The U.S.-led war on Iran provides a real-time stress test for Japan’s energy security architecture. So far, the system has held up well. The longerterm picture, however, is more complicated.

As the conflict drags on, the fiscal resources required to cushion households and industry from higher energy prices could limit Japan’s ability to fund infrastructure and energy-transition investments.

Japan has a hybrid power market; the retail market was fully liberalized in 2016.

Yet, the power market is still in its infancy, in particular from a talent perspective. We visited the E-World Energy & Water event in Germany to contrast the European and Japanese power markets from a talent lens.

ASIA PACIFIC REVIEW

This column provides a brief overview of the region’s main energy events from the past week

Nuclear power plants and a copper refinery are candidates for the next phase of Japan’s pledged $550 billion of investments in the U.S.

METI Minister Akazawa was due to visit Washington March 5-8 to meet Commerce Secretary Lutnick to discuss projects. The two countries might announce the next batch of investments at the Japan–U.S. summit scheduled for March 19.

Leading candidates include construction of one or more of Westinghouse NPPs and a new copper refining facility by Falcon Copper. A 2025 fact sheet estimated Japanese funding to Westinghouse projects at $100 billion.

CONTEXT: The $550 billion “investment” acts more like a loan that has allowed Japan to bargain down tariffs on its exports to the U.S.

Earlier this year, the two countries selected the first projects, including a gas-fired power plant, oil export infrastructure and synthetic diamond manufacturing.

Major Japanese marine insurers such as Tokio Marine & Nichido Fire Insurance, Mitsui Sumitomo Insurance and Sompo Japan are considering expanding the areas where ships must pay additional war-risk premiums as tensions around Iran escalate.

Waters around Qatar and Kuwait could be added to existing high-risk zones that already include Iran and the UAE.

Ship operators entering these “excluded areas” must notify insurers and pay additional premiums for coverage.

CONTEXT: The move follows a Lloyd’s of London-linked reinsurance committee’s decision to broaden the list of areas excluded from standard coverage due to the war. Some international insurers have already suspended coverage in parts of the Persian Gulf and Iranian waters, but Japanese insurers are considering maintaining coverage in the region while charging higher premiums.

Residents in Inzai, Chiba Pref filed a lawsuit to revoke building approval for a large data center (DC), arguing the facility violates local zoning rules.

The plaintiffs claim the DC should be classified as either a “factory” or “warehouse”, both of which are prohibited under the area’s district plan.

The project involves a 50-meter-tall DC surrounded by commercial facilities, residential buildings and hotels.

Plaintiffs argue the facility functions like a factory because it processes data to generate value and stores large volumes of fuel for emergency generators.

CONTEXT: Japanese building regulations do not explicitly define “data center” as a building category. It’s often classed as an office. Inzai has become one of the nation’s largest DC clusters, hosting around 30 facilities.

The Tokyo Public Prosecutor and Japan Fair Trade Commission searched petroleum product distributors on suspicion of price-fixing diesel fuel sold to corporate clients.

The 8 targeted firms include ENEOS Wing, ENEX Fleet, Kitaseki, Kyoei Oil, and Shin-Idemitsu. They operate “fleet” fuel businesses supplying diesel to logistics companies.

Authorities suspect sales staff from the distributors agreed on price increases before talks with customers.

(Exchange data, Company statement, Nikkei, March 4-6)

Trading in electricity futures on the EEX surged to a record 4.91 TWh on March 3, far exceeding the previous daily high of 2.82 TWh in March 2025.

CONTEXT: That daily record was a third of the entire February volume.

The spike was driven by hedging demand from generators and power retailers amid concerns that the Iran war could disrupt natural gas supplies and push up fuel costs.

Among the traded volume was heavy interest in longer-dated products such as FY2026 contracts. Prices also rose sharply, but less than the 2.4-fold jump in Asian LNG spot rates in early March.

TAKEAWAY: Volumes and prices were up significantly in the power market, making the case for electricity spot prices and futures contracts as the best tools to gauge sentiment over the Iran war’s perceived impact. See this week’s Analysis section for a deep dive into how electricity prices are reacting to the war.

TEPCO Power Grid made its first curtailment of renewable generation, instructing solar and wind operators to cut output during the midday to maintain system balance.

The grid operator reported a maximum curtailed capacity of 1.84 GW on March 1 (Sunday). Dispatch data show the actual curtailed volume totaled about 2.28 GWh, affecting several 30minute curtailment intervals.

Solar generation rose rapidly through the morning and peaked at roughly 14.8 GW, supplying more than half of the 25–26 GW of midday electricity demand.

Before curtailment was introduced, the grid operator deployed substantial system flexibility. Pumped-storage hydro plants were operated at roughly 6.17 GW, absorbing excess electricity by pumping water to upper reservoirs.

Thermal generation was also reduced sharply during the day. LNG-fired output fell from about 8.3 GW in the morning to 5.4–5.6 GW, while coal-fired generation declined from ~5.1 GW to ~2.6 GW as solar output increased.

Despite this, the grid had to curtail primarily solar and some wind facilities.

CONTEXT: Renewable capacity in the TEPCO area now exceeds 21 GW after growing about 1 GW annually in recent years. It is mostly solar.

TAKEAWAY: The March 1 event confirms that even the Tokyo area is not immune from curtailments, despite having the country’s biggest demand load. The data reveals some interesting issues. In energy terms, the curtailment was small, only a fraction of daily power consumption. But the 30-min data shows that the grid operator went to great lengths to stave off curtailment: putting the max pumped-hydro capacity available to work and dropping thermal run rates substantially. Over 5 GW of gas and coal was sacrificed. Thus, it’s possible to conclude that the ceiling was reached for solar and wind generation in the TEPCO area – at least on the weekends, when industrial load drops. While gas plants showed much flexibility, they’ll have a minimum stable operating level. And with Kashiwazaki-Kariwa NPP’s restart, the TEPCO system’s flexibility will surely decline. As temperatures rise and daylight hours lengthen, the traditional low power demand season of late April and May could see many more curtailments, at least on weekends. For the grid to balance without curtailment, the TEPCO region will require much more BESS than it has in place.

TEPCO Power Grid instructed renewable generators to curb output on March 7, the second curtailment in the Tokyo area in a week.

The grid operator was due to restrict up to 870 MW of solar and wind generation between 08:00 and 16:00, according to its curtailment notice published on March 6.

The operator also said curtailment may be required again on 8 March, with reference forecasts suggesting potential reductions of around 2.3 GW if weather and demand conditions lead to excess supply.

Total electricity sales rose 0.5% YoY in November 2025 to 60.12 TWh, the first increase in four months, according to the EGC, Japan’s market regulator.

Demand across retailers rose 0.3% to 63.22 TWh, the first YoY rise in four months.

Sales by new power retailers continued to expand, rising about 12–13% YoY to roughly 12.7 TWh, extending their growth streak to 21 consecutive months. Their market share increased by about 2.3 percentage points to 21%.

In contrast, sales by EPCO-linked retailers declined about 2–2.4% YoY, continuing a multi-month downward trend.

