PM Modi’s visit to Tokyo in August put energy at center stage, with critical minerals as a key aspect. Still, much of the agenda consists of frameworks and memoranda rather than large-scale projects.

Can the two countries can turn complementary strengths into concrete outcomes or will the partnership remain aspirational?

LNG is no longer just a commodity; it’s now a lever of U.S. foreign policy. To placate Washington, Japan recently pledged an annual $7 billion worth of additional U.S. energy purchases.

This deeper entanglement with U.S. gas has a cost. By narrowing options, Tokyo risks swapping one vulnerability for another: what is sold as a step toward energy security could undermine it.

ASIA PACIFIC REVIEW

This column provides a brief overview of the region’s main energy events from the past week

At a televised debate for the LDP leadership race, three of the four other candidates directed questions at Koizumi Shinjiro, underscoring his status as a front-runner.

Koizumi defended his pledge to raise average wages by ¥1 million by 2030, citing productivity gains, DX, tax incentives, and public-sector price reforms as tools, while linking the plan to the Bank of Japan’s 2% inflation target.

Rivals questioned whether tax incentives would reach loss-making SMEs and suggested focusing on median wages, while Koizumi insisted broader productivity measures and stronger subcontracting rules would spread gains.

On energy, rival candidate Kobayashi Takayuki highlighted the instability and cost of solar, plus reliance on imports, asking about Koizumi’s security strategy. Koizumi said Japan must raise domestic energy self-sufficiency by expanding both renewables and nuclear, with safeguards against local environmental harm.

Former economic security minister Kobayashi Takayuki pledged to shift Japan’s energy policy “from decarbonization to low-carbon development,” stressing pragmatism over climate idealism.

Kobayashi said he would “strongly promote nuclear power” as part of a realistic energy security strategy.

He argued renewables are “expensive and unstable,” warning against Japan’s reliance on Chinese-made solar panels, and urged a pause in further expansion.

He said moving away from what he called “excessive decarbonization” toward a more realistic balance of cost, security, and supply stability.

Former economic security minister and LDP leadership candidate Takaichi Sanae said she was “strongly opposed” to seeing Japan’s landscape covered with foreign-made solar panels, criticizing the government’s utility-scale solar policy.

CONTEXT: Around 95% of solar panels shipped in Japan in 2024 were imported, with more than 80% made in China.

Takaichi mentioned challenges with the safe disposal of aging first-generation panels and called for greater use of perovskite solar cells (PSC), a technology largely developed in Japan that promises lighter, thinner, and more flexible panels.

Takaichi argued PSC could become an export sector and “bring wealth to Japan.”

TAKEAWAY: Koizumi is assumed to be the front-runner for leadership. Given his close connection with previous PM Suga and LDP heavyweight Kono – who promoted renewables and was a nuclear power skeptic – Koizumi’s stance on both green energy and nuclear are questioned closely. So far, Koizumi has been keen to show that he is aware of the challenges that come with solar power (i.e. intermittency, the need to import nearly all the panels from China, etc.). Overall, Koizumi’s position seems to have moved closer to the center, while his rivals have taken up a stance that is not completely antagonistic to further solar development, but in effect likely to slow its rollout.

ANRE reviewed the challenges of grid connection for large power-demand facilities, such as data centers (DCs), based on an actual-condition survey.

It surveyed DCs applying for grid connection and found delays due to unclear plans or unacquired land; only 44% paid construction fees within three months – as per the rules – and some postponed their full demand by over ten years.

To address this, officials have confirmed that fees must be paid within three months of approval or the contract will be canceled. Contracted capacity must also reach final demand within a set period to ensure cost recovery.

CONTEXT: As power demand from DCs grows, ensuring a rapid, reliable power supply is crucial to promote domestic investment. Main considerations include efficient facility development, grid planning, and sustainable construction resources.

JERA Cross will supply environmental value to a Google data center in Inzai, Chiba Pref by March 2027 through a solar virtual PPA.

Acting as the aggregator, JERA Cross will bundle electricity and environmental value generated by 15 MW in solar power facilities to be developed by West Holdings.

EVolity, a JV between Marubeni and Panasonic, will launch a diagnostic service for EVs in Thailand, to detect battery degradation, battery fire and other problems.

The service will target large EV trucks and pickup trucks.

Thailand is the first overseas business for the Japanese JV and the beginning of an international expansion in EV applications.

TAKEAWAY: Even though this diagnostic service relates to batteries for EVs, a similar testing system for grid-scale batteries could prove profitable for Japanese BESS developers looking to reduce project costs by sourcing batteries from elsewhere in Asia, while making sure national quality standards are met.

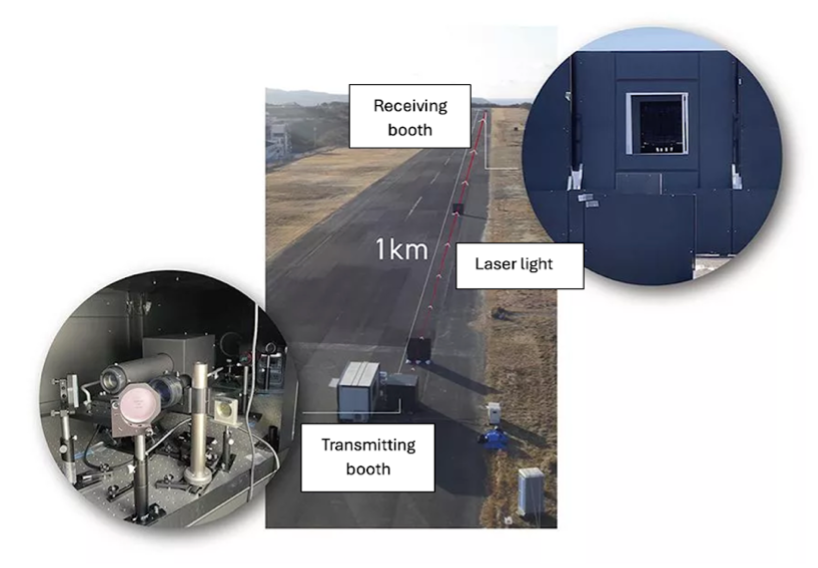

NTT and Mitsubishi Heavy Industries (MHI) conducted an optical power transfer experiment to wirelessly supply energy 1 km away. Power was continuously supplied for 30 minutes, generating on average 152 W.

A laser beam with a 1,035 W capacity was generated. An optical tool shapes the beam so that the intensity distribution is flat on the whole distance to improve photoelectric conversion efficiency.

CONTEXT: Such technology is intended to be used in remote or disaster-stricken areas, where it is difficult to install power cables.

NKY Group’s subsidiary NYK NEO delivered the chemical tanker Golden Thetis.

This follows the expansion of its 47-carrier fleet that includes LPG, chemical and dry bulk vessels, demonstrating future growth in energy transport.

