WEEKLY

July 6, 2026

ANALYSIS

LOW LATENCY, LONG DISTANCE: JAPAN’S NEXT DATA-CENTER CATALYST

- Japan’s data-center site selection is largely an energy problem. Tokyo and Osaka are the nation’s core datacenter markets, offering dense fiber networks and high demand.

- But land there is expensive, grid capacity is tight and local resistance is building. New technological advances might allow data center capacity to move to regions with cheaper land, and cooling and renewable-energy advantages.

SQUEEZING THE ATOM: JAPAN AIMS TO MAXIMIZE NUCLEAR ENERGY OUTPUT

- Government reports view nuclear power as a low-carbon baseload that stabilizes the grid, and they plan for it to once again play a major role in the nation’s future.

- But practical problems surrounding reactor restarts and building new-gen reactors will limit the state’s options.

ASIA PACIFIC REVIEW

This column provides a brief overview of the region’s main energy events from the past week

NEWS

- Govt to accelerate energy conservation and transition to non-fossil energy

- Daiki Axis and Morgenrot launch a renewable-powered AI data center business

- OCCTO publishes draft demand curve for capacity market main auction

- ANRE proposes market design options for mid- to long-term trading

- PM Takaichi backs India green ammonia project aimed at Japan buyers.

- ANRE announces new CfD-certified project

- MGC, Gold Hydrogen ink MoU for green methanol using natural H2 in Australia

- First FY2026 PV auction attracts many bids

- Toyota Tsusho expands Tunisia solar portfolio

- EneCoat’s PSC generates power in space demo

WIND POWER AND OTHER RENEWABLES

- Kyushu launches offshore wind partnership to strengthen regional supply chain

- Vestas completes assessment for turbines for offshore wind project

- Sumitomo sells stakes in Belgian offshore wind farms

- NRA reveals Chubu Electric continued falsifying earthquake data at Hamaoka NPP

- Kyushu Electric applies for long-term facility management for Genkai NPP reactor

- Crude oil from U.S. increases while total imports fell in May

- JERA sets up unit to manage LNG imports

- INPEX buys stake in Malaysian gas field

CARBON CAPTURE & SYNTHETIC FUELS

- Clean Energy Connect and Green AI partner on decarbonization solution

EVENTS

Jun 11-Jul 19 FIFA World Cup

August Asia-Pacific Economic Cooperation / Energy Ministerial Meeting

Sept 7-10 APPEC 2026, Singapore

Sept 9-11 Smart Energy Week (Autumn) 2026 @ Makuhari Messe (co-exhibiting H2 & FC Expo, Battery Japan, Smart Grid, Wind Expo, CCUS Expo, etc.)

Sept 9-11 Automotive World @ Makuhari Messe

September 14-18 IAEA General Conference 2026 @ Vienna, Austria

October International Maritime Organization –

Net-zero Discussions

Nov 2-5 ADIPEC 2026 @ Abu Dhabi

Nov 3 U.S. Midterm Elections

Nov Publication of International Energy

Agency – World Energy Outlook 2026

Nov 18-19 Asia-Pacific Economic Cooperation –

Leaders Meeting @ Shenzhen, China

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Chief Editor)

John Varoli (Senior Editor, Americas)

Kyoko Fukuda (Data, Events)

Magdalena Osumi (Renewables & Storage)

Filippo Pedretti (Thermal, CCS, Nuclear)

Tetsuji Tomita (Power Market, Hydrogen)

Aglaé Bange (Renewables and Biomass)

George Hoffman (Sales, Business Development)

Tim Young (Design)

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com. For all other inquiries, write to info@japan-nrg.com

NEWS: GENERAL OUTLOOK AND TRENDS

Govt to accelerate energy conservation and transition to non-fossil energy

(Government statement, June 26)

- ANRE proposed measures to accelerate energy conservation and transition to non-fossil energy in response to energy security risks.

- The govt will expand support for high-efficiency industrial equipment while strengthening energy efficiency regulations through stricter standards, revised benchmarking, and enhanced oversight of underperforming businesses.

- For transition to non-fossil energy, electrification and fuel switching will be accelerated by supporting hydrogen-ready equipment, heat pumps, energy management systems (EMS), and onsite solar power.

- To help SMEs save energy, the govt will expand energy audits, strengthen cooperation with regional financial institutions, and promote supply-chain partnerships.

- For households, the govt will promote high-efficiency appliances and energy-efficient homes through financial support, awareness campaigns, and new building standards.

- TAKEAWAY: As the global energy supply becomes more unstable due to geopolitical confrontation, Japan must reduce dependence on imported fossil fuels. Energy policy should go beyond conventional energy conservation and promote electrification, renewable energy use, and fuel switching as part of a structural transformation. These policies must address practical challenges, such as cost burdens, labor and skill shortages, technical constraints, and slow progress by some firms.

Daiki Axis and Morgenrot launch renewables-powered AI data center business

(Company statement, June 30)

- Daiki Axis Sustainable Power, Mirait One and GPU cloud provider Morgenrot launched a renewable energy-powered data center business.

- Daiki Axis opened two facilities in Ehime and Chiba Prefs, powered primarily by on-site solar generation.

- The firms aim to expand beyond the initial two locations to provide low-carbon computing capacity for AI, cloud, GX, government, and corporate customers.

- TAKEAWAY: The Chiba facility is significant because the prefecture is emerging as one of Japan’s key AI and hyperscale data center clusters due to its proximity to Tokyo, and strong power and communications infrastructure. New AI data centers are expected to become major sources of electricity demand, increasing the need for grid upgrades, renewable power procurement and flexible power resources. By pairing AI computing with on-site solar generation, the project reflects a broader trend toward locating DCs alongside clean electricity sources to help manage rising power demand. Please see this issue’s Analysis section for more on this topic.

NEWS: ELECTRICITY MARKETS

OCCTO publishes draft demand curve for capacity market main auction

(Agency statement, June 30)

- OCCTO published the draft demand curve for the FY2026 capacity market main auction (delivery year: FY2030).

- The forecasted nationwide highest demand for FY2030 is 161.9 GW, an increase of about 0.11 GW from the previous estimate.

- The reference price (Net CONE – Cost of New Entry) is calculated at ¥20,911/ kW, reflecting updated generation cost assumptions and inflation.

- The price cap of the demand curve is 1.5 times the Net CONE, or ¥31,366.5/ kW.

- The proposed demand curve for FY2026 is based on:

- Target procurement volume: 196.91 GW;

- Procurement volume at the price cap: 195.27 GW;

- Procurement volume at zero price: 203.90 GW;

- About 28.51 GW of supply capacity, including expected capacity from FIT-supported generation and contracted capacity from the LTDA (Long-term Decarbonized Power Sources Auction) will be added during the auction clearing process (excluding post-auction adjustments).

- In addition, as capacity is no longer reserved for the additional auction, the full procurement requirement for FY2030 will be secured through the main auction.

- CONTEXT: In the capacity market, the demand curve defines the relation between the volume of capacity procured and the clearing price. It shows how much capacity should be procured at different price levels to ensure reliable electricity supply.

- TAKEAWAY: The most important changes in the FY2026 main auction are the major increase in target procurement volume and Net CONE. The revisions should strengthen capacity procurement for FY2030 while raising the maximum capacity market price.

ANRE proposes market design options for mid- to long-term trading

(Government statement, June 25)

- ANRE proposed market design options for new mid- to long-term trading, focusing on tradable products, bidding/ contract mechanisms, and market scope.

- The market will initially offer one-year products traded three years and one year ahead of delivery, with base-load products as the core offering and middle-load products introduced for shorter-term trading.

- Both fuel-cost-adjusted and fixed-price products are being considered to meet different market participants’ hedging and pricing needs, using standardized adjustment formulas to ensure transparency.

- Continuous trading (order matching) will be the main trading mechanism, complemented by flexible bidding rules and possible auction-based trading to improve market liquidity and establish reliable long-term price benchmarks.

- The proposal also examines how to define the market scope (nationwide, regional, or area-based) and how to manage market congestion risks through appropriate settlement mechanisms and reference price areas.

- CONTEXT: The mid- to long-term electricity market is a new wholesale market where electricity can be traded one and three years ahead of delivery. It is designed to improve long-term price transparency, increase market liquidity, and support retailers in securing future electricity supply.

- TAKEAWAY: The design of the mid- to long-term electricity market has moved from the conceptual stage to detailed system design. While the basic market framework has now been outlined, its effectiveness will largely depend on the supply rules and market operation mechanisms to be developed. Without sufficient trading volume and robust market surveillance, it will be difficult to establish the market as a reliable price benchmark.

