WEEKLY

OCTOBER 14, 2025

ANALYSIS

WILL A NEW PM SHAKE UP JAPAN’S ENERGY POLICY?

- The ruling LDP selected Takaichi Sanae as its leader, making her the likely candidate to become the nation’s first female PM.

- Given energy’s central role in Japan’s digital modernization, and Takaichi’s own keen interest in the topic, we expect energy policy to be a major focus. Takaichi also wants the energy sector to reflect national security and industrial concerns.

BESS MARKET BOOMING AS MORE NON-ENERGY FIRMS ENTER THE SECTOR

- With the rapid expansion of renewable energy, battery storage is moving from a niche supportive technology to one of its central drivers.

- Yet Japan’s grid infrastructure remains ill-prepared. Curtailments of solar power are common, and large-scale transmission upgrades are not expected until the 2040s. How will the BESS sector fare in the circumstances?

ASIA PACIFIC REVIEW

This column provides a brief overview of the region’s main energy events from the past week

NEWS

- Japan’s new infrastructure plan to focus on resilience and decarbonization

- Aramco looks for future energy breakthroughs at Japanese universities

- Three firms chosen for METI’s support program for hard-to-abate industries

- Tokyo to issue world’s first resilience bond for climate adaptation

- JERA considers hosting DCs within thermal power plants around Yokohama

- Furukawa Electric to build ¥100 bln submarine power cable factory

- KHI sells world’s first large-scale gas engine with H2 co-firing at 30%

- ENEOS to test room-temperature hydrogen production in Australia

- KEPCO to expand battery storage business

- Mitsubishi HC sets up unit for asset management of renewable energy

WIND POWER AND OTHER RENEWABLES

- 4th round of offshore wind auction postponed

- Survey: 80% of business leaders view wind targets

- unrealistic

- Coexistence tax approved for solar and wind farms

- Chubu Electric began dismantling older reactor

- TEPCO to provide massive fund to Niigata Pref as a sweeter for reactor restart approval

- Japan reassures Australia over gas exports

- Osaka Gas explains its LNG strategy and outlines plans to enter India’s city gas market

CARBON CAPTURE & SYNTHETIC FUELS

- ANRE moves forward in designing Generation

- Benchmark for power sector

- METI explains rules around CCS storage

- Firms aim to commercialize MOFs after Kitagawa’s Nobel win

EVENTS

Oct 15-16 Japan CCUS Summit

Oct 15-16 Connecting Green Hydrogen Japan

Oct 15-17 Global Offshore Wind Summit – Japan @Akita Prefecture

Nov 10-21 COP30 @ Belem, Brazil

Dec 4 Japan CCS Forum 2025 @Tokyo

Jan 28-30 Renewable Energy 2026 @Tokyo Big Sight

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Chief Editor)

John Varoli (Senior Editor, Americas)

Kyoko Fukuda (Data, Events)

Magdalena Osumi (Renewables & Storage)

Filippo Pedretti (Thermal, CCS, Nuclear)

Tetsuji Tomita (Power Market, Hydrogen)

Aglaé Bange (Renewables and Biomass)

George Hoffman (Sales, Business Development)

Tim Young (Design)

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

NEWS: GENERAL OUTLOOK AND TRENDS

Japans new infrastructure plan to focus on resilience and decarbonization

(Nippon Kogyo Keizai Shimbun, Sept 30)

- The Ministry of Land, Infrastructure, Transport and Tourism (MLIT) is developing its next Five-Year Plan for Social Infrastructure Development for FY2026–2030, aiming to turn population decline into a plan for revitalization.

- Main goals are: 1) building sustainable communities; 2) building resilient infrastructure; and 3) advancing a decarbonized society.

- The plan promotes renewables use in infrastructure spaces, life-cycle decarbonization of facilities, expanded green infrastructure, improved construction recycling, and better use of water, etc.

- MLIT also emphasizes data-driven infrastructure management (“cluster management”), securing skilled construction workers, and public-private collaboration to modernize asset maintenance.

- CONTEXT: The plan aligns with the broader GX strategy, positioning infrastructure development and management as a key method to both enhance economic resilience and accelerate carbon neutrality goals.

Aramco looks for future energy breakthroughs at Japanese universities

(Japan NRG, October 3)

- CONTEXT: Saudi Aramco executive VP of technology & innovation Ahmad O. Al-Khowaiter spoke at Kyoto University about industry-academia cooperation on sustainable energy.

- Aramco is scouting for new energy sector technologies, and Japanese universities are fertile ground for the world’s largest oil company.

- Aramco seeks tech that can: 1) scale without enormous upfront costs; 2) have strategic applications; and 3) is managed by strong teams. Al-Khowaiter cited Japanese startup TerraDrone as an example. • CONTEXT: In 2023, TerraDrone raised $14 million from Aramco’s venture capital arm, Wa’ed Ventures. TerraDrone and Aramco also signed an MoU this April on developing drones to enhance safety and streamline energy sector operations.

- He emphasized Aramco’s interest in original technology that creates disruption, such as metalorganic frameworks (MOFs).

- CONTEXT: MOFs are central to Aramco’s efforts to develop advanced materials for efficient carbon capture, particularly in DAC.

- Universities account for 90% of Aramco’s major transformations. Person-to-person exchanges are essential, such as a company-sponsored student research position.

- Al-Khowaiter said exchanges require time, patience, and constant communication (e.g., explaining the company’s changing priorities to university researchers).

- TAKEAWAY: The Tokyo Stock Exchange and METI are proceeding with regulatory reforms to make Japan’s startups more attractive to institutional investors. A greater presence by corporate investors such as Aramco could provide startups with a welcome source of funding, long-term perspectives, and deep tech understanding. Such support raises the likelihood that a given deep tech startup – in energy or any other field – can scale globally.

Three companies chosen for METI support for hard-to-abate industries

(Government statement, October 7)

- CONTEXT: In FY2024, METI launched a program to support energy and manufacturing modernization in hard-to-abate industries, funded by GX Economic Transition Bonds. It continues in FY2025.

- The program partly subsidizes equipment costs for industries such as steel, chemicals, paper, and cement to promote carbon neutrality and improve competitiveness.

- The subsidy is, in principle, up to one-third of total costs.

- The call for applications has two phases: 1 (steel), and 2 (chemicals, paper and pulp, cement.). This time, three companies from phase 2 were selected:

- Daio Paper – Shutdown of coal boilers, and replaced with new power generation facilities running on waste at Mishima Plant;

- Resonac – Introduction of hydrogen-fueled gas turbines at Kawasaki Plant;

- Osaka Soda – Low-carbon conversion project for epichlorohydrin production that uses biomass feedstock and non-fossil electricity.

- The project runs until February 2030 (FY2029).

- CONTEXT: In FY2024, JFE Steel (conversion to innovative electric furnace) and Nippon Paper (GHG emission reduction by biorefinery) were selected. In FY2025, Nippon Steel (conversion to innovative electric furnaces at three plants) was selected.

- CONTEXT: The govt aims to mobilize over ¥150 trillion in GX (decarbonization) investments across all industries over the next decade. To support this, it is issuing ¥20 trillion in GX Economic Transition Bonds. The main target areas include steel, chemicals, hydrogen, offshore wind, etc.

- SIDE DEVELOPMENT:

- Daio Paper builds waste-to-energy facility

- (Company statement, October 7)

- Daio Paper will shut its coal boilers and build a new waste-to-energy plant at its Mishima Factory (Shikokuchuo City, Ehime) with METI support.

- Total investment – ¥27.2 billion, of which ¥8 billion to be subsidized by METI. o CONTEXT: Daio Group aims for carbon neutrality by 2050, promoting energy efficiency and biomass fuel use. By 2030, it targets a 46% reduction in fossil CO2 emissions and a 20% cut in total GHGs compared to 2013 levels.

- SIDE DEVELOPMENT:

- Resonac introduces hydrogen co-firing gas turbine

- (Company statement, October 7)

- Resonac was chosen for METI’s GX investment program.

