WEEKLY

April 6, 2026

ANALYSIS

CARBON PRICING AND NFCs IN JAPAN: RETHINKING DECARBONIZATION INCENTIVES

- This month, Japan launches its mandatory CO2 credits scheme. But recent reforms to non-fossil certificates (NFCs) may be even more consequential for carbon pricing and its impact on the power sector.

- What are the changes and can these pricing signals motivate investment decisions?

ENERGY JOBS IN JAPAN: CLEAN ENERGY CAN NO LONGER HIRE LOCALS-ONLY

- Japan’s past efforts to fill jobs in the renewables sector by relying only on local hires ultimately failed.

- This could repeat. Functions that now bite hardest include power traders and BESS asset managers.

- How will Japan cope with the labor challenge this time? Will it be more open to international hires?

ASIA PACIFIC REVIEW

This column provides a brief overview of the region’s main energy events from the past week

NEWS

- Iran conflict impacts prices across Japan’s economy

- Two Japan-linked vessels transit the Strait of Hormuz

- METI minister also named “critical materials czar” to manage Middle East supply risks

- Japan and France to build rare-earth supply chains

- Spot power prices spike above ¥34 as supply tightens

- OCCTO submits FY2026 supply plan to METI

- Govt launches three working groups on electricity system reform

- Hibiki LNG Power Station starts operations

- Japan to tighten hydrogen/ ammonia eligibility in LTDA auctions

- Renova, partners invest in 90 MW BESS in Shizuoka

- Neoen to open a 100 MW BESS in Hyogo Pref

- Tokyu to power railway lines via solar PPA and green certificates

- Chubu Electric and Toenec to hold a demo of PSCs

WIND POWER AND OTHER RENEWABLES

- J-Power acquires MHI’s onshore wind business

- Akita targets 4.5 GW of renewables by 2035, led by offshore wind

- Eastland Generation launches geothermal plant in New Zealand

- ANRE outlines status of nuclear sector, pledges to complete Rokkasho reprocessing plant

- Kashiwazaki-Kariwa NPP set to reach commercial operation on April 16

- Japan and France deepen cooperation on nuclear fuel cycle and advanced reactors

- JOGMEC introduces initiatives to secure LNG supply

- Japan oil stockpile metrics may underplay total petroleum product consumption

- Energy firms say LNG prices will rise later in FY26

EVENTS

Mid-April FIT/FIP Solar Auction #28

Japan Atomic Industrial Forum

(JAIF) Annual conference @ Tokyo

April 24 Green Elements at Work @ Google for Startups

May 3-6 Golden Week (many companies will close from April 29 to May 6)

May 26-28 Japan Energy Summit @ Tokyo Big Sight

June 3 South Korea – Local Elections

June 23-25 “Summer Davos” in Dalian, China

September 14-18 IAEA General Conference 2026

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Chief Editor)

John Varoli (Senior Editor, Americas)

Kyoko Fukuda (Data, Events)

Magdalena Osumi (Renewables & Storage)

Filippo Pedretti (Thermal, CCS, Nuclear)

Tetsuji Tomita (Power Market, Hydrogen)

Aglaé Bange (Renewables and Biomass)

George Hoffman (Sales, Business Development)

Tim Young (Design)

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

NEWS: GENERAL OUTLOOK AND TRENDS

War in Persian Gulf impacts prices across Japanese economy

(Japan NRG, April 2)

- The war in the Persian Gulf is impacting prices in a number of sectors.

- Fuel prices for Kawasaki city buses doubled, forcing the city to shorten fuel contracts.

- Jet fuel prices doubled in one month, hitting major domestic airlines with an estimated ¥30 billion in extra monthly costs. Flight reductions are possible.

- Farmers face record-high prices and supply shortages for the fuel oil used to heat greenhouses. Rice farmers are dealing with daily increases in tractor diesel costs.

- Fuel costs for deep-sea tuna boats have doubled. Coastal fishing fleets face diesel shortages that might prevent boats from even leaving port.

- Tokyo Gas and ENEOS stopped accepting new electricity supply contracts for large facilities due to LNG prices. Because many power retailers don’t generate all their own electricity, they have to buy from Japan’s wholesale market.

- The Tokyo electricity wholesale price doubled between Feb and early April. TEPCO still takes new applications but needs more time to double-check its supply capacity.

- Unlike Tokyo providers, over 50% of Hiroshima Gas’s LNG comes from Russia’s Sakhalin-2 project. But, because global oil prices are up, their LNG costs are still rising. The company expects city gas prices to increase by summer.

- Online retailers consider raising prices to cover fuel surcharges of delivery firms.

- SIDE DEVELOPMENT:

- Japanese LNG and LPG vessels pass Strait of Hormuz

- (Reuters, Jiji April 3)

- Two ships associated with Mitsui O.S.K. Lines were able to cross the Strait of Hormuz. These are the first Japanese ships known to have navigated the strait since the outbreak of the Iran war.

- The Panama-flagged LNG tanker ship, Sohar LNG, jointly owned by the Japanese shipper, and the Indian-flagged LPG tanker Green Sanvi, owned by an Indian affiliate of Mitsui O.S.K., safely passed the strait, according to Mitsui O.S.K.

- About 45 ships owned or operated by Japanese companies remain stranded in the region. o CONTEXT: Japan relies on the Persian Gulf for roughly 90% of its oil and 6% of LNG imports.

METI minister also named as “critical materials czar” to manage Middle East supply risks

(Government statement, March 31)

- METI minister Akazawa is now also minister in charge of securing critical materials.

- He ordered the launch of a cross-ministerial task force to monitor and respond to supply risks stemming from the Middle East conflict.

- The govt said that while Japan’s overall oil and petroleum product volumes remain sufficient, bottlenecks and uneven distribution have hit parts of the country, prompting the need for coordination across ministries to stabilize supplies of fuel, chemicals, etc.

- Japan is expanding oil sourcing from the U.S., Central Asia and Latin America, while preparing further stockpile releases to maintain stable domestic supply.

- TAKEAWAY: The crisis has emerged from an oil shock to a supply chain problem that – in a worse case scenario – could rival the disruptions of the Covid pandemic. With a fifth of the world’s oil flow disrupted, a long-term effective closure of the Strait of Hormuz could have a greater demand disruption impact than the 2020 pandemic, during which oil demand fell by about 9% YoY. The impact on certain supply chains would be even worse as many materials depend on refined crude oil products for feedstock. From a political perspective, this also gives the METI minister an outsized role in shaping Japan’s response to the crisis.

- SIDE DEVELOPMENT:

- Naphtha supply risks raise concerns over medical equipment shortages

- (Nikkan Gendai, March 31)

- Concerns are growing in Japan over potential shortages of medical supplies as disruptions to naphtha supply threaten production of essential equipment.

- Many critical items, including syringes, dialysis circuits and IV bags, rely on petrochemical feedstocks.

- CONTEXT: The situation underscores the fragility of global supply chains for medical goods, where disruptions in upstream petrochemicals can cascade into healthcare risks.

- SIDE DEVELOPMENT:

- INPEX to supply Japan with crude oil for naphtha production

- (Nikkei, March 31)

- INPEX will supply Japan with an ultra light type of crude oil from Australia instead of selling it on the open market. This oil can be refined into naphtha and gasoline.

- INPEX’s Ichthys LNG project in Australia will supply some byproducts to Japan that usually are sold on the spot market.

- TAKEAWAY: Naphtha is the main feedstock for producing ethylene. More than 40% of Japan’s naphtha imports come directly from the Middle East, and around 20% from other sources. But the oil used for its 40% domestically produced naphtha also comes from the Middle East. Due to the Iran war, the operating rate of Japan’s ethylene producers has fallen from 75.7% in February to 70%, a critical threshold.

Japan and France agree to build joint rare-earth supply chains

(Government statement, April 1)

- Japan and France agreed to develop a roadmap for diversifying supplies of rare earths and other critical minerals, reducing reliance on China.