- SIDE DEVELOPMENT:

- Govt presents phase-1 business design for simultaneous market

- (Government statement, June 29)

- ANRE and OCCTO presented their plan for the first phase of a detailed business design for the proposed simultaneous electricity market.

- The first phase will combine stakeholder interviews, technical validation, institutional design, and reviews of overseas market practices.

- Research will use the North American ERCOT market as a reference model to conduct simulations, assessing whether a market-clearing system tailored to Japan’s regulatory framework and grid conditions can be implemented.

- The study group work is organized into 11 topic areas, including market scheduling, bidding and market substitution, operational constraints, scheduling and automation, congestion and TSO interventions, settlement and balancing services, distributed energy resources (DERs), pumped storage and batteries, and system integration.

- CONTEXT: On June 22, a new Working Group on Business Design and Technical Studies for the Simultaneous Market was established. It comprises experts, market participants, and system vendors. It will develop the market design and assess the technical feasibility of a cooptimized market system based on overseas case studies and stakeholder consultations. Meetings are private due to the inclusion of commercially sensitive information.

- TAKEAWAY: The simultaneous market has moved from conceptual discussions to detailed business and operational design, like the mid- to long-term market. The balancing market design was revised on March 14 by moving the transaction timing of the products (Primary, Secondary-1 & 2, Tertiary-1, and Composite) from weekly auctions to day-ahead trading and shortening the bidding interval from three hours to 30 minutes. This is part of the preparations for integration with the JEPX wholesale electricity market. Although new transactions in the balancing market began only about three months ago, the findings from this review will likely be useful in designing the simultaneous market.

NEWS: HYDROGEN

PM Takaichi backs India green ammonia project aimed at Japan buyers

(Nikkei, June 29)

- PM Takaichi backed Japanese and Indian private-sector plans to produce hydrogen and green ammonia during her visit to India to meet with counterpart PM Modi.

- The main project is the partnership between IHI and India’s ACME Group, expected to need ¥480 billion in investment. The latter aims to produce around 400,000 tons/ year of ammonia using hydrogen made by electrolysis from solar power.

- The ammonia will be exported to Japan. Potential buyers include Hokkaido Electric as a co-firing fuel for coal-fired power; Sumitomo Chemical and Mitsubishi Gas Chemical as chemical feedstock; and UBE for semiconductor cleaning fluids.

- This week, the Japanese govt certified the project for support under the Hydrogen Society Promotion Act under the CfD mechanism. These subsidies cover 15 years of the difference in price between renewable ammonia and existing fuels or feedstocks.

- CONTEXT: Japan’s latest public-private investment roadmap calls for ¥6.2 trillion in funding to develop hydrogen and ammonia power by FY2040.

- TAKEAWAY: Under its CfD-style support program for hydrogen and related fuels, Japan already approved blue ammonia imports from the U.S. Now, India is set to become the second major production geography for Japan-backed low-carbon ammonia imports, reflecting its potential as a low-cost green hydrogen/ammonia producer outside China, thanks to large-scale renewables development. The Japan-India energy partnership has expanded across both clean and traditional fuels over the past decade, and the latest project fits Japan’s effort to reduce strategic dependence on Middle Eastern energy imports. But it should also be read as a longer-term attempt to build Indo-Pacific supply chains with trusted partners to counter geopolitical and business competitor, Beijing.

- SIDE DEVELOPMENT:

- MHI study shows cost reduction potential for green H2 and ammonia from India

- (Company statement, June 26)

- An MHI study assessed the economic viability of exporting green hydrogen and green ammonia produced in India for use in Singapore.

- The study, which aims to develop a regional green hydrogen and ammonia value chain, found that coordinated operations and optimized infrastructure could foster significant cost reductions.

- CONTEXT: METI supports projects in Global South countries that help growth industries by enabling Japanese and local companies to leverage their strengths to build resilient supply chains and advance carbon neutrality.

- TAKEAWAY: The study shows that integrated optimization of production, logistics, and operations can improve the economics of green hydrogen and ammonia exports. The findings strengthen the business case for cross-border green fuel projects linking low-cost production hubs such as India with demand centers like Singapore. In fact, on June 30, the supply of green ammonia to Japan, planned by India’s ACME Group and IHI, was certified as a CfD project under the Hydrogen Society Promotion Act. Low-carbon fuels from India are expected to play an increasingly important role going forward.

- SIDE DEVELOPMENT:

- ANRE announces new CfD-certified project under Hydrogen Society Promotion Act

- (Government statement, June 30)

- On June 30, ANRE announced a new CfD-certified project to supply low-carbon ammonia under the Hydrogen Society Promotion Act.

- The certified firms are IHI, Mitsubishi Gas Chemical, Hokkaido Electric, Nippon Beet Sugar Manufacturing, Kobelco Power Kobe, Sumitomo Chemical, and UBE.

- The annual supply volume of low-carbon ammonia during the subsidy period is 228,000 tons (hydrogen equivalent: 35,419 tons).

- The project will run from Sept 2030 to Aug 2055.

- CONTEXT: Prior to this announcement, three hydrogen CfD projects, three ammonia CfD projects, and two ammonia hub development projects had been certified.

MGC, Gold Hydrogen ink MoU to study green methanol via natural H2 in Australia

(Company statement, June 29)

- Mitsubishi Gas Chemical and Gold Hydrogen (Australia) inked an MoU to assess the feasibility of producing green methanol using natural hydrogen in South Australia.

- MGC invested in Gold Hydrogen in July 2025. By combining natural hydrogen with renewable energy, the firms aim to develop a zero-emission green methanol supply.

- CONTEXT: Gold Hydrogen is a startup developing the Ramsay Project to explore and commercialize natural hydrogen and helium resources. Drilling in the Yorke Peninsula confirmed high-purity natural hydrogen, helium, and helium-3.

- CONTEXT: Natural hydrogen is generated underground and may offer lower production emissions than manufactured hydrogen, depending on extraction and processing.

- TAKEAWAY: Most natural hydrogen projects focus on resource exploration and hydrogen production; the MGC– Gold Hydrogen project stands out by integrating downstream green methanol production from the outset. It targets a higher-value, exportable product rather than just hydrogen alone. This integrated approach could accelerate commercialization and position South Australia as a leading hub for natural hydrogen-based green fuels.

Mitsubishi Shipbuilding wins order for ammonia fuel handling system

(Company statement, June 26)

- Mitsubishi Shipbuilding received an order from Hitachi Zosen Marine Engine (HZME) for its ammonia fuel handling system,

- The system is compatible with ammonia engines from both Everllence SE and WinGD, supporting HZME’s dual-license production, and will be used to conduct shop tests of ammonia-fueled marine engines.

- CONTEXT: Everllence SE (Germany) and WinGD (Switzerland) are two of the world’s leading marine engine licensors, providing advanced engine designs for commercial vessels, including next-gen ammonia-fueled engines.

- TAKEAWAY: As the shipping industry accelerates decarbonization under International Maritime Organization targets, ammonia is expected to play a key role as a zero-CO2 marine fuel. Mitsubishi Shipbuilding secured an early position in the emerging ammonia-fueled vessel market by supplying a fuel handling system compatible with major marine engine platforms. As ammonia engine development accelerates, demand for safe onboard fuel supply and handling systems is expected to grow alongside engine adoption.

IHI completes verification of ammonia single-firing burner for thermal power

(Company statement, June 29)

- IHI developed an ammonia single-firing burner for thermal power plant boilers and completed technical verifications for practical application.

- The development builds on a prior demo of 20% ammonia co-firing at JERA’s Hekinan Thermal Power Station Unit 4.

- It aims to enable staged decarbonization toward 100% ammonia firing while minimizing modifications to existing boiler systems.

- CONTEXT: IHI developed the ammonia single-firing burner to gradually increase the ammonia co-firing ratio while minimizing modifications to existing boiler facilities, with the goal of achieving 100% ammonia firing. In 2022, IHI showed stable 100% ammonia combustion using a small-scale combustion test facility.

- TAKEAWAY: The technology’s successful commercialization could boost decarbonization of existing thermal power plants by reducing the need for complete boiler replacement and lowering transition costs. The test supports Japan’s staged ammonia-combustion pathway, but commercial adoption will still depend on boiler integration, NOx control, fuel cost and low-carbon ammonia supply.

JERA signs MoU with EGAT for hydrogen/ ammonia value chain in Thailand

(Company statement, June 30)

- JERA signed an MoU with Thailand’s state-owned utility, EGAT, to explore development of hydrogen and ammonia value chains in Thailand.

- The partnership will assess market opportunities, and the use of hydrogen and ammonia for power generation in Thailand.