- Its Kawasaki Plant (Kawasaki City, Kanagawa) will be upgraded with a 30-40 MW gas turbine that co-fires city gas and hydrogen; operations to start in FY2030.

- Total investment ¥21.7 billion; ¥7.1 billion to be subsidized by METI.

- CONTEXT: The company’s long-term vision targets a 30% reduction in Scope 1 and 2 emissions by 2030 (over 2013).

- SIDE DEVELOPMENT:

- Osaka Soda converts to low-carbon manufacturing

- (Company statement, October 7)

- Osaka Soda will modernize production with energy-saving measures.

- This will shift the main raw materials for epichlorohydrin production from fossil-based to bio-based sources.

- Total investment of ¥3 billion; of which ¥970 million to be subsidized. o CONTEXT: Osaka Soda aims to cut GHG emissions 30% by 2030 (over 2013).

Tokyo to issue world’s first resilience bond for climate adaptation

(Government statement, October 10)

- The Tokyo Metropolitan Govt announced plans to issue a ¥50 billion in foreign-currency– denominated ‘resilience bonds’ this month, with proceeds dedicated exclusively to disaster prevention and climate adaptation projects.

- CONTEXT: The bond issuance, recognized by the UK-based Climate Bonds Initiative (CBI), will be the world’s first officially certified ‘resilience bond.’ The CBI certification follows the introduction of a new taxonomy for resilience finance in August, making Tokyo the first issuer globally under this standard.

- Funds will finance infrastructure such as flood control reservoirs, coastal measures to prevent storm surges, and undergrounding of power lines to mitigate typhoon-related outages.

- The bond’s use of proceeds is restricted to climate-related disasters, excluding projects tied to earthquake mitigation.

- The move comes amid rising recognition that governments must pursue not only climate mitigation (emission cuts) but also adaptation measures. The topic is expected to be a key agenda item at COP30 in Brazil next month.

- TAKEAWAY: Tokyo’s initiative signals Japan’s entry into the adaptation finance market, a growing focus for ESG investors seeking projects that strengthen resilience against climate-intensified floods, typhoons, and heatwaves. These complement the capital in traditional green bonds that center on emission reduction. Tokyo has already issued over ¥500 billion in SDG-linked bonds, including green, social, and sustainability bonds, since its first green bond in 2017.

China tightens rare earth export controls targeting defense and chip industries

(Reuters Japan, October 9)

- China’s Ministry of Commerce announced new export restrictions on rare earth materials, expanding earlier curbs introduced in April.

- The new rules ban unauthorized overseas cooperation by Chinese companies on rare earth processing or recycling, and tighten licensing requirements for exporting related manufacturing equipment.

- Exports to foreign defense and semiconductor firms will face stricter screening, with defense-related applications denied outright and advanced semiconductor-related requests reviewed case by case.

- The scope of restricted technologies now includes a wider range of rare earth magnets and recycling equipment, signaling Beijing’s intent to protect strategic supply chains amid geopolitical tensions.

- TAKEAWAY: This move will further increase China’s leverage as the dominant player in global rare earth processing, which is critical to global clean energy and defense industries, and mirrors similar controls Beijing previously imposed on gallium, germanium, and graphite. Japan relies on China for just over half of its rare earths supply and in the past has faced manufacturing stoppages when export volumes were restricted.

Mitsui & Co to invest in $650 million expansion of Australian iron ore mine

(Company statement, October 7)

- Mitsui & Co, in cooperation with Rio Tinto and Nippon Steel, will expand the West Angelas iron ore mine in Western Australia.

- Total investment is A$998 million (roughly ¥100 billion). Mitsui covers 33%. Nippon Steel will contribute 14% (or A$140 million).

- Production is planned to begin in 2027, with the site offsetting declining output from other areas.

Annual production will be about 35 million tons (Mt) after expansion.

- CONTEXT: This move follows Mitsui’s February acquisition of a stake in Australia’s Rhodes Ridge iron ore project for ¥800 billion, targeting production by 2030. Mitsui aims to raise production from the current 62 Mt/ year to over 100 Mt.

- TAKEAWAY: This investment underscores Japan’s push to secure stable supplies of key raw materials. Reliable iron ore sourcing supports the steel sector, which remains central to Japan’s energy transition and infrastructure development.

Univ of Tokyo, TEPCO PG promote Watt-Bit collaboration

(University statement, October 8)

- TEPCO Power Grid and the University of Tokyo are promoting the “Watt-Bit Collaboration Project.”

- Univ of Tokyo will advance visualization and optimization of campus-wide power use and carbon footprint, leveraging data and renewables.

- TEPCO PG will use this project to develop next-gen power grid operations by linking distributed energy sources and computing resources through wide-area workload shifting and digital twins.

- CONTEXT: Univ of Tokyo has promoted GX-related initiatives since launching the Alliance for Global Sustainability in 1994. In April, it set up the GX Strategy Promotion Center to lead efforts toward carbon neutrality and a circular economy.

NEWS: ELECTRICITY MARKETS

JERA considers hosting DCs within thermal power plants near Yokohama

(Denki Shimbun, October 6)

- JERA will consider hosting data centers (DCs) at its thermal power plant sites near Yokohama. On Oct 3, it signed a MoU with the city for cooperation.

- The initiative aligns with the push for integrated “Watt-Bit” infrastructure, and also explores collaboration in AI-related human resource development.

- DCs inside power plants could reduce connection delays and allow faster electricity supply, addressing the challenge of meeting data centers’ massive power demand. Similar projects are also under consideration at other JERA plants such as a partnership with Sakura Internet.

- CONTEXT: JERA’s plans concern Yokohama Thermal Power Station (3 GW) and Minami-Yokohama Thermal Power Station (1.15 GW). Both are LNG fuelled.

- TAKEAWAY: The power company made an open pitch to DC operators to host them on the grounds of its LNG plants earlier this year. Initially, many hyperscalers were hesitant to agree to power their DCs with fossil fuels, but a shortage of CO2-free sources and surging demand for power is making some large firms reconsider.

- SIDE DEVELOPMENT:

- GX strategic regions applications to start next year drawing funding for CO2-free power

- (Denki Shimbun, October 8)

- The govt plans to subsidize capital investment in regions hosting decarbonized power sources such as renewables and nuclear power. Examples are investments in energy-saving facilities and advanced manufacturing equipment.

- The goal is to encourage companies to get electricity via PPAs from new renewable projects or restarted nuclear plants. Greater subsidies will be for those that contribute to increasing supply capacity.

- Starting in early 2026, prefectures will apply as “GX strategic regions,” focusing on areas like data center hubs or industrial complexes.

Furukawa Electric to build ¥100 bln submarine power cable factory

(Nikkei, October 8)

- Cable manufacturer Furukawa Electric plans to build a new submarine power cable factory in Futtsu, Chiba Pref, investing about ¥100 billion, with up to ¥31 billion from govt subsidies. Operations are slated to start in 2030.

- The cables will transmit renewable energy generated in regions such as Hokkaido and Kyushu to Tokyo, etc; and could be used for projects in Asia and the Middle East.

- The plant will produce high-voltage DC submarine cables that are more efficient for long-distance, large-capacity transmission than AC systems. Annual production will reach 200 km of 500 kV HVDC cable.

- About 800 km of cable with 2 GW capacity is needed to link Hokkaido and Tohoku with Tokyo; and 40–55 km of 1 GW cable connecting Kyushu with Honshu.

- CONTEXT: Submarine power cables are essential to balance renewables generation by transmitting surplus power between regions. Rising global power demand from expanding data centers is another factor. More national transmission projects are expected to be announced by March 2026.

- TAKEAWAY: While cross-border grid connections allow regions to share reserves and balance supply with demand, as well as create economies of scale by sharing infrastructure, they can introduce vulnerabilities. These include the mundane, such as difficult but costly repair and maintenance, as well as more serious problems such as extensive potential security threats across a wide distance. Also, a technical fault in one area, such as an interconnector malfunction, can affect all the connected regions.

September power spot prices eased as heat moderated mid-month

(Exchange statement, Oct 9)

- The electricity spot market softened in September, as prices in both East (50 Hz) and West (60 Hz) Japan declined over August as extreme heat subsided.

