WEEKLY

April 13, 2026

ANALYSIS

CORPORATE PPAs: THE NEED TO HEDGE AGAINST FUTURE POWER SUPPLY RISK

- Corporate procurement strategies are often built on a simple assumption – tomorrow’s market conditions will resemble today’s. Govt energy plans suggest this won’t be the case, especially in terms of capacity availability.

- Corporate PPAs offer a strategic tool to hedge against the risk of energy shortages.

TOKYO AREA’S FIRST CURTAILMENTS BECOME RECURRING, STRENGTHENING CASE FOR BESS

- The TEPCO Power Grid saw its first curtailment in March. Then it happened again four more times in the same month.

- Our analysis shows TEPCO area curtailments are here to stay. Integration of nuclear power will be key to the system response.

ASIA PACIFIC REVIEW

This column provides a brief overview of the region’s main energy events from the past week

NEWS

- PM Takaichi says 2026 oil supply secure, avoiding new measures amid price surge for now

- Japan edging towards next wave of oil stock releases

- Prices for industrial materials rising due to Iran war

- ANRE proposed new short-term mechanism to secure additional power supply capacity

- 3rd round of reserve power auction highlights regional imbalance

- Kyushu Electric makes first investment in Kansai data center fund

- Hitachi selected for Tokyo hydrogen station study to develop onsite production model

- Chinese solar makers hike Japan prices as costs rise

- Tokyu Land and partners to invest ¥3 billion in extrahigh-voltage BESS

- Energy Vault enters Japan’s BESS market with acquisition

- ANRE aims to limit BESS grid connection applications

WIND POWER AND OTHER RENEWABLES

- Cosmo’s large Hokkaido onshore wind project enters early environmental review

- Kyushu Electric targets first commercial tidal power

- JFE Engineering enters India waste-to-energy market

- Govt outlines timeline and roadmap for operations of innovative reactors

- Blackstone, SoftBank among bidders for TEPCO capital tie-up

- METI forecasts over 10% decline in oil product demand through FY2030

- INPEX considers reallocating Middle East investments to SE Asia

- Chiyoda mulls construction restart at Qatari LNG plant

CARBON CAPTURE & SYNTHETIC FUELS

- ANRE sets FY2026 external procurement ratio for NFC

EVENTS

Mid-April FIT/FIP Solar Auction #28

Japan Atomic Industrial Forum

(JAIF) Annual conference @ Tokyo

April 24 Green Elements at Work @ Google for Startups

May 3-6 Golden Week (many companies will close from April 29 to May 6)

May 26-28 Japan Energy Summit @ Tokyo Big Sight

June 3 South Korea – Local Elections

June 23-25 “Summer Davos” in Dalian, China

September 14-18 IAEA General Conference 2026

October International Maritime Organization –

Net-zero Discussions

Nov 2-5 ADIPEC 2026 @ Abu Dhabi

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Chief Editor)

John Varoli (Senior Editor, Americas)

Kyoko Fukuda (Data, Events)

Magdalena Osumi (Renewables & Storage)

Filippo Pedretti (Thermal, CCS, Nuclear)

Tetsuji Tomita (Power Market, Hydrogen)

Aglaé Bange (Renewables and Biomass)

George Hoffman (Sales, Business Development)

Tim Young (Design)

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

NEWS: GENERAL OUTLOOK AND TRENDS

PM Takaichi says 2026 oil supply secure, avoids new measures amid price surge

(Asahi Shimbun, Nikkei, April 6)

- PM Takaichi said Japan has secured sufficient supplies of oil and petroleum products to last for the rest of this year.

- The govt now relies on strategic stockpiles and alternative procurement routes that bypass the Strait of Hormuz, and coordinates with the private sector. Purchases of oil from the U.S. and other regions are up by a fifth this month.

- In May over half of supplies are expected from alternative sources, said the PM.

- Naphtha supplies remain stable, with inventories covering four months of domestic demand, extending to more than six months when including domestic production.

- “Japan has oil reserves equal to about eight months of supply, and thanks to progress in alternative procurement, there is now a clear outlook for maintaining petroleum supplies beyond the end of the year while limiting stockpile releases,” said the PM.

- Takaichi didn’t commit to more measures, despite calls from ruling and opposition lawmakers for action, including supplementary budgets and more fuel subsidies.

- TAKEAWAY: The PM’s stance signals that Japan’s fuel supplies so far remain secure. At least, this is the strategy until after Golden Week holidays in early May. The situation may be different by summer if Iran continues to block shipping through the Strait of Hormuz. But progress in securing alternative supplies is already strengthening Japan’s energy security.

- SIDE DEVELOPMENT:

- Japan weighs further oil reserve releases, may add 20-day supply

- (Sankei, April 9)

- The govt is considering an additional release of ~20 days’ worth of national oil reserves as early as May, following an initial drawdown of ~50 days’ supply set to conclude by end-April.

- METI is also reviewing further measures to extend supply, including prolonging the temporary reduction of private stockpiling obligations (cut from 70 to 55 days), due to expire mid-April.

- Authorities say current releases may be insufficient if disruptions persist; shipping through the Strait of Hormuz remains unstable despite a ceasefire. o CONTEXT: As of early April, Japan held ~146 days of national reserves and ~80 days of private reserves; levels may be lower due to ongoing releases.

- On naphtha, the govt says it can secure over six months of domestic consumption through existing stocks, domestic refining, and imports from outside the Middle East.

- TAKEAWAY: Although global oil benchmarks have not jumped as high as following the start of the Russia-Ukraine war, the scale of the Iran conflict has been much larger in terms of impact on Japan’s energy supplies. For comparison, in 2022 the govt’s total oil stockpile release amounted to 22.5 million barrels, equivalent to 11 to 12 days of demand.

MOL cautious on Hormuz reopening, cites need for “full safety assurance”

(Bloomberg, April 9)

- Mitsui O.S.K. Lines (MOL) said it will only resume transits through the Strait of Hormuz once “complete safety can be guaranteed.”

- MOL President Tamura said criteria for safety are difficult to define, and decisions will be made case by case, with the company awaiting guidance from the govt.

- Shipping disruptions are already pushing up freight rates and tightening transport capacity, with broader impacts expected if instability persists.

- TAKEAWAY: Even with a ceasefire, risk aversion remains high in the shipping industry and it’s not just the cost of insuring passage. Lives are at stake, which points to a much more prolonged disruption in Hormuz traffic for now. LNG futures prices in Japan reflect this and point to elevated prices until at least 1Q of next year. The highest pricing is currently for May 2026 contracts.

Prices for industrial materials rise due to war

(Japan NRG, April 9)

- Domestic prices for many industrial materials will likely rise, especially for plastics, chemicals, aluminum, steel, and paper.

- Disruptions to supply chains and higher oil prices are making key raw materials like naphtha more expensive and harder to get.

- Prices for about two-thirds of major industrial materials will increase in Q1.

- Plastics (polyethylene and polypropylene) could see price hikes of up to 30%. As a result, the prices of food packaging, polyester fiber for clothing, and even artificial leather products – such as those used for the traditional school rucksack in Japan – will need to rise accordingly.

- Aluminum and steel prices are also rising due to supply concerns, higher raw material costs, and a weaker yen. Paper producers are trying to pass on higher costs as well.

- As for LPG, Japan faces no immediate physical supply shortages. Only 3.7% of its LPG comes from the Middle East. But Japan will see an increase in household propane gas bills because the formula used by LPG distributors to set wholesale prices is weighted 70% toward Middle Eastern benchmarks.

- Saudi Aramco’s recent 40% export price hike inflates LPG and other costs in Japan. Wholesale prices are already reflecting this. Consumers will see these increases feed into their utility bills as early as May.

- SIDE DEVELOPMENT:

- METI requests oil wholesalers to sell fuel to critical facilities

- (Sankei Shimbun, April 6)

- METI requested oil wholesalers to sell fuel to hospitals and public transportation. This applies only when regular procurement becomes difficult.

- As of April 1, the government received notice for about 400 consultations on fuel supply uncertainty. Medical, welfare, transport, public services, and agriculture account for over 30%.

Honda invests in Gachaco to develop electric motorcycles in Japan

(Company statement, April 1)

- Via a ¥340 million share allotment, Honda took full control of Gachaco, a firm specializing in battery charging and swapping services for motorcycles.

- CONTEXT: Total investment is ¥440 million; Suzuki and Yamaha also participated.

- Honda intends to expand services to users of electric machinery and equipment utilizing interchangeable batteries.

- TAKEAWAY: Japan’s electric motorcycle market is tiny compared to its neighbors, particularly China, where in 2025, nearly 55% of two-wheeler sales (including bicycles, scooters, and motorcycles) were electric. This compares to under 8% in Japan (global average is 15%). By 2030, Honda seeks 50% of the global motorcycle market, and to grow the share of electric motorcycles in its sales from 0.6% to 7%; Yamaha targets a 30% share by 2027.

NEWS: ELECTRICITY MARKETS

Govt proposes new measures to secure supply capacity

(Government statement, April 3)

- ANRE proposed a new short-term supplemental mechanism to secure additional supply capacity, replacing the emergency procurement scheme; it will be positioned within the capacity market framework, with costs ultimately borne by electricity retailers.

- This will address supply-demand fluctuations that occur after the main and additional capacity auctions.

- While the capacity market secures supply four years ahead (main auction) and two years ahead (additional auction), risks such as unexpected plant outages can still arise within one year of delivery.