- CONTEXT: JERA and EGAT began cooperation in 2015 on LNG fuel procurement, infrastructure, and power generation. In 2022 and 2023, JERA expanded its collaboration with EGCO (Electricity Generating Public Co), partially owned by EGAT to explore hydrogen, ammonia, and CCUS projects.

- TAKEAWAY: The MoU represents JERA’s transition from project-based collaboration to supporting Thailand’s nationwide hydrogen and ammonia value chain. By partnering with EGAT, JERA strengthens its role in Thailand’s energy transition. If commercial projects are realized, the partnership could establish Thailand as a leading hydrogen and ammonia market in SE Asia while expanding regional low-carbon fuel supply chains and creating new opportunities for Japanese companies across ASEAN.

NEWS: SOLAR AND BATTERIES

OCCTO announced the results of first FY2026 PV capacity auction

(Government statement, June 22)

- OCCTO announced the results of FY2026’s first utility-scale solar FIP auction, which was about 1.5 times oversubscribed.

- The 28th solar auction attracted 33 bids for a total 135 MW capacity, with 30 projects awarded the full 91 MW of available capacity.

- The weighted average successful bid price was ¥6.74/ kWh, while the highest winning bid reached ¥7.89/ kWh; the lowest successful bid was ¥0.00/ kWh.

- KA Solar and HEXA led with seven and four winning bids, respectively.

- TAKEAWAY: These results are positive for the solar industry with evidence of continued cost declines. This auction may also reflect developers rushing viable projects under current rules since FIP support for large-scale (“mega”) solar projects will stop in FY2027. In recent years, the auction has frequently been undersubscribed. This time, there were 135 MW of bids chasing 91 MW of available capacity.

Results of the 28th solar capacity auction:

| Company name (JP) | Company name (English) | Winning price (¥/ kWh) | Awarded capacity (kW) |

| 地域電力株式会社 | HEXA Renewables | 0.00 | 1,999 |

| 地域電力株式会社 | HEXA Renewables | 0.00 | 600 |

| 地域電力株式会社 | HEXA Renewables | 0.00 | 400 |

| 地域電力株式会社 | HEXA Renewables | 0.00 | 800 |

| GVSJ20 合同会社 (SPC) | Greenvolt Solar Japan GVSJ20 | 0.00 | 1,125 |

| GVSJ11 合同会社 (SPC) | Greenvolt Solar Japan GVSJ11 | 0.00 | 750 |

| UNIVERGY 株式会社 | UNIVERGY | 0.00 | 750 |

| GVSJ04 合同会社 (SPC) | Greenvolt Solar Japan GVSJ04 | 0.00 | 625 |

| MIRARTH エナジーソリューションズ | MIRARTH Energy Solutions | 5.00 | 1,100 |

| エンブルー | EnBlue | 5.30 | 1,990 |

| エンブルー | EnBlue | 5.30 | 875 |

| エンブルー | EnBlue | 5.30 | 500 |

| WAKO | WAKO | 5.49 | 600 |

| WAKO | WAKO | 5.49 | 400 |

| WAKO | WAKO | 5.49 | 350 |

| 大和ハウス工業 | Daiwa House Industry | 6.49 | 499 |

| シリウス・ソーラー・ジャパン 55 合同会社 (SPC) | Sirius Solar Japan 55 (Trina Solar) | 6.50 | 19,950 |

| リニューアブルエナジーデベロップメント合同会社 (SPC) | Renewable Energy Development (NCS RE Capital) | 6.50 | 1,000 |

| リニューアブルエナジーデベロップメント合同会社 (SPC) | Renewable Energy Development (NCS RE Capital) | 7.20 | 1,999 |

| リニューアブルエナジーデベロップメント合同会社 (SPC) | Renewable Energy Development (NCS RE Capital) | 7.20 | 750 |

| 株式会社町おこしエネルギー | Machiokoshi Energy | 7.77 | 9,999 |

| 八ヶ岳太陽光発電所合同会社 (SPC) | Yatsugatake Solar Power Plant | 7.87 | 29,500 |

| KA Solar 合同会社 (SPC) | KA Solar | 7.88 | 1,990 |

| KA Solar 合同会社 | KA Solar | 7.88 | 1,725.7 |

| ES 太陽光さくら合同会社 (SPC) | ES Solar Sakura | 7.88 | 999 |

| KA Solar 合同会社 | KA Solar | 7.89 | 1,990 |

| KA Solar 合同会社 | KA Solar | 7.89 | 1,990 |

| KA Solar 合同会社 | KA Solar | 7.89 | 1,990 |

| KA Solar 合同会社 | KA Solar | 7.89 | 1,990 |

| KA Solar 合同会社 | KA Solar | 7.89 | 1,764.3 |

Toyota Tsusho expands Tunisia solar portfolio with 100 MW IPP project

(Company statement, July 1)

- Toyota Tsusho will join a 100 MW solar independent power producer (IPP) project in Sidi Bouzid Governorate, Tunisia, through its renewables subsidiary AEOLUS.

- The project will be developed with Norwegian renewables company Scatec, which will co-own, build and operate the solar plant.

- Commercial operations will begin in the first half of 2027; electricity will be sold to Tunisia’s state utility, STEG, under a 25-year PPA.

- The project marks Toyota Tsusho Group’s third solar IPP in Tunisia and will increase its total solar generation capacity in the country to 200 MW.

- The project has financing from the EBRD and the EIB, along with EU guarantees and grants, and support under Japan’s JCM scheme.

- CONTEXT: Tunisia relies heavily on imported fossil fuels but aims to increase the share of renewables to 35% of the national power mix by 2030. Toyota Tsusho targets expansion of its renewables portfolio in Africa from 1 GW to 3 GW by 2030.

- TAKEAWAY: Africa installed 4.5 GW of new solar capacity in 2025, according to the New Global Solar Council, a trend expected to support BESS deployment and create new business opportunities for Japanese companies. Toyota Tsusho’s expansion into Africa’s renewables market is a long-term effort tied to the company’s “With Africa For Africa” policy in order to take advantage of the continent’s positive demographic and economic growth trends.

- SIDE DEVELOPMENT:

- Toyota Tsusho to build 50 MW BESS in West Africa

- (Company statement, June 25)

- Toyota Tsusho won an order from Benin’s electricity company to install a 50 MW / 160 MWh BESS in Pobè state.

- The facility, scheduled for completion by 2027, will be installed alongside a 25 MW solar power plant, built by Toyota Tsusho in 2023.

- TAKEAWAY: Benin aims for renewables to account for 31% of its national energy mix by 2030, with a particular focus on rural areas, where electrification rates remain lower. Nationwide, around 40% of households have access to electricity.

ENEOS to repower solar PVs in Wakayama

(Company statement, June 24)

- ENEOS Renewable Energy began repowering the 16.8 MW Hidakagawa solar power plant (Wakayama Pref).

- The PVs will either be recycled or reused where possible. Other components will also be treated to avoid landfill disposal.

- TAKEAWAY: With the volume of end-of-life solar equipment expected to reach 500,000 to 800,000 tons annually by the 2030s, companies have already begun expanding services to include recycling. With a considerable number of solar power plants now halfway through FIT, such as this plant commissioned in 2016, repowering is expected to become increasingly common. Repowering projects also involve replacing inverters and power conditioning systems, in addition to PV modules.

FPS inks virtual PPA with Konica Minolta for solar environmental attributes

(Company statement, July 1)

- FPS signed a long-term virtual PPA with Konica Minolta to supply the environmental attributes of solar power.

- FPS will provide non-FIT, non-fossil certificates equivalent to about 1 GWh/ year, helping Konica Minolta reduce its Scope 2 emissions.

- FPS will aggregate the environmental value associated with surplus electricity generated by solar plants after on-site self-consumption, while the physical electricity continues to be sold separately. • TAKEAWAY: The deal reflects the expanding use of virtual PPAs in Japan, where companies increasingly procure renewable energy attributes separately from electricity supply. The model offers a flexible pathway for reducing Scope 2 emissions while supporting the financing and expansion of new renewables projects.

Sustech inks PPA for rooftop PV at Taipei Port

(Company statement, July 1)

- Climate tech startup Sustech inked a long-term corporate CPPA to supply renewable electricity from a 3.7 MW rooftop solar project at Taipei Port in Taiwan.

- The project, Sustech’s first abroad, begins operations in 2029.

- Sustech will develop, own and operate the solar system using its AI-based energy management platform ELIC.

- While the project is small, Sustech plans to expand rooftop PV deployment at ports across Taiwan and other Asian markets.