- Monthly average temperature was 2.49° C above normal, third highest since records began, but cooler than record highs of 2023 and 2024. Abundant supply of renewable energy prevented price spikes similar to those seen in previous summers.

- CONTEXT: There has been virtually no curtailment of solar power in the last three months due to high temperatures.

- Spot prices fell in six regions including Hokkaido, Tohoku, Tokyo, Hokuriku, Chubu, and Kansai; while Chugoku, Shikoku, and Kyushu saw modest gains. All nine areas were below year-earlier levels.

- Fuel prices also weakened. By late September, crude oil averaged ¥66,962/ kl; LNG ¥84,655/ ton; and coal ¥17,846/ ton. All were down from the previous month.

Intraday market trading jumps but prices remain mostly flat

(Denki Shimbun, Oct 9)

- In September, JEPX intraday market’s average daily contracted volume rose 12.5% MoM to 19.06 TWh, reflecting increased trading activity during midday demand surges. Despite this, averages were mostly flat, except for a sharp spike on Sept 17, when tightening supply and high temperatures pushed midday prices up to ¥199.99/ kWh, the highest since March 1.

- The share of intraday trades relative to total demand increased by 1 point to 0.7%, with an average of 8813 transactions per day. The monthly average contract price was ¥12.934/ kWh, about ¥0.72 lower than the spot market’s system price.

- Trading volumes peaked on Sept 17 at 43.22 GWh, and transaction counts were highest on Sept 30 with 10,094 deals. The 17th’s surge was due to rising temperatures and a system operation error by one major utility, which caused partial non-bidding in the spot market and subsequent compensatory trading.

- Meanwhile, tight supply during early September saw imbalance charges exceed ¥100/ kWh, prompting aggressive buying to secure generation capacity.

TOCOM power futures trading volume drops sharply

(Exchange statement, Oct 9)

- TOCOM futures trading volume fell to 1,134 contracts in September, down more than half from August’s 2,698, as the number of larger-lot sales declined and most activity shifted to smaller offexchange deals.

- The number of executed trades dropped to 73, from 144 the previous month, with 63 over the counter; roughly 40% of all trades were under 10 lots, reflecting limited participation by major utilities.

- Market participants attributed the slowdown to narrow spot price fluctuations and reduced hedging demand, though attention is turning to autumn and winter risk hedging ahead of maintenancerelated power shortages.

- The largest trades included 100-lot (10 MW) base-load contracts for October 2025 delivery, priced at ¥11.6 in the West and ¥12.3 in the East. Final monthly settlement prices stood at ¥12.92 (East base) and ¥11.26 (West base).

JFE Engineering wins fuel supply system contract at Himeji Gas Power Plant

(Company statement, October 2)

- JFE Engineering Corp won an order from Osaka Gas to build a complete natural gas fuel supply system for Himeji Natural Gas Power Plant Unit 3.

- Still under construction, Unit 3 (622 MW) was chosen for the long-term decarbonized power sources auction (LTDA) in April 2024. Operation is planned by FY2030.

- JFE Engineering is already building similar fuel supply systems for Units 1 and 2, set to launch in January and May 2026.

Kawasaki GE launches electricity production/ consumption with waste

(Company statement, October 1)

- Kawasaki Green Energy launched a local electricity production and consumption project utilizing waste-to-energy power.

- This project will supply electricity from the new waste treatment facility to municipal offices and schools in Kodaira, Higashiyamato, and Musashimurayama.

- CONTEXT: Kawasaki GE is a new electricity retailer set up by Kawasaki Heavy Industries (KHI), by separating the power retail business of Kawasaki Trading. KHI was awarded a waste treatment facility project in May 2020.

NEWS: HYDROGEN

KHI sells world’s first large-scale gas engine with co-firing 30% hydrogen

(Company statement, September 30)

- KHI began sales of the world’s first large-scale gas engine facility capable of co-firing 30% hydrogen.

- The 8 MW-class engine was verified at Kobe Works in Oct 2024, completing field tests last month.

- Based on its proven “Kawasaki Green Gas Engine” series with over 240 units delivered since 2011, the new hydrogen-ready model can burn up to 30% hydrogen mixed with natural or city gas.

- As a transition technology, it utilizes existing facilities and infrastructure.

- TAKEAWAY: The development of power generation technologies using hydrogen and ammonia as fuels is progressing globally, but KHI leads by commercializing large gas engines for hydrogen co-firing. Hydrogenblended gas turbines are also moving from field tests in large units (tens of MW class) toward commercialization. MHI is also developing small-scale (~500 kW) hydrogen-only gas engines, with commercial sales expected soon.

ENEOS to test room-temperature hydrogen production in Australia

(Nikkei Asia, October 8)

- ENEOS will begin a hydrogen production field test in Australia in FY2026, investing about ¥20 billion.

- It will use electrolysis to produce hydrogen, combine it with toluene to create methylcyclohexane (MCH), a liquid similar to gasoline, and test large-scale production and equipment durability over two years.

- The project will produce 190 tons of hydrogen and 3,000 tons of MCH annually, eight times the scale of a previous trial.

- The goal is for commercial production in the 2030s, envisioning large-scale MCH output in countries with low renewable power costs for export to Japan.

- CONTEXT: ENEOS developed a technology called “Direct MCH” that directly synthesizes MCH by reacting hydrogen generated in an electrolyzer with toluene. From 2022 to 2023, it tested a green hydrogen supply chain using the Direct MCH process in Australia, where renewable energy is abundant. A demo plant with a 150 kW Direct MCH electrolyzer and a 250 kW solar power system was built in Brisbane to verify operations. Subsequently, ENEOS developed a large, MW-scale electrolyzer as the minimum commercial unit.

- TAKEAWAY: ENEOS is still demonstrating its MCH supply chain and refining the Direct MCH technology for electrochemical synthesis. While ammonia seems to have gained an upper hand as the hydrogen carrier of choice for power plants, other H2 pathways have a chance to win over other sectors. Each carrier has its own advantages and disadvantages, making it difficult to determine the single best option for all parties.

MHI studies decarbonization value chain for green hydrogen/ ammonia in India

(Company statement, October 3)

- MHI launched a study to develop a master plan for optimizing facilities for green hydrogen and ammonia exports from India.

- As India promotes these fuels for export, MHI aims to model and simulate production and then use them across India and SE Asia to assess feasibility.

- India’s Hygenco will share data on green ammonia production. The results will support a crossborder decarbonization master plan and policy proposals for introducing low-carbon fuels in countries such as India and Singapore.

- CONTEXT: METI supports projects where Japanese companies collaborate with local firms in Global South countries to build resilient supply chains for carbon neutrality.

NEWS: SOLAR AND BATTERIES

KEPCO seeks to expand nationwide battery storage business

(Nikkei, October 6)

- KEPCO (Kansai Electric) is rapidly expanding its battery storage business across Japan, planning new facilities in the Kanto and Chubu regions.

- By the early 2030s, the utility aims to build 1 GW of storage capacity.

- In addition to operating its own facilities, KEPCO will provide O&M services for third-party battery plants. Its new O&M subsidiary, with expertise in battery diagnostics and safety, will provide onestop services for other companies.

- KEPCO already operates the largest domestic facility, Kinokawa Battery Station, jointly with Orix, and is building large-scale 100 MW-class storage in Sapporo, Osaka, Hamamatsu, and Mito.

- KEPCO’s strengths include ownership of suitable land near transmission lines, enabling efficient facility placement. The Kansai Electric Group also offers integrated support through market trading and real estate development.

- CONTEXT: KEPCO is not the only major Japanese corporate investing in expanding its BESS business, with firms like Orix seeking to leverage their experience from solar operations and O&M services. The market has new foreign entrants, from Asia (Taiwan, China) and Europe with support from the Japanese govt via subsidies.

Idemitsu Kosan enters BESS market with large-scale Himeji project

(Company statement, October 10)

- On Oct 10, Idemitsu Kosan began operating its first large-scale grid-scale BESS, the Himeji Battery Energy Storage Station, in Hyogo Pref. This marks Idemitsu’s entry into the grid-scale battery business.