By customer category, low-voltage sales (mainly households and small businesses) rose about 4%, while high-voltage and extra-high-voltage segments declined slightly.

CONTEXT: Data suggests that modest demand growth combined with continued customer switching to new retailers helped push electricity sales higher after several months of decline.

ANRE proposed creating a technical study group to examine system development for introducing a simultaneous market, where supply capacity and balancing resources would be traded at the same time.

The group will examine key technical challenges and explore solutions, such as contract processing functions, which are considered particularly complex to implement, and members will include generators, TSOs, retailers, and system vendors.

Meetings are expected to be held every one to two months and will not be open to the public.

The study will review international examples and explore ways to simplify optimization for unit commitment and dispatch to reduce processing time. The simultaneous market is intended to optimize generator dispatch decisions – including plant start-ups, shutdowns and output allocation – but requires large-scale system functions. The contract processing function is particularly challenging to develop, according to the officials.

ANRE aims to compile a report outlining possible system designs and implementation approaches, potentially by March 2027, depending on the progress of the work. It will be the first phase of a five-stage process toward implementing the simultaneous market system.

CONTEXT: In October 2025, ANRE presented a roadmap for introducing the simultaneous market. Phase 1: Business design; Phase 2: Requirements definition; Phase 3: System development; Phase 4: Coordination with market participants and final preparation; Phase 5: Implementation.

TAKEAWAY: Although no discussions on the simultaneous market were held after the October 2025 meeting, full-scale, detailed design will finally begin. Confirming technical feasibility will be crucial, and the focus will shift from market design to system development. Regulations for the balancing market, which will be integrated into the simultaneous market, have also changed. We expect the system development process to go smoothly, ensuring a seamless transition.

ANRE discussed revisions to measures and regulations in the capacity market, including the reference price (Net CONE – Cost of New Entry) and the price cap.

The proposed increase is to about ¥20,000/ kW for Net CONE, and ¥30,000/ kW for the price cap, starting with the FY2026 auction if modification is finalized by April.

This increase is about double the current level and is intended to secure sufficient generation capacity amid rising inflation and soaring maintenance costs.

This measure will be reviewed after the results of the FY2026 main capacity auction.

The govt will assess changes in bidding behavior and consider factors such as total clearing costs and capacity procurement.

Measures to curb inefficient coal-fired power plants will remain in FY2026. o CONTEXT: The results of the 6th (FY2025) capacity market main auction were announced in January. OCCTO held a Call for Evidence to gather ideas from market players and made a comprehensive review of the capacity market for FY2025.

TAKEAWAY: Net CONE is calculated by subtracting revenues from sources other than the capacity market from the Gross CONE, making it highly sensitive to trends in construction costs, maintenance costs, operating costs, and capital costs. Rising prices are also affecting clearing prices, making it unavoidable to raise the Net CONE.

Prices for non-FIT non-fossil certificates in the third FY2025 trading session remained at the ceiling of ¥1.30/kWh, unchanged from the previous round.

Market conditions tightened somewhat compared with the second session. Buy bids continued to exceed sell offers, keeping prices pinned at the cap despite weaker bidding activity.

For certificates without renewable designation, traded volume rose 69.3% from the previous round. For renewable-designated certificates, volume increased 31.7%.

Total buy bids have fallen by more than 50% from the first round, continuing a downward trend seen across three consecutive auctions. However, demand still exceeds available supply.

TAKEAWAY: Despite declining buy bids, the market remains structurally tight. Compliance demand for nonfossil value continues to exceed supply, keeping prices at the ceiling. As in FY2024, companies may again be allowed to substitute FIT certificates to meet their obligations if shortages persist. The rebound in traded volume after the second round also suggests that corporate demand for renewable attributes remains firm, even as bidding activity moderates.

ANRE has proposed revisions to the price caps and floors for non-fossil certificates (NFC) during the third phase of the scheme (FY2026–FY2028).

For the FIT certificate market (renewable energy value), the price floor will rise from ¥0.4/ kWh to ¥0.6/ kWh in FY2027, matching the current floor for non-FIT certificates. The price cap of ¥4 may be abolished during Phase 3, potentially by FY2028.

For the non-FIT certificate market, the floor will increase from ¥0.6 to ¥0.8 by FY2028, reflecting inflation since the market’s creation in 2021 and aligning incentives with the new mandatory carbon pricing scheme (GX-ETS). The price cap will remain at ¥1.3, which effectively limits the compliance cost for electricity retailers.

The government indicated that price levels will remain unchanged in FY2026 to allow market participants time to prepare. Starting in FY2027, the government may revise the Phase 3 supply–demand balance for interim targets, potentially incorporating a supply buffer to reduce the likelihood of certificate shortages and price spikes.

CONTEXT: The government has been discussing revisions to price caps and floors for NFC markets in Phase 3 (FY2026–FY2028), while continuing to expand non-fossil power through measures such as the long-term decarbonized power sources auction (LTDA) and the FIT/FIP schemes.

TAKEAWAY: Raising the FIT price floor and removing its cap could shift demand away from FIT certificates toward direct purchases of non-FIT certificates. However, the resulting changes in non-FIT supply are difficult to predict and could tighten the market, pushing prices to the cap and increasing costs for retailers. The government is therefore considering adjusting Phase 3 supply–demand targets from FY2027 to mitigate this risk.

The Transmission and Distribution Grid Council (TDGC) plans to launch the next-gen central load dispatching system in FY2032, postponing the original late-2020s target.

The system will integrate nationwide supply-demand adjustment data and enable congestion-aware grid operation.

It will consist of a central system and regional systems, standardizing dispatch specifications across areas and incorporating SCUC (Security Constrained Unit Commitment) and SCED (Security Constrained Economic Dispatch) functions to optimize unit commitment and dispatch while minimizing balancing costs.

Shared use among utilities is expected to reduce costs and improve resilience, while integration may also help address shortages of system engineers.

CONTEXT: The TDGC has set the goal of “standardizing the specifications of central load dispatching systems.” In response, TSOs have been studying system sharing. Initially aiming for operation in the late2020s, the target was postponed to accommodate Japan’s unique systems and equipment constraints.

Hokkaido Electric will move forward with construction of Unit 2 at Ishikari Bay New Port Power Station. Work will start earlier than expected, in August 2026.

The utility revised the output capacity of Units 2 and 3 from 569.4 MW to 580 MW.

Unit 2 has a planned start of operation in FY2030; Unit 3 construction will start in May 2030, operation in FY2033.

Both units will run on LNG, but the company plans to consider future decarbonization options such as hydrogen combustion.

KHI signed an MoU with Alderley Saudi Arabia for a service partnership for centrifugal hydrogen compressors that are used in the oil and gas industry.

The deal includes local packaging work, sales, and maintenance for compressors.

TAKEAWAY: The collaboration is in preparation for future hydrogen energy markets. Saudi Arabia and other Middle Eastern countries are interested in hydrogen-based energy systems. KHI seeks to play a role in this development.

The Development Bank of Japan and eight private railway operators will invest in RD Solar Power, which will operate a 21.75 MW solar farm in Rokkasho (Aomori Pref).

