WEEKLY

February 24, 2026

ANALYSIS

CAN JAPAN BUILD A NATIONAL CCS INDUSTRY?

- The success of Japan’s decarbonization efforts depends on innovative technologies such as Carbon Capture and Storage (CCS), as well as hydrogen/ ammonia co-firing.

- While the CCS legal and logistical framework is nearly completed, the economic engine – carbon pricing – is underpowered.

FINDING THE RIGHT BALANCE: HOW JAPAN IS FINETUNING ITS POWER ADJUSTMENT MARKET

- Japan’s electricity balancing market is entering a new phase. Starting April, three changes will take effect that are a recalibration of how flexibility is priced, forecast and financed.

- They also offer a glimpse of energy planners’ vision: restraining price surges while preserving incentives for fast-response capacity.

ASIA PACIFIC REVIEW

This column provides a brief overview of the region’s main energy events from the past week

NEWS

- Trump says first projects agreed under $550 bln U.S.–Japan investment deal

- Sojitz to expand rare earth imports from Australia, adding samarium

- Deal signed to promote sites for data centers in Aomori Pref

- OCCTO seeks to improve utilization rates of Kansai-Shikoku interconnection

- Marubeni agrees with Hyosung and Skeleton for next-gen power grid stabilization

- OCCTO again orders power transfer amid tight supply-demand in Hokkaido

- Govt conducts pre-screening for hydrogen and ammonia projects with 4th LTDA

- Hydrogen station network shrinks as FCV sales fall

- Companies shift focus to small-scale solar after large-scale support phase-out

- Equinix signs PPA with ENEOS Renewable Energy

- PowerX agrees with IIJ on BESS for data centers

WIND POWER AND OTHER RENEWABLES

- EES to build Japan’s first blade training center

- Matsumae wind project files environmental report

- KEPCO’s Mori appointed chairman of FEPC

- Regular rule change could speed up reactor restarts

- TEPCO begins power transmission from Kashiwazaki-Kariwa Unit 6

- INPEX’s Abadi LNG faces cost surge

- Tokyo Gas’s U.S. shale subsidiary to expand inhouse drilling operations

CARBON CAPTURE & SYNTHETIC FUELS

- Big utilities lodge comments warning about impact of GX-ETS on power prices, investments

- MHI succeeds in liquid synthetic fuels production

- NYK Line operates low-carbon methanol carrier

EVENTS

Feb 24-26 ICEF Japan Roadshow 2026

@ Keio Plaza Hotel, Tokyo

ICEF – Korea Roadshow 2026

@ Seoul, Korea

March 5 Nepal – First Parliamentary Election

March 11 “REVision 2026” symposium by

Renewable Energy Institute @ Tokyo

Mar 17-19 Smart Energy Week Spring 2026 / H2& FC EXPO / PV EXPO / Battery Japan / Smart Grid EXPO / Wind Expo / Biomass Expo / Zero-E Thermal Expo /Decarbonization EXPO 2026 @ Tokyo Big Sight

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Chief Editor)

John Varoli (Senior Editor, Americas)

Kyoko Fukuda (Data, Events)

Magdalena Osumi (Renewables & Storage)

Filippo Pedretti (Thermal, CCS, Nuclear)

Tetsuji Tomita (Power Market, Hydrogen)

Aglaé Bange (Renewables and Biomass)

George Hoffman (Sales, Business Development)

Tim Young (Design)

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

NEWS: GENERAL OUTLOOK AND TRENDS

Trump says first projects agreed under $550 bln U.S.–Japan investment deal

(NHK, WSJ, February 18)

- President Trump launched the first projects under last summer’s $550 billion U.S.–Japan trade and investment deal, according to which Japan must commit to finance projects in strategic U.S. sectors.

- Initial projects include a 9.2 GW gas-fired power plant in Ohio, a deepwater crude oil export facility in the Gulf of Mexico, and a plant in Georgia to make synthetic industrial diamonds used in semiconductors. The three projects represent a $36 billion commitment, said Trump.

- Commerce Secretary Lutnick said Japan will provide capital, with profits split 50–50 until Japan recoups its principal and interest.

- CONTEXT: The investment framework functions more like a loan fund, and was agreed to in exchange for the U.S. lowering tariffs on Japanese goods to 15%.

- TAKEAWAY: PM Takaichi visits the U.S. next month and needs these agreements to enjoy a productive and positive conversation with Trump. But days before Trump posted this news, METI minister Akazawa said the two sides had yet to resolve several major issues. Another issue will be how quickly Japan must send the money and how much. As this is a state investment and not private, internal checks and budget processes can take a long time – something Trump has little patience for.

- SIDE DEVELOPMENT:

- U.S. reveals projects under deal with Japan

- (Government statement, February 17)

- The U.S. Dept of Commerce outlined projects in a trade agreement with Japan, highlighting a $33 billion natural gas facility in Ohio (9.2 GW capacity), the world’s largest natural gas generation project.

- Plans include a $2.1 billion deepwater terminal in Texas (Gulf Coast) to bolster crude oil exports that could generate $20–$30 billion in annual U.S. exports.

- A third project is a $600 million synthetic diamond plant in Georgia, aiming to secure critical raw materials for the semiconductor and automotive sectors.

- CONTEXT: Toshiba, Hitachi and Mitsubishi Electric could provide equipment to the gas facility. Nippon Steel, JFE Steel and MOL could take part in the Texas terminal.

- SIDE DEVELOPMENT:

- Japan to keep investment pledge to U.S. after tariff ruling

- (Jiji Press, February 22)

- Despite the U.S. Supreme Court ruling against President Trump’s reciprocal tariffs, Japan is expected to maintain its $550 billion investment and loan pledge to the U.S.

- The Japanese government is closely monitoring whether U.S. tariff policy-related uncertainties will resurface following the U.S. top court ruling. Tokyo has asked Washington to ensure that the court ruling would not affect Japanese companies.

PM Takaichi introduces multi-year budget for growth and crisis investments

(Jiji Press, Government statement, February 17 and 20)

- In her first policy speech to the Diet, PM Takaichi proposed a multi-year, separately managed budget framework for growth and crisis-management investments.

- Takaichi wants to shift away from reliance on annual supplementary budgets, instead securing key funds in initial budgets or long-term investment funds to improve predictability for businesses and investors, and encourage R&D and investment.

- Takaichi also wants to concentrate all budgeting in the main budgetary process from FY2027 and stop governments from relying on supplementary budgets.

- Govt officials say this is part of an effort to build fiscal predictability around strategic areas such as AI, semiconductors, energy security and economic security – following previous multi-year frameworks for green transformation and technology sectors.

- In March, the govt will outline a public–private investment roadmap detailing priority sectors, investment timing, and targets. In energy, Takaichi reiterated her support for nuclear restarts and next-gen nuclear reactors, fusion, perovskite solar cells and next-gen geothermal tech.

- Takaichi also emphasizes “responsible fiscal expansion,” pledging to contain state debt growth within the pace of economic growth to reduce the debt-to-GDP ratio.

- TAKEAWAY: The multi-year framework is a significant shift that seeks to bolster Japan’s economic security and global competitiveness. It also allows Takaichi to increase spending early on to commit resources to her 17 key sectors and relevant infrastructure. The Rapidus cutting-edge semiconductor project in Hokkaido is among those likely to benefit. A new subsea power gridline to link the Tokyo area with Hokkaido is another. Still, Takaichi will need to show how state spending will ease off in the future. She promised to unveil a state investment roadmap to show how sectors such as energy and technology will benefit.

Sojitz to expand rare earth imports from Australia, adding samarium

(Nikkei, February 16)

- Sojitz will expand imports of Australian rare earths, adding samarium in April, and increasing the number of medium and heavy rare earth elements handled from two to as many as six by mid-2027.

- Materials will be supplied by Lynas Rare Earths, in which Sojitz and JOGMEC have invested, with ore mined in Australia and processed at a new facility in Malaysia.

- Samarium, used in permanent magnets for fighter jets and in nuclear reactors, will be produced commercially outside China for the first time. Lynas also plans to begin producing gadolinium and increase output of dysprosium and terbium, critical for EV motors.

- The Malaysian facility aims to reach a processing capacity of 5,000 tons of ore per year by 2028, with additional imports potentially including yttrium.

- CONTEXT: Sojitz invested in Lynas in 2011 and expanded that in 2023 to secure heavy rare earth supply. Supply of dysprosium and terbium started in October 2025.