- Positioned as a complement to the capacity market, this new mechanism would target resources that failed to clear or did not participate in previous auctions.

- It would be implemented only when necessary, based on reserve margin assessments, and applied to limited areas and time periods.

- CONTEXT: The emergency capacity procurement scheme (kW tender) was introduced as a temporary measure in winter 2021 to address unexpected supply shortages before the capacity market became operational in FY2024. Under this scheme, TSOs procure capacity on behalf of retailers and recover costs through wheeling charges, due to unresolved cost-allocation rules at the time.

- TAKEAWAY: One emergency measure to ensure supply capacity is the reserve power system, which maintains idle plants as a strategic backstop that can be reactivated in emergencies. The new mechanism, by contrast, replaces kW tenders by securing additional resources that did not clear previous auctions and ensuring their availability for dispatch when needed. Its role is therefore distinct from that of the reserve power system, which operates outside the market framework.

ANRE announces 3rd reserve power auction for FY2026

(Government statement, April 3)

- ANRE announced the third round of the reserve power (strategic reserve) auction for FY2026, setting procurement volumes at 1 GW in Eastern Japan and 0.68 GW in Western Japan.

- In the second round, two projects totaling 1.36 GW were awarded in the West, with no bids in the East.

- Reflecting this imbalance, the third round, covering FY2027–2028 delivery, will differentiate volumes by region, although cross-regional participation will be allowed.

- While system requirements in both regions are estimated at 1.5–2 GW, the East’s volume is capped at 1 GW to ensure sufficient competition; the West’s volume is reduced to 680 MW due to already secured capacity.

- The power market regulator, EGC, reported monitoring results from the second round, noting that some cost components were not recognised as eligible in bid prices. They recommended revising guidelines to include certain minimum refurbishment costs and generator-side charges, with application from the third round.

- CONTEXT: OCCTO began accepting bids in August 2025 for the previous reserve power auction and announced the results on March 10.

Govt revises reference price and settlement method for capacity market

(Government statement, April 3)

- ANRE decided to raise the reference price (Net CONE) in the FY2026 capacity market main auction to about ¥20,000/ kW (double the current level), with a price cap of around ¥30,000/ kW.

- To mitigate impact on retailers, a two-tier single-price settlement will be introduced.

- While the proposal was largely approved, concerns remain over higher costs and the pricing methodology.

- An additional auction for FY2027 delivery will be held due to a projected supply shortfall of about 5.18 GW. Bidding starts on June 3, with results announced by late July.

- CONTEXT: At the previous meeting, there was consensus to revise Net CONE based on updated costs, while maintaining its benchmark role and ensuring supply capacity. Three mitigation measures were also proposed to support electricity retailers affected by the increased burden of capacity contributions. On March 27, OCCTO presented the results of its contribution cost estimates.

Kyushu Electric makes first investment in data center fund

(Company statement, April 8)

- Kyushu Electric invested in a private fund acquiring a data center in the Kansai region, its first such investment.

- The fund, managed by Mitsui & Co Realty Management, will hold the asset via a trust beneficiary.

- The company sees data centers as both critical infrastructure and a growing real estate investment segment, driven by rising demand from AI and cloud services.

- TAKEAWAY: Power utilities are expanding into data center infrastructure as a demand-linked investment gambit. This aligns power supply growth with digital infrastructure development. JERA, Kansai Electric, etc have similar plans and more investments are expected later this year.

EEX to launch Kansai daily power futures to meet short-term hedging demand

(Exchange statement, March 26)

- Starting May 26, the European Energy Exchange (EEX) will launch daily power futures for Kansai region. The product covers baseload and peakload contracts, allowing trading for next-day and week-ahead delivery; weekend contracts are also introduced.

- This follows the rollout of similar products for Tokyo in 2023, bringing Kansai in line with a more complete futures product lineup.

- TAKEAWAY: The move responds to growing price volatility in spot markets, driven by renewables, weather forecast changes, and unexpected outages in the days before delivery. The launch reflects rising demand for short-term risk management tools since Japan’s power market is more volatile and participants seek greater flexibility beyond traditional monthly and seasonal hedging.

JEPX spot prices rise on fuel surge and outages

(Exchange report, April 6)

- In March, electricity spot prices rose sharply across both eastern (50 Hz) and western (60 Hz) regions, driven by higher fuel costs and tightening supply conditions.

- The Persian Gulf war has pushed up oil, LNG and coal prices, raising thermal generation costs. Upward pressure also came from increased thermal plant outages due to maintenance and transmission constraints.

- Prices rose in the second half of the month on higher fuel costs and as power generators raised offer prices.

- Regionally, eight out of the nine main TSO areas saw price increases, with Shikoku the exception due to strong solar output and increased interconnection flows.

TOCOM power futures volumes halve as volatility curbs trading

(Exchange report, April 6)

- March TOCOM power futures trading volume fell sharply to 1,981 lots, down by half from 4,043 in February, due to Persian Gulf war fears.

- While volume dropped, trades rose to 134 (vs. 111 in Feb), reflecting a shift toward smaller-lot transactions as market players adopted a wait-and-see approach.

- Trading was heavily off-exchange (122 out of 134 deals), focused on hedging positions across FY2026, seasonal (summer/winter), and semi-annual contracts.

- Prices were highly volatile, tracking fuel markets. East Japan baseload annual contracts rose from ¥12.3/ kWh (March 2) to ¥22/ kWh (March 23).

- Large block trades included 100-lot deals (10 MW) in West Japan contracts, with summer (July– Sept) priced at ¥21.75/ kWh and winter (Dec–Feb) at ¥20.55/ kWh.

JFE Engineering gets order for large-scale gas engine power generation facility

(Company statement, April 2)

- JFE Engineering inked an order with Toho Gas to build a large-scale gas engine power generation facility – capacity 105 MW (14 x 7.5 MW units); the project includes engineering, procurement, construction and 20 years of operation services.

- The facility will be built on the site of JFE Steel’s Chita Works in Aichi Pref.

- Construction begins in April 2027, with commercial operation by FY2030.

- The facility will help balance power supply and demand amid renewables growth.

- CONTEXT: KHI will provide Toho Gas with the 14 gas engines. Please refer to last week’s summary section for more info.

NEWS: HYDROGEN

Hitachi selected for Tokyo hydrogen station study to develop onsite production model

(Company statement, April 8)

- Hitachi was chosen by the Tokyo Metropolitan Govt to study onsite hydrogen stations, focusing on integrating energy management systems.

- The study will assess cost reduction and business viability, aiming to develop an urban hydrogen station model based on local production and consumption.

- The project will test optimization of power sourcing (grid, solar, fuel cells, batteries) to reduce hydrogen production costs.

- TAKEAWAY: Of Japan’s 150 or so hydrogen fuel stations, several run by ENEOS and Iwatani utilize onsite hydrogen production models. These facilities often use solar panels to power onsite electrolyzers, producing a small portion of the fuel sold at the station. The schemes are largely backed by state subsidies from JHyM or METI. Now, Hitachi and other firms aim to build onsite output that goes beyond pilot scale. The Eurus Energy project to supply Aichi Steel – one of the winners of the CfD subsidy – is basically an onsite production model for a steel heating furnace. Eurus targets production of 1,600 tons/ year by 2030.

Japan Engine begins full-scale testing of hydrogen-fueled engine for large vessels

(Company statement, March 27)

- Japan Engine Corp began full-cylinder hydrogen co-firing tests on a full-scale two-stroke marine engine, a global first at this scale.

- The engine achieved over 95% hydrogen co-firing at 100% load, confirming both stable operation and GHG reduction potential.

- The system is designed for large, long-distance vessels, combining the engine with KHI’s liquefied hydrogen fuel supply system. It will be installed in a 17,500 DWT hydrogen-fuelled vessel, set for delivery in 2027.

- The project is backed by NEDO and involves MOL, Onomichi Dockyard, and ClassNK covering development, shipbuilding and operational testing.

NEWS: SOLAR AND BATTERIES

Chinese solar makers hike Japan prices as costs rise, subsidies end

(Asia Nikkei, April 8)

- Chinese solar panel makers, including Jinko Solar, LONGi and Trina Solar, hiked prices in Japan on growing costs and the end of China’s export tax rebates.

- Canadian Solar, which mainly produces residential panels in China, hiked prices by about 20%, with broader industry cost pressures driven by surging input prices – silver (roughly tripled), silicon (+40%), copper (+30%) and aluminum (+10%). Some estimates put total production cost increases at 60%.

- Beijing’s abolition of VAT export rebates marks a structural shift for the sector, aimed at curbing overcapacity after major Chinese panel makers posted losses in 2024.

- CONTEXT: Japan sources over 80% of its solar panels from China.

- TAKEAWAY: Rising panel prices mark a reversal after two decades of deflation in solar costs, posing a near-term headwind to Japan’s solar capacity expansion. While higher prices may slow adoption especially in the residential market, the industry recognizes that solar PVs have sold for very low prices – especially in the last year or so – and those levels were unsustainable. The big factor yet to be quantified is how shipping disruptions in the Mid East will increase solar PV prices. The Mid East accounts for 10% of the world’s aluminum supply, used for panel frames. Also, petroleum products are used as sealants and coatings for solar panels to protect the cells from moisture and degradation.

