ANRE made several changes to requirements for the third round of the Long-term Decarbonized Power Sources Auction (LTDA).

Eligible are retrofit projects that convert or adapt thermal power plants to co-fire hydrogen at a rate of at least 10% or ammonia at a rate of at least 20%. Installing CCS at existing coal-fired or gas-fired plants is also eligible for subsidies as long as it removes at least 20% of the total emissions. Projects with biomass mono or co-firing can also bid.

Retrofit subsidy price caps:

Hydrogen co-firing: ¥762,865/kW/year (with a noted lower reference value of ¥312,955)

Ammonia co-firing: ¥378,807/kW/year (with a lower reference value of ¥79,243)

Coal plants installing CCS: ¥343,799/kW/year

LNG/gas plants installing CCS: ¥137,939/kW/year

Biomass: ¥100,000/kW/year

If a project fails to receive approval under the support scheme for low-carbon fuel supply, or if the actual support is lower than the expected amount, such cases will be treated as force majeure and will not be subject to market exit penalties.

For hydrogen and ammonia, the definition of exclusive firing will not be tightened; projects with a co-firing ratio of 90% or more will be allowed to participate as exclusive (i.e. mono) firing projects.

Although around 90% of revenue earned from other markets must be returned, the scope will be expanded to include revenue obtained through the use of equipment included in the bid price, in addition to revenue from power generation and non-fossil value.

On bid price adjustments, automatic corrections will be made to reflect inflation and interest rate fluctuations. However, for large-scale power sources that require long-term construction (period exceeding 10 years) and high-level investment (several hundred billion yen) – whether for new installations or ‘replacements’ – a mechanism will be set up to address the risk of cost increases caused by regulatory or external factors.

CONTEXT: These updates for the LTDA 3rd round aim to promote investment in new power sources by addressing the increase in construction costs caused by inflation, interest rate hikes, and currency depreciation.

TAKEAWAY: METI is positioning the LTDA as another mechanism to support hydrogen and ammonia, along with the price difference support (CfD) scheme. To date, however, the LTDA has not been a big draw for utilities interested in using those fuels. The first round resulted in a small number of successful bids – one project for hydrogen co-firing (55 MW) and five projects for ammonia co-firing (770 MW) that will involve retrofitting existing thermal plants. The second round yielded only one project for ammonia co-firing (95 MW), aso a thermal station retrofit. The next round is raising the caps significantly to encourage more bids. Also, new institutional measures will be introduced to mitigate investment recovery risks for large-scale projects, not limited to hydrogen and ammonia.

METI, MoE, JOGMEC and the National Institute for Environmental Studies (NIES) made a statement calling for collaboration and data transparency to reduce methane emissions across the LNG value chain. The UN Environment Programme’s International Methane Emissions Observatory also joined.

The statement highlights Japan’s ongoing efforts through the CLEAN initiative. MoE and NIES are contributing through the GOSAT satellite program that provides global GHG data, including methane.

The collaboration includes four initiatives: 1) improving transparency through project-level methane emissions data disclosure; 2) supporting publication of the CLEAN Annual Report with data from IMEO; 3) validating methane detection technologies in Asia-Pacific LNG facilities; 4) integrating GOSAT-GW satellite data into IMEO’s Methane Alert and Response System (MARS).

Imabari Shipbuilding will increase its stake in Japan Marine United (JMU) from 30% to 60%, thus making JMU a subsidiary.

The new shares will come from co-investors JFE Holdings and IHI. The goal is to integrate operations to better compete with Chinese and South Korean shipbuilders.

Imabari will hold 60% of voting rights in JMU, while JFE and IHI will see their stakes fall from 35% to 20% each.

CONTEXT: Imabari is Japan’s largest shipbuilder. IMU is the second largest. And Japan is the world’s third-largest shipbuilding nation.

TAKEAWAY: Imabari is a key player in Japan’s energy transition, both as a maker of LNG carriers and future vessels that will be fueled entirely with ammonia. Imabari is also involved in the development of liquified CO2 carriers, which will be used for CCS projects.

OCCTO released a draft report summarizing discussions of the “Study Group on Future Electricity Supply and Demand.”

Its scenarios are based on diversity, verifiability, objectivity, and adaptability: demand/ supply assumptions, stakeholder input, and model scenario setting.

For demand, multiple model cases are set for both 2040 and 2050, with detailed breakdowns by factor and supporting qualitative explanations and indicators.

For supply, model cases are developed for nuclear, renewables, batteries, and decarbonized thermal with CCS, based on technical assumptions and public information, considering plant replacements.

Future load curves consider demand characteristics by factor, demand response (DR), and the effects of on-site solar generation.

Scenarios will be reviewed every 3–5 years based on changes in assumptions, with earlier revisions if needed.

CONTEXT: The study group launched in Nov 2023 to work on a long-term electricity supply and demand scenarios for 2040 and 2050. These are shared among national authorities, relevant institutions, and businesses to support implementation of long-term decarbonized power auctions and planned power development. It differs in purpose from the Basic Energy Plan, supply plans, or interregional grid master plans.