- The plant has a capacity of 15 MW/ 48 MWh. Idemitsu will operate the plant and generate revenue through Japan’s electricity balancing market and wholesale electricity trading.

- It was developed jointly with Renova, and is located on the site of Idemitsu’s former Hyogo oil refinery that shut in 2003. Ownership breakdown: o Idemitsu Kosan – 51% (operations and power trading) o Renova – 22% (engineering and financing) o Nagase & Co. – 22% (battery engineering support)

- SMFL Mirai Partners – 5% (project finance)

- TAKEAWAY: While Idemitsu says it has no immediate plans for additional plants, the Himeji project highlights rising big-business interest in leveraging energy storage for grid balancing and power trading, signaling potential long-term growth opportunities in Japanese power markets.

Mitsubishi launches subsidiary in asset management of renewable energy

(Company statement, October 1)

- Mitsubishi HC Capital Energy created a new wholly owned subsidiary, MHC Asset Management, specializing in solar and BESS asset management.

- TAKEAWAY: MHC’s current asset management portfolio totals 336 MW across nine power plants, previously managed by a dedicated in-house department. Establishing a standalone subsidiary – similar to when ENEOS founded ENEOS Renewable Energy Management in 2013 – reflects MHC’s intention to remain flexible and competitive as power demand grows.

- SIDE DEVELOPMENT:

- Kitahama Capital Partners acquires solar farms in Hokkaido

- (Company statement, September 16)

- Kitahama Capital Partners subsidiary, Kitahama PV Development 2, gained rights to sell energy to operators from eight solar farms. Revenue is estimated at ¥860 million.

- The facilities, located in Hokkaido, have combined peak capacity of 21.5 MW (i.e the maximum power output of the combined solar installations under ideal conditions).

Ricoh develops low-cost, flexible PSCs using inkjet technology

(Company statement, October 10)

- Ricoh is developing perovskite solar cells using its inkjet printing tech, aiming to make them with a total capacity of 300 MW by FY2030.

- It also aims to achieve power generation costs of ¥14/ kWh, the govt’s target for next-gen cells.

- The method simplifies manufacturing, reduces material use, and eliminates the need for lasers or vacuum deposition, lowering costs.

- Ricoh is collaborating with NTT Anode Energy to optimize electrical design, and with Daiwa House to test wall-integrated installations.

- CONTEXT: The govt targets 20 GW of PSCs by 2040. Other Japanese firms like Panasonic, Konica Minolta, and Seiko Epson are also exploring inkjet-based approaches for perovskite and buildingintegrated solar cells.

- SIDE DEVELOPMENT:

- NFC agrees with Gosan Tech on inkjet coating equipment for PSCs

- (Company statement, September 29)

- NFC signed a MoU with South Korean company Gosan Tech to develop inkjet coating equipment for PSCs.

- The technology enables rapid and uniform coating, including on large surfaces, with a pressure control precision of ±5 Pa or less.

- The coating equipment will be sold to solar manufacturers in Japan and the U.S.

Osaka Gas and GS Yuasa begin demo of new PCS-integrated BESS

(Company statement, September 25)

- Osaka Gas and GS Yuasa began a field test of GS Yuasa’s new PCS-integrated battery storage system – the 840 kWh Li-ion system – that will run until March 2028.

- The project will test multi-use operations in several electricity markets and develop optimal control methods based on battery performance.

- Osaka Gas provides the site and manages operations, while GS Yuasa supplies and maintains the system.

- The system can be installed without large cranes, allowing more flexible site selection than container-type units. It’s also linked to Shizen Connect, a VPP platform, enabling grid and renewables storage use.

Kyocera TCL Solar to transition Fukuoka PV plant to FIP, seeks more BESS

(Company statement, October 6)

- Kyocera TCL Solar said its Fukuoka Iizuka solar farm in Fukuoka Pref will transition from the FIT to the FIP, adding a battery storage system.

- Construction began, with operation planned for February 2026. This will be the company’s third project combining battery storage with FIP conversion.

- It has an AC capacity of 1.99 MW, paired with a 1.5 MW/ 6 MWh battery system.

- CONTEXT: Tokyo Century aims to expand new battery-equipped plants and hybrid battery-solar facilities as part of its mid-term strategy. In June 2024, it added a battery system to the Kumamoto Arao solar farm. In June work began on a battery at the Kagoshima Kirishima solar farm.

- TAKEAWAY: The plan shows a growing interest in hybrid solar-battery storage systems partly as a means to address grid constraints. Still, most of these projects seem to be in Kyushu and on the smaller-side, reflecting the challenge of having the land available, the right grid connection and economics all line up.

JAPEX begins building BESS in Hokkaido

(Company statement, October 6)

- JAPEX began building its first extra-high voltage grid-scale battery, Tomakomai BESS, (Tomakomai City, Hokkaido). Operation is set to launch in autumn 2027.

- The batteries will have a capacity of 20 MW/ 106 MWh.

- The project is partially state subsidized. It follows JAPEX’s first battery facility in Chiba City (launched in August) and is part of the company’s push into energy storage and grid stability.

- TAKEAWAY: More companies seem to be refocusing strategy to large-scale EHV projects, which are projected to overtake the now mainstream high-voltage projects in the coming years.

TESS Engineering receives EPC contract for BESS

(Company statement, September 24)

- TESS Engineering won a EPC contract from DEI Battery Fund Alpha for a ¥130 billion BESS facility.

- The project is expected to be completed by April 2028.

- CONTEXT: In 2024, TESS Engineering released its long-term strategy plan, TX2030, which calls for extending the battery storage business to 700 MW by 2030. In February, the company signed a MoU with Daiwa Energy & Infrastructure for a 2 GWh battery storage project.

Tensor Energy optimizes AI simulation service for solar and BESS

(Company statement, October 9)

- Tensor Energy has optimised its AI service Tensor Cloud, which evaluates profitability of solar projects with BESS equipment for decision-making.

- The platform allows users to set a flexible minimum bid price and shows the expected revenue impact from joining the balancing market, as well as to simulate grid charging scenarios.

- The update adds advanced features such as:

- dynamic scenario comparisons across various market and contract structures, including FIT, FIP, bilateral contracts, spot, and ancillary service markets

- visualize expected revenues from multiple power trading strategies

- simulate IRR and cumulative cash flow when acquiring operating assets

- display 30-min spot prices and curtailment rates in long-term simulations.

Idemitsu Kosan launches solar system at Australia’s Bogabri coal mine

(Company statement via Nikkei, October 8)

- Idemitsu Kosan launched a 5 MW solar power system at its Bogabri coal mine in New South Wales, Australia, where it holds a 90% stake.

- CONTEXT: Australia has been tightening regulations on GHG emissions and environmental impact from mining operations.

- Idemitsu also plans to introduce a vanadium redox flow battery in the second half of FY2026. It will have a capacity of 2 MW/ 12.6 MWh.

- The vanadium electrolyte, provided by Australia’s Vecco (51% owned by Idemitsu’s subsidiary), is non-flammable, recyclable, and 99% of materials can be reused.

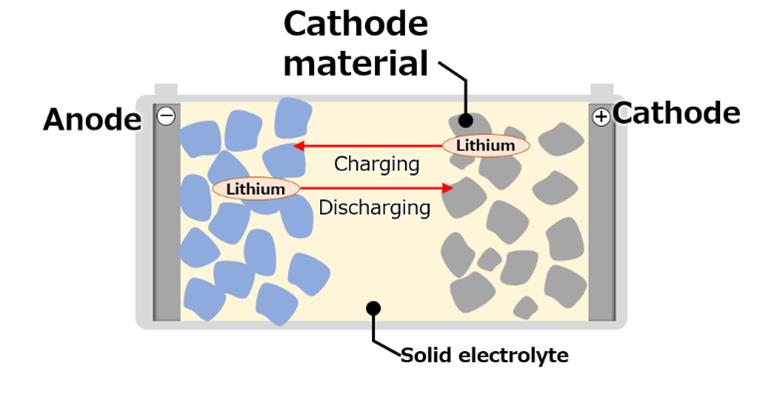

Sumitomo Metal and Toyota to make cathode materials for solid-state batteries

(Company statement, October 8)

- Sumitomo Metal Mining and Toyota Motor agreed to mass-produce cathode materials for all-solidstate batteries for battery EVs (BEVs).