The facility is expected to start operations and supply electricity to investing rail operators (Odakyu, Keio, Keisei, Keikyu, Seibu, Sotetsu, Tokyu and Tobu) in 2029.

TAKEAWAY: Since 2022, Tokyu has powered all of its railway lines using renewable electricity backed by the purchase of FIT NFCs, and since 2024 Seibu has supplied 100% of its rail operations with renewable electricity procured through TEPCO. The other companies have not yet announced full renewable coverage of their train operations, although they are expanding green procurement. In FY2022, transport accounted for roughly 18% of Japan’s total GHGs, with rail representing only about 4–5% of transport emissions. Beyond the decarbonization of electricity, the main source of consumption, railway decarbonization involves the introduction of fuel-cell powered rolling stock, energy efficiency in stations and diesel-electric units, multi-mode traction systems, automatic train operations, and installation of on-board storage batteries.

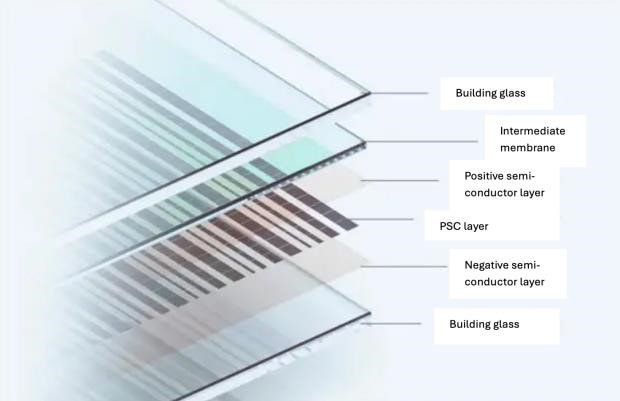

YKK launched a joint demo of BIPV PSCs in Sapporo City Hall.

EneCoat Technologies supplied the cells to YKK, which developed a BIPV interior window installation solution.

The demo aims to evaluate window insulation performance and PSC power generation in a snowy and cold climate, and is expected to run until January 2027.

CONTEXT: In 2024, YKK first partnered with the city of Sapporo to test PSCs during the Sapporo Snow Festival, where power generation under snow-reflected light was confirmed. This aspect is particularly important, as BIPV solutions help mitigate risks associated with snow accumulation on ground-mounted solar structures.

Hankyu Hanshin’s new building (Osaka Pref) will feature 18 PSCs, each 1.4 meters high, along a balcony. The glass-type PSCs will be supplied by Panasonic HD.

The building has already received ZEB Ready certification and a five-star rating under the DBJ Green Building program. o Construction on the building is scheduled for completion in December 2027.

CONTEXT: The DBJ Green Building certification evaluates the environmental performance of buildings and is operated by Development Bank of Japan in cooperation with the Japan Real Estate Institute. ZEB Ready refers to buildings whose energy consumption is at least 50% lower than that of standard buildings, excluding renewable energy use, and represents a step toward full ZEB certification.

Seiko Electric agreed with RKP (Dalian Rongke Power) on R&D in redox flow batteries, combining Seiko’s expertise in EMS and PCS (Power Conditioning Systems) with RKP’s battery cell technology.

CONTEXT: Redox flow batteries store energy in two electrolyte solutions in separate tanks, which decouples the system’s energy capacity from the power of the cell stack. They are mostly used in stationary applications due to their large size. Vanadium redox flow batteries are the most popular, with a lifespan exceeding 20 years.

TAKEAWAY: Suited for long-duration, stationary energy storage due to high safety (the electrolyte is not flammable) and low degradation over time, the redox flow battery market in Japan is expected to grow, with Sumitomo Electric the main manufacturer with more than 50 MW total capacity installed.

ESREE Energy, Digital Grid and ReGACY Innovation Group raised funds to develop heat-storage technology using gravel to decarbonize industrial heat. The amount raised was not disclosed.

ESREE Energy aims to convert surplus solar-derived electricity into heat, store it, and supply lowcost industrial steam in a reliable way, including at nighttime. The company’s technology is based on Pumped Thermal Energy Storage, which combines a high-temperature heat pump with a Rankine-cycle power generation system.

CONTEXT: A Rankine cycle is a thermodynamic process that converts heat into electricity by vaporizing a working fluid to drive a turbine connected to a generator. It can use various heat sources, including renewable heat or stored thermal energy.

TAKEAWAY: Decarbonized LDES (Long-duration Energy Storage) is part of Japan’s GX policy, as thermal storage can help manage surplus renewable electricity alongside BESS. For example, Toshiba ESS and Chubu Electric plan to install a 10 MWh rock-based thermal energy storage facility in Aichi Pref, expected to launch in FY2029.

GATES agreed with KEPCO to help search for sites for BESS stations and evaluate the profitability of potential projects.

CONTEXT: In May 2025, KEPCO launched a support service for BESS stations, providing feasibility studies, development assistance, financing support, and operational assistance. The company aims to provide this service to up to 1 GW of BESS capacity by the early 2030s and seeks partners.

Suzuki agreed with Kanadevia to acquire its all-solid state battery business. Operating results, assets and liabilities have not been disclosed.

CONTEXT: Kanadevia started production in 2006 using a dry manufacturing method that prevents liquid leakage and allows operation over a wide temperature range.

Startup 3DC raised ¥370 million in a Series A second close, bringing total round funding to ¥2.82 billion to develop an advanced carbon materials platform.

CONTEXT: The company develops Graphene Mesosponge (GMS), a 3D porous graphene structure designed to enhance electrical conductivity and stability in battery electrodes, improving the power– capacity–lifetime in lithium-ion systems.

The company is building the world’s first GMS production facility in Toki, Gifu Pref.

In April, Aisin will launch a solar-priority mode in its Ene-Farm type S residential energy system to enable customers to switch from selling solar power to self-consumption, avoiding selling electricity at a lower unit price after the FIT system expires.

Under this mode, the battery:

automatically adjusts electricity use depending on solar generation during sunny or cloudy daytime periods;

prioritizes self-consumption when most economical for households.

Kamigumi plans a 20 MW / 80 MWh BESS in Oita (Oita Pref).

Start of operations is set for March 2029, using batteries supplied by PowerX.

CONTEXT: Primarily a logistics company, Kamigumi is expanding into BESS to address its own logistics-related energy needs while also pursuing overall profitability.

Commercial operations started at the Kitakyushu Hibikinada Offshore Wind Farm in Kitakyushu. It is Japan’s largest operational offshore wind facility.

The project comprises 25 turbines (9.6 MW each) installed across a 2,700-hectare sea area, with a total capacity of 220 MW.

Electricity will be sold to Kyushu Electric Power T&D under a 20-year, ¥36/ kWh FIT. Total project costs are estimated at about ¥170 billion.

The project is operated by Hibiki Wind Energy, a consortium including Kyuden Mirai Energy, JPower, Hokutaku, Saibu Gas and Craftia, selected by Kitakyushu City in 2017 as part of an initiative to develop a regional offshore wind industry hub.