TAKEAWAY: This current scenario includes projections extending to 2050, going beyond the “Outlook for Energy Supply and Demand in FY2040” published as a reference for the 7th Basic Energy Plan. It serves as a reference for measures to achieve carbon neutrality. Detailed simulations were conducted using separate models developed by the Central Research Institute of Electric Power Industry (CRIEPI), the Research Institute of Innovative Technology for the Earth (RITE), and Deloitte Tohmatsu Consulting. The differences in results stem from varying assumptions and model characteristics and are noteworthy.

OCCTO proposed supply-demand measures in response to intra-area grid congestion.

In the event of grid congestion, the constrained supply is deducted from the reserve margin to assess risks and plan countermeasures. If the available grid capacity is small and difficult to address, no deduction is made.

In case of intra-area congestion, additional supply measures are made only in uncongested grids. If the location cannot be identified, action may be taken regardless of congestion status. OCCTO’s power transfer instructions specify transmission areas based on the congestion situation.

Even if the area reserve margin exceeds 3%, OCCTO may issue power transfer instructions as needed if actual conditions worsen due to local constraints.

CONTEXT: In Japan, a non-firm connection is used when connecting a power source to a transmission line with limited capacity. This type of connection assumes output curtailment during grid congestion. Also, a redispatch system has been introduced under which both non-firm and other types of connections are subject to output curtailment according to a merit order. However, as the impact of grid constraints on supply and demand operations has become more apparent during periods of peak demand, discussions have begun regarding how to calculate reserve margins and operate the supply and demand system when constraints arise within regional grids.

ANRE outlined requirements for offshore wind power projects with zero premium to participate in the capacity market.

For publicly solicited projects with bid prices of ¥3/ kWh or less, participation in the capacity market under the FIP is permitted, on condition of forgoing the portion of the FIP grant equivalent to balancing costs.

However, allowing these projects to receive the FIP grant, even if they bid in the capacity market but fail to win a contract, could influence bidding behavior compared to when the grant is not received.

CONTEXT: Offshore wind power is eligible to participate in the capacity market; however, projects under the FIT/ FIP were not allowed to participate in order to prevent double recovery of fixed costs. Since zero-premium projects do not receive FIP subsidies, the February meeting decided that such projects may participate in the capacity market even during the FIP period, on condition that they forgo the portion of the subsidy equivalent to balancing costs.

OCCTO disclosed results of the first round of FY2025 auctions for FIP-certified solar projects with outputs of over 250 kWh.

Notably, 38 of the 57 winning projects, about 36% of total capacity, bid ¥0.00/ kWh, indicating revenue that relies entirely on market-based contracts or sales.

The 38 winning projects with a ¥0/ kWh bid were from Chiiki Denryoku/ HEXA Renewables, GPSS Agri B, Mitsubachi 101, and Bison Energy.

The two largest overall bids were from Mirai Soden Gamo Hino (19.5 MW at ¥5.7/ kWh) and Machi Okoshi Energy (9.99 MW at ¥7.77/ kWh).

TAKEAWAY: More firms appear to opt for ¥0/ kWh contracts to enter and build a market presence, indicating they use the scheme to secure grid access ahead of finalizing PPAs.

Power futures trading in Kansai region surged, with total volume from January to June 20 rising 3.7 times compared to the same period last year, said the EEX.

According to EEX, the trading volume for all Kansai contracts in the first half of this year (specifically, Jan 1 to June 20) reached about 20 TWh, a sharp rise from the 5.4 TWh in the same period in 2024.

This growth is driven by an increase in the number of trading participants and trading volume per company. Major utilities from western Japan, such as Chugoku Electric, have begun trading.

The number of participants trading in Kansai rose to 44 companies by May, up from 27 in May 2024. The number trading over 100 GWh doubled from 6 to 15.

Currently, Japan’s power futures cover two regions: Tokyo and Kansai. Until around 2023, nearly 90% of the trading was in Tokyo area contracts, but from January to June 2025, Kansai’s share of the volume has grown to about 30%.

CONTEXT: Power futures are financial instruments that allow buying and selling of electricity at a fixed price for future delivery, such as in a year. These contracts settle the price difference with spot electricity on the JEPX. Sellers lock in prices, while buyers can hedge against unexpected increases in procurement costs.

TAKEAWAY: Buoyed by improved liquidity in Kansai, EEX plans to introduce daily futures trading in the region, which is now available only in Tokyo. Daily futures are used to hedge short-term price fluctuations, such as those caused by weather-related supply-demand imbalances.

Panasonic Holdings and Kawasaki Heavy Industries will launch a hydrogen project in Romania aimed at helping the country decarbonize energy production.

Panasonic will work on a heat supply project with its hydrogen fuel cells tech, while KHI would supply compressors for Romania’s planned hydrogen pipeline.

Tokyo-based Odyssey and HT Solar, a branch of China’s Haitai Solar, have developed a new line of compact, high-output solar modules.

The modules, Reborn, use bifacial cells and come in two versions: a 320 W model compatible with the old 60-cell size, and a 400 W model for the old 72-cell format.

CONTEXT: Japan’s solar market needs to replace aging modules installed under the 2012 FIT scheme. However, the recent trend towards larger, high capacity modules reveals difficulties with sourcing modules that would fit into older mounting systems and existing inverters. The new panels are expected to help solve this issue.z

J-Power announced a capital increase for its U.S. subsidiaries – J-POWER Charger Capital and J-POWER Charger Partners – with $260 million and $270 million investments, respectively.

