Trump thinks more LNG sales can help bridge the $69 billion trade deficit the U.S. runs with Japan. Also, he’s keen to develop the Arctic region.

Japanese companies, however, aren’t convinced the vast investment in an Alaska LNG project will pay off. There’s also the perennial threat of a change of WH administration.

The most basic issue faced by the nuclear power industry when building a new facility is: Where to site it in a mountainous nation riddled with fault lines?

Beyond engineering concerns, there are a lot of local politics to navigate. This is where the various incentive schemes come in. We review the way that they are set up.

ASIA PACIFIC REVIEW

This column provides a brief overview of the region’s main energy events from the past week

Japan’s ESG bond issuance fell 8% YoY to ¥1.92 trillion in the period covering January–July, marking the second consecutive annual decline.

Companies prefer issuing straight bonds over ESG bonds due to rising interest rate expectations and higher costs. Also this is due to complexity in preparing ESG-related documentation and third-party verification.

CONTEXT: President Trump’s opposition to ESG investing has dampened enthusiasm in Japan. ESG bonds accounted for 19.5% of all Japanese corporate bonds issued, down 1.5 percentage points from last year.

The number of ESG issuances dropped 10% to 81. July saw a particularly steep 25% decline, signaling a likely annual decrease.

Sustainability-linked bonds were down 42% to ¥155 billion. Social bonds were down 12% to ¥874 billion.

Green bonds, however, were up 23% to ¥447 billion.

Some companies, like Fujifilm Holdings, switched to straight bonds after issuing ESG offerings. Yet, analysts stress that long-term demand for ESG bonds remains strong due to ongoing sustainability goals.

The Electricity and Gas Market Surveillance Commission (EGC) proposed revising regulations under the ‘revenue cap system’ to improve financing conditions for TSOs.

Key changes: expanding rate-base eligible assets to include construction-in-progress (now counted at 50%), and revising the treatment of special grid installation grants to be deducted after operation begins rather than at time of payment.

The reforms are targeted for the second regulatory period starting FY2028, and aim to ease financial burdens during long-term grid projects and reduce funding costs.

CONTEXT: This system sets a maximum revenue for power grid operators, ensuring fair consumer prices while promoting efficiency and investment. The grant for grid installation, funded by the renewable energy surcharge, supports transmission upgrades, paid by OCCTO to the TSOs after facilities launch. The grant provides funds during construction for projects certified by METI as vital transmission lines.

TAKEAWAY: Rising power demand from new data centers and semiconductor plants is driving the need for major grid upgrades. Such projects require large, long-term investments by transmission operators, but under the revenue cap system, cost recovery starts only after operation, creating funding challenges during construction. Therefore, easing financing for large-scale grid projects is a key issue in the ongoing electricity system reform.

Japan and India will set up a 10-year framework to strengthen business collaboration and reduce reliance on China in key supply chains, focusing on six strategic sectors including chips, critical minerals, clean energy and advanced tech like AI.

The framework will support end-to-end supply chains, encourage business investment, and provide financial backing through existing public funds.

PM Ishiba and PM Modi are expected to formalize the plan during a Tokyo summit later this month.

Sumitomo seeks to turnaround its nickel project Ambatovy, (Madagascar), which has faced heavy losses since 2012; it’s one of the world’s largest nickel facilities.

A cloud- and AI-based trouble detection system has cut smelter shutdowns over the past five years to one-tenth of previous levels.

The plant’s high-temp, high-pressure acid leaching process was upgraded, raising utilization above 90%.

Sumitomo aims to increase output to 40,000 tons/ year, and reduce costs. In 2022, actual production was 36,000 tons (equivalent to 1-2% of global market share).

CONTEXT: In 2024, the project’s book value was written down to zero, and $3.3 billion in creditor loans forgiven. Nickel prices remain around $7/ pound, half of early-2023 levels, due to higher production in Indonesia and slower EV demand.

TAKWAWAY: Ambatovy is one of the few significant assets in the critical raw materials space fully or largely owned and operated by a Japanese company. Nickel and its byproducts from Ambatovy could supply key materials for Li-ion batteries, hydrogen storage, and renewables tech, essential for EV production, energy storage, and grid stabilization.

Sumitomo Heavy Industries Environment launched the anaerobic digestion system “BIOIMPACT-AC” that converts organic wastewater generated from industrial activities into resources, producing biogas.

The technology fosters high-efficiency capacity and equipment miniaturization.

A demo unit will be installed at Asahi in Ibaraki, with operations to begin in 2026.

CONTEXT: Conventional anaerobic digestion systems face challenges for implementation such as high equipment costs and limitations on installation space.

Despite a continuing heatwave, national power supply has remained stable.

The projected capacity in reserve ratio is forecast to stay above the crucial 3%, with the lowest point so far this summer being 8.8% in certain regions.

The more comprehensive wide-area reserve ratio will likely stay more healthy.

The smallest ratio is seen at 13.4%, indicating no immediate risk of power shortages.

Enechain will develop and offer “eSquare Live for JEPX”, a trading platform with transaction functions for JEPX members, as part of efforts to upgrade trading systems.

The platform is designed to be simple and intuitive. When used together with “eSquare Live,” Enechain’s online wholesale electricity marketplace, it enables one-stop trading of futures products with mid- to long-term physical contracts.

CONTEXT: The new system will operate via dedicated-line server-to-server data communication, and the trading screen will be discontinued. Users will need to either apply for their own dedicated line and develop trading functions in-house or prepare for trading by using services or systems that offer equivalent functionality.

Georgia Power in the U.S. received the first of three advanced natural gas combustion turbines for Plant Yates.

The Mitsubishi Power M501JAC turbines, assembled locally, are part of Georgia Power’s first new natural gas additions in a decade.

They’ll provide 1.3 GW of generation capacity once all units are operational by late 2027. The new turbines can run on oil if natural gas is unavailable, with future potential to utilize hydrogen blends.

CONTEXT: Georgia Power is expanding other facilities, including Plant McIntosh. It requested approval for extra combined cycle units totaling 3.69 GW to meet growing energy demand. Natural gas currently supplies 40% of Georgia Power’s electricity.