- TAKEAWAY: This is the next step in Japan’s effort to diversify rare earths supply that is now almost entirely sourced from China. While Australian material carries higher production costs due to lower ore concentrations and processing complexity, backing from JOGMEC and coordination with allies could help stabilize non-Chinese supply chains for critical minerals.

- SIDE DEVELOPMENT:

- Mitsui Mining & Smelting to establish rare earth R&D hub in Kyushu

- (Nikkei, February 14)

- Mitsui Mining & Smelting set up the Kyushu Advanced Materials Development Center in Fukuoka Pref, investing ¥10 billion in a new facility.

- The center will pursue refining technologies for rare earths derived from both conventional ores and seabed mud collected near Minamitorishima.

- The company will study which of the 17 rare earth elements to prioritize, target end-use applications, potential refining locations, etc.

- TAKEAWAY: With the Kyushu hub Mitsui Mining aims to capitalize on Japan’s plans to develop a rare earth value chain. If Minamitorishima’s seabed resources prove commercially viable – and this is likely the real genesis of this R&D hub – Mitsui Mining will become vital to energy security. So far, academics have pushed Minamitorishima, with little participation from Japanese companies. Mitsui Mining would be the first firm associated with it.

- SIDE DEVELOPMENT:

- Takaichi says U.S. welcome to join Japan’s rare earths seabed mining project

- (Mainichi Shimbun, February 9)

- PM Takaichi seeks to cooperate with the U.S. on rare earths off Minamitorishima, a seabed mining project.

- “We want to get the U.S. firmly involved and speed this up,” she stated.

- The issue may be discussed at the Japan-U.S. summit on March 19.

Agreement signed to promote sites for data centers in Aomori Pref

(Government statement, February 12)

- Aomori Pref, Tohoku Electric, NTT East, Development Bank of Japan and Shin-Mutsu-Ogawara agreed to work on attracting data centers (DCs) to Aomori.

- As DC investment and electricity demand are expected to grow rapidly, Aomori aims to leverage its advantages for DC sites – its potential for large volumes of green electricity, vast land availability, and a cool climate.

- Aomori Pref also announced plans for the DC cluster model and the decarbonized power utilization model under the GX Strategic Area Program.

- CONTEXT: In April 2025, the DBJ issued a report on the suitability of Tohoku region for DCs, concluding that the region is well suited for them. Shin-Mutsu-Ogawara is a public-private development firm in Aomori that promotes large-scale industrial and infrastructure projects in the Mutsu-Ogawara area.

- TAKEAWAY: This agreement goes beyond a typical municipality-led investment promotion initiative. It’s an integrated effort to develop the key elements required for DC sites: power supply (Tohoku Electric), telecommunications (NTT East), finance (DBJ), and land (SMO). The national govt started accepting municipality bids for the GX Strategic Area program on Dec 23 and closed on Feb 13. While it’s unclear when the winners will be selected, Aomori Pref has set out its ambition to become one such new hub for DCs and related industries.

MoE selects proposals for Decarbonization Leading Areas

(Government statement, February 13)

- The MoE announced results of the 7th round for Decarbonization Leading Areas.

- 39 local govts submitted 18 proposals. 12 proposals covering four prefectures and 14 municipalities were selected. These include:

- Choshi City and 13 organizations: Economic circulation through wind power; o Tokushima City and 10 organizations: Biomass power and next-gen farming; o Takamatsu City and 23 organizations: Carbon neutral port (CNP);

- Arao City (Kumamoto) and three organizations: Regional revitalization through community energy firms;

- Oita Pref, Saeki City, Usuki City, Tsukumi City and 4 organizations: Heat pumps for disaster resilience.

- CONTEXT: Decarbonization Leading Areas seek to achieve zero CO2 emissions from electricity consumption in residential and commercial sectors by FY2030. Also, it aims to reduce emissions from transport, heat use, and other sources in line with Japan’s national 2030 targets, while considering local characteristics.

- TAKEAWAY: The GX Strategic Area program, promoted by METI, also supports carbon neutrality through regional initiatives and deployment of green energy. However, their focus differs. Decarbonization Leading Areas emphasizes reducing emissions at the community level, with a focus on achieving near-zero CO2 emissions from residential and commercial electricity use by 2030. In contrast, the GX Strategic Area program is industry-oriented, aiming to attract large-scale investment and strengthen industrial competitiveness through GX-related projects.

NEWS: ELECTRICITY MARKETS

OCCTO seeks to improve utilization rates of Kansai-Shikoku interconnection

(Agency statement, February 16)

- OCCTO proposed a new scheme to improve the HVDC interconnection link between Shikoku and Kansai.

- Operating capacity will be preset based on expected spot market volumes in order to stabilize flow. Currently, capacity is restricted when flow changes exceed a set limit, significantly reducing availability.

- Since 2023, the link has had oil leaks, likely linked to thermal expansion and contraction associated with frequent power flow fluctuations.

- Implementation of the scheme is set for spring.

- CONTEXT: The Anan–Kihoku Link is a 1,400 MW (700 MW × 2 lines) direct current transmission facility, including a submarine cable connecting Anan City in Tokushima Pref (Shikoku), and Yura Town in Wakayama Pref (Kansai).

Marubeni agrees with Hyosung and Skeleton for next-gen power grid stabilization

(Company statement, February 18)

- Marubeni agreed with Hyosung Heavy Industries (South Korea) and Skeleton Technologies (Estonia) to develop a next-gen power grid stabilization system that uses Hyosung’s reactive power tech and Skeleton’s supercapacitor to stabilize voltage and frequency from renewables or data center (DC) loads.

- Marubeni will supply HV Racks, aiming for commercialization in 2027.

- Since investing in Skeleton in 2021, Marubeni has been a strategic partner in Asia, supporting supply and sales in South Korea and exploring expansion to the U.S.

- CONTEXT: Rising renewable energy and DCs cause power demand fluctuations, making technologies that ensure power quality and strengthen the grid essential.

OCCTO again orders power transfer amid tight supply-demand in Hokkaido

(Agency statement, February 15)

- Due to a sudden increase in power demand caused by low temperature and reduced wind power output, Hokkaido’s supply–demand balance deteriorated on Feb 15.

- OCCTO ordered Tohoku Electric to provide electricity interchanges to Hokkaido, and the reserve margin improved.

- Feb 15, 17:30–18:00: Up to 60 MW from Tohoku to Hokkaido;

- Feb 15, 21:00–22:30: Up to 80 MW from Tohoku to Hokkaido;

- Feb 15, 23:00–24:00: Up to 70 MW from Tohoku to Hokkaido

- CONTEXT: OCCTO operates the Inter-area Corrective Power Interchange to adjust actual power flows between regions when real-time supply-demand deviates from initial plans.

Hokkaido Electric begins operation at Tomatoh Biomass Power Plant

(Denki Shimbun, February 16)

- Hokkaido Electric said the Tomatoh Biomass Power Plant (50 MW) began commercial operation. It uses wood pellets and palm kernel shells (PKS) as fuel.

- CONTEXT: The plant is owned by Equis Group (80%) and Hokkaido Electric (20%).

- The owners are considering the use of CCUS and hydrogen methanation.

NEWS: HYDROGEN

Govt conducts pre-screening for hydrogen and ammonia projects with the 4th LTDA

(Company statement, February 18)

- ANRE proposed screening for hydrogen and ammonia projects starting in the fourth round of the Long-term Decarbonized Power Source Auction (LTDA) in FY2026.

- The aim is to secure supply capacity and select projects comparable to those eligible for CfD certification (Contract for Difference).

- To streamline the process, eligibility will be determined through a checklist-based assessment instead of a comprehensive evaluation.

- From the fourth auction onward, only low-carbon hydrogen and ammonia will be eligible, although grey hydrogen was allowed in the first three rounds.

- Upstream projects must ensure stable supply through Japanese participation with secure contractual arrangements that do not disadvantage Japan.

- To enhance industrial competitiveness, at least one key facility in both supply and utilization must contribute to Japan’s global competitiveness.

- CONTEXT: The first and second LTDA rounds for hydrogen and ammonia-fired power plants covered only fixed costs. From the third round onward, hydrogen and ammonia fuel costs were also included, and the price cap was significantly raised to support the entire supply chain up to power generation.

- TAKEAWAY: LTDA has so far played a secondary role to the CfD in promoting hydrogen technologies. The third auction launched in Oct 2025, closed in Feb 2026, and results are expected in April. In the first round, about 770 MW of ammonia and 55 MW of hydrogen co-firing retrofits were awarded. In the second round, only 95 MW of ammonia co-firing was selected. With revised rules from the third round, participation by hydrogen and ammonia projects will likely increase. This will help to support projects that were unable to tap the CfD channel. As the number of LTDA hydrogen projects expands, compliance with the Hydrogen Society Promotion Act will be required.