Mitsubishi Corp’s withdrawal from three domestic offshore wind projects leaves unresolved local infrastructure, including roughly 400 road excavation sites in Chiba Pref where digging for transmission cable routes has not been fully restored.

The roads remain in temporary repair years after work was carried out.

Similar situations are reported in Akita Pref, where about 100 excavation sites linked to a separate cancelled project remain.

TAKEAWAY: While most focus is on re-tendering the projects that Mitsubishi gave up, this publicity may deter other localities from getting involved in the future. Decommissioning issues appear much later. So, Japan needs to improve the process to provide clarity over what happens to deals with local stakeholder groups, project contractors and grid operators if the original developer walks away.

The Makigawa Masaki Wind Farm – 28.8 MW capacity, but with a derated 25 MW of capacity due to grid restrictions – began commercial operations on March 1.

GF and JR East are project developers. Sumitomo Corp is the aggregator, purchasing all electricity and environmental attributes and selling them through the wholesale market and PPAs. ENEXIA, a Sumitomo firm, will handle balancing operations.

The project was developed under FIT but transitioned to FIP, enabling market-based power sales and bilateral contracts with corporate buyers.

The facility is licensed to operate for 20 years, from March 2026 to February 2046.

METI gave construction firm Toda the green light for a study on a 151 MW wind project in Mindanao in the Philippines.

It will assess the commercial viability and potential equity participation by Japanese companies in what would be Mindanao’s first large wind power project.

Toda said the project already obtained development permits and is negotiating a power sales agreement.

CONTEXT: Japan is promoting clean energy in SE Asia via the state-led Asia Zero Emissions Community (AZEC) framework. This allows Japanese firms to tap state resources to develop clean energy projects in the region.

CONTEXT: Monthly magazine Sentaku offers a behind-the-scenes look at companies, but its sources are usually unnamed and unattributed, making the articles speculative.

Chubu Electric’s recent share price rebound, despite scandals linked to seismic data irregularities at Hamaoka NPP, reflects market expectations of enhanced shareholder returns, including possible dividend increases or share buybacks.

There are questions about internal governance at Chubu Electric following revelations that seismic data irregularities at Hamaoka date back to 2018. It suggests that internal reporting and board-level oversight may have been insufficient, though the full details are expected to emerge in a report to regulators at the end of March.

Prolonged delays to Hamaoka’s restart – potentially 10 years or more – combined with shortened reactor lifetimes could make full decommissioning a possibility.

Despite potential impairment losses of up to ¥500 billion, decommissioning might strengthen Chubu Electric’s investment capacity by avoiding safety upgrades.

TAKEAWAY: There has long been speculation that realignment among the EPCOs will occur around the stronger companies. During the deregulation phase of the previous decade, that would have been highly unlikely. Today, with vast investments needed to upgrade aging infrastructure, this may be looked on favorably by the govt. JERA, Chubu’s JV with TEPCO, has been praised as an example of collaboration.

METI will apply to the village of Ogasawara, Tokyo, to conduct a literature review on Minamitorishima Island.

This regards a potential final disposal site for high-level nuclear waste from NPPS.

Minamitorishima is Japan’s easternmost island, located about 2,000 km from Tokyo in the Pacific. Only Maritime Self-Defense Force and Japan Meteorological Agency staff are based there.

CONTEXT: Selecting a final disposal site involves a three-stage process that takes about 20 years. Phase one is the Literature review (collecting records). Phase two is Preliminary investigation (boring surveys). The final phase is Detailed investigation (underground facilities). Waste must be buried deeper than 300 meters.

TAKEAWAY: This is a shift in strategy from the previous “local application” method. Previously, the national govt waited for municipalities to volunteer. The previous volunteer-based system has stalled. METI’s move is aimed at accelerating the selection of a final disposal site. Since 2020, only three municipalities (Suttsu and Kamoenai in Hokkaido, and Genkai in Saga Pref) have started literature surveys. Also, progress is facing political opposition, particularly from the Hokkaido governor. In response, METI Minister Akazawa stated in January that the national govt would take responsibility for requesting cooperation. Using a remote island could seem a smooth way to solve the issue. But, it could also create international issues with bordering countries.

GE Vernova’s nuclear subsidiary, GE Hitachi Nuclear Energy (GVH), will develop a design for the BWRX-300 SMR (300 MW) for use in Poland.

GVH inked a deal with Orlen Synthos Green Energy (OSGE), a JV between Polish state-owned and private companies.

CONTEXT: In December 2023, the Polish govt approved a plan to build up to 24 BWRX-300 reactors. Creating a standardized reactor design will make it easier to deploy BWRX-300 units.

Mitsui & Co invested in MiRESSO, a Japanese startup developing technology for fusion energy.

MiRESSO is a startup linked to the National Institutes for Quantum Science and Technology. It focuses on refining beryllium, a mineral essential for fusion reactors.

It can refine beryllium at ~300°C, compared with about 2,000°C in conventional methods. This method is cheaper and more energy-efficient.

CONTEXT: This is Mitsui’s third investment in fusion energy. It follows investments in Kyoto Fusioneering in 2023 and Commonwealth Fusion Systems in 2025.

CONTEXT: Beryllium helps produce tritium, a fuel needed for fusion reactions. A single fusion reactor needs hundreds of tons of beryllium, but global production is only about 300 tons per year.

Japanese oil refiners asked the govt to release crude from strategic petroleum reserves as tensions in the Middle East incite concerns about supply disruptions.

The companies seek access both to state-controlled reserves and to crude stored in Japan under joint stockpiling arrangements with suppliers such as Saudi Arabia, the UAE and Kuwait.

Refiners also asked authorities to speed up the process, as standard bidding procedures could delay deliveries.

CONTEXT: Japan imports more than 90% of its crude oil from the Gulf, leaving it highly exposed to potential disruption of shipments through the Strait of Hormuz.

At least one refiner has already canceled planned exports of gasoline, jet fuel and diesel to prioritize domestic supply.

TAKEAWAY: See this week’s Analysis section for a deep dive into Japan’s oil, gas and other stockpiles and the fallout from the war in Iran.

JAPEX will withdraw from a planned LNG terminal project in Vietnam, citing poor profitability prospects.

JAPEX joined the project in 2022 by acquiring a minority stake in a local company. The initial plan called for facilities capable of handling up to 650,000 tpa.

JAPEX will sell all its shares in the local company to a co-investor. While the sale amount was not disclosed, JAPEX said its ownership stake was below 50%.

CONTEXT: The company targeted a FID in 2022 and start of operations in 2025. Yet, the project faced delays, with no FID made or construction started. JAPEX said securing customers and procurement sources was more difficult than expected.

JERA is evacuating staff from the Gulf region following U.S. and Israeli attacks on Iran and that country’s response targeting other American allies in the region.

CONTEXT: Chiyoda Chemical was also reported to evacuate its personnel in Qatar and UAE. The firm suspended construction at a LNG plant in Qatar. INPEX took similar measures. Japan has a heavy dependence on Middle East energy. Tohoku Electric has a contract for LNG supply from the Qatargas 3 project. Also, LNG from Qatar made up 13% of KEPCO’s procurement of the fuel in FY2024. Japanese companies are considering measures if disruptions at the strait of Hormuz continue.