CONTEXT: All-solid-state batteries, which use solid electrolytes instead of liquid ones, offer smaller size, higher output, and longer lifespan, potentially improving driving range, charging speed, and performance of BEVs. Toyota aims to commercialize them around 2027–2028.

- Since 2021, the two firms cooperated on research, focusing on cathode material degradation during charge-discharge cycles. Using Sumitomo’s powder synthesis tech, they developed a durable cathode material suitable for all-solid-state batteries.

- The partnership aims for the world’s first practical BEV using all-solid-state batteries.

NEWS: WIND POWER AND OTHER RENEWABLES

Japan postpones 4th round of fixed-bottom offshore wind auction

(Government statement, October 1)

- The govt postponed the fourth round of fixed-bottom offshore wind power tenders (FY2025). The bidding process was set to begin on Oct 14.

- The decision follows a request from the national govt, which is reviewing the reasons behind the withdrawal of operators from three Round 1 offshore wind sites and examining how to strengthen the business environment to ensure future power generation investments are completed.

- The review is expected to be concluded by the end of the year. A new schedule for the auction will be announced once it is finalized.

- TAKEAWAY: Given the flux around the offshore wind sector, it was always inevitable that METI would delay the next round bidding. Without clarity around the status of projects from previous rounds – which are facing heavy commercial and other pressures – bidding appetite for R4 was expected to be weak. Still, officials have stressed that they remain committed to helping the offshore wind industry get on its feet in Japan and will move expeditiously to resolve current issues. So, the R4 delay is not necessarily a negative development. It’s a pause to ensure that the sector rules are on the right track before auctions resume.

Survey shows over 80% of business leaders view wind targets as unrealistic

(Nikkei, October 8)

- A recent Nikkei survey of 100 CEOs found that over 80% of business leaders view the govt’s wind power targets as difficult to achieve, citing soaring material and labor costs that make projects unprofitable.

- CONTEXT: Japan aims to raise wind power’s share of electricity from 1% to 4–8% by 2040. But the exit of a Mitsubishi-led group from offshore wind projects in Chiba and Akita has cast doubts on the sector’s viability.

In response, the govt is revising its system to allow cost pass-through and longer project terms, but transmission grid connections and feasibility remain a concern.

- Amid rising electricity demand from AI and data centers, nuclear energy is gaining renewed support, with 87% of executives backing new or next-gen reactors, a sharp rise from the previous year.

- Despite that, nearly 40% still support expanding offshore wind, emphasizing the need for a balanced energy mix. Executives also stressed that large-scale renewable projects require stronger national leadership, funding, and public acceptance.

Coexistence tax approved for solar and wind farms

(Government statement, October 6)

- The Ministry of Internal Affairs and Communications approved Aomori Pref’s proposal for a “coexistence tax” on solar and wind facilities with a production capacity exceeding 2 MW and 0.5 MW, respectively.

- The tax applies as follows:

- Protected / Conservation area (solar): ¥410/ kW

- Protected / Conservation area (wind): ¥1,990/ kW

- Adjustment area (solar): ¥110/ kW

- Adjustment area (wind): ¥300/ kW

- The tax will be reviewed five years after implementation.

- CONTEXT: “Protected / conservation area” is a location where renewable energy facility construction is strongly restricted due to biodiversity protection (national parks, natural reserves, etc); and a special construction permit from METI or the MoE is required. An “adjustment area” is where renewable energy facility building is less restricted, but still requires a special construction permit from the prefecture.

Pasco introduces Japan’s first floating lidar for offshore wind

(Company statement, October 8)

- Pasco, a geospatial services provider, introduced Japan’s first floating observation system for monitoring both wind conditions and fish schools. In September, the firm began surveys off the coast of Wajima City, Ishikawa Pref.

- The new floating lidar system combines wind and ocean condition measurement with fish monitoring in a single buoybased platform.

- The collected data will help energy developers make decisions and support consensus-building with fisheries and other local stakeholders.

- TAKEAWAY: For offshore wind projects more than 10 km from the coast, wind condition surveys using floating lidar are essential to assess project feasibility. Traditionally, wind, ocean, and fish surveys required separate equipment. By integrating these functions into one system, Pasco’s approach improves survey efficiency and could help reduce costs.

MHI subsidiary to supply ORC equipment for U.S. geothermal project

(Company statement, October 2)

- Turboden, an Italian subsidiary of MHI, will supply three additional Organic Rankine Cycle (ORC) units to Fervo Energy for the second phase of its geothermal power project in Utah, USA.

- Each ORC unit has a 40 MW capacity, bringing the project’s total to 300 MW when combined with the units already delivered for Phase 1.

- ORC technology enables efficient power generation using heat from low- to mid-depth geothermal resources.

- Phase 1 is expected to be completed in 2026; Phase 2 in 2028.

JOGMEC releases geothermal project granted subsidies

(Company statement, October 8)

- JOGMEC released results for the FY2025 geothermal power resource subsidies.

- Yunuma-Atosanupuri Geothermal Resource Survey Project (Teshikaga, Kawakami District, Hokkaido) was chosen.

- The project is subsidized by the city and Teshikaga Geothermal Promotion Corp.

NEWS: NUCLEAR ENERGY

Chubu Electric began dismantling reactor at Hamaoka NPP Unit 1

(Nikkei, October 7)

- Chubu Electric began dismantling the reactor at Hamaoka NPP Unit 1, the second time in Japan that a commercial reactor entered this stage of decommissioning.

- The work to cut up and remove the reactor pressure vessel and containment structure will run until 2035. The entire decommissioning, including the reactor building, will finish by 2042.

- CONTEXT: Unit 1 went offline in 2009. Chubu Electric is decommissioning Unit 2, work on which began in March. The deadline for dismantling and decommissioning Units 1-2 is the same.

TEPCO to provide ¥100 billion to Niigata Pref for Kashiwazaki-Kariwa restart

(Asahi Shimbun, Oct 8)

- TEPCO will provide about ¥100 billion to Niigata Pref as a regional contribution measure, aiming to gain support for restarting Kashiwazaki-Kariwa NPP.

- The money will go into a prefectural fund for local development and will come from profits generated by the plant once it is operational. TEPCO will discuss payment details and usage with the prefecture.

- CONTEXT: Restarting the NPP is crucial for TEPCO’s financial recovery, as it still faces onerous costs from the Fukushima accident cleanup and compensation. Yet, local consent is essential, and the governor’s approval is the final hurdle.

- SIDE DEVELOPMENT:

- Mayor comments on recent survey for Kashiwazaki Kariwa’s restart

- (Nikkei, October 7)

- Kashiwazaki’s mayor said TEPCO hasn’t dispelled public “anxiety and distrust.” On Oct 16, TEPCO’s president will explain safety measures to the regional assembly.

- The mayor’s words follow a survey showing 69% of residents worry about TEPCO operating the plant.

- The mayor wants TEPCO to clarify “determination and specific measures” and criticized the govt’s definition of “local consent” for a restart as insufficient.

- He said more discussion is needed before the city agrees to Tokyo’s request to restart.

- TAKEAWAY: As we have noted in the past, it would likely have been easier for the restart to occur if the entity in charge was not called TEPCO and linked to the original Fukushima disaster. No matter how much the utility promises in local funds or claims that it is ready technically, local stakeholders are clearly divided. Arguably, TEPCO would benefit from being allied with another, more ‘respectable’ entity to run this NPP. For now, we expect these local procedures to drag well into 2026.

KEPCO delays completion of spent fuel’s interim storage at Takahama NPP

(Nikkei, October 11)

- KEPCO said the completion of the dry storage for spent nuclear fuel at its Takahama NPP is now slated for 2028, a delay of one year.