This will help launch the Refugio solar project in Texas, a part of the firm’s strategic pivot away from gas-fired energy towards renewables.

GridBeyoned, Ireland’s provider of AI-powered energy services, and its Japanese partner Port have launched Japan’s first front-of-the-meter (FTM) battery power trading system, supported by the Irish government.

GridBeyond and Port seek to expand AI‐driven energy storage solutions across Japan.

Earlier in June, Port energized a 2 MW/ 8 MWh grid-scale battery in Gunma Pref, marking GridBeyond’s inaugural trading asset in Japan. This is the first of several planned battery projects set to come online between 2025 and 2028.

CONTEXT: GridBeyond plans to integrate demand response, cogeneration (CHP), data-center flexibility, and AI-based energy management, tailored to Japan’s market.

UK BESS specialist, Gore Street Capital, acquired a 20 MW / 80 MWh battery energy storage project in Kasama City, marking the first investment from its dedicated Japan fund.

CONTEXT: The company claims that this is Japan’s first fund dedicated to energy storage. It was announced in Sept 2024 as Tokyo Energy Storage Investment Limited Partnership, and is led by Gore Street Capital and trading house Itochu. Other fund investors include Japanese banks and real estate developers, such as Mori Trust and Tokyu Land.

The Kasama City project qualifies for the LTDA capacity market payments, but these government subsidies will complement a predominantly merchant revenue model.

Nagoya-based Kaihan, operator of eateries and renewables businesses, will work with China National Building Material (CNBM) to develop renewables projects in Japan.

The two firms plan to co-develop a total of: 50 MW of solar power, 50 MW of battery storage and 30 MW of wind power.

Kaihan plans to build and sell 150 low-voltage solar installations by March 2026.

Wind projects are also under consideration, but details haven’t been disclosed.

METI proposed upgrading areas off the coast of Matsumae Town and Hiyama District (Hokkaido) to ‘promotion zones’ from the previous designation of ‘promising zones’.

The Matsumae site is expected to support development of 250-320 MW, while the Hiyama site is planned for 910 MW to 1.14 GW of capacity.

The measure is a step forward in developing offshore wind and, if approved, would be the first zones off the Hokkaido coast.

While the announcement does not equate to official selection for Round 4 of the offshore wind auction, it signals that these sites are likely candidates. A decision is expected as early as August.

CONTEXT: Environmental impact assessments are already underway: KEPCO is active in Matsumae, while Hokkaido Electric, J-Power, Copenhagen Infrastructure Partners (CIP), RWE, and Cosmo Eco Power, etc, are involved in Hiyama.

METI updated its list of designated offshore wind development zones and announced a “central approach” for local govts to take a stronger role in streamlining the early stages of project planning. Surveys will be conducted by JOGMEC.

METI designates potential development zones in three categories of descending readiness: promotion zones, promising zones, and preparation zones.

Five new potential areas for floating wind projects were designated as preparation areas off the Tokyo govt-administered island towns of Oshima Town, Nijima Village, Kozushima Village, Miyake Village, and Hachijo Town.

Currently, all designated zones for offshore wind development are as follows:

Category

Zone Names (off the coast of)

(1) Promotion Zones

(Development-ready)

(促進区域)

– Gotō City, Nagasaki Pref (Floating)

– Noshiro, Mitane & Oga, Akita Pref

– Yurihonjō City, Akita Pref

– Chōshi, Chiba Pref

– Happō & Noshiro, Akita Pref

– Oga, Katagami & Akita City, Akita Pref

– Murakami & Tainai, Niigata Pref

– Eshima, Saikai City, Nagasaki Pref

– Aomori Pref (Sea of Japan, South)

– Yuza Town, Yamagata Pref

(2) Promising Zones

(有望区域)

– Ishikari, Hokkaido

– Iwau & Southern Shiribeshi, Hokkaido

– Shimamaki, Hokkaido

– Hiyama, Hokkaido

– Matsumae, Hokkaido

– Aomori Pref (Sea of Japan, North)

– Sakata, Yamagata Pref

– Kujūkuri, Chiba Pref

– Isumi, Chiba Pref

(3) Preparation Zones

(準備区域)

– Iwau & Southern Shiribeshi, Hokkaido (Floating)

– Shimamaki, Hokkaido (Floating)

– Mutsu Bay, Aomori Pref

– Kuji, Iwate Pref (Floating)

– Akita City, Akita Pref

– Ōshima Town, Greater Tokyo (Floating)【New】

– Niijima Village, Greater Tokyo (Floating)【New】

– Kōzushima Village, Greater Tokyo (Floating)【New】

J-Power joined WHEEL, a floating offshore wind power demo led by ESTEYCO, a Spanish engineering firm, off the coast of Gran Canaria, Spain.

Installation begins in Q1 2026: operations to begin in Q2 2026.

The project will use one floating offshore wind turbine that will be built and tested using WHEEL, a floating foundation tech developed by ESTEYCO. It combines the advantages of barge-type and spar-type foundations.

