraints.

In a major policy speech by a Japanese leader, the choice of geothermal energy, which uses underground heat to drive turbines, was unusual. Despite its well-known potential, geothermal energy development has barely progressed in Japan even after the feed-in-tariff (FIT)-driven renewables boom was unleashed in 2012.

Most of the capacity added since then has been in solar power, and the big bet for the 2030s is on offshore wind. Meanwhile, biomass and hydro have enjoyed mild success. But geothermal?

Since Ishiba’s inauguration, however, geothermal energy has gained momentum. In November, METI and MoE unveiled a policy package to bolster developments in the sector. The package includes the “Geothermal Frontier Project” to expand geothermal power using conventional technologies. Officials also set up a public-private forum to promote next-generation geothermal technologies, with more than 70 companies and groups joining as members.

Buoyed by increased demand for clean electricity, the sector is on the cusp of a technological breakthrough. Some of the emerging tech is forecast to increase Japan’s geothermal potential by more than four-fold. So, what’s different this time?

Hello again, Sunshine

“For the first time since the Sunshine Project of the 1970s, the geothermal energy sector is being revitalized,” Hosono Goshi, a former minister of the environment, declared in November in relation to the Geothermal Frontier Project. Hosono is a member of the ruling Liberal Democratic Party. He’s also become the head of a coalition of bipartisan lawmakers that promote geothermal power.

The government launched the Sunshine Project in 1974 to boost R&D in “new energy” technologies following the oil shock of the previous year. The idea was to reduce Japan’s dependence on oil by developing alternative energy sources. While it is best known for guiding the early progress with solar panels, the project also supported geothermal and wind power.

The renewed focus on geothermal comes as Japan’s electricity demand is projected to increase substantially thanks to wider application of AI and data centers. The change also comes amid an increasing need to decarbonize the power mix to meet climate goals.

Japan’s push in renewables has been so far centered around solar and wind, both intermittent sources that are causing a growing curtailment trend. In contrast, geothermal is classified as a baseload power source.

Geothermal tech uses heat to produce steam, which drives turbines to generate decarbonized electricity consistently and continuously. Hence, geothermal is welcomed by planners looking for clean energy sources to integrate more solar and wind on the grid.

Currently, Japan has more than two dozen geothermal power stations, many located in the Tohoku and Kyushu regions. The country’s installed capacity is about 0.6 GW, a fraction of its potential of 23 GW, which is the world’s third largest.

Table 1: Yearly addition of geothermal capacity in Japan

Before 2012 | 2015 | 2017 | 2018 | 2019 | 2020 | 2022 | 2023 | 2024 | |

# of plants | 13 | 3 | 1 | 1 | 2 | 1 | 1 | 3 | 3 |

MW | 375 | 9 | 5 | 5 | 54 | 15 | 2 | 19 | 26 |

Source: Compiled by Japan NRG based on JOGMEC data

About half of Japan’s geothermal plants launched before 2012, when the government introduced the FIT program to incentivize renewable energy deployment. In the early 2000s, domestic turbine makers such as Toshiba, Mitsubishi Heavy Industries, and Fuji Electric held a two-thirds global market share in geothermal turbines thanks to sales at home, in Southeast Asia, Kenya and elsewhere.

But not many new plants are due to come online in Japan in the near future. According to a government report, there are only two projects with definite start dates over the next four years. INPEX is building a 15 MW project with Idemitsu and TEPCO Renewable Power in Akita Pref, slated to open in March 2027. Another 15 MW station, also in Akita, is under development by Tohoku Electric’s renewables unit, and slated to start operations in November 2029.

Two more projects are in advanced stages, but they have no publicly available start dates.

Greater Expectations

In the Sixth Basic Energy Plan released in October 2021, geothermal power’s FY2030 target was set at 1.5 GW (11 TWh), or 1% of Japan’s total electricity. That was upgraded in the Plan’s seventh edition, adopted by the Cabinet in February, calling on geothermal power to account for 1 – 2 % of the generation mix by FY2040. The latest Plan does not specify capacity and generation targets, but that share roughly translates to 11 to 12 TWh, according to Japan NRG calculations.

Even based on the minimum FY2040 target, which can be assumed as 1.5 GW, Japan needs to add nearly 1 GW of geothermal capacity within 15 years. That’s not easy given the size of the stations under construction and the fact that it takes about 10 years to build a new plant.