Japan Power Procurement Solutions enhanced its electricity cost reduction support for firms using last-resort power supply, offering an expected savings of over 20%.

The goal is to support corporations with electricity contracts and renewable energy procurement. It offers optimal rate plans from partners’ electricity retailers.

CONTEXT: The “last resort supply” is electricity provided by regional utilities to customers without a retail contract. While it ensures stable supply, the rates are higher than normal contracts, making long-term use costly. According to METI, there are still 2,205 such contracts nationwide, totaling about 150 MW.

NEDO selected Toshiba ESS and Toyota Chemical Engineering for a program to promote energy-saving technologies, to develop a 100kW-class binary generator using CO2-absorbed amine solutions instead of high-GWP refrigerants.

This system enables efficient power generation from unused low-temperature waste heat (80–150°C), offering over 10% higher output than conventional systems.

A test will be conducted at TCE’s Handa plant from FY2025 to FY2028.

CONTEXT: In factories and power plants, low-temperature heat is discharged as unused energy. Effective use of this waste heat is vital for a carbon-neutral society, but economic, environmental, and safety challenges limit its utilization in Japan, especially below 150°C. Binary power generation can help by using working fluids with lower boiling points than water, such as ammonia or refrigerants, which are vaporized by hot water or steam to drive turbines and generate electricity.

GRID is partnering with Hokkaido Electric Power Network to develop ReNom Power, a digital system that supports priority power supply operations.

With the rapid growth of solar and wind energy in Hokkaido, managing priority dispatch has become increasingly complex.

The new system will use past operation records and supply-demand forecasts to calculate which power plants need output control, including scale and timing, helping operators make decisions more efficiently.

CONTEXT: GRID is a firm that provides AI solutions to optimize front-line field operations related to electricity, shipping, SCM, and smart cities. Hokkaido Electric Network adjusts power plant output to match fluctuating demand.

The MoE announced the FY2025 winners of grants for feasibility studies and test projects related to building a renewable energy–based hydrogen supply chain model.

This program focuses on scale-up in response to increased demand and efficiency improvements, including in storage and transportation.

Selected study projects are:

Study on building a hydrogen supply chain and creating added value through local industry and tourism in Imabari City, Ehime Pref, led by Japan Environment System, Imabari City, and five other firms;

Study on demand creation and optimization of transportation for deployment of green hydrogen in inland areas, led by FCyFINE PLUS (Fuel Cell Yamanashi Frontier for Innovation and Ecosystem PLUS) with four firms.

Selected test projects:

Test of a low-carbon hydrogen model town in Chita City, Aichi Pref, led by Aichi Pref, Chita City, and 10 firms;

Verification of low-cost centralized / distributed supply chains using byproduct and renewable hydrogen, led by Yamaguchi Pref Industrial Technology Institute, Yamaguchi Pref, and four firms.

From FY2025 to FY2029, Yamaguchi Prefectural Industrial Technology Institute will implement the MoE’s commissioned project of low-cost centralized/ distributed supply chains using byproduct and renewable hydrogen.

The project will transport byproduct hydrogen from caustic soda plants to commercial facilities via hydrogen pipelines for use in chiller systems and deliver produced hydrogen through gas cylinder distribution networks for use in boilers, etc.

Tokuyama will handle the supply and utilization of byproduct hydrogen; Choshu Industries and NF Device Technology will be responsible for hydrogen production, storage, and utilization; and TECHNOVA will conduct various surveys.

Kansai Electric, BIPROGY and Kawasaki Heavy Industries launched a field test on environmental value management in hydrogen co-firing power generation at Himeji No.2 Power Plant.

The goal is to track hydrogen from production to power generation, calculating CO2 emissions and managing environmental value.

It will verify whether power generated from co-firing hydrogen can be identified as coming from low-carbon hydrogen produced in Himeji and Fukui (nuclear-derived) or green hydrogen produced in Yamanashi (renewable-derived).

CONTEXT: Since 2018, using blockchain BIPROGY and Kansai Electric have been researching environmental value trading, including determination of prices. The firms also developed the environmental management platform used in this test.

JERA agreed to join carbon neutrality efforts at Yokkaichi Complex.

The Hekinan Thermal Power Station, near Yokkaichi, aims for fuel conversion from coal to ammonia and might transfer part of the ammonia fuel to Yokkaichi.

MOL and Itochu inked a deal for ammonia bunkering demos in Singapore in order to accelerate adoption of ammonia-fueled vessels and bunkering vessels.

Demos will begin later in 2027 and involve ship-to-ship ammonia bunkering. They’ll use Itochu’s 5,000 m³ ammonia bunkering vessel alongside MOL’s upcoming ammonia dual-fuel Capesize bulkers.

Mitsubishi Logistics will invest over ¥40 billion by 2030 to enter the grid-scale battery storage business, aiming to develop seven sites nationwide with a cumulative capacity of some 700 MWh.

The first two facilities, in Kanagawa and Saitama Prefs, will launch in FY2027.

The firm will use its warehouse sites, well-suited for transporting and installing large batteries, to trade electricity in wholesale and balancing markets. From this business alone the goal is to reach ¥10 billion in annual revenue by 2030.

CONTEXT: Mitsubishi Logistics is active in logistics and real estate, especially warehouse management, and develops many datacenter-compatible buildings such as Tokyo Dia Building. The firm is a pioneer and holds the largest domestic market share in buildings for rent with emergency generators.

TAKEAWAY: As with solar, the BESS market is attracting companies outside of the energy sector because they may have a strategic advance. In the case of Mitsubishi Logistics, it’s the availability of land at its warehouses that are already connected to the grid and therefore relatively easier and faster to develop. It will be interesting to see whether Mitsubishi Logistics and others in a similar position choose to operate the BESS themselves or outsource this to sector specialists.

OCCTO awarded 114 MW (AC) of capacity to 47 FIP-certified solar projects with outputs over 250 kWh in the latest, 25th round of auctions.

A total of 60 bids for a cumulative capacity of 202 MW were submitted, showing a second straight case of oversubscription. Only 115 MW was on offer via the auction.

KASolar won the most projects, seven in total. The highest bid was ¥7.89/ kWh while the average bid price rose to ¥5.38/ kWh from ¥4.06/ kWh.