- TAKEAWAY: The project shows how Japanese clean energy developers are exporting their expertise by combining renewable energy, AI-powered energy management and innovative financing. It also highlights growing demand for corporate PPAs in Taiwan as ports and other industrial facilities seek to decarbonize operations.

EneCoat’s PSC generates power in space demo

(Company statement, July 2)

- EneCoat Technologies said its flexible PSC successfully generated electricity in space during an on-orbit demo aboard the OrigamiSat-2 microsatellite that was launched from New Zealand in April.

- The satellite measured the voltage of EneCoat’s PSC in orbit on June 6.

- CONTEXT: The Institute of Science Tokyo and Japan Aerospace Exploration Agency (JAXA) collaborated on this demo. EneCoat is a Kyoto University spin-off developing PSCs for indoor IoT applications and outdoor renewables systems.

- TAKEAWAY: The successful test demonstrates the potential of PSCs for space applications, where reducing satellite mass and enabling deployable structures are vital. The milestone also supports efforts to commercialize PSC tech for use on Earth. The test is an early validation step, but longer-duration data will be needed to assess durability and performance in orbit.

Hokkaido Gas receives subsidy for energy management system for households

(Company statement, June 26)

- Hokkaido Gas’s HEMS platforms, “EMINEL Smart” and “EMINEL”, were selected for an MoE subsidy under the CO2 emission control project promotion program.

- The platforms use household sensors with residential solar PV and BESS to automatically control air conditioning and heating systems through DR, improving energy efficiency.

- Currently available in Hokkaido, the services will expand to other cold regions of Japan, such as Tohoku and Hokuriku.

- SIDE DEVELOPMENT:

- NTT to conduct a remote device control demo

- (Company statement, June 25)

- NTT Anode Energy, Panasonic Electric Works, Osaki Electric, and ACCESS will conduct a demo of the smart meter platform IoG®.

- Through HEMS (Home Energy Management Systems), the platform can remotely control customer devices – including water heaters, EV chargers, and residential solar power systems – without requiring a router.

- TAKEAWAY: This device, more adaptable and suitable for installation in a wider variety of homes, aims to support the expansion of renewable energy and energy-saving measures.

Koshidaka and partners sign low voltage solar PPA

(Company statement, July 1)

- Kakuichi, Updater and Koshidaka signed a PPA for low-voltage solar installations (4.95–9.9 kW) on container and garage roofs.

- Starting August, 41 karaoke clubs operated by Koshidaka will procure solar electricity or associated environmental value equivalent to their consumption.

- Kakuichi’s tracking system, “ENECTION 2.0”, ensures traceability by issuing tokens representing electricity matched to the amount consumed by the clubs; this ensures a match between consumption and generation from dispersed solar installations.

- TAKEAWAY: This agreement offers several advantages. On the one hand, it avoids local opposition by using existing rooftops instead of developing new solar sites. And it secures local support by providing property owners with an additional source of income through roof lease agreements.

NTT Data to enter balancing market using data center backup batteries

(Company statement, June 25)

- NTT Data plans to become the first data center operator to participate in Japan’s electricity balancing market starting FY2027, using uninterruptible power supply (UPS) systems to provide grid balancing services.

- The firm aims to secure up to 50 MW of balancing capacity by 2030, helping stabilize the grid by discharging stored electricity during periods of tight supply and recharging when demand is low.

- To develop the tech and infrastructure, NTT Data will work with 4R Energy, the EV battery reuse JV between Nissan Motor and Sumitomo Corp. The UPS systems will incorporate second-life EV batteries.

- TAKEAWAY: The initiative reflects a trend to turn data centers from electricity consumers into active grid assets. As growth in AI fuels rapid growth in power demand, leveraging existing backup batteries for balancing services could create new revenue streams for DC operators while improving grid flexibility. It will also complement dedicated battery storage.

Toshiba wins order for inverters in Shimane Pref

(Company statement, June 29)

- Toshiba won an order from Chugoku Electric for a 4 MW grid-forming inverter.

- The inverters will be installed in eight power conditioners on the Oki Islands (Shimane Pref), a remote area.

- CONTEXT: A grid-forming inverter (GFM) is a power converter for renewable energy that can operate as an independent AC voltage source; conventional grid-following inverters rely on an existing grid voltage reference. GFM inverters help maintain grid stability by regulating voltage and frequency, reducing the risk of outages, and can continue supplying electricity during grid disturbances or disasters.

Plugo raises ¥300 million for EV charging

(Company statement, June 26)

- Plugo raised ¥300 million through a third-party allotment of shares, bringing its total funding to ¥3.2 billion.

- New shares were subscribed to by JICN (Japan Green Investment Corp for Carbon Neutrality), an MoE-affiliated public-private fund.

- This latest fundraising will help Plugo to accelerate development of its EV charging services and expand partnerships with OEMs (Original Equipment Manufacturers) in the automotive industry.

- CONTEXT: METI targets installation of 300,000 EV chargers nationwide by 2030. Plugo offers EV charging services with automotive partners and software to remotely control chargers.

- SIDE DEVELOPMENT:

- Nitto Kogyo launches service for faster charging

- (Company statement, July 1)

- Nitto Kogyo launched the Pit-2G series of 9.6 kW EV chargers, certified by the Japan Automobile Research Institute.

- For compatible EVs and Plug-in Hybrid Electric Vehicles, the charger provides about 67 km of range from one hour of charging, compared with 21 km for a 3 kW charger.

- CONTEXT: Currently, many vehicles are not compatible with 9.6 kW chargers. However, as battery capacities increase, compatibility is expected to expand, including among taxis and trucks.

DOWA develops process to recover nickel and cobalt sulfates from spent EV batteries

(Company statement, June 30)

- DOWA Eco-System developed a recycling process to recover nickel and cobalt sulfates from spent Liion batteries.

- It began demo trials to supply the materials directly to cathode manufacturers for performance evaluation.

- The new process complements the firm’s existing lithium carbonate recovery tech, enabling recovery of the three key battery metals – lithium, nickel and cobalt – from recycled battery “black mass.”

- CONTEXT: The firm is an environmental and recycling arm of DOWA Holdings, one of Japan’s largest non-ferrous metals and resource recycling groups.

- TAKEAWAY: Japan seeks to build a closed-loop battery materials supply chain by producing battery-grade nickel and cobalt chemicals from recycled batteries rather than relying on imported mined metals. As EV battery waste grows and regulations tighten, direct supply of recycled materials to cathode manufacturers could improve resource security while reducing the environmental footprint of battery production.

NEWS: WIND POWER AND OTHER RENEWABLES

Kyushu launches offshore wind partnership to strengthen regional supply chain

(Government statement, June 24)

- METI, the Kyushu Economic Federation and the GX Acceleration Agency set up the Kyushu Offshore Wind Industry Promotion Partnership.

- It will accelerate development of an offshore wind industrial cluster by strengthening domestic supply chains, attracting manufacturers and suppliers, improving port infrastructure and developing a skilled workforce.

- It will coordinate regional efforts to build a nationwide offshore wind supply chain.

- CONTEXT: Kyushu hosts major offshore wind assets, including Hibikinada Offshore Wind Farm and Japan’s first commercial floating offshore wind project off Goto.

- The initiative will also seek to leverage local shipbuilding and steel industries to support production of foundations and other offshore wind components.

- TAKEAWAY: This partnership reflects Japan’s focus on building a domestic offshore wind manufacturing base rather than relying on imported equipment. Kyushu is keen to position itself as the country’s leading offshore wind hub and to serve as a manufacturing and logistics gateway for the broader East Asian market.

Vestas completes assessment for turbines for offshore wind project

(Company statement, July 1)

- Vestas completed the conformity assessment for its V236-15 MW offshore wind turbine for the OgaKatagami-Akita project in Akita Pref.

- The certification marks a major regulatory milestone ahead of construction.

- The project is the first fixed-bottom offshore wind project in Japan’s general sea area to complete the assessment process, and the first domestic project using turbines larger than 10 MW to receive approval.

- The review validated the Japan-specific design, including enhanced seismic resistance, typhoon-hardened nacelle and spinner cover, and improved winter lightning protection.

- TAKEAWAY: The approval highlights one of the biggest engineering hurdles facing offshore wind in Japan: designing turbines that can withstand earthquakes, typhoons and complex seabed conditions. Unlike Europe’s North Sea, where offshore wind standards were largely developed, projects in Japan must satisfy additional domestic certification requirements that assess seismic loading, extreme typhoon winds, wave conditions and soil behavior. This often requires reinforced towers, foundations and support structures tailored to local conditions rather than simply importing standard turbine designs.