Tokyu Land and partners to invest ¥3 billion in extra-high-voltage BESS

(Company statement, April 3)

- Tokyu Land and ReENE formed a consortium in which eight companies – Tokyu Land, IbeeT, Fuyo General Lease, Nomura Real Estate, Maeda Construction, Nippon Steel Kowa Real Estate, Sumitomo Mitsui Trust Bank and Sumitomo Mitsui Trust Panasonic Finance – will invest ¥3 billion in six EHV BESS stations.

- Totaling 174 MW of installed capacity, the BESS are the following:

| TSO area | MW | Expected COD |

| Tohoku | 20 | 2028 |

| Tohoku | 45 | 2028 |

| Tohoku | 26 | 2029 |

| Kyushu | 40 | 2027 |

| Chubu | 14 | 2028 |

| Hokkaido | 29 | 2027 |

Energy Vault enters Japan’s BESS market with 850 MW pipeline

(Company statement, April 9)

- U.S.-based Energy Vault entered Japan’s BESS market by acquiring an 850 MW portfolio from a domestic developer, marking its first move into one of the fastest-growing global storage markets.

- The portfolio consists of:

- 350 MW of advanced-stage BESS projects, with construction targeted for H2 2027 and commercial operation from 2028;

- 500 MW of early-stage projects, forming a longer-term development pipeline.

- The transaction includes the onboarding of a local development team, giving Energy Vault an immediate footprint in Japan’s complex market for land, permitting and grid interconnection.

- The company will deploy its B-VAULT™ AC platform and adopt a technology-agnostic approach, including the integration of next-generation sodium-ion batteries through its partnership with Peak Energy. These are being positioned as an alternative to lithium-ion for applications requiring enhanced safety and thermal stability.

- CONTEXT: Sodium-ion batteries are an alternative to lithium-ion batteries, offering several advantages. Sodium reserves are estimated to be more than 440 times greater than lithium, are widely distributed globally, and do not rely on toxic metals such as lead or cadmium. They are of interest for stationary BESS due to improved fire safety, limited temperature rise during operation, and better resistance to high temperatures. IRENA said global production capacity could reach 400 GWh per year by 2030. For now, these batteries have not been deployed in stationary BESS in Japan.

- TAKEAWAY: Several international players have entered Japan’s fast-growing BESS market in recent months. Most are having to build local teams and secure semi-developed projects with land and grid access already in place. Energy Vault has done both through acquisition, combining advanced-stage assets with local execution capability. CEO Robert Piconi described Japan as “one of the most compelling energy storage growth opportunities globally,” citing projected 50%+ CAGR in BESS capacity. Renewable expansion is accelerating, but grid constraints remain severe: connection applications exceed 170 GW, while less than 1 GW of BESS capacity is currently online, according to the Japan NRG BESS tracker.

ANRE moves to curb surge in BESS grid connection applications

(Government statement, March 27)

- ANRE outlined measures to manage a surge in BESS grid connection applications, as queues become increasingly congested.

- CONTEXT: As of December 2025, around 172 GW of BESS capacity was under review for grid connection nationwide, with a further 30 GW already approved and progressing toward connection. Tohoku has emerged as the most sought-after region, with connection study requests reaching 69 GW, up from 36.8 GW in December 2024 (+53%). Okinawa Electric is the only TSO not experiencing this trend.

- Proposed measures include: o Setting an upper limit on the number of connection study applications per operator, following cases where individual applicants submitted more than 100 requests;

- Prioritising main applications when submissions exceed the cap, or requiring resubmission; o Introducing indicative caps on application volumes.

- Indicative caps are as follows:

| TSO area | Cap per applicant |

| Hokkaido | 5 |

| Tohoku | 6 |

Tokyo | 11 |

| Chubu | 5 |

| Hokuriku | 8 |

Kansai | 10 |

| Chugoku | 5 |

| Shikoku | 5 |

| Kyushu | 8 |

- TAKEAWAY: The government aims to better track applicants through company-level identification (e.g. name and address), but the effectiveness of this approach remains uncertain, as developers may still be able to circumvent the rules. Moreover, the cap – set at five applications per operator – already covers around 90% of current submissions. While this reflects a deliberate effort to avoid unduly restricting developers, it may limit the measure’s impact on overall queue congestion.

ANRE releases FIT/ FIP certification suspensions and revocations

(Government statement, April 6)

- ANRE announced 57 suspensions and 55 revocations of FIT and FIP certifications due to legal violations in FY2025; five cases are under appeal.

- Reasons for suspension include:

- Failure to address issues during METI on-site inspections: 13 cases;

- Violations of the Forest Act: 10 cases;

- Irregular reporting under Special Measures Act on Renewables: 29 cases.

- Reasons for revocation include use of non-biomass fuels, falsification of documents, and installations located outside the approved project site.

- TAKEAWAY: Most suspended projects are biomass; several involve solar installations due to the decision in late 2025 to phase out FIT/ FIP support for large-scale solar power plants. When evaluating these figures it’s important to consider the total number of projects under FIT/ FIP – more than 650 for biomass, several thousands for solar. Revocations of FIT certifications were first recorded in 2019, with eight agrivoltaic projects affected in Okinawa. In 2024, the Special Measures Law for Renewable Energy was revised to introduce “suspension” in addition to revocations, in order to give firms time to clean up their act.

Fuji Keizai report highlights dominance of on-site PPAs in Japan

(Nikkei, April 6)

- On-site PPAs continue to dominate Japan’s market, accounting for around 80% of total installations, according to a report by Fuji Keizai, as companies favour rooftop solar solutions requiring no upfront investment.

- As of FY2025, Fuji Keizai recorded 740 on-site PPAs and 147 off-site PPAs.

- On-site PPAs dominate the market and are primarily used for rooftop solar on commercial and industrial buildings.

- Off-site PPAs accelerated growth since 2024, as not all customers can rely on their own land or facilities. Development of ground-mounted projects on idle land is expected to increase the share of off-site PPAs to about 30% by 2040.

- Total PPAs are expected to reach 4,300 by FY2040; about 1,400 will be off-site.

- TAKEAWAY: This shift toward increased off-site PPAs is seen in the types of deals signed in 2025. Off-site PPAs (both physical and virtual) even overtook on-site PPAs, accounting for nearly 50% of the 237 deals recorded by Japan NRG that year. For more information on current PPA trends, see the March 2, 2026 issue.

EDP to develop solar farm in Miyagi, aims for 500 MW in Japan

(Company statement, April 8)

- Portugal-based EDP will develop a 28 MW power plant in Motoyoshi (Miyagi Pref), expected to start operations in 2028 and generate 33 GWh of electricity annually.

- The company has a pipeline of about 500 MW of solar projects in Japan.

- CONTEXT: In the APAC region EDP has a pipeline of over 1.7 GW of renewable energy projects through 2030 (mostly solar and BESS), with Japan a leading market.

JERA invests $10 mln in U.S. battery startup, inks MoU on supply chain collaboration

(Company statement, April 8)

- JERA invested ~$10 million in the U.S.-based battery startup TeraWatt Technology via its venture arm, targeting next-gen lithium-ion cell manufacturing.

- The two companies also signed an MoU to explore collaboration across the entire battery value chain, including manufacturing, supply, and deployment.

- Potential areas include stable supply of domestically produced batteries to JERA, development of battery supply chains, and clean power provision to TeraWatt’s manufacturing facilities.

- TeraWatt is developing high-output, compact and safer lithium-ion cells.

Kingdom finances LTDA BESS asset in Okayama

(Company statement, April 10)

- Kingdom, which is backed by investment firm Stonepeak, made a project finance loan for a 29 MW BESS project in Mimasaka (Okayama Pref).

- MUFG Bank is the original lender and lead manager.

- This project is the first of nine that will get financing. In total, Kingdom’s portfolio equals 479 MW of installed capacity awarded during the first two rounds of LTDA.

iChoosr agrees with Nara Pref in solar and BESS

(Company statement, March 31)

- iChoosr agreed with Nara Pref to provide solar and BESS solutions.

- The deal takes effect in June for residential customers and in July for corporate customers.

- CONTEXT: Nara Pref aims to reduce carbon emissions nearly 46% compared to 2013 levels. Also, about 30% of its emissions come from the residential sector, compared to a national average of 20%.

- SIDE DEVELOPMENT:

- Bywill agrees with Nara Pref for procurement of environmental value

- (Company statement, April 3)

- Bywill agreed with Nara Pref for the procurement and sale of J-Credits to companies located in the prefecture.

- CONTEXT: This deal aligns with Nara’s decarbonization strategy, which includes promotion of J-Credits.

AUG launches acidic cleaning product for solar PVs

(Company statement, April 7)

- AUG, a company specializing in cleaning products and coatings, launched a new cleaning solution for solar PV systems, “PowerClean-e”.

- This highly acidic product is designed to remove stubborn stains such as rust, carbon deposits, and iron filings.

- TAKEAWAY: Removing deposits from solar panels is essential to maintain performance, which can decline by several percentage points due to soiling losses. Effective cleaning as part of PV maintenance depends on a solar plant’s location. Since Japan’s climate isn’t arid (where PV systems can lose more than 40% of performance if poorly maintained), issues related to insufficient cleaning are less severe. Rainfall contributes to natural cleaning. Manually applied cleaning products are primarily suited for small-scale installations or residential systems, or used as a complement to robotic solutions for larger plants.

- SIDE DEVELOPMENT:

- Campbell Scientific launches sensor to monitor soiling on solar PVs

- (Company statement, April 9)

- Campbell Scientific Japan launched “DustVue 10”, a sensor that measures soiling on solar PVs by comparing the performance of a soiled PV module with a clean module.