The two largest winning projects were awarded to Sonnenblume No. 4, a firm affiliated with Shizen Energy, (20 MW) and Sirius Solar Japan 55, affiliated with Trina Solar (20 MW).

Eight winning bids at ¥0/ kWh included projects by Hexa Renewables, Univergy, Shizen Energy and Greenvolt Solar Japan.

CONTEXT: Companies awarded a win must submit a deposit within two weeks and secure FIP certification by March 23, 2026, to finalize contracts. Since the bids surpassed this round’s target, OCCTO will raise the procurement target to ~162 MW for the year’s third solar auction. It will start accepting business plans on Sept 24.

TAKEAWAY: The results indicate that bidding at ¥0/ kWh has become increasingly standard, reflecting a recent trend in which companies leverage the scheme to secure grid access while using PPAs to generate revenue. Still, the number of companies bidding ¥0 was much lower compared to the previous round (announced June 20). This was the second straight case of oversubscription, following a period of undersubscription.

TEPCO PG will begin a demo to supply 100% renewable energy to Ogasawara Village, including Haha-jima Island.

The goal is to provide renewables-only electricity for roughly six months, using innovative tech over a three-year trial.

TEPCO PG installed solar panels (1.5 MW each) and batteries (four units, 600 kW each, total 7.81 MWh).

These are operated and controlled with a newly developed Energy Management System that charges the batteries with excess solar power during the day and discharges them at night. If batteries run low, diesel generators provide backup.

TAKEAWAY: Since around 2020, the Tokyo Metro Govt has cooperated with TEPCO PG in transitioning from diesel power, aiming to reduce diesel emissions and for the remote island chain to be powered exclusively through solar power. Challenges remain, such as infrastructure limits, environmental protection, high costs and a lack of skilled personnel capable of installing and maintaining advanced energy systems. Given that small grids are vulnerable to fluctuations, and batteries can’t always cover low-sunlight periods, backup diesel is required. A hybrid approach using solar, storage, smart management, and selective diesel seems to be a more practical path toward low-emission power.

Panasonic and ENEOS Power will hold an energy management demo in TEPCO Power Grid’s service area, using batteries, heat pump water heaters, and other devices.

They’ll target 100 households and 20 businesses with ENEOS solar power contracts, installing Panasonic batteries and HEMS/BEMS (home and building energy management systems) that can be operated via remote control.

The system will remotely manage batteries, heat pumps, and air conditioning, using algorithms to maximize self-consumption of solar power and reduce energy costs.

Real estate developer Hulic seeks to acquire 20% of Canadian Solar Infrastructure Fund, raising its tender offer price from ¥86,710 to ¥89,930 per unit, a 19.3% premium to the pre-announcement closing price.

Hulic seeks to expand its renewables portfolio, including solar and battery storage projects, as part of its RE100 and decarbonization strategy.

CSIF has invested ¥102 billion in 34 solar farms, with a total capacity of 246 MW.

Osaka Gas aims to operate 1 GW of BESS capacity by FY2030 by establishing a nationwide network of battery facilities.

Osaka Gas launched its first local BESS facility in Suita City (capacity of 1.1 MW/ 2.3 MWh), to participate in the wholesale, balancing, and capacity markets.

Osaka Gas plans to add new facilities in Hokkaido and Saga Prefs.

PowerX launched a power aggregation service for solar power plants equipped with storage batteries. The service optimizes both power generation and battery charge/discharge operations.

The first project is with Senko (part of Senko Denki) that specializes in wholesaling electric equipment and operates a solar power plant in Osaki, Kagoshima Pref.

The firm plans to install its proprietary Mega Power 2700A storage system with a 2.74 MWh capacity. Operations will begin Feb 2026, shifting from FIT to FIP.

TAKEAWAY: The initiative addresses Japan’s growing issue of power output curtailment, where solar generation exceeds daytime demand, especially in Kyushu. The system is expected to help improve profitability under the FIP system.

Sumitomo Heavy Industries developed tech for forming the electron transport layer in perovskite solar cells, offering high reactivity and low substrate damage, enabling formation of high-quality crystalline films.

The firm’s Reactive Plasma Deposition (RPD) helps form tin oxide (SnO₂) films suitable for use as electron transport layers in PSCs.

Mitsubishi Corp’s offshore wind power project in three areas – two in Akita Pref and one in Chiba – suffered a setback after construction firm Kajima withdrew as a core contractor due to surging construction costs.

Mitsubishi and partner Chubu Electric won the 2021 public tender, planning completion in 2029. Chubu Electric’s Chudenko was tapped for onshore works, while Kajima was to team up with Dutch offshore infrastructure solutions provider Van Oord for offshore works.

Kajima’s exit stems from material and labor cost hikes. Turbine costs rose around 1.5 to 1.8 times between 2020–2024.

Mitsubishi has already posted a ¥52.4 billion loss from offshore wind, prompting a full business reassessment. Their bid relied on Japan’s FIT scheme with very low fixed power prices (¥11–16/ kWh), leaving very little room to absorb cost inflation.

CONTEXT: Since Japan lacks specialized offshore construction vessels, rival firms like Shimizu and Penta-Ocean are already tied up with other projects, which poses additional challenges for the Mitsubishi-led consortium.

TAKEAWAY: Mitsubishi’s offshore wind projects, originally planned with GE Vernova as turbine supplier, remain in limbo as the contracts were never finalized, leaving procurement unsecured. Kajima’s withdrawal adds further uncertainty. METI is now revising auction rules to allow sales linked to market prices, a shift that could ease financial strain and even enable Kajima’s return, which would effectively rescue Mitsubishi’s projects. But such support risks a backlash from competitors who lost earlier tenders. Since these projects were Japan’s first large-scale offshore wind bids, the govt will likely continue backing them as a pillar of its energy transition, especially given the risk of a domino effect: delays in Round 1 projects disrupt logistics, port use, and the wider supply chain, threatening subsequent offshore wind developments. Still, the support needs to come through soon to revive the sector.

Osaka Gas’s subsidiary Daigas G&P Solution canceled a wind power project in Atsuma Town and Tomakomai City, Hokkaido, due to rising costs.