- The countries will launch a public-private project in south France to refine heavy rare earths used in EV motors and other technologies; operations will begin by end-2026.

- CONTEXT: The deal comes as Japan and France position themselves as like-minded partners linking Indo-Pacific and European security, with leaders emphasizing stable supply of critical materials and coordination through frameworks such as the G7.

- SIDE DEVELOPMENT:

- Mitsubishi Materials invests in U.S. rare-earth recycler to build supply chain

- (Company statement, Nikkei, March 31)

- Mitsubishi Materials invested in U.S.-based ReElement Technologies and signed an MoU on Japan-U.S. cooperation in rare-earth and rare-metal recycling to strengthen critical mineral supply chains.

- ReElement’s chromatography-based technology enables high-purity (99.5%+) recovery of rare earths from scrap such as magnets and batteries.

- The partnership will integrate Mitsubishi Materials into North American supply chains through offtake and tolling agreements.

- CONTEXT: The move comes as Japan and the U.S. step up efforts to reduce reliance on China, which dominates rare-earth processing.

Japan partners with Belgian firm on deep-sea mining of battery metals

(GSR, March 30)

- Global Sea Mineral Resources (Belgium) inked an MoU with Japan’s DORD to hold a demo of deepsea polymetallic nodule mining in the Clarion-Clipperton Zone.

- They plan a test in the early 2030s at depths over 4,000 meters, validating a full mining system including seabed collectors, etc.

- CONTEXT: The Clarion-Clipperton Zone is in the central Pacific between Mexico and Hawaii. It holds some of the world’s largest deposits of polymetallic nodules.

- Polymetallic nodules contain key energy transition metals such as nickel, cobalt, copper and manganese. Japan sees seabed resource development as a priority under its ocean policy framework.

- TAKEAWAY: Deep-sea mining (or “harvesting” as its proponents describe it) is moving from exploration toward pre-commercial testing. For Japan, which has few mining resources on land, this is a major move offering the chance to build its own upstream assets and supply chains, securing strategic control over critical minerals. But, there are many technical hurdles to overcome, as well as environmental and regulatory risks.

NEWS: ELECTRICITY MARKETS

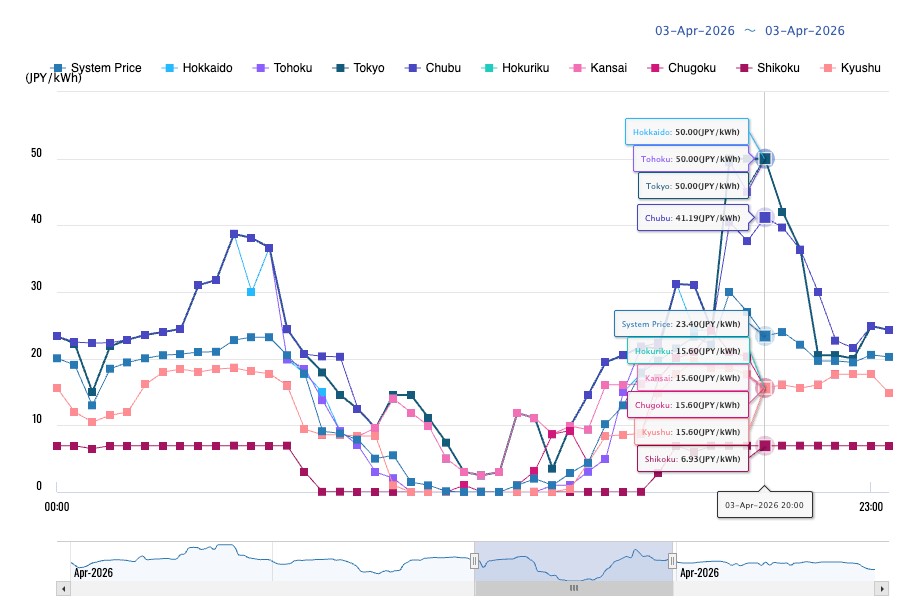

Spot power prices spike above ¥34 as supply tightens

(Exchange data, April 3)

- The wholesale power market surged on April 1, as the system price peaked at ¥34.6/ kWh, and the daily average reached ¥23.15/ kWh, the highest since early 2023.

- Daily average prices eased in subsequent days to ¥17.46 on April 2, and ¥14.68 on April 3, but intraday volatility remained elevated. On April 3, evening peak prices reached ¥50 in Tokyo, Hokkaido and Tohoku.

- Price spreads widened significantly throughout the period, often ranging between ¥10 and ¥40. At the 16:00 slot on April 3, prices briefly spiked to ¥100 – half the market cap – while some periods during the week saw lows near zero (~¥0.01).

- CONTEXT: The price movements reflect tight supply-demand conditions, including reduced thermal generation availability and rising fuel costs, alongside fluctuations in renewable output.

- Volatility remained high during the week, with large intraday swings indicating unstable system conditions and limited reserve margins.

- TAKEAWAY: Japan’s power market is operating with thinner buffers; short-term supply disruptions and renewable variability can trigger extreme price spreads within the same day. Volatility is likely to continue as we move to the low-demand period in late April and May.

OCCTO finalizes and submits FY2026 supply plan report to METI Minister

(Agency statements, March 30 and April 2)

- OCCTO finalized the FY2026 supply plan and sent it to the METI Minister with concerns about securing supply capacity over the mid- to long-term.

- The supply plan shows a sharp decline in thermal power capacity until just before FY2030, followed by a recovery, before stabilizing. Tight supply-demand conditions are evident especially around FY2028, driven by coal phase-out and the replacement of older LNG plants via the LTDA mechanism.

- Demand and supply uncertainty complicate investment decisions, while stranded asset risks limit new investments. Current incentives are insufficient, highlighting the need for stronger policy support and market reforms.

- Looking ahead, rising demand from DCs, EVs, and GX sectors may deepen supply shortages. Stronger policies, improved markets, and better coordination are essential to ensure stable supply while advancing decarbonization.

- CONTEXT: OCCTO is the key body coordinating transmission and distribution networks across regions since electricity market liberalization a decade ago. Its main roles: Aggregating and reviewing electricity supply plans submitted by utilities; Ensuring stable nationwide supply-demand balance; Overseeing cross-regional power flows, grid development, capacity markets, and balancing resources.

- TAKEAWAY: The FY2026 plan serves as a key reference for market participants, investors, and policymakers on whether additional measures (auctions, grid investments, etc.) are required to avoid shortages. The overwhelming message from this plan is that the power sector faces severe pressure from rising electricity demand after years of decline, driven by economic recovery, AI/ data centers, and semiconductor plants. And yet, as OCCTO itself acknowledges, it is difficult in the current environment for generators to make investment decisions due to uncertainties such as delays in DC operations. The onus is now on the state to offer more guarantees for new capacity. This suggests an expanded future role for the LTDA and similar mechanisms.

OCCTO reviews capacity market, signals reforms from FY2026

(Agency statement, March 27 and 31)

- OCCTO has published a comprehensive review of Japan’s capacity market for FY2025, drawing on past auctions and operational experience.

- The report concludes that the market framework is largely in place, but requires further refinement to support stable operation and long-term development.

- From FY2026, reforms will focus on four areas: near-term adjustments ahead of the FY2026 main auction (for FY2030 delivery); broader structural changes led by OCCTO; efficiency improvements based on cost-effectiveness and stakeholder input; and closer coordination with related systems and government bodies.

- CONTEXT: Launched five years ago, the capacity market is now entering a consolidation phase. Notably, the review used a “call for evidence” process – rather than formal public consultation – to gather more detailed stakeholder input.

Govt launches three working groups on electricity system reform

(Government statement, March 27)

- ANRE will continue electricity system reform by reorganizing the System Design Working Group (WG) and the System Review Task Force into three new WGs.

- 1) Power Supply Stability WG will focus on adequate short- and long-term supply capacity while balancing stable electricity supply with decarbonization via mechanisms such as capacity markets, LTDA, and balancing markets.