CONTEXT: Barge-type foundations, with a flat-bottom design that maintain stability by maximizing the surface area in contact with the water, can be used in shallow waters. Spar-type ones, cylindrical structures that extend deep below the waterline to lower the center of gravity, maintain stability and reduce sensitivity to wave motion.

The WHEEL foundation, primarily made of concrete, is less costly.

METI and Siemens Gamesa set up a public-private framework to advance supply chain and market development for offshore wind.

Also, Siemens Gamesa and TDK signed an MoU at METI to enhance cooperation on critical magnet supply for wind turbines. The deal is expected to help Japan reduce reliance on China and other countries for critical minerals.

The moves come as METI seeks to boost its offshore energy infrastructure and development, aiming for a 4-8% share, from the current 1% share, by FY2040.

TAKEAWAY: With Japanese firms having exited turbine production, METI is trying to rebuild expertise and competitiveness in wind energy. The deal is expected to help connect wind turbine producers with domestic component makers. Industry players and the govt also hope to attract Siemens Gamesa to set up local production. The deal with Siemens Gamesa follows another MoU agreement with GE Vernova signed earlier in June.

Marubeni increased its stake in Singapore’s Senoko Energy from 30% to 50% after purchasing shares from Kyushu Electric, KEPCO, and the Japan Bank for International Cooperation (JBIC).

The move positions Marubeni as a co-owner with Sembcorp Utilities. Senoko supplies around 20% of Singapore’s electricity with a 2.6 GW capacity.

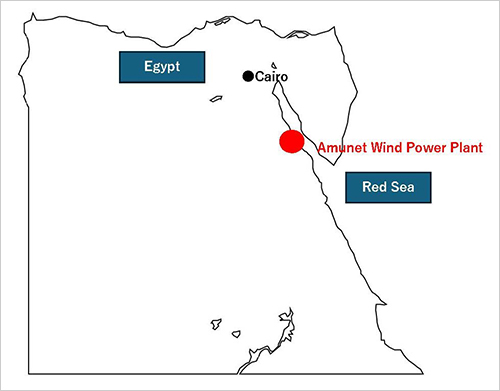

In a JV with Dubai-based AMEA Power, Sumitomo Corp launched the 500 MW Amunet wind farm in Ras Ghareb, Egypt. Sumitomo has a 40% stake.

With 77 turbines, 6.5 MW each, the wind farm is Egypt’s largest. It will provide power for 25 years under a PPA to the country’s public power utility, Egyptian Electricity Transmission Company (EETC).

CONTEXT: Currently, Egypt gets roughly 80% of its power from gas but aims to boost renewables to 42% by 2030, focusing on wind and solar expansion.

The Yamaguchi Eastern Forestry Cooperative completed work on a new Nishiki Biomass Center in Iwakuni City, Yamaguchi Pref.

It will produce about 28,000 tons of biomass fuel chips/ year, with unused forest materials: branches and offcuts.

Starting FY2026, the facility will operate under a 20-year plan, supplying chips to nearby power plants in and outside the prefecture.

CONTEXT: Japan is developing a wide range of biomass power plants, from the 75 MW Sojitz and Nippon Paper project in Hokkaido, to the 112 MW Tahara plant in Aichi Pref, and smaller local initiatives that use forest residues and woodchips to boost renewables and support sustainable forestry.

TAKEAWAY: Nishiki joins a growing network of biomass centers across Japan aimed at transforming unused forest material into renewables. What sets it apart is a focus on electrified, cost-efficient chip production and its strategic role in forest cleanup.

Osaka Gas and JFE Engineering were selected for a NEDO-funded project to build a groundbreaking chemical looping combustion (CLC) system, capable of producing electricity, hydrogen, and CO2 simultaneously from biomass or organic liquid waste.

CLC uses oxygen from metal oxides, rather than air, to combust fuels, enabling high-purity CO2 capture while also generating high-temperature steam for power and hydrogen. The metal oxide is reused in a continuous loop, making the system highly efficient and sustainable.

A 300 kW demo plant will be built at Osaka Gas’s Torishima site by FY2027.

Nomura Real Estate Development Group inked a 20-year PPA with NF Power Services and Higashi-Izu Wind Power, a JV by WPD Group and GPSS.

It will procure 18 GWh annually from a new onshore wind farm in Higashi-Izu, Shizuoka Pref, with operation set to begin in 2026.

TAKEAWAY: The operation is one of an increasing number of 20-year-long PPAs, a fixed contract length that differs from the usually shorter ones abroad.

Nishiyama Masaru, Kyushu Electric’s new president, aims to accelerate decarbonization by shifting the company’s business model.

Instead of relying on long-term operation of power plants for returns, he plans to sell power assets earlier. This is to recycle capital into new projects. Kyushu Electric has set a target of ¥1.5 trillion in decarbonization investments by FY2036.

He emphasized that nuclear energy remains crucial for Kyushu. The region can become a hub for data centers and semiconductor industries due to its stable and low-carbon power supply. But, he said that nuclear projects face long construction periods and uncertain financial returns. This makes state-backed financing essential.

For renewables, Nishiyama advocates early-stage sales of developed projects rather than long-term ownership. He also wants Kyushu Electric to go beyond development and engage in integrated renewable operations. These include selling bundled projects and managing plant operations.