The project, initially planned for 10 turbines (later reduced to 5) with total capacity over 20 MW, was scheduled to start in 2028.

CONTEXT: Although the firm was progressing with an environmental assessment, it submitted notices the same day to METI, as well as the mayors of Atsuma and Tomakomai, informing them of the project’s cancellation. In April, the project had been scaled down in response to environmental concerns.

TAKEAWAY: Cancellation highlights the mounting challenges facing the wind sector, where rising costs are putting heavy pressure on upcoming projects. Industry players increasingly call on METI for stronger support to keep planned developments on track.

Kitakyushu City began planning for a base to produce and assemble floating offshore wind power components, mainly in the Hibikinada West area.

The site covers 72 hectares of land and 50–100 hectares of surrounding water. It will host manufacturing of semi-submersible floaters and mooring lines, plus assembly and storage yards.

This onshore hub will support construction, operation, and maintenance of floating offshore wind across Japan and East Asia.

CONTEXT: The initiative builds on Kitakyushu’s Green Energy Port Hibiki project, which already hosts a fixed-bottom offshore wind assembly base, including Japan’s largest fixed-bottom offshore wind farm, with a capacity of 220 MW, set to start operation by late FY2025.

ENEOS Renewable Energy has partnered with Shoreline Wind, a Norwegian provider of SaaS solutions for the wind energy industry, to accelerate construction of offshore wind projects in Japan.

Shoreline has an AI-powered platform to manage the full lifecycle of wind farms.

ERE will deploy Shoreline’s platform across its current offshore projects to tackle complex logistics, unpredictable weather, and tight supply chains.

A startup has launched in Ube City to commercialize Yamaguchi University’s tech that generates electricity from the salinity difference between seawater and freshwater.

The new firm, Blue Water Energy, plans to build a manufacturing plant, and begin selling equipment in 2029.

The firm uses a tech called reverse electrodialysis power generation that produces stable, 24-hour renewable energy simply by mixing seawater and freshwater.

The process converts ion movement through ion-exchange membranes into electricity, with 1 cubic meter of seawater and freshwater generating about 500 Wh.

The system requires less land than other renewables — about 1/50th the area of solar and 1/200th that of wind for the same output. It can be installed anywhere seawater and freshwater are available.

CONTEXT: Separately, Fukuoka City has also begun operating a different type of salinity-gradient power plant, which uses osmotic pressure to drive turbines.

In Sept, JAPC will launch new geological surveys at Tsuruga NPP Unit 2.

The firm seeks to reapply for safety approval after regulators rejected the plant in Nov 2024. The NRA ruled that the company failed to prove the K fault beneath the site was neither active nor continuous.

The new two-year survey will include deep drilling at the D-1 trench and excavation around the reactor building. The firm needs to prove that the fault is both ancient and discontinuous. A new technical team will oversee the work.

CONTEXT: Debates over Tsuruga’s faults have continued since 2012, making this one of Japan’s most contentious nuclear safety cases.

Saga Pref and Karatsu city will decline state subsidies for the ongoing literature survey in Genkai Town for the selection of a final disposal site for high-level radioactive waste from NPPs.

A prefectural official said there is no desire to have a nuclear waste repository.

In March, the govt informed Genkai Town it would receive an initial ¥1 billion subsidy for FY2025, and asked the town to discuss allocation with municipalities.

In July, Genkai proposed ¥250 million each to Saga Pref and Karatsu City, but both declined. Thus, Genkai Town plans to apply to receive the entire ¥1 billion.

Similar cases occurred in Hokkaido where Suttsu Town and Kamoenai Village conducted literature surveys and received subsidies, but the prefecture refused its share based on local ordinances opposing acceptance of nuclear waste.

CONTEXT: Genkai Town hosts Genkai NPP. It began the literature survey in June 2024, expected to last about two years. Under the subsidy scheme, up to ¥2 billion is available over two years. More than half will go to the municipality conducting the survey. The rest should go to neighboring local govts and the prefecture.

TAKEAWAY: The lack of leadership at the national govt level on this issue is a concern. For all the willingness of individual towns to host a nuclear waste storage facility, the ability of regional authorities to block it makes the years and the taxpayer money spent on the surveys likely a waste. Bureaucrats in Japan prefer a softly-softly approach to sensitive issues. However, should the storage site remain an open question into the 2030s, public appetite for new reactor construction will suffer.

Tohoku Electric said completion of safety upgrades at its Higashidori NPP Unit 1 in Aomori will continue until March 2027. The previous deadline was September.

The utility said extra tsunami countermeasures, such as raising site elevation, need a further 1.5 years to plan.

CONTEXT: Unit 1 has been offline since February 2011, originally for regular inspections but remained shut following the March 2011 earthquake. In 2014, Tohoku Electric applied for a NRA safety review, which is still ongoing. The NPP’s safety work has faced repeated delays due to additional construction plans.

TEPCO will begin work inside Fukushima Daiichi NPP for radioactive sandbag removal. Remote-controlled robots will move the debris over the course of about a month.

More than 40 tons of high-radiation sandbags remain inside. TEPCO started the removal but halted it after discovering scattered debris.

TEPCO initially aimed to complete the recovery by FY2027 but will now “reassess the schedule.”

CONTEXT: The sandbags contain zeolite and activated carbon to absorb radioactive materials.

TAKEAWAY: TEPCO continues decommissioning. Dismantling empty water tanks moves forward, with the 12th tank set for removal by the end of August. Around 1,000 tanks remain on-site as treated water release will continue through 2051. Monitoring shows tritium levels remain within safety limits, but the lack of practical separation technologies underscores the need for innovation.

Mozambique President Filipe Nyusi said a local LNG project, in which Mitsui & Co is an investor, will begin production in 2029.

The project, developed by France’s TotalEnergies and Mitsui, stalled in 2021 due to security threats from an Islamist insurgency in north Mozambique.

President Nyusi said development could restart as early as August or September. Production could start around 2029-2030 (delayed from an initial plan of 2024).

CONTEXT: The project has a planned production capacity equal to 20% of Japan’s annual LNG consumption. Japanese state agencies are providing financial support, and companies like JERA and Tokyo Gas will likely buy the LNG.