- Power losses due to contamination can be determined with an accuracy of ±1%.

- The product is compliant with IEC standards.

- CONTEXT: International Electrotechnical Commission (IEC) is a Swiss-based organization that publishes standards for electrical technologies. IEC 61724-1 defines requirements for monitoring equipment used in solar PV systems.

Nissan Electric joins demo of silicon and PSC cells in sewage plant

(Company statement, April 7)

- Nissan Electric joined an MoE demo with Kyoto City and KEPCO, exploring installation methods for solar power generation in water and sewage infrastructure, where conventional PV systems are difficult to deploy.

- Silicon cells and PSCs are installed in the upper space of a sewage treatment plant to assess performance degradation, and maintainability.

- CONTEXT: The govt aims to install 267 MW of solar capacity in such facilities by FY2030.

NEWS: WIND POWER AND OTHER RENEWABLES

Cosmo’s large Hokkaido onshore wind project enters early environmental review

(Company statement, March 31)

- Plans for Cosmo Energy’s Shimamaki–Kuromatsunai No.2 wind farm in Hokkaido were disclosed under the environmental impact assessment process.

- CONTEXT: The project envisages up to 215 MW of onshore wind capacity, with about 50 turbines (~4.3MW each). The proposed site spans ~3,948 hectares in Shimamaki and Kuromatsunai towns, where a separate wind project is under construction (targeted for 2029 start-up).

- TAKEAWAY: Hokkaido offers some of Japan’s strongest wind resources and already leads in installed capacity, but further expansion faces structural constraints. The region’s relatively small grid and limited interconnection capacity make it particularly sensitive to fluctuations in renewable output, increasing the risk of curtailment and stricter connection requirements. At the same time, large-scale wind developments in Hokkaido have faced growing environmental scrutiny in recent years, particularly over impacts on forests and wildlife. Against this backdrop, projects that incorporate mitigation measures are better positioned to advance. For example, for the original Shimamaki–Kuromatsunai wind farm project, Cosmo planned to install Tesla Megapacks to absorb output fluctuations.

Sompo launches offshore wind insurance and earthquake risk assessment services

(Company statement, March 31)

- Sompo Japan will launch services in April to reassess insured asset values and quantify earthquake risk for offshore wind projects.

- The insurance valuation service updates project values to reflect inflation, FX, equipment costs and rebuilding expenses.

- This addresses gaps between original construction costs and current replacement values. It’s meant to help with project finance structuring.

- Sompo partnered with Kroll to create a model that enables quantitative assessment of earthquake risk, incorporating Japan-specific hazards using seismic data and joint research with the University of Tokyo.

Nippon Steel develops ultra-thick steel plate to support larger offshore wind turbines

(Company statement, April 7)

- Nippon Steel has developed 140 mm-thick steel plates for offshore wind support structures, exceeding the previous practical limit of 100 mm in Japan.

- The product passed METI technical standards for wind power equipment.

- The thicker plates are designed for foundations and towers (monopiles, jackets) needed to support larger turbines.

- CONTEXT: The development addresses Japan-specific challenges, including strict seismic requirements and complex seabed conditions.

Kyushu Electric targets first commercial tidal power in Japan

(Nikkei, April 8)

- Kyushu Electric plans to commercialize tidal power generation by FY2030, with sites under consideration in the Goto Islands, including Naru Strait in Nagasaki Pref.

- The project will be led by Kyuden Mirai Energy, building on field tests (FY2019–2025) that confirmed stable generation and transmission using a single turbine. A long-term pilot (FY2026– 2028) is planned ahead of commercialization.

- Commercial deployment will use multi-unit “farms”, with each turbine expected to have ~2 MW capacity, supplying power primarily to nearby remote islands.

- Tidal power is seen as a reliable and predictable renewable source, with potential to replace aging diesel generation on islands and reduce dependence on imported fuels. However, costs remain a key hurdle, with current estimates ~50% higher than existing island electricity costs, due to reliance on imported equipment.

- TAKEAWAY: The topic comes up from time to time: How to decarbonize Japan’s remote islands or improve their energy security in the face of fuel shipping challenges. At first, it seems like a niche topic, but it could have broader application on the mainland in microgrids and new city developments. For now, most island projects revolve around a single energy facility and do not show scalability.

Takagi Seiko agrees with partners to power factory with local biomass

(Company statement, March 31)

- Takagi Seiko will partner with Tokyo Gas and Hokuriku Electric to fully power its factory in Takaoka (Toyama Pref) with locally sourced renewable energy.

- CONTEXT: In 2025, the factory secured an off-site PPA for solar power and subscribed to an electricity supply plan with Hokuriku Electric.

- The firm subscribes to the utility’s new plan, “Kagayaki Green RE100,” and buys environmental value from a 51 MW biomass power plant owned by Tokyo Gas.

MHI agrees with Fervo Energy on supply of geothermal equipment in Utah

(Company statement, April 8)

- Italy-based Turboden, a subsidiary of MHI, inked a three-year deal with Fervo Energy to deliver 35 Organic Rankine Cycle (ORC) units (total capacity 1.75 GW) for the Cape Station project in Utah, U.S.

- The company is testing the equipment, with operations to begin in H2 of 2026.

- CONTEXT: This deal follows a previous contract under which Turboden supplied three ORC units. ORC converts low-temperature heat sources into mechanical energy and is suited for Enhanced Geothermal Systems, as well as for solar and biomass.

JFE Engineering enters India waste-to-energy market

(Company statement, Nikkei, April 10)

- JFE Engineering will build and operate two waste-to-energy plants in Andhra Pradesh, its second overseas waste management project after Vietnam.

- The company is partnering with India’s Antony Waste Handling Cell, forming SPVs with ¥3 billion total capital; Antony holds 75% and JFE 25%.

- The facilities start operations in FY2028, and will process 750 tons of waste per day and generate about 15 MW of power, sold at ¥8.1/ kWh.

- CONTEXT: The move comes as India shifts from landfill disposal toward incineration-based waste treatment.

Tohoku Electric installs AI security cameras in hydro plant

(Company statement, April 10)

- Tohoku Electric installed 260 cloud cameras to monitor equipment at one of its hydroelectric power plants in Aomori Pref.

- The cameras, provided by AI company Safie, allow real-time monitoring, and feature PTZ (Pan, Tilt, and Zoom) functionality, and WDR (Wide Dynamic Range).

NEWS: NUCLEAR ENERGY

Govt targets operations for innovative reactors in the 2030s

(Government statement, April 8)

- The govt’s Innovative Reactor Working Group released the timeline for next-gen innovative reactors.

- Fast Reactor:

- The design and R&D phase is underway until 2028.

- Then, “Decision to transition to basic design” to check technological maturity, long-term energy policy, and economic viability.

- This year, “Fuel Selection” will take place, deciding between oxide and metal fuels.

- Demo operations in the 2040s.

- High-Temperature Gas-cooled Reactors (HTGR):

- Conceptual design for the demo should conclude this year. o Next year, the basic design phase for the HTGR demo reactor will begin.

- In FY2028, hydrogen production testing through the High Temperature Engineering Test Reactor (HTTR) will begin.

- In FY2029, check costs and determine the transition to the next stages of development and implementation.

- Launch should begin in the late 2030s; commercial operations in the 2050s.

- SMRs: By mid 2030s Innovative Light Water Reactors will be operating, with design and construction slated for later in 2020s.

- Small Light Water Reactors should enter design and construction in the 2040s, with design and construction targeted in the earlier decade.

- Fusion: Japan aims to achieve a power generation demo in the 2030s.

Blackstone, SoftBank among bidders for TEPCO capital tie-up worth >¥1 trillion

(Nikkei, April 9)

- CONTEXT: TEPCO Holding is state-owned thanks to a bailout after disaster struck its Fukushima Daiichi NPP in March 2011. The utility has endured ongoing financial strain partly due to Fukushima cleanup costs, with seven consecutive years of negative free cash flow through FY2024. The company’s most recent business plan called for the formation of new capital alliances to help recover.

- TEPCO has interest from Blackstone, Apollo, Bain Capital, KKR, SoftBank and JIP to secure a capital alliance under its latest restructuring plan.

- Initial bids closed at end-March, with dozens of applicants, though some, such as Kansai Electric, have withdrawn at the screening stage.

- TEPCO will now shortlist partners and structure deals over the coming months.

- External investment could exceed ¥1 trillion, with financial sponsors seen as strong candidates, though TEPCO is also prioritizing strategic synergies, including with data center operators, telecom firms, construction companies and gas utilities.

- SIDE DEVELOPMENT:

- TEPCO announces ¥258 billion for Fukushima decommissioning

- (Nikkei, April 6)

- TEPCO announced its FY2026 decommissioning cost plan for Fukushima Daiichi; costs are projected at ¥257.8 billion, a decrease of ¥2.6 billion from the previous year.

- This includes ¥41.3 billion for waste management and ¥13.2 billion for preparing to remove melted fuel debris. o Costs also include an increased frequency of treated water releases, and a robotic arm test for debris retrieval at Unit 2.

- Costs could rise to ¥308 billion in FY2027, and ¥275 billion in FY2028 due to debris retrieval surveys and preparation for removing spent fuel.

- CONTEXT: The decommissioning funds are pre-accumulated by TEPCO with the Nuclear Damage Compensation and Decommissioning Corp. The plan for FY2026–2028 received approval from METI Minister Akazawa on April 6.