On floating offshore wind, he said Japan must capture first-mover advantages. These systems are essential due to geographical challenges for fixed-bottom installations.

On coal, he supports phasing down rather than full shutdowns; transitional technologies like ammonia co-firing and CCS could maintain stable supply.

Finally, he confirmed that Kyushu Electric signed a long-term LNG supply deal with a U.S. company. Kyushu Electric is shifting away from dependence on Australia, Russia, and Indonesia for the chilled fuel.

TEPCO will set up the Kashiwazaki-Kariwa NPP Operations Council to invite external perspectives into management and safety operations.

The Council will consist of external experts, including community reps and lawyers, and will have authority to give advice to TEPCO HD’s Board of Directors.

TEPCO President Kobayakawa Tomoaki reported the plan to METI Minister Muto in order to enhance the trust-building framework, and added that Council experts will have a permit to inspect the NPP.

TAKEAWAY: The Council will strengthen public trust in the NPP and TEPCO, which still needs local consent for restart. In the meantime, TEPCO completed the fuel load of Unit 6. On June 25, TEPCO finally said that as the time-frame for restarting Unit 7 closes, TEPCO will now prioritize Unit 6.

Tokyo Gas is negotiating long-term LNG supply deals with at least four U.S. exporters based on the Gulf Coast, such as Energy Transfer and Commonwealth.

Tokyo Gas is also deepening upstream U.S. gas investments, acquiring Rockcliff Energy and assets from Chevron, while selling its Eagle Ford stake to Shizuoka Gas.

Chiyoda Corp agreed with Golden Pass LNG Terminal in the U.S. to revise their contract for an LNG plant construction project.

Chiyoda, McDermott and Golden Pass will again negotiate the EPC contract with new pricing and conditions, particularly for the second and third liquefaction trains. The first train’s contract was revised in Nov 2024.

CONTEXT: This revision comes after the bankruptcy of JV partner Zachry Industrial that left Chiyoda with a ¥15.8 billion net loss.

ENEOS Xplora extended its production sharing contract for Malaysia’s SK10 offshore block from 2028 to 2038. The deal is with Malaysia’s oil company, Petronas.

Production began in 2003. This gas goes to a liquefaction plant in Sarawak and then exported as LNG to East Asia, including Japan.

CONTEXT: The volume represents about 4% of Japan’s annual LNG imports.

JGC Holdings received an EPC contract from Interstellar Technologies (IST), a startup specializing in rocket development.

A new rocket launch test and fuel facilities will be built in Taiki Town, Hokkaido.

The facility will produce fuel for IST’s ZERO rocket, set to launch from the LC1 satellite launching port, construction for which is underway in the same town.

CONTEXT: JGC has expertise in building LNG plants, and will leverage this to develop the necessary infrastructure. LNG’s main component is methane. IST is developing a rocket fueled by liquefied biomethane.

As of June 22, the LNG stocks of 10 power utilities were 2.25 Mt, up 5.1% from the previous week (2.14 Mt), up 5.6% from end June 2024 (2.13 Mt), and up 7.1% from the 5-year average of 2.10 Mt.

CONTEXT: No sooner had the rainy season begun, it’s already ending. A few days ago it was declared as over in western Japan – the shortest rainy season on record. It seems power companies decided to ramp up their LNG stocks to be well prepared for the increase in electricity demands for air-conditioner use. The typhoon season is now starting.

METI will select CCS projects starting in the early 2030s. An evaluation system will assess project plans.

CCS support covers the gap between actual CCS project costs and CO2 abatement costs borne by emitters. Support will last until CCS becomes cost-competitive.

Pipeline projects have priority. Shipping-based CCS will come later.

Pipeline transport has high upfront costs and cross-chain risks due to fixed infrastructure. Mitigation requires regional CO2 source aggregation to gain economies of scale and share risks.

Ship transport has higher operational costs (liquefaction, shipping) but offers flexibility. An efficient model could be of centralized CO2 sources and liquefaction facilities. That is, creating a hub-cluster model.

A common ship type and standardized value chain are being pursued to improve efficiency and reduce fleet size.

TAKEAWAY: Support targets capture, transport, and storage based on Benchmark price and Reference price. Benchmark price is capture (CAPEX + OPEX) + auction-based transport/ storage fees. Reference price is annual carbon price. The amount of support will equal Benchmark − Reference.

Toshiba Energy Systems completed a demo of its “C2One™” system, capable of producing 150 tons of carbon monoxide annually from 250 tons of CO2 without using hydrogen or high temperatures, operating under 100°C.

The technology allows for safer, low-cost CO production and supports future applications such as for SAF.

ANALYSIS

BY YURIY HUMBER

In a Volatile Energy Neighborhood, Who You Gonna Call? LNG

A reliable method to gauge industry momentum is to follow the money. Applying this logic to recent remarks from global energy executives points to LNG. Amid significant shifts in energy policy and market sentiment, the LNG sector is emerging as the focal point for investment and planning, reflecting an industry-wide pivot toward pragmatism, security, and affordability.

During recent conferences in Tokyo, executives from energy majors reiterated a commitment to low-carbon fuels and said that decarbonization remains firmly on their agendas. However, their primary emphasis has shifted toward LNG due to its ability to balance decarbonization goals with immediate and realistic energy needs. This aligns perfectly with Japan’s own energy security and affordability concerns.