Japan’s hydrogen station network shrinks as FCV sales plunge

(Asia Nikkei, February 18)

- Japan’s hydrogen refueling infrastructure is contracting, with the number of stations falling to 149 in FY2025, down roughly 10% from 2021, far below the government’s target of 320 stations by 2025.

- Annual fuel-cell vehicle (FCV) sales have dropped 83% since 2021, to just 431 units in 2025, as high vehicle prices and limited infrastructure weigh on demand.

- About 90% of Japan qualifies as a “gap area”, more than 15 km from a hydrogen station. More than 1,500 municipalities lack hydrogen infrastructure, compared with only 11 without gasoline stations.

- About 70% of hydrogen stations close by 5 p.m. Station operators cite poor economics despite subsidies.

- CONTEXT: Starting April, FC subsidies will fall ¥1.05 million to a max of ¥1.5 million, while EV subsidies will rise by ¥1.3 million, widening the cost gap.

- TAKEAWAY: Japan’s hydrogen mobility strategy faces a classic chicken-and-egg problem: weak vehicle demand undermines station economics, while shrinking infrastructure discourages new buyers. Global automakers seem to be scaling back FCV development and with it hydrogen’s near-term prospects in passenger transport appear to be narrowing. The sector will refocus on industrial hydrogen use and heavy-duty applications instead.

GI Fund selects SOEC hydrogen production project by Denso and JERA

(Agency statement, February 17)

- Under the Green Innovation Fund program on green hydrogen, NEDO selected a project by DENSO and JERA to develop large-scale and modular Solid Oxide Electrolysis Cell (SOEC) systems.

- Total project cost is ¥46 billion, of which ¥35 billion will be supported by NEDO. The project will run from FY2025 to FY2032, aiming to reduce SOEC capital costs below ¥68,000/ kW by 2032.

- CONTEXT: DENSO and JERA have tested hydrogen production since Sept 2025 at JERA’s Shin-Nagoya Thermal Power Station, using a 200 kW SOEC water electrolysis system developed by DENSO.

- TAKEAWAY: SOEC offers higher energy efficiency than alkaline and proton exchange membrane (PEM) electrolysis because it can utilize waste and external heat, potentially providing cost advantages when electricity prices are high. It is suitable for integration with industrial plants and power stations and can leverage Japan’s strengths in ceramics and solid oxide fuel cell (SOFC) technologies to compete globally. However, its high operating temperature (above 600°C) causes material degradation and requires complex system design, and equipment costs remain higher than those of alkaline and PEM systems.

Yanmar Power Solution builds factory for marine hydrogen engines

(Company statement, February 16)

- Yanmar Power Solution will build a new factory in Amagasaki City, Hyogo, to manufacture marine hydrogen engines.

- The site covers about 3.4 hectares.

- CONTEXT: Yanmar Power Solution was set up in April 2025 when spun off from Yanmar Power Technology. The firm focuses on large marine and land-based engines, including propulsion and powergeneration systems, as well as the development of hydrogen- and methanol-compatible engines.

NEWS: SOLAR AND BATTERIES

Companies shift focus to small-scale solar after large-scale support phase-out

(Nikkei, February 15)

- Clean Energy Connect, Renova, Sojitz, and Marubeni plan to increase installed capacities of smallscale solar power plants.

- This follows the govt’s decision in December to phase out support for large-scale solar facilities (above 1 MW). The segment has been in decline since FY2020, with annual newly installed capacity dropping 59% from FY2020 to FY2024.

- The new capacities projected (total 2.13 GW) are:

| Company | Sites (units) | Installed capacity (MW) | Targeted year (FY) |

| Clean Energy Connect | 10,000 | 880 | 2029 |

| Renova | 9,000 | 900 | 2030 |

| Sojitz | 3,000 | 150 | 2027 |

| Marubeni* | 2,000 | 200 | 2028 |

*Power end-user is Aeon

- TAKEAWAY: Compared to large-scale, smaller solar power plants are quicker to install (typically within six months to a year) and can be developed in neglected areas without subsidies. According to the agriculture ministry (MAFF), up to 90,000 hectares of former farmland could be converted into solar power plants (2010 estimate). These company roadmaps show the extent to which the market has achieved a high degree of autonomy with a demonstrated ability to adapt to major regulation changes. Nevertheless, while this points to an encouraging trend, it does not completely remove the potential for pushback from local stakeholders. In 2014 in Chino (Nagano Pref), a 247 kW solar power plant proposed on former farmland triggered local opposition due to landscape concerns, leading to calls for suspension. Although an amicable settlement was reportedly reached thereafter, such outcomes should not be deemed automatic.

Equinix signs PPA with ENEOS Renewable Energy, largest to date

(Company statement, February 16)

- Equinix inked a 15-year virtual PPA with ENEOS Renewable Energy for solar power from the Mita Power Plant (Hyogo Pref), with an installed capacity of 121 MW.

- This PPA will supply power to the firm’s data centers and AI infrastructure.

- CONTEXT: This marks Equinix’s second PPA, following a 30 MW agreement signed with Trina Solar in April 2025.

- TAKEAWAY : This large-scale PPA – the largest deal to date for a single asset – highlights the growing role of data centers in driving Japan’s renewable energy market. Japan is among the markets with more than 1 GW of operational data center capacity, and continues to see steady growth in its development pipeline, recording + 8% YoY expansion in 2025.

- SIDE DEVELOPMENT:

- Nichiei Intec develops double-wing solar carport for PPA operation

- (Company statement, February 18)

- Nichiei Intec developed a double-wing solar carport, EportY, for deployment of PPAs in parking lots and other areas.

- The system features a patentpending rainproof roof design and a steel-frame structure that enables rapid construction.

PowerX agrees with IIJ to leverage BESS for data centers

(Company statement, February 13)

- PowerX agreed with Internet Initiative Japan to develop containerized data centers that integrate BESS with computing platforms, explore use cases for digital infrastructure, and establish power utilization frameworks based on BESS.

- Electricity will be stored at a lower cost and supplied to server equipment within the containers, while surplus energy will be sold during periods of high demand.

- CONTEXT: A containerized data center has processing capacity that can be adjusted by adding or removing modular servers.

- TAKEAWAY: Containerized modular data facilities (CMDFs) are easier to deploy and more scalable compared to traditional data centers. Using less space and energy, they enable smoother integration of renewable energy sources. Japan’s CMDF market is estimated at $918 million and is expected to grow by 18-20% through 2034 ($4.2 billion), helping to drive the BESS rollout.

Panasonic tests cybersecurity solution for BESS

(Company statement, February 16)

- Panasonic, in collaboration with Itochu, launched cybersecurity testing for telecom systems and servers used in BESS installations. Tests were made onsite and offsite.

- Onsite testing includes intentionally modifying control parameters, creating incorrect device connections, and simulating abnormal or malicious system behavior. Offsite testing involves simulating external cyberattacks or unauthorized intrusions.

- TAKEAWAY: This demo highlights the importance of cybersecurity, echoing the govt’s decision to combat cyberattacks targeting BESS and solar systems. Hacking Battery Management Systems can deteriorate charge levels or temperature. Given that stored energy inherently carries safety risks (gas release, fire hazards, etc) significant physical damage can result. Also, if a BESS unit is interconnected with the grid, an attack could disrupt system stability and trigger disturbances, such as blackouts.

Digital Grid exceeds 50 MW aggregation capacity milestone

(Company statement, February 4)

- Digital Grid’s total BESS aggregation operations reached 58 MW.

- By 2028, the company aims to expand this capacity to 383 MW.

- To this end, the company plans to invest ¥10 billion.

- CONTEXT: Digital Grid is an aggregator created in 2017.

- SIDE DEVELOPMENT:

- Girasol Energy to become VPP aggregator for BESS and solar farms

- (Company statement, February 5)

- Girasol Energy will provide aggregation and digital services for VPPs starting April.

- Services will be available for installations above 20 kW, including EV chargers, datacenters, heat pumps, gas generators, solar power plants and BESS.

Kyushu Electric and Sharp to test DR response for residential batteries

(Company statement, February 17)

- Kyushu Electric and Sharp will conduct a DR demo to remotely control residential batteries.

- In the Kyushu region, batteries will be charged during midday hours when PV production is highest and discharged in the evening through DR signals.