Osaka Gas christened its first LNG bunkering vessel, Seto Azure.

It has electric propulsion with a dual LNG/ fuel oil engine.

The ship will begin operations in April and will supply LNG to LNG-fueled vessels at sea, including capesize bulkers operated by MOL, “K” LINE, and NYK.

This is a new ship-to-ship bunkering method, to complement Osaka Gas’s existing truck-to-ship and port-to-ship operations.

By offering all three bunkering methods, Osaka Gas intends to ensure a stable and flexible LNG fuel supply.

There are also plans to introduce e-methane as a next-gen marine fuel to further reduce carbon emissions.

As of March 1, the LNG stocks of 10 power utilities were 2.19 Mt; up 9.5% from the previous week (2 Mt); up 3.3% from end March 2025 (2.12 Mt), and up 1.9% from the 5-year average of 2.15 Mt.

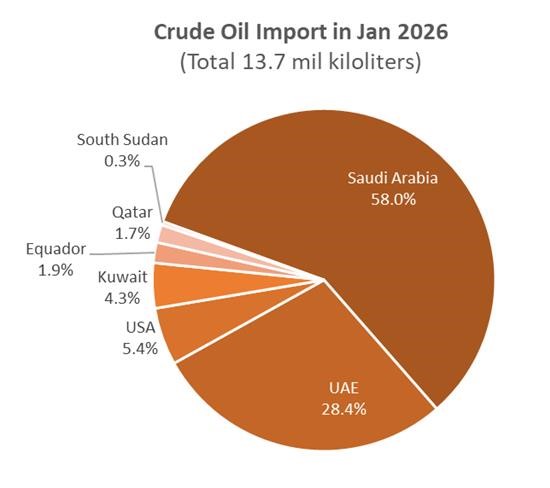

In January, Japan imported 13.7 million kiloliters of crude oil, down 2.5% over December 2025, but up 5.7% YoY. The total value was ¥901.6 billion, down 5.8% MoM, and down 8.1% YoY. Import sources narrowed to just seven countries in 2026, from 16 in 2025. A little over 92% of the oil came from the Middle East.

As of late February, a large number of oil tankers destined for Japan were trapped in the Hormuz Strait. The govt said that oil reserves can last for 254 days. If the crisis in the Middle East resolves in a month or so, Japan’s energy market will see no significant impact.

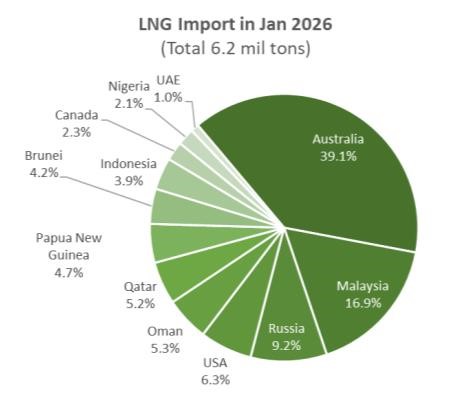

LNG imports in January totaled 6.2 Mt, down 4.5% over December 2025 (6.5 Mt) and down 6% YoY. LNG was sourced from 12 countries, down from 18 in 2025. Australia remains the biggest LNG exporter to Japan, followed by Malaysia. Total import value was ¥546.2 billion, down 2.6% over December, and down 18.1% YoY.

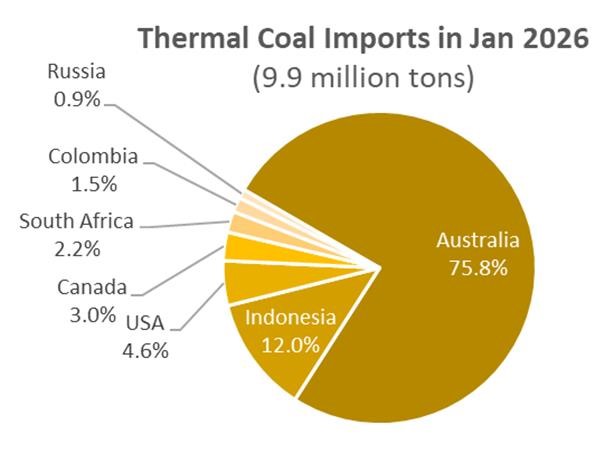

Thermal coal imports totaled 9.9 Mt, up 5.9% from December 2025 (9.3 Mt), but down 4.8% YoY. The import value totaled ¥190 billion, up 7.9% over December, but down 21.8% YoY. Australia is the primary source for Japan, sourcing three-quarters of thermal coal. Sources of imports decreased to seven countries, compared to 10 in 2025.

JAPEX is conducting exploratory drilling for two test wells offshore Tomakomai to assess geological conditions for its carbon capture and storage (CCS) project there.

The project would store CO2 captured from industrial sources such as Idemitsu’s Hokkaido refinery and Hokkaido Electric’s Tomato-Atsuma power station.

The planned storage volume is 1.5 to 2 million tons a year (Mtpa), with the aim to begin storage operations by the 2030 fiscal year.

The drilling results will help determine whether the project can move toward a final investment decision in FY2026, as Japan seeks to scale up CCS to support its decarbonization strategy.