This pragmatic pivot is underlined by immense financial appetite: LNG projects alone are expected to attract investment of $200 billion in just the next five to seven years, with top Japanese firms eager to benefit from this anticipated “golden age for gas.”

Further fueling this investment surge is a dramatic increase in energy demand driven by the technology sector, particularly data centers powering cloud computing, AI, and quantum computing infrastructure.

Forecasts suggest power consumption from data centers could spike by more than 1,500% over the coming years, propelled by various AI applications and advances in computational capabilities. Energy providers, sensing this massive growth opportunity, are quickly aligning their expansion strategies to supply the burgeoning energy appetite of the technology giants.

Japanese officials emphasize that green energy initiatives remain central to the GX (Green Transformation). Plans in hydrogen, battery technology, renewables, and nuclear power continue to advance. But concerns are mounting among industry leaders and bureaucrats at the Ministry of Economy, Trade and Industry (METI) about the ability of these to satisfy demand growth.

Consequently, the immediate priority is strengthening Japan’s foundational energy infrastructure through investments in LNG, viewed increasingly as indispensable to ensuring stability and economic resilience.

It’s different now

“I wouldn’t say that focus on sustainability has slowed, but there’s a recognition the transition will look different from what people saw 5-10 years ago,” said BP’s SVP Marisa Buchanan at the Japan Energy Summit & Exhibition in Tokyo. She added that with geopolitics at center stage and a new focus on security and affordability, sustainability is no longer the top priority.

LNG veterans, such as Steve Hill from Mercuria, lamented that LNG often serves as a fallback for ambitious clean initiatives that don’t materialise, and yet the sector rarely received due recognition or international policy support. Hill was skeptical about the outlook for renewable energy sources in Asia and urged regional leaders to focus on creating benchmarks for LNG that are separate from those of Europe and the U.S., thus better reflecting local realities.

Shell CEO Wael Sawan was even more forthright. “We have absolute conviction in the future of LNG”, forecasting a 60% growth in demand over the decade. The global LNG market is now at around 400 Mtpa, but will surely expand to 700 Mtpa, Sawan added, citing vast growth in the marine sector where more than 2,000 ships are on order with dual-fuel engine that can run on LNG, as well as China’s annual demand growth for natural gas expanding to double digits.

That sector growth will likely require vast investments. Current liquefaction plants suggest a CAPEX of around $1 billion per 1 Mtpa. Investments in pipelines and upstream natural gas development for greenfield sites can easily double or triple that figure, suggesting the need for hundreds of billions of dollars to meet the sector’s expansion targets.

Traditionally, Japan has been a big part of that investment story – and many of the overseas executives that visited Tokyo last month touted their new projects and available capacity. These are primarily in the U.S., but officials such as TotalEnergies CEO Patrick Pouyanné warned about looking further afield – at Africa, the Middle East, South America, and elsewhere – to avoid swapping one regional energy dependency for another.

Japanese tastes also changing

The approach of Japanese LNG buyers, however, has changed with the years. As the country’s own demand for the fuel wanes, and power market demand becomes more volatile, Japanese imports seek greater flexibility on delivery terms and volumes, and scrutinize the CO2 impact of cargoes more than before.

Sugesawa Nobuhiro, senior managing executive officer at Tokyo Gas, stressed that Japanese firms are no longer immediately interested in buying equity in new LNG projects as a way of securing offtake agreements.

Japanese firms are more attuned to judging the financial impact of these investments and whether they will be seen by their own investors as efficient use of capital with the risks justified. More and more, Japanese buyers will judge new project investment opportunities based on whether they can and wish to market the LNG cargoes to their clients or not.

The challenge of making investments, rather than simply buying the fuel, is magnified by rising LNG project costs. Hara Tadashi, the EVP at Mitsubishi Corp’s Diamond Gas highlighted how higher interest rates and construction expenses make new LNG projects difficult. This is where Japanese investors will look at differentiation.

For example, Hara, whose parent firm invested in the LNG Canada project, praised the Canadian regulatory environment for its stability and also talked up the lower carbon footprint of the country’s facilities due them using hydroelectric power.

Don’t forget about hydrogen

Voices in favor of hydrogen, ammonia and synthetic fuels were more subdued this year at the Japan Energy Summit & Exhibition, and barely audible during the LNG Producers-Consumers Conference staged by METI immediately afterwards. But the sector has not fallen out of favor in the Japanese capital – World Hydrogen Asia will be held in Tokyo on July 8-10.

While progress as an alternative to LNG has slowed due to rising costs and disparity between the prices manufacturers can offer and the costs consumers are willing to endure, energy officials and stakeholders were keen to point out that their future remains on the up.

METI’s top hydrogen planner, Hirota Daisuke, confirmed that interest in its Contract for Differences (CfD) support plan was oversubscribed (more than 30 bids) and the initial round won’t have enough money to satisfy most bidders.Thus, he urged suppliers to seek other sales avenues. Power is one sector bound to drive revenue, with METI keen to offer a better hydrogen subsidy in the next round of the Long-Term Decarbonized Power Source capacity auction.