- SIDE DEVELOPMENT:

- Panasonic to launch system using home energy management

- (Company statement, February 17)

- In April, Panasonic will launch a new cogeneration system “Ene-Farm” for GX-oriented houses.

- It is equipped with an upward and downward DR system, and an optimized system to power water heaters.

- CONTEXT: In 2027, the govt will introduce the GX-ZEH standard for new houses, setting higher performance requirements and mandating the installation of HEMS to increase residential renewable energy self-consumption.

Monochrome launches seamless solar PV wall

(Company statement, February 12)

- Monochrome launched “Wall-1,” a series of PV panels designed to blend seamlessly into building facades.

- It can be installed on walls for residential, commercial, etc.

- Built to withstand wintry conditions, heavy rain, and damage from animals, the modules can be replaced individually if needed.

- SIDE DEVELOPMENT:

- Upsolar Japan launches new vertical double-sided PV

- (Company statement, February 12)

- Upsolar Japan installed its vertical PV model “UP-Stand”, double-sided solar modules for snowy regions and in space-constrained areas such as parking lots.

- The modules face east and west, enabling distributed power generation from morning to evening, and securing output when market prices are likely to be higher.

NEWS: WIND POWER AND OTHER RENEWABLES

EES to build Japan’s first blade training center in Ishikawa

(Company statement, February 17)

- Eos Engineering & Service plans Japan’s first dedicated Blade Training Center (BTC) in Suzu City, Ishikawa Pref, to train wind turbine blade repair technicians.

- The center will train personnel ranging from inspection and minor repair technicians to advanced blade repair specialists, responding to rising maintenance needs as turbines grow larger and offshore wind expands.

- Construction began in 2025 with completion scheduled for 2026.

- Starting FY2026, BTC will offer Japan’s first GWO-certified Blade Repair Training, based on international standards set by the Global Wind Organization.

- TAKEAWAY: An assessment in 2024 by the Global Wind Energy Council said more than 574,000 wind turbine technicians globally will have to be hired this decade, with almost 43% as new talent. Within the next couple of years Japan will need at least 5,000 engineers and other trained staff capable of installing, operating and doing maintenance and repair on wind projects. For more details on training for wind sector technicians in Japan, see the Analysis section in the Oct 7, 2024 issue of Japan NRG.

Matsumae wind project files environmental impact assessment

(Company statement, February 13)

- The developer of the proposed RE100 Matsumae Wind Farm in Hokkaido published the environmental impact assessment (EIA) methodology report.

- The project plans 11 onshore wind turbines in Matsumae Town, south Hokkaido; max total capacity of 47 MW, and will cover 1,035 hectares

- Turbine height could reach 195 meters, with visual impact studies covering 11 km.

- CONTEXT: The methodology report outlines proposed survey and assessment methods for evaluating impacts on landscape, ecology, meteorological conditions, and local communities. The project is subject to national EIA procedures following revisions that lowered capacity thresholds for wind projects requiring assessment.

- TAKEAWAY: At 47 MW, the project sits just below 50 MW, a threshold that can trigger more stringent national review requirements for the environmental review, reflecting what has become a common sizing strategy in Japan’s onshore wind sector. As Hokkaido is one of the few regions with substantial wind potential, the assessment outcome will be closely watched amid growing scrutiny of cumulative environmental impacts and grid constraints in the area.

NUCLEAR ENERGY

KEPCO’s Mori appointed chairman of FEPC

(Nikkei, February 20)

- KEPCO President Mori was appointed chairman of the Federation of Electric Power Companies (FEPC). The power industry faces urgent challenges such as rising electricity demand driven by AI and data centers.

- Mori has led KEPCO’s efforts to restart and develop nuclear plants. After becoming president in 2022, he oversaw the restart of the Takahama Units 1 and 2 reactors. He achieved the full restart of KEPCO’s nuclear fleet.

- In 2025, the utility also began surveys toward building a new reactor at Mihama NPP, the first new nuclear project in Japan since the 2011 Fukushima disaster.

- Mori will now lead discussions with the govt and work to gain local community support for nuclear facilities.

- CONTEXT: KEPCO was involved in a 2019 scandal involving improper payments from a local official that led to the resignation of the then-FEPC chairman.

NRA considers revising grace period for anti-terrorism facilities at NPPs

(Tokyo Shimbun, February 19)

- The NRA discussed revision of the five-year grace period for installation of anti-terrorism facilities at NPPs. The move comes after a growing number of operators failed to meet the deadline.

- These facilities help with remote cooling of reactors in the event of an attack on a plant. Cooling is needed to prevent the release of radioactive materials.

- The NRA said 12 reactors have already completed these facilities, though only Oi Unit 4 met the original deadline.

- TAKEAWAY: In case the NRA decides to postpone the grace period for operations to start, this could impact the restart of TEPCO’s Kashiwazaki-Kariwa NPP Unit 7, which can’t restart due to the uncompleted anti-terrorism facilities. Should the revision come into place, the NPP could restart earlier than expected.

TEPCO begins power transmission from Kashiwazaki-Kariwa Unit 6

(Japan NRG, February 16)

- TEPCO began power transmission from Kashiwazaki-Kariwa NPP Unit 6, the first time in 14 years the facility has supplied electricity to the Tokyo metropolitan area.

- This is the second nuclear restart in east Japan since the Fukushima disaster in March 2011. The unit should achieve full commercial operation by mid-March.

- CONTEXT: Resuming operations is vital for TEPCO’S financial recovery plan. More nuclear restarts are planned in both Niigata and Hokkaido in the coming years.

Tohoku Electric submits improvement plan over Higashidori NPP irregularities

(TBS, Denki Shimbun, February 18-19)

- Tohoku Electric sent corrective measures to the NRA and to Aomori Pref, following misconduct involving falsified performance test records at Higashidori NPP.

- The misconduct began in FY2018 as an effort to streamline operations. The utility admitted that intrusion-monitoring sensors and cameras were not properly tested, and that records were fabricated by reusing other documentation.

- Tohoku Electric identified three root causes: weak execution of PDCA (Plan-Do-Check-Act) cycles, insufficient recognition of the importance of nuclear security operations, and inadequate oversight by HQ and plant management.

- Based on third-party recommendations, the utility has set up 19 corrective measures, such as strengthening monitoring and internal reporting systems.

- TAKEAWAY: The episode underscores persistent governance and compliance challenges at Japan’s nuclear operators, where documentation and procedural rigor remain under regulatory scrutiny. Beyond procedural failures, this case highlights deeper organizational culture issues – particularly the risks of entrenched “precedent-following” behavior in safety-critical operations. For nuclear operators under strict regulatory scrutiny, restoring trust will require changes in internal oversight and compliance culture. In effect, this means more time and money spent before the idled reactors are turned back on.

QST, Sojitz Machinery, etc partner on tools for ITER

(Company statement, February 9)

- The National Institutes for Quantum Science and Technology (QST) will partner with Sojitz Machinery and Sugino Machine to produce specialized assembly tools for the ITER fusion project.

- ITER had planned to develop these components internally, but it then sought Japanese expertise due to technical difficulty.

- These advanced tools are essential for the initial assembly of the reactor’s blanket. Delivery of these systems is planned for 2030.

Rokkasho new mayor supports local fuel reprocessing plant

(Nikkei, February 15)

- Rokkasho Village voters elected Hashimoto Takaharu as mayor, which follows the resignation of the previous mayor.

- The election focused on the future of a local nuclear fuel reprocessing plant that is a cornerstone of national energy policy but has faced decades of construction delays.

- Hashimoto secured a huge victory by running on a platform of support for the project.

- Election results confirm the village is committed to its role in the nuclear fuel cycle.

TRADITIONAL FUELS

INPEX’s Abadi LNG faces cost surge ahead of 2027 FID

(Energy Intelligence, February 18)

- The cost of the INPEX-led Abadi LNG project in Indonesia rose to $27 billion, up from prior estimates of about $21 billion, as inflation, a tight market for contractors, and the addition of carbon capture and storage (CCS) drove capex higher.

- The project targets a 2027 final investment decision (FID) and will develop the giant Abadi gas field in the Masela Block, which will supply a planned 9.5 Mtpa onshore LNG plant, supported by an FPSO and CCS infrastructure.

- CONTEXT: Abadi is owned by INPEX (65%), Pertamina (20%), and Petronas (15%). Abadi is currently the only major greenfield LNG project planned in Asia.

- Indonesia’s regulator SKK Migas approved the project’s environmental impact assessment on Feb. 11; a revised plan incorporating CCS was cleared in late 2023.