- SIDE DEVELOPMENT:

- Arup facilitates certification for offshore wind project

- (Company statement, July 1)

- Engineering consultancy Arup said it supported certification of the offshore wind project off Oga, Katagami and Akita in Akita Pref.

- The conformity certificate was issued June 30 by Bureau Veritas Japan.

- Arup provided technical verification and coordination among stakeholders, including site assessment, design criteria, load analysis and structural evaluation.

- CONTEXT: This is the world’s first 15 MW-class offshore wind project designed with earthquake loading incorporated into the turbine and support structure design.

- TAKEAWAY: The project establishes a new engineering benchmark for offshore wind in seismic regions. Successfully integrating earthquake-resistant design into a 15 MW-class turbine could provide a model for future projects in Japan and other earthquake-prone markets, where, for instance, European offshore wind designs are not sufficient.

Sumitomo sells stakes in three Belgian offshore wind farms

(Company statement, July 3)

- Sumitomo is divesting its interests in three Belgian offshore wind projects – Northwind, Nobelwind, and Northwester2 – as part of a strategy to recycle capital into higher-growth businesses.

- The firm’s stakes in Nobelwind and Northwester2 will go to existing shareholder JERA Nex bp; while the Northwind stake will be sold to Belgian investment consortium Publiwind.

- CONTEXT: The divestment aligns with the firm’s 2026 plan, under which proceeds from mature assets will go to new opportunities. Sumitomo also recently launched its offshore wind project in France. • TAKEAWAY: The sale reflects a common strategy among major infrastructure investors: monetizing mature, operating renewables assets to free up capital for new developments. The move allows Sumitomo to recycle capital while maintaining its focus on expanding its renewable energy portfolio in Europe.

J-Power partners with Kitakyushu on offshore wind environmental credits

(Company & Government statement, June 24)

- J-Power entered into a contract with Kitakyushu City to act as an agent for the procurement of tracked FIT non-fossil fuel certificates generated by the Kitakyushu Hibikinada Offshore Wind Farm.

- CONTEXT: The certificates are environmental attributes of renewable power, and include tracking information such as the power plant name, generation source, location and commissioning date.

- Kitakyushu Hibikinada Offshore Wind Farm, Japan’s largest operating offshore wind farm, began commercial operation in March.

- It generates 500 GWh of electricity annually. J-Power is an investor in the consortium operating the plant.

- TAKEAWAY: The deal highlights a trend in Japan toward local consumption of renewable energy certificates, allowing municipalities to claim the environmental benefits of renewable power generated within their own regions. It also shows how offshore wind projects can support regional decarbonization strategies and corporate or municipal carbon accounting.

Cosmo Eco Power, NSK validate bearing monitoring tech for wind turbines

(Company statement, July 1)

- Cosmo Eco Power and bearing producer NSK completed the first field test of bearing lubrication monitoring tech for wind turbines.

- The tech can detect changes in lubrication earlier than conventional vibration-based monitoring methods, improving turbine reliability and lower O&M costs.

- TAKEAWAY: The test reflects a shift in Japan’s wind sector from reactive and scheduled maintenance to predictive maintenance, as operators seek to maximize turbine availability and reduce O&M costs amid larger turbines, harsher operating environments and growing pressure to improve project economics. The tech should help improve the long-term operational stability of wind farms.

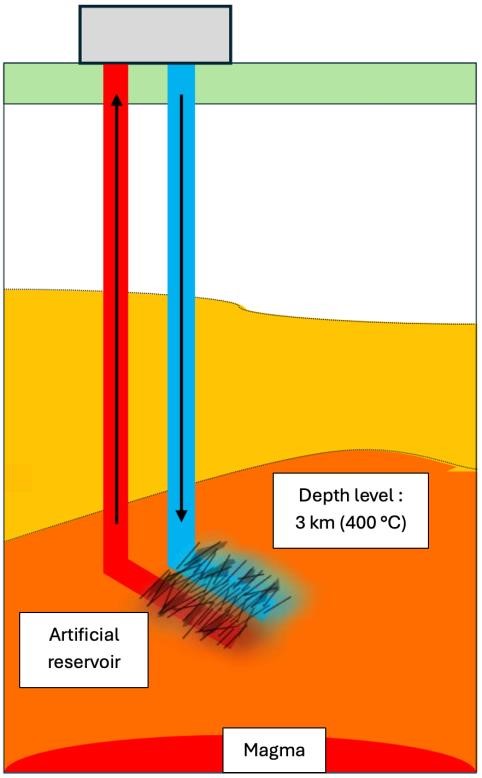

Idemitsu Kosan invests in next-gen geothermal energy in the U.S.

(Company statement, June 25)

- Idemitsu Kosan invested in U.S.-based Quaise Energy, which is developing millimeter-wave drilling technology.

- CONTEXT: Millimeter-wave drilling is a next-gen geothermal technology that excavates rock by irradiating it with high-frequency electromagnetic waves, heating and melting the rock instead of mechanically drilling it. It enables drilling to depths of up to 20 km, with temperatures of 300–500°C.

- Idemitsu is also considering participating in Quaise Energy’s Project Obsidian, a 250 MW geothermal power plant in Oregon, U.S. expected to begin operations in 2030.

- TAKEAWAY: Millimeter-wave drilling is a nascent technology. Beyond its potential to unlock high-power generation from superhot rock resources, it could also significantly reduce the cost of deep geothermal drilling. Kyoto Fusioneering was awarded ¥500 million by NEDO to develop a gyrotron (a vacuum electron tube that generates millimeter waves) to accelerate deep geothermal drilling.

Chubu Electric receives METI grant for hydropower facility upgrades

(Government statement, June 26)

- METI selected Chubu Electric for a FY2026 subsidy to upgrade the operation of pumped-storage hydropower facilities.

- The award, made under a second application round, covers operational enhancement projects at the 340 MW Takane No 1 and 1.5 GW Oku Mino pumped-storage hydropower plants, both in Gifu Pref.

- The subsidy supports investments to improve operational flexibility, expand revenue opportunities and reduce operating costs at existing pumped-storage facilities.

NEWS: NUCLEAR ENERGY

NRA reveals Chubu Electric continued falsifying earthquake data at Hamaoka NPP

(Nikkei, July 1)

- The NRA revealed that Chubu Electric continued falsifying earthquake data at Hamaoka NPP, even after the NRA began an investigation in May 2025.

- Of the 225 earthquake data cases, 69 were rewritten after the investigation started. The company manipulated the selection process to make it appear correct.

- The standard procedure requires a random generation of 20 seismic wave patterns per case and then selecting the one closest to the average. Chubu Electric, however, ordered contractors to calculate up to 1,000 patterns (and in some cases as many as 30,000), and then selected favorable options.

- The NRA is considering penalties for failing the safety review for Units 3 and 4. Chubu Electric issued an apology.

- TAKEAWAY: For more information, please see this issue’s Analysis section.

Kyushu Electric applies for long-term facility management for Genkai NPP Unit 4

(Company statement, July 2)

- Kyushu Electric applied to the NRA for approval of its “Long-term Facility Management Plan” for Genkai NPP Unit 4.

- The unit will reach 30 years of operation on July 25, 2027.

- CONTEXT: The Reactor Regulation Act makes such a plan mandatory for operating reactors beyond the 30-year mark. Utilities have to renew the plan every 10 years.

- SIDE DEVELOPMENT:

- Kyushu Electric begins regular inspection at Genkai Unit 3

- (Company statement, Japan NRG, June 30)

- Kyushu Electric began a regular inspection of Genkai NPP Unit 3. Normal operations will resume on Nov 25.

- During inspection, the reactor safety sequence panel will be updated, and some of the 193 fuel assemblies will also be replaced.

- The reactor (1.18 GW) restarts on Oct 27, with power generation resuming on Oct 29.

- CONTEXT: In November, Genkai NPP Unit 4 will enter regular inspection. Sendai NPP Unit 1 begins inspection in Feb 2027, and Sendai NPP Unit 2 in May 2027.

NEWS: TRADITIONAL FUELS

Crude oil from U.S. increases while total imports fell in May

(Government statement, June 30)

- METI reported May crude oil imports of 7.29 million kiloliters, a 38.4% YoY decrease. But imports of U.S. crude rose 74.8% YoY to 1.63 million kiloliters, five times April imports. There were also 120,000 kiloliters of Russian crude imports.

- Middle Eastern imports came in at roughly 5.38 million kiloliters, a 50% drop YoY.

- In May, the govt secured alternative supplies to the Hormuz routes to meet 65% of typical crude volumes. It expects to cover 100% of normal volumes by July.

- Naphtha production and domestic sales dropped YoY, but naphtha inventories rose.