CONTEXT: In April, NYK Group acquired an 80% stake in NYK Energy Ocean Corp, taking over ENEOS Ocean’s shipping business excluding its crude oil tanker operations. Together with the 16 vessels operated by NYK, the fleet now totals 34.

ANRE reported on the status and short-term outlook of curtailments of renewable energy output, as well as operational improvements by grid users.

CONTEXT: Renewable energy curtailment is increasing nationwide, driven by wider adoption, simultaneous controls, and weather conditions.

The FY2025 short-term outlook for renewables curtailment was revised from the initial January forecast, reflecting actual results and updated assumptions.

Compared to the initial outlook, curtailment is expected to increase in Tohoku, Tokyo, Kansai, and Shikoku; remain flat in Hokkaido; and decrease in Chubu, Hokuriku, Chugoku, Kyushu, and Okinawa.

Regarding grid operational improvements, TSOs highlighted some issues for grid users, so ANRE sent a notice asking them to follow the rules. This is still insufficient, so ANRE will update the notice to warn that noncompliance with power supply instructions may lead to contract termination.

CONTEXT: Each TSO estimates the outlook based on actual results. ANRE compiles these estimates and reports them to the advisory council. The short-term outlook is presented twice a year, while a long-term outlook is presented once a year.

ANRE reported the mid- to long-term outlook for grid congestion and set rules for decisions on local grid reinforcement.

FY2030 outlook expects renewables curtailment mainly in eastern grids, continuing previous trends.

Each TSO bases their reinforcement decisions on grid conditions. But, the ANRE is proposing to unify the approach by using the mid- to long-term outlook calculated by OCCTO.

For grids expected to face congestion within five years, reinforcement plans will be developed via a cost-benefit assessment that takes into account congestion forecasts 10 years ahead.

CONTEXT: To help power producers assess profitability, improving curtailment forecasts due to grid constraints is essential.

ANRE and OCCTO prepared a draft of the second interim report at the Study Group on Design of a Simultaneous Market, and presented a roadmap for the market’s rollout.

The first step will be to define requirements for market design from a practical perspective and also the development of a system to support market functions.

CONTEXT: The study group began discussing the simultaneous market in August 2023 and released its first interim report in November 2024. Following the approval of the 7th Basic Energy Plan in February 2025 and review of power system reforms in March, it resumed discussions to further examine the remaining issues.

TAKEAWAY: Rising wholesale electricity prices, insufficient bids, and increasing operational uncertainties for TSOs are challenges to ensure stable and efficient power procurement. These issues become more pressing as more intermittent power sources are added to the grid. The simultaneous market has been studied in various committees as a market mechanism to enable stable and efficient procurement and operation of power facilities, even with a high ratio of intermittent power sources in the system.

Japan Electricity Procurement Solution (JEPS) and Beyond Next Energy developed a method to forecast Japan’s electricity market prices through 2050 and launched a new Electricity Market Price Data Service.

CONTEXT: JEPS is an expert enterprise specializing in maintenance, management, operation, and monitoring of electrical equipment and facilities, including power plants and solar power facilities. BNE is a consultancy specializing in energy markets and decarbonization strategies.

The service uses an enhanced merit order model, a system that ranks power plants by marginal cost (cheapest first) but also factors in real-world conditions such as the minimum output levels of thermal plants that are needed for grid stability.

By combining demand forecasts, generation patterns, marginal costs of different power sources, and CO2 pricing, the system produces 30-minute interval price projections for up to 2050.

Kyushu Electric said revenue from sales of non-fossil fuel certificates in FY2024 rose by ¥8.6 billion over FY2023 to ¥19 billion. Although sales volume was flat, differences in payment timing boosted income. The revenue went to hydro plant upgrades, maintenance, and nuclear safety measures.

Annual revenues from these certificates were ¥9 billion in FY2020, ¥10.6 billion in FY2021, ¥8.1 billion in FY2022, and ¥10.4 billion in FY2023.

Woodside Energy, Japan Suiso Energy (JSE), and Kansai Electric inked an MoU to collaborate on a liquefied hydrogen supply chain between Japan and Australia.

The three will discuss transporting liquefied hydrogen produced by Woodside’s H2Perth project in West Australia to Japanese terminals using specialized carriers.

The project plans to produce hydrogen from natural gas in the Rockingham and Kwinana industrial areas, while capturing and storing CO2; it will use carbon credits as needed, and aim for net-zero Scope 1 and 2 emissions from the start.

CONTEXT: JSE was launched in 2021 as a JV between KHI and Iwatani Corp. It aims to build and operate global liquid hydrogen supply chain infrastructure. The H2Perth project has been in the works since 2021 and intends to establish both green and blue hydrogen production with a combined initial capacity of 0.84 million tons per annum (Mtpa) in 2027. Woodside might sell to Keppel, which plans to use the hydrogen to power its data centers in Singapore.

JERA and Denso began a hydrogen production test at the JERA Shin-Nagoya Thermal Power Plant using Denso’s solid oxide electrolysis cell (SOEC) water electrolysis unit (200 kW).

Denso’s thermal management tech minimizes heat released from the SOEC, aiming to achieve hydrogen production with world-class electrolysis efficiency.

CONTEXT: SOEC operates at high temperatures using a ceramic membrane as the electrolyte to create steam and produce hydrogen. It features very high electrolysis efficiency (up to about 80%) and reduces electricity costs.

TAKEAWAY: Compared to Alkaline and PEM (proton exchange membrane) types, SOEC technology is still in the R&D stage, but demos are underway overseas. Along with NEDO’s R&D projects, SOEC development will now proceed under Green Innovation Fund projects, so further progress by domestic companies is expected.

Itochu, Toray, and Uyeno Transtech inked an MoU to set up domestic ammonia fuel supply hubs for ships, aiming to verify safety, plan necessary facilities and permits, and review supply and trading conditions.

CONTEXT: Ammonia is gaining attention as a zero-emission marine fuel, with shipowners, cargo owners, and fuel producers exploring its use.

Itochu coordinates studies on ammonia bunkering ships and fuel. Toray provides information on land facilities, ammonia handling. Uyeno Transtech supports information sharing and coordination with authorities for bunkering ships.

CONTEXT: The International Maritime Organization approved treaty amendments to support the 2050 goal of zero GHG emissions from shipping. These include measures to switch to low-GHG alternative fuels and provide incentives for zero-emission ships that are expected to accelerate alternative fuel supply and ship adoption.

Air Water and Toda Kogyo completed a DMR (direct methane reforming) hydrogen production plant in Toyotomi Town, Hokkaido, that runs on unused natural gas.

The project involves establishing a commercial-scale hydrogen production plant in Toyotomi Town using the DMR process.

It will produce high-purity hydrogen from unused natural gas without direct CO2 emissions and supply it to local customers for quality validation.