- The delay is due to a slow safety review of the Japan Nuclear Fuel reprocessing plant under construction in Rokkasho.

- CONTEXT: KEPCO planned to start work this year and complete it in 2027, but both deadlines are now pushed three years forward. The facility transfers spent fuel from the plant’s storage pools to support smoother fuel shipments.

NEWS: TRADITIONAL FUELS

Japan reassures Australia over gas exports

(Financial Review, October 8)

- Japan’s ambassador, Suzuki Kazuhiro, reassured Australians that Japan’s resale of LNG is minimal. He said it’s not a major cause of energy shortages on Australia’s east coast, adding that when such resales do occur, they help decarbonize coal-reliant economies in SE Asia.

- The ambassador welcomed Australia’s extension of the North West Shelf gas project, a positive signal to Japanese investors about Australia’s long-term commitment to gas.

- Australian manufacturers, led by Bluescope Steel, are calling for state intervention in the gas market. The goal is to secure lower prices for domestic users.

- Bluescope’s CEO argued for redirecting uncontracted gas to the local market and creating a gas reserve.

- TAKEAWAY: Australia is Japan’s largest source of LNG, covering almost 40% of its total imports in FY2024. While Australia is relatively close to Japan, without shipping chokepoints, and is politically friendly, importing LNG from Australia has downsides. Analysts say Australia’s longer-term capacity to stay an LNG exporter is doubtful. For a while, Eastern Australia ceased exports, experiencing energy shortages because of aging gas fields and limited pipeline capacity. Moreover, the local industry faces increasing costs and more stringent regulations. In the meantime, Japanese companies have intensified LNG trading, a tendency that has alarmed some Australians, who see it as profiteering. Hence, Suzuki decided to make the reassurance.

Osaka Gas explains its LNG strategy

(Government statement, October 7)

- Osaka Gas seeks diversified LNG sources – from Australia, Malaysia, U.S., and Russia. The firm has a fleet of 10 long-term chartered LNG carriers for transport.

- The firm covers most of its needs with long-term contracts to manage price volatility. It uses spot purchases and swaps to optimize costs and respond to demand flux.

- The company presented the Asahi Kasei Project – to convert a coal-fired power plant to gas that involved building a new LNG terminal and pipeline.

- Another is the Daio Paper Project, requiring fuel conversion for a paper mill, as well as building an LNG satellite station and pipeline.

- SIDE DEVELOPMENT:

- Osaka Gas plans to enter India’s city gas market

- (Reuters, October 8)

- Osaka Gas plans to enter India’s city gas market through a JV with a foreign firm.

- OG aims to supply natural gas to vehicles, homes, and industries in India using trucks and pipelines.

- If successful, OG would be the first Japanese company to enter this market.

- CONTEXT: India is promoting natural gas use, offering exclusive marketing rights and infrastructure ownership to operators for a limited time.

Sewage-based biomass plant opens in Ehime Pref

(Company statement, October 1)

- Nippon Steel Engineering, Nippon Steel Environmental & Energy Services, Yonden and Tesco launched a sewage sludge solid fuel facility at Western Purification Center in Matsuyama (Ehime Pref).

- It will convert sludge from 4 purification centers into fuel for biomass production.

NEWS: CARBON CAPTURE & SYNTHETIC FUELS

ANRE moves forward in designing Generation Benchmark for power sector

(Government statement, October 10)

- ANRE is designing a “Generation Benchmark” for the power sector, a key part of its emissions trading scheme (GX-ETS). This will set a standard for CO2 emissions intensity (t-CO2 per kWh) for power generators.

- The initial focus is on fossil-fuel power plants. The plan is to start with fuel-specific benchmarks (coal, LNG, oil), followed by a transition to a single benchmark for all thermal power by 2033.

- There is debate on whether to group power plants by size and efficiency for fairer comparison. Cogeneration (heat and power) will be part of the scope. But only the emissions associated with electricity generation will fall under this benchmark.

- Power from non-fossil fuels like hydrogen, ammonia, and biomass co-fired with fossil fuels will fall under separate activity data.

- The final WG meeting for this fiscal year will present specific benchmark levels. In autumn, it will submit the proposal to a higher-level subcommittee to be finalized.

- TAKEAWAY: Japan is accelerating the GX-ETS design, aiming for an outline by year-end. A central design choice is the initial use of fuel-specific benchmarks. This is to prevent undue burden on coal plants and ensure grid stability, while acknowledging their higher emissions. Still, the competitive advantages under this initial system could well become entrenched since the plan entails a transition from the fuel-specific benchmarks to a single average for all thermal power.

METI explains rules and regulations for CCS storage projects

(Government statement, October 8)

- METI set up a new working group for regulations in four critical areas in carbon capture and storage: 1) Monitoring leak prevention; 2) Site closure and project termination; 3) Financial security; and 4) Business Rules.

- Under the framework, the private operator injects CO2, conducts monitoring, and other measures. After injection stops, the operator must submit a Site Closure Plan for ministerial approval. It also has to plug wells, remove surface facilities, and ensure well integrity to prevent leakage.

- After closure work, there’s a post-closure monitoring period. Upon proving the site is stable, the operator can apply for project termination. Once approved, responsibility for long-term monitoring and management transfers to JOGMEC.

- To transfer the site responsibility to JOGMEC, an operator must prove long-term stability – that CO2 is stored according to standards based on monitoring data and predictive models.

- Operators must secure funds during operation to cover future closure costs.

Firms aim to commercialize MOFs after Kitagawa’s Nobel win

(Nikkei, October 9)

- Companies are racing to commercialize metal-organic frameworks (MOFs), originally developed by Kitagawa Susumu who won the 2025 Nobel Prize for Chemistry.

- MOFs can capture and release CO2 with minimal energy, making them a key decarbonization technology.

- Resonac Holdings and Crasus Chemical aim to cut CO2 separation costs to ¥2,000/ ton by 2030, with pilot tests by 2028 and commercialization by 2035.

- Osaka Gas is developing direct air capture (DAC) using MOFs to produce e-methane, targeting 50– 90% clean gas by 2050.

- Nippon Fusso uses MOFs for corrosion-resistant coatings made by startup Atomis.

JGC Holdings and SLB Capturi sign MoU on CO2 capture

(Company statement, October 10)

- JGC Holdings signed a MoU with SLB Capturi (Norway) and its parent company SLB (U.S) to collaborate on post-combustion CO2 capture technologies.

- JGC, with prior experience in CCS projects in Algeria and Australia, will offer consulting services covering research, simulation, and risk assessment.

- The collaboration will target Asia-Pacific and Middle East markets – regions with rising CCS demand.

Four companies join “Fry to Fly” to produce cooking-oil based SAF

(Company statement, October 1)

- Daiichi Kosho, Revo International, Saffaire Sky Energy and JGC signed a MoU on the “Fry to Fly” project that aims to convert used cooking oil (UCO) into sustainable aviation fuel (SAF).

- Daiichi Kosho will source UCO from its 224 karaoke venues and 143 eateries to Revo International, which will send it to SAF production sites operated by Saffaire Sky Energy. JGC will oversee overall operations.

- TAKEAWAY: In 2021, Japan set a target to replace 10% of jet fuel consumption on domestic flights with SAF by 2030. In April 2025, the Sakai manufacturing site became the first to produce SAF in Japan, supplying JAL and ANA with around 30,000 kL per year. As for imported SAF, Idemitsu began a trial plantation of non-edible oilseed tree crops in Australia; the oil extracted will serve as a feedstock for SAF production.

- SIDE DEVELOPMENT:

- Sumitomo Forestry joins “Mori Sora” to produce bioethanol-based SAF

- (Company statement, October 7)

- Sumitomo Forestry signed an MoU to expand domestic bioethanol production from wood chips under the “Mori Sora” project.

- CONTEXT: The project was launched in 2023 by Sumitomo Shoji, Green Earth Institute, and Nippon Paper. Its main goal is a stable bioethanol supply for various decarbonization uses. In March 2025, the scope was extended to include SAF.