- 2) Electricity Business Environment Development WG will address a supportive environment for power generation, grid investment, and electricity trading, including public financing and stable business conditions for retail electricity providers.

- 3) Mid- to Long-Term Market Design WG will develop detailed frameworks for mid- to long-term electricity trading markets, covering areas such as pricing, settlement, product design, and market governance.

ANRE discusses challenges toward building next-gen power industry

(Government statement, March 27)

- ANRE discussed challenges toward building a next-gen power industry, focusing on efficient investment in generation and grid through vertical and horizontal collaboration, as well as creating a sustainable industrial base and supply chains.

- The power industry faces key challenges from workforce shortages, driven by aging staff and fewer new workers, and supply chain constraints due to limited manufacturing capacity and reliance on overseas suppliers.

- These challenges require strengthening human resource development and building more resilient and well-coordinated supply chains across the industry.

OCCTO presents results for measures to mitigate impact of reference price increase

(Agency statement, March 27)

- OCCTO has released simulation results on how rising Net CONE (cost of new entry) could affect capacity contribution charges, alongside potential mitigation measures.

- Three options are under consideration: a gradual increase in Net CONE; a hybrid pricing model combining a single-price zone (up to Net CONE) with a multi-price system above it; and a two-tier single-price structure.

- All scenarios point to higher costs for retailers. Estimated charges would rise by 5–17% compared with FY2025 levels, depending on the design, with total costs reaching roughly ¥2.4–2.7 trillion:

- 1) ¥2.4 trillion (+5%) for 1st year (Price cap: ¥20,000/ kW, Net CONE: ¥13,333/ kW); ¥2.6 trillion (+12%) for 2nd year (Price cap: ¥25,000/ kW, Net CONE: ¥16,666/ kW)

- 2) ¥2.6 trillion (+12%) (Price cap: ¥30,000/ kW, Net CONE: ¥20,000/ kW)

- 3) ¥2.7 trillion (+17%) (Price cap: ¥30,000/ kW, Net CONE: ¥20,000/ kW)

- CONTEXT: The analysis follows government discussions in March on raising price caps and Net CONE to incentivise new capacity, while limiting the resulting burden on electricity retailers.

Hibiki LNG Power Station starts operations

(Denki Shimbun, April 1)

- Commercial operations began at Hibiki LNG Power Station, a JV run by Hibiki Power Generation, funded by Kyushu Electric (80% stake) and Saibu Gas.

- The plant (620 MW) is in Kitakyushu City, next to Saibu Gas’s Hibiki LNG Terminal.

- It utilizes a combined cycle system that pairs a gas turbine with a steam turbine, with a thermal efficiency of 64%.

- Hibiki can go from gas turbine ignition to 100% power output in about 60 minutes.

- TAKEAWAY: The power plant could serve as a regulating source to help balance the output of renewable energy facilities.

JERA decommissions its last oil-fired power plant

(Denki Shimbun, April 1)

- JERA decommissioned the Atsumi Thermal Power Station, retiring the remaining units (3 and 4). Units 1 and 2 were already retired.

- JERA said that maintaining the deteriorating equipment was too difficult. The utility no longer owns any oil-fired thermal power plants.

- The retirement won’t affect current power supply and demand.

- CONTEXT: Unit 1 began operating in 1971, while Units 3 and 4 launched in 1981.

- JERA is discussing future uses of the site with the community. The schedule for dismantling the main facilities is undecided.

MHI and Kyoto Univ to research boosting GTCC power plant efficiency

(Company statement, March 30)

- MHI and Kyoto University launched the “MHI Innovative Combustion Dynamics Laboratory” to develop GTCC power plants with 70% efficiency and carbon-neutral combustion technology.

- CONTEXT: GTCC systems now have a 64% high efficiency rate using natural gas and lower CO2 emissions compared to coal-fired power.

Osaka Gas to double U.S. gas-fired plants

(Nikkei, April 2)

- Osaka Gas plans to double its U.S. gas-fired power generation, adding up to five new plants (from current five) to meet surging electricity demand from AI data centers.

- The move is separate from the $550 billion Japan-U.S. tariff and trade deal. Other Japanese firms like SoftBank, Panasonic, and Murata are also investing. U.S. power prices have jumped 10-fold in some regions.

- Osaka Gas thinks its overseas energy ventures will soon generate more profit than domestic operations.

- CONTEXT: Osaka Gas, however, must navigate logistical hurdles, especially equipment delivery delays such as gas turbines and grid connection challenges.

TEPCO launches VPP visualization platform with Tokyo to track power flows

(Company statement, March 30)

- TEPCO launched an online “VPP visibility map” with the Tokyo Metro Govt to show electricity flows between public facilities as part of a virtual power plant demo.

- The platform shows solar generation, electricity demand and power transfers between facilities, updated every 30 minutes, enabling real-time matching of surplus and deficit sites.

- The project aims to improve utilization of distributed renewables and show area-wide energy management.

NEWS: HYDROGEN

Japan to tighten hydrogen/ ammonia eligibility in LTDA auctions

(Government statement, April 3)

- The govt will introduce stricter eligibility criteria for hydrogen and ammonia projects in the 4th LTDA round, requiring all fuel to meet the “low-carbon” definition under the Hydrogen Society Act.

- CONTEXT: The Act specifies a carbon intensity threshold of around 3.4 kg-CO2e/ kg-H2, or 0.87 kgCO2e/ kg-NH3 (well-to-gate).

- Pre-screening of projects for R4 will favor projects with Japanese participation, which must show potential upstream investment by Japanese firms and include the use of Japanese technology or equipment at a key stage in the supply chain.

- The govt plans to open a public consultation on the new pre-screening framework in mid-April for about one month.

- METI discussions on the LTDA consider requiring winners of previous auction rounds to revise their decarbonization roadmaps to use the “low-carbon” hydrogen/ ammonia definitions, replacing colorbased terminology.

- Separately, METI is reviewing penalty rules for projects unable to reach FID due to upstream supply constraints. A proposal would waive the standard exit penalty if FID can’t be secured within eight months of auction award due to actions by a third party.

KHI to supply 14 gas engines to Toho Gas

(Company statement, April 2)

- Kawasaki Heavy Industries will provide Toho Gas with 14 gas engines; each will generate 7.5 MW for a 100 MW-class plant.

- These engines currently run on natural gas, but can be modified later to run on hydrogen.

- They have a power generation efficiency of 49.5%, and can start and stop fast, acting as a balancing power source to support the grid as renewable energy expands.

NEWS: SOLAR AND BATTERIES

Renova and partners invest ¥6 billion in 90 MW BESS in Shizuoka Pref

(Company statement, March 31)

- Renova, NCS RE Capital and SMFL Mirai Partners invested ¥6 billion in a 90 MW / 270 MWh BESS facility in Kikugawa (Shizuoka Pref), to start operation in 2028.

- CONTEXT: The agreement follows a framework similar to that used for Renova’s Himeji BESS project (10 MW/ 27 MWh, Hyogo Pref) in 2023.

- By 2030, Renova aims to invest in a total of 900 MW of BESS capacity. To date, the company has invested in 352 MW of BESS capacity.

- SIDE DEVELOPMENT:

- Neoen to open a 100 MW BESS in Hyogo Pref

- (Company statement, April 2)

- Neoen will open a 100 MW / 400 MWh BESS station in Ako (Hyogo Pref), with operation expected to begin in 2028.

- CONTEXT: Neoen holds a global BESS portfolio totalling 2.8 GW / 8.1 GWh across seven countries, mostly Australia. The company plans to commission more BESS stations in Japan (projected installed capacity not disclosed). EDF Japan is the other major French company involved in the BESS market, with a 110 MW / 330 MWh asset won in LTDA’s second round.

- TAKEAWAY: Large-scale BESS projects (above 30 MW) have been experiencing a significant increase in Japan, particularly since 2025, with most EHV projects scheduled for the end of the decade. Furthermore, the recent entry of major foreign players in addition to Chinese battery suppliers reflects the market’s rapid expansion and investor confidence.