A hydrogen production system using DMR will be set up by April 2026.

CONTEXT: In Toyotomi Town high-quality natural gas with a methane content of 95% is produced from hot springs, but much of it remains unused. Efforts are underway to revitalize local industry through its use.

A 95,000-panel solar farm at Sendatsuyama, west of Fukushima City, is set to begin power sales on Sept 30, despite local residents objecting to glare from the panels and scarring of the mountain slope. They accuse the developer of underplaying landscape impacts in documents submitted to the city.

The city acknowledged discrepancies in the developer’s submissions but stopped short of declaring them false; it pledged to demand restoration of greenery to align with initial projections.

The project company, backed by AMP, apologized for altered scenery and promised vegetation recovery, while also committing to test for panel reflection issues.

CONTEXT: Fukushima City decided not to accept the developer’s completion notice under the local landscape ordinance due to pressure from residents.

TAKEAWAY: Community pushback has become a recurring challenge for Japan’s solar expansion. While national policy promotes rapid deployment to meet decarbonization goals, local concerns over land use, glare, biodiversity, and scenery have slowed or reshaped projects in multiple prefectures, underscoring the tension between climate policy targets and regional acceptance.

METI and other ministries unveiled more than ¥800 billion in requests tied to perovskite solar (PSCs) and supply chain support, spanning three programs.

MoE, in cooperation with METI and MLIT, requested ¥5 billion in FY2026 for a model project to promote PSCs in buildings and infrastructure such as rooftops and windows, aiming to cut initial costs and expand demand.

ANRE budgeted ¥3.1 billion to develop technology to overcome mass-deployment challenges, targeting eight technical breakthroughs over FY2025–29.

A further ¥792 billion is sought under the GX Supply Chain Support program to subsidize large-scale domestic investments in clean energy manufacturing, including perovskite solar, floating offshore wind, fuel cells, and HVDC cables, with goals such as reaching 65% domestic procurement in offshore wind by 2040.

Together, the measures are designed to accelerate PSC commercialization, ensure local production capability, and strengthen competitiveness in the global solar sector.

TAKEAWAY: Japan seeks to target subsidies for specific technologies, with emphasis on domestic manufacturing and supply-chain security. The supply is often pegged to local purchasing targets, such as a 60% or more ratio for domestic content in offshore wind by 2040. These technology-focused budgets are split between several ministries, all of which frame it within a unified national program, such as the GX strategy. This approach contrasts with the EU, which prioritizes carbon-reduction and other climate targets.

In December, Kyuden Mirai Energy will begin a demo test of next-gen chalcopyrite solar cells at Fukuoka Airport.

The panels will be tested for power generation performance and ease of installation, and compared with existing silicon-based panels already in place.

CONTEXT: Chalcopyrite solar cells weigh just 0.8 kg/ square meter (about 1/ 20th the weight of silicon panels) and have an 18% efficiency rate. This makes them less efficient than the silicon option but more durable and lighter than perovskite solar cells. They can also generate power under weaker light.

Because of their light weight, these panels can be installed without cranes and on roofs that cannot support heavy panels, reducing construction costs.

The goal is to combine perovskite (efficient with UV light) and chalcopyrite (efficient with infrared light) into a ‘tandem solar cell’ with up to 28% efficiency, which is about 1.5 times higher than current models.

ANRE discussed strengthening grid connection procedures and revising connection rules for storage batteries to enable their rapid connection to the grid.

According to the government review, the surge in battery grid-connection requests includes many applications for unusable sites, with some developers submitting over 100 requests to the same utility.

Therefore, applicants will be required to submit land-related documents, and a cap will be set on the number of applications allowed per developer.

CONTEXT: As the number of connection requests increases, the time it takes the TSO to process applications also increases. This delays not only grid access procedures for grid-scale batteries, but also those for all power generation facilities, extending the time required to connect to the grid.

As of late June, applications for grid-scale battery storage have surged with:

Applications for connection under study reaching some 143 GW, roughly 2.4 times higher than a year earlier;

Contract applications totaling around 18 GW, a fourfold increase YoY.

Growth was particularly strong in the Tohoku, Tokyo, Chugoku, and Kyushu regions. Despite this pipeline, only about 250 MW of grid-scale battery storage has actually been connected to date.

TAKEAWAY: Based on internal study and interviews with industry members, Japan NRG estimates the actual number of commissioned BESS projects at least twice the reported number. However, officials seem to categorize standalone batteries and those connected to renewables projects for frequency regulation differently.

Osaka-based EPC company TESS Engineering was contracted by Nakayoshi Sekizai to install storage batteries at three solar power plants (one in Oita, two in Kagoshima Prefs) as they transition from the FIT to the FIP.

Nakayoshi Sekizai is a Kagawa-based quarrying and stonework firm. The developer is using Chinese Huawei batteries, with a total storage capacity of 22.35 MWh.

The work is scheduled for completion in April 2026, with TESS also handling aggregation after the switch.

CONTEXT: This project is part of TESS Group’s medium-term plan, which prioritizes FIT-to-FIP conversions with battery installations. TESS targets a cumulative 150 MW of installations by 2030. By combining FIP operation with storage, the facilities are expected to improve profitability amid frequent output curtailments.

TAKEAWAY: The FIT-to-FIP switch is mandated by METI. This project is part of a recent rush of companies that launched solar plants soon after the 2011 Fukushima disaster now adding BESS as part of their FIP transition. TESS Engineering is gaining recognition as an EPC provider in this sector, with more than 60% of its revenue now coming from contracted BESS projects.

Sun Village joined a sales agreement funded by Sumitomo Mitsui Funding & Leasing (SMFL) to build non-FIT solar power plants with a total capacity of around 11.8 MW in Japanese northern regions, with targeted grid connection by December 2027.

Next, Sun Village aims to develop 50 MW of new capacity nationwide each year.

CONTEXT: One of SMFL core activities involves financial support of clean energy projects. It financed a significant number of solar projects in Japan.

KEPCO is set to build new battery storage facilities in Hamamatsu and Mito, in partnership with Sparx Group and JA Mitsui Lease.

Hamamatsu facility: 30 MW/ 113 MWh capacity, commercial operation to start in June 2028.

Mito facility: 50 MW/ 175.5 MWh capacity, operation – from June 2029.

CONTEXT: The utility aims for a total storage capacity of 1 GW by the early 2030s. It already started the Kinokawa storage facility and is building others in Sapporo and Misaki, Osaka. With the two new facilities, the total developed capacity will reach 330 MW. President Mori Nozomi said the company aims to become Japan’s top battery storage operator through rapid development.

Trina Storage, the energy storage arm of China’s Trina Solar, inked an MoU with Yuasa Trading to collaborate on large-scale battery storage projects in Japan.

They will supply a total of 500 MWh of industrial storage systems to Japan.