- SIDE DEVELOPMENT:

- METI to increase subsidies to oil distributors, naphtha sales fell 18.8% YoY

- (Japan NRG, July 3)

- Procuring crude oil outside of the Hormuz route is much more expensive and requires longer shipping times, driving up base costs.

- National oil reserves that previously offset such costs are depleting. So, METI is increasing subsidies to oil distributors to factor in alternative procurement costs. This should stabilize regular gasoline prices at about ¥170/liter for consumers.

- METI reports a ¥380 billion subsidy fund balance as of end-June, with May payouts at ¥290 billion. It expects the June payout to be lower as falling crude prices reduce subsidy amounts.

- JAPEX is halting new investments in the Persian Gulf, instead focusing on regions with strong infrastructure, such as SE Asia, the U.S., and Norway.

- In May, naphtha sales fell 18.8% YoY, and operations at ethylene production facilities dropped to historic lows due to scheduled maintenance.

JERA sets up new subsidiary to manage LNG imports

(Company statement, July 1)

- JERA set up JERA Global Energy Solutions (JERA GES), a wholly owned subsidiary headquartered in Singapore.

- JERA GES will manage long-term LNG imports, upstream investments and shipping portfolio, as well as manage hydrogen and ammonia procurement.

- It will focus on long-term portfolio strategy with JERA Global Markets (JERAGM), which handles short-term global trading and optimization.

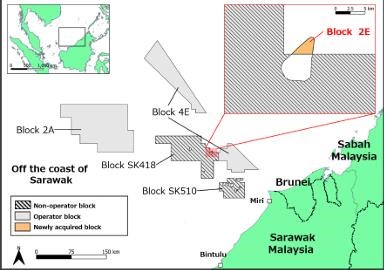

INPEX buys stake in Malaysian offshore gas field

(Company statement, July 2)

- INPEX bought an 85% stake in Block 2E located off the coast of Sarawak, Malaysia. It was purchased from TotalEnergies for $350 million.

- The remaining 15% belongs to Malaysia’s state-owned oil company, Petronas.

- The acquired block is part of the larger Majoram gas field.

Tokyo Gas to supply city gas derived from overseas biomethane feedstock

(Government statement, June 25)

- Fujifilm, Tokyo Gas, and Tokyo Gas Engineering Solutions agreed to supply city gas derived from imported biomethane to Fujifilm’s Ashigara Site in Kanagawa.

- This is Japan’s first use of imported biomethane-based city gas in the chemical sector.

- Biomethane is produced by capturing and reusing organic methane emissions.

- CONTEXT: To reduce emissions, Fujifilm is combining multiple measures, including energy efficiency improvements, the use of renewable electricity, and the adoption of low-carbon fuels, particularly for high-temperature chemical manufacturing. Tokyo Gas Group has a long-standing partnership with Ashigara, providing on-site energy services, including the supply of electricity, water, air, etc.

- TAKEAWAY: Imported biomethane can decarbonize city gas while using existing LNG and gas infrastructure, allowing fast deployment. Other projects from the U.S. are underway, and there are new supply options, such as from Brazil. But expansion faces major challenges: higher costs than conventional gas, limited sustainable feedstock supply, the need for reliable certification and carbon accounting rules, logistics and shipping infrastructure, and strict methane leakage management to ensure real climate benefits.

LNG stocks down from previous week, down YoY

(Government data, July 1)

- As of June 28, the LNG stocks of 10 power utilities were 2.08 Mt, down 1.4% from the previous week (2.11 Mt), down 6.7% from end June 2025 (2.23 Mt), and down 1.9% from the 5-year average of 2.12 Mt.

- Rainy-season weather has so far kept temperatures below last summer’s late-June levels, limiting near-term cooling demand.

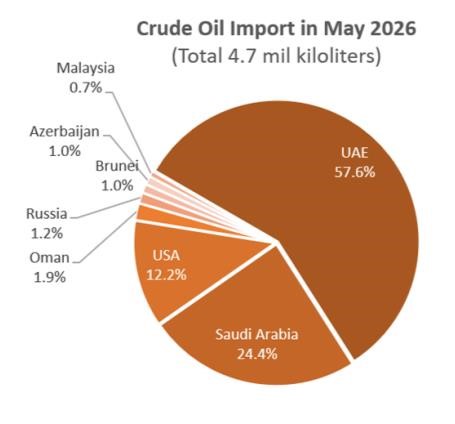

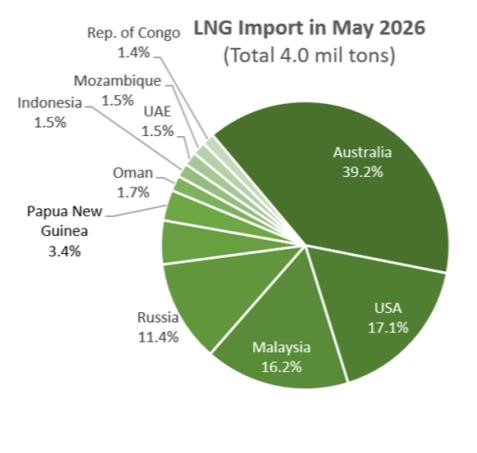

May Oil/ Gas/ Coal trade statistics

(Government data, June 30)

- In May, Japan imported 4.7 million kiloliters of crude oil, up 5.5% over April, the lowest on record, and down 57.3% YoY. The govt tapped into Azerbaijani and Russian supplies. Imports from the Middle East accounted for nearly 84%, down 10% over past averages.

- LNG imports in May totaled 4 Mt, down 7.3% over April (4.3 Mt) and down 15.1% YoY. Still, total import value was up 3.3% MoM. About 40% of LNG came from Australia, and an additional 25% from the rest of Asia Pacific. Imports from the U.S. jumped nearly 2.5-fold (from 190,000 tons to 680,000 tons).

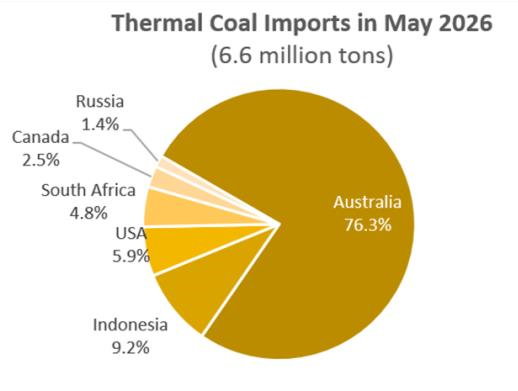

- Thermal coal imports in May totaled 6.6 Mt, down 7.1% from April, but up 14.1% YoY. Japan imported more coal to back up crude oil and LNG. The import value (¥148.2 billion) was down 0.2% MoM, but up 48.4% YoY. Imports from Australia and South Africa were up 7.6% and 6%, respectively.

NEWS: CARBON CAPTURE & SYNTHETIC FUELS

Clean Energy Connect and Green AI partner on decarbonization solutions

(Company statement, June 25)

- Clean Energy Connect, a Japanese renewables developer and corporate PPA provider, will partner with Green AI, a startup offering AI-based energy management and decarbonization planning software.

- Their goal is to provide an integrated package combining renewable power procurement with energy efficiency solutions for corporate clients.

- The firms aim to help businesses lower both energy costs and GHG emissions by integrating renewable power procurement with demand-side energy optimization.

- The service will identify the most cost-effective emissions reductions, estimate CO2 savings and investment payback periods.

Anritsu launches circular model of electricity supply with biogas

(Company statement, June 25)

- Anritsu, JBio Food Recycle and Urban Energy launched a circular electricity supply model using biogas.

- Anritsu will supply food waste to JBio Food Recycle, which will process it into biogas through methane fermentation. Then, Urban Energy will supply electricity to Anritsu’s office in Atsugi (Kanagawa Pref).

- TAKEAWAY: Until now, similar initiatives have mainly involved food manufacturing plants. This demonstrates that a circular electricity supply model can also be implemented using smaller volumes of food waste, especially if combined with environmental value.

ANALYSIS

BY ALEX FARRELL

Low Latency, Long Distance: Japan’s Next Data-Center Catalyst

Japan’s data-center site selection is increasingly an energy problem. AI, cloud computing and digital services require ever-larger facilities, but the power, land and cooling capacity needed to host them are difficult to secure around Tokyo and Osaka.

Those cities remain the nation’s core data-center markets because they offer dense fiber networks, telecom exchanges and corporate demand. Yet land is expensive, grid capacity is tight and local resistance to new construction is rising. Regions with more renewables potential, cheaper land or lower cooling costs offer an alternative. Their disadvantage, however, is distance from Japan’s main users and network hubs.