- However, a Capex increase of more than 10% could trigger a fresh review of the development plan, potentially slowing progress toward FID.

- INPEX targets an IRR of 15% and plans to dilute its stake from 65% to around 50%.

- TAKEAWAY: With cost increases for LNG projects rising across the world, it’s not a surprise that Abadi’s price tag has also risen. The question is whether INPEX and its partners will continue with the current schedule or push it back several years to navigate a period in which many new projects come online, pressuring fuel prices. This is where state interest could come into play – either from Japan or Indonesia. For Japan, Abadi represents geographic diversification of LNG supply and ongoing commitment to the ASEAN region at a time when China is pitching itself as the better partner. INPEX may be able to lobby Tokyo to add support thanks to the CCS component, which will reduce CO2 emissions.

Tokyo Gas’s U.S. shale subsidiary to expand in-house drilling operations

(Nikkei, February 19)

- Craig Jarchow, president of TG Natural Resources (TGNR), discussed the growing demand for natural gas in the U.S., and said the firm will expand drilling operations.

- CONTEXT: The company is Tokyo Gas’s shale development subsidiary in the U.S.

- TGNR develops gas in the Haynesville Basin (Texas/ Louisiana), producing 1.2 billion cubic feet per day.

- Its proximity to Gulf Coast LNG plants is a major advantage. Gas demand from LNG plants could double by 2030-35.

- Additionally, the growth of data centers will increase electricity needs. While growth came from asset acquisitions, rising gas prices have made acquisitions expensive.

- Jarchow said shale gas risks have decreased. Location of gas reserves is now well understood, reducing the need for excessive capital investment.

- CONTEXT: U.S. natural gas prices have fallen to a four-month low, down below the threshold of $3 per Mbtu as a recent cold wave subsides and demand for heating eases. Analysts suggest prices will likely trade in the $3-$3.5 range barring another major cold blast.

METI and Yamaguchi Godo Gas explain accident, propose changes in standards

(Government statement, February 19)

- METI and Yamaguchi Godo Gas released documents on a gas pressure accident in Ube City in December caused by a malfunctioning gas pressure regulator.

- Supply was disrupted to over 12,000 customers. Investigators determined that the failure involved a dislodged seal ring.

- The govt proposes upgrading gas facilities standards, making safety measures on regulators mandatory where there is a risk of abnormal gas pressure increases.

LNG stocks up from previous week, down YoY

(Government data, February 18)

- As of Feb 15, the LNG stocks of 10 power utilities were 2 Mt; up 5.8% from the previous week (1.89 Mt); down 1.5% from YoY (2.03 Mt); and down 6.5% from the 5-year average (2.14 Mt).

January Oil/ Gas/ Coal trade statistics

(Government data, February 18)

| Imports Volume YoY Value (Yen) YoY | ||||

| Crude oil | 13.7 million kiloliters (86.1 million barrels) | 5.7% | 901.7 billion | -8.1% |

| LNG | 6.2 million tons | -6.0% | 546.1 billion | -18.1% |

| Thermal coal | 9.9 million tons | -4.8% | 190 billion | -21.8% |

Chubu Electric withdraws from four biomass projects amid uncertain viability

(Company statement, February 17)

- Chubu Electric said it’s withdrawing from four biomass projects in Gunma and Niigata Prefs, with a total installed capacity of 7.9 MW.

- The plants were scheduled to begin operations between October 2026 and May 2027 and were expected to use pruned street tree branches as fuel.

- TAKEAWAY: This withdrawal by Chubu Electric echoes its earlier decision to dismantle the Yonago biomass power plant (Tottori Pref) in January, shut down the previous year. Most biomass projects rely on imported fuel, but rising wood prices in recent years have made these projects riskier. In this context, erex’s 300 MW plant in Niigata Pref was canceled in November. As for domestic biomass supply, costs remain high, with a volume of wood residues insufficient to meet demand, discouraging investors from large-scale deployment, even though some plants continue to come online (see Hokkaido biomass plant summary).

CARBON CAPTURE & SYNTHETIC FUELS

FEPC submits comments to METI for GX-ETS implementation

(Denki Shimbun, February 20)

- The FEPC submitted comments to METI on draft guidelines for Japan’s GX-ETS.

- It said carbon-related costs should be reflected in electricity prices so that GX (Green Transformation) investments can proceed, and urged the govt to clarify how the system will operate in the electricity spot and baseload markets.

- On benchmark levels seeking emissions reductions by FY2030, the FEPC said the design is too strict and that decarbonization measures need lead time. It called for flexible operation, including revising benchmarks if they impose excessive burdens.

- The FEPC supports upper and lower bounds for carbon prices, and asked the govt to analyze impacts on business costs and investment progress.

- The FEPC commented on the paid auction system for the power generation sector starting FY2033, and warned against unfair burdens on specific sectors or firms.

- TAKEAWAY: It’s natural to expect pushback by the big utilities as they know that they will be affected the most in the power sector. In the past, what the utilities have usually won through such tactics is time. But since the paid auction is not due for another seven years, METI will be aware that pushing back the dates will effectively render the GX-ETS toothless until the mid 2030s.

MHI succeeds in liquid synthetic fuels production

(Company statement, February 13)

- Mitsubishi Heavy Industries (MHI) demonstrated production of liquid synthetic fuels through an integrated end-to-end process.

- Hydrogen and carbon monoxide are produced through SOEC co-electrolysis (Solid Oxide Electrolysis Cell) and used as feedstock for a Fischer-Tropsch synthesis unit.

- Using MHI’s proprietary cylindrical cell stack, co-electrolysis simplifies the process and improves efficiency, enabling cost-competitive synthetic fuel production.

- Analysis of the resulting fuel confirmed it’s suitable for SAF.

- MHI aims to provide high-value SAF production systems by integrating SOEC co-electrolysis with conventional FT synthesis processes.

- CONTEXT: SOEC co-electrolysis uses solid oxides as electrolytes to simultaneously electrolyze CO2 and water vapor at high temperatures. FT synthesis generates chemical reactions in H2 and CO to produce liquid hydrocarbons.

- TAKEAWAY: In addition to SOEC, hydrogen production by electrolysis includes alkaline water electrolysis (AWE), proton exchange membrane (PEM) electrolysis, and anion exchange membrane (AEM) electrolysis. AWE and PEM are more mature and commercially deployed. AEM electrolysis is a newer hybrid approach combining advantages of AWE and PEM systems. However, SOEC offers superior efficiency and unique co-electrolysis capability, making it highly promising for large-scale H2 and synthetic fuel production.

Taisei opens zero-carbon research institute in Saitama Pref

(Company statement, February 16)

- The Taisei Next-Generation Technology Research Institute opened in Saitama Pref as a zero-carbon building.

- The facility was built under the company’s “T-ZCB” system (Taisei Zero Carbon Building) designed to minimize lifecycle carbon emissions.

- Key features include:

- Concrete made from recycled steel T-eConcrete®/ Carbon-Recycle;

- On-site solar power generation;

- Two labs conducting road infrastructure research using recycled materials;

- These measures aim to achieve net-zero lifecycle emissions over 60 years.

NYK Line operates low-carbon methanol bulk carrier

(Company statement, February 12)

- NYK Bulk & Projects operated the dual-fuel bulk carrier Green Future using low-carbon methanol fuel, achieving a 65% emission reduction compared to conventional fuel.

- The fuel was made from biomass, and bunkered in Sept 2025 in South Korea.

- CONTEXT: NYK Line has been involved in methanol projects, inking a deal in April 2025 to build a large crude oil carrier equipped with a main engine compatible with methanol; final delivery is expected in 2028.

ENEOS and Suzuyo provide SAF environmental value to Fuji Dream Airlines

(Company statement, February 19)

- Suzuyo provided SAF environmental value to Fuji Dream Airlines at Shizuoka Airport. The physical SAF is supplied by ENEOS to Narita Airport.

- The initiative is implemented under the govt’s SAF support demo project for local production and consumption.

- CONTEXT: The deal is based on ENEOS’s book-and-claim model, under which SAF’s environmental attributes are allocated separately from physical fuel supply.

ANALYSIS

BY FILIPPO PEDRETTI

Can Japan Build a CCS National Industry?

The success of Japan’s decarbonization efforts depends on innovative technologies such as Carbon Capture and Storage (CCS), as well as hydrogen/ ammonia co-firing.

CCS is widely seen as playing an important role in resolving emissions from LNG and coal-fired power generation facilities. In fact, the 7th Strategic Energy Plan clearly states that thermal power is still needed for grid stability.