Yuasa will leverage its local sales channels, project development, and service network, while Trina will provide fully integrated storage solutions, from battery cells and system integration to complete power supply.

The partnership is aimed at speeding up deployment of large energy storage projects in Japan and is seen by Trina as a key milestone in its expansion in the country.

Gogin Energy is entering the grid-connected battery storage business, the first in Japan for a bank subsidiary.

It is building a storage facility in Kurayoshi City, Tottori Pref, scheduled to launch in November to expand use of renewables and ensure stable power supply.

The facility will have four Li-ion batteries with a combined installed capacity of 1.9 MW and a storage capacity of 8.12 MWh. Investment costs were not disclosed.

CONTEXT: Gogin Energy, a wholly owned subsidiary of San-in Godo Bank established in 2022, was the first local bank in Japan to set up a power subsidiary, focusing on renewables and decarbonization initiatives.

PowerX, in collaboration with Itochu, has launched the co-branded energy storage package PowerX×Bluestorage.

It’s been adopted at four sites across Kanto, Chubu, Kyushu, including a solar plant in Karatsu, Saga Pref.

The systems – 20-foot container Mega Power 2700A and/or 10-foot Mega Power 2500 – use SMA power conditioners and offer storage capacities of 2.7 MWh and 2.5 MWh, respectively.

Itochu’s sales network will support expansion in the Japanese market.

An offshore wind power project off Murakami and Tainai in Niigata Pref – led by a consortium comprising Mitsui & Co., Osaka Gas, and RWE Japan – will begin some onshore construction work on Oct 1, such as surveying for transmission lines.

The work had been delayed from April due to contractor selection. Regardless of the delay, the planned operation start set for June 2029 remains unchanged.

Onshore construction is expected to finish by mid-2028, with offshore foundation installation starting in June 2027.

Originally, the plan was to use some of the world’s largest wind turbines, but procurement issues have forced a redesign.

CONTEXT: Rising equipment and construction costs have made offshore wind projects less profitable – for these reasons Mitsubishi-led consortium’s recently withdrew from three similar projects in Akita and Niigata Pref. Mitsui and its partners are asking the Japanese govt for support, such as long-term fixed-income guarantees and extended sea-use permits.

Chubu Electric President Hayashi apologized for the group’s withdrawal from offshore wind projects in three domestic areas, but affirmed the company’s commitment to offshore wind in general.

He stressed the firm maintains its 2030 target of increasing renewables capacity by over 3.2 GW from FY2017 levels. Hayashi also reiterated plans to explore other renewables such as onshore wind, solar, and geothermal power.

He stressed plans to leverage available tech and innovations to achieve these goals, but declined to comment on future participation in offshore wind projects.

TAKEAWAY: The public comment comes about a month after the official announcement of the Mitsubishi-Chubu Electric consortium’s withdrawal. The media has put the blame mainly on Mitsubishi Corp as the party responsible for poor management of the project, making it unsalvageable and thus resulting in the exit. While the group’s exit has cast a shadow on its reputation in the offshore wind sector, Chubu Electric has an opportunity to rebuild trust by continued commitment to its renewables expansion. Leveraging its extensive know-how in power generation, the company could still play a role in Japan’s wind power deployment.

FEPC Chairman Hayashi said the nation’s recently established emissions trading scheme could discourage decarbonization investments – if the benchmark system places excessive burdens on power companies. He urged the scheme to be coordinated with existing policies like the Energy Conservation Act.

Hayashi, who is also the president of Chubu Electric, commented on offshore wind. He apologized for his company’s withdrawal – alongside Mitsubishi Corp – from all projects won in the first auction round. He called it a serious setback.

Japan Wind Farm Construction (JWFC), backed by Toda Corp and five other major construction firms, chose Hakodate Port as the home base for its SEP vessel, used for offshore wind farm construction and maintenance.

The agreement includes sourcing materials locally when possible and coordinating port use with cruise operations.

JWFC cited Hakodate’s deep waters and proximity to Tohoku projects as reasons for the choice.

The SEP vessel, currently being refurbished in China, is expected to arrive in mid-May 2026 and will be capable of installing offshore wind turbines as large as 18 MW.

TAKEAWAY: Amid Japan’s growing commitment to offshore wind, SEP vessels are key for construction and maintenance of large-scale projects. A home base in Hakodate will help support regional supply chains – one of the govt’s goals, and position Japan to accelerate its offshore wind deployment in the Tohoku and Hokkaido regions.

Hokkaido Electric began the environmental assessment process for an up to 170 MW onshore wind project in Shimamaki Village, Hokkaido Pref.

The project will have 40 turbines, (4.3 MW each), across 1,036 Ha. Construction is planned to start in 2030; operations by about 2034.

The utility seeks to add over 300 MW of renewables to its portfolio by FY2030.

CONTEXT: Hokkaido Pref’s decarbonization targets are: a 48% reduction in carbon emissions by 2030 and net zero by 2050. Besides Shimamaki Village, Hokkaido Electric is involved in an up to 183 MW onshore project and an up to 1.14 GW offshore project.

Renewables firm Renova announced the environmental assessment plan for an onshore wind project in Yurihonjo City, Akita Pref. The project aims for a max capacity of 105 MW.

Construction is planned to start in May 2029; operation in December 2032.

The project plans to install either 16 turbines (4–6.6 MW each), or 24 turbines (4 MW each). Vestas 4 MW turbines are under consideration.

CONTEXT: Nearby, Cosmo Eco Power also plans its Akita Yurihonjo Wind Farm.

TEPCO outlined new initiatives to improve safety and revitalize the local economy in Niigata Pref. These are focused on the Kashiwazaki-Kariwa NPP.

They will open TEPCO facilities as temporary evacuation sites; and will expand and reinforce evacuation routes.

The Kashiwazaki-Kariwa NPP Operations Council was set up to integrate external experts into management decisions and allow them to make proposals to TEPCO’s Board of Directors.

The Cabinet Office and METI said restarting the NPP is crucial, as it will help in addressing eastern Japan’s electricity supply vulnerabilities.

TEPCO said that Unit 6 of the Kashiwazaki-Kariwa NPP could be technically ready for restart as early as mid-October.

A malfunction with the equipment occurred in August but they resolved the problem by September 20. The company is now aiming for operations during the winter.

TAKEAWAY: Technical readiness is not TEPCO’s main problem. It still struggles to get local consent, as the Prefectural governor still has not made a final decision. Hence, this “announcement” by the company has little practical impact on the restart.

Genkai NPP Unit 4’s inspection is almost complete.

The reactor will restart on Sept 30 and should reach criticality the same day.

Power generation should resume on Oct 2.

CONTEXT: Genkai NPP Unit 4 is a pressurized water reactor with a rated output of 1.18 GW. It has been undergoing its 17th periodic inspection since July 27.

The NRA approved KEPCO’s plan to build a dry storage facility at Mihama NPP.