The government has tried to identify the factors holding back the sector. In the geothermal policy package released in November, the following reasons were cited:

- Large risks during early stages of development

- Long lead time to receive approvals and permissions aligned with laws on hot springs, natural parks, and forests, as well as the need to gain local understanding, and agreement with hot spring operators

Natural parks play a big role in geothermal in Japan. About 80% of the country’s potential is located in national and quasi-national park acreage. Development in those parks, however, has been largely restricted since 1974 after water quality concerns and landscape damage issues marred several projects.

Officials revised these development guidelines in 2012, 2015 and 2021, in effect expanding the areas open for drilling and construction amid increasing calls to deliver more renewables. The government has been also working to promote understanding from hot spring operators to placate their concerns about possible impact on hot water sources, since geothermal power plants are often built nearby.

Table 2: Geothermal potential in and out of natural parks

Areas (zones in bold are inside natural parks) | Potential capacity (GW) |

Special Protection Zone | 7 |

Special Zone 1 | 2.6 |

Special Zone 2 | 2.5 |

Special Zone 3 | 5.2 |

Regular Zone | 1.1 |

Outside national, quasi-national parks | 5 |

Total | 23.4 |

Source: METI

In order to address these geothermal industry’s problems, the government said it will make changes including:

- The government will take on the early development risks. State-backed energy firm, JOGMEC, will expand the scope of survey from the very early stage (ground-level geological survey, small diameter drilling) to the early stage (drilling, short-term flow tests) and the exploration stage (flow tests).

- METI will lead the coordination with ministries and local governments to expedite the approval process and the consensus-building process among local stakeholders.

- The government will replicate successful approaches to other projects to speed up geothermal development nationwide.

The above initiatives are intended to accelerate geothermal deployment using conventional technologies, which use hot water and steam that naturally exist in geothermal reservoirs. But there are also technological innovations.

Next Generation

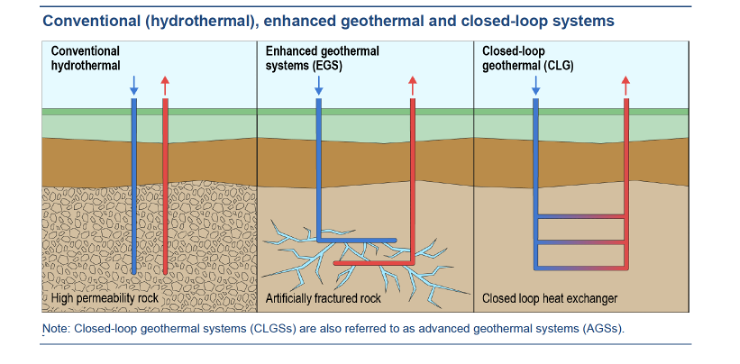

Last November’s package also included measures to support new tech. Japan, like other major countries, is increasingly looking at the next set of technologies that promise to utilize more of geothermal resources by delving into wider and deeper areas.

Introducing technologies such as enhanced geothermal systems (EGS), closed-loop geothermal systems, supercritical geothermal systems, and EGS using carbon dioxide, could add 77 GW more of geothermal potential in Japan, according to METI estimates.

Chart 1: Different types of geothermal technologies

Source: IEA report “The Future of Geothermal Energy”

On April 14, METI launched a public-private council to specifically discuss next-generation geothermal technologies, planning to commercialize these and strengthen industrial competitiveness by the early 2030’s.

The council, uniting more than 70 companies and groups, will set targets and plans to deploy more geothermal, as well as to compile a roadmap by around October this year. This will include measures to reduce costs and expand Japan’s market share for this tech overseas.

Conclusion

The planned roadmap appears to heavily focus on how to ensure Japan can lead in geothermal technology. Past government pilot projects, however, indicate that technology alone will not be enough.

Expanding next-gen geothermal power requires more overarching plans to address challenges, such as how to develop a supply chain and where to build new plants in order to offer baseload power to heavy energy users such as data centers.

The co-location of clean power and new heavy energy users is being discussed by the Cabinet’s industry location working group for the Green Transformation (GX) that kicked off in April. WIth a stronger concerted effort, geothermal energy could become well positioned to make its mark in Japan’s energy sector.

ANALYSIS

BY TETSUJI TOMITA

Watt-Bit Coordination: Future of Integrated Power and Comm Infrastructure

The rise of artificial intelligence and Japan’s drive for digital transformation is forecasted to boost power demand from data centers by 12-fold over the next 10 years. For such a surge to be met with clean energy, Japan needs both massive investment and thorough state planning.