TAKEAWAY: This project was one of the biggest LNG investments by Japanese players outside of the U.S. The uncertainty of its construction amid a tough political and safety environment underscores the difficulties of opening up new markets for Japan’s LNG buyers.

As of Aug 20, the LNG stocks of 10 power utilities were 2.01 Mt, up 2.6% from the previous week (1.96 Mt), up 18.2% from end Aug 2024 (1.7 Mt), and down 1.5% from the 5-year average of 2.04 Mt.

CONTEXT: Daytime temperatures in Japan hover around 35 °C, and soon it will be typhoon season.

Sumitomo Chemical and JFE Engineering will test CO2 recovery using membrane separation technology. It will be Japan’s first at a waste incineration facility.

The trial, commissioned by NEDO, will start in March 2026, at Kawasaki City’s Ukishima Processing Center.

The goal is to to develop a compact, low-cost CO2 capture system suitable for medium- and small-scale emission sources.

Sumitomo Chemical will provide the CO2 separation membranes and basic process design that enable CO2 recovery from flue gas containing less than 10% CO2. JFE Engineering will manage system integration and on-site operations.

CONTEXT: Since May 2022, Sumitomo Chemical has been working with Japanese startup OOYOO to develop CO2 separation membranes, and has since then produced full-scale membrane modules. JFE Engineering joined the project in April 2025.

METI will survey power generation companies utilizing thermal facilities, to assess the state of electricity generation and CO2 emissions.

The goal is to set up methods for proposing power generation benchmarks based on emissions. METI will focus on electricity generation and FY2022-24 emissions.

The results will inform discussions in the Emissions Trading Subcommittee.

Toyo Engineering said its feasibility study on sustainable aviation fuel (SAF) production technologies was approved by NEDO.

The study will assess the technical and economic potential of two methods – gasification FT synthesis and methanol-based SAF production – using diverse feedstocks such as municipal waste.

It will also examine co-production of synthetic fuels like gasoline and diesel, review supply potential and cost competitiveness, etc.

CONTEXT: Toyo Engineering previously made pilots of SAF production through gasification and FT synthesis, as well as studies on building the SAF supply chain.

ANALYSIS

BY FILIPPO PEDRETTI

On Thin Ice: Energy Companies Remain Cautious over Trump’s Alaska LNG

Over the past six months, among the G7 countries, LNG has turned from an undesirable though grudgingly accepted fossil fuel to a crucial bargaining chip in trade negotiations with President Trump, who demands that Japan and other allies buy more of the super-chilled fuel.

With his unabashed fondness for fossil fuels, much unlike Biden’s administration, Trump thinks more LNG sales can help bridge the $69 billion trade deficit that the U.S. runs with Japan. Toward that goal, in June, companies such as JERA and Kyushu Electric saw the writing on the wall and were eager to announce long-term LNG deals with the U.S.

In addition to appeasing Trump, buying LNG from the U.S. brings other advantages, such as no resale restrictions to third parties. And such sales help Japan ease its dependence on LNG imports from Australia (40% of total imports), as well as Russia (10%), trade with which has been complicated due to sanctions.

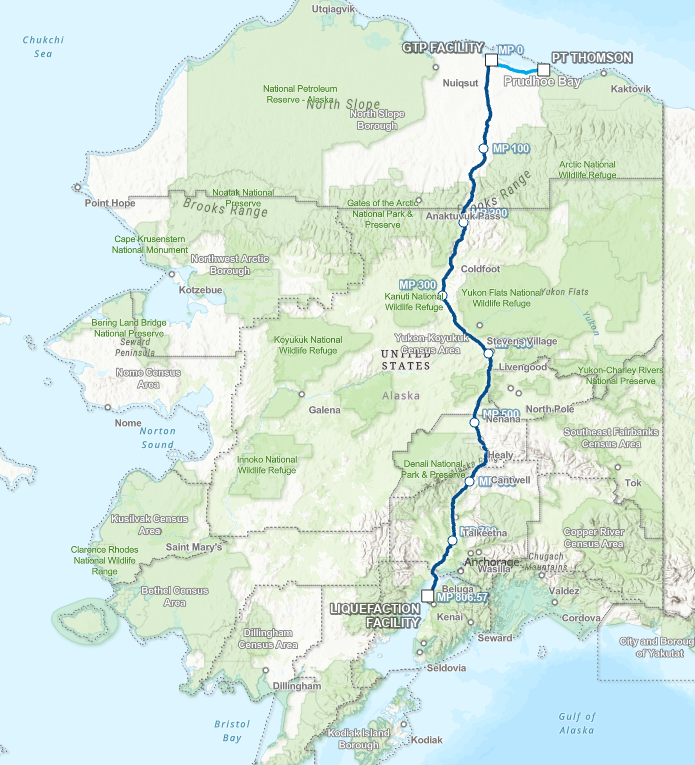

Beyond boosting the U.S. LNG sales in general, Trump is keen to develop the country’s Arctic region, which he says is a new frontier to help cement America’s return to ‘greatness’. Key to these plans is the long-stalled Alaska LNG project, which calls for exporting natural gas from Alaska to Asia.

That project’s price tag is a hefty $44 billion, partly because it will require building a lengthy pipeline to carry the gas from northern Alaska to a port in the south, where it would be liquified and put on a vessel to Asia. Foreign support is seen as crucial for the project to go ahead both for offtake and financing reasons. Japan, already the top direct foreign investor in the U.S., is encouraged by the White House to play a leading role on the Alaska project.

Japanese companies, however, remain cautious – not convinced the vast required investment will pay off or that the project will meet the touted deadlines. There’s also the perennial threat of a change of administration – and with it, a change of stance on this project and the broader U.S. LNG export narrative.

The project

Alaska LNG’s proposed capacity is 20 Mtpa, which is equivalent to about 30% of Japan’s current annual LNG consumption. U.S. Glenfarne owns 75% of the project, and the Alaska Gasoline Development Corp (AGDC) holds the remaining 25% share.

The project entails transportation of natural gas from the north Arctic coast, southward via a 1,300 km pipeline to a liquefaction plant not far from Anchorage, where the gas will be processed and then shipped. If all goes as planned, gas could start flowing by late 2028, with the first exports to Asia starting in the early 2030’s.