This facility will store spent nuclear fuel by cooling it with air instead of water.

CONTEXT: KEPCO aims to use such facilities to move spent fuel from NPPs within Fukui Pref to an outside interim storage site. The NRA concluded that Mihama met safety standards.

Actual construction and use still need approval from Fukui Pref and local govts.

KEPCO already has similar approval for a facility at Takahama NPP.

The company plans to start operating these facilities around 2027.

It will begin transferring fuel to an outside interim storage site by late 2035.

The BW Opal FPSO (a large floating production, storage, and offloading vessel) received its first gas. This marks a shift from Barossa LNG project execution to production operations.

Of the six wells, five are capable of producing more than expected, about 300 million cubic feet per day per well on average. With the renewal of the Darwin LNG plant’s environmental license, gas will flow from the FPSO to the onshore plant.

The BW Opal has the capacity to handle 850 million cubic feet of gas per day and 11,000 barrels of condensate per day.

The FPSO will remain in the Barossa gas field, 285 km offshore from Darwin, supplying the Darwin LNG plant for the next 20 years.

CONTEXT: The Darwin LNG plant exports most of its LNG to Japanese buyers. It is partly owned by Japanese energy companies INPEX, JERA and Tokyo Gas.

Erex began a trial co-firing biomass at Vietnam’s state-owned Na Duong coal power plant, blending up to 20% wood chips with coal.

The test, on Sept 18 with Vinacomin, targets one of the plant’s two 55 MW units.

CONTEXT: The company aims to raise the ratio to 30% and commercialize it by FY2027. By using locally sourced biomass, the project seeks to cut CO2 emissions while improving Vietnam’s energy self-sufficiency amid rising power demand.

Mitsui O.S.K. Lines (MOL) began a voyage using biofuel on a Capesize bulker for Anglo American, a major resource company.

This voyage demonstrates the MOL Group’s carbon inset program, Blue Action Net-Zero Alliance, which supports net-zero shipping.

Guided by Blue Action 2035, MOL will continue advancing clean fuel adoption to decarbonize marine transport.

CONTEXT: ISCC-EU certifies that sustainable fuels derived from biomass and waste meet the EU’s legal requirements for sustainability and greenhouse gas emission reduction, as defined under the European Renewable Energy Directive.

As of Sept 21, the LNG stocks of 10 power utilities were 1.88 Mt, up 7.4% from the previous week (1.75 Mt), up 2.7% from end Sept 2024 (1.83 Mt), and 8.3% down from the 5-year average of 2.05 Mt.

CONTEXT: Nationwide temperatures have dropped by about 10°C in the past week, but JMA forecasts still expect above-average temperatures for at least the first half of October.

India’s Ministry of Environment, Forest and Climate Change hosted the first Joint Committee (JC) meeting for the Japan–India JCM.

The Japanese and Indian sides agreed to make final adjustments for the Rule of Implementation to serve as the framework for JCM under Article 6 of the Paris Agreement.

The JC will be the decision-making body for JCM between Japan and India. It discussed rules and covered credit allocation, reporting, and use of credits.

CONTEXT: The JCM allows Japan and partner countries to cooperate on low-carbon technologies and finance. They share the resulting GHG emission reductions. Japan has already implemented around 270 JCM projects globally. A new implementing agency (JCMA), established in April, serves to speed up processes.

Tohoku Electric will support farmers in decarbonization efforts through carbon credits.

The company will partner with Tokyo-based Faeger, which generates and sells such credits. Tohoku Electric will buy the credits, helping stabilize farmers’ income.

Faeger reduces methane emissions from rice cultivation by adjusting water management practices. Tohoku Electric will introduce farmers in the Tohoku region and Niigata Pref to Faeger.

ANALYSIS

BY PARUL BAKSHI

Securing the Transition: Unlocking India–Japan Collaboration on Critical Minerals

The 11th India–Japan Energy Dialogue and Indian Prime Minister Narendra Modi’s visit to Tokyo in August put energy at center stage, with critical minerals as one of the key aspects of economic strategies.

At the end of August, India’s Ministry of External Affairs released a Fact Sheet on India–Japan Economic Security Cooperation, identifying semiconductors, critical minerals and clean energy, etc, as priority sectors for collaboration. Both governments pledged support for private sector–led initiatives and emphasized cooperation through multilateral frameworks such as the Mineral Security Partnership, the Indo-Pacific Economic Framework, and Quad Critical Minerals Initiatives.

Concrete measures have been taken in this direction, like India’s Ministry of Mines and METI signed a Memorandum of Cooperation in August, while Toyota Tsusho expanded its rare earths refining project in Andhra Pradesh, India to set up a stable supply chain. Meanwhile, initiatives like the battery supply chain roundtable organized by JETRO in India signal appetite for further cross-border links.

Yet despite this momentum, much of the agenda still consists of frameworks, dialogues, and memoranda rather than large-scale projects. This “pending promises” gap is striking, particularly given Japan’s own track record of building durable supply chain architecture in response to past crises (see author’s analysis in Japan NRG, June 2, 2025), and India’s rising urgency to reduce its critical mineral dependencies.

While opportunities span joint exploration, refining, recycling, and technology collaboration, persistent challenges of policy execution, infrastructure, and investor confidence continue to weigh on delivery. Whether Tokyo and New Delhi can now translate complementary strengths into concrete outcomes will determine whether critical minerals become a genuine pillar of their partnership, or remain aspirational.

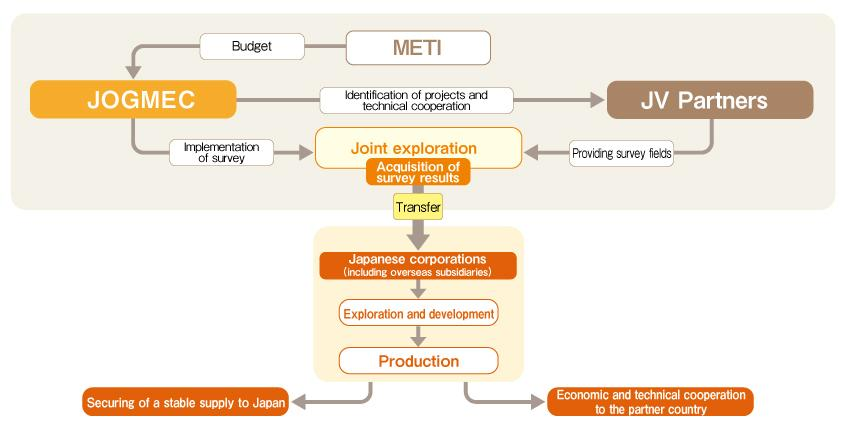

Diplomacy and Ambitions

Japan’s resource security architecture has been steadily reinforced over the past two decades through institutional and legal innovation. The Supply Chain Diversification Programme, launched in 2020 with a budget of $2 billion, was an early step, providing subsidies for Japanese firms to relocate production out of China, initially to ASEAN, and later to India and Bangladesh under its expanded second phase.