Toward that goal, the Watt-Bit Coordination (WBC) initiative will play a crucial role. Created to promote a strategic approach to infrastructure development, particularly proposing how to integrate the power (Watt) and communication (Bit) facilities, the initiative has gathered a broad body of Japanese and international businesses.

Proposed by TEPCO Power Grid during the “GX2040 Leaders Panel” in 2024, the WBC focuses on an integrated development of power systems and communication infrastructure, recognizing that physical separation between decarbonized power sources and data centers can lead to increased costs and time for grid development.

By leveraging the cost-effectiveness of optical fiber cables – at 1% the cost of power transmission lines – the strategy involves situating data centers near clean power sources and extending cables to transmit information, thereby overcoming physical distance constraints.

Challenges

In March 2025, the Ministry of Internal Affairs and Communications (MIC) and METI launched the Public-Private Council on Watt-Bit Coordination Roundtable to shepherd stakeholders in the power and telecommunication sectors into coordinating their activities, aiming to improve the efficiency of new infrastructure built to support DCs.

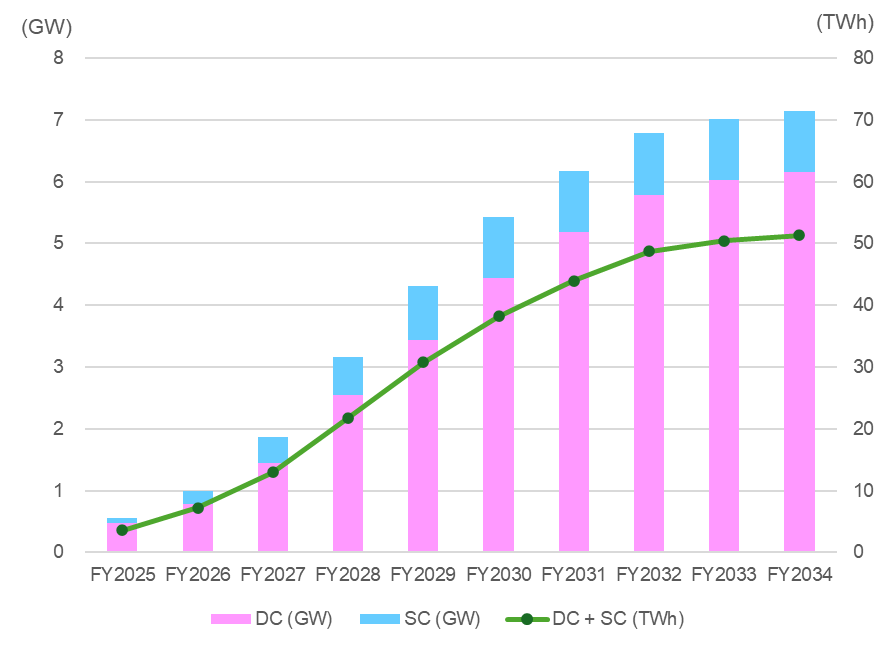

The widespread adoption of AI technologies has led to a major increase in power consumption by data centers. According to an OCCTO January 2025 report, the maximum power demand nationwide for FY2034 will be 165 GW, while total power consumption will be about 852 TWh.

When compared to the final year (FY2033) of the supply plan submitted by TSOs last year, the maximum power demand was revised upward by 3.06 GW from 162 GW to 165 GW, and the total electricity demand was revised upward by 17,960 GWh from 835 TWh to 852 TWh. By FY2034, the power usage and peak demand by data centers and semiconductor factories is projected to rise to 51.4 TWh and 7.15 GW, respectively.

In terms of regional breakdown, the Tokyo area is expected to account for nearly 60% of the total, with further growth anticipated. However, the report also indicates that demand at data centers and semiconductor factories is also expected to increase in regions outside the metropolitan area.