Eurus Energy to build 30 MW BESS in Hokkaido

(Company statement, March 30)

- Eurus Energy began building a 30 MW/ 143 MWh BESS station in Shiranuka (Hokkaido), with commercial operation to begin in 2028.

- The batteries will be lithium-ion systems supplied by GS Yuasa; Kyocera Communication Systems will be the EPC contractor.

- CONTEXT: With this project, Eurus Energy will have a total of five BESS assets in Japan, including another facility in Ikeda (Hokkaido), capacity 10 MW / 27 MWh.

Brawn Capital agrees with HiTHIUM for 3 GWh of energy storage in APAC

(Company statement, March 30)

- HiTHIUM agreed with Brawn Capital to deploy 3 GWh of long-duration energy storage in the AsiaPacific region by 2030.

- CONTEXT: Twenty UHV projects financed by Brawn Capital are in the preparation phase, with 300 MWh of energy storage systems scheduled for delivery by 2027. HiTHIUM is targeting up to 30% of Japan’s market for energy storage batteries and utility-scale BESS.

Blue Sky Energy agrees with Sungrow on BESS supply

(Company statement, March 24)

- Blue Sky Energy agreed with Sungrow for procurement of grid-scale BESS.

- The company aims to develop 100 projects, but no timeframe was stated.

- CONTEXT: This deal comes amid a series of BESS developed recently by Blue Sky Energy: three in Kyushu and one in Chubu; each 2 MW / 8 MWh capacity.

- SIDE DEVELOPMENT:

- NEXTES agrees with AESC for supply of battery storage cells

- (Company statement, April 1)

- NEXTES agreed with AESC to supply 1.5 GWh of battery cells over three years.

- CONTEXT: NEXTES develops and sells next-gen Battery Management Systems and modules for lithium-ion batteries. AESC focuses on battery solutions for EVs.

Tokyu to power railway lines via solar PPA and green certificates

(Company statement, March 31)

- Starting this month, Tokyu will supply its railway lines with green electricity from a 98 MW solar power plant under a 25-year corporate PPA.

- Annually, 370 GWh of green electricity will be supplied by SPCs in which Tokyu has invested, with 30% to be procured together with environmental value by FY2028.

- TAKEAWAY: Railway companies, which need stable electricity supply to operate electric trains, are ideal PPA buyers. Beyond local operators, JR companies are among the key drivers of PPA adoption in the railway sector. In 2025, JR East secured a PPA to procure 90 GWh of electricity annually from biomass and hydropower plants. Earlier this year, JR Kyushu signed a PPA for a 14 MW wind power plant to supply electricity to local shinkansen. For more on the procurement of environmental value via PPAs, see this issue’s analysis section.

Chubu Electric and Toenec to launch a demo of PSCs

(Company statement, March 27)

- In July, Chubu Electric, Chubu Electric Power Miraiz and Toenec will launch a demo of PSCs in Toyota (Aichi Pref), installing cells on the roof of a park building.

- The demo aims to evaluate power generation performance, long-term degradation, and installation methods in places where deploying lightweight and thin cells is challenging.

- SIDE DEVELOPMENT:

- Sekisui Chemical and Solafil launch new film-type PSCs

- (Company statement, March 27)

- Sekisui Chemical and Solafil launched a new film-type PSC model.

- Cells will be installed on metal roofs in Tokyo, Saitama, Shiga and Fukuoka Prefs.

KEPCO agrees with Mitsubishi in EMS for EVs

(Company statement, March 26)

- Kansai Electric will partner with Mitsubishi Motors to develop an EV-EMS that collects data on EV electricity consumption; Solar power generation forecasts; Vehicle mobility; and Battery charge.

- The system aims to optimize battery control based on supply-demand forecasts.

NEWS: WIND POWER AND OTHER RENEWABLES

J-Power completes acquisition of Mitsubishi Heavy’s onshore wind business

(Company statement, April 1)

- J-Power completed acquisition of MHI’s domestic onshore wind business, strengthening its engineering and service capabilities in the sector.

- The assets are now owned by a new entity, J-Wind e Solutions (JWeS), which will provide engineering and after-sales services for existing Mitsubishi wind turbines.

- CONTEXT: The acquisition is expected to enhance reliability of J-Power’s wind assets and support new development, building on the firm’s position as Japan’s second-largest wind power operator.

Akita targets 4.5 GW of renewables by 2035, led by offshore wind

(Government statement, April 1)

- Akita Pref adopted its third energy strategy, targeting expansion of renewable energy led by offshore wind, with total installed capacity to reach 4.49 GW by FY2035.

- The plan builds on strong progress under the previous strategy, with renewable capacity expected to reach around 1.79 GW by FY2025, exceeding earlier targets. New interim targets call for 2.57 GW by FY2030 and further expansion thereafter.

- Offshore wind is positioned as the core strategy, reflecting Akita’s role as a leading development hub. Wind capacity alone is expected to more than triple to 3.47 GW by FY2035 from less than 1 GW today.

- The majority of the additions are expected to come online after FY2030.

- The strategy emphasizes industrial development, including attracting related industries, building local supply chains, and expanding workforce training.

- CONTEXT: Akita is Japan’s leading offshore wind region, with multiple projects already operating or under development in both port and general sea areas.

Kajima obtains Japan’s first certification for wind turbine foundation design

(Company statement, March 25)

- Kajima secured Japan’s first technical certification for a design method for onshore wind turbine foundations, approved by ClassNK.

- It improves anchor bolt pull-out resistance by adding horizontal reinforcement bars, enabling stable foundations without increasing size, reducing construction costs.

- The certification allows developers to skip repeated validation and simulation processes for each project, streamlining approvals.

- TAKEAWAY: Japan needs engineering innovation to lower costs of its supply chains, which are about twice that of Europe in the wind power sector. Kajima was the contractor for the three Round 1 offshore wind projects in the Mitsubishi Corp-led consortiums, and is expected to be a major industry player.

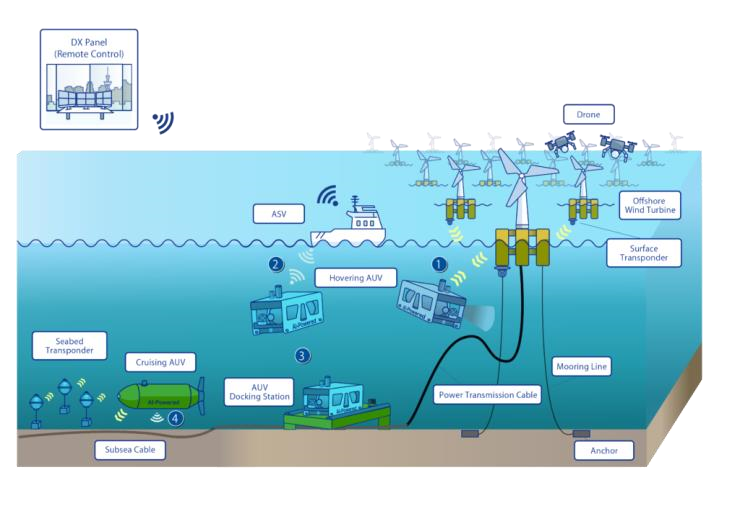

Japan proposes roadmap for autonomous offshore wind inspections using AUVs

(Company statement, March 30)

- Toyo Engineering and partners including Nippon Steel Engineering, FullDepth and OKI proposed a roadmap to commercialize unmanned inspection systems for offshore wind facilities using autonomous underwater vehicles (AUVs).

- The roadmap targets early deployment around 2030 and outlines fully autonomous inspection systems by 2040, combining AUVs, surface vessels and remote-operated vehicles to monitor subsea structures such as cables and mooring lines.

- A demo in 2025 identified key technical and operational challenges, including underwater positioning, data transmission and system integration.

- CONTEXT: The initiative is backed by the Cabinet Office and reflects efforts to build digital and robotic infrastructure to support expansion of offshore wind capacity.