Beisia, Yoshikawa Oils and Tanaka Iron collaborate for BAF and SAF

(Company statement, October 10)

- Beisia, Yoshikawa Oils and Tanaka Iron Works will jointly make SAF and biomass fuel for asphalt production from used cooking oil (UCO).

- Yoshikawa Oils will oversee recycling and purification and use the oil as: o SAF, to be processed at ENEOS’s Wakayama plant, which plans a future production capacity of 400,000 kL/ year, and

- Biomass fuel, to be used at Tanaka Iron Works’ plant to produce asphalt.

ITOCHU supplies low-carbon methanol fuel to NYK Line

(Company statement, September 30)

- ITOCHU supplied low-carbon methanol fuel to Green Future, a methanol dual-fuel bulk carrier chartered by NYK.

- This was done via ship-to-ship bunkering at the Port of Ulsan, South Korea.

- They produced the fuel from biomass-derived materials. It should emit fewer GHGs across its life cycle than conventional fuels.

ANALYSIS

BY MAGDALENA OSUMI

Likely Next PM Takaichi’s Energy Ambitions Collide with Political Uncertainty

On October 4, Japan’s ruling Liberal Democratic Party (LDP) selected 64-year old Takaichi Sanae as its leader, making her the likely candidate to become the nation’s first female prime minister. This marks a historic moment for a country yet to promote women to the highest levels of political power.

Gender issues aside, what does this mean for the energy sector? Given energy’s central role in Japan’s digital modernization, and Takaichi’s own keen interest in the topic, we expect energy policy to be a major focus under her anticipated premiership. She has often spoken about the need for the energy sector to reflect national security and industrial concerns.

In practice, Takaichi is likely to deliver nuanced support for the renewables sector – one that places emphasis on home-grown tech and regional integration. She’s also likely to prove a staunch nuclear power backer, contrasting with the ambivalence of outgoing PM Ishiba. That pro-nuclear stance is further assured via Takaichi’s close ties to veteran power brokers such as Aso Taro, but will surely bump against regional resistance to reactor restarts.

How much of Takaichi’s grand energy vision can filter into reality is unclear. The LDP holds only a minority of seats in the Diet, and Takaichi will need to rely on other parties’ support to enact policies, especially after coalition partner Komeito announced its exit from the 26-year arrangement. This also makes Takaichi, should she become PM, even more reliant on support from elders like Aso, who helped her secure the leadership win.

Overall, a Takaichi government is unlikely to result in significant departures from current energy policy.

Past stances on energy

Takaichi’s past stance on energy serves as an indicator for future policies. As a former

Minister of Internal Affairs and Communications, and Minister of State for Science and Technology Policy, Takaichi consistently advocated for a shift toward decentralized, resilient energy systems to address vulnerability to natural disasters and demographic decline.

At a conference a decade ago, during a dialogue with Professor Kashiwagi Takao of the Tokyo Institute of Technology, Takaichi spoke of the potential of distributed energy systems to realize the “Local Abenomics” agenda – a localized iteration of former Prime Minister Abe Shinzo’s economic revitalization program. This is based on the idea that self-sufficient energy infrastructures can spur regional economies by fostering resilience against major shocks.

Takaichi’s historical advocacy for energy efficiency infuses this framework with a nationalist inflection, interpreted here as a strategic emphasis on bolstering energy facilities’ robustness against extreme weather and resource inefficiencies. Such resilience-oriented nationalism is likely to manifest itself as support for revitalizing aging hydroelectric facilities, advancing next-generation geothermal tech, and promoting perovskite solar cells (PSCs).

Takaichi has already stressed her support for next-generation PSCs, which is touted as Japan’s next big breakthrough in clean energy. At the same time, she criticized the expansion of large-scale solar farms due to their impact on neighboring residential areas and biodiversity. Her approach supports recent trends favoring smaller, decentralized solar projects that minimize environmental and social disruption.

This chimes well with the direction of Japan’s next five-year infrastructure plan, administered by the Ministry of Land, Infrastructure, Transport and Tourism (MLIT). Oriented toward resilience and decarbonization, this plan is based on four principal objectives: the cultivation of sustainable local communities; the fortification of economic and societal structures via resilient infrastructure; the progression toward a green, decarbonized society; and the reinforcement of foundational support for infrastructure development.

Photo credit: Cabinet Public Affairs Office via

Creative Commons/Openverse

Nuclear buff

Following her LDP leadership victory, some media forecast that Takaichi would prioritize nuclear power as a key means of reducing emissions.

At past conferences, Takaichi has demonstrated strong nuclear expertise, engaging with specifics of reactor design, safety enhancements, and fuel cycle efficiencies. This suggests she would favor a policy framework that prioritizes innovation in small modular reactors (SMRs) and advanced systems, which would alleviate the scalability issues that plague traditional nuclear sites.

Likewise, she has in the past voiced support for Mitsubishi Heavy Industries’ SRZ-1200 advanced light-water reactor, Takaichi Sanae which revealed a nuanced appreciation for nuclear tech.

During her time as Minister of State for Science and Technology Policy, she convened the Cabinet Office Expert Panel on Fusion Strategy in 2021, advocating for coordinated industrialization of Japan’s fusion capabilities. This initiative spotlighted the JT-60SA experimental reactor, a collaborative endeavor symbolizing Japan’s leadership in plasma physics and magnetic confinement fusion.

Takaichi’s endorsements reflect a forward-looking stance on energy tech, envisioning fusion as a paradigm-shifting energy source capable of delivering baseload power with minimal environmental impact.

However, these nuclear innovations will not yield electricity today and Takaichi’s most urgent task as PM would be to continue pushing forward the restart of existing nuclear power facilities. This is an issue that bested even PMs with high voter support and it will be a test of Takaichi’s diplomacy.

Trump endorsement

Takaichi has already surrounded herself with veteran allies. She appointed former Prime Minister Aso as LDP vice president, while filling other top positions with conservative figures including Suzuki Shunichi, Arimura Haruko, Kobayashi Takayuki, and Furuya Keiji – many of whom belong to the Aso faction, the LDP’s last remaining intraparty faction.

By relying on established networks, Takaichi signaled both loyalty to party elders and a continuation of traditional conservative priorities. Together, this lineup underscores that even amid promises of economic relief, Takaichi’s leadership will likely emphasize conservative social and political values.

Praised last week by President Trump in one of his social media posts, such an endorsement indicates that Takaichi’s candidacy has Washington’s prior approval and that her policies will accord with the Trump White House plans for the U.S.–Japan relations, such as boosting LNG deals and joint infrastructure projects, such as Alaska LNG.

LNG export deals play a central role in Trump’s plans to shrink U.S. trade deficits with Japan, South Korea, Taiwan and the EU.

Not yet the nation’s leader

Still, Takaichi’s path to national leadership is far from assured. On Friday, Oct 10, Komeito, the junior coalition partner of the LDP said it will end the arrangement citing policy differences.

An extraordinary Diet session to elect the next prime minister, initially scheduled for October 15 has already been delayed to allow more time for coalition talks. The LDP will now engage with other parties to shore up its base and get enough votes for the Diet to confirm Takaichi as prime minister. The main opposition party, the CDP, however, sees a chance to form its own ruling coalition.

The timing could not have been worse given Trump’s announced intentions to visit Japan from October 27 to 29. The new Japanese prime minister will also need to travel to South Korea to attend the Asia-Pacific Economic Cooperation (APEC) forum at the end of the month, with Chinese President Xi Jinping among the expected attendees.

As PM, Takaichi would face the challenge of balancing sensitive regional diplomacy with the views of her conservative backers at home. Her core supporters include groups such as the Shinto Association of Spiritual Leadership and long-standing allies like Furuya Keiji.

With the LDP’s minority position and pressure from all sides, even ascending the post of PM may leave Takaichi very little room to maneuver. As such, she may end up speaking about energy policies more than enacting them.

ANALYSIS

BY MAGDALENA OSUMI

BESS Market Booming as More Non-Energy Firms Enter the Sector

With the rapid expansion of renewable energy, battery storage is moving from a supportive nche technology to one of its central drivers. Once seen as a backup tool, battery energy storage systems (BESS) are now indispensable to balancing Japan’s energy transition, ensuring stability, and fostering greater renewable penetration.