The Economic Security Promotion Act (2022) gave this approach a statutory backbone, mandating supply chain risk assessments for strategic goods. It established a new system of subsidies and insurance for companies, and enhanced public–private coordination across critical sectors such as minerals, semiconductors, and energy.

Flow of JV survey implementation system

Source: JOGMEC

The result is a distinctive playbook that combines financial incentives, statutory authority, and institutional depth to build supply chain resilience. Despite gaps, these tools provide Tokyo with a relatively well-developed framework to confront today’s fractured geopolitics.

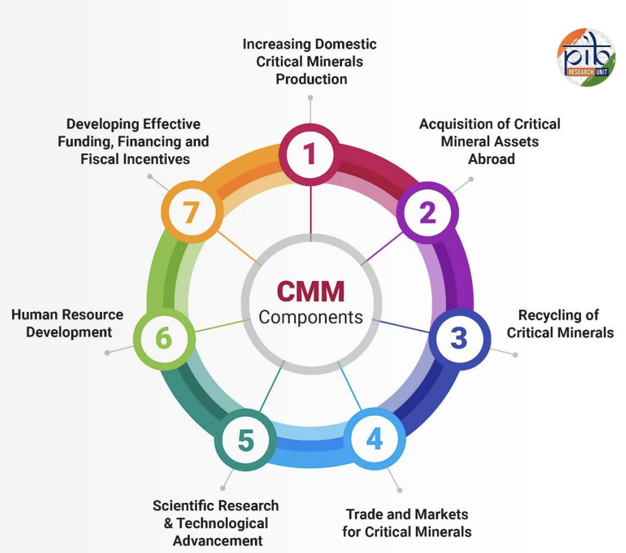

Components of NCMM

Source: Press Information Bureau, Government of India

On the other hand, India has entered the critical minerals race with growing urgency. According to the Ministry of Mines, India met 80% of its lithium and cobalt requirements and 90% of its rare earth element demand through imports in 2023, underlining its dependence on external supply. The launch of the National Critical Minerals Mission (NCMM) in January 2025 signalled a strategic shift, from being primarily a consumer to an ecosystem builder across exploration, processing, and recycling.

The scale of India’s dependency is stark. Imports from China surged dramatically in recent years; lithium by 921% and nickel by 137% in 2024 and graphite by 85% between 2022–24 . This rising reliance has sharpened the policy push to diversify. Early-stage deals have been pursued with Zambia, Mongolia, and the Democratic Republic of Congo, while domestic players are being encouraged to accelerate exploration.

Institutional mechanisms have also expanded. Khanij Bidesh India has been tasked with overseas acquisitions, while Indian Rare Earths Limited and private explorers are mobilized to strengthen refining and recycling capacity. The NCMM is designed to coordinate these efforts under a single umbrella.

There is a reason for India to dig locally. India holds 6.3% of global rare earth reserves, with deposits including neodymium and praseodymium. In 2023, significant lithium reserves were identified in Jammu and Kashmir, though exploration remains at an early stage. India is also in the top five producers of natural graphite, with 3.1% of global reserves and growing capability in producing spherical graphite for EV batteries.

However, critical mineral auctions have struggled to draw investor interest, due to unclear reserve data, concerns over mining capabilities, and inadequate technology.

In refining, however, India is beginning to scale. The International Energy Agency projects its global share of refined copper capacity will rise from 2.1% in 2023 to 3.5% by 2035. This aligns with India’s ambition to become not only a major consumer but also a processing hub within critical mineral value chains.

From dialogue to delivery

India and Japan have the foundations for deeper critical minerals cooperation, but the real test lies in whether these frameworks can translate into bankable projects.

A flagship example is Toyota Tsusho’s rare earth venture in Andhra Pradesh, launched with Indian Rare Earths in 2012 and now run through its subsidiary, Toyotsu Rare Earths India, has become a critical supply chain node. The facility processes thousands of tons of rare earth oxides for export to Japan, proving that joint projects can move from MoU to market.

Indian industrial groups such as JSW, Vedanta, and Adani are also reportedly exploring partnerships with Japanese firms on battery technologies and minerals projects.

Beyond individual ventures, the two countries share a converging outlook. Their official lists of critical minerals overlap and this provides a clear platform for scaling cooperation into practical, investor-ready ventures.

Further pathways for collaboration include:

Joint Exploration & JVs: India allows 100% FDI under the automatic route for mining and exploration of metal and non-metal ores, which opens the door for Japanese capital and technology to participate directly in local exploration. Further, Japan and India (e.g. via JOGMEC + KABIL) could undertake JV exploration in other countries based on Japanese expertise in such ventures.

Processing & Refining Close to Market: Japanese investment in Indian refining (for example, rare earth oxides or magnets) could fast-track supply chain integration, with lower environmental clearance and less capital risk. For example, both countries already have footholds in the copper supply chain. Japan is the third-largest refiner by company ownership and the fifth by location, while India is bringing new capacity online.

Recycling / Urban Mining: The India–Japan Clean Energy Partnership, signed in 2022, names recycling as a candidate for future collaboration. Expanding capacities for recycling of e-waste and end-of-life batteries in India, using Japanese recycling technology, could reduce import dependence and improve environmental outcomes.

Regulatory Incentives & Project Support: India eliminated customs duties on 25 minerals, reduced Basic Customs Duties (BCD) on others, accelerated environmental and mining clearances, and introduced financial incentives for exploration.

Human Capital, Standards & Agile Pipelines: Scaling of refining, recycling, and processing will require investment in training and ESG standards.

Together, these initiatives would not only bolster supply chain resilience but also offer a portfolio of investable opportunities. For Japanese firms, India provides scale, growth, and market proximity; for Indian stakeholders, Japan offers technology, financing, and credibility in global markets. For global investors, their convergence is a hedge against geopolitical risk.

Pending promises: Gaps in delivery

Progress on critical minerals has been limited compared to Japan’s strides with partners like Australia, Chile, or France. India–Japan initiatives remain disproportionately heavy on paper promises and discussions.

Meanwhile, the JBIC’s 2024 survey reaffirmed India as the most promising long-term destination for Japanese firms, while also revealing declining business planning ratios. Many companies remain cautious, citing policy uncertainty, legal complexity, infrastructure bottlenecks, and execution risks.

This gap underscores the broader problem: India–Japan critical minerals cooperation has momentum in vision but remains patchy in delivery. For now, the partnership risks lagging behind the pace of both market demand and competitor alliances. Without credible midstream and downstream infrastructure, even expanded exploration risks stalling at the mine gate.