In recent years, Japan has made significant strides in CCS, developing legal, financial and technological frameworks. Concrete results are expected with the nine Advanced CCS projects that include both domestic and overseas CO2 shipping.

The country’s main domestic CCS project, in Tomakomai, nears a FID set for this year. As for projects involving cross-border CO2 injection, operation is still a matter for the future, but Japan’s shipping giants are working on securing their technological basis.

While Japan has nearly completed the legal and logistical framework for CCS, the economic engine – carbon pricing – remains underpowered. Japan NRG takes a closer look at what to expect in CCS over the next year.

CCS expectations and policies

According to Global CCS Institute, there are 313 CCS projects worldwide now in early development, 297 in advanced development, 47 under construction, and 77 already in operation. Many of the operational projects are enhanced oil recovery (EOR), the sector with the fastest-growing application since there’s an economic incentive to use the CO2 to boost oil production while simultaneously storing it.

Japan has set audacious targets for CCS as a decarbonization tool. METI aims for 6-12 million tons of annual CO2 storage by the early 2030s, possibly scaling that figure to 120-240 million tons by 2050.

The national government says it’s ready to back up those ambitions with generous funding, pledging over ¥4 trillion in public and private investment in CCS over the next decade. In the draft FY2026 budget, the Ministry of the Environment is reserving ¥2.6 billion for related CCS demonstrations.

Developing CCS is not only a domestic matter. There is also a global impetus, with the CCS market forecasted to grow from $3.5 billion in 2024 to $14.5 billion by 2032. AsiaPacific is the fastest-growing region, with Japan eager to position itself as a key player in a future value chain, from capture and shipping to storage and carbon finance.

Toward such goals, Japan must build the legal framework. In May 2024, Japan passed the CCS Business Act, creating the first legal framework for transport and storage. It includes a licensing system and provisions to transfer monitoring liability to JOGMEC.

| Law name | CCS Business Act |

| Date passed | May 2024 |

| Purpose | Establish a comprehensive legal framework for CO2 geological storage and transportation, ensuring regulatory certainty and promoting private-sector investment |

| Scope | Onshore and offshore CCS activities |

| Key regulatory feature | Licences for CCS-related activities |

| Exploration rights | Licences for geological surveys to assess CO2 storage potential |

| Storage rights | Licences for CO2 injection, storage operations, and long-term monitoring |

| CO2 transportation | Pipeline regulations introduced under a notification system to accelerate pipeline development |

| Policy alignment | Supports Japan’s decarbonization strategy alongside electrification, hydrogen, and nonfossil energy |

| Specified area designation | Offshore area in Tomakomai City, Hokkaido Prefecture designated in February 2025 |

| First licence issued | First exploration licence granted in September 2025 |

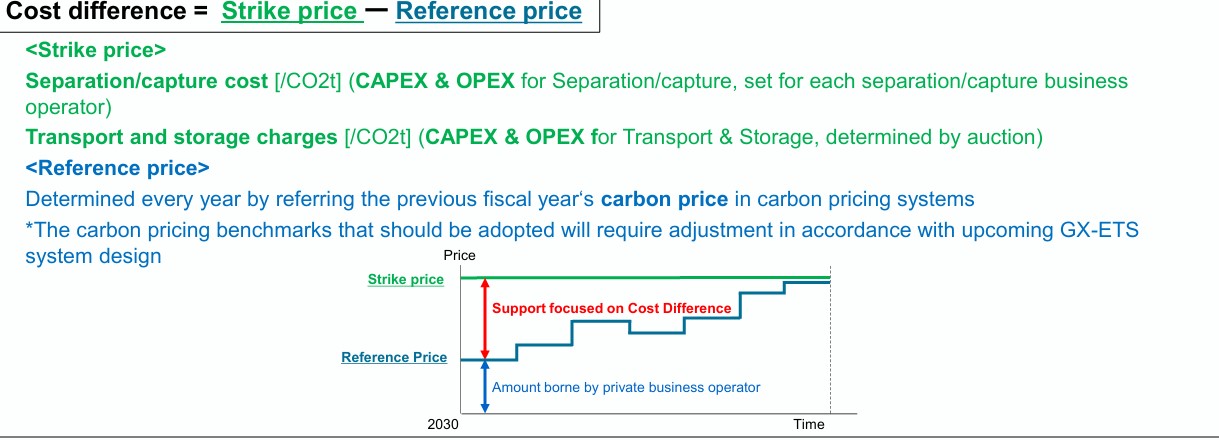

Business model

METI also introduced a “strike price” model where for initial projects the government will cover the gap between the full cost of CCS and a designated “reference price”. That reference price should reflect the carbon market, notably the GX Emissions Trading Scheme (GX-ETS), a cap-and-trade system that will be mandatory for large emitters starting April.

The strike price mechanism is designed to de-risk early CCS investments. Over time, however, the government’s strategy rests on the GX-ETS generating a carbon price high enough to make decarbonization technologies commercially viable without direct subsidies.

METI has finalized the scheme’s core framework, setting an initial price corridor for FY2026 at ¥1,700 to ¥4,300 per ton of CO2, with a planned annual increase of 3%. Yet this cautious ramp-up prioritizes political and industrial acceptability over transformative pressure.

The corridor sits well below the roughly ¥9,000 per ton that Japan NRG estimates will be required in the midterm to cover decarbonization costs. It is also far short of the $100–$150 (about ¥15,000–¥22,500) per ton considered necessary for CCS to stand on its own.

Still in its infancy, the GX-ETS risks being a relatively weak signal, unlikely on its own to catalyse a full-scale CCS industry this decade.

Another issue for CCS is public acceptance – the “Social License to Operate”. The High Pressure Gas Safety Institute of Japan is developing the country’s first technical standards for CO2 pipelines in order to build public trust through transparent safety rules.

Carbon management ecosystem

Tokyo already has a flagship CCS project, and the first commercial-scale project is advancing in Tomakomai, Hokkaido. Led by JAPEX with Idemitsu Kosan and Hokkaido Electric, test drilling is underway in a state-designated offshore area. After receiving the necessary license under the CCS Business Act, the goal is to explore two wells, aiming to confirm suitable geological formations.

The project seeks a FID by 2026 and operations to start by 2030, storing 1.5 to 2 million tons of CO2 a year from local industry. Idemitsu Kosan and Hokkaido Electric will capture CO2 from their refinery and power plant, respectively. JAPEX will handle underground injection and storage. The operators are now advancing engineering design work.

Japan, however, has limited geological storage potential, compelling the country to build an overseas CO2 logistics network. K Line, Mitsui O.S.K. Lines (MOL), and NYK seek to leverage LNG expertise to dominate the nascent liquefied CO2 (LCO2) carrier market. MOL has approvals for 96,000 m3 LCO2 carriers and even a methanol/ CO2 dual-fuel design. In Norway, K Line and MOL participate with LCO2 vessels in the CCS project Northern Lights.

NEDO commissioned the development and demonstration of CO2 ship transportation, allocating ¥38 billion for seven R&D projects that explore different CO2 capture methods. A NEDO-commissioned consortium led by Japan CCS is demonstrating LCO2 ship transportation technology to support CCUS deployment by 2030.

The project focuses on transporting CO2 from emission sources to use at storage sites. Since November 2024, a demonstration vessel has operated between Maizuru and Tomakomai.

In parallel, JOGMEC and METI are working to establish a council to standardize technical specifications for CO2 ship transport and to reduce associated costs. Shipping is central to projects like Japan’s nine Advanced CCS Projects. Three of those entail sending CO2 to storage sites in Sarawak, Malaysia, while one project plans to ship CO2 to Oceania. Projects are also being studied for Australia and Alaska.

Japan is discussing bilateral agreements with Malaysia and Singapore that’s needed for international CCS shipping. But while Japan’s shipping companies are ready to take CO2 on board, the realization of Tokyo’s overseas CCS projects is still a goal far in the future.

| Stage | Description | Role in the CCS Value Chain |

1 | CO2 capture | Separation of CO2 from an industrial or power-generation source |

2 | Liquefaction | Conversion of gaseous CO2 into liquid form for efficient transport |

3 | Temporary storage | Buffer storage prior to shipment |

4 | Loading | Transfer of liquefied CO2 onto transport vessels |

5 | Marine transportation | Shipment of CO2 to offshore or distant storage sites |

6 | Heating | Temperature adjustment before injection |

7 | Boosting | Pressure increase to meet injection requirements |

8 | Injection | Permanent storage of CO2 in geological formations |

Conclusion

CCS is not, for Japan, primarily a climate-first policy. Rather, it’s an industrial continuity strategy — a way to preserve LNG-based power generation and heavy industry in a carbon-constrained world. Whether it succeeds depends less on technical feasibility than on political willingness to impose costs on emissions. The financial hurdles remain formidable.