Japan-backed Eastland Generation launches geothermal plant in New Zealand

(Company statement, March 26)

- Eastland Generation, a company in which Obayashi has invested, began operations at its new 49 MW geothermal power plant, TOPP2, in Kawerau, New Zealand.

- This boosts the firm’s total installed geothermal capacity to 118 MW.

- SIDE DEVELOPMENT:

- JOGMEC awards grant to INPEX for geothermal survey in Hokkaido

- (Organization statement, March 18)

- JOGMEC awarded a grant to a geothermal survey project by INPEX in Shibetsu (Hokkaido).

- CONTEXT: INPEX has been pursuing geothermal exploration in the region since 2020. Geothermal energy in Hokkaido has gained momentum in recent years, with the commissioning of two plants: Minami-Kayabe (6.4 MW) and Mori (2 MW).

NEWS: NUCLEAR ENERGY

ANRE outlines status of nuclear sector, pledges to complete Rokkasho plant

(Government statement, March 31)

- ANRE outlined the current status of Japan’s nuclear energy policy.

- Japan retains its 2040 vision for nuclear power to make up 20% of the energy mix.

- Since August 2015, fifteen units have resumed service, though more are still awaiting restart.

- ANRE addressed the suspension of safety reviews for Hamaoka NPP following data irregularities.

- A renewed timeline was presented for the long-delayed Rokkasho fuel cycle complex, now slated for completion in late FY2026.

- CONTEXT: Rokkasho’s completion has been delayed 27 times over the past 25 years; the original completion date was 1997.

- Policy focus is widening to backend challenges: reuse of surplus MOX powder from processing, tighter safeguards on plutonium handling, and a renewed push to identify final disposal sites. The most recent step was a formal request for a literature survey at Minamitorishima in the Pacific.

- SMR technology is accepted overseas but Japanese safety regulations are not yet established. So, Japan will support its firms to join SMR projects abroad.

- SIDE DEVELOPMENT:

- Aomori governor opposes additional spent fuel shipments

- (Nishi Nippon Shimbun, March 31)

- Aomori governor said this year the prefecture won’t approve accepting 60 tons of spent nuclear fuel at the interim storage facility in Mutsu City. o The decision is due to delays completing the Rokkasho reprocessing plant. There’s only a slim chance that the plant will be finished during FY2026.

- CONTEXT: Mutsu launched in Nov 2024. It is Japan’s only interim storage site for spent nuclear fuel, and is used by utilities such as TEPCO and Japan Atomic Power.

- TAKEAWAY: Japan’s nuclear policy relies on a “nuclear fuel cycle” including reprocessing spent fuel. But the plan can’t be fully realized due to delays in Rokkasho’s completion. A prolonged refusal by Aomori could further hinder this nuclear fuel cycle policy.

Kashiwazaki-Kariwa NPP to restart commercial operation on April 16

(Company statement, March 30)

- TEPCO said commercial operation of Kashiwazaki-Kariwa NPP’s Unit 6 will begin on April 16. The utility applied to the NRA for final equipment inspection.

- CONTEXT: TEPCO originally planned to start commercial operation on Feb 26, but the timeline was delayed twice due to a series of issues. Unit 6 restarted on Jan 21 after about 14 years of dormancy, but was then halted due to problems with fuel handling equipment. The reactor’s thermal output reached 100% on March 27.

Japan and France deepen cooperation on nuclear fuel cycle and advanced reactors

(Government statement, April 1)

- Japan and France agreed to expand cooperation in nuclear energy, including fuel cycle development, next-gen reactors and nuclear supply chains.

- The two countries will work together on reprocessing, MOX fuel, uranium supply and enrichment capacity, and support safe long-term operation of existing reactors and decommissioning efforts.

- They also plan to advance joint development of sodium-cooled fast reactors and continue collaboration on fusion projects such as ITER and JT-60SA.

NRA extends deadline for NPP anti-terrorism facilities completion

(Asahi Shimbun, April 1)

- The NRA finalized its decision to change the deadline for installing anti-terrorism facilities at NPPs.

- Before, it was within five years of approval of construction. Now, it will be within five years of operation start.

- The decision received approval from all five commissioners. Chairman Yamanaka Shinsuke noted that 11 out of 12 reactors failed to meet the deadline in the past.

- CONTEXT: Plants must build facilities that allow remote control of reactor cooling systems in case of a terrorist attack. If these are not completed on time, even operating reactors must shut down.

- TAKEAWAY: The change applies only to plants that haven’t reached their deadline. Reactors that have missed them – such as Kashiwazaki-Kariwa Unit 7 and Tokai No. 2 – are excluded.

NEWS: TRADITIONAL FUELS

JOGMEC introduces initiatives for securing LNG supply

(Company statement, April 1)

- JOGMEC introduced two initiatives to stabilize medium- to long-term LNG supply.

- The first is the creation of a new investment system, providing incentives for projects that meet specific energy supply requirements.

- The second is the revision of debt guarantee rates. JOGMEC is strengthening incentives for LNG projects by adjusting debt guarantee rates based on the offtake volume of LNG purchased and the contracted volume designated for Japan.

- CONTEXT: This policy revision reflects the necessity of securing long-term LNG contracts. It addresses medium- to long-term demand uncertainties, as outlined in the 7th Strategic Energy Plan.

- SIDE DEVELOPMENT:

- ANRE proposes extending standard gas supply planning period

- (Government statement, March 31)

- ANRE proposed extending the standard gas supply planning period from three to five years, as well as tightening monitoring of LNG inventories and procurement.

- Working group participants supported this extension, noting that a five-year period aligns better with the long lead times for infrastructure development.

- This allows regional operators to alert authorities to medium- to long-term challenges.

- TAKEAWAY: ANRE is tightening its oversight of LNG supplies due to energy security demands. The govt plans to check more frequently LNG shipping trends and raw material inventory levels. However, this procurement data is sensitive and could affect market competition.

Japan oil stockpile metrics may underplay total petroleum product consumption

(Nikkan Gendai, April 3)

- The govt calculated oil stockpile releases based on daily consumption of about 1.77 million barrels, but international statistics suggest actual consumption is closer to 3.36 million barrels per day.

- The discrepancy stems from differing definitions: Japanese official figures exclude products such as LPG and naphtha, while international data includes a broad range of petroleum-related consumption.

- Based on the govt’s measure, a planned release of roughly 53 million barrels equates to about 30 days of supply. Using international benchmarks, it would cover 16 days.

- Separately, while Japan’s total oil stockpiles are estimated at around 245 days including private and producer reserves, naphtha – critical for petrochemicals – is not covered by stockpiling rules. Japan only had 2–3 weeks of naphtha inventory before the Iran conflict.

- TAKEAWAY: The gap highlights how definitions can materially affect perceived energy security, with petrochemical feedstocks like naphtha emerging as a key blind spot in Japan’s stockpiling framework. It’s no surprise that several refiners have already called for new stockpile releases barely days after the first national reserves were distributed.

Energy companies say LNG prices will increase later in FY2026

(Nikkei, March 31)

- Energy firms in central Japan commented on Iran’s control of the Strait of Hormuz.

- Electricity prices will be impacted starting in June.

- Due to a time lag of about 7–8 months between oil and LNG price increases, the full impact on LNG prices may appear only in the second half of the fiscal year.

- Toho Gas doesn’t source oil or LNG from the Middle East, so supply volumes are not a concern. But, it warned that if the crisis continues, price rises could be significant.

Chevron’s Wheatstone LNG facility to remain offline for several weeks

(Bloomberg, March 29)

- Chevron’s Wheatstone LNG facility in Western Australia will remain offline for several weeks due to storm damage from Tropical Cyclone Narelle.

- CONTEXT: In February, the facility accounted for 2.4% of global LNG trade, shipping 11 cargoes; of those, 10 went to Japan and one to Thailand. Woodside Energy is resuming operations at its North West Shelf facility. Chevron said its Gorgon site restarted one of its three production units.