Both need to proceed to co-financed mines, processing hubs, and recycling plants. For India, this means mobilising Japanese capital and technology to unlock its resource potential. For Japan, the upside is securing resilient access at a time when diversification is no longer optional but essential.

Conclusion

As global competition over critical minerals intensifies, the risks of autarky and fragmented supply chains are becoming clearer. If markets segment along geopolitical lines, prices will rise, volatility will increase, and supply shocks will ripple more widely. Neither India, Japan, nor even China benefits from such an outcome.

What is needed instead are transparent international markets where rules and standards encourage open flows, while balancing national security concerns. Especially so because demand and technological shifts constantly reshape which minerals are “critical.”

India and Japan are well placed to build on their complementarities. Japan brings capital, technology, and institutional depth in refining, recycling, and standards-setting; India offers scale, a growing manufacturing base, and untapped reserves. Together they cover significant ground across copper, graphite, rare earths, and lithium; minerals central to electric vehicles, semiconductors, and renewable energy.

Institutional frameworks are already in place. These initiatives provide scaffolding for long-term cooperation, but credibility will depend on whether the two sides can move quickly from frameworks to deliverable projects that attract investors.

Dr. Parul Bakshi is Fellow – Energy and Climate at the Observer Research Foundation Middle East. She was previously a Visiting Researcher at the University of Tokyo and a Japan Foundation Indo-Pacific Partnership Research Fellow.

ANALYSIS

BY FILIPPO PEDRETTI

Caught Between U.S. Politics and a Volatile LNG Market

LNG is no longer just a commodity; it has become a lever of U.S. foreign policy. For Japan, wary of trade tensions with the Trump administration, that means adjusting fuel procurement plans at a time when free-trade principles among G7 allies look increasingly fragile.

To placate Washington, in early September, Japan pledged an annual $7 billion worth of additional U.S. energy purchases. The decision carried political undertones, but Japanese utilities found a commercial upside: with demand at home easing, they can resell surplus American cargoes on world markets.

That reshaping of Japan’s import mix will ripple into the 2030s, testing ties with traditional suppliers in Australia, Southeast Asia and the Middle East. Pricing dynamics may also shift, particularly if America secures Japanese capital for the $44 billion Alaska LNG project—an undertaking whose costs will almost certainly exceed its billing.

Washington is urging Japan, along with Seoul and Taipei, to bankroll the Alaska venture – which includes building a 1,300-km pipeline partly predicated on resolving local gas supply issues. Yet the mega-project’s economics are shaky, and if these falter, Asian backers will shoulder the losses.

For Japan, this deeper entanglement with U.S. gas comes at a cost. By narrowing its supply options, Tokyo risks swapping one vulnerability for another: what is sold as a step toward energy security could in time undermine it.

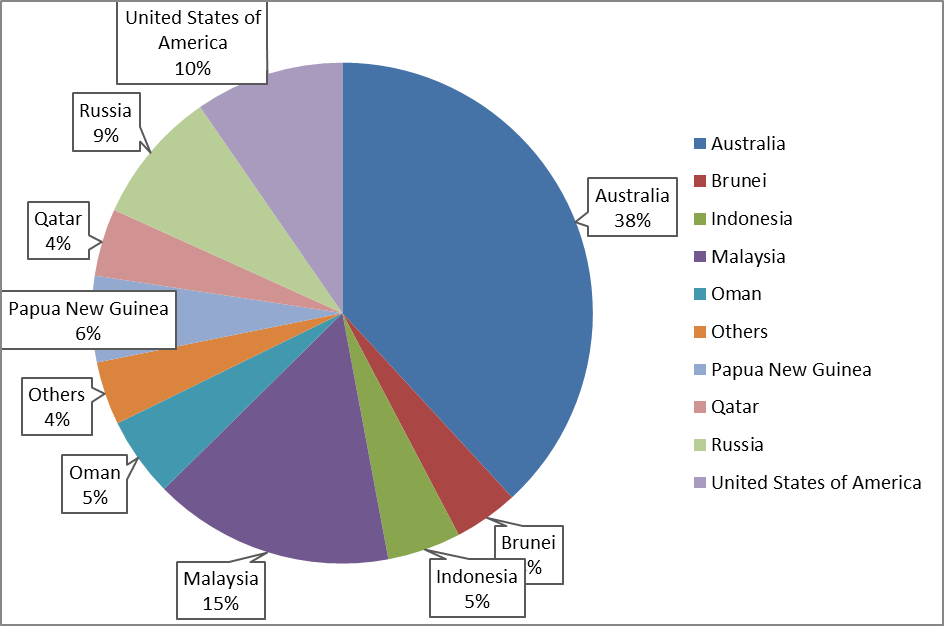

Japan’s reliance on Australian LNG

In 2024, Japan imported almost 66 million tons of LNG. Despite the decline in domestic demand, LNG remains crucial for power generation. That year, LNG covered around 30% of Japan’s electricity. Of that, roughly 40% came from Australia and 10% from the U.S.

Japan’s LNG imports in 2024.

Source: government data.

apan’s storage infrastructure is meager. JERA said its Tokyo Bay facilities can hold only about 10 days’ worth of gas consumption, compared with Europe’s months-long reserves. That leaves Tokyo exposed to price spikes or supply shocks. Thus, JERA signed a seasonal contract with Woodside Energy in 2024, covering winter months.

A heavy reliance on Australia may seem a safer choice due to shared political values and routes that avoid chokepoints such as Hormuz and Malacca. But it also has drawbacks.

Rystad Energy points out that Australia’s ability to remain an LNG exporter is weakening. Eastern Australia stopped exports, facing shortfalls due to aging gas fields, as well as limited pipeline capacity. Also, Canberra’s industry faces rising costs.

Alternative suppliers: U.S. and the others

In 2023, the U.S. became the world’s largest LNG exporter, and in 2024, the country shipped over 88 million tons (half of which went to Europe alone). Australia and Qatar follow as second and third largest exporters. In less than six months after taking the presidency, Trump approved five projects, including one backed by Mitsui O.S.K. Lines.

There are also a few other countries emerging as suppliers. As the U.S.-China tensions fester, Canada found space for developing its LNG projects. LNG Canada’s Phase 1, led by Shell and scheduled to start in 2025, will export 14 million tons per annum (Mtpa) from British Columbia. Shipping time to Japan is 10 days, or even less, compared with at least 20–25 from the U.S. Gulf. Regulatory hurdles remain, but Japanese buyers see Canada as politically stable and closer.

Mitsubishi, Japan’s largest LNG producer, is also sourcing from that project, holding a 15% stake in it and having secured 2.1 Mtpa. With a portfolio of 12.8 Mtpa from projects across several countries, Mitsubishi aims to expand its volumes to 15 Mtpa by 2026 – when LNG Canada is fully operational – and to 18 Mtpa by the early 2030s.