JOGMEC acknowledges high capital expenditure for pipelines and elevated operating costs for ship-based liquefaction. Geological uncertainties add further risk. Even Norway’s Northern Lights joint venture reported an operating loss of ¥43 billion in 2024, sustained by state backing in its early years.

The government’s strike price model is therefore a temporary bridge – a mechanism to move CCS from demonstration to deployment. But the long-term bet is on carbon pricing. A price of $100–150 per ton is widely seen as necessary to make CCS commercially viable, yet the current GX-ETS corridor falls far short. Moreover, allowances are tied to company transition plans rather than a fixed national emissions cap, diluting the system’s disciplinary force.

Japan Climate Transition Bonds could provide supplementary funding, and tighter emissions standards for thermal power operators may eventually make carbon capture unavoidable. Ultimately, however, CCS will not stand on financial engineering alone. Without a substantially stronger carbon price – whether through an expanded GX-ETS or an explicit carbon tax – the economic gap will persist.

In the end, CCS in Japan hinges on a simple question: is METI prepared to make carbon expensive enough to matter?

ANALYSIS

BY TETSUJI TOMITA

Finding the Right Balance: How Japan is Fine-Tuning its Power Adjustment Market

Japan’s electricity balancing market is entering a new phase. Starting April, three changes will take effect simultaneously: the price cap for key frequency response products will fall from ¥19.51 to ¥15/ ΔkW per 30 minutes; procurement volumes will be reduced; and trading for most balancing products will shift from weekly to day-ahead procurement in 30-minute slots. Finally, device-level participation for household batteries and EVs will be introduced.

These changes are a meaningful recalibration of how flexibility is priced, forecast and financed. And they offer a glimpse of Japanese energy planners’ vision: restraining price surges while preserving incentives for fast-response capacity.

For battery energy storage system (BESS) operators, the reform goes to the heart of revenue expectations. The balancing market is one of the most attractive early monetization channels.

Lower caps and tighter procurement raise the question: is this the beginning of structural revenue compression or a controlled normalization of a maturing market? Japan NRG believes the answer leans toward the latter.

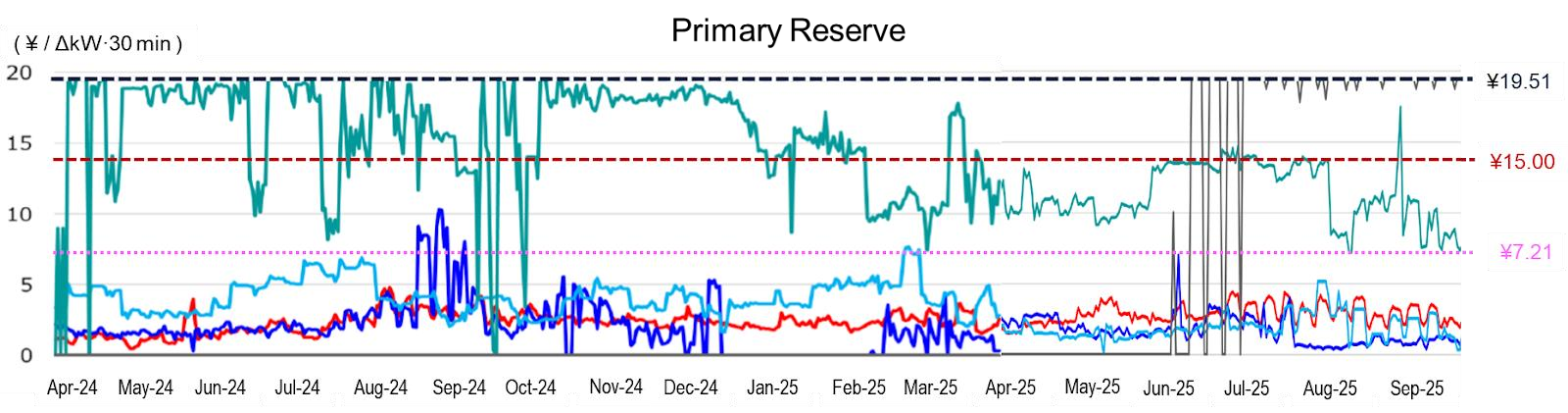

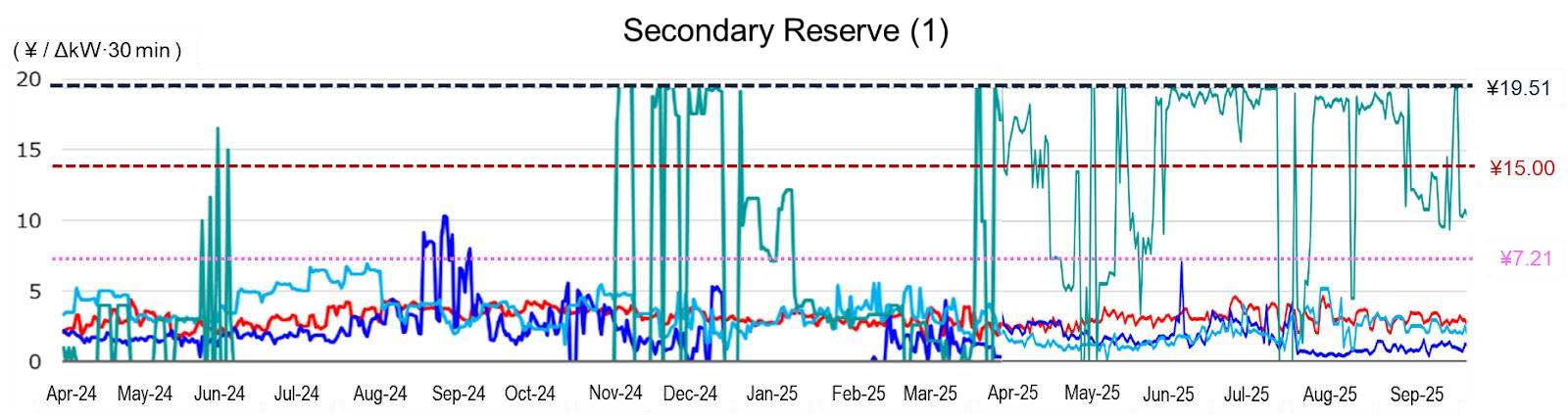

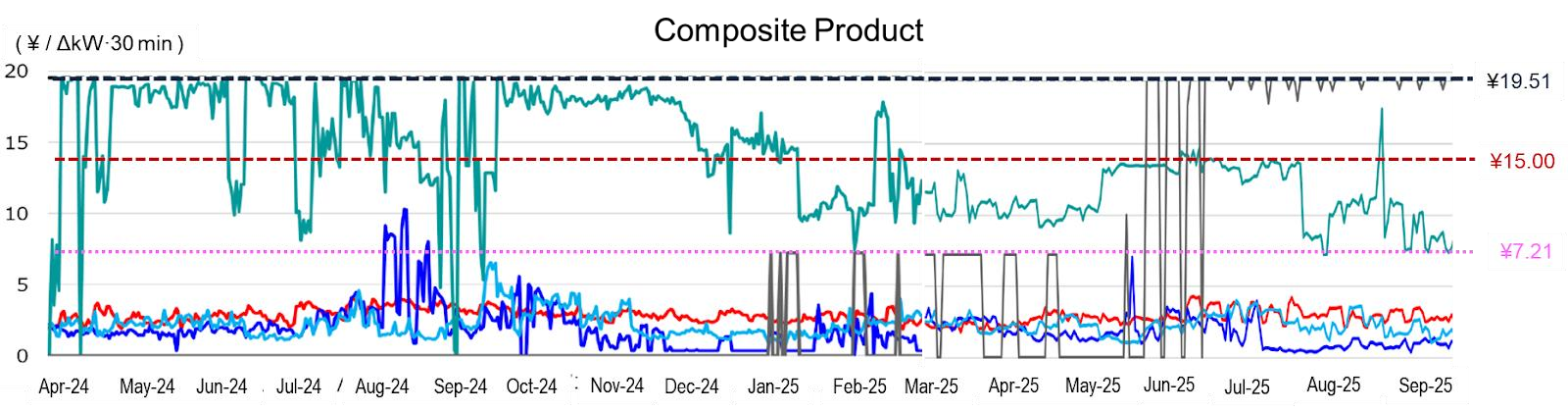

Revision of Price Cap After FY2026 (Unit: ¥ / ΔkW·30 min)

| Balancing Power Products | Function | Until FY2025 | After FY2026 | ||

| Single | Composite | Single | Composite | ||

| Primary Reserve | FCR (Frequency Containment Reserve) | 19.51 | 19.51 | 15.00 | 15.00 |

| Secondary Reserve (1) | S-FRR (Synchronized Frequency Restoration Reserve) | 19.51 | 15.00 | ||

| Secondary Reserve (2) | FRR (Frequency Restoration Reserve) | 7.21 | 7.21 | ||

| Tertiary Reserve (1) | RR (Replacement Reserve) | 7.21 | 7.21 | ||

| Tertiary Reserve (2) | RR-FIT (Replacement Reserve for FIT) | No limit | – | No limit | – |

Scale of the Price Cap Reduction

Under the current ¥19.51 cap, bid prices for Primary Reserve (FCR) and Secondary (1) have frequently clustered near the upper bound. Regulators grew concerned that persistent high awards would embed elevated procurement costs across the system.