- TAKEAWAY: This disruption is adding pressure to the global LNG market, adding to other supply issues, including halted operations in Qatar due to the Iran war.

- SIDE DEVELOPMENT:

- JERA exits Commonwealth LNG project in Louisiana

- (Poten & Partners, April 3)

- JERA has exited Commonwealth LNG. In 2025, it signed a deal to buy 1 Mtpa from the project, but Commonwealth did not reach FID before the contract deadline.

- CONTEXT: A Poten & Partners analyst posted on social media a PDF of an official notice, adding that during CeraWeek he was told Commonwealth already replaced the volumes from the JERA deal. Commonwealth still seeks to reach an FID by June.

- TAKEAWAY: This project located in the state of Louisiana on the Gulf of Mexico was one of the LNG deals that JERA signed with the U.S. last summer totaling 5.5 Mtpa and estimated at about ¥400 billion ($2.76 billion) a year. With these agreements, JERA planned to triple its U.S. LNG imports to 10 Mtpa by the early 2030s, increasing the U.S. share to around 30% of total imports. The other deals are with Cheniere, Sempra and NextDecade (Rio Grande LNG). This 1 Mtpa from Commonwealth is about 20% of that total target, which puts a slight dent in JERA’s overall U.S. purchase goals, but it won’t derail those ambitions.

JGC selected as EPC contractors for Papua LNG project

(Company statement, March 31)

- Papua LNG will build a new LNG plant in Port Moresby, Papua New Guinea.

- JGC and Hyundai E&C were tapped as EPC contractors to build the facility.

- The plant will have a 4 Mtpa capacity (three production trains) using gas from the Elk-Antelope fields.

- The project will use electric-driven tech to reduce CO2 emissions.

- CONTEXT: The project’s operator is TotalEnergies. Partners include ExxonMobil, Santos, and ENEOS Xplora. This project will expand Papua New Guinea’s LNG production, boosting total national capacity above 10 Mtpa.

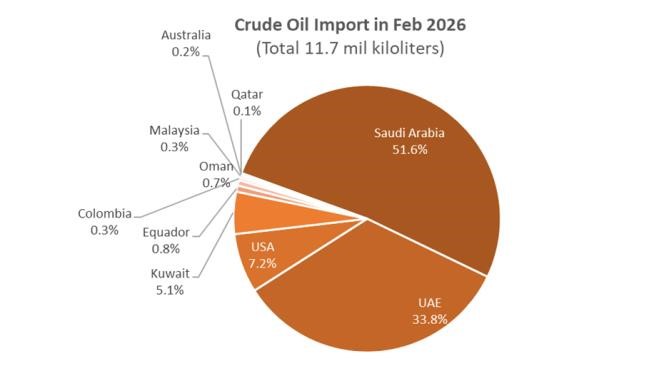

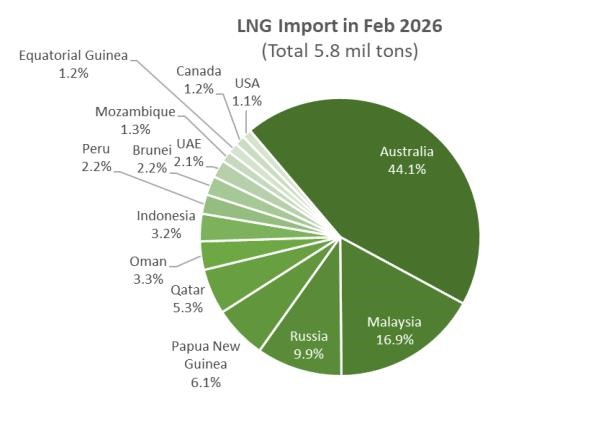

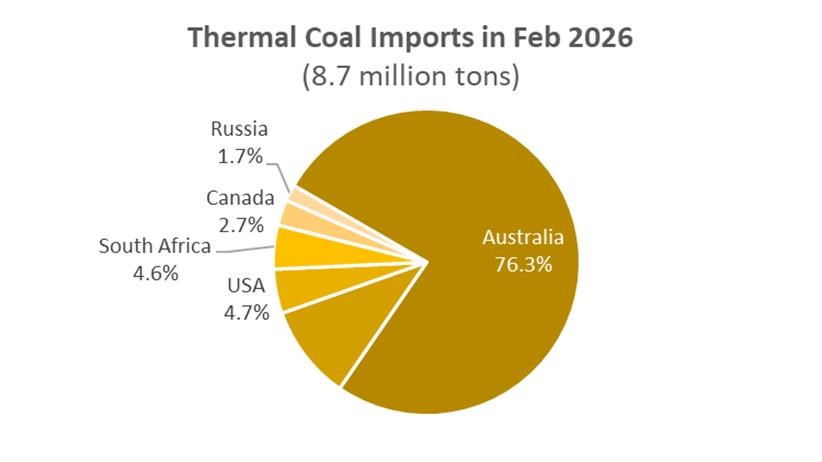

February Oil/ Gas/ Coal trade statistics

(Government data, April 1)

- In February, Japan imported 11.7 million kiloliters of crude oil, up 15.9% YoY, but down 14.5% MoM, likely due to a seasonal decrease.

- A little over 91% of the oil came from the Middle East. For the first time in 2026, Japan imported crude oil from Malaysia, Oman, and Colombia.

- LNG imports in February totaled 5.8 Mt, down 6.8% MoM, and down 0.9% YoY. A little over 11% of LNG came from the Mid East – Qatar, Oman, and UAE. LNG from the U.S. dropped 84.4% (from 393,254 tons to 61,232 tons). For the first time in 2026 – Peru, Equatorial Guinea, and Mozambique began delivering LNG to Japan. So far, 15 countries have supplied LNG to Japan this year, compared to 17 in 2025.

- Thermal coal imports in February totaled 8.7 Mt, down 1.1% YoY, and down 11.7% MoM. No thermal coal was sourced from the Middle East. Australia is Japan’s top supplier as usual. PM Takaichi called to increase power generation output from coal-fired thermal power plants; thus, imports may increase in coming months.

LNG stocks down from previous week, up YoY

(Government data, April 1)

- As of March 29, the LNG stocks of 10 power utilities were 2.19 Mt, down 8% from the previous week (2.38 Mt), up 3.3% from end March 2025 (2.12 Mt), and up 9.5% from the 5-year average of 2 Mt.

ANALYSIS

BY AGLAÉ BANGE

Carbon Pricing in Japan: Rethinking Decarbonization Incentives

Japan’s carbon pricing landscape is entering a new stage. Recent reforms to Non-Fossil Certificates (NFCs) – including revisions to the floor price and caps – coincide with the GX Emissions Trading System (GX-ETS) entering its mandatory phase this month. Both are intended to strengthen carbon price signals.

Yet the two systems operate differently. The GX-ETS targets direct emissions, while NFCs operate through power markets, shaping how companies source and account for low-carbon electricity. While together they’re meant to drive low-carbon procurement, the link between them remains weak.

The reforms come at a difficult time for global energy markets. The Iran war and the resulting disruptions to LNG supply chains have put energy security back at the center of policy concerns, raising the risk that governments may slow the use of climate-related tools such as carbon pricing.

Yet this is precisely where Japan’s persistence with carbon pricing – even if imperfect at first – could prove valuable. A more robust framework, involving NFCs and the GX-ETS, would help create stronger signals for developers to invest in low-carbon generation. This is key for Japan, which remains dependent on fossil fuels and is already facing tightening power supply.

How, then, is Japan’s carbon pricing architecture evolving, and what price signals are likely to emerge across its different mechanisms?

Fragmented carbon pricing landscape

Japan’s approach to carbon pricing remains modest by international standards. A national carbon tax, introduced in 2018, has significant shortcomings, including traceability. But its biggest weakness is price: just ¥289 per ton of CO2, a tiny fraction of the €57.10 per ton (about ¥10,500) on average in EU countries. A more meaningful carbon levy is planned for FY2028, but the levels for that are not yet set.