While recent energy headlines focus on the retreat of Mitsubishi Corp from offshore wind projects, a quieter but equally consequential shift is happening — A surge in applications to connect BESS projects to the national grid. This trend reveals both the urgency of addressing Japan’s grid limitations and the growing recognition of storage as a backbone of the decarbonized energy system envisioned in government plans.

Japan’s revised 7th Basic Energy Plan, released in early 2025, envisions renewables contributing up to 50% of the national energy mix by 2040. Much of this growth is expected to come from solar and wind, both onshore and offshore. Yet Japan’s grid infrastructure remains ill-prepared for such a transformation.

Curtailments of solar power are already common, and large-scale transmission upgrades are not expected until the 2040s. In this context, the immediate need for flexible, deployable storage is driving a short-term boom in BESS projects, with the government expecting that it will lead to around 21 GW of installations by 2040.

Whether this momentum will sustain at the breakneck speed of the BESS grid applications seen today – and amid changing electricity market structures and regulations – is difficult to express in empirical terms. What is clear, however, is that storage is no longer an afterthought. It’s an essential pillar of Japan’s energy future.

Growing fast, but how far?

As of June, Japan had applications for 143 GW of BESS capacity — more than double the total from just a year earlier. Applications surged by 30 GW in a single quarter, underscoring both developer enthusiasm and the urgency of grid flexibility.

One mid-sized international solar developer exploring the BESS sector told Japan NRG they alone had filed more than 120 grid-connected applications – the vast majority for small-scale projects in the Tokyo region.

Yet projects are not the same as operating capacity. The reality on the ground is that energy storage in Japan is starting from a very small base. Japan NRG data and calculations indicate that commissioned capacity stood at only about 560 MW as of July 2025.

As such, what will actually be delivered onto the grid over the rest of the decade is more modest. The government forecasts an initial 6–8 GW of operating BESS by 2030; this could rise to above 20 GW a decade later. These forecasts, however, and especially the 2030 number, were derived largely from government assumptions that a portion of grid connection applications will translate into operating BESS. But with application numbers rising almost exponentially, METI officials admit that this may no longer be a reliable approach.

The problem with the sprint to connect is that the application criteria are fairly open and do not involve large capital outlays. METI recently noted in a sector update that it now sees that many project owners are applying for connection to sites already in use or unavailable for lease. Officials are urging developers to take more time and care in their due diligence.

With many firms applying for over 100 projects at once, the government might cap the number of allowed grid submissions. It has become clear that a notable portion of the applications are essentially middlemen traders, seeking a quick resale of the project after securing grid access with no intention of completing it themselves.

This trend leads to a conclusion that official estimates for BESS development may be a stretch, based on projects that are still at an early stage. The likelihood is that less than 10% of grid-seeking capacity will materialize. The exact numbers will depend on the evolution of the regional grids, financing mechanisms, and revenue models.

Government push, incentives and uncertainties

Policy backing from METI has been a major driver of the BESS market. The ministry has three priorities as it supports the emergence of this sector: stabilizing electricity prices, improving market rules, and streamlining the grid connection process. To meet these objectives, it has leaned heavily on subsidy schemes, the most prominent of which is the Long-Term Decarbonized Power Sources Auction (LTDA).

The LTDA has been both a catalyst and a point of contention. The Round 1 auctions set attractive prices and spurred early enthusiasm among BESS developers. But subsequent rounds have faced criticism: Round 2 prices were seen as too low to make large-scale projects viable, while Round 3, to be held in early 2026, has set conditions that make Lithium-ion batteries less economical compared with other resources.

Other BESS subsidies on offer in Japan, such as the Sustainable Investment Initiative (SII), cover roughly half of the capital expenditures but come with restrictive conditions, including requirements that favor domestic battery manufacturers.

This patchwork of incentives has created a mixed investment climate: supportive enough to generate momentum, but fragmented enough to leave many developers cautious.

Balancing scale and speed

Developers are pursuing a range of strategies shaped by project size, interconnection timelines, and financing structures. Early movers, particularly those bringing highvoltage (HV) projects online before 2028, seem well-positioned to capture outsized profits. These smaller projects, typically 2–8 MW in scale, can reach commercial operation within 12 to 18 months, providing quick cash flow.

By contrast, extra-high-voltage (EHV) projects, often exceeding 50 MW, take up to five years to interconnect. While slower to mature, they offer greater scale and long-term positioning. That may be one reason that some developers are opting for mixed portfolios, balancing smaller HV projects with EHV ones to navigate upcoming policy shifts and market uncertainties.

Whichever size or model is chosen, nearly all market players say they face challenges in terms of grid allocation and technical constraints, land acquisition, and the unwritten rules around subsidy eligibility.

Many developers are adapting by scaling project sizes to align with charging limits and interconnection hurdles. This may result in projects being split into stages to accommodate on-the-ground conditions while retaining growth optionality.

Banks warm up, funds push in

Financing remains a challenge but is gradually improving as lenders and investors gain confidence in the sector. Japanese banks such as MUFG and Orix have started to participate, alongside foreign players like Société Générale. At this stage, however, financing options are still limited, partly due to the lack of know-how, directly linked to the market’s immaturity.

Foreign private equity and infrastructure funds are also showing an appetite for BESS. These investors typically prefer portfolios rather than single-asset deals, making aggregation an attractive strategy for developers seeking capital. Offshore financing is another emerging avenue, particularly as global players enter Japan’s market.

Japan’s battery storage sector is in a pivotal moment. The current boom reflects both the urgency of integrating renewables and the systemic challenges of a grid built for largely thermal baseload.

Policies and subsidies have primed the market for rapid growth. However, longer-term sustainability will depend on smarter market rules, better revenue models, and continued investor confidence.

If Japan succeeds in navigating these challenges, battery energy storage will not just be a stopgap solution, it will be a cornerstone of the country’s clean energy mix.

ASIA ENERGY REVIEW

BY JOHN VAROLI

A brief overview of the region’s main energy events from the past week

Australia / Coal power

Queensland will keep its state-owned coal plants running for up to a decade longer than previous plans, which means at least until 2046.

Australia / Hydrogen

Round two of the Hydrogen Headstart program launched. It will provide up to $2 billion in revenue support for large-scale renewable hydrogen projects.

Australia / Renewables

The Capacity Investment Scheme awarded 20 successful projects that will deliver 6.6 GW of new renewable generation capacity by 2030. The latest round in the National Electricity Market attracted 84 bids totaling 25.6 GW, more than four times the 6 GW target.

China / Offshore wind

Rystad Energy said new global offshore wind capacity will reach 16 GW by year’s end, with two thirds developed in China. By 2030, China’s offshore wind projects will have 45% of the world’s cumulative capacity as more countries build installations.

China / Offshore wind

China’s Ming Yang Smart Energy will invest up to 1.5 billion British pounds to build a wind turbine manufacturing facility in Scotland.

China / Oil

China is rapidly building oil reserve sites as part of a campaign to boost crude stockpiles. State oil companies such as Sinopec and CNOOC will add at least 169 million barrels of storage across 11 sites during 2025 and 2026.

India / Electricity

India plans to open up its retail electricity market for private companies nationwide, ending the dominance of state-run distributors in most states.

Indonesia / Hydropower

PT Arkora Hydro Tbk is accelerating 200 MW of projects while embedding AI into plant operations. Arkora operates 3 hydropower plants with a total 27.4 MW capacity.

Taiwan / Energy security

The WSJ reports Chinese military exercises have sparked an urgent effort in Taipei and the U.S.

to address a critical vulnerability: The island is mostly dependent on imported fuel.

Taiwan / Offshore wind

Installation of all 37 turbines at the 532 MW Hai Long 2 Offshore Wind Farm was completed. And installation of 36 turbines for Hai Long 3 will be completed next year.

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Hulic Ochanomizu Bldg. 3F, 2-3-11, Surugadai, Kanda, Chiyoda-ku, Tokyo, Japan, 1010062.