ANALYSIS

BY YURIY HUMBER

War On Iran Tests Japan’s Energy Security System

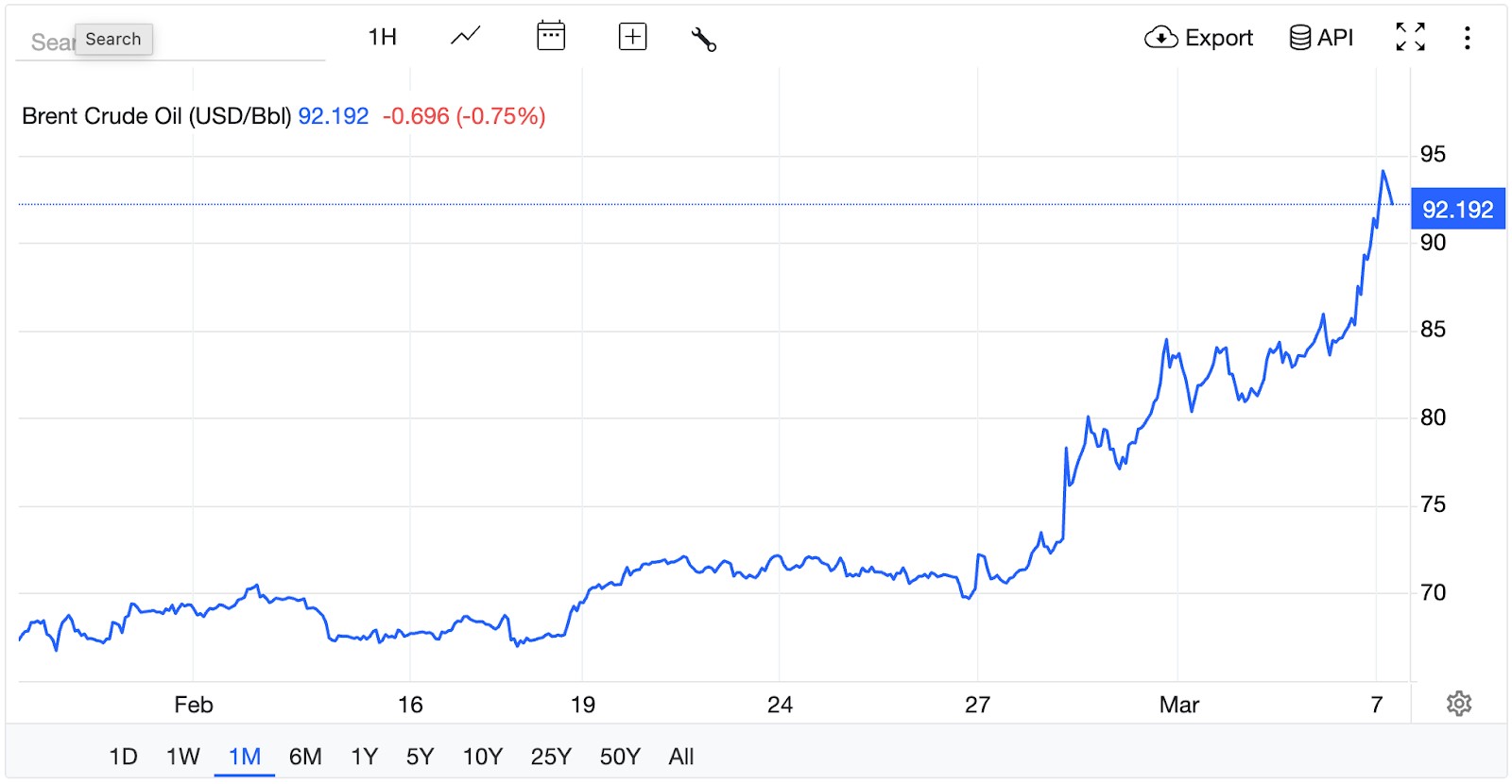

The U.S. war on Iran and escalation across the Persian Gulf over the past week has provided a real-time stress test for Japan’s energy security architecture. So far, the system has held up well. The country’s crude oil reserves – the world’s fourth-largest – combined with a diversified LNG portfolio and subdued seasonal power demand have shielded the economy from supply disruptions.

The longer-term picture, however, looks complicated. The distinction between a shortlived shock and a conflict that drags on for months or years could prove decisive. The war in Ukraine offers a sobering precedent: what began as a three-day ‘special operation’ evolved into a four-year war of attrition that reshaped global energy markets. A similar dynamic in the Gulf would test Japan’s resilience far more severely.

For now, the risk of physical shortages remains limited. But the economy is still exposed to higher import prices, shipping disruptions and financial market spillovers. Rising fuel costs could feed into electricity tariffs, manufacturing costs and inflation. A prolonged crisis could weaken the yen further, reinforcing the price impact of imported energy.

Electricity markets illustrate this dichotomy well. Prices for immediate delivery of power have barely moved since the initial strikes. By contrast, forward contracts – used by utilities and traders to hedge future electricity sales – have surged. In some cases, prices for delivery later in the year have jumped by over 80%. The risk of tighter LNG supply is being priced into contracts starting as early as April.

PM Takaichi’s government still retains several levers to manage electricity prices in the short to medium term. Utilities can increase coal use, restart idled oil-fired plants or draw on emergency fuel reserves, though the trade-offs would be higher costs and emissions. A much worsening situation could even provide political momentum for faster nuclear restarts.

Still, if the conflict drags on – as leading global oil benchmarks suggest – the fiscal resources required to cushion households and industry from higher energy prices could limit the government’s ability to fund longer-term infrastructure and energy-transition investments. And a war-induced downturn in the global economy would dampen demand for Japanese machinery and other exports.

Global oil benchmark, Brent (covers two-thirds of the world’s oil)

Source: Trading Economics

Background: what happened

On February 28, while diplomatic talks were underway, the U.S. and Israel launched a wave of air and missile strikes against Iranian military, nuclear and political targets. Washington claims to have decapitated Iran’s leadership, but the country continues to fight back, directing missile and drone attacks targeting Israeli territory as well as U.S. military facilities and infrastructure in several Gulf states including Qatar and Bahrain. The exchange has quickly expanded into a regional crisis, drawing in proxy actors and raising fears of broader escalation across the Middle East.

Vitally, Tehran has threatened shipping in the Strait of Hormuz, warning vessels not to transit the waterway. The resulting security risk has effectively halted most commercial traffic through the strait, a chokepoint that normally carries roughly one-fifth of global oil supply and a similar share of LNG trade.

Impact on energy sector

Oil dependence

Last year, 94% of Japan’s oil imports came from the region, supplied primarily by Saudi Arabia, the United Arab Emirates, Kuwait, Qatar, Iraq and Oman. Disruptions to the Strait of Hormuz pose an obvious and outsized risk as 80% of the Middle Eastern oil bound for Japan passes through it. As of early March, around 40 Japan-bound ships were reported waiting inside the Persian Gulf rather than attempting to transit the strait.

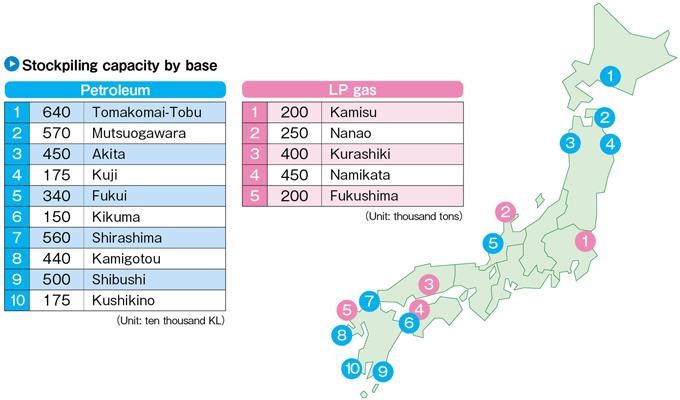

Japan’s large oil reserves are its primary buffer. The latest ANRE data show that the country holds 254 days of crude oil stockpiles. However, this headline figure combines several distinct reserve categories. The first is the national strategic reserve, operated directly by the government and managed by JOGMEC. As of December 2025, national reserves stood at around 146 days.

The second category consists of commercial inventories held by private oil companies, which amount to roughly 101 days of demand. This is higher than the sub-80 days level that firms used to hold two-three years ago and reflects learnings since the war in Ukraine, which upended energy supply chains. The private stockpiles are also mandated by law.

A third, less widely discussed category consists of joint stockpiles held with oil-producing nations. Under these arrangements, producers such as Saudi Arabia, the UAE and Kuwait store crude in Japan. The oil remains their property but can be prioritized for Japanese use during emergencies.