Meanwhile, Muraki Shigeru, head of Japan’s Clean Fuel Ammonia Association, confirmed that the technologies to support hydrogen use in industry are well on their way to commercialization. The smaller 2 MW turbines that can run on ammonia fuel already function and large 400 MW units will be available in the early 2030s.

A 700 MW diesel engine that can also run on ammonia is due to hit the market by 2026. These developments should lead to industrial furnaces, naphtha crackers and boilers being able to utilize clean-burning ammonia in the next five years or so. Japan’s ammonia demand could hit 30-40 million tons a year by 2040, Muraki said.

Energy – now

Firms like JERA say they’re spreading their bets. Renewable energy and low-carbon fuels like ammonia and hydrogen are central to development strategy, said JERA’s global CEO Kani Yukio. But with uncertainties about the speed of the rollout of cleaner technologies, the utility is keen to ensure that it can deliver energy without interruptions. And, for Kani, that means securing JERA’s position in the gas sector.

Kani revealed that JERA’s LNG inventory in the Tokyo Bay area is enough to meet just 10 days of current demand, making volatility in delivery due to conflict, logistic issues, or the weather a cause of concern. As such, JERA looks favorably at the “concept” of a major LNG project in Alaska that could deliver the chilled molecules to Japan within about seven days.

“New LNG supply after 2030 is limited and this is maybe the last round to secure cost effective LNG contracts as EPC costs are growing,” he said. Meanwhile, Japan’s demand is also in for greater volatility as the differences between peak and low demand seasons are already a factor of two, and that will become a factor of three by 2030.

To ensure JERA can balance volatility on both sides, Kani seeks to connect the AI boom to gas. With two-thirds of data center demand in Japan in Tokyo and the surrounding area, where JERA has the majority of its power plants and other facilities, the company wants to lure developers to build new data centers adjacent to its power plants. That will alleviate grid connection issues and the scramble to secure land sites on the client side, and will offer JERA a big-volume baseload power user to help justify longer-term LNG purchase contracts.

Kani acknowledged that Big Tech’s data center end-users still want to “hear the decarbonization story”. To this, Kani proposed that JERA use LNG’s low temperature to help cool data centers and to mix the electricity supplied to these facilities with those produced by the power company’s offshore wind projects, which are due to start up around 2030.

“These facilities need 24/7 power. That’s what we want to provide,” Kani said.

ANALYSIS

BY MAGDALENA OSUMI and ANDREW SMALL

Chinese Solar Panels – Are Geopolitical and Monopolization Fears Justified?

In recent weeks, Japan has witnessed an intensifying debate over Chinese-made solar power equipment, fueled by growing concerns about its potential to be controlled remotely by malign actors and to interfere with the grid.

Spurred by investigative reports in international media, these revelations prompted the government to initiate a probe into China-made inverters, crucial devices in an electricity system. METI and affiliated organizations are now investigating. Concerns are heightened by the blackout on the Iberian Peninsula earlier this year.

This highlights the technical and security vulnerabilities of Japan’s electrical grid, which faces reassessment amid growing calls for upgrades to tackle issues such as limited interregional connectivity, aging infrastructure, and insufficient capacity to integrate variable renewables like solar and wind.

The allegations concerning Chinese PV and grid technology raise a critical question: Do they reflect genuine security concerns or is China unfairly scrutinized amid broader industrial and geopolitical anxieties over its market dominance?

Abroad-originated concerns

The issue gained traction in Japan after similar concerns were raised in the U.S. and Europe, mainly in response to alarming media reports that sparked debate and legal action. On May 14, Reuters claimed rogue communication equipment was found in Chinese-made solar installations, prompting U.S. officials to investigate.

The devices in question were power inverters, the component of solar panels that converts electricity to feed directly into the energy grid. The discovery raised fears that malign actors could shut off or alter the inverters remotely, which could destabilize, damage, or destroy the energy grid. The article quoted anonymous inside sources and did not provide exact figures on how many panels were inspected.

For much of the past decade, China has held sway over the global solar supply chain, with control over more than 80% of capacity across several key segments including cells, modules and materials. Coupled with many other serious issues, this market dominance has fueled anti-Chinese sentiment and suspicions across the G7.

Since 2010, China’s companies have rapidly conquered the Japanese solar market. Once a global leader with around 50% of global solar module production in the early 2000s, Japan’s domestic output has significantly plummeted to less than 1%, unable to compete against low-cost Chinese units.

Amid rising concerns about Chinese firms active in critical infrastructure in the U.S. and Europe, in March, two U.S. lawmakers submitted the Decoupling from Foreign Adversarial Battery Dependence Act, which would ban the Department of Homeland Security from procuring batteries from six Chinese firms: Contemporary Amperex Technology Company (CATL), BYD Company, Envision Energy, EVE Energy Company, Hithium Energy Storage Technology Company, and Gotion High-tech Company.

In Europe, following the massive blackouts on the Iberian Peninsula in April, concerns grew over the outsized role that Chinese technology plays in energy infrastructure, and solar in particular. While experts estimate that control of just 3-4 GW of Europe’s electricity would be enough to massively disrupt the energy grid, around 200 GW of solar capacity operates with Chinese-made inverters.

Against this sensitive background, the Reuters article that claimed doubts over the integrity of inverters sparked a firestorm of controversy and interest in the role that Chinese technology plays within the broader energy infrastructure.