What’s more, Japan’s carbon pricing is fragmented across multiple instruments. In addition to ETS, Japan has developed a range of environmental value mechanisms: Green Energy Certificates (GECs, started in 2000); J-Credits (launched in 2013), in parallel to international instruments such as I-RECs (first trialed in Japan in 2021).

But the most important environmental value instruments by far are the Non-Fossil Certificates (NFCs), launched in 2018. NFCs account for the largest share of transactions, about 93% of total volumes in FY2022, forming the bulk of corporate Scope 2 decarbonization activity.

In FY2025, around 60 TWh of NFCs were traded across JEPX auctions – slightly below the previous year, but still substantial. As such, NFCs currently set the tone for corporates’ decarbonization agenda.

What is an NFC?

NFCs were introduced in 2018 to reduce the renewable energy surcharge and support carbon neutrality objectives, particularly by enabling retailers to meet regulatory requirements.

An NFC is a certificate that proves the environmental value of electricity generated from non-fossil (renewables or nuclear) energy sources. By attaching these certificates to electricity consumption, companies can lower their reported Scope 2 emissions and meet both regulatory and voluntary targets such as RE100.

The system also plays a regulatory role. By FY2030, retailers are required to ensure that at least 44% of electricity sales come from non-fossil sources – or to use NFCs to bridge the gap. This has entrenched NFCs as a compliance tool as well as a market instrument, which rewards low-carbon power sources through market trading.

The market has evolved rapidly. Initially limited to FIT-backed certificates, the system expanded in 2020 to include non-FIT NFCs, reflecting the growing share of merchant renewables. Reform in 2024 introduced full tracking of generation attributes, aligning Japan with international standards and increasing the credibility of NFC-based claims.

JEPX facilitates the trading of both FIT and non-FIT NFCs, although only non-FIT NFCs can be traded through bilateral agreements. NFCs are divided into three categories:

- FIT NFCs: issued for electricity purchased under the FIT scheme, where prices are fixed and guaranteed by the government.

- Non-FIT NFCs with renewables attributes: issued for electricity purchased outside the FIT scheme, including hydropower or renewable energy whose FIT support period expired.

- Non-FIT NFCs without renewables attributes: issued for electricity that is nonfossil, but still not classified as renewable energy, primarily nuclear power.

Pricing reform: rebalancing the market

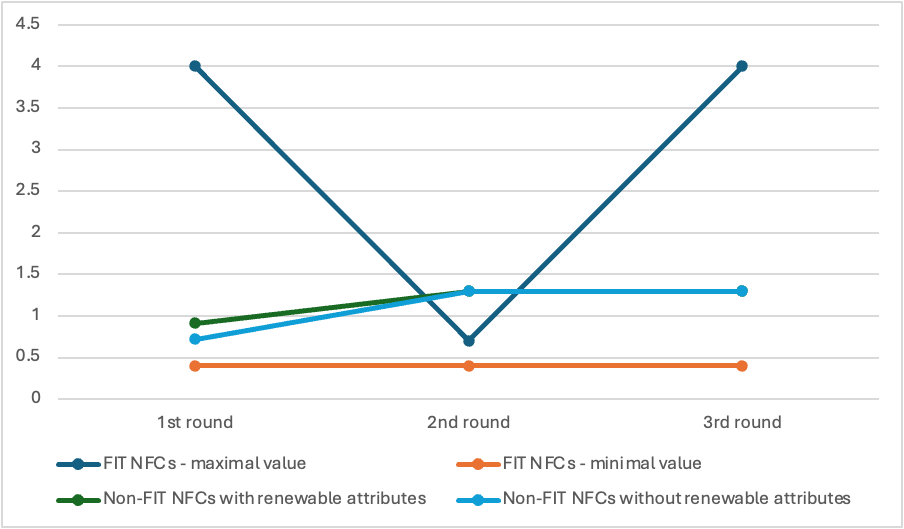

Despite their central role, NFC prices remain heavily shaped by administrative controls.

FIT NFCs typically clear at the floor price – around ¥0.3–0.4/kWh – equivalent to roughly ¥900/ tCO2, according to METI’s own calculations. This is far below both international carbon prices and the underlying cost of renewable support under the FIT scheme, which is passed on to consumers via surcharges exceeding ¥3/ kWh.

The result is a clear disconnect: the environmental value embedded in NFCs captures only a fraction of the true system cost of decarbonization. ANRE has acknowledged that price caps act as a barrier to clean energy investment by keeping environmental values artificially low.

Non-FIT NFCs show a different pattern. Prices have consistently hit the ceiling – ¥1.3/ kWh in recent auctions – reflecting stronger demand for traceable, subsidy-free renewable attributes. Yet even here, price formation remains constrained by caps.

Recognizing these distortions, METI is considering a series of reforms:

- Raise the floor price for FIT NFCs to the same level as for non-FIT NFCs from FY2027 (¥0.6/ kWh); and

- Remove the FIT NFCs price cap by FY2028.

These changes would mark a shift from a compliance-driven model to a more marketbased system, with potentially significant implications for price formation.

Source: JEPX

These contrasting dynamics underscore the need to maintain a balanced pricing relationship between FIT and non-FIT NFCs. By revising both floor and ceiling levels from FY2027 onwards, purchasers are expected to increasingly shift from FIT NFCs to direct procurement of non-FIT NFCs primarily through PPAs.

PPAs, main driver of non-FIT NFCs

Since 2020, when PPAs first appeared in the Japanese market, the number of deals has risen significantly, exceeding 750 according to Japan NRG data. The publicly available PPA deals had a cumulative capacity of about 3 GW in 2025.

Non-FIT NFCs traded through bilateral transactions via PPAs offer several advantages over those available on JEPX. Above all, they respond to corporate demand for longterm supply certainty. Fixed pricing – unconstrained by regulatory caps – reduces exposure to market volatility, while providing direct access to specific generation assets.

As these agreements bundle electricity with non-FIT NFCs, they increasingly draw volume away from exchange-based trading. As more renewable output is contracted through PPAs, fewer non-FIT NFCs are exchanged on the JEPX – particularly those with renewable attributes. The result is a tighter market, helping to explain persistent price pressure at the ceiling.

The recent virtual PPA signed between Equinix and ENEOS last February shows the scale of such arrangements. The deal involves a 121 MW solar power plant in Hyogo Prefecture that will supply power to ENEOS over 20 years.

Over time, this dynamic could lead to a liquid but persistently low-priced FIT segment on one hand, but also a scarce, premium-priced non-FIT segment increasingly tied to PPAs.

Price caps: potential alignments of the GX-ETS

Running alongside NFCs is the GX-ETS, which from April 2026 becomes mandatory for large emitters (above 100,000 tCO2), covering around 400 companies and roughly twothirds of national emissions.

The current price ceiling – ¥4,300/ tCO2, rising to ¥4,840 by FY2030 – is designed around the cost of switching from coal to LNG. This is insufficient. Given current fuel spreads, the carbon price required to make LNG competitive in 2026 is likely well above ¥8,000/ tCO2, implying that the cap would need to at least double to drive meaningful fuel switching.

Combined with the similarly low price caps in FIT NFCs, the cap on GX-ETS weakens the overall economic signal for decarbonization by allowing coal-fired power generation to remain competitive.

NFCs and GX-ETS: convergence or divergence?

The coexistence of these mechanisms raises a central question: will Japan’s key carbon pricing instruments converge or continue to operate in parallel with limited interaction?

In theory, the two systems could reinforce each other. Higher GX-ETS prices would increase demand for low-carbon electricity, while higher NFC prices would better reflect the cost of decarbonization and support renewable investment.

In practice, both remain constrained. NFC reforms may push certificate prices upward, particularly for non-FIT renewable attributes, but starting from a low base. Even a doubling of FIT NFC prices to ¥0.6/ kWh would still imply a carbon value well below EU and other international benchmarks. Similarly, unless GX-ETS price ceilings are raised more aggressively, its impact on fuel switching and industrial emissions will remain limited.