Qatar, meanwhile, is expanding its North Field to lift capacity from 77 Mt to 126 Mt by 2027. Tokyo seeks slots in the expansion. Still, Qatari cargoes must pass through the Strait of Hormuz — a persistent strategic concern.

Russia, despite sanctions, continues to supply LNG to Japan from Sakhalin-2, totaling 5.68 million tons in 2024. The current Sakhalin-2 supply contracts are due to renew with the first of these expiring in March 2026.

JERA’s deals with the U.S.

Contracts from the U.S. are flexible, without destination clauses, allowing Japanese buyers to resell cargoes. This is a hedge against their own declining domestic demand: In 2023, Japanese firms resold about 37% of the purchased LNG, up from 16% in 2018.

In the past few months, JERA expanded its U.S. LNG portfolio with a series of long-term agreements, for example a deal to buy about 1 Mtpa of LNG between 2029 and 2050 from Cheniere’s Corpus Christi-Sabine pass.

Another deal was struck with Sempra Infrastructure for 1.5 Mtpa from the planned Port Arthur LNG Phase 2 project in Texas, on a 20-year free-on-board basis. JERA also secured 2 Mtpa from NextDecade’s Rio Grande LNG project and 1 Mtpa from Commonwealth LNG.

In total, these recent agreements amount to 5.5 Mtpa, worth an estimated ¥400 billion ($2.76 billion) a year, which is just over 15% of JERA’s 35 Mtpa procurement target for 2035.

JERA was reported facing contract expirations of around 4 Mtpa before 2030 and 16 Mtpa in the 2030s, making U.S. supply crucial to its renewal strategy. JERA plans to triple its U.S. LNG intake to 10 Mtpa by the early 2030s, raising the American share of imports to almost 30%.

During the recent Gastech industry event in Milan, JERA signed a Letter of Intent on exploring buying LNG from Glenfarne, the operator of the Alaska LNG project. This could be as much as 1 Mtpa with a 20 years contract, FOB.

Overview of JERA’s recently closed contracts for U.S. LNG imports

Supplier / Project

Volume (Mtpa)

Contract Type

Tenor / Period

Cheniere Energy

1.0

FOB

20 years

Sempra Infrastructure

1.5

FOB

20 years

NextDecade (Rio Grande LNG)

2.0

FOB

20 years

Commonwealth LNG

1.0

FOB

20 years

Also, JERA is said to be in talks to buy natural gas production assets worth $1.7 billion from GEP Haynesville II. This would be JERA’s first direct investment in shale gas production.

Others

Kyushu Electric has been among the most vocal of the Japanese buyers in pressing for faster U.S. LNG export approval permits. The utility signed a long-term agreement with Energy Transfer LNG Export, the firm’s first contract with a U.S. supplier. Kyushu Electric will receive up to 1 Mtpa of LNG for 20 years from Lake Charles LNG in Louisiana. The deal has FOB delivery conditions and no destination clause.

In 2024, the company procured 2.59 million tons of LNG, with about 70% from Australia. Tokyo Gas was reported negotiating long-term LNG supply deals with at least four U.S. Gulf Coast exporters, such as Energy Transfer and Commonwealth. The firm is also in talks with Venture Global for 1 Mtpa of LNG under a 20-year deal.

Set to start in 2028, their Louisiana plant will export 28 Mtpa. The company is also restructuring its U.S. upstream investments by acquiring Rockcliff Energy and Chevron assets while divesting its Eagle Ford stake to Shizuoka Gas. That adds up to Tokyo Gas signing a 15-year contract in 2023 with Venture Global LNG for 1 Mtpa.

But cost overruns remain a warning. Chiyoda, Japan’s leading LNG engineering group, has booked more than $1 billion in losses on projects such as Cameron and Golden Pass. The Cameron LNG project suffered from a labor shortage, while Golden Pass LNG was a JV with U.S. firm Zachry Industrial, which went bankrupt due to rising costs.

Conclusion

As climate concerns subside due to the agenda emanating from the White House, countries are abandoning decarbonization imperatives. This is opening up new opportunities for LNG, with plans being made decades into the future. No longer is there much talk of totally decarbonizing the energy sector by 2050.

Trading house Trafigura forecasts that LNG prices will remain elevated until at least 2028, in part due to Europe buying more LNG (especially from the U.S.) New U.S. and Qatari supply volumes are unlikely to arrive soon enough to ease shortages.

The U.S. Energy Information Administration expects domestic gas prices to more than double by 2026. This would feed into LNG export costs, meaning buyers like Japan would pay more. Japan, with limited storage and declining demand, remains vulnerable.

Washington’s insistence that allies buy more U.S. LNG doesn’t look like a gift of “energy security”, but rather a strategic move for economic and geopolitical assertiveness. Japan must be careful not to make too big of a bet on an industry caught between volatile prices and geopolitical tensions, and one which would continue the country’s energy-import reliance.

For Japan, diversification — not excessive dependence on the U.S. — is the only strategy that makes sense. That’s why Tokyo will continue to hedge supplies across U.S., Australian, Canadian, Qatari and Russian sources, while gradually expanding renewables at home. After all, energy security rests on having many good options.

ASIA ENERGY REVIEW

BY JOHN VAROLI

A brief overview of the region’s main energy events from the past week

Australia / EVs

The govt will provide AU$40 million to expand the public EV charging network, targeting curbside and fast-charging sites across the country.

Australia / Renewables

In a $1.1 billion deal, investment group La Caisse will acquire Australian renewable energy and battery storage company Edify Energy.

China / Natural gas

Domestic gas production rose at an average annual rate of 10% since 2000. Fastest growth is from newer producing areas in the Northwest where combined output rose 13%. The established gas producing heartland of the Sichuan Basin saw output rise 9%.

China / Renewables

China aims to increase its installed wind and solar power capacity to 3,600 GW by 2035, over six times the 2020 levels.

India / Nuclear power

Commerce Minister Goyal said that India and the U.S. plan to develop small modular reactors (SMRs).

India / Oil & Gas

Goyal also said the U.S. has been the fifth-largest supplier of crude oil to India, and the second-largest supplier of LNG.

Philippines / Nuclear power

The Philippines was elected to the Board of Governors of the International Atomic Energy Agency (IAEA) for the term 2025 to 2027.

South Korea / Solar power

Over the past 3 years, the solar power energy that’s wasted due to insufficient transmission capacity in South Korea exceeds the combined output of three 1-GW class nuclear reactors.

Taiwan / Chips

TSMC, the world’s biggest manufacturer of chips, said it will produce a new generation of chips that consumes less energy.

Singapore / Wind power

Nexif Ratch Energy will invest more than US$233 million to develop a wind power project in Gia Lai Province.

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

NEWS:

・Koizumi under fire as rivals press him on wages, energy policy in LDP debate

・ANRE reviews the challenges of grid connection for data centers

・Marubeni and Panasonic launch EV diagnostic service in Thailand