Tohoku Electric replaces detectors that malfunctioned at Onagawa NPP

(Company statement, April 7)

- Tohoku Electric replaced four hydrogen concentration detectors (including the two functioning ones).

- CONTEXT: On May 26 and June 20, 2025, two hydrogen concentration detectors in the reactor containment vessel at Onagawa Unit 2 malfunctioned, failing to show correct values.

- SIDE DEVELOPMENT:

- Malfunction at Fukushima Daini NPP leads to temporary suspension

- (Kyodo, April 7)

- A malfunction of a cooling pump at Fukushima Daini NPP led to a temporary suspension of operations at Unit 1’s spent fuel pool on April 5.

- Officials confirmed that water temperatures remained well below safety limits and posed no immediate threat.

Takahama NPP Unit 3 enters periodic inspections

(Company statement, April 3)

- Takahama NPP Unit 3 will undergo periodic maintenance starting April 7. The operator, KEPCO, will make a total replacement of steam generators and will install reactor protection panels.

- The schedule also includes nuclear fuel replacement. The reactor should resume full commercial operations by early December.

NEWS: TRADITIONAL FUELS

METI forecasts over 10% decline in oil product demand through FY2030

(Government statement, April 7)

- Japan’s total fuel oil demand (excluding power-sector C heavy oil and naphtha) is forecast at 99.6 million kL in FY2026 (-2.1% YoY vs FY2025), declining further to 91.2 million kL by FY2030 (10.3% vs FY2025).

- The decline reflects electrification, fuel switching, efficiency gains, and demographic contraction, with demand falling at an average -2.2% per year over 2025–2030.

- Gasoline (transport fuel):

- FY2025: 43.5mn kL → FY2026: 42.4mn kL (-2.6%) → FY2030: 39.2mn kL (-10% vs 2025);

- Drivers:

- Declining passenger vehicle ownership

- Improved fuel efficiency and use of hybrid engines

- Gradual EV penetration;

- Diesel / gasoil (freight, commercial transport):

- FY2025: 30.7mn kL → FY2026: 30.4mn kL (-0.9%) → FY2030: 29.2mn kL (-4.7%);

- Drivers:

- Logistics efficiency improvements

- Declining freight volumes

- Efficiency gains in trucks;

- Kerosene (heating):

- FY2025: 10.8mn kL → FY2026: 10.6mn kL (-1.8%) → FY2030: 8.5mn kL (-21.2%);

- Drivers:

- Electrification and gasification of heating

- Warmer temperatures

- Population decline;

- Jet fuel (aviation):

- FY2025: 4.16mn kL → FY2026: 4.12mn kL (-0.8%) → FY2030: 4.08mn kL (-1.7%);

- Drivers:

- Recovery in passenger demand offset by

- Aircraft efficiency improvements;

- Heavy oil A (industrial, agriculture, marine):

- FY2025: 9.2mn kL → FY2026: 8.8mn kL (-4.0%) → FY2030: 7.5mn kL (-19.0%);

- Drivers:

- Fuel switching (to gas, electricity, biomass) – Declining activity in agriculture and fisheries;

- Heavy oil B/C (industrial and marine fuels):

- FY2025: 3.3mn kL → FY2026: 3.18mn kL (-3.6%) → FY2030: 2.72mn kL (-17.7%);

- Drivers:

- Industrial fuel switching

- Shipping sector efficiency and structural decline;

- TAKEAWAY: Japan’s population is declining but the reduction in oil consumption is far outpacing that decline. Japan will have about 3% fewer people by the end of the decade compared with 2025. In that period, the percentage drop in oil use is estimated in double-digits. These declines are broad-based – across all fuels, with transport fuels (gasoline, diesel) showing a gradual erosion, but heating fuels (kerosene) and industrial fuels (heavy oils) on course for an accelerated phase-out. The least predictable is the outlook for the power-sector fuel oil, due to the generation mix variability.

JBIC to back Mitsubishi Corp in Aethon acquisition

(Nikkei Asia, April 10)

- JBIC will provide a $2.8 billion loan to support Mitsubishi Corp’s $7.55 billion acquisition of Aethon, a U.S. natural gas developer.

- Part of the gas produced will go to Japan. JBIC is coordinating with private banks including MUFG.

- CONTEXT: The loan follows a similar public-private financing for Nippon Steel’s acquisition of U.S. Steel. Aethon’s shale gas output, equal to about 15 Mtpa of LNG, equals one-quarter of Japan’s annual LNG demand.

- TAKEAWAY: This is Mitsubishi Corp’s largest deal ever and completes its U.S. natural gas supply chain. Mitsubishi already has wholesale and LNG plant operators. The IEEJ foresees a decline in long-term LNG contracts, especially supplies from Australia, and so the deal strengthens Mitsubishi’s position in the global market.

INPEX considers reallocating Mid East investments to SE Asia

(Nikkei, April 10)

- INPEX is considering reallocating part of its Middle East investment to SE Asia.

- The company had planned to invest up to ¥300 billion in Abu Dhabi as part of its ¥850 billion growth investment for FY2026. Now it’s looking at acquiring stakes in producing or pre-production oil and gas fields in Indonesia and Malaysia.

- INPEX handles 500,000 bpd, accounting for 20% of Japan’s crude imports, with about two-thirds coming from Abu Dhabi. Restrictions on transiting the Strait of Hormuz have reduced output. While no major damage has occurred at UAE facilities, the company is assessing the situation.

- CONTEXT: Japan relies on the Middle East for 95% of its crude oil imports; the UAE supplied over 40% in 2024. PM Takaichi recently requested the UAE’s cooperation in ensuring stable supply.

Japan turns to offshore oil transfers to avoid Mid East risk

(Bloomberg, April 7)

- Japan increasingly relies on risky ship-to-ship oil transfers in SE Asia and off the coast of India to secure crude supplies while avoiding direct tanker exposure to the Iran war zone.

- A VLCC carrying Murban crude recently transferred around 1.2 million barrels off Malaysia before heading to Hokkaido, following a similar offshore transfer in late March – an uncommon practice for Japanese buyers.

- CONTEXT: Japanese shipowners have largely suspended operations through the Persian Gulf due to security risks. Only two Japan-owned oil tankers have transited the Strait of Hormuz since the conflict began.

- TAKEAWAY: About 94% of the crude imported by Japan’s refineries comes from the Middle East, which has particular kinds of oil grades not easily replaced with supplies from other regions. Engaging in STS transfers highlights growing strain on Japan’s oil supply chains despite the nation’s ample stockpiles. Officials are reportedly seeking other routes that could switch oil from Persian Gulf producers to Asian countries.

Chiyoda mulls construction restart at Qatari LNG plant

(Bloomberg, April 8)

- Chiyoda is thinking of restarting construction at the Ras Laffan LNG complex in Qatar if a ceasefire can be reached between Iran and the U.S.

- CONTEXT: Ras Laffan accounts for nearly all of Qatar’s LNG output with 77–80 Mtpa, about 20% of global LNG supply. Ras Laffan halted operations after an Iranian drone attack in March forced evacuations.

- Major damage to the facility may take years to repair.

- Investors reacted well to the news, sending Chiyoda’s shares up 16%.

- It is widely believed that Chiyoda and other Japanese engineering firms will play a major role in rebuilding infrastructure across the Middle East.

- CONTEXT: Chiyoda has a deep history in Qatar’s LNG industry, carrying out the EPC for 12 out of the 14 LNG trains at Ras Laffan. Chiyoda is also a key partner in Qatar’s North Field East and North Field West.

Strike risk emerges at Inpex’s Ichthys LNG project in Australia

(Bloomberg, April 9)

- A union representing ~400 workers at the Ichthys LNG project applied for a protected ballot, opening the door to potential strike action after six months of stalled negotiations with operator INPEX.

- If approved, a worker vote could take place later in April, with industrial action possible from May 3.

- The Offshore Alliance said this is an escalation in labor talks, while INPEX maintains its offer is “fair and competitive” and aims to reach a deal without disruption.

- CONTEXT: Ichthys supplies about 10% of Japan’s LNG fuel needs. The dispute is sensitive amid tight global gas markets and intense geopolitical risk. Several other Australian LNG projects are repairing damaged capacity due to recent storms.

LNG stocks flat from previous week, up YoY

(Government data, April 8)

- As of April 5, LNG stocks of 10 power utilities were 2.2 Mt, same as the previous week; up 10% from end April 2025 (2 Mt), and up 3.8% from the 5-year average of 2.12 Mt.

NEWS: CARBON CAPTURE & SYNTHETIC FUELS

ANRE sets FY2026 external procurement ratio at 14.8% in non-fossil trading

(Government statement, April 3)

- ANRE discussed the external procurement ratio and the use of alternative procurement in the nonfossil certificate (NFC) market.

- The external procurement ratio used for interim targets under the Sophisticated Energy Supply Structure Act will be set at 14.8% for FY2026, broadly unchanged from FY2025.

- This level is calibrated to maintain the supply–demand balance in the non-FIT NFC market at around 1.05, in order to limit price volatility.

- Reflecting the latest supply plan – including increased nuclear restarts – the volume available for external supply rose significantly (by about 15.5 TWh to around 127 TWh). The procurement ratio is then set based on this updated supply outlook while maintaining the fixed balance assumption.

- To achieve FY2025 targets, the use of FIT certificates for substitute procurement will continue, as in the previous year. Substitution is permitted if retailers bid for the required volume in the final nonFIT auction at the price cap of ¥1.3/kWh.