Glenfarne and AGDC have the role of developing the infrastructure. It consists of the pipeline, the gas treatment plant on the North Slope, and the liquefaction/export facility. The gas should come from two long-established fields on the North Slope, called Prudhoe Bay and Point Thomson. They should supply around 3.5 billion cubic feet of gas per day. Both fields are already in production. Their operators include ExxonMobil, ConocoPhillips, BP, and Hilcorp, among others.

To spread out the investment burden, the U.S. is urging Asian allies – Japan, South Korea, and Taiwan – to join the liquefaction project, tying their potential participation to ongoing tariff negotiations. In March, Alaska governor Mike Dunleavy visited those countries, as well as Thailand, together with delegations from AGDC and Glenfarne Group.

Project location. Source: Alaska LNG

In June, Officials from Japan, South Korea, and Taiwan attended a U.S. government briefing in Alaska that was led by U.S. Energy Secretary Chris Wright, Interior Secretary Doug Burgum, and Governor Dunleavy.

Of that group, Taiwan has emerged as the most eager, with state-run CPC Corp inking a non-binding deal in March for a possible purchase of 6 Mtpa of LNG. Overall, Taiwan plans to increase its total share of U.S. LNG from 10% to 20–30% of national imports. LNG is replacing nuclear power in Taiwan, which shut down its last operating reactor in May.

South Korea, however, is cautious. In theory, Korea Gas Corp (KOGAS) should take the lead, but the company is struggling with high debt and would have to pass the new project costs onto consumers. A Korean think tank warned in April that Alaskan LNG is more expensive than Russian gas.

South Korea prefers a multilateral approach, acting in concert with Japan, Taiwan, and Vietnam to reduce risks. Meanwhile, the U.S., including Alaska’s governor, is pressuring Korea to commit, with the carrot of tariff concessions. Finally, Thailand’s PTT announced a non-binding agreement in June to buy 2 Mtpa of LNG from the Alaska project for 20 years.

Japan’s stance

Japan remains noncommittal. While it sees Alaska LNG as a potential bargaining chip in talks, it’s also concerned about economic feasibility. Doubts over viability came from research institutes such as the METI-allied IEEJ. Others worry about the project’s future after Trump and whether it will be built and begin deliveries as promised.

A delay of several years could have major implications down the line if Japanese buyers suddenly need to find large volumes of LNG at short notice. It could cause a spike in spot market rates.

Potential Japanese investors in Alaska include the usual suspects: Inpex, Mitsubishi, Mitsui, JERA, JOGMEC, and the Japan Bank of International Cooperation. Mitsubishi President Nakanishi Katsuya has already remarked on the project’s complexity, citing the very long 1,300 km pipeline and an uncertain demand in Southeast Asia, to where most of the Alaskan volumes would probably go because demand in Japan is currently on a long-term downward trajectory.

On July 22, Trump announced plans for a joint venture with Japan to develop Alaska LNG, but there were no statements supporting this claim from Japanese businesses. In fact, trading firms like Itochu and Mitsubishi contradicted Trump, saying they’re either not involved or still only gathering information about the project.

JERA, Japan’s largest LNG buyer, showed interest but stated its desire for cost clarity. Chiyoda Corp expressed interest in conducting feasibility studies, but INPEX questioned the project’s profitability altogether, citing the long pipeline route and the scale of the liquefaction facilities.

Despite such tepid public responses, Alaska LNG operator Glenfarne says it secured buyers for half of the planned 20 Mtpa output, without providing details. If Glenfarne is counting the volumes from the non-binding deals with Taiwan and Thailand entities, then the numbers may work. But non-binding commitments do not typically win bank financing. And so, the Alaska side and Trump’s White House are desperate to secure some form of financing or offtake guarantees from Japan, hoping they will have a snowball effect on other Asian allies.

Trump card: distance

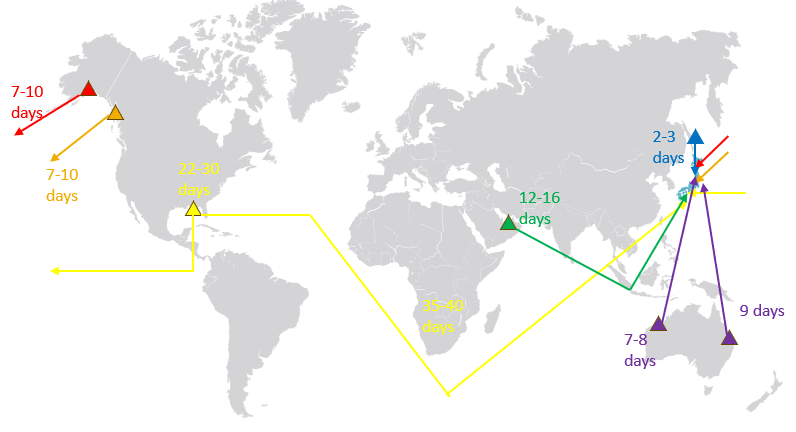

Despite all the obstacles, Alaska LNG holds one trump card – especially over the hitherto more favored U.S. projects in the Gulf Coast. It’s estimated to take about 7-10 days to deliver an LNG cargo by ship from Alaska to Japan. It takes at least double, and sometimes triple the time from the Gulf Coast due to the congested Panama Canal. Avoiding the Canal and taking the cargo south via the Cape of Good Hope is even lengthier.

For a country like Japan, which doesn’t have the resources to store LNG for more than a few weeks, the shorter route is an attractive proposition.

Origin

To Japan

Western Australia

7-8

Queensland (Gladstone)

9

Sakhalin

2–3

Alaska

7-10

Canada (West Coast)

10

China (Shanghai)

8

South Korea (Incheon)

7

India (Gujarat)

9

Qatar

12

Middle East (M.E.)

12–16

US Gulf Coast (via Panama)

22-30

US Gulf Coast (via Cape of Good Hope)

35–40

Nigeria

22

Malaysia

3-5

The problem for Alaska’s backers is that Canada has just started delivering LNG from a brand new project – with Japanese investment – about 1,000 km further south. The LNG Canada facility, operated by Shell, is 15% equity backed by Mitsubishi Corp and 5% by Korea Gas Corp. The initial phase offers 14 Mtpa and Mitsubishi has already signaled an interest in expanding the plant.