Policy discussions inside METI suggest a clear strategy for any potential drawdown. In a Middle East crisis, officials would first release high-mobility private stocks and oil stored at national bases capable of rapid distribution, preserving slower-moving strategic reserves for more severe disruptions.

In other words, Japan’s oil security system is designed as a tiered response mechanism capable of smoothing supply shocks over several months.

Nationalstockpiles

Private-sector stockpiles

Stockpiles held jointly with oil-producing nations

petroleum

41.79 million kiloliters

13.72 million kiloliters

2.07 million kiloliters

(days of consumption)

146 days

101 days

7 days

Source: METI / ANRE

Gas dependence

Japan’s LNG exposure to the Gulf is far smaller but still significant. Qatar, Oman and the UAE together supply roughly 10-12% of Japan’s LNG imports, equivalent to around 7 million tons annually. Only a month earlier, JERA had signed a 27-year contract with Qatar that would add 4 Mt to that number.

Most of the Middle East LNG volumes are delivered under long-term contracts, which provide price stability. But even contracted fuel supply can be disrupted by physical or logistical constraints. With Iran declaring its intent to stop all traffic entering the Strait of Hormuz, on March 4, QatarEnergy declared force majeure and halted operations at key facilities for at least two weeks.

The company’s core Ras Laffan site was also hit by Iranian drones. The extent of the damage is unclear but repair work will likely require substantial time.

Even once operations resume, LNG production cannot restart instantly. Liquefaction plants require several weeks to cool and stabilize before exports can resume. Replacing Middle Eastern cargoes is possible but costly. Japanese buyers may request additional shipments from producers in Australia, the U.S. or Southeast Asia, though their spare capacity is limited.

Turning to the spot LNG market would expose Japan to intense competition. Europe is emerging from a winter season with reserves at 30% of capacity (compared to 45% on average at this time of year). Europe will need to replenish underground gas storage ahead of the next heating season. Asian buyers that are highly dependent on Qatari supply will also be scrambling for any available cargos.

In the past week, Asian and European LNG benchmarks have surged toward $20 per MMBtu, while the U.S. Henry Hub benchmark – reflecting domestic supply conditions – has remained largely unchanged.

Unlike oil, LNG cannot be easily stockpiled. Japan can hold only two to three weeks of buffer supply, making it sensitive to shipping disruptions. Domestic LNG reserves are about 4.4 Mt, according to Kpler.

One bright spot is liquefied petroleum gas (LPG), widely used in Japanese households for cooking and heating. Japan imports about 85% of its LPG, but the Middle East accounts for only 3.7% of supply.

The U.S. and Canada together provide nearly 87% of Japan’s LPG imports, with Australia the next biggest seller. Japan also maintains around 110 days of LPG reserves, split between government and private stocks.

Source: JOGMEC

Electricity markets

Spot prices in Japan’s wholesale power market have held around ¥10-11/ kWh, reflecting relatively weak seasonal demand and ample generation capacity.

But futures markets are sending a very different signal. Trading volumes on the European Energy Exchange (EEX) surged at the start of March. Around 5 TWh changed hands on the first trading day of the month, equivalent to about a third of February’s total volumes and a new daily record. The rest of the week saw similarly elevated activity.

The driver is LNG risk. Traders appear confident that short disruptions can be absorbed, but worry that prolonged shipping interruptions will force Japan to switch to more expensive fuels.

Utilities could increase coal-fired generation or temporarily boost oil-fired plants. Spring demand is relatively low, giving utilities some flexibility.

The April 2026 Tokyo baseload contract jumped from ¥11/ kWh at the start of March to ¥20.41 by the close of March 5. Contracts for subsequent months have also risen sharply, with most approaching the ¥19 level. (Tokyo baseload contracts account for about two-thirds of EEX Japan volumes.)

Interestingly, the forward curve begins to ease from late summer, suggesting traders still expect the crisis to resolve or ease substantially by August-September.

Seasonal contracts reflect similar expectations. Prices for the Tokyo Summer 2026 contract climbed to almost ¥19; the derivative covering the winter period rose only slightly and kept around the ¥15.5 level.

Next steps

If the conflict continues, the Takaichi government is likely to pursue several parallel strategies. Diplomatically, Japan will coordinate with producer nations and other major consuming countries. That includes contingency planning with the IEA for coordinated emergency stockpile releases.

Japanese refiners have already asked the government to consider such steps, but much of the industry concern seems to be around speeding up the administration, rather than immediate access to supplies.

Domestically, policymakers may consider temporary fuel and electricity subsidies if energy prices rise sharply. METI and the major importers will intensify efforts to secure replacement LNG supplies.

In the medium term, energy officials are likely to accelerate efforts to restart the reactors that already have regulatory approval. Faster grid connections for battery projects could also help stabilize the system by reducing curtailments.

The longer-term implications, however, could be more significant. A prolonged disruption to shipping through the Strait of Hormuz would reinforce the argument for greater reliance on domestically controlled energy sources.

That strengthens the hand of nuclear, but not only. Next-generation geothermal and solar technologies will attract even more state support. Further LNG supply chain diversification is likely. A national program to revamp grid equipment manufacturing is possible.

In short, Japan’s energy system has proved resilient so far. But the longer the conflict persists, the more strain will fall on the country’s import-dependent energy model. The system is built to weather temporary disruptions. It’s less clear how well it can withstand a world in which those disruptions become commonplace.

Economic Impact of Iran war on Japan, as seen by Nomura Research Institute

Category

Scenario 2 – Base

Scenario 3 – Worst-case

Conflict dynamics

Continues for an extended period

Conflict escalates with strong anti-US sentiment inside Iran

Strait of Hormuz

Not formally closed, but military activity disrupts tanker traffic

Fully closed by Iran

Duration of disruption

Prolonged disruption, but shipping still partially possible

Long-term closure (about 1 year)

Oil price assumption

Oil rises to about $87 per barrel (similar to 2024 Iran–Israel escalation peak)

Oil rises to about $140 per barrel (similar to 2008 pre-financial crisis peak)

Impact on Japan GDP

−0.18% over one year

−0.65% over one year

Impact on inflation

+0.31%

+1.14%

Gasoline prices

About 30% increase, exceeding ¥200/ litre

Much larger increase

Electricity & gas prices

Over 10% increase within 6–12 months

Larger and longer price increases

Economic risk

Significant cost pressure on firms, especially SMEs

Stagflation risk

ANALYSIS

BY ANDREW STATTER

Energy Jobs in Japan: EU vs Japanese Power Market Talent Landscape

Japan is the world’s third largest electricity market after China and the U.S., consuming about 1,000 TWh each year of electricity, the equivalent of 25% of Europe’s total.

Japan has a hybrid power market (partially deregulated); the retail market was fully liberalized in 2016, establishing imbalance settlement based on market price. TOCOM launched power futures in 2019, and EEX launched in 2020 and now has 95% of the market share.

Today, Japan has over 700 Power Producer Suppliers (PPS / energy retail companies), about 300 companies trading on the spot market, and 110 companies trading on EEX. Yet, the Japanese power market is still in its infancy, in particular from a talent perspective.