- TAKEAWAY: The external procurement ratio defines the share of non-fossil value that retailers must procure externally to meet regulatory targets. It is set annually by ANRE based on projected supply–demand conditions, with the explicit aim of maintaining a stable market balance (around 1.05) and limiting price volatility. In practice, it serves as a key policy lever to control demand for NFCs and ensure a level playing field between utilities with different generation portfolios.

ANALYSIS

BY NICOLAS VIERGE

Corporate PPAs: Hedging Against Future Power Supply Risk

Corporate energy procurement strategies are often built on a simple, implicit assumption: that tomorrow’s market conditions will broadly resemble today’s. Chief among these assumptions is that energy – like most commodities – will remain readily available, provided buyers are willing to pay the prevailing price.

In Japan, this premise is becoming increasingly uncertain.

Power demand is expected to rise significantly, driven by the expansion of data centers and semiconductor manufacturing. The grid oversight body, OCCTO, projects electricity demand could reach as much as 1,100 TWh by FY2040 – an increase of roughly 25% from current levels. In parallel, METI targets a similar level of generation, at about 1,150 TWh by FY2040.

However, the assumptions underpinning METI’s outlook, as laid out in the nation’s 7th Basic Energy Plan, face mounting physical and structural constraints. Several of the power sectors that are forecasted to grow substantially are struggling with costs, regulations, diminishing returns and grid integration issues.

The one electricity source that was quietly expected to pick up the slack should others fail to deliver – gas-fired power generation – now faces greater scrutiny over fuel delivery disruptions due to the Iran war and extreme weather events in Australia.

As a fallback to the fallback plan, the government is easing restrictions on the use of older, less efficient coal-fired stations. Many are already half a century old. To assume that these will be around to backstop supply shortages in 2040 is naive. So would be the idea that the current electricity supply cornucopia will continue into the next decade.

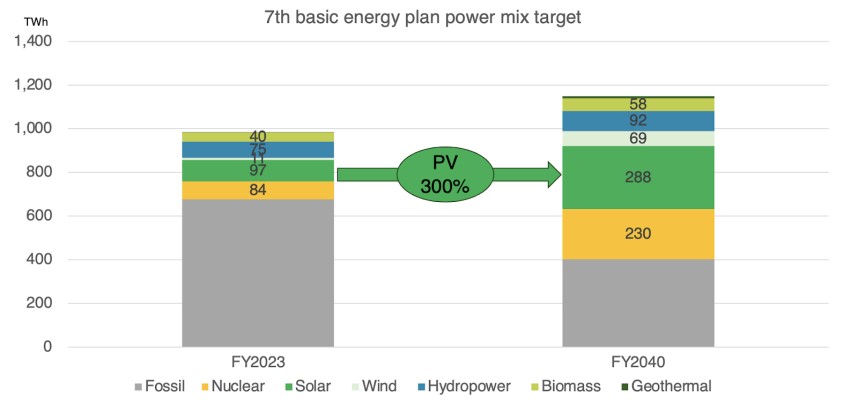

Solar ambitions vs realities

A significant challenge to METI’s plans lies in the expansion of Japan’s solar PV capacity, which energy planners aim to nearly triple over the next 15 years. This target is compounded by the need to repower a substantial share of existing solar farms.

Source: METI

In effect, within the next 15 years Japan would need to install almost four times the solar capacity that it added over the past 14 years – while contending with shrinking land availability, EPC manpower, and the difficulties of grid integration.

Even a doubling of installed solar capacity might be difficult under present conditions.

Nuclear constraints

Nuclear restarts represent another critical pillar of the plan. The “slack” in the system is real. There is more than 18 GW of nuclear capacity classified as operable but sitting idle. Yet restart progress remains constrained by regulatory processes and resource limitations in the industry watchdog, the NRA.

Tensions between operators and the regulator continue, partly due to scandals over falsified data that over the past years has related to several utilities. The latest, over data reports for Hamaoka NPP, threatens to substantially delay or, at worst, derail the operation of Chubu Electric’s station.

The assumption that all restartable reactors will return to service within the METI timeline is far from guaranteed. After all, it took 14 years to restart about 15 GW of capacity, starting with the “low hanging fruit.”

Thermal generation: relief?

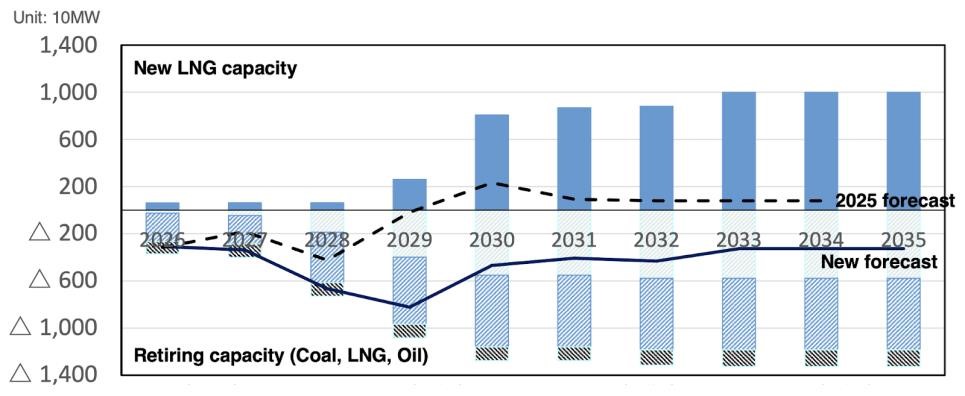

Thermal generation offers limited relief. METI anticipates a net decline in fossil fuel capacity – coal, oil, and gas – through at least FY2034, with annual net reductions ranging from 2.5 GW to 8 GW. Moreover, even under optimistic scenarios where all retiring capacity is replaced, METI has indicated a potential shortfall of about 13 GW of dispatchable capacity by FY2040 if demand evolves in line with OCCTO projections.

Source: METI

Compounding these challenges are long development timelines for new generation assets. METI, in its Long-Term Decarbonized Power Sources (LTDA) auction rules, estimates lead times of around 17 years for nuclear projects and six to 11 years for gasfired plants. At the same time, fuel procurement security is becoming a salient concern, and recent global disruptions in the Middle East and elsewhere highlight the potential for sustained volatility in energy markets.

Taken together, these dynamics point to a growing risk of structural tightness in Japan’s power supply over the mid and long term. As physical constraints intensify, demand-side adaptation may become unavoidable, with some industrial activity potentially constrained by electricity availability rather than price alone.

The question of which industries should be prioritized for their power supply — and which should be constrained — is something Japan will have to address in the coming decade.

Buyers should draw conclusions

In this context, corporate buyers should expand planning frameworks beyond assumptions of “business-as-usual.” This includes explicitly considering scenarios characterized by heightened price volatility and, more fundamentally, by constraints on physical power availability – whether renewable or conventional.

Corporate PPAs offer a strategic tool to hedge against these risks. While typically valued for their ability to lock in long-term prices, PPAs also provide something more fundamental: secured access to electricity over extended periods. This supply security dimension is rarely quantified in negotiations and is even less frequently reflected in pricing.

To date, approximately 4 GW of corporate PPAs have been disclosed in Japan. Although deal activity is accelerating, overall volumes remain modest relative to potential demand.

Several structural barriers continue to limit market growth and this should make big power buyers more cautious about whether their long-term supplies are secured. First, the pipeline of new renewable assets is constrained by land scarcity, EPC availability, and grid connection delays – particularly for projects that meet additionality requirements.

Second, a persistent gap exists between the cost of developing new assets and the price levels that offtakers are willing to accept. This disconnect is often rooted in two misconceptions: that decarbonization will inherently reduce energy costs, and that renewables costs will continue to decline, as they have historically.

Third, many industrial buyers in Japan remain unfamiliar with PPA structures, risk allocation, and strategic benefits. As a result, transactions often require lengthy education processes and protracted negotiations.

These factors help explain the prevalence of smaller-scale PPA transactions in the Japanese market. Frequently, there are high-voltage projects benefiting from FIP mechanisms, where development constraints are less acute. The price differential between such projects and unsubsidized, utility-scale greenfield solar (10 MW and above) can exceed ¥3/ kWh.

In effect, while demand for corporate PPAs in Japan is strong, it is highly price-sensitive. This creates friction between rising development costs and offtaker expectations.

A more explicit recognition of long-term power supply risks – beyond price alone – could help bridge this gap. Incorporating the value of supply security into procurement strategies may not only reshape buyer perspectives but also support the execution of a greater number of PPA transactions.

In that sense, corporate PPAs should not be viewed merely as a decarbonization tool or a hedge against price volatility. They are increasingly a hedge against something more fundamental: the risk that power may simply not be available when it is needed.

In a system where supply adequacy can no longer be taken for granted, securing electrons – not just managing their cost – may become the defining challenge for industrial buyers.

Nicolas Vierge is Founder and Principal at Carbon50, providing consulting in the Japanese power industry on corporate PPA structuring, pricing and negotiations, BESS tolling and monetization, physical power trading, and M&A deals. He is also a part-time lecturer at Rikkyo University.