From April 2026, the cap will fall to ¥15.00 — a reduction of roughly 23%. This is far less severe than the originally proposed ¥7.21 level, which would have implied a 63% cut. The adopted figure therefore reflects a compromise between cost containment and investment continuity.

The practical impact will vary by technology. Thermal, hydropower and pumped hydro have not typically bid above ¥15.00. By contrast, BESS, VPP and DR assets have cleared above that level in recent years.

Also, the number of three-hour blocks clearing above ¥15 per ΔkW has increased markedly since mid-2025 in both Primary and Secondary (1) markets. Several regions, notably Kansai, Chugoku, Shikoku and Kyushu, have recorded sustained tight pricing, while others remain looser, according to an assessment made by Volue.

This regional divergence matters. In tighter regions, the ¥15 cap will become a constraint. In structurally long regions, its impact may be limited. The result is likely to be geographically uneven revenue compression rather than a uniform national effect.

Average Winning Bid Price by Power Source Type (Nationwide)

Structural changes to procurement

Under the previous cap of ¥19.51, balancing power providers – thermal generators, pumped hydro, BESS, and DR aggregators – could anticipate relatively robust upside revenue in tight supply-demand conditions. Although actual clearing prices often fell below the cap, the ceiling itself influenced bidding psychology.

From April 2026, Primary through Tertiary (1) products will move from weekly to dayahead procurement. Forecasting complexity will increase: participants must predict system conditions 24 hours ahead rather than seven days in advance. Organisations with advanced forecasting, optimisation and bidding systems will gain an edge. Smaller players relying on simpler tools will face higher execution risk.

Procured volumes will also be reduced in FY2026 to about 84% of the FY2025 level, according to a OCCTO clarification of the METI document. At the same time, household batteries and EVs will be permitted to participate at device level, gradually broadening the potential supply base.

Taken together, these measures suggest a market shifting from early-stage scarcity pricing toward tighter governance and greater competitive discipline.

Impact on BESS revenues

For standalone battery projects, the central question is revenue mix.

A representative two-hour, BESS participating actively in Primary and Secondary markets typically stacks revenue across several channels. A conservative illustrative mix might be:

- Balancing market (FCR + S-FRR): 40–50% of gross revenue

- Capacity market: 20–30%

- Wholesale arbitrage (JEPX day-ahead and intraday): 15–25%

- Other services: variable

Actual outcomes vary by region, strategy and contracting structure. Many long-term institutional developers assume base-case clearing prices well below the cap. Still, balancing services remain a significant revenue pillar.

If balancing accounts for 45% of gross revenue and balancing income declines by, say, 20% due to the lower cap and tighter volumes, overall project revenue could fall by about 9%. For a project targeting equity IRRs in the low teens, that could reduce returns by perhaps 1–3 percentage points, depending on leverage and cost assumptions.

This would be meaningful. But it would mostly trim the upside during periods of tight supply, rather than undermine the core economics of carefully structured projects. Developers who already build in cautious price assumptions are unlikely to see their business cases fundamentally altered.

Those most exposed may be smaller HV projects designed to capture near-term scarcity premiums following early grid connections in tight regions. By contrast, larger EHV-scale projects backed by long-term capital tend to rely on diversified revenue stacking and more conservative underwriting.

Crucially, METI pulled back on the more aggressive ¥7.21 proposal, which signals that officials wish to limit the risk of abrupt investment withdrawal and continue to see BESS as a vital part of a decarbonized energy system.

Future reductions?

Of course, officials have indicated that, if competition does not improve sufficiently, the cap could be lowered further in stages to ¥10 and eventually ¥7.21.

Even if conditional, this pathway introduces regulatory optionality into long-term models. Investors must now consider not only current compression but the possibility of additional tightening. Viewed differently, however, this optionality may serve as a guardrail against speculative entry. Policymakers appear keen to avoid a repeat of the early solar FIT boom, when generous incentives attracted very short-term investors, distorting market dynamics.

Equally, the shift to day-ahead procurement should create new opportunities for traders and aggregators with strong optimization capabilities. In other words, the reform reorientates the skill set from hunting scarcity rents to efficient operations.

For developers, this will intensify analysis of regional tightness patterns, interconnection constraints, and wholesale arbitrage strategies. Larger BESS operators may further diversify portfolios across regions as a deliberate risk-management tool.

It’s all relative

In the UK, Dynamic Containment initially delivered high returns for early battery entrants. Rapid capacity growth followed, and ancillary prices compressed sharply as the market matured. Australia’s FCAS markets underwent similar normalization as storage penetration increased.

In many liberalised systems, storage economics follow a recognisable sequence: early scarcity pricing attracts entry; capacity grows; regulators refine market design; revenues normalize and diversify.

Japan appears to be moving in a similar direction, but with a key difference. The cap adjustment and procurement reform are occurring before a dramatic oversupply of BESS materializes. This should avoid a boom-and-bust dynamic, which ultimately benefits the industry as much as the consumers.

Conclusion

For serious long-term developers planning 20-year assets, the implications of the triple reforms from April are manageable. Upside scarcity scenarios will be moderated and financing models will incorporate a more cautious regulatory outlook.

At the same time, the structural drivers of storage demand remain intact: rising renewable penetration, increasing curtailment, growing system volatility, and limited scope to expand pumped hydro.

Japan’s balancing market is moving into a more competitive and operationally demanding phase, where forecasting sophistication and regional strategy matter more than simple exposure to a high price cap.

The opportunities are not disappearing, they are evolving.

ASIA ENERGY REVIEW

BY JOHN VAROLI

A brief overview of the region’s main energy events from the past week

Australia / Energy transition

The govt said 2025 was a “breakout year” for the energy transition as a record number of projects – 53 – gained approval. The pipeline for the national grid swelled to 275 projects.

Australia / Renewables investment

Victoria leads in capital investment committed, with $9.62 billion to be spent on new renewable assets. Much of it goes to wind ($4.65 billion), and $2.24 billion to solar. But Queensland leads in wind with $5.07 billion committed, and only $480 million for solar.

Australia / Solar

Australia is expected to generate around 1 million tons of solar panel waste by 2035, equivalent to roughly 50 million individual panels.

China / LNG

China marked one year since it last imported LNG from the U.S. Yet, Chinese firms continue purchasing U.S. LNG only to resell it to Europe, where demand has surged.

China / Solar

When smaller solar projects – such as home rooftop panels – are taken into account, China’s total solar capacity is 1,063GW, said Global Energy Monitor, citing its own research.

China / Wind

China tested a blimp-like wind turbine that harnesses the wind at high altitudes. Power is sent via the tethering cable to the ground below, where it can enter the grid.

Green hydrogen

Electrolyser growth will reduce gas-based blue hydrogen’s share, says GlobalData. By 2030, green hydrogen could account for about 88.6 % of global low-carbon hydrogen production.

India / Renewables

Adani Group will invest $100 billion to build renewable-energy-powered data centers across India by 2035. The project will create a $250 billion AI ecosystem over the next decade.

India / Wind

An Inox-led consortium inked deals to build a 600-MW wind portfolio globally. And Inox Green will also manage a 4.5-GW maintenance portfolio.

Philippines / Coal

The Philippines will auction off 18 coal blocks. The bid round covers three coal areas – Antique, Cagayan, and Isabela.

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Hulic Ochanomizu Bldg. 3F, 2-3-11, Surugadai, Kanda, Chiyoda-ku, Tokyo, Japan, 101-0062.