Japan’s probe into Chinese PV tech

The issue prompted Japan’s government to launch a formal investigation in late May, with the news curiously making headlines outside of Japan first. One article that first ignited debate within Japan appeared in the South China Morning Post. Meanwhile, the claims received little coverage in Japan’s mainstream media, with only pro-government, conservative Sankei Shimbun reporting on the issue.

During a recent House of Councillors session, METI Minister Muto addressed allegations that Chinese-made solar power generation systems may contain suspicious communication devices. He said no such cases have been reported but emphasized ongoing international cooperation and the importance of cybersecurity. He noted that countermeasures against outside interference with the equipment are already required from operators.

Opposition lawmakers still called for a full investigation, given the extensive role that Chinese companies play in Japan’s solar sector – from grid equipment and panel suppliers to investors and developers of solar farms and other green assets. According to lawmakers’ comments, loopholes in foreign investment rules don’t require full transparency on corporate entity ownership, which is a concern because of land and asset resales in the solar sector.

Justice Minister Tanaka acknowledged the potential national security risks and said policy revisions are under consideration.

Role of solar inverters

What are the core concerns behind the probe into Chinese solar technology? Solar inverters serve as the “brains” of solar energy systems, converting the direct current generated by solar panels into alternating current usable by homes, businesses, and the power grid. Without inverters, solar electricity cannot be integrated into existing infrastructure. These devices often include remote access for maintenance and updates, and are used in clean energy technologies, including wind turbines, batteries, heat pumps, and EV chargers.

Following concerns raised in the U.S. and Japan, South Korea also began examining the potential cybersecurity risks of Chinese-made inverters. Notably, up to 95% of inverters available in South Korea are manufactured in China, though they are typically rebranded and sold under the names of Korean companies.

Japan’s role as a global solar inverter producer is minor, overshadowed by China where 75% of the products are manufactured. Japanese companies like Omron, Sharp, Mitsubishi Electric, TMEIC, and Kyocera design and manufacture inverters tailored to Japan’s strict JET certification standards.

While these home brands hold a strong domestic market position due to quality and certification compliance, they face high production costs, making their inverters significantly more expensive – about 35–50% more than Chinese-made equivalents.

Security threat or market fear?

The growing debate over Chinese-made solar panels underscores not only legitimate technical and security concerns but also deeper anxieties about China’s dominance.

While Japan launched a formal probe following international alarm, questions remain whether the scrutiny is driven primarily by genuine risks or by fears within the industry of losing market share to Chinese firms. As Japan’s energy grid undergoes critical reassessment, balancing security with fair market competition will shape the country’s renewables future.

None of the governments investigating the issue have concluded a probe or succeeded in confirming the allegations. But if confirmed, the impact on the market for devices used in the solar industry would be profound.

Complicating the situation further, Japan is not well placed to switch to domestic production should it find that Chinese inverters really are a risk. Buying the devices elsewhere, whether from home brands or allied nations would also inevitably lead to higher costs for solar power and grid modernization – something that Japan can ill afford as it embarks on a wholesale revamp of its electricity transmission infrastructure.

In the meantime, expect officials to keep stressing the need to improve cybersecurity of grid and grid-connected facilities, and look more closely at energy asset ownership.

ASIA ENERGY REVIEW

BY JOHN VAROLI

A brief overview of the region’s main energy events from the past week

Australia / Solar

ACE Power secured approval for a 200 MW solar farm near Narrogin in West Australia. It will also have a 200 MW, 4-hour battery energy storage system (BESS).

Australia / Wind

RWE Renewables secured state approval for its 1 GW Theodore onshore wind project in central Queensland. It will have up to 170 turbines and a battery energy storage system.

China / Battery storage

China Energy Engineering Corp launched one of China’s largest energy storage procurements to date, tendering 25 GWh of lithium iron phosphate (LFP) battery systems.

China / Solar and wind

Between January and May, China added 198 GW of solar and 46 GW of wind, enough to generate as much electricity as Indonesia or Turkey.

Hydropower

Hydropower remains the world’s largest renewable energy source, growing 10% in 2024 to 4,578 TWh in terms of generation, adding 24.6 GW in new capacity.

India / Coal

India’s energy consumption is up 5.8%, coal still dominates, said World Energy Review. The share of coal in primary energy at 57 per cent, followed by oil at 29%.

Indonesia / Geothermal

Indonesia inaugurated a 110-MW geothermal power plant that is backed by a state-owned enterprise as part of the government’s effort to green national energy supply.

Singapore / Renewables

Renewables’s share in the power generation mix rose to a record high in May, to 2.56% of the total, as the city-state ramped up renewables imports and accelerated solar power generation

South Korea / Nuclear

The Nuclear Safety and Security Commission officially confirmed the decommissioning of reactor number one at the Kori plant, which is the country’s last NPP.

South Korea / Hydrogen

South Korea has pledged $600 million to develop a hydrogen-based steelmaking project by 2030 using FINEX technology; the goal is to cut CO2 emissions in the steel sector by 95%.

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

Sumitomo launches Egypt’s largest onshore wind farm

Sumitomo launches Egypt’s largest onshore wind farm