ANALYSIS

BY YURIY HUMBER

Tokyo’s First Curtailments Become Recurring, Strengthens Case For BESS

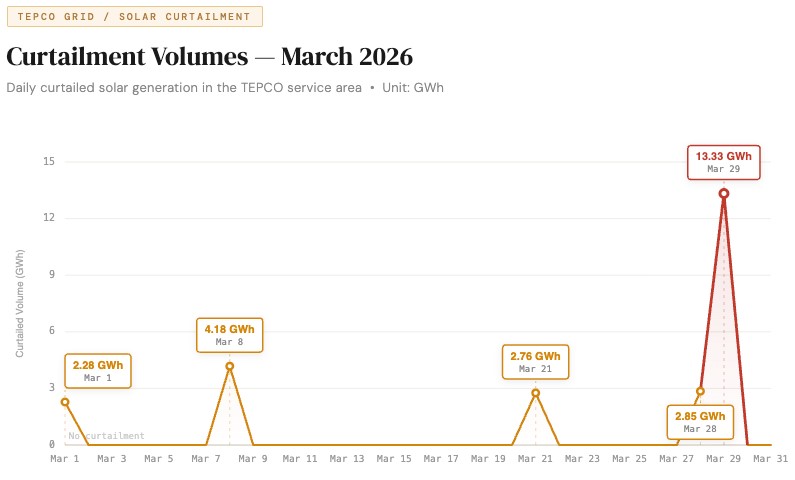

Since the start of Japan’s solar boom in 2012, the power grid serving the Tokyo metropolitan area has never been forced to turn off solar or wind farms due to excess supply. In March, it happened not once but five times.

The curtailments have so far been confined to weekends, when electricity demand is lower, but they have already formed a recurring pattern that extended into April. With flexibility in the TEPCO Power Grid area increasingly constrained, the combination of weather and demand conditions that trigger curtailment is more frequent.

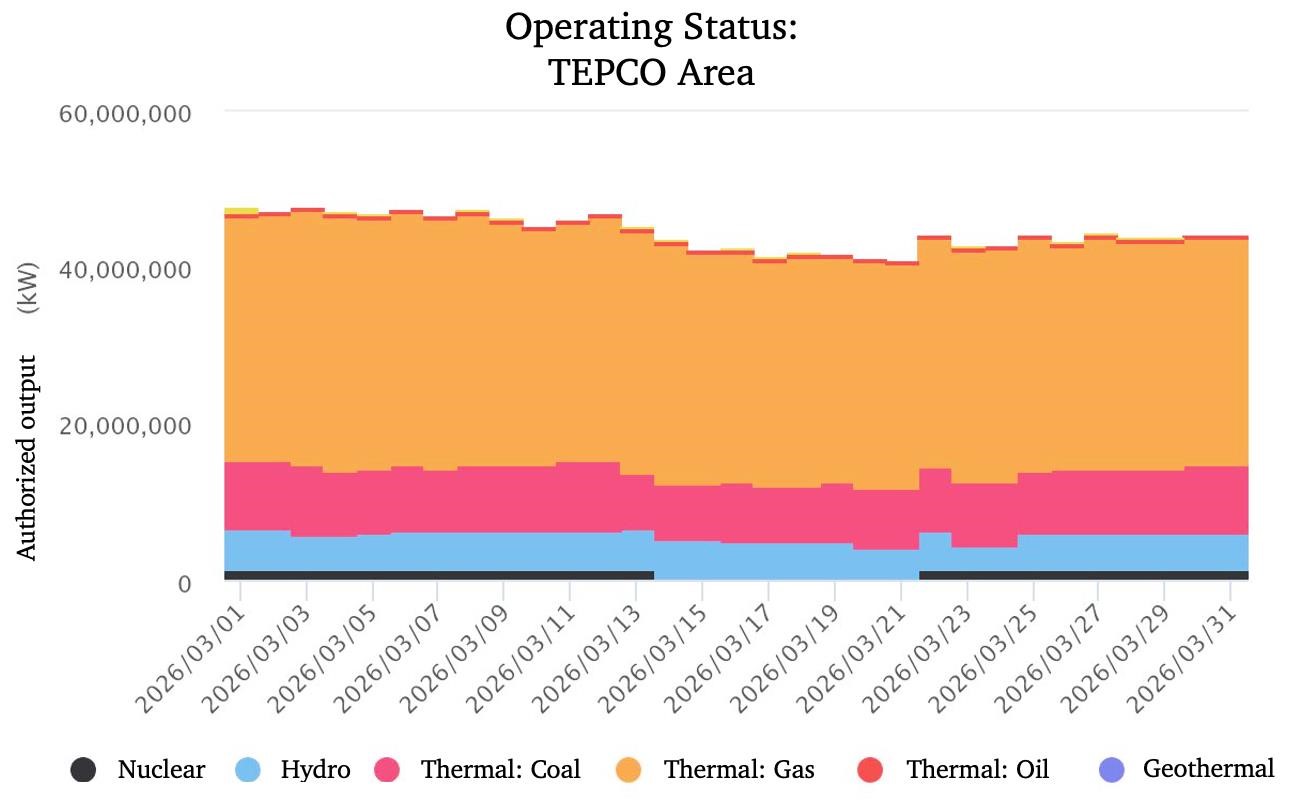

This suggests the issue is no longer incidental but structurally embedded, according to Japan NRG analysis of grid, weather and plant maintenance data.How the Tokyo grid absorbs the return of nuclear power will be a key test for renewable integration. While in western Japan nuclear generation has largely displaced coal- and gas-fired output, the Tokyo system appears more tightly balanced.

Curtailment patterns in March suggest that the availability – and inflexibility – of thermal and nuclear generation is already influencing when renewable output must be reduced, as Kashiwazaki Kariwa NPP Unit 6 moved in and out of service during the month. TEPCO’s operating approach has also shifted since the first curtailment on March 1, and is likely to continue evolving.

Curtailing renewable output when supply exceeds demand is becoming a broader feature of Japan’s power system. Almost all ten of the regional grids faced curtailment conditions in March, with Kyushu the most affected, at times curtailing roughly a sixth of its solar output.

Beyond the immediate loss of zero-carbon electricity, curtailment highlights a deeper challenge: renewable capacity is expanding faster than the system’s ability to absorb it, increasing pressure on storage, transmission and flexible generation.

Source: TEPCO Power Grid

First time becomes regular

The first curtailment in the Tokyo area took place on March 1, when TEPCO Power Grid instructed solar and wind operators to reduce output for several hours around midday. The intervention was brief and limited, amounting to roughly 2.3 GWh of curtailed electricity, according to dispatch data.

Within a week, however, the pattern began to repeat. A second curtailment on March 8 lasted significantly longer, running from early morning through mid-afternoon. Although the peak reduction in output was smaller, the longer duration resulted in a larger total volume of curtailed generation.

Further events followed later in the month. Curtailment was implemented again on March 21 and March 28, before intensifying sharply on March 29, when clear weather and low demand combined to produce the largest intervention of the period. Dispatch data indicate that more than 13 GWh of renewable generation was curtailed that day, several times the volume seen at the start of the month. It was also equivalent to 1.2% of all electricity consumed that day in the TEPCO area.

Taken together, the March data show how quickly curtailment moved from a one-off to a recurring feature of power system management. In fact, the clustering of events and particularly the back-to-back curtailments on the final weekend of the month suggests that the underlying conditions are now appearing with increasing regularity rather than by chance.

| Date | Day | Demand (GW) | Solar peak (GW) | Weather | Nuclear status | Thermal availability | Curtailment (GWh) |

| Mar 1 | Sun | ~25–26 | ~14.8 | Clear | Online | Normal | 2.28 |

| Mar 8 | Sun | ~25–26 | ~14–15 | Mostly clear | Online | Normal | 4.18 |

| Mar 21 | Sat | ~25–27 | ~13–14 | Fair | Offline | Higher flexibility | 2.76 |

| Mar 28 | Sat | ~25–26 | ~12–13 | Cloudy / light rain | Online | Reduced (~-2 GW) | 2.85 |

| Mar 29 | Sun | ~25–26 | ~15+ | Sunny | Online | Reduced (~-2 GW) | 13.33 |

Weather impact

One of the clearest features of the March curtailments is their timing – the interventions occurred on weekends, when electricity demand in the Tokyo region is typically lower due to reduced industrial activity.

Lower demand reduces the system’s ability to absorb renewable output. On weekdays, midday electricity demand in the TEPCO area typically reaches around 30–35 GW. On weekends, it can fall closer to 25–27 GW. That difference represents the margin that determines whether solar generation can be accommodated or must be curtailed.

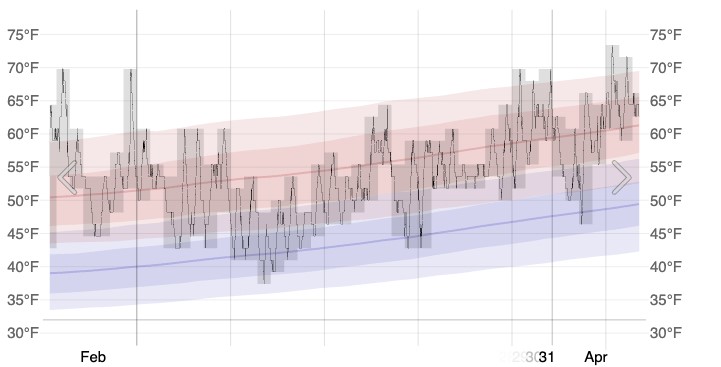

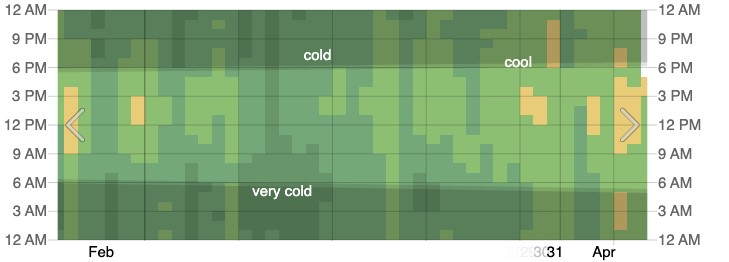

Weather conditions amplified the effect as the month progressed. Daylight hours in Tokyo increased from about 11 hours and 24 minutes at the beginning of March to more than 12 and a half hours by the end of the month, according to WeatherSpark data. Combined with clearer skies, this led to higher solar output during late-March weekends.