Peak Power Demand and Power Consumption for Data Centers

Source: Japan NRG (based on OCCTO data in 2025)

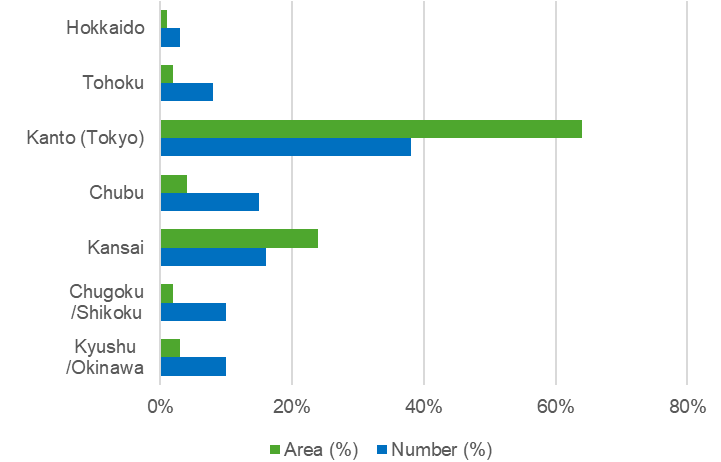

Currently, over 80% of Japan’s data centers are concentrated in the Tokyo and Osaka metropolitan areas, which poses risks related to natural disasters and power supply constraints. Also, the limited availability of suitable land and high cost of electricity in these regions hinder expansion of data center facilities. Plans to build data centers in urban downtowns have met strong opposition from residents.

Percentage of Data Centers by Region

Source: Japan NRG (based on MIC, METI Watt-Bit Coordination Meeting)

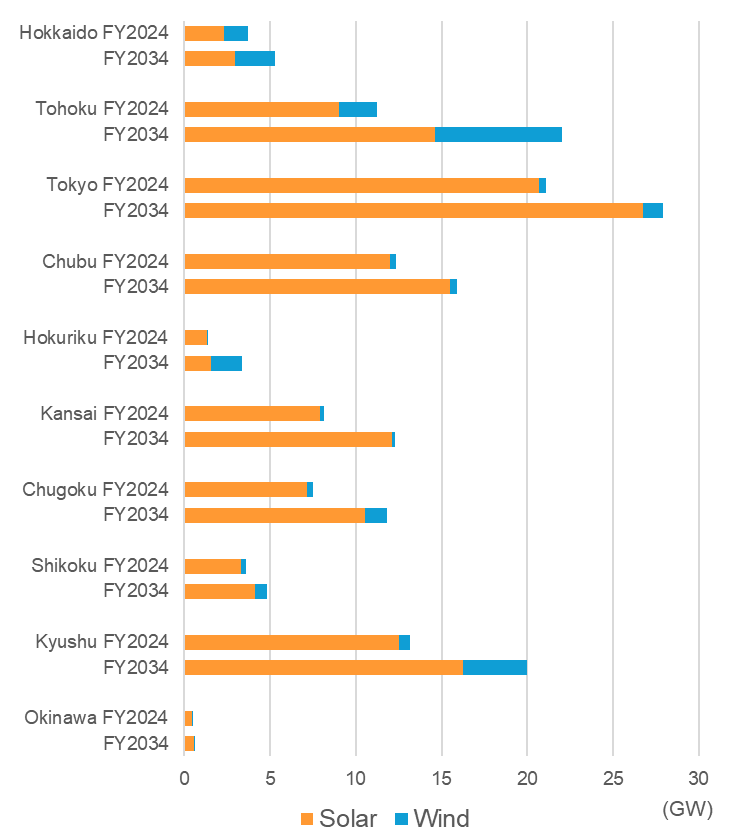

The OCCTO report also provides area-specific forecasts for solar and wind deployment by FY2034. Wind power generation is expected to be introduced in Hokkaido, Tohoku, and Kyushu in the future, and can be utilized to supply renewable electricity for DCs.

Current and Future Solar and Wind Power Installation Capacity by Area

Source: Japan NRG (based on OCCTO “FY2025 Supply Plan”)

Power infrastructure investment

According to the Second Master Plan for Regional Interconnection Systems announced by OCCTO in March 2023, the estimated investment required to strengthen the power system through 2050 varies slightly depending on the scenario, but is estimated to be about ¥6 trillion to a maximum of ¥7.9 trillion.

- Construction of a new undersea DC transmission line connecting Hokkaido, Tohoku and Tokyo: about ¥2.5 trillion to ¥3.4 trillion

- Strengthening the power transmission network between Kyushu and the Chugoku region: about ¥420 billion

- Strengthening of frequency conversion facilities between the eastern and western regions: about ¥400 to ¥430 billion

- Strengthening within each area: Hokkaido about ¥1.1 trillion, Tohoku about ¥650 billion, and Tokyo about ¥640 billion.