Which brings us back to cost. Can the Alaska natural gas, which will feed into the LNG project, offer a competitive advance to other North American projects? Since the gas fields in the north of Alaska are already operational, sourcing the gas could be competitive. But taking the gas by pipeline over mountains and raging rivers will not be easy. Which is why prior attempts to draw Alaskan gas field owners such as Exxon, BP and ConocoPhillips into the grander LNG export project have failed.

The 2016 iteration of the Alaska LNG project – which had been considered by various parties for already several decades – involved Exxon, BP, ConocoPhillips, and state-owned Alaska Gasline Development Corp (AGDC) making initial cost estimates, only to find that the numbers would not work based on low oil prices and due to the huge CAPEX. A Wood MacKenzie analysis at the time said the Alaska LNG project ranked poorly in terms of competitiveness globally.

Since 2016, LNG is back in vogue and oil prices are up from mid $40s per barrel to low $60s. But is that enough?

Estimates of LNG shipping time

To bring investors to the table, Glenfarne plans to de-risk part of the project by working on the pipeline first before moving onto the LNG plant phase. Alaska officials estimate that the state will soon need more gas on its southern coast and without a pipeline they would need to import the fuel. Once the pipeline is completed, the thinking is that investors from Japan and South Korea could upgrade their commitments into binding ones.

The pipeline cost is estimated at $11 billion (a quarter of the total LNG project budget). Amid inflation concerns, Glenfarne CEO Adam Prestidge says efforts are made to control costs.

Glenfarne wants to start pipeline operations in 2028, about three years before the liquefaction plant would be operational. The piped gas would arrive in the city of Anchorage, which faces gas shortages. Prestidge claims the pipeline will bring in local revenues even before the LNG plant completion.

As the work begins, potentially as soon as from the end of this calendar year, Prestidge is also looking to investors beyond Asia. He has claimed that the UAE and other countries have indicated interest in this project.

Conclusion

Unlike Trump with his bully pulpit, Prime Minister Ishiba cannot compel Japanese firms to join a massive energy venture abroad, especially when the commercial upside remains uncertain. Corporate decisions will hinge on economics, not politics: feasibility studies will be the prime factors for Japanese companies. Unless… the Japanese government decides to extend financial support or guarantees to domestic firms.

Among previous examples is Russia’s Arctic LNG 2 project. Trading house Mitsui made the final investment decision to buy equity in this development in September 2019, five years after Russia took control of the Crimea peninsula and incited international sanctions. With the Japanese firms reluctant to wade into hot legal waters, the Mitsui deal was made in concert with state-backed company JOGMEC Corp. The latter took the bigger stake and offered guarantees to Japanese banks who lent money to the project – money that JOGMEC had to repay in early 2024 after the U.S. government sanctioned the project.

Whether PM Ishiba can offer similar conditions for an Alaska LNG investment is a big question. The premier’s political support is shaky and influence waning, meanwhile the national debt of Japan is at record levels. There’s also the issue of uncertainties that lie beyond a Trump presidency to consider.

Optimists still see a path to a final investment decision. LNG demand in Asia is on the up. For now, the pressure from environmental groups, many of which contest the need for more LNG use, is lower than it has been in recent years. And a project that ties the interests of Japan, South Korea and Taiwan to those of the U.S. would be expedient from a geopolitical perspective. But, someone has to pick the bill for all this. Who will that be?

ANALYSIS

BY ANDREW SMALL

The Politics and System of Incentives to Smooth the Siting of Nuclear Power Plants

Perhaps the most fundamental issue faced by Japan’s nuclear power industry when seeking to build a new facility is a very straightforward one – Where to site it in a nation that’s almost 70% mountainous and riddled with geological fault lines?

From the point of view of science and engineering, the issue comes down to whether or not a potential site will guarantee the power plant’s safe operation under even the most extreme circumstances. From a political point of view, however, choosing a site becomes enormously challenging to manage due to the need for approval from local governments and powerful agricultural cooperatives.

Japan’s limited land space makes land acquisition for any major infrastructure project a considerable political challenge, involving many stakeholders. Given its complex post-war history and engineering challenges, nuclear power faces an even greater set of challenges, with opposition both at a local and national level that the Fukushima disaster only exacerbated.

These sensitivities have led Japan to avoid using the more controversial tactics often deployed for large infrastructure projects to force the sale of land, such as eminent domain. Instead of coercive measures, when it comes to nuclear power, the state has developed sophisticated compensation mechanisms based on strong financial incentives for towns that host nuclear power plants. How do these processes work and how much money is at stake?

Building local consent with a ‘carrot’

The most important tool by which the government, in conjunction with Japan’s major EPCOs, responded to siting challenges is a financial mechanism called dengen sanpou (電源三法・Three Power Source Development Laws). The system allocates an ‘invisible tax’ – a portion of consumer energy bills – to fund hefty subsidies to small, rural towns with low tax bases that host NPPs. These subsidies are used to fund substantial local infrastructure and public facilities.

While also applicable to hydropower and geothermal host communities, dengen sanpou subsidies play an outsized role in nuclear power development given the huge amounts on offer and the political sensitivity of nuclear power itself.

Although on a smaller scale than the main host community, municipal governments within a specified range surrounding the NPP are also eligible for subsidy payments. In June of this year, the government expanded the range of towns eligible for such payments from 10 to 30 km in order to end the previous source of contention of towns not receiving subsidies that were located within evacuation zones. The latter usually covers a 30 km radius around the NPP.

The system was developed in response to both the first Oil Shock of 1973, the economic damage of which brought energy independence to the forefront of national politics. In an effort spearheaded by Prime Minister Tanaka Kakuei, the Diet eventually passed dengen sanpo to systematize host community benefits and strengthen incentives for negotiations with town councils, fishery cooperatives, or industrial associations in potential siting towns.

Massive capital

The subsidies provide host communities with massive injections of capital to spend on municipal functions, infrastructure, and education. According to ANRE, municipalities could receive over ¥183 billion ($1.24 billion) in subsidies per reactor over the asset’s lifespan. This is why these rural towns – usually with populations of just a few thousand people – boast impressive public facilities that, in any other context, would appear to be a developmental miracle.