Outlook

Reforms of Japan’s carbon pricing architecture shows a clear direction.

On the NFC side, reforms point towards price increases and a growing role for corporate procurement through PPAs. This is likely to tighten supply and support higher prices for high-quality renewable attributes. Over the next three to five years, non-FIT NFC prices could increasingly reflect corporate willingness to pay for clean electrons, rather than administratively defined benchmarks.

On the GX-ETS side, the key variable is political willingness to raise the ceiling. Energy security concerns, heightened by ongoing global LNG market disruptions, may delay more aggressive pricing. But over time, the need to align with overseas carbon markets and meet climate targets will likely push prices higher.

A plausible outcome as things stand today is not a single, unified CO2 price, but a layered system of interdependent mechanisms:

Against this backdrop, the following trends are emerging:

- A relatively low and regulated price for compliance (FIT NFCs);

- A higher, market-driven price for premium decarbonization (non-FIT NFCs and PPAs); and

- A gradually strengthening, but still constrained, ETS.

For businesses, this means navigating an increasingly complex landscape where the choice of instrument will matter as much as the price. As a result, officials may well end up creating a hybrid system tailored to Japan’s specific constraints. The key will be to maintain policy coherence across the different mechanisms while allowing prices to move more freely to reflect the underlying realities of fuel markets and decarbonization costs.

ANALYSIS

BY ANDREW STATTER

Energy Jobs in Japan: Clean Energy Can No Longer Hire Locals-Only

A few years ago, we saw this peculiar situation play out in the offshore wind sector: Japan tried to hire almost all of its needed talent pool from within its own borders, despite having only a couple of small operational offshore wind farms.

Much of that talent pool came from other renewables (solar primarily), as well as from oil and gas or conventional energy, especially in engineering disciplines. For two reasons, this became a clear handicap for offshore wind.

First, offshore wind is a very complex industry that requires hiring experienced talent. Second, as a nascent market, many players look to hire from the same extremely narrow talent pool. In the end, the math simply did not add up.

Today we face a similar challenge across flexibility markets, power trading, forecasting, and some of the data science and machine learning disciplines. As energy trading volumes increase, new players enter the market, and more flexible assets come online, these skills, which are still rare in Japan, face increasing demand. Japan has some talent in this space, but not enough to cater to the rapidly growing market.

This isn’t a temporary gap. Japan’s energy market liberalization only began in earnest in 2016. The talent pipeline is structurally behind the investment pipeline, and the gap is widening as capital flows in faster than people can be trained.

Functions where this bites hardest now are: power traders with futures and structured product experience; forecasting and analytics specialists; BESS optimization and asset managers.

Demographic reality: Japan is running out of workers

Japan’s population is declining by about one million per year. The working-age population is shrinking faster than the overall population, and the energy sector, competing against tech, finance, automotive and semiconductors, is not at the top of most graduates’ target list.

The energy industry has an additional problem: the generation of engineers who built Japan’s nuclear, thermal and early grid infrastructure is retiring, taking decades of specific knowledge with them. There is no qualified cohort behind them. The TSO talent bleed discussed in recent articles is one symptom of a much larger structural problem.

This is not a problem that training programs alone can solve within the timeframes that Japan’s energy transition requires. Over time, through structured education and reskilling, Japan will be able to fill some of the needs across its talent landscape; but in many sectors, in the short term at least, Japan will need to rely on imported talent.

Cultural and structural barriers for global talent

Japan’s energy sector has long been insular, dominated by large trading houses and utilities where lifetime employment and Japanese language ability are assumed. For an experienced Australian storage developer or a Danish power trader, the question isn’t just salary and skill fit, it’s whether the environment is one where they can do their job and build a career.

For many roles within the energy sector, even if the hiring companies shift their policies and become open to hiring foreign talent, support with Japanese language training, the fact of the matter is that many roles are difficult for non-Japanese to perform.

Considering that renewables, or any energy projects, are developed in the countryside and rural Japan, people in charge of development, local relationships, and permitting absolutely need to speak Japanese and preferably, actually be Japanese.

Compensation is a genuine barrier. Japan’s base salaries at mid-to-senior levels remain uncompetitive versus equivalent roles in Singapore or Australia, particularly when adjusted for cost of living and the weak yen. Companies serious about global hiring need to benchmark internationally, not domestically.

This is the exact same issue that you find with regional investment funds looking to deploy capital in Japan and other markets. Japan is competing for capital, both monetary and human, not only domestically but against other countries in Asia Pacific, Australia, and beyond.

The companies already getting it right

A small but growing cohort of companies in Japan’s energy sector are attracting and retaining global talent: typically foreign-backed IPPs, specialist advisory firms, and energy tech firms. A key challenge is identifying which roles are best suited to Japanese workers, and which roles face a dearth of talent and whether overseas talent is better suited because of more experience.

A common success formula is to hire global talent into senior leadership roles of a particular function, and then hire bilingual Japanese talent directly underneath them. As that team builds, it can be either bilingual or monolingual Japanese talent. Not everyone needs to speak English.

Over time, this allows for a well-developed, highly skilled native Japanese workforce in a particular function. The space industry has done this well, where you can find multiple high-quality Japanese startups with a well-balanced blend of foreign and Japanese talent.

The mistakes made by companies that have tried and failed are also instructive: hiring global talent into roles that are junior, surrounding them with monolingual teams, and expecting cultural assimilation rather than cultural integration. Global talent hired into these environments typically exits within 18 months.

By all means, Japan can do this on its own – a highly educated nation with excellent engineering, manufacturing, and financial talent. That said, if there are countries active in certain markets for ten years, then that means they have talent with ten years of specific experience.

Japan would be better off learning the lessons that others have learned from practical experience rather than making those same mistakes all over again.

Andrew Statter is a Partner at Titan GreenTech, an executive recruitment agency focused on the clean energy space.

ASIA ENERGY REVIEW

BY JOHN VAROLI

A brief overview of the region’s main energy events from the past week

Australia / Fuel crisis

The energy minister said 53 ships with 3.7 billion liters of fuel are on their way to Australia. But experts warn that shipments can be delayed, diverted or canceled.

Australia / Fuel supplies

As of April 4, Australia had 39 days’ worth of petrol, 29 days’ worth of diesel and 30 days’ worth of jet fuel.

China / LNG

Chinese firms are reselling record volumes of LNG, cashing in on soaring spot prices. China is the world’s top LNG importer; in March it reloaded 8 to 10 cargoes, its highest monthly total, reported Kpler.

China / Natural gas

China can weather the energy crisis thanks to a diversified portfolio in gas. While China imports 40% of its gas, 60% of this amount is delivered as LNG by sea; the rest via pipeline. Turkmenistan accounts for 45% of China’s pipeline gas imports. Russia about 40%.

India / Jet fuel

State-owned oil marketing companies got approval for a “partial and staggered” 25% increase in aviation fuel prices. India buys almost 50% of energy supplies from the Middle East.

India / Oil & Gas

India will boost both onshore and offshore oil & gas exploration, said the Energy Ministry.

Philippines/ LNG

Iran will allow vessels carrying energy for the Philippines to pass through the Strait of Hormuz, said the Dept of Foreign Affairs.

South Korea / Energy crisis

President Lee Jae Myung said the country is in a “war-like situation”. To mitigate the energy crisis he called to approve a $17 billion supplementary budget.

South Korea / Nuclear power

Korea Hydro & Nuclear Power confirmed that the Gori-2 reactor resumed operations. The NPP was halted in 2023 when its 40-year license expired.

Taiwan / Jet fuel

Airlines will raise domestic fares 157% after the govt approved higher fuel surcharges.

Taiwan / LNG

Taiwan received supply assurances from a “major” LNG -producing country, said the economy minister. Taiwan relied on Qatar for a third of its LNG before the Iran war.

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Hulic Ochanomizu Bldg. 3F, 2-3-11, Surugadai, Kanda, Chiyoda-ku, Tokyo, Japan, 101-0062.