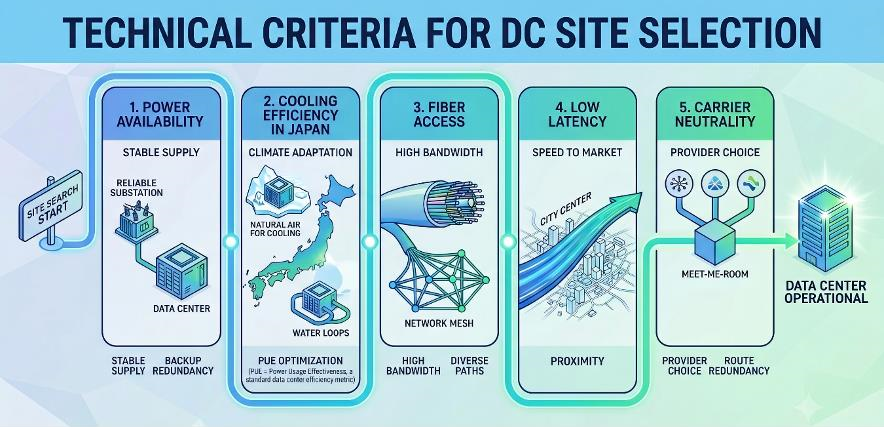

Latency – the delay between sending data and receiving a response – has long made geography matter. The closer a facility sits to dense fiber networks, telecom exchanges, cloud users and corporate customers, the more valuable it becomes. But that equation is starting to change. IDC Frontier, for example, advertises latency of just 3.5 ms to central Tokyo from its Fukushima Shirakawa site, about one-third of the typical delay between Tokyo and Osaka.

If low-latency fiber can reduce the distance penalty for regional data centers, it could open new siting options in lower-cost areas. For energy companies, the implication is important. More viable regional sites could create new demand near renewable-power resources, support local PPAs, and strengthen the case for generation and grid investment outside the country’s most congested urban markets.

Advances in data transmission have given rise to a new approach: “connectivity-first”. The term refers to selecting and designing infrastructure sites around superior fiber access, low-latency network reach and resilient interconnection.

In the past, connectivity-first logic reinforced the concentration of data centers in Tokyo and Osaka. In the next phase, it may become the condition that allows more capacity to move outward, toward regions with land, cooling and renewable-energy advantages.

Connectivity as an energy enabler

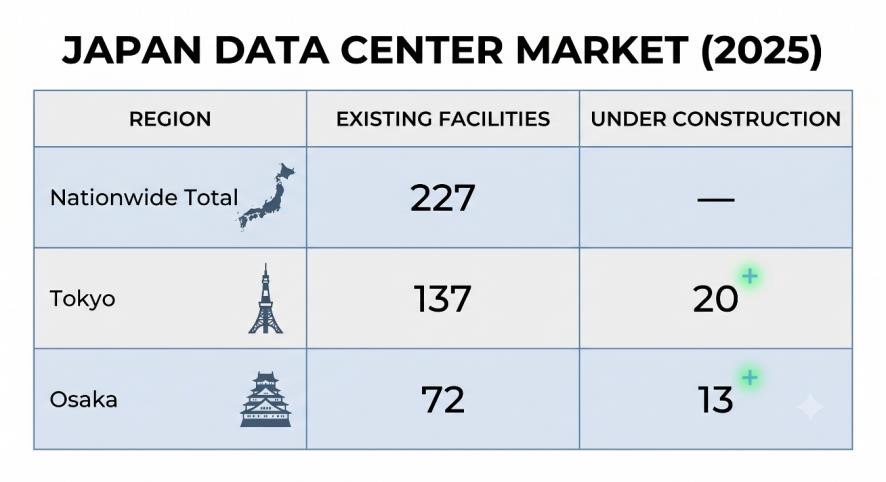

The old connectivity-first model has already shaped Japan’s data-center geography. Tokyo remains the country’s primary interconnection hub, while Osaka is emerging as a secondary core market with strong demand, improving interconnection options and a role in geographic diversification. Together, Tokyo and Osaka account for roughly 90% of Japan’s DC facilities.

The limits of this model can be seen in Inzai, Chiba Prefecture. The city is now one of Japan’s largest DC clusters, with around 20 facilities in operation and another dozen in the pipeline. Its appeal is clear: available land, proximity to Tokyo and hard ground with no nearby active tectonic faults. Yet Inzai has also begun curbing additional construction in response to residents’ concerns. Connectivity can make a location valuable, but it does not remove constraints around land use, local acceptance or power supply.

That’s why the next phase of connectivity-first development matters for energy. The issue is not whether regional sites can replace Tokyo or Osaka as network hubs. They cannot. The question is whether better fiber routes, carrier diversity and low-latency interconnection can reduce the penalty of distance enough to make more regional sites viable.

The energy implications are significant. Regions with cheaper land, lower cooling needs or renewable-energy resources could become more attractive if they can offer acceptable latency. Hokkaido is the clearest example. Its cold climate can reduce cooling loads, and projects such as Soya Green Data Center I in Wakkanai are designed to take advantage of local conditions by connecting directly to wind power.

Kyushu offers a different case. Its large solar fleet has created recurring curtailment during low-demand periods, including very high curtailment rates in spring months. A large data center would not automatically solve that problem: curtailment is seasonal, hourly and grid-specific, while DCs require stable power around the clock.

If regional sites become more viable from a connectivity standpoint, they could create new anchor demand for local PPAs, storage-backed supply models and grid investment. This is why the issue matters to energy companies.

More viable regional data-center sites could create new buyers for renewable electricity outside Japan’s most congested urban markets. They would also appeal to RE100 members such as Google and Amazon, telecoms such as KDDI and SoftBank, and site developers such as Tokyu Land, all of which need access to credible low-carbon electricity.

Connectivity does not make renewables dispatchable or grids unconstrained. But it can help bring power-intensive demand closer to places where clean power, land and cooling advantages are available.

Technologies narrowing the gap

Two technology trends could help regional data centers compete with urban sites, though they solve different problems.

The first is modular data centers. Containerized and prefabricated systems cannot replace hyperscale campuses, but they can reduce construction time, lower upfront commitment and allow developers to add capacity in smaller increments. That makes them useful in locations where demand, grid availability or local permitting may develop gradually.

Alongside startups such as Getworks, established firms including Daiwa House, Hitachi and NTT East are offering modular or containerized systems that can be deployed faster than conventional facilities.

For energy developers, modularity can better match the pace of local power development. A giant co-location campus may require large grid capacity from day one. A modular facility can begin smaller, then expand as grid connections, renewable PPAs, storage and local demand mature. This does not remove the need for reliable power, but it can make the relationship between compute growth and energy infrastructure less rigid.

The second technology is NTT’s All-Photonics Network, part of its broader IOWN vision. APN is more ambitious and less mature, but it goes directly to the long-term siting question. By reducing optical-electrical conversions and moving more data through photonics-based networks, NTT aims to cut latency, increase transmission capacity and improve power efficiency. If the technology scales, it could make it easier to shift some workloads to data centers located farther from Tokyo and Osaka without losing the responsiveness users expect.

Neither technology eliminates the trade-off. Modular systems help developers build faster and in smaller increments; they do not create grid capacity or clean power. APN may reduce the network penalty of distance; it does not make every workload insensitive to latency. Together, however, they point to a more flexible data-center geography: one in which the most latency-sensitive workloads remain in dense urban hubs, while other capacity moves toward regions with better energy fundamentals.

Conclusions

Connectivity-first development will not make geography irrelevant. Tokyo and Osaka will remain Japan’s core data-center markets, especially for workloads that require the densest interconnection and the lowest possible latency.

Nor will better networks turn every renewable-rich region into a natural DC hub.

What connectivity can do is widen the range of viable choices. A regional site no longer needs to replicate Tokyo’s network density to be useful. It needs to offer enough connectivity for the right workload, alongside the right mix of power, land, cooling, resilience and local support.

For energy companies, the opportunity lies in recognizing that data centers are not just new power demand. They are a new class of location-sensitive demand, whose value will depend on how well electricity and connectivity can be developed together.

ANALYSIS

BY FILIPPO PEDRETTI

Squeezing the Atom: Japan Aims to Maximize Nuclear Energy Output

In 2026 alone, METI’s working group on nuclear power produced more than 300 pages of documents discussing the sector’s development.

Just a couple of weeks ago, the cabinet released the 2025 edition of its nuclear energy ‘white paper’. For the last 10 years or so, the ministry has been producing files like this, ranging from 200 to over 400 pages each.