The contrast between March 28 and March 29 illustrates the point. The Saturday was marked by cloud cover and intermittent rain, limiting solar generation and resulting in relatively modest curtailment. The following day was clearer and sunnier, and curtailment volumes rose sharply as solar output increased.

Temperature also played a role. Colder conditions earlier in the month likely supported higher electricity demand for heating, helping to absorb renewable generation. As temperatures rose toward the end of March, demand weakened while solar output increased, creating conditions more conducive to oversupply.

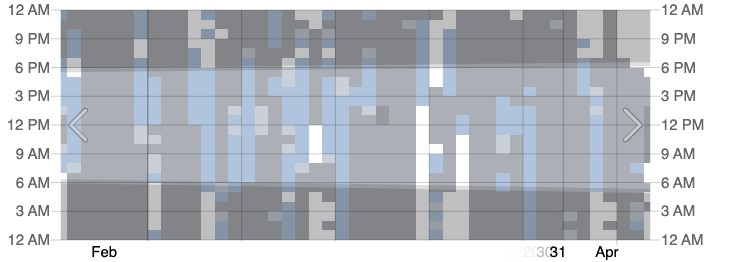

March 2026 in Tokyo Area Temperature history

Hourly Temperature

Cloud Cover

Flexibility hits limit

March curtailments offer an interesting glimpse into the small room for error in the TEPCO area grid and the lack of system flexibility.

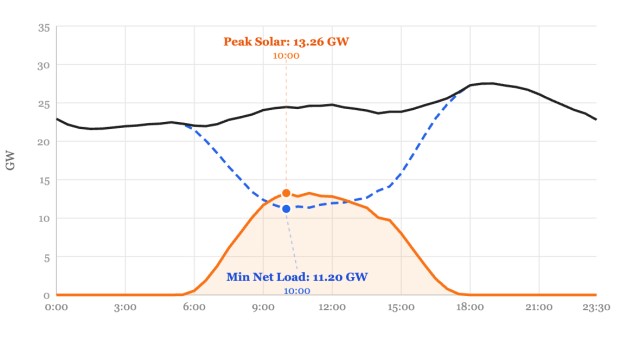

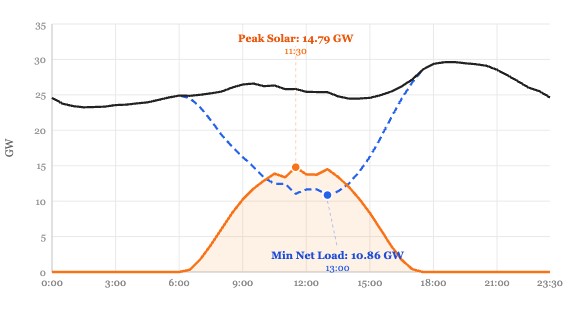

The issue hinges on the balance between renewable generation and what grid operators refer to as “net load” – the portion of demand that must be met by controllable power sources such as thermal plants and hydropower to maintain system stability and grid reliability.

During the curtailment events, net load in the TEPCO area appears to have fallen to around 10–11 GW at midday. This level seems to be close to the minimum at which the TEPCO system can operate reliably. Below that point, thermal plants cannot reduce output further without compromising stability, and additional renewable generation must be curtailed.

Before resorting to curtailment, the grid operator deployed a large share of the system’s available flexibility. Pumped-storage hydro plants absorbed several gigawatts of excess electricity by shifting energy into reservoir storage. At the same time, output from gas- and coal-fired power plants was reduced significantly.

Even so, these measures proved insufficient once solar output rose above a certain level. The data suggest that under low-demand conditions – such as weekends and holidays – TEPCO Power Grid can absorb roughly 15 GW of solar generation before curtailment becomes necessary.

Of course, this threshold is not fixed. It depends on demand, weather and the availability of flexible generation. But the March events indicate that the system is now operating close to its limits during periods of strong solar output.

Role of thermal power

The availability of conventional generation played an important role in shaping the curtailment pattern during March.

Between March 14 and 22, no nuclear power was supplied to the TEPCO grid after Kashiwazaki Kariwa Unit 6 was taken offline to address a control rod issue. During that period, the system relied more heavily on gas- and coal-fired generation, which can be adjusted more flexibly than nuclear in response to changing conditions.

Notably, no curtailment occurred during that weekend despite favorable solar conditions. This suggests that the absence of inflexible nuclear generation increased the system’s ability to accommodate renewables.

Later in the month, however, the situation changed. Available thermal capacity appears to have been reduced by around 2 GW compared with early March, reflecting maintenance outages. At the same time, nuclear generation resumed.

The combination reduced the system’s flexibility just as solar output was increasing, contributing to the larger curtailment volumes observed toward the end of the month.

This dynamic highlights that curtailment is not driven solely by the volume of solar and wind generation but by the interaction between renewables and the flexibility of the rest of the energy system.

Grid operator changed tack

The way TEPCO managed curtailment evolved over the course of the month. The first intervention on March 1 was short and concentrated around the midday peak in solar output, suggesting that the grid operator allowed renewables generation to rise close to system limits before acting.

Subsequent curtailments were implemented earlier in the day and sustained over longer periods. By mid-March, curtailment windows extended from morning through midafternoon, spreading reductions in output more evenly over time.

This shift indicates a move from reactive to anticipatory system management. In effect, by curtailing earlier, the operator can avoid sharper reductions later in the day and reduce the risk of instability. That’s an approach also seen in more mature renewables markets.

TEPCO Power Grid — Duck Curve Comparison

March 1 vs March 29, 2026 | 30-minute interval dispatch data | Unit: GW

Conclusion

March provided an early indication of how curtailment may evolve in the Tokyo area.

With Kashiwazaki Kariwa Unit 6 due to enter commercial operation on April 16, the system will lose a further degree of flexibility. Curtailments in April are likely to follow the pattern established in March, but could become more pronounced toward the end of the month and into early May, when the Golden Week holiday period reduces industrial demand.

At the same time, longer daylight hours and rising solar intensity will increase renewable output, coinciding with a seasonal lull in electricity consumption when demand for both heating and cooling is limited.

For now, curtailment appears likely to remain concentrated on weekends and holidays. Weekday demand still provides sufficient headroom to absorb most solar generation, particularly while thermal plants retain some flexibility. However, the addition of another 4–5 GW of solar and wind capacity without corresponding increases in storage or grid flexibility could begin to push curtailment into regular working days.

Seen from another perspective, these conditions are strengthening the business case for BESS in the TEPCO area, where opportunities for further pumped hydro expansion are limited. Greater deployment of storage, alongside demand-response measures, will be key to managing rising renewables output.

ASIA ENERGY REVIEW

BY JOHN VAROLI

A brief overview of the region’s main energy events from the past week

Australia / Energy security

In a phone call, the Chinese and Australian premiers discussed the “importance of energy security” seeking “ways to work together for the benefit of our nations and our region.

Australia / Natural gas

Santos said it’s progressing the Barossa gas project towards restarting production and delivering full rates, following a temporary production stop at the Darwin LNG project.

China / Decarbonized power

President Xi called for accelerating plans to build new energy systems, especially hydropower development, as well as expansion of nuclear power.

China / Oil refineries

China granted independent refiners additional crude import quotas to continue to produce fuels at mandated levels. The concession aims at keeping fuel production high.

India / Renewables financing

Access to suitable debt financing will be crucial to India’s plan to install 500 GW of renewable capacity by 2030 and achieve 60% non-fossil fuel in its power mix by 2035, said the Institute for Energy Economics and Financial Analysis.

India / Renewables ranking

India ranks third globally in renewable energy installed capacity, surpassing Brazil. In 2025-26, India added a record 55 GW of non-fossil power capacity, now totaling 283 GW.

Philippines/ Renewables

The govt is fast-tracking 1.47 GW of new power capacity from 22 projects. This includes 12 solar projects totaling 1.28 GW, six hydroelectric plants generating 48.2 MW, two biomass facilities with 38 MW.

South Korea / Helium

Presidential policy adviser Kim Yong-beom said South Korea secured about four months’ worth of helium supplies for the semiconductor industry.

South Korea / Oil

The presidential chief of staff will travel to Kazakhstan, Oman and Saudi Arabia to secure supplies of crude oil and naphtha. South Korea is diversifying supply lines; the Hormuz route accounts for about 61% of its crude oil and 54% of its naphtha imports.

Taiwan / Coal

Taiwan Power, the state-owned utility, will buy power from the Mailiao coal-fired plant starting May after Units 1 and 3 are ramped up, said the Economic Affairs Ministry.

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Hulic Ochanomizu Bldg. 3F, 2-3-11, Surugadai, Kanda, Chiyoda-ku, Tokyo, Japan, 101-0062.