An example of this outsized capital influx can be seen in Kashima Town, Shimane Prefecture, which hosts the Shimane NPP. The town, with a mostly older population of under 6,000, used the capital it received from approving the siting of a third reactor to build a massive sports complex for local residents, complete with baseball and soccer fields, an indoor pool, and a $35 million gymnasium. The entire facility is co-located with the Shimane NPP’s visitor center.

In Ooi Town, Fukui Prefecture, which hosts Ooi NPP, an ocean-side luxury hotel and spa sits on newly built reclaimed land, next to a multi-story family and children’s play center, and retail facilities. Located next door is a nuclear PR center equipped with amusement park-style attractions that teach about nuclear energy.

Such expensive infrastructure is typical of nuclear host communities and sticks out in depopulated rural areas. Without strong industry, outside investment, and tax bases, such infrastructure only becomes possible through the unique structure of dengen sanpo subsidies.

Once one reactor is built on the site, others usually follow. This makes sense from the NPP operator’s point of view, because most nuclear power plants have multiple reactors, making them more efficient to run and easier to maintain. But the stacking of several reactors on one site is also attractive for the local community.

Once towns go through the complicated process of siting the initial facility, there is much less additional community resistance and even stronger financial incentives to allow additional reactors. Each time, a new set of long-term subsidies is unlocked, helping to support the town and its newly built premium-level public infrastructure. As a result, all but one nuclear power plant in Japan added at least one reactor beyond initial construction, with some adding multiple, like Kashiwazaki-Kariwa NPP’s six.

The trend of stacking reactors on one site creates a tremendous degree of fiscal dependence on nuclear-related revenues for the host community. For Ooi Town in Fukui Prefecture, one of the few local governments that publishes details of its nuclear revenue, such income comprised over 64% of its FY2024 budget. This includes the direct subsidy payments, as well as fixed asset taxes, income taxes from employees at the plant, and other indirect revenue sources.

In an economic arrangement reminiscent of former coal mining communities in the U.S., most nuclear host communities – particularly those with smaller populations – exist as one-company towns. With lower motivation to attract more industries to the area, local economies become dominated by NPPs, their related operations, and subsidy-powered investment projects.

Conclusion

Moving forward, dengen sanpo and nationwide nuclear infrastructure will play an important role in the future of Japan’s energy sector. Despite the government’s recent extension of potential reactor operating licences to beyond 60 years, in the coming decade, many NPPs will reach their upper operating limits and require decommissioning or replacement.

There is, however, essentially no precedent for a complete decommissioning of all nuclear reactors in a fiscally dependent host community – except the mostly evacuated towns near Fukushima Daiichi – and whether payments would continue.

Subsidies and broader economic benefits seem highly likely to remain as the central driver in nuclear siting. As units built in the 1970s reach their maximum planned operating lifespan over the coming decade, the system and its role in nuclear siting will enter an unprecedented era. To ensure long-term fiscal and economic security, local governments hosting older reactors will be highly receptive to utilities building replacement or additional units.

What’s more, increasing depopulation and impending fiscal difficulties of rural authorities with declining tax bases will also increase the allure of potential nuclear revenues.

As the urgency to replace the aging nuclear fleet increases, the government will need to decide how to use the subsidy trump card. If nuclear host communities are allowed to receive subsidies indefinitely, will they be more supportive of projects to build “replacement” reactors on the sites where aging units are scheduled for decommissioning or less? Can Japan’s public purse even afford to retain subsidies at today’s levels, and should this spending be taken into account when estimating the total cost of nuclear power generation?

A solution for one town will be copied by another, and the first case of a utility seeking to build a new reactor to replace an aging unit is already at hand. Kansai Electric plans to add a modern reactor at the Mihama NPP location. The local mayor already signaled his backing. The question is: What was the cost of his support?

ASIA ENERGY REVIEW

BY JOHN VAROLI

A brief overview of the region’s main energy events from the past week

Australia / Renewable energy

The Australian Energy Market Operator predicted the National Electricity Market will see a steady rise in renewable energy generation capacity, reaching 229 TWh by 2035.

China / AI

While the U.S. leads in AI development, its aging power grid and fragmented infrastructure are obstacles. Meanwhile, China’s surplus power capacity, bolstered by innovative ultra-high voltage transmission lines, is powering its AI ambitions.

China / CO2 emissions

Clean-energy growth helped China’s CO2 emissions fall 1% YoY in H1 of 2025, continuing a declining trend that started in March 2024.

China / Hydrogen

A joint EU-China report features multiple EU-based companies with pilot hydrogen projects or technology licensing arrangements in China, despite geopolitical tensions. Ceres was singled out for its SOFC platform development.

India / Nuclear power

Top Indian energy firms are advocating for nuclear power to decarbonize, while cautioning that electricity from reactors needs to be affordable to substitute coal.

India / Weather forecasting

India is working to significantly improve the accuracy of its weather forecasting systems to meet the growing demands of its renewables power generation sector

Indonesia / Oil & Gas

The Indonesia Energy Corp inked an MoU with Aguila Energia, an affiliate of Rio de Janeiro–based investment firm Aguila Capital, to develop oil and gas assets in Brazil.

South Korea / Nuclear power

Korea Hydro & Nuclear Power is in talks with Westinghouse to create a JV to develop nuclear energy in the U.S. Trump has pledged to quadruple nuclear energy capacity by 2050.

Taiwan / Nuclear power

A referendum this weekend on whether to restart the Maanshan nuclear plant, Taiwan’s last operational NPP, ended in failure due to low voter turnout. Hence, no restart will take place.

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

NEWS:

・ESG bond issuance in Japan drops for second year

・EGC proposes revising regulations under revenue cap system

・Japan and India to focus on chips, critical minerals

ongoing tariff negotiations. In March, Alaska governor Mike Dunleavy visited those countries, as well as Thailand, together with delegations from AGDC and Glenfarne Group.

ongoing tariff negotiations. In March, Alaska governor Mike Dunleavy visited those countries, as well as Thailand, together with delegations from AGDC and Glenfarne Group.