This may seem like a waste of paper for a country that built its last nuclear power plant 17 years ago. But after over 15 years since the Fukushima disaster Tokyo officials want to reaffirm that reintegrating the nuclear fleet is vital for two reasons. The first has to do with the nation’s dual pursuit of 2030 decarbonization targets; the second, with its energy security.

As geopolitical events reverberate on fluctuating LNG prices, nuclear power is seen as a panacea for energy stability. Government documents defend nuclear as a low-carbon baseload that stabilizes the grid, and plan that it will once again play a major role in the nation’s future.

But the reality of what can be achieved may be different.

Maximizing existing plants and replacements

The government’s main goal is to have as many nuclear plants operating as possible. For example, the recent restart of Kashiwazaki-Kariwa Unit 6 is a highly significant event, marking TEPCO’s return to the nuclear power scene. While that asset is in Tohoku region’s legacy territory, it’s also a vital link for the Tokyo metropolitan region’s energy security. For TEPCO’s service area, this means a projected 2% increase in the reserve margin.

Next, all eyes are on Hokkaido’s Tomari Unit 3 and Tokai II, both dealing with safetyrelated works. Tomari could restart as soon as next year. In 2029, Unit 7 of

Kashiwazaki-Kariwa should follow the same path — when its Unit 6 will go offline for anti-terrorism upgrades.

But the industry has had setbacks, such as the exclusion of Tsuruga Unit 2 from the review pipeline. This followed its permit denial in late 2024 due to the plant’s vicinity to an active fault line. Regulatory requirements, geological and seismic compliance dictates restarts.

Another setback was the Hamaoka misconduct case in January this year. Chubu Electric disclosed its intentional misconduct whereby it selected specific seismic waves to manipulate earthquake data assessments. The NRA responded with a stop-work order on the plant’s restart review process.

While such firm action ensures safety, it shortens the list of potential NPP restarts. To compensate, the NRA has shortened the process of approving antiterrorism measures, reducing the burdens on operators.

| Status | Count | Key facilities |

| Restarted | 15 units | Kashiwazaki-Kariwa Unit 6; Onagawa Unit 2; Shimane Unit 2; and units across the Kansai, Kyushu, and Shikoku regions. |

| Permitted | 3 units | Kashiwazaki-Kariwa Unit 7 (targeting completion of Specialized Safety Facilities by 2029); Tokai II (currently addressing protective wall design requirements); and Tomari Unit 3 (targeting restart in 2027). |

| Under review | 8 units | Ohma (safety review began in June 2025); Hamaoka Units 3 & 4 (currently suspended); Tomari Units 1 & 2; Higashidori Unit 1; Shika Unit 2; and Shimane Unit 3. |

With the list of possible restarts limited, the government seeks to maximize the generational potential of each, proposing to extend the period after which a reactor must undergo periodic inspections. Currently, inspections are due after 13 months, but regulators want to extend the timeline to 15, 18, or even 24 months.

The government also released new targets for replacing nuclear reactors. This is due to the fact that by 2040 four domestic reactors will have exceeded 60-year lifespans. By the 2040s, the government aims to replace two to five reactors (about 2.2 to 5.5 GW of capacity). For the 2050s, the goal is a total of 11 to 14 reactors (12.7 to 16 GW).

Getting local support

Getting NPPs to work also implies dealing with communities. In 2025, the “Special Measures Law for the Promotion of the Development of Regions Hosting Nuclear Power Plants” was revised. National support, previously confined to a 10 km “Emergency Planning Zone” (EPZ), now applies to a 30 km area. The new designation is “Urgent Protective Action Planning Zone” (UPZ).

Such national disaster and emergency support comes through subsidies, which can go towards reinforcing and widening roads to ensure multi-directional transit during emergencies. Also, funds can enhance port facilities to ease emergency response and the delivery of critical supplies; as well as help upgrade local communication networks and regional shelter capacities. The government hopes this will foster public trust and crush any anxiety over possible accidents.

The government is also using the Regional Industrial Structure Transformation

Infrastructure Promotion Grant that links nuclear stability with high-tech manufacturing. Nuclear power will play a major role in powering projects such as the semiconductor plant Rapidus, provided the Tomari nuclear power plant will restart.

In a similar fashion, Kumamoto (JASM/ TSMC) needs to secure the power supply for advanced chip production. The recent restart of Kashiwazaki Kariwa should also help Niigata’s industrial goals.

Waste reprocessing and disposal

Nuclear power generation goals are tethered to a closed fuel cycle. Completing this task is the crucial prerequisite for any other future nuclear activity, and the core issue lies in the Rokkasho reprocessing plant.

After around 30 years of delays, completion looks possible in FY2026. But, safety inspections and large-scale upgrades are still required by the regulator. As for the MOX Fuel Plant, completion targets FY2027.

| Item | Cost estimate | Increase from previous year |

| Rokkasho Reprocessing Plant – total project cost | ¥15.98 trillion | +¥360 billion |

| Rokkasho Reprocessing Plant – construction cost (included in total) | ¥3.92 trillion | +¥180 billion |

| Rokkasho MOX Fuel Plant | ¥2.68 trillion | +¥80 billion |

As for a final disposal site, the last major hurdle was selection of the remote Pacific Ocean island Minamitorishima-Ogasawara as a candidate in March, with local authorities adamant in proceeding with the relevant surveys.

Conclusion

The absence of a fully operational solution for nuclear fuel waste is obstructing future plans for the sector in Japan. Reactor restarts face strict regulations that often lead to unexpected delays. Compounding these obstacles is the fact that many reactors are close to retirement age and could soon be shut, even with the government’s time limit extension. All this limits the potential to boost nuclear energy in Japan in the short to mid term.

The only way to increase operational nuclear capacity would be rebuilding nuclear plants. But, Japan has not completed a new nuclear plant since 2009, and the stagnation since then has left the country with an aging and inactive workforce, with few young people joining the sector’s ranks.

Building a new nuclear power plant after many years of hiatus is expected to bring delays and higher costs to the already long and expensive construction process. A new plant requires a giant initial investment (over ¥1 trillion per unit), with a lead time of about 20 years before they generate revenue.

In a liberalized market, recovering such investments is uncertain without government intervention. Help could come from measures such as the Regulated Asset Base model.

In other words, Tokyo’s room for action in the nuclear power sector is limited to a few possible restarts and the immense task of managing nuclear fuel waste.

ASIA ENERGY REVIEW

BY JOHN VAROLI

A brief overview of the region’s main energy events from the past week

Australia / BESS

Wärtsilä brought online the 150 MW / 300 MWh Bungama BESS in South Australia, confirming commercial operations for owner and operator Revera Energy.

Australia / Natural gas

Australian Energy Producers, representing the country’s upstream oil and gas industry, welcomed the 2026 Integrated System Plan by the Australian Energy Market Operator that highlights the need for new gas investments to enable grid reliability.

China / LNG

LNG imports rebounded to above last year’s levels. China will buy about 5.29 Mt of LNG this month, reports Kpler. The uptick is due to lower domestic output, depleting storage levels, a hot summer, and international prices falling from highs reached during the peak of the U.S.Iran war.

China / Five-year plan

The latest five-year energy plan confirms two seemingly contradictory positions: China will continue to be the world’s leader in both renewable energy output and coal production.

India / Fuel reserves

The govt plans to create reserves of at least one month for crude oil, LPG, and natural gas in order to avoid the disruption that it suffered during the U.S.-Iran war.

India / Oil exports

Russia began seaborne imports of gasoline from India, say media reports, in an effort to mitigate fuel shortages caused by Ukrainian attacks on its energy infrastructure.

Indonesia / Blackouts

Recent blackouts in Sumatra and Java exposed vulnerabilities in Indonesia’s electricity system. PLN says constrained coal supplies contributed to the Java outage. Analysts say the outages reveal the risks of Indonesia’s centralized, coal-dependent electricity system

South Korea / Offshore wind

The Ministry of Climate and Energy opened a 1.8 GW offshore wind tender, featuring separate and reduced price caps for fixed-bottom and floating turbines.

South Korea / Renewables

SK Inc. and private equity firm KKR will set up the country’s largest renewable energy platform, combining solar, wind, and fuel cell assets into a $1.3 billion business to supply clean electricity to the country’s rapidly growing industrial sector.

Taiwan / LNG

Taiwan seeks to maintain a policy of diversified LNG procurement following the energy crisis sparked by the U.S.-Iran war.

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Hulic Ochanomizu Bldg. 3F, 2-3-11, Surugadai, Kanda, Chiyoda-ku, Tokyo, Japan, 101-0062.