These investments will strengthen the power transmission network connecting regions with abundant renewable energy generation (Hokkaido, Tohoku, Kyushu, etc.) and major consumption areas (Tokyo, Osaka, etc). For the transmission network connecting Hokkaido and Tokyo, ¥1.5 to ¥1.8 trillion will be invested in laying undersea cables in the Sea of Japan, with plans to expand capacity to 3.5 times the current level by around FY2030.

These transmission network improvements are expected to facilitate the expansion of renewable energy use while ensuring stable supply. Other benefits include reduced fuel costs resulting from the shift from thermal to renewable power generation.

Energy conservation can help

Energy-saving technologies for DCs are also advancing, such as highly efficient cooling systems, improvements in power usage effectiveness, and effective utilization of waste heat. Also, technology development is being promoted in areas such as all-photonics network (APN) technology, which minimizes processing in DC and communication networks by using light as much as possible, and optoelectronic fusion device technology.

NTT’s IOWN (Innovative Optical & Wireless Network) initiative is an innovative effort to realize a new world and a prosperous society that cannot be achieved with the current network infrastructure.

To mitigate risks associated with data center concentration, the government wants their regional distribution, which involves developing in areas with abundant renewable energy sources, such as Hokkaido and Kyushu. These regions offer advantages like cooler climates, which reduce cooling costs, and the availability of solar, wind, and geothermal energy.

The Watt-Bit Coordination emphasizes the integration of power and communication infrastructure to enhance efficiency. By building data centers near decarbonized power sources and utilizing optical fiber cables for data transmission, the initiative aims to reduce the need for extensive power grid development. This also supports the establishment of off-grid data centers, which can operate independently using local renewable energy sources.

In summary, the Coordination represents a strategic response to the evolving demands of the digital infrastructures. Its key policy implications include:

- Encouraging public and private investment in integrated infrastructure.

- Aligning regulations across sectors to facilitate Watt-Bit planning and development

- Incentivizing the establishment of data centers in regions with renewable energy potential.

Conclusion

This summer, the government has promised to deliver more details and concrete steps for the Watt-Bit Coordination initiative that should act as the blueprint for new energy and digital facility developments.

Such a comprehensive roadmap and plan is unlikely to deliver all the answers for either the energy or telecommunications sectors. Further updates will likely be needed to address also any non-technical challenges, such as local community consent and water management.

Most importantly the process has started. Over the coming decades, data and energy developers should soon have a baseline from which to plan their business growth.

ASIA ENERGY REVIEW

BY JOHN VAROLI

A brief overview of the region’s main energy events from the past week

Australia / BESS

The govt will fast-track ACEnergy’s $350 million battery storage project. The BESS will be able to store up to 770 MWh of energy during times of high generation.

Bhutan / Hydropower

Adani Group and the Druk Green Power Corp (Bhutan) agreed to develop 5 GW of hydropower and pumped storage projects in Bhutan. The deal is backed by both govts.

China / Energy imports

U.S. and Chinese efforts to reduce import tariffs on each other will do little to restore trade in energy commodities in the near future, experts say.

China / Solar panels

U.S. energy officials claim they found ‘unexplained communication equipment’ inside some Chinese-made solar panels that in theory could allow unauthorized external access.

India / Data centers

By 2030, India needs to build 40 to 45 TWh of incremental power capacity to support growing demand for AI infrastructure, according to Deloitte India.

India / Energy storage

Installed storage-backed renewable energy is projected to increase from near zero to 25 GW by 2028, reports Crisil Ratings. It will account for 25% of additional RE over that period.

Indonesia / LNG

Bosowa Energy Group will partner with BK LNG Solution to modernize Indonesia’s energy infrastructure and accelerate the shift toward cleaner energy alternatives such as LNG.

Singapore / Power system

Singapore formed a new unit called Singapore GasCo to centralize procurement and supply of natural gas for the power sector. The Energy Market Authority said that natural gas, which accounts for around 95% of Singapore’s electricity generation, will continue to be vital.

Singapore / Virtual power plants

Singapore is developing new energy technologies, including linking small power sources and managing them to act like a single, larger power plant, to hit its goal of 40% renewable power generation by 2035.

Taiwan / Energy demand

By 2030, electricity needs will rise about 13%, driven by the boom in AI. And chipmaker TSMC alone will consume as much electricity as 25% of the island’s 23 million people.

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Hulic Ochanomizu Bldg. 3F, 2-3-11, Surugadai, Kanda, Chiyoda-ku, Tokyo, Japan, 101-0062.