Last month, Titan headed to E-World Energy & Water in Germany, gaining a chance to contrast the European and Japanese markets from a talent lens.

E-World vs Japanese events

This 25th edition of E-World, Energy & Water in Germany was a record breaking year with over 37,000 attendees from 126 different countries, and over 1,100 exhibitors across power trading, utilities, consulting & analytics, offtake solutions, optimization solutions and data / AI / IoT. The event spanned three days, across six halls of a major exhibition venue.

Smart Energy Week in Tokyo this month has a similar size and scale over three days and boasts attendance and exhibition numbers. But SEW has a large focus on manufacturing supply chains, including OEMs and component suppliers across solar, wind, batteries, IoT systems, EV infrastructure, hydrogen and clean fuels.

For a more power market industry specific comparison in Japan, however, one needs to put the spotlight on Power Week, which takes place in October. This is a conglomeration of events sponsored by key players such as Vanir, EEX, Tullet Prebon, etc, and is more focused on seminars plus evening gatherings over drinks for cross-industry networking.

Power Week has grown from a couple of hundred attendees just four years ago to close to 1,000 in 2025, yet it is still much smaller, less structured and organized compared to events such as E-World in Europe.

The power talent market in Japan is at the same place as renewable energy talent was in 2015 — still nascent, with people joining from adjacent industries and learning as they go. In 2015 we saw an influx of people from manufacturers, finance and real estate move to power developers. Today, we see the shift from commodities, developers and power retailers becoming new power market participants.

Maturity of market, what happens at the event:

For Titan, as a player in the Japanese energy ecosystem, we noticed E-World’s scale as the first and obvious impact. One layer beyond that though is the size of the organizations. Whereas in Tokyo you will have power trading organizations with between two to 20 people in the business across front, middle and back office, at EWorld you would see the major players bringing 10-25 front office people just to the event.

During E-World’s daytime hours, all the trader booths were full and not with people browsing. Meetings were booked ahead of time, clients, partners, offtakers were meeting the traders, getting updates on pricing, products and global expansion efforts. Deals were not necessarily signed on the spot, however a significant effort of account management and new business development was conducted from 9AM to 4PM.

Similar situations at the booths of the solution providers, consulting firms, etc that were also educating new prospects and updating / managing existing relationships. From 4PM the vibe changed, beers cracked open, cocktails started flowing, music began pumping and people let their hair down. Traders caught up with competitors, people exchanged information, views and generally caught up in a relaxed environment.

Japan Power Week is not yet at that stage. Most important matters take place after 4PM, where the traders, originators, brokers, intel providers get together, talk, drink, exchange opinions and gossip. Daylight business still happens, but not so much at the event. Rather, it is more private, behind closed doors, and by invite.

For global companies in the power markets hiring in Japan, whether they be a trader, optimizer, intelligence provider or other, the sheer size of the talent market is a fraction of Europe’s.

Trading ecosystem development:

A similar story played out with other market participants such as trading optimization solution providers, PPA advisories and market intelligence platforms. These players commonly have hundreds of members, with the same 10-25 commercial focused members in attendance, manning the booths, giving demos and working on business development.

Advanced, AI-based trading and asset optimization solutions commonly had teams between 50-200 members, most of them engineers and data scientists. In Japan you may see teams of 5-20, all newer to the market and with a fraction of the number of companies playing the game.

Market intel and forecasting is the same. The booths and show of force from players such as Montel or Volue was impressive – yet in Japan Montel is non-existent and Volue has a small presence. Baringa, Wood Mackenzie and AFRY have direct market presence here, but again this is limited to a handful of people. Aurora would be the exception to the rule, with enough of a local team to be able to host an event, man a booth and show powerful presence.

This is an illustration of a younger market, resulting in a smaller and less experienced talent pool; however, it also demonstrates a more fragmented Asian market. Despite Japan’s impressive market size in terms of TWh procured, it is still a single-country market.

Talent mobility:

Continuing on the theme of Japan as a single-country market, the talent needed to service the industry will not reach Europe’s level, and it does not need to. Language is a major factor. Of over 700 power retail companies, most do not employ any English speakers. Over 90% of staff employed by the 10 power utilities are monolingual Japanese.

Foreign talent makes up about 5% of Japan’s workforce across the wider energy industry. This is in stark contrast to Europe, where members from early movers such as the UK and Denmark mobilize rapidly into high growth markets such as Germany.

Japan has a local, domestic, homogenous talent market, but multinational players are entering the market. Japan is modeling its structures on UK, U.S. and European mature versions; still, at the ground level there is less mobility and exchange of talent.

For global firms looking to hire, the language barrier and lower mobility mean that not only the total market size is smaller, but the total relevant, addressable market is a fraction of what prospective employers have access to back at home.

Andrew Statter is a Partner at Titan GreenTech, an executive recruitment agency focused on the clean energy space.

ASIA ENERGY REVIEW

BY JOHN VAROLI

A brief overview of the region’s main energy events from the past week

Australia / Renewables

Australia’s utility-scale solar PV and wind assets delivered a combined 5 TWh of generation in February, an 11% increase from the 4.5 TWh recorded in the same month in 2025.

China / Hydrogen

Chinese firm Shuangliang said it will send 80 MW of electrolysers to ACME’s 300 MW green hydrogen and ammonia project in the special economic zone at Duqm, Oman.

China / LNG

China is in talks with Iran to allow Qatari crude oil and LNG tankers safe passage through the Strait of Hormuz as the U.S.-Israeli war with Tehran intensifies.

India / Green hydrogen

India recorded its lowest-ever discovered price for green hydrogen and its ambition to achieve green hydrogen at USD 2/kg is not a distant dream anymore, says Niti Aayog’s CEO.

India / Nuclear

Canada and India agreed on a strategic energy partnership, anchored by a C$2.6 billion uranium supply deal and new cooperation across renewables, hydrogen and critical minerals.

Indonesia / Oil & Gas

The Ministry of Energy launched 10 new high-potential oil and gas blocks, following a series of technical studies. These areas are now open to international investors.

Indonesia / Waste-to-energy

Sovereign wealth fund Danantara chose Chinese partners to build waste-to-energy facilities in trash-infested Bekasi and Denpasar. Huzhou-based Wangneng Environment will help Bekasi turn its waste into watts. Zhejiang Weiming Environment Protection inked a deal to operate a facility in Bali’s Denpasar.

Malaysia / Oil

Malaysia can capitalize on oil supply disruption caused by the Iran war by positioning itself as a more reliable energy supplier to Asia, said oil and gas expert Nazery Khalid.

Taiwan / Coal

The Minister of Economic Affairs said coal-fired power generation could be used as a “last resort” if natural gas supply becomes difficult amid the war in Iran.

Thailand / Electricity

National energy demand has grown rapidly. In 2025, peak electricity demand reached 34.6 GW, a 132% increase from 2000’s peak of 14.9 GW.

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

NEWS

・Nuclear plants and copper refinery among next U.S. projects Japan may sponsor

・Insurers consider widening Gulf war-risk zones for shipping insurance

・Residents challenge